Blood Ketone Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

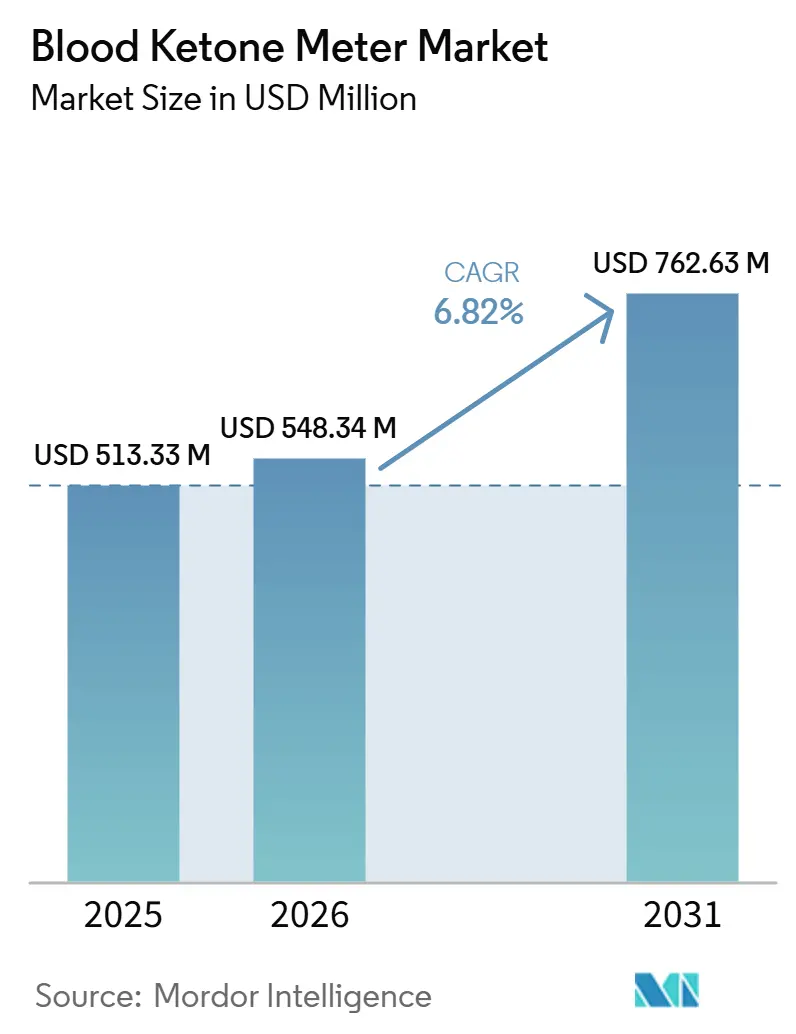

| Market Size (2026) | USD 548.34 Million |

| Market Size (2031) | USD 762.63 Million |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Blood Ketone Meter Market Analysis by Mordor Intelligence

The Blood Ketone Meter Market size is projected to expand from USD 513.33 million in 2025 and USD 548.34 million in 2026 to USD 762.63 million by 2031, registering a CAGR of 6.82% between 2026 to 2031.

Demand is expanding beyond traditional diabetes care into ketogenic diet monitoring, critical-care sepsis pathways, and athletic performance optimization. Multifunctional meters that combine glucose, ketone, and other metabolic biomarkers are reshaping purchasing criteria, while improvements in biosensor accuracy and lower blood-sample volumes make daily testing more acceptable. Reimbursement shifts—especially CMS coverage of dual glucose–ketone strips—together with remote patient-monitoring (RPM) billing codes in the US and EU, are accelerating adoption in outpatient and home settings.

Key Report Takeaways

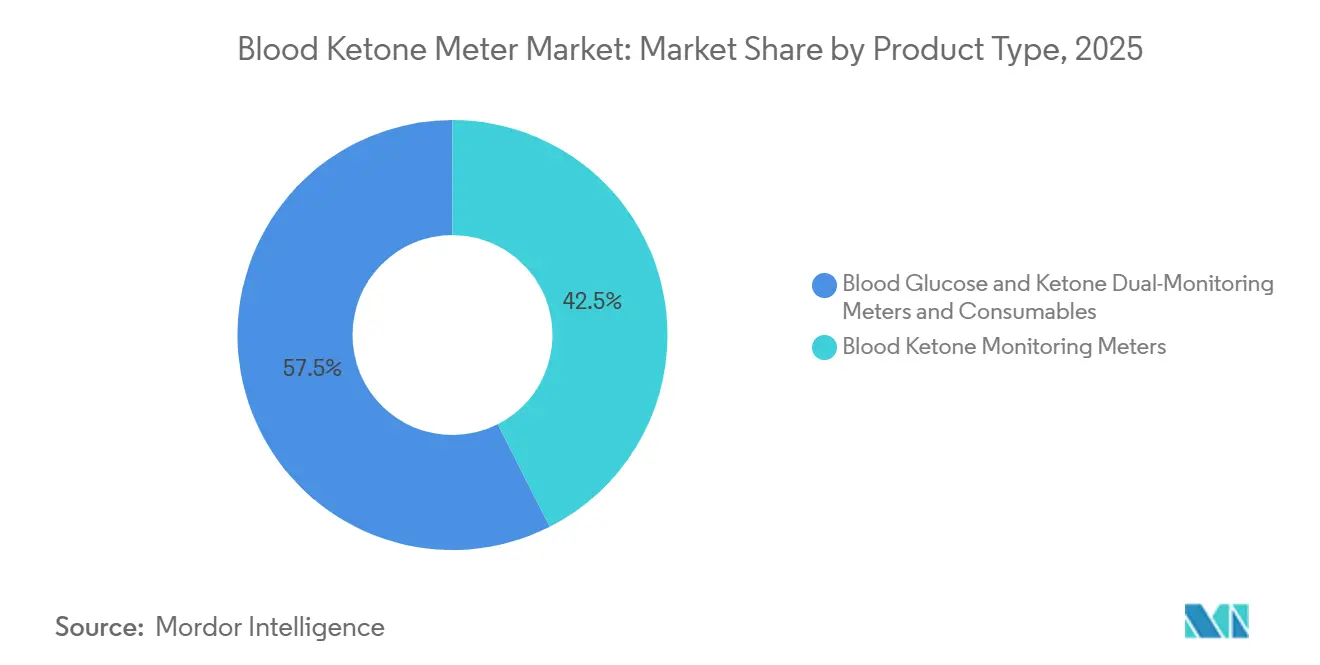

- By product type, Blood Ketone Monitoring Meters held 42.54% of blood ketone meter market share in 2025, whereas Blood Glucose & Ketone Dual Meters are set to grow at a 7.20% CAGR to 2031.

- By application, Diabetes (Type-1) Management accounted for 46.67% of the blood ketone meter market size in 2025; Ketogenic Diet Monitoring is projected to expand at 7.51% CAGR through 2031.

- By end user, hospitals led with 45.56% revenue share in 2025, while home-care settings will register the fastest 7.81% CAGR between 2026-2031.

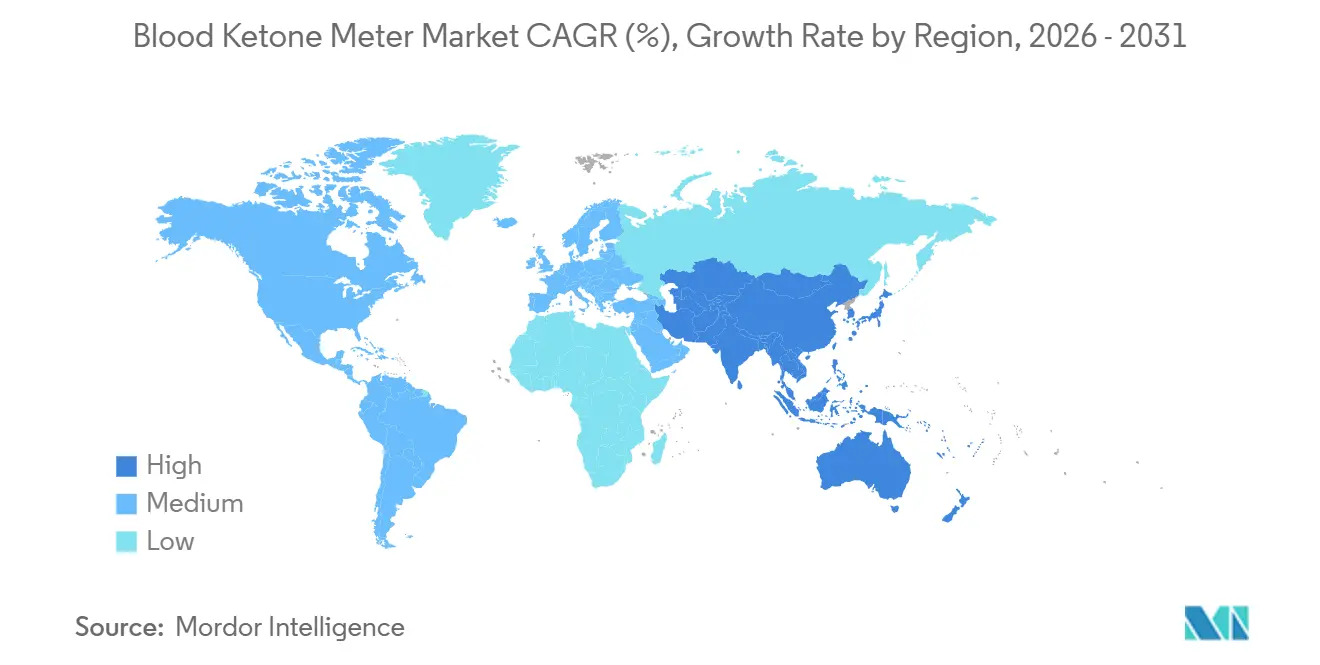

- By region, North America commanded 37.34% of the blood ketone meter market size in 2025; Asia-Pacific is poised for the highest 7.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blood Ketone Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Rapid Uptake of Ketogenic Diets Among Fitness-Conscious Millennials in Europe | ~1.7% | Europe, North America, with spillover to urban centers in APAC | Medium term (~ 3-4 yrs) |

| Mandatory Ketone Testing Protocols in ICU Sepsis Pathways | ~1.4% | North America, Europe, Advanced healthcare markets in APAC | Short term (≤ 2 yrs) |

| CMS Reimbursement Expansion for Dual Glucose-Ketone Strips | ~1.5% | United States, with influence on global reimbursement standards | Medium term (~ 3-4 yrs) |

| Remote Patient-Monitoring (RPM) Billing Codes Fueling Home-Based Ketone Testing US/EU | ~1.2% | North America, Europe | Medium term (~ 3-4 yrs) |

| Growing Prevalence of Insulin-Pump-Induced DKA Episodes in North America | ~1.1% | North America, Europe | Short term (≤ 2 yrs) |

| Increasing Product Launches and Approvals | ~1.0% | Global | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Ketogenic Diets Among Fitness-Conscious Millennials in Europe

Mainstream acceptance of ketogenic nutrition is pushing consumer demand for compact, app-connected meters. Randomized trials confirming metabolic and critical-care benefits have broadened shopper profiles beyond patients to lifestyle users [1]Mathias Rahmel et al., “Ketogenic nutrition improves clinical outcomes in sepsis,” Science Translational Medicine, science.org. European fitness retailers now stock devices previously limited to pharmacies, and app developers integrate ketone data into workout dashboards. Manufacturers position products as daily wellness tools, which is enlarging the blood ketone meter market and increasing brand visibility in non-medical channels

Mandatory Ketone Testing Protocols in ICU Sepsis Pathways

Hospitals in the US and EU have embedded ketone checks into sepsis bundles after studies showed ketogenic support reduced insulin use and improved ventilation-free days. Procurement teams now seek meters that auto-sync with electronic health records (EHRs), driving institutional demand. Suppliers able to certify interoperability and fast sample turnaround are winning tenders, lifting the blood ketone meter market’s institutional sales.

CMS Reimbursement Expansion for Dual Glucose–Ketone Strips

The April 2024 CMS reclassification of integrated monitors as DME opened nationwide coverage for dual strips [2]Centers for Medicare & Medicaid Services, "Glucose Monitor – Policy Article (A52464)," cms.gov Centers for Medicare & Medicaid Services, “Glucose Monitor – Policy Article (A52464),” cms.gov. Private insurers such as Cigna mirrored the update in early 2025 The clearer payment pathway eliminates a key cost barrier, encouraging clinicians to prescribe dual-function meters and expanding the blood ketone meter market footprint in chronic-care management.

Remote Patient-Monitoring (RPM) Billing Codes Fueling Home-Based Ketone Testing US/EU

New CPT codes allow providers to bill for home ketone data reviews, spurring telehealth programs that ship meters directly to patients. Platforms such as MedM integrate 900-plus sensors, including ketone devices, with automated billing logs. This financial catalyst is steering growth from episodic clinic checks to continuous home monitoring, vital for rural and elderly populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Product Recalls | -1.30% | Global, particularly in North America and Europe with stringent post-market surveillance | Medium term (2-4 years) |

| Patient Discomfort Over Repetitive Finger-Pricks Reducing Long-Term Compliance | -1.60% | Global, particularly among home-care users and pediatric populations | Long term (≥4 years) |

| Accuracy Gap vs. Laboratory β-Hydroxybutyrate Assays Limiting Adoption in ICUs | -1.50% | Global, with higher impact in developed healthcare systems across North America, Europe, Japan, and South Korea | Medium term (2-4 years) |

| Persistent Import Tariffs on Biosensor Chips in Brazil & Argentina | -0.80% | Brazil and Argentina (Latin America) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Product Recall

FDA Class 1 recalls of glucose-ketone systems in 2024-2025 dented provider confidence. Manufacturers faced supply gaps, higher insurance premiums, and brand damage[3]Washington State Health Care Authority, “Continuous Glucose Monitors New Populations,” hca.wa.gov. Larger companies leveraged established quality frameworks to mitigate risk, whereas smaller firms struggled with compliance costs, nudging the blood ketone meter market toward consolidation.

Patient Discomfort Over Repetitive Finger-Pricks

While capillary sampling remains accuracy gold-standard, user studies reveal dwindling adherence due to pain and skin damage. Device makers are reducing required blood volume to 0.3 µL and exploring alternate-site lancing, yet uptake among preventive and weight-management users stays constrained. Continuous, minimally invasive solutions remain in R&D, and until commercialized, this restraint will temper the blood ketone meter market growth curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dual-Function Meters Reshape Market Dynamics

Blood Ketone Monitoring Meters accounted for 42.54% of blood ketone meter market share in 2025 and remain a staple in diabetic ketoacidosis (DKA) prevention. Dual glucose-ketone meters, however, are advancing at a 7.20% CAGR, buoyed by SGLT-2 inhibitor protocols that require simultaneous biomarker tracking.

Consumables sustain recurring revenue and push innovation in strip chemistry, targeting ±3% accuracy and capillary volumes under 0.4 µL. Premium devices such as LifeSmart’s Smart Blood Glucose Plus Ketone Monitor archive 1,000 readings and export to mobile dashboards. Budget-centric institutional meters retain importance in bulk contracts, creating a bifurcated competitive field within the blood ketone meter market.

By End User: Home-Care Settings Drive Future Growth

Hospitals held 45.56% of 2025 revenue, driven by ICU and emergency protocols. Early DKA triage and critical-care ketone tracking keep procurement strong, yet home settings will outpace with a 7.81% CAGR to 2031.

Clinics and diagnostic centers bridge inpatient discharge and full self-management, offering education and baseline testing. RPM software auto-transfers capillary readings into EHRs, enabling clinicians to bill remotely reviewed data under CPT 99457 and related codes J Diabetes Sci Technol. This shift underpins durable expansion of the blood ketone meter market toward community care.

By Application: Ketogenic Diet Monitoring Expands Market Scope

Type-1 Diabetes Management delivered 46.67% of 2025 revenue, backed by American Diabetes Association standards emphasizing ketosis surveillance. Hospitals also rely on bedside ketone checks during DKA emergencies. Meanwhile, ketogenic diet monitoring will grow at 7.51% CAGR, adding lifestyle users to the blood ketone meter market and spurring demand for meters styled as wellness gadgets rather than medical devices.

Sports performance optimization and veterinary ketoacidosis surveillance contribute niche volumes but command premium price points. Elite athletes seek millimolar-level trend analytics for recovery planning, and veterinary clinics adapt human meters for companion-animal ketoacidosis without major redesign costs, adding incremental revenue to the blood ketone meter market

By Age Group: Pediatric Segment Shows Highest Growth Potential

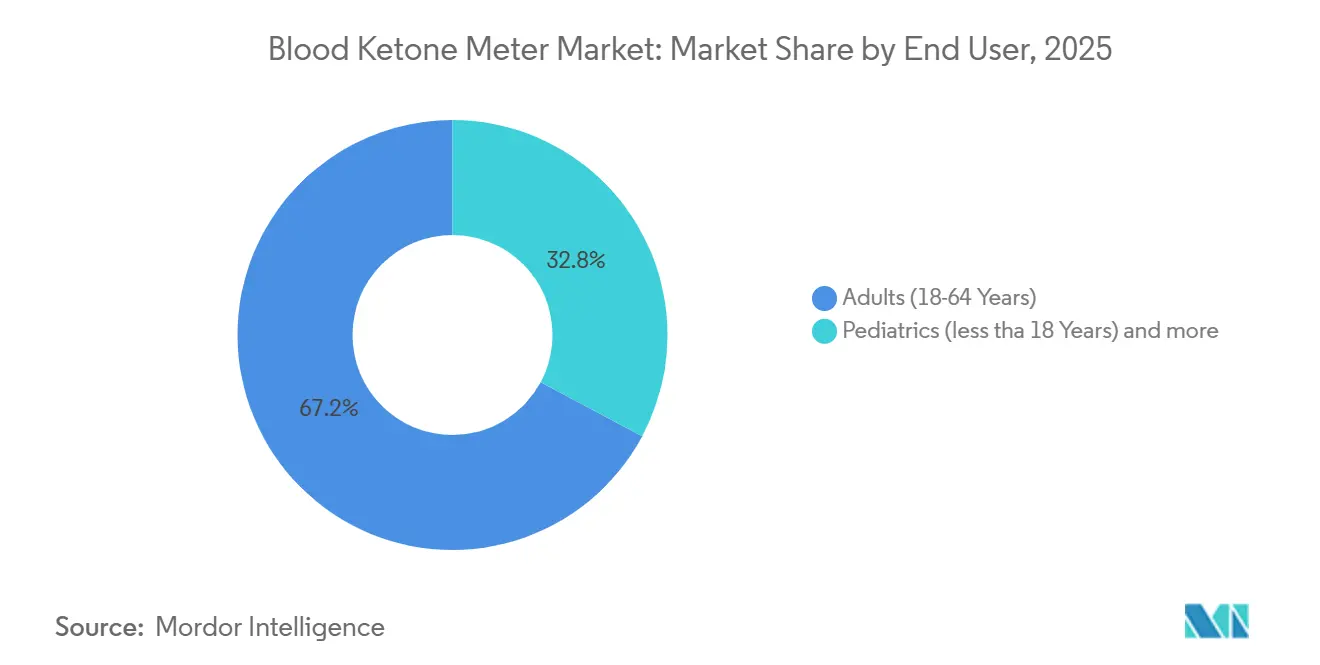

Adults aged 18-64 represented 67.19% of 2025 sales thanks to higher diabetes prevalence and purchasing power. Companion apps with actionable insights appeal to this tech-literate cohort, fortifying their spending share. The pediatric group (<18 years) will register an 8.10% CAGR, benefiting from rising type-1 diabetes incidence and ketogenic protocols for epilepsy. Stanford Medicine research links early tech adoption to improved glycemic outcomes stanford.edu.

Geriatric users value large-font interfaces and caregiver alerts. Polypharmacy risks heighten monitoring needs, and manufacturers address dexterity limitations with wide-grip lancets. These adaptations, though incremental, shield the blood ketone meter market from age-related attrition.

Geography Analysis

North America accounted for 37.34% of 2025 revenue, with the US benefiting from CMS reimbursement and rapid tech upgrades. Private insurers mirror federal policy, amplifying device penetration. Canada’s single-payer model yields steadier uptake but lower average selling prices, whereas Mexico shows double-digit growth off a smaller base. The blood ketone meter market continues to gain from academic-industry collaborations that fast-track regulatory clearance.

Asia-Pacific will post the fastest 7.75% CAGR to 2031, led by China and Japan. Domestic makers exploit cost advantages and localize firmware for Mandarin and Kanji interfaces, challenging Western imports. India’s diabetes burden drives state insurance pilots covering dual meters. Urban consumers in Seoul, Sydney, and Singapore adopt ketogenic diets, widening non-medical demand. Collectively, these drivers lift the blood ketone meter market across APAC’s diverse payor environments.

Europe maintains strict MDR compliance, raising entry barriers yet enhancing trust. The UK and Germany anchor volume, while France and Italy supply steady institutional demand via standardized DKA protocols. Continental R&D into microneedle sampling positions the region as a testing ground for less-invasive next-gen devices, promising long-term tailwinds for the blood ketone meter market.

Competitive Landscape

The blood ketone meter market remains moderately concentrated. Abbott, Nova Biomedical, and EKF Diagnostics leverage broad portfolios and distribution muscle. Keto-Mojo’s direct-to-consumer focus appeals to lifestyle users, fostering brand evangelism. Strategic partnerships, such as Nova’s EHR integration announced April 2025, solidify incumbent positions. AI-enhanced analytics become a new battleground, with vendors embedding trend-prediction engines to elevate clinical utility.

White-space opportunities persist in emerging economies and specialty niches such as veterinary care and elite sports. Larger firms scout acquisitions of sensor start-ups to secure IP on multi-parameter platforms. Product recalls pressure smaller players, nudging the blood ketone meter market toward greater consolidation. Yet strong lifestyle uptake ensures room for agile brands that marry consumer design with clinical-grade accuracy

Blood Ketone Meter Industry Leaders

-

Abbott Laboratories

-

Nova Biomedical

-

Nipro Corporation

-

TaiDoc technology Corporation

-

ForaCare, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: The American Diabetes Association updated its Standards of Care in Diabetes — 2025, underscoring the value of technology-driven management and calling for routine ketone testing in select patient groups. The guidance is expected to steer hospital protocols and purchasing policies, encouraging faster uptake of next-generation blood ketone meter

- December 2024: Nova Biomedical Corp initiated a recall of its StatStrip Glucose Ketone (mmol/L) Hospital Meter System, according to a notice issued by the California Department of Public Health. The event highlights the regulatory and quality-control pressures facing established suppliers and could give competitors an opening to grow share in the hospital segment

- April 2024: Brazil’s health-regulator ANVISA released IN Nº 290, a streamlined pathway that lets officials leverage foreign regulatory reviews when evaluating high-risk devices, including in-vitro diagnostic products such as blood ketone meters. The rule shortens the registration timeline and eases market entry for international manufacturers

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the blood ketone meter market as all handheld or benchtop devices that quantify β-hydroxybutyrate in capillary blood and the proprietary single-use strips and lancets required for each measurement. In scope are stand-alone ketone meters and dual glucose-ketone meters sold through retail, hospital, clinic, and online channels to human end users across 17 countries covered in the report, with values presented in constant 2024-USD.

Scope exclusion: devices that estimate ketones from breath or urine are not counted.

Segmentation Overview

-

By Product Type

- Blood Ketone Monitoring Meters

- Blood Glucose & Ketone Dual-Monitoring Meters

-

Consumables

- Test Strips

- Lancets

- Control Solution

-

By End User

- Hospitals

- Clinics & Diagnostic Centers

- Home-Care Settings

-

By Application

- Diabetes (Type-1) Management

- Diabetic Ketoacidosis (DKA) Emergency Management

- Ketogenic Diet Monitoring

- Sports & Athletic Performance Optimization

- Veterinary Ketoacidosis Surveillance

-

By Age Group

- Pediatrics (<18 Years)

- Adults (18-64 Years)

- Geriatric (>65 Years)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing endocrinologists, procurement managers at tertiary hospitals, national diabetes program officials, and e-commerce distributors across North America, Europe, and Asia-Pacific. These conversations validated strip consumption rates per treated patient, typical meter replacement cycles, and recent reimbursement shifts that influence demand elasticity.

Desk Research

Our analysts first comb public sources such as the International Diabetes Federation, U.S. FDA 510(k) database, national customs statistics, and trade association bulletins to size installed meter bases and annual strip imports. Company 10-Ks, investor decks, and peer-reviewed journals on diabetic ketoacidosis incidence add clinical and commercial context. Subscription tools like D&B Hoovers and Dow Jones Factiva supply revenue splits and shipment news that anchor brand shares. The sources listed illustrate our desk work; many others were reviewed to test consistency, fill gaps, and cross-check figures.

Secondary findings suggested the strip market is the main revenue driver, yet public data alone could not resolve country-level average selling prices. This is where Mordor Intelligence supplements the desk work with focused outreach.

Market-Sizing & Forecasting

A top-down and bottom-up framework underpins the model. Country diabetic populations, DKA hospitalization rates, and ketogenic diet adoption levels generate a demand pool that is then adjusted by meter penetration and average strip use to reach unit volumes. Select supplier roll-ups and channel checks give a bottom-up sense check on totals before values are derived by applying weighted average selling prices. Key variables tracked include treated Type-1 diabetic base, annual SMBG frequency, strip-to-meter pricing ratio, regulatory approvals pipeline, and e-commerce share of device sales. Forecasts to 2030 employ multivariate regression blended with ARIMA smoothing, with scenario ranges reviewed by our primary experts. Missing datapoints, most often on strip pricing, are bridged using neighboring-country analogs that are later overwritten when primary evidence emerges.

Data Validation & Update Cycle

Outputs pass variance screens against independent import data and hospital utilization surveys. Senior reviewers reassess anomalies, after which the model is locked. Reports refresh every twelve months, and interim updates are triggered by major regulatory, pricing, or supply-chain events. A final sense check is completed just before client release.

Why Our Blood Ketone Meter Baseline Commands Reliability

Published market values often differ because each firm chooses its own scope, product mix, and forecast cadence.

Key gap drivers in other studies include exclusion of test-strip revenues, use of uniform global CAGRs without country calibration, and reliance on secondary sources without live price checks, whereas Mordor's baseline incorporates verified ASPs and nation-specific patient metrics and is refreshed annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 513.3 M (2025) | Mordor Intelligence | - |

| USD 519.9 M (2025) | Global Consultancy A | Leaves consumables outside scope and depends mainly on desk research |

| USD 415.1 M (2024) | Industry Databank B | Applies single CAGR to all regions and omits dual meters |

The comparison shows that once scope differences and pricing assumptions are aligned, figures converge toward Mordor's balanced midpoint, underscoring why decision-makers favor our transparent, regularly refreshed baseline.

Key Questions Answered in the Report

What is the current size of the blood ketone meter market?

The market is valued at USD 513.33 million in 2025 and is projected to hit USD 762.63 million by 2031.

Which product category is growing fastest?

Blood glucose & ketone dual-monitoring meters are expanding at a 7.20% CAGR, driven by the benefit of simultaneous biomarker tracking.

Why is Asia-Pacific considered a key growth region?

Rising healthcare spending, a larger diabetes population, and growing ketogenic diet adoption contribute to a 7.75% regional CAGR forecast.

How are reimbursement changes influencing adoption?

CMS and private-payer coverage for dual strips plus RPM billing codes reduce out-of-pocket costs, spurring both clinical and home-care uptake.

What challenges limit long-term user compliance?

Finger-prick discomfort and occasional device recalls discourage sustained testing, prompting R&D into less invasive sampling and stricter quality control.

Which age group offers the highest growth potential?

The pediatric segment (<18 years) is forecast to rise at an 8.10% CAGR as type-1 diabetes diagnoses increase and ketogenic therapy gains traction in epilepsy care.

Page last updated on: