Water-based Resin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 48.76 Billion |

| Market Size (2031) | USD 57.27 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

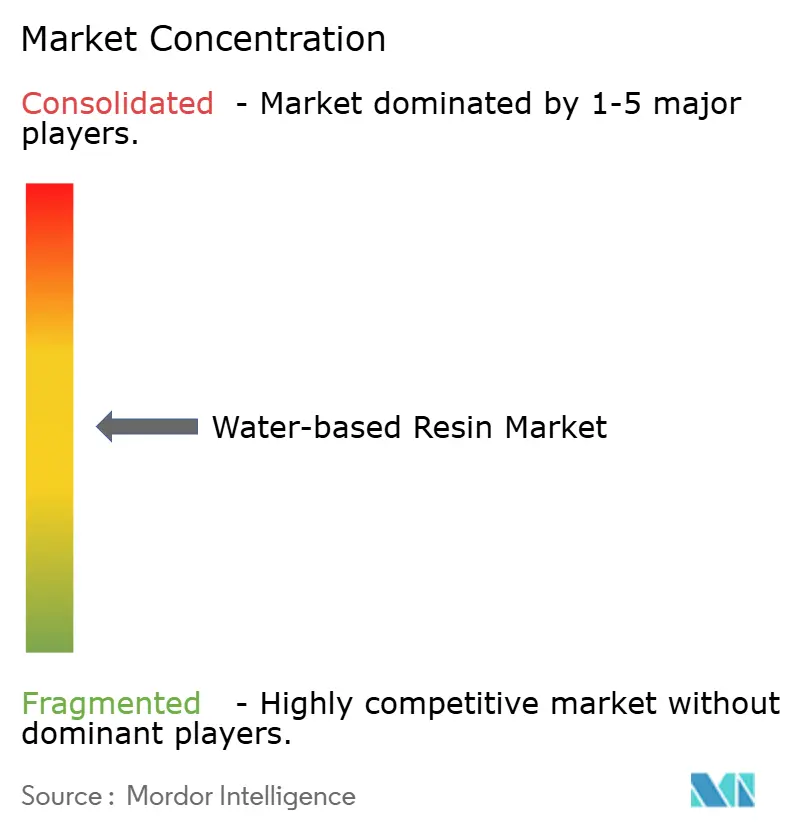

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water-based Resin Market Analysis by Mordor Intelligence

Water-based Resin Market size in 2026 is estimated at USD 48.76 billion, growing from 2025 value of USD 47.22 billion with 2031 projections showing USD 57.27 billion, growing at 3.27% CAGR over 2026-2031. Growing regulatory pressure on volatile organic compound (VOC) emissions, particularly in China and North America, is the primary catalyst for the conversion from solvent-borne to water-borne chemistries. The limited availability of bio-based feedstock has tightened the supply, pushing mid-tier converters that lack captive monomer capacity into margin compression. Asia-Pacific leads demand because China’s 14th Five-Year Plan compels architectural coatings to increase waterborne penetration, while the South Coast Air Quality Management District in California is closing solvent exemptions for automotive refinishers. Digital inline curing and AI-driven color matching are reducing batch changeover times, enabling the economic production of 500-liter custom lots and supporting fragmentation in decorative end uses.

Key Report Takeaways

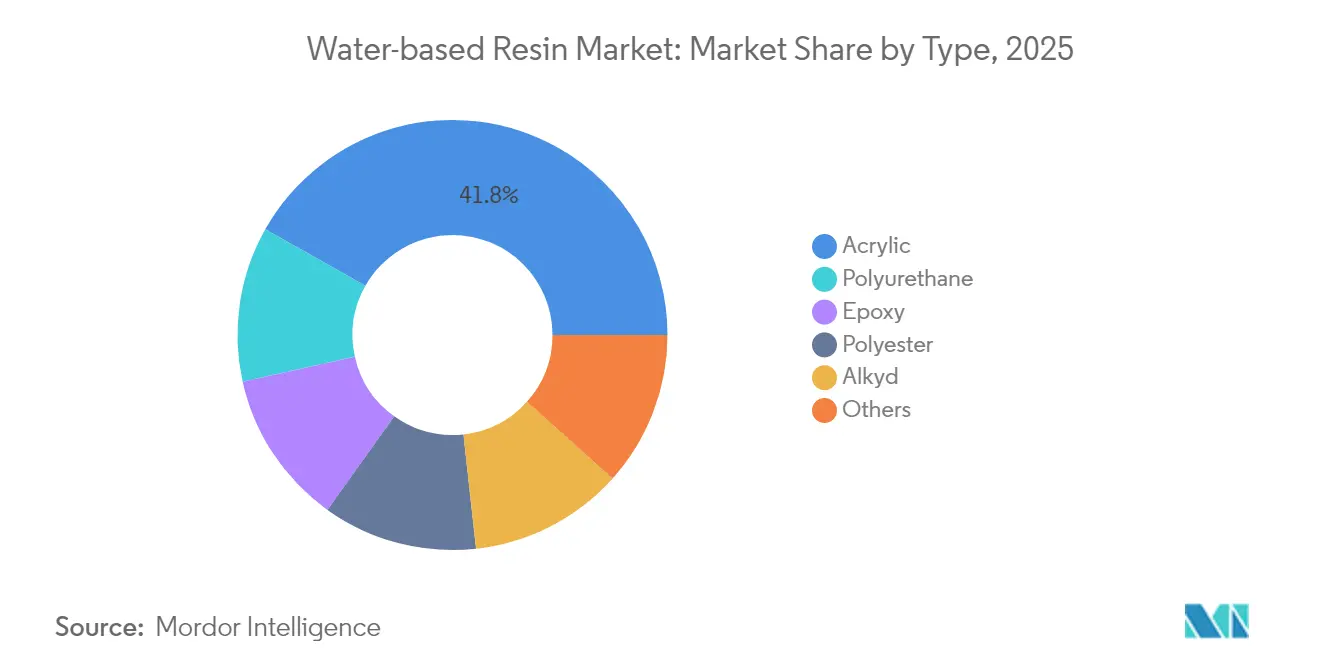

- Acrylic resins held the largest water-based resin market share at 41.82% in 2025, whereas polyurethane dispersions posted the fastest growth at a 4.02% CAGR through 2031.

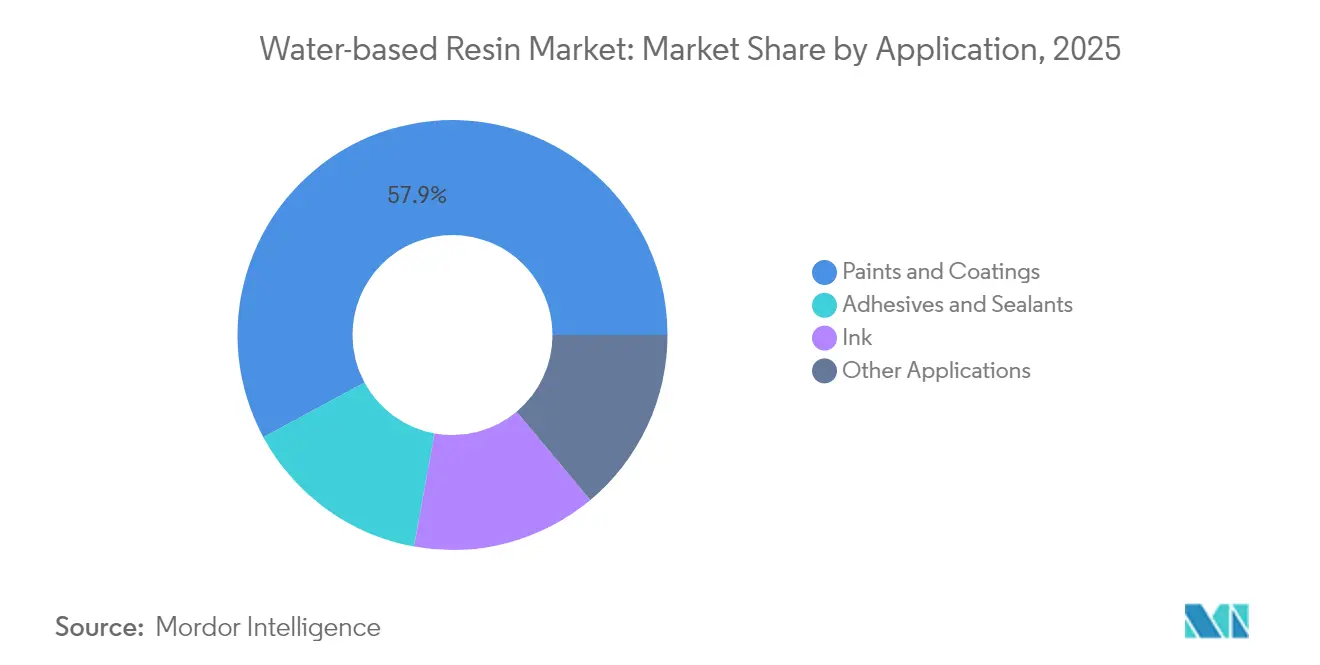

- Paints and coatings accounted for 57.88% of 2025 demand; adhesives and sealants will advance at a 4.11% CAGR to 2031, the swiftest among applications.

- Asia-Pacific commanded 47.10% of 2025 revenue and is projected to expand at 4.12% through 2031, outpacing all other regions

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Water-based Resin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VOC and EHS regulations accelerating solvent-to-water shift | +1.2% | Global, led by North America, EU, China | Medium term (2-4 years) |

| Decorative and protective coatings surge in APAC construction | +0.9% | China, India, ASEAN | Short term (≤ 2 years) |

| OEM push for low-VOC adhesives in consumer electronics | +0.5% | East Asia manufacturing hubs | Medium term (2-4 years) |

| Brand-owner ESG targets favoring bio-based content | +0.4% | North America, EU, early APAC | Long term (≥ 4 years) |

| Digital color matching and inline curing advances | +0.3% | Western Europe, North America, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

VOC And EHS Regulations Accelerating Solvent-To-Water Technology Shift

China’s GB 18581-2020 caps architectural coatings at 80-120 g VOC per liter, stricter than the EU limits, while provincial audits now occur monthly rather than annually, forcing rapid reformulations into waterborne dispersions[1]Ministry of Ecology and Environment, “GB 18581-2020 Architectural Coatings,” mee.gov.cn. South Coast AQMD Rule 1151, which has been in effect since January 2024, removes exempt solvents for automotive refinish, compelling California body shops to adopt compliant basecoats. Resin producers with certified idle capacity in Southeast Asia are earning premium margins during the transition; however, a 12-18-month lag in new dispersion reactor approvals continues to pinch supply.

Surge In Decorative And Protective Coatings Demand In Asia-Pacific Construction Boom

In the first half of 2025, China produced coatings, with over 70% of new jobs now focusing on waterborne products, a rise from previous years. Meanwhile, in India, the adoption of low-VOC protective coatings for metro rail tunnels in cities such as Bangalore, Chennai, and Hyderabad is driving growth in construction chemicals, a trend projected to continue until 2030. Additionally, contractors are increasingly opting for waterborne systems, sidestepping the costs associated with ventilation upgrades needed for solvent controls. This shift is accelerating the adoption in segments that were previously slow to adopt change.

OEM Push For Low-VOC Adhesives And Sealants In Consumer Electronics

Apple now stipulates VOC levels below 30 g/L in display lamination adhesives, disqualifying conventional polyurethane hot melts. Samsung extends similar requirements to conformal coatings on printed circuit boards[2]Samsung Electronics, “Sustainability Purchasing Guidelines 2025,” samsung.com . Covestro’s INSQIN dispersion, launched in February 2024, maintains adhesion strength within 10% of solventborne analogs while containing mostly water, enabling contract compliance without retooling.

Digital Colour-Matching / Inline Curing Advances Enabling Faster Water-Borne Lines

UV-LED units now cure waterborne acrylics rapidly, cutting energy use significantly. With AI-driven color matching, paint waste is minimized. This advancement enables mid-sized coaters to produce custom runs profitably. Inline spectroscopy automates viscosity adjustments, ensuring precise coat weight. This precision is driving faster adoption in high-speed packaging lines, even in segments previously seen as lagging. Additionally, these upgrades streamline solvent controls, further boosting uptake.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance gap in high-humidity/extreme-climate exterior uses | -0.6% | ASEAN tropics, Middle-East coast, South Asia monsoon | Medium term (2-4 years) |

| Acrylic and polyurethane feedstock price volatility | -0.4% | North America and Europe most acute | Short term (≤ 2 years) |

| Limited coater-level expertise in emerging markets | -0.3% | South America, Sub-Saharan Africa, tier-2 ASEAN cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance Gap In High-Humidity/Extreme-Climate Exterior Uses

When humidity surpasses a certain threshold, untreated steel can develop flash rust quickly. This urgency compels contractors to resort to phosphate pretreatments, inflating labor costs. In colder regions, freeze-thaw cycles diminish the tensile strength of waterborne acrylics. Meanwhile, in tropical climates, heightened humidity extends the tack-free time of these materials, leading to increased dirt accumulation. As a result, despite regulatory pressures, a significant portion of offshore platforms and bridges continue to rely on solventborne treatments.

Acrylic And Polyurethane Feedstock Price Volatility

In Q4 2023, propylene shortages linked to hurricanes drove up North American acrylic acid prices, significantly reducing converter margins. In 2024, toluene diisocyanate prices fluctuated due to China's energy control policies, which curbed capacity. While resin giants with upstream monomer units can navigate these price swings, mid-tier converters grapple with substantial quarterly margin volatility, causing them to postpone investments in water-based solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Acrylic Dominance Faces Polyurethane Disruption

Acrylic dispersions accounted for 41.82% of 2025 revenue, the highest among resin chemistries, thereby securing the leading water-based resin market share. The top positions reflect a cost-to-performance balance valued in architectural and industrial coatings. Polyurethane dispersions are projected to grow at a 4.02% annual rate to 2031, the fastest pace among chemistries, as automotive original equipment manufacturers (OEMs) adopt low-temperature curing clear coats that reduce oven energy consumption. BASF’s 2025 Zhanjiang acrylic monomer complex and its earlier Huizhou dispersion expansion secure raw materials at scale for acrylics, whereas Wanhua’s 2024 Yantai facility demonstrates Chinese entrants' push toward upstream integration.

Polyurethane momentum challenges acrylic dominance by offering greater chemical resistance for automotive refinishing and electronics assembly. Epoxy dispersions remain a specialty for infrastructure where adhesion to steel outranks cost, though flash-rust sensitivity limits their outdoor appeal. Polyester dispersions are growing modestly, with furniture players adopting low-bake powder slurries. Alkyd-modified hybrids, which blend one-quarter alkyd into acrylic emulsions, provide professional painters with a familiar flow while still reducing VOCs. The other category, covering silicone and fluoropolymer dispersions, serves release liners and anti-graffiti niches where performance supersedes price.

By Application: Paints And Coatings Lead, Adhesives Accelerate

Paints and coatings accounted for 57.88% of the 2025 demand, retaining the highest market share in the water-based resin market. Architectural paints are making strides, bolstered by China's monthly VOC audits and California's elimination of solvent exemptions. In India, there's a notable shift: protective coatings for tunnels and metros are now opting for low-VOC waterborne epoxies, catching up to decorative systems. Meanwhile, automotive refinishing is adapting to regulations such as California's Rule 1151 and European initiatives, with BASF's Glasurit 100 basecoat leading the charge by cutting VOC emissions well below EU limits.

Adhesives and sealants, although a smaller base, are forecast to grow at 4.11% through 2031—the fastest among applications. This surge is largely driven by fast-moving consumer goods giants like Unilever, which are committing a portion of their contract value towards Scope 3 emission reductions. In Southeast Asia, flexible-packaging laminators are making a strategic shift, moving away from solvent lamination lines to adopt water-based acrylic and polyurethane systems, despite a cost premium. On the electronics front, while there is cautious adoption of waterborne dispersions due to concerns about ionic contamination, Covestro's new grades are bridging the performance gaps, suggesting a potential uptick in adoption.

Geography Analysis

Asia-Pacific generated 47.10% of global revenue in 2025, the largest slice of the water-based resin market, and is projected to post a 4.12% CAGR to 2031. China's stringent monthly VOC audits are catalyzing a swift shift towards water-based solutions in decorative and protective coatings. Meanwhile, India's metro projects are bolstering the momentum in infrastructure. Both Japan and South Korea have achieved mature penetration of water-based resins in the automotive and electronics sectors, which curtails any significant growth in replacement demand. Southeast Asia lags the regional average; many tier-2 coating companies are constrained by capital limitations, particularly in upgrading to curing ovens. This gap presents an opportunity for suppliers willing to offer technical credit and deferred payment options.

North America showcases a dichotomous landscape. In California, the enforcement of Rule 1151 is propelling the shift towards waterborne solutions in automotive refinishing. In contrast, states along the Gulf Coast continue to depend on solvent-based systems for their industrial maintenance needs. Volatility in feedstock prices has dampened converter margins for 2024. Yet, the recent expansion of Lubrizol's acrylic emulsion facility in North Carolina underscores a bullish outlook on the DIY and architectural segments. In Canada, federal VOC regulations are supplemented by bio-content incentives, creating a unique market space for Arkema's bio-ethyl acrylate, despite its limited supply.

Europe boasts a dominant presence of waterborne solutions in the decorative paints industry. This is largely driven by the Architectural Coatings Directive, which imposes a VOC cap. While decorative paints have largely transitioned, protective coatings for offshore wind and marine assets still rely significantly on solvent-based solutions. This is due to the current limitations of waterborne epoxies in providing adequate corrosion resistance in challenging saline conditions. Nordic nations are leveraging carbon-border levies to promote bio-based resins, but Russia remains steadfast in its preference for solvent systems, a stance influenced by ongoing import restrictions. In South America, the Middle-East, and Africa, the transition rates to water-based solutions are sluggish. Brazil's regulatory focus is on industrial sources, while in Saudi Arabia, the emphasis is on meeting infrastructure delivery timelines, even at the expense of VOC compliance.

Regulatory Landscape

VOC and chemical-safety rules remain the primary compliance trigger accelerating conversion from solvent-borne systems to water-based resins across coatings, inks, adhesives, and sealants. In the United States, EPA VOC controls are a key lever for downstream demand, including 40 CFR Part 59 Subpart D for architectural coatings and the January 2025 final amendments to the National Volatile Organic Compound Emission Standards for Aerosol Coatings, which extended the final manufacturer compliance deadline to January 17, 2027.

In Europe, sustainability labeling and chemical regulation are increasingly shaping resin selection. The European Commission established updated EU Ecolabel criteria for decorative paints and performance coatings (Decision 2025/2607, December 2025), explicitly covering water-based aerosol spray paints within the criteria scope. Separately, Regulation (EU) 2026/1168 amended REACH Annex XVII to restrict synthetic polymer microparticles, introducing timelines and derogations that affect formulation design and additive packages used with waterborne systems.

Value Chain Analysis

Water-based resin value chains begin upstream with petrochemical and, increasingly, alternative feedstocks (acrylic monomers, polyurethane intermediates, epoxy raw materials, and emerging recycled or bio-attributed inputs). They then progress through polymerization and dispersion manufacturing, formulation into coatings, adhesives, and inks, and finally distribution to OEMs, contractors, and packaging and printing converters. Integration into monomers remains a differentiator during periods of acrylic and isocyanate volatility, while mid-tier producers and formulators depend more on spot supply and tolling for critical monomers and specialty additives.

Downstream demand is increasingly compliance-led, which raises the role of application testing, certification, and technical service alongside physical production. Regional localization is visible in Asia through new and expanded resin and adjacent chemical capacity aimed at demand centers, including the Berger-Becker Coatings resin facility inaugurated in Nagpur, India (May 2026), and integrated-site investments such as BASF’s Zhanjiang expansion for acrylics. Qualification cycles and supply allocation stay constrained by factors cited in the market context, including approval lead times for new dispersion reactors and limited availability of bio-based feedstock.

Competitive Landscape

The water-based resin market is moderately fragmented. Chinese producers are scaling rapidly. Mid-tier players focus on formulation support. Synthomer divested its performance elastomers to concentrate on specialty dispersions, freeing capital to embed application engineers at key OEM sites. White-space opportunities cluster around bio-based feedstocks and digital process control. Dow and Evonik partner with equipment suppliers to embed inline viscosity monitoring, while smaller firms explore agricultural-waste ethanol as a route to lower-cost bio-acrylics. Competitive intensity is expected to remain steady as large producers balance capacity additions with demand growth, avoiding oversupply.

Water-based Resin Industry Leaders

BASF

Dow

Arkema

Allnex Netherlands BV

Covestro AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory tightening is creating near-term whitespace for compliant waterborne resin systems in industrial and architectural coatings, where solvent exemptions or fragmented local standards previously slowed reformulation. China implemented mandatory national standards GB 30981.1-2025 and GB 30981.2-2025 on June 1, 2026, setting unified VOC and hazardous-substance limits across architectural and industrial coatings. That expansion increases the volume of reformulation and qualification work that resin suppliers can capture through turnkey technical packages covering resin, additives, and process support. Saudi Arabia also tightened compliance for industrial coatings by revoking the VOC exemption for water-based industrial coatings and requiring full-scope testing per SASO 2511:2024 as of May 8, 2026, which drives demand for documented, test-ready waterborne binder platforms.

Supply-side actions and certification pathways are widening commercial lanes beyond basic solvent replacement. Capacity and localization moves, such as WYN Polymers commissioning a new reactor in Mexico in April 2026 (lifting water-based polymer output by about 30%) and Berger-Becker Coatings starting resin manufacturing in Nagpur, India (May 2026), point to active investment aimed at shorter lead times and localized grades for regional coatings and packaging markets. In parallel, adoption of mass-balance and bio-attributed inputs, such as ISCC PLUS-certified waterborne resin sites, along with R&D progress in bio-based and non-isocyanate waterborne polyurethane chemistries, offers a route to address two barriers highlighted in the market context: constrained bio-based feedstock availability and performance gaps in harsh exterior or high-humidity environments.

Recent Industry Developments

- July 2026: BASF expanded its portfolio of certified biomass-balanced additives for architectural coatings, including new Rheovis biomass-balanced grades. This supports formulators seeking lower-carbon raw material options within existing waterborne coatings lines while retaining familiar rheology and handling performance.

- November 2025: BASF commissioned a new high-performance dispersant production line at the Jiangbei New Material Technology Park in Nanjing, China, using Controlled Free Radical Polymerization (CFRP) technology. The added capability strengthens supply for waterborne formulations that require tighter control of pigment dispersion and stability in coatings and inks.

- November 2024: BASF opened a new production line for water-based dispersions in Heerenveen, the Netherlands, increasing capacity for Joncryl and Acronal Pro without adding CO2 emissions by leveraging existing infrastructure. The expansion improves availability of water-based polymers used in packaging inks and coatings, where qualification cycles and supply continuity influence converter switching decisions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from resins formulated and sold as water-based systems, where water is the main carrier medium, and used as binders in downstream products such as coatings, adhesives, and inks.

Scope exclusions: We exclude solvent-borne resins and reactive systems sold primarily as 100% solids, even if they are later dispersed in water.

Segmentation Overview

- By Type

- Acrylic

- Polyurethane

- Epoxy

- Polyester

- Alkyd

- Others

- By Application

- Paints and Coatings

- Adhesives and Sealants

- Ink

- Other Applications

- Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by setting the technical boundary for what is counted as a water-based resin, then mapping where demand shows up first in public data. We use open sources such as US EPA regulations and VOC control guidance, European Commission and ECHA chemical information pages, UN Comtrade trade statistics for relevant polymer and resin movements, and national statistics offices that publish industrial output series linked to coatings and construction activity.

To keep the model tied to real-world production and usage, we review company annual reports, investor presentations, product catalogs, and association publications that document shifts from solvent-borne to water-borne formulations. Where the public record is thin, we rely on paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data to sanity-check the direction and magnitude of supply and demand changes. These desk research sources are illustrative and not exhaustive, since other public documents were used throughout for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work is used to stress-test key assumptions that desk sources do not quantify well, such as typical formulation shifts, pricing movement by resin family, and how fast water-based systems are replacing legacy chemistries in each end use. We spoke with manufacturers, distributors, formulators, and downstream buyers across major regions, so our sizing choices reflect actual purchasing behavior rather than only published production signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 48% |

| Mid tier: 44% | Functional/Unit leaders: 33% | EMEA: 30% |

| Smaller Players: 21% | Managers: 55% | Americas: 22% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where demand pools are reconstructed from downstream activity indicators, then translated into resin consumption and revenue using interview-validated share and pricing assumptions. In practice, we start from end-use signals such as paints and coatings output, construction and refurbishment activity, packaging and printing volumes, and then apply water-based penetration rates and resin-intensity factors that are specific to each use case.

Once the demand pool is formed, the revenue layer is created using realistic price bands by resin family and application, with adjustments for mix changes highlighted by industry respondents. To avoid overreliance on any one assumption, we corroborate totals using selective bottom-up approximations such as sampled supplier revenues, channel checks, and volume times average selling price calculations for key resin types. Where a bottom-up view is incomplete, gaps are handled by scaling using coverage ratios anchored to trade flows, capacity additions, and regional coatings demand patterns.

For forecasting, scenario analysis is used with a base case that tracks expected regulation tightening on VOCs, gradual substitution timelines, and normal capacity utilization behavior. The variables that most often move the forecast are water-based share progression by application, regional construction spending direction, industrial production growth, crude-linked raw material cost pressure passing into resin pricing, and announced capacity or debottlenecking plans.

Data Validation & Update Cycle

Outputs are checked through several passes so the final numbers do not depend on one dataset or one analyst judgment. We compare modeled results against independent signals such as import and export movements for relevant materials, downstream coatings volume trends, and public commentary on utilization and pricing, then investigate any variance that looks out of line.

Before sign-off, assumptions are reviewed across the team, and follow-up calls are triggered when new information changes a core driver such as water-based penetration, pricing, or capacity additions. The report is refreshed annually, and interim updates are made when material events occur that can change demand or supply behavior. Right before delivery, a final update pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Water Based Resins Market Size Compared With Other Published Estimates

Published market values for water-based resins can look far apart, even when the market name appears identical, because the scope and the measurement choices are not always the same. The biggest drivers usually come from what is counted as water-based resin revenue, how pricing is treated across resin families, and which years are used for currency conversion and inflation effects.

Coatings and construction activity trends, together with trade-flow checks for resin-related materials and interview feedback on penetration rates, are the evidence that keeps Mordor Intelligence's estimate tied to a defined demand pool rather than a broader chemical basket. Gaps also show up when some publishers fold in adjacent water-dispersed polymer categories, count formulated end products rather than resin binders, or apply faster adoption curves and higher price escalation without re-checking against supply additions and utilization behavior.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 48.76 B (2026) | |

| Global Consultancy A | USD 56.50 B (2024) | Uses an earlier base year and can capture a broader value chain by mixing resin value with higher-level application reporting, which can lift totals when coatings and adhesives are bundled with binder revenue. |

| Industry Publisher B | USD 60.64 B (2025) | Applies a different base-year choice and longer-horizon growth assumptions, and the definition may include adjacent water-dispersed polymer categories, which can increase the counted revenue beyond binder-focused resin scope. |

Taken together, the spread is mostly explained by boundary setting, base-year timing, and how adoption and pricing are carried forward. Our approach stays transparent because the total can be traced back to a small set of observable demand signals, validated shares, and repeatable checks that can be rerun as new public data and expert feedback arrive.

Key Questions Answered in the Report

What is the current global value of the water-based resin market?

The water-based resin market size is expected to reach USD 48.76 billion by 2026.

Which region leads demand growth through 2031?

The Asia-Pacific region is forecast to grow at 4.12% annually, the fastest among all regions.

Which resin type is expanding most quickly?

Polyurethane dispersions are projected to grow at a 4.02% CAGR to 2031.

What is the chief regulatory driver of conversion?

Stricter VOC limits in China, the EU, and California eliminate solvent exemptions and force the adoption of water-based formulations.

Page last updated on: