Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 26.28 Billion |

| Market Size (2031) | USD 32.12 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

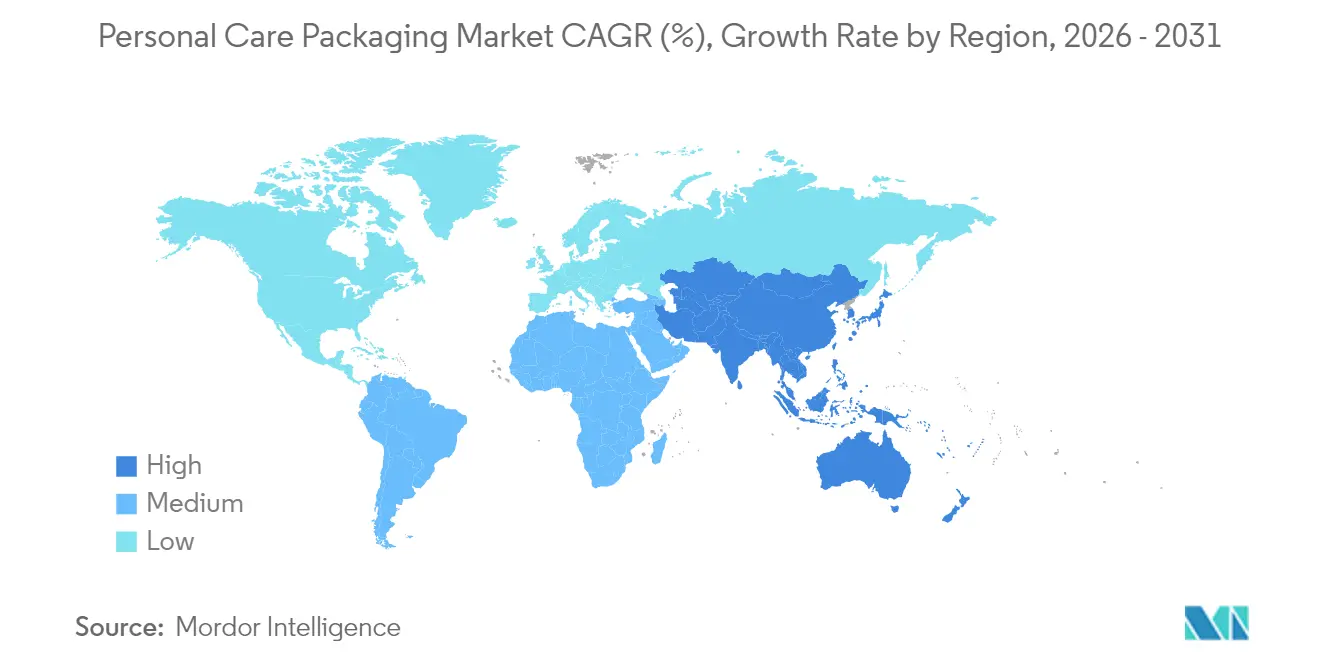

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

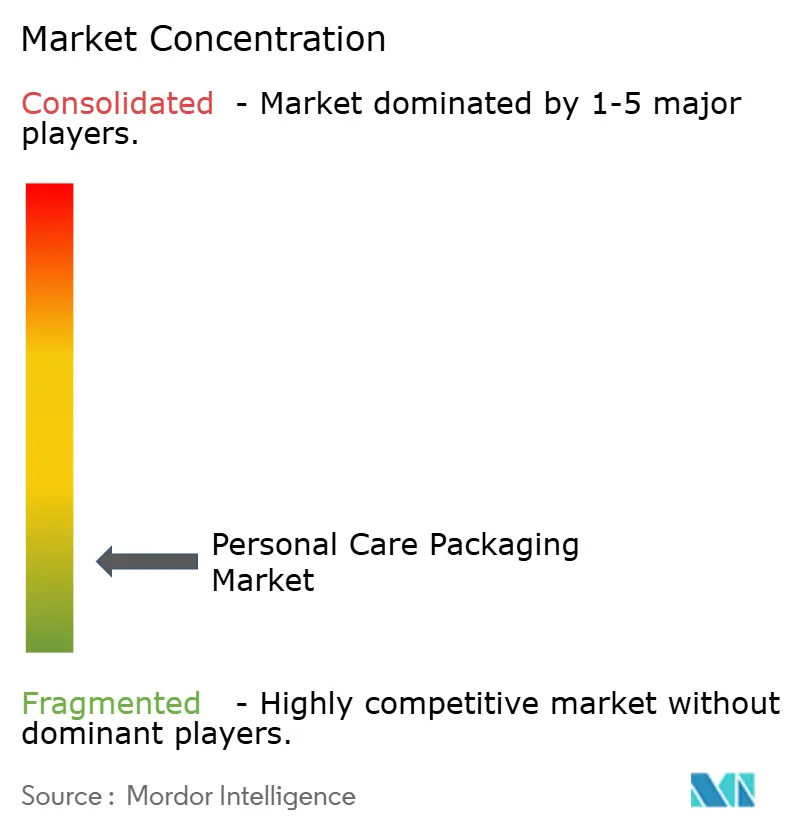

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Care Packaging Market Analysis by Mordor Intelligence

The Personal Care Packaging Market size was valued at USD 25.14 billion in 2025 and is estimated to grow from USD 26.28 billion in 2026 to reach USD 32.12 billion by 2031, at a CAGR of 4.09% during the forecast period (2026-2031).

Intensifying regulation on post-consumer recycled (PCR) content, e-commerce’s need for ship-ready packs, and consumer premiumization together pull the sector away from commodity supply toward precision-engineered formats. Plastics remain the volume backbone, yet flexible pouches, mono-material tubes, and refill cartridges capture momentum because they cut freight costs and simplify recycling. Converter capital now flows into chemical-recycling partnerships and edge-AI inspection lines that trim changeover waste, while brand owners renegotiate resin contracts to de-risk feedstock swings. Competitive focus shifts from pure scale to modular platforms that allow closure or dosage changes without retooling, letting marketers launch limited editions at lower cost and faster speed.

Key Report Takeaways

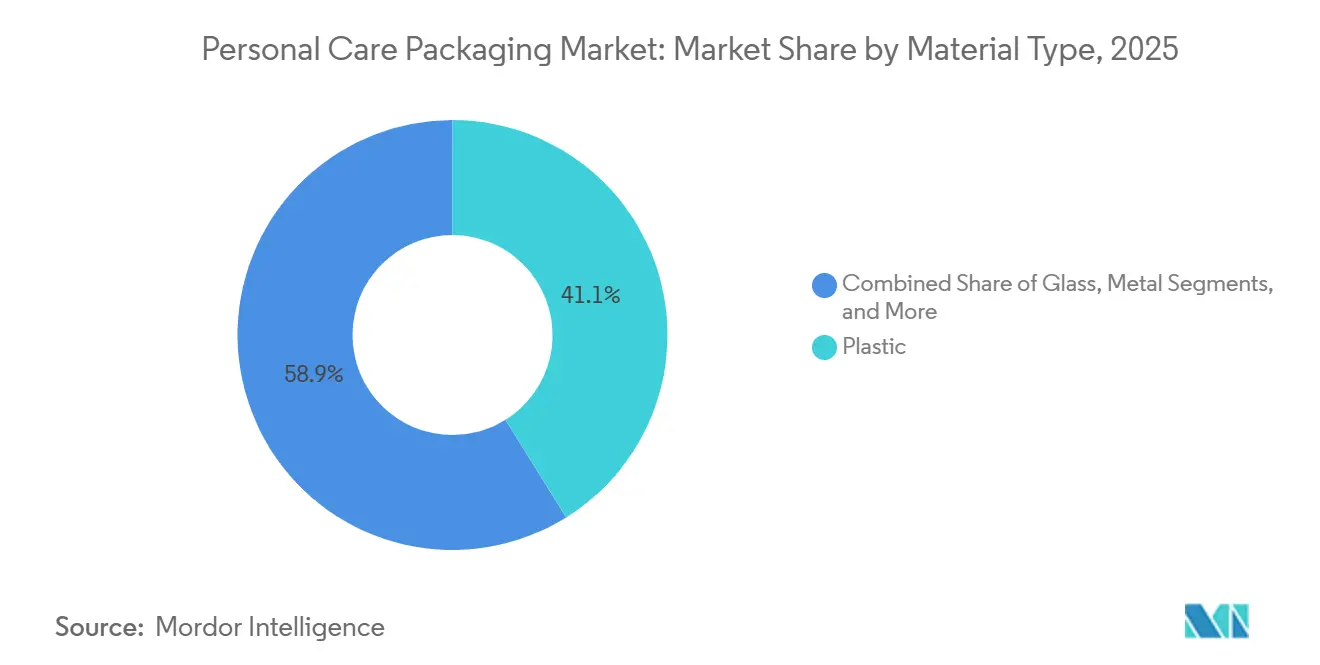

- By material type, plastics held 41.12% of the personal care packaging market share in 2025 and are set to post a 4.89% CAGR through 2031.

- By packaging format, rigid variants accounted for 62.76% of the personal care packaging market in 2025, whereas flexible formats posted the fastest growth at a 4.51% CAGR to 2031.

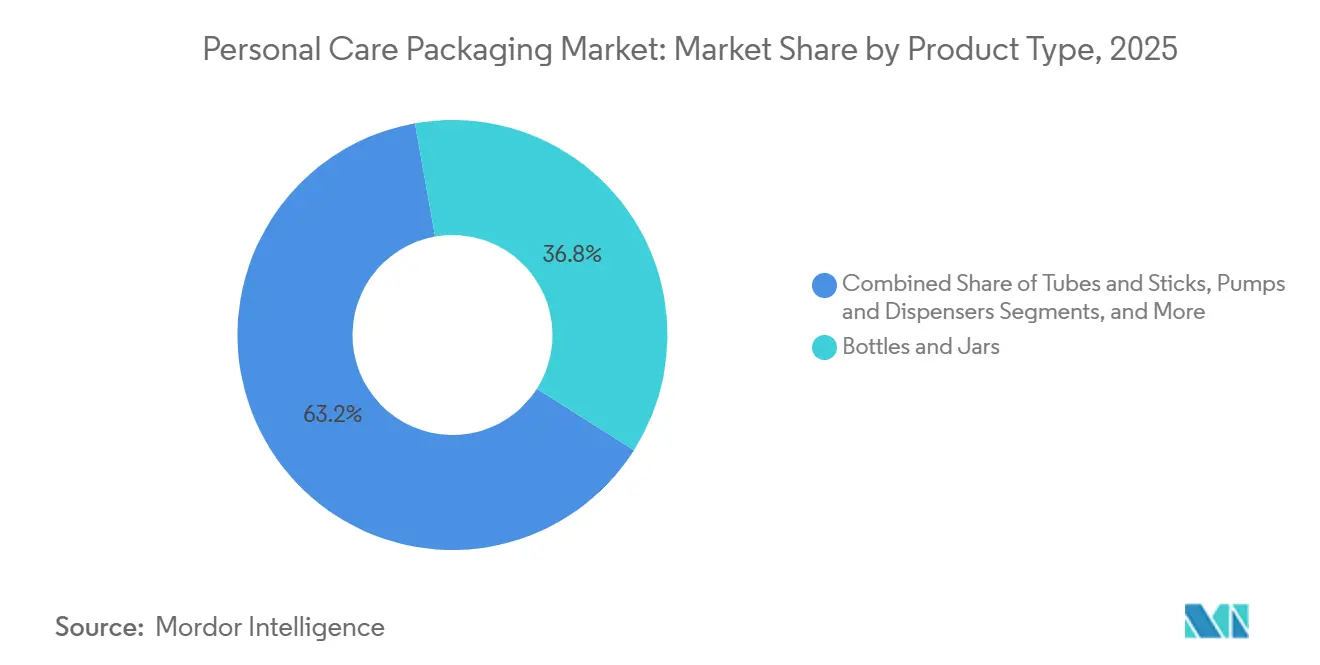

- By product type, bottles and jars accounted for 36.81% of revenue in 2025, while pouches and sachets are projected to grow at 5.27% over 2026-2031.

- By application, skin care led with 31.12% of value in 2025; deodorants and fragrances record the highest projected CAGR at 5.44% to 2031.

- By geography, Asia-Pacific accounted for 33.37% of 2025 sales, yet South America is forecast to grow at a 5.08% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Care Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of Beauty SKUs in Emerging Markets | +0.8% | Asia-Pacific core, South America, Middle East | Medium term (2-4 years) |

| Omni-Channel Fulfilment Driving Protective and Ship-Ready Packs | +0.7% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Sustainability Rules Mandating More Than 30% PCR Content | +0.9% | Europe and North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Rapid Adoption of Refill-at-Home Dispensing Formats | +0.6% | Europe and North America urban centers | Medium term (2-4 years) |

| Edge-AI Enabled Filling Lines Cutting SKU Cost | +0.5% | Global, early adoption in North America and Asia-Pacific | Long term (≥ 4 years) |

| Explosive Growth of Male Grooming in Southeast Asia | +0.6% | Southeast Asia (Indonesia, Vietnam, Philippines, Thailand) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization Of Beauty SKUs In Emerging Markets

Rising middle-class incomes in India, Brazil, and China steer shoppers toward branded personal-care products packaged in glass, aluminum, and premium plastics that signal quality.[1]Economic Times, “India Beauty Personal Care Market Grows 12 Percent 2025,” economictimes.indiatimes.com India’s beauty sector grew 12% in 2025 as urban consumers traded up to embossed bottles, metallized jars, and tamper-evident pumps. Brazilian brand Natura scaled refillable glass programs that position permanence as proof of sustainability, fostering premium shelf pricing. In China, tier-2 cities recorded an 18% surge in male-grooming serums that require airless dispensers to protect active ingredients and reinforce scientific branding. Converter investment therefore tilts to hot-stamping, vacuum-metallization, and airless-pump lines that deliver higher-margin orders while satisfying retailer calls for luxury aesthetics.

Omni-Channel Fulfilment Driving Protective And Ship-Ready Packs

Beauty e-commerce reached 35% of North American sales and 28% in Europe during 2025, shifting packaging design toward variants that survive parcel sorting while remaining shelf-presentable.[2]McKinsey and Company, “Beauty E-Commerce Packaging Trends 2025,” mckinsey.com Amcor’s dual-wall flexible pouch reduced breakage rates by 40% in direct-to-consumer shipments, proving that thin, rigid bottles can be replaced with lighter films. Retailers also demand packs that migrate from store display to mailing carton without extra void fill, promoting stackable rigid bottles with integrated handles and pouches reinforced at stress corners.As freight averages 8-12% of landed cost, shippers favor designs that boost pallet density and reduce dimensional weight fees.

Sustainability Rules Mandating More Than 30% PCR Content

European Union Regulation 2025/40 obliges plastic packs to contain at least 30% PCR by 2030, catalyzing converter deals with chemical recyclers and investment in chain-of-custody traceability. L’Oréal targets 50% PCR globally by 2030, forcing the renegotiation of polyethylene and polypropylene contracts that meet cosmetic-grade purity standards. California’s Senate Bill 54 mirrors European thresholds, so multinationals harmonize portfolios worldwide to avoid dual tooling. ISO 14021 disclosure norms tighten proof requirements for “recyclable” claims, hiking compliance budgets but also rooting out greenwashing. PCR premiums of 5-8% over virgin resin raise input costs, yet brands absorb the hit because sustainability credentials increasingly sway consumer choice.

Rapid Adoption Of Refill-At-Home Dispensing Formats

Refill systems grew quickly in Europe and North America as brands raced to cut single-use plastic. Unilever’s Refill on the Go kiosks spread to 150 UK stores, slicing pack weight per use by 70% and shrinking transport emissions via concentrate logistics. L’Oréal’s refillable lipstick uses magnetic cartridges that sell at a 40% discount to traditional units after the initial case purchase, generating customer lock-in. France’s AGEC law sets a 20% refillable target in large retail by 2030, spurring investment in dispenser design and reverse logistics for collection and sanitation. Concentrate pouches riding inside durable containers shift volume to flexible films and drive repeat online orders that balance convenience with sustainability messaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Polyolefin and PET Feedstock Prices | -0.6% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Single-Use Plastics Bans Across the EU and Select US States | -0.5% | Europe and North America (California, Washington, New York) | Medium term (2-4 years) |

| Supply-Chain Chokepoints in Aluminium and Glass | -0.4% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Rise of Solid-Format Toiletries Replacing Primary Packs | -0.3% | North America and Europe urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Polyolefin and PET Feed-Stock Prices

Polyethylene and PET swung 15-25% quarter-over-quarter during 2024, compressing margins for converters locked into 60-90-day selling prices.[3]ICIS, “PET Resin Prices Volatile Amid Supply-Demand Shifts,” icis.com PCR PET trades at a 10-15% premium to virgin PET, magnifying volatility for firms pursuing recycled-content mandates. Smaller players without hedging tools exited or merged, evidenced by three European tube makers that sold out in 2025. Capital-spending pauses follow price spikes, delaying the installation of new extrusion or blow-molding lines and crimping supply responsiveness. PCR PET trades at a 10-15% premium to virgin, compounding volatility for firms chasing recycled-content mandates. Brands respond by signing annual resin contracts that sacrifice opportunistic savings for budgeting certainty, yet the strategy stifles short-term flexibility.

Single-Use Plastics Bans Across The EU And Select US States

The EU’s Single-Use Plastics Directive restricts non-recyclable items. California’s SB 54 extends similar rules, fragmenting the US market.[4]California Legislature, “Senate Bill 54: Plastic Pollution Producer Responsibility Act,” leginfo.legislature.ca.gov Brands either retool packs to meet the strictest global rule or maintain region-specific SKUs, increasing inventory complexity and tooling amortization stress, particularly for smaller companies. Certification ambiguity on compostable or novel bio-based films further slows material innovation because municipal infrastructure remains patchy. Retailers apply extra charge-backs for non-compliant packs, squeezing margins and prompting accelerated shifts to mono-material polyethylene tubes, paperboard secondary packs, or aluminum formats that clear recyclability tests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Sustain Leadership While Bio-Based Variants Gain Traction

Plastics generated 41.12% of 2025 revenue and, aided by PCR and bio-resin integration, are on track for the fastest 4.89% CAGR to 2031, reinforcing their primacy in the personal care packaging market. Polyethylene pouches and squeeze tubes dominate because chemical resistance and heat-seal strength align with concentrate refills, while polypropylene excels in closures and pumps that require fatigue resilience. PET maintains share for clear rigid bottles that protect fragrances, even as PVC recedes under European phase-out pressure tied to plasticizer migration. Sugarcane-based polyethylene and corn-origin PLA pick up 3% of the plastics segment, favored by brands willing to pay double-digit premiums to flag sustainability on-pack.

Glass, accounting for 22% in 2025, wins in prestige fragrance where heft signals craftsmanship, yet e-commerce breakage and higher freight hinder volume scaling. Aluminum’s 18% foothold, driven by deodorant aerosols and travel formats, benefits from narratives of infinite recyclability. Paperboard’s 19% share centers on folding cartons that tell brand stories, though moisture sensitivity curtails primary-pack usage. Together, these dynamics keep plastics at the core of the personal care packaging market, but rising bio-derived options broaden material choices and encourage converters to diversify their extruder portfolios.

By Packaging Format: Rigid Retains Scale Advantage While Flexible Accelerates

Rigid units accounted for 62.76% of the 2025 value and maintain dominance due to established filling-line infrastructure and shelf presence vital to skin and hair care. Integrated pumps and aerosol valves bolster brand trust through precise dosing, supporting higher price points within the personal care packaging market. Flexible packs, the remaining 37.24%, outpace the market at 4.51% CAGR, fueled by e-commerce durability, material-weight savings of up to 70%, and regulatory eco-modulation fees that penalize heavy, rigid items.

Amcor’s dual-wall pouch that merges barrier and cushioning layers proves the next step, eliminating separate inserts while halving breakage claims. Refill platform preferences further tilt toward flexible concentrates, as multi-use pouches amortize freight emissions across several bathroom cycles. Meanwhile, rigid producers mitigate share erosion by pushing lightweighting and tethered-cap compliance to satisfy EU directives without sacrificing consumer familiarity.

By Product Type: Bottles And Jars Anchor Spend, Pouches Present Fastest Upside

Bottles and jars supplied 36.81% of 2025 turnover, with PET bottles leading mass hair care and glass jars anchoring prestige creams. Transparent walls let users monitor fill levels, helping sustain repeat purchases in the personal care packaging market. Pumps and dispensers follow at 21%, distinguished by AptarGroup’s 2025 SimpliSqueeze valve that meters viscous serums, curbing over-dispensing and reinforcing premium perceptions.

Pouches and sachets, forecast to climb 5.27% through 2031, ride trial-size demand, travel rules, and home-refill economics. Single-use sachets face bans in Europe and select US states, pushing brands to resealable multi-use pouches that meet recycling thresholds. Caps and closures, 15% in 2025, transition to tethered designs that add fractions of a cent to unit cost but avoid regulatory penalties. Mono-material airless dispensers and dropper assemblies are ideal for oxygen-sensitive formulations, capturing niche revenue and raising average selling prices for converters.

By Application: Skin Care Leads Revenue, Deodorants And Fragrances Outpace Growth

Skin care delivered 31.12% of 2025 sales because serums, moisturizers, and sunscreens command complex barrier packs that justify premium margins inside the personal care packaging market share discussion. Hair care, at 24%, contends with solid shampoo bars that remove bottle demand, yet color-treat and anti-dandruff liquids sustain PET bottle throughput.

Deodorants and fragrances project the fastest 5.44% CAGR to 2031 as male grooming in Southeast Asia spikes and premium perfumes in Latin America gain disposable income traction. Aerosol aluminum cans and sculpted glass flacons dominate these categories, lifting average pack value. Oral care sits at 16%, with laminated toothpaste tubes moving to mono-material PE designs that streamline recycling. Make-up, baby care, and travel amenities fill the remainder, each adopting lightweight or refillable formats to align with retailer waste thresholds.

Geography Analysis

Asia-Pacific held 33.37% in 2025 and remains the anchor of the personal care packaging market. China’s premium fragrance launches adopt refillable glass to court eco-minded shoppers, while India’s urban consumers trade up to metallized pumps across skin and hair care. Southeast Asia’s double-digit growth in male grooming drives aluminum aerosol can lines, while Japan’s aging society supports anti-aging airless dispensers. South Korea’s export-oriented K-beauty labels specify moisture-barrier pouches that withstand tropical transits, and Australia moves early on 30% PCR mandates, serving as a proving ground for traceability tech before Asia-wide rollout.

Europe controlled 28% in 2025, shaped by strict PCR quotas, tethered-cap rules, and eco-label audits that force converters into chemical-recycling alliances. Germany and France scale in-store refill aisles, cutting per-use material by 70% and binding shoppers to durable containers. Italy and Spain rely on glass flacons to express luxury in fragrance clusters, but freight and breakage temper unit growth. Eastern Europe, led by Poland, attracts converter nearshoring that pairs lower labor cost with regional proximity, adding tube and closure capacity for Western brands.

North America contributed 22% of revenue in 2025, with US omni-channel demands spurring packs that move from shelf to doorstep without extra void fill. Canada’s phased single-use plastics ban accelerates mono-material flexibles and paperboard. Mexico’s nearshored capacity alleviates tariff and lead-time constraints for US brands. Divergent state laws, notably California’s SB 54 and Washington’s packaging tax, raise complexity, prompting nationwide adoption of the toughest standard to avoid fragmented portfolios.

South America, forecast to rise 5.08% CAGR through 2031, benefits from Brazil’s refillable glass initiatives and Argentina’s aspirational urban buyers who invest income in imported fragrances that command elevated pack values. The Middle East, at 8%, focuses on ornate glass and metallized closures for luxury scents, with Turkey as a converter hub. Africa’s 7% share of the market relies heavily on sachets for affordability, yet municipal bans on single-use plastics are nudging markets toward resealable, multi-use pouches.

Competitive Landscape

The top-10 suppliers, including Albea, Amcor, AptarGroup, Gerresheimer, HCP Packaging, Silgan Holdings, and Verescence, command roughly 45% of the global capacity. This dominance, however, leaves a gap for regional specialists, particularly in areas like mono-material tubes and airless pumps. The competitive landscape is shifting focus towards modular platforms. These platforms facilitate closure swaps and dosage tuning without the need for retooling. A testament to this trend is Amcor’s Moda system, which has successfully reduced SKU proliferation costs by 20%. Similarly, AptarGroup’s SimpliSqueeze valve, known for its precise dose control, commands a 15-25% price premium in the luxury skincare segment.

Securing post-consumer recycled (PCR) resin has become a strategic move, leading to a wave of forward-integration deals. A prime example is Amcor’s January 2026 partnership, which secured 50,000 tons per year of PCR PET, underscoring the importance of hedging against feedstock risks. In the realm of mergers and acquisitions, Silgan's USD 120 million acquisition of a Brazilian tube manufacturer not only broadens its nearshore presence but also highlights the industry's consolidation trend. Meanwhile, Verescence's innovation in producing lighter glass not only cuts freight emissions in half but also ensures the continued relevance of glass in packaging.

While established players dominate, startups are venturing into innovative territories, exploring seaweed films and mycelium closures. However, these newcomers grapple with significant challenges, facing cost premiums ranging from 50-100% and navigating uncharted regulatory pathways, which keeps their adoption limited. On the technological front, edge-AI vision systems are making waves. These systems not only minimize defect scrap but also facilitate micro-batch runs. This capability allows brands to cater to micro-segmentation, further enhancing the value proposition for converters beyond mere commodity forming.

Personal Care Packaging Industry Leaders

Albéa S.A.

HCP Packaging Group

Gerresheimer AG

Amcor plc

AptarGroup, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Amcor partnered with a European chemical recycler to secure 50 000 t/y of PCR PET, jointly investing in sorting and washing lines to lift food-grade output by 25% by 2027.

- December 2025: AptarGroup released a mono-material polypropylene airless dispenser that eliminates landfill-bound multi-material parts and commands a 20% price premium.

- November 2025: Gerresheimer finished a EUR 80 million (USD 84.8 million) expansion of its German glass-vial plant to serve cosmetics requiring ISO 15378 compliance.

- October 2025: Silgan Holdings bought a Brazilian tube maker for USD 120 million, adding 200 million units of annual capacity and proprietary barrier lamination.

- September 2025: Albea opened a USD 50 million facility in India featuring automated filling and in-house decoration to cut lead times for domestic and multinational clients.

Global Personal Care Packaging Market Report Scope

The Personal Care Packaging Market Report is Segmented by Material Type (Plastic, Glass, Metal, Paper and Paperboard), Packaging Format (Flexible, Rigid), Product Type (Bottles and Jars, Tubes and Sticks, Pumps and Dispensers, Pouches and Sachets, Caps and Closures, Other Product Types), Application (Skin Care, Hair Care, Oral Care, Make-Up Products, Deodorants and Fragrances, Baby Care, Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Plastic | Polyethylene |

| Polypropylene | |

| PET and PVC | |

| Polystyrene | |

| Bio-Based Plastics | |

| Other Plastic Material Types | |

| Glass | |

| Metal | |

| Paper and Paperboard |

By Packaging Format

| Flexible |

| Rigid |

By Product Type

| Bottles and Jars |

| Tubes and Sticks |

| Pumps and Dispensers |

| Pouches and Sachets |

| Caps and Closures |

| Other Product Types |

By Application

| Skin Care |

| Hair Care |

| Oral Care |

| Make-Up Products |

| Deodorants and Fragrances |

| Baby Care |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Material Type | Plastic | Polyethylene |

| Polypropylene | ||

| PET and PVC | ||

| Polystyrene | ||

| Bio-Based Plastics | ||

| Other Plastic Material Types | ||

| Glass | ||

| Metal | ||

| Paper and Paperboard | ||

| By Packaging Format | Flexible | |

| Rigid | ||

| By Product Type | Bottles and Jars | |

| Tubes and Sticks | ||

| Pumps and Dispensers | ||

| Pouches and Sachets | ||

| Caps and Closures | ||

| Other Product Types | ||

| By Application | Skin Care | |

| Hair Care | ||

| Oral Care | ||

| Make-Up Products | ||

| Deodorants and Fragrances | ||

| Baby Care | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the expected global spending on personal care packaging by 2031?

The market is forecast to reach USD 32.12 billion by 2031, up from USD 26.28 billion in 2026.

Which packaging material is growing fastest within beauty and personal care?

Plastics, driven by bio-based resins and post-consumer recycled content, are projected to expand at a 4.89% CAGR through 2031.

Why are flexible pouches gaining share in personal care shipments?

They cut packaging weight by up to 70%, lower freight costs, and resist damage during e-commerce parcel sorting, supporting a 4.51% CAGR to 2031.

How do PCR mandates in Europe affect packaging choices?

Rules requiring at least 30% recycled content push brands toward PCR plastics, spur chemical-recycling investments, and raise raw-material costs by 5-8%.

Where is demand for deodorant packaging rising most quickly?

Southeast Asia, especially Indonesia and Vietnam, shows double-digit growth as male grooming accelerates, supporting a 5.44% CAGR for deodorant and fragrance packs.

What technological upgrade helps converters cut SKU changeover costs?

Edge-AI–powered vision systems streamline filling-line adjustments, while modular platforms such as Amcor’s Moda can trim SKU-proliferation expenses by about 20%.

Page last updated on: