Persulfates Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.04 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

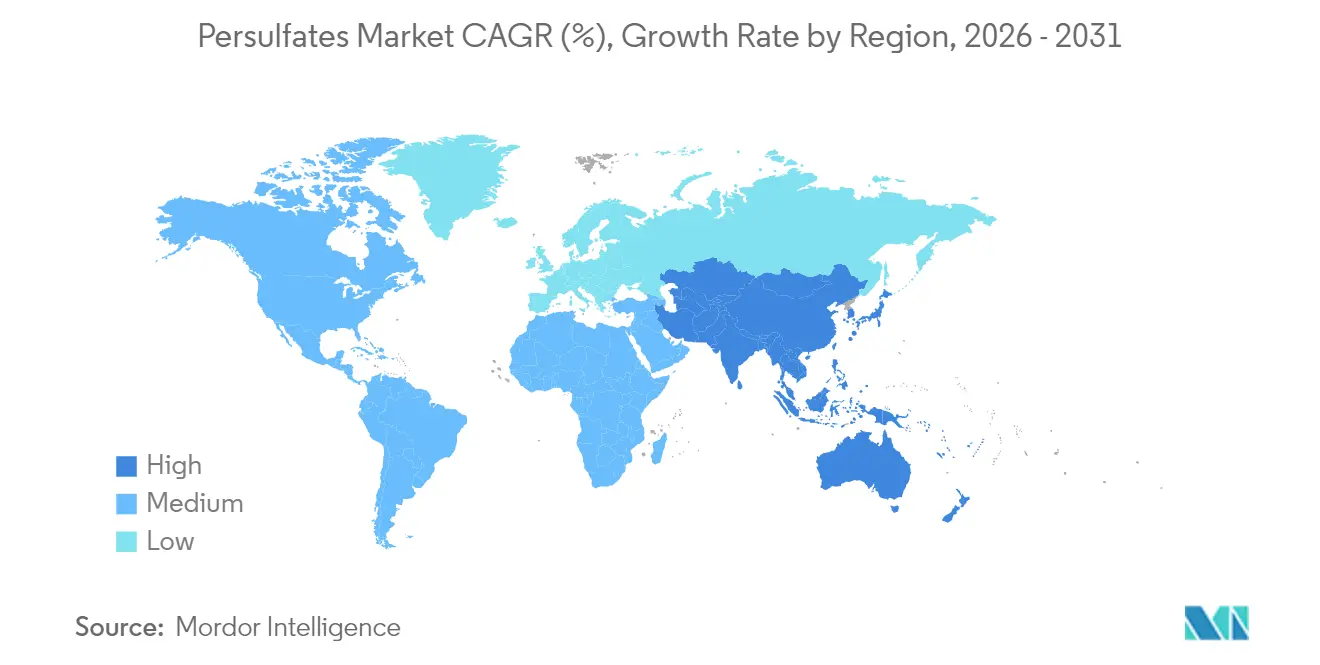

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

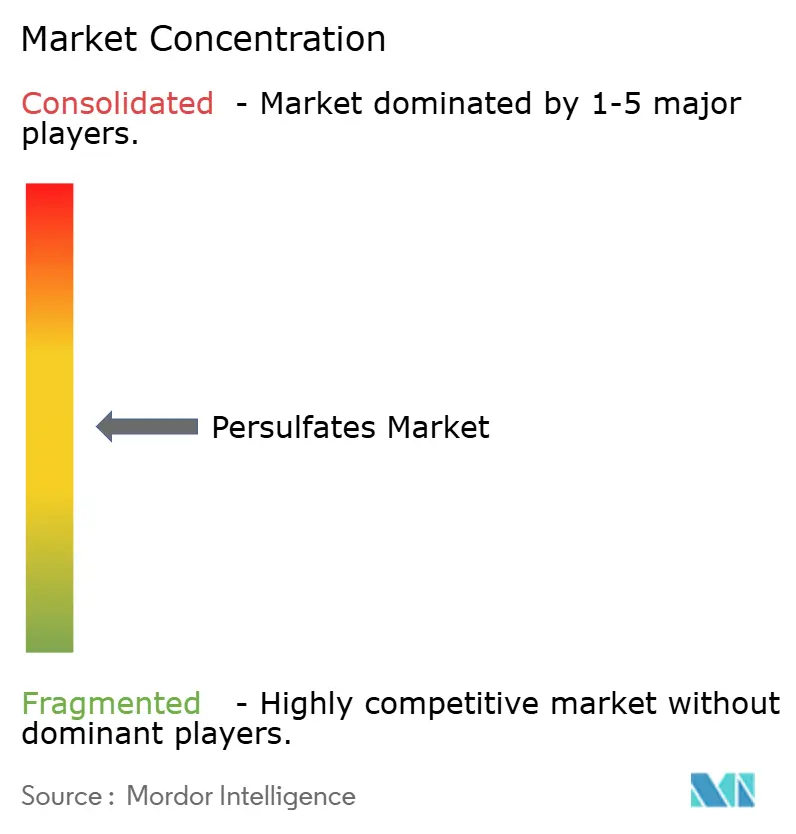

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Persulfates Market Analysis by Mordor Intelligence

Persulfates market size in 2026 is estimated at USD 895.9 million, growing from 2025 value of USD 870 million with 2031 projections showing USD 1.04 billion, growing at 2.98% CAGR over 2026-2031. Demand resilience rests on persulfates’ strong oxidizing capacity, which underpins their use in semiconductor wafer cleaning, polymer initiation, oil‐field stimulation, and advanced water treatment. Asia-Pacific keeps the largest regional share and the fastest growth tempo as governments boost chip manufacturing incentives, while specialty grades priced at a premium are expanding faster than commodity volumes in North America and Europe. Tight hydrogen-peroxide supply, stricter warehousing codes, and sulfate-discharge rules raise the cost floor but also elevate the technical entry barrier, favoring integrated producers. Competitive focus has shifted toward value-added formulations, on-site dosing technologies, and service agreements that lock in multi-year volumes, sheltering margins even as bulk chemical prices fluctuate.

Key Report Takeaways

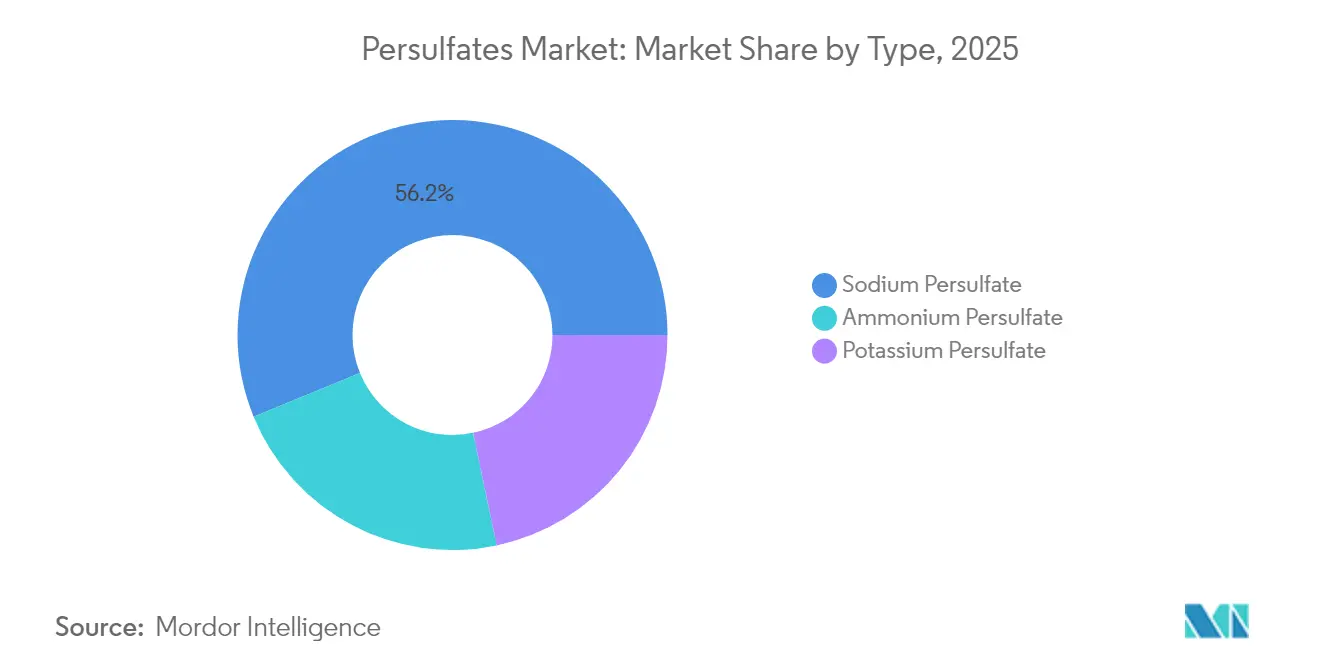

- By type, sodium persulfate led with a 56.20% persulfates market share in 2025, while ammonium persulfate is projected to expand at a 3.65% CAGR through 2031.

- By application, polymer initiators accounted for 39.10% of the persulfates market size in 2025, while electronic etching and other niche uses are advancing at a 3.78% CAGR to 2031.

- By end-user industry, polymer accounted for 28.70% of the persulfates market size in 2025, while electronics end-user industry is advancing at a 3.92% CAGR to 2031.

- By geography, Asia-Pacific commanded 50.60% of the global persulfates market in 2025, while the same region is poised to post the highest 3.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Persulfates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for High-Performance PCB Cleaning Agents in Advanced Node Semiconductor Fabs | +0.8% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Rising Consumption of Persulfate-Based Polymer Initiators in Water-Borne Acrylics | +0.6% | Global, with concentration in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Strong Growth of Pulp, Paper and Textile Bleaching Operations in Developing Countries | +0.5% | Asia-Pacific developing markets, emerging Africa | Medium term (2-4 years) |

| Demand Uptick from Enhanced Oil Recovery (EOR) Pilots in Shale Plays | +0.4% | North America core, expanding to Middle East | Long term (≥ 4 years) |

| Shift Toward On-Site Persulfate Generation Modules at Industrial Wastewater Plants | +0.3% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for High-Performance PCB Cleaning Agents in Advanced Node Semiconductor Fabs

Sub-5 nm logic and 3-D memory nodes require ultra-pure persulfate solutions that lift nanoscale polymer residues without trench damage. Fab operators in Taiwan and South Korea specify sodium persulfate grades with metal ions below 0.1 ppm to meet yield targets. A 6.3% rebound in global PCB output during 2024 improved order visibility for persulfate suppliers, while national AI and chip-sovereignty programs in the United States, Japan, and Europe are regionalizing demand. Investments in single-wafer wet benches now bundle persulfate feed systems, embedding the chemical in capital equipment contracts and dampening cyclical swings. Suppliers offering analytical support and closed-loop recycling services capture stickier revenue streams as fabs strive for zero-liquid-discharge goals.

Rising Consumption of Persulfate-Based Polymer Initiators in Water-Borne Acrylics

Environmental directives that phase down VOCs are accelerating the shift toward water-borne coatings, where persulfates deliver tight molecular-weight control at neutral pH. Ammonium persulfate enables low-residual monomer profiles in concrete admixtures and architectural paints, improving labor safety and indoor air quality. Global acrylic acid capacity is forecast to grow from 8.16 million tons in 2025 to 10.41 million tons in 2030, underpinning large-volume initiator needs. Asian mega-plants in China and Thailand are installing distributed control systems with real-time redox monitoring, cementing persulfate usage over legacy organic peroxides. Paint producers in Europe are hedging supply risk via dual-sourcing agreements that prefer integrated persulfate manufacturers who also supply monomer purification aids.

Strong Growth of Pulp, Paper and Textile Bleaching Operations in Developing Countries

Textile centers in Vietnam, Bangladesh, and Indonesia are retrofitting continuous-bleach lines to replace chlorine with persulfate solutions that cut wastewater salt load by 40%. Dissolving-grade pulp makers adopting closed alkali recovery loops prefer persulfates for precise lignin removal, enhancing fiber brightness without high COD effluent spikes. International Paper’s 2024 Georgetown mill shutdown tightened North American sulfite pulp supply, pushing specialty bleachers to source Asian volumes and raising import opportunities for persulfate producers[1]ResourceWise Pulp & Paper, “North American Mill Closures Reshape Bleaching Chemical Demand,” ResourceWise, resourcewise.com. African cellulose-fiber projects supported by the African Development Bank stipulate green bleaching chemistries, reinforcing long-term regional demand. Niche apparel brands now include “chlorine-free bleaching” on sustainability scorecards, pulling persulfates deeper into fashion supply chains.

Demand Uptick from Enhanced Oil Recovery (EOR) Pilots in Shale Plays

EOR pilots in the Eagle Ford, Bakken, and Oman’s Block 6 report 20–30% incremental recovery when persulfate-activated surfactant floods are combined with cyclic gas injection. Laboratory studies show imbibition recovery climbing to 29.03% with mixed-charge surfactants and sodium persulfate versus 9.84% for brine alone [MDPI.COM]. Monophasic persulfate packages remain stable above 120 °C, outperforming peroxide systems that decompose rapidly under reservoir brine. State-level tax credits for incremental oil have trimmed project paybacks to under three years, encouraging independent operators to scale field trials. Service companies are forming joint ventures with persulfate suppliers to bundle downhole tools, chemicals, and monitoring services under performance-based contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Bottlenecks for Key Raw Material Hydrogen Peroxide | -0.4% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Safety and Handling Concerns Driving Stricter Warehousing Codes | -0.3% | North America and Europe core, expanding globally | Medium term (2-4 years) |

| Regulatory Scrutiny on Sulphate Discharge | -0.2% | Global, with stringent enforcement in Europe and North America | Long term (≥ 4 year |

| Source: Mordor Intelligence | |||

Supply-Chain Bottlenecks for Key Raw Material Hydrogen Peroxide

Hydrogen peroxide accounts for up to 60% of persulfate production cost, and four multinationals control more than 70% of global capacity. Outages in East Asian peroxide plants during 2024 lifted spot prices by 22%, squeezing persulfate margins. Electrolytic peroxide projects promise 80% energy efficiency yet require multi-year capital outlays. Semiconductor-grade peroxide shortages ripple through high-purity persulfate supply, hiking lead times from four weeks to eight. Battery-grade sulfuric acid scarcity compounds the problem, as converters prioritize cathode materials over oxidizer markets, forcing persulfate makers to implement force-majeure clauses.

Safety and Handling Concerns Driving Stricter Warehousing Codes

Persulfates are class-5.1 oxidizers, subject to temperature-controlled storage and segregation from organics. New NFPA 400 updates mandate greater aisle spacing and remote-monitored sprinklers, elevating warehouse retro-fit expenses. In the European Union, Seveso III thresholds for persulfates trigger additional reporting once stock exceeds 50 tons, discouraging small distributors. OSHA guidance on dust inhalation risks in cosmetic formulations has pushed hair-bleach brands to switch from powder to cream bases, marginally diluting persulfate content but adding emulsifier cost. Training, containment, and emergency-response spending add roughly USD 0.05 per kilogram to downstream users, nudging some toward on-site generation alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sodium Persulfate Dominance Faces Specialty Growth

Sodium persulfate controlled the largest slice of the persulfates market size, equating to 56.20% in 2025. Its cost-to-performance ratio aligns with high-volume PCB etching, polymer initiation, and industrial cleaning duties. Ammonium persulfate, although holding a smaller base, leads type-level growth at a 3.65% CAGR through 2031 thanks to hair-bleach, EOR, and emulsion-polymer niches where low pH decomposition is beneficial. Demand for potassium persulfate stays niche, driven by food-contact films and electrolyte-sensitive processes requiring minimal sodium carryover. Rising tailings-pond remediation and lithium-battery recycling lines further diversify the persulfates market, adding specialty blends that achieve higher margins than bulk grades. Suppliers spotlight trace-metal control and tailored particle size to justify premiums and discourage commoditization.

By Application: Polymer Initiators Lead Amid Electronic Etching Surge

Polymer initiators captured 39.10% of the total persulfates market share in 2025. Construction and packaging sectors favor water-borne acrylics and vinyl acetates initiated with persulfates to meet tightening emissions rules. Electronic etching, soil remediation, and other specialty uses are climbing fastest, advancing at a 3.78% CAGR to 2031 as semiconductor complexity and environmental mandates intensify. Enhanced oil recovery maintains niche but profitable uptake, especially where high-temperature reservoirs constrain alternative chemistries. PFAS destruction reactors, adopted by airports and military bases, represent an emerging demand pocket that cushions cyclicality. As on-site generation gains traction, service-based revenue models linked to total oxidant demand strengthen supplier lock-in.

By End-User Industry: Electronics Growth Outpaces Polymer Stability

The polymer industry remained the top consumer, taking 28.70% of 2025 demand through steady coating, adhesive, and composite output. Electronics is the fastest riser with a 3.92% CAGR, propelled by AI accelerators, advanced packaging, and national chip-sovereignty programs that intensify high-purity persulfate needs. Pulp, paper, and textiles follow, adopting chlorine-free bleaching to satisfy eco-label criteria. Water treatment utilities deploy persulfates to oxidize refractory organics and destroy PFAS, a trend reinforced by tighter drinking-water standards. Oil and gas operators employ persulfates for reservoir stimulation and produced-water polishing, although capital discipline tempers volumes. Soil-remediation contractors leverage in-situ chemical oxidation for brownfield redevelopment, extending the persulfates market beyond traditional manufacturing corridors.

Geography Analysis

Asia-Pacific’s persulfates market dominance draws on robust semiconductor fabs, rising polymer capacity, and expanding textile bleaching. Chinese demand spans commodity and specialty grades, though anti-dumping reviews may redirect export flows. Taiwanese and South Korean fabs consume ultra-clean persulfate for sub-5 nm processes, while Southeast Asian nations cultivate new chemical hubs to capture supply-chain diversification. Rapid urbanization increases local water-treatment investment, adding another demand pillar.

North America leverages its unconventional oil and gas strength, with EOR pilots gradually scaling from laboratory validation to commercial zones. Semiconductor reshoring plus state incentives undergird new demand for electronic-grade persulfates, lessening historical reliance on Asia-Pacific supply. Environmental regulations steadily promote persulfate oxidation in groundwater remediation and industrial wastewater treatment, securing baseline offtake independent of macro cycles.

Europe’s market growth is slower yet steadier, animated by strict discharge norms and the circular-economy agenda. Battery recycling plants in Germany, France, and Sweden apply persulfates to leach lithium and cobalt, aligning with EU critical-materials policy. Soil remediation in Brownfield redevelopment programs adds predictable volumes, and consolidation within the regional chemical industry favors large persulfate producers able to offer technical audits, on-site pilot work, and closed-loop supply agreements.

Competitive Landscape

The persulfates market shows moderate concentration, with Evonik, LANXESS, and Adeka Corporation leading revenue. Vertical integration into hydrogen peroxide, captive sulfuric acid, and onsite energy lowers variable cost and shields margins during feedstock spikes. LANXESS expanded Oxone monopersulfate capacity by 50% at its Memphis plant, targeting pool, hygiene, and electronics segments[2]Cleanroom Technology Staff, “LANXESS Boosts Oxone Capacity by 50% at Memphis Site,” Cleanroom Technology, cleanroom-technology.com . Evonik markets the KLOZUR line for soil-remediation, bundling field-support services and kinetic modeling software that make switching costs high for contractors. Adeka focuses on semiconductor wet-clean agents, collaborating with equipment makers to embed dosage modules within spin-rinse tools.

Second-tier players in China and India compete on price but face regional warehousing code updates and REACH audits that may re-rank supply hierarchies. Joint ventures between Western formulators and Asian producers aim to combine low-cost manufacturing with route-to-market expertise in North America and Europe. Start-ups developing on-site generation and membrane activation solutions partner with established suppliers for electrolyte blends, offering a technology hedge should distributed production outpace centralized plants.

Strategic moves lean toward application diversification, where persulfate makers align with lithium-battery recyclers, PFAS treatment integrators, and shale service firms. Intellectual-property filings focus on stabilized persulfate slurries, binary activator systems, and metal-ion scavengers, raising the barrier for commodity entrants. Customer loyalty increasingly hinges on quality analytics, short lead times, and regulatory support, placing a premium on producers that maintain ISO 9001 labs near major consumption hubs.

Persulfates Industry Leaders

United Initiators

MITSUBISHI GAS CHEMICAL COMPANY, INC

Evonik Industries AG

LANXESS

Adeka Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Fujian ZhanHua Chemical Co., Ltd is implementing a third-phase expansion project for its ammonium persulfate production. The company aims to achieve an annual production capacity of 80,000 tons by 2025, strengthening its position in the global persulfate market.

- September 2022: Calibre Chemicals acquired RheinPerChemie, a manufacturer of ammonium and sodium persulfates. These chemicals serve as initiators in polymerization and other applications. Through this acquisition, Calibre became a global supplier offering a complete range of persulfates, including ammonium, sodium, and potassium variants.

Global Persulfates Market Report Scope

Persulfate is a colorless crystalline salt of persulfuric acid. It is also known as peroxysulfate or peroxodisulfate. It contains anions SO² or S O² . The persulfates market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into sodium persulfate, potassium persulfate, and ammonium persulfate. By application, the market is segmented into polymer initiator, enhanced oil recovery, oxidation, bleaching, and sizing agent, and other applications. By end-user industry, the market is segmented into polymers, pulp, paper, and textile, electronics, cosmetics and personal care, oil and gas, water treatment, soil remediation, and other end-user industries. The report also covers the market sizes and forecasts for the persulfates market in 15 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Sodium Persulfate |

| Potassium Persulfate |

| Ammonium Persulfate |

| Polymer Initiator |

| Enhanced Oil Recovery |

| Oxidation, Bleaching and Sizing Agent |

| Other Applications (Electronic etching, etc.) |

| Polymer |

| Pulp, Paper and Textile |

| Electronics |

| Cosmetics and Personal Care |

| Oil and Gas |

| Water Treatment |

| Soil Remediation |

| Other End-user Industries (Mining, Ashesives, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Sodium Persulfate | |

| Potassium Persulfate | ||

| Ammonium Persulfate | ||

| By Application | Polymer Initiator | |

| Enhanced Oil Recovery | ||

| Oxidation, Bleaching and Sizing Agent | ||

| Other Applications (Electronic etching, etc.) | ||

| By End-user Industry | Polymer | |

| Pulp, Paper and Textile | ||

| Electronics | ||

| Cosmetics and Personal Care | ||

| Oil and Gas | ||

| Water Treatment | ||

| Soil Remediation | ||

| Other End-user Industries (Mining, Ashesives, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the persulfates market by 2031?

The persulfates market size is expected to reach USD 1.04 billion by 2031, reflecting a 2.98% CAGR over 2026-2031.

Which region will add the most incremental demand for persulfates?

Asia-Pacific will contribute the largest absolute growth, maintaining a 3.84% regional CAGR as semiconductor and polymer capacities expand.

Why are persulfates preferred over organic peroxides in water-borne acrylics?

Persulfates enable precise polymerization control at neutral pH, cut residual monomers, and comply better with low-VOC regulations.

How do supply constraints in hydrogen peroxide affect persulfate pricing?

Hydrogen peroxide makes up to 60% of production cost, so supply tightness quickly inflates persulfate prices and stretches lead times.

What role do persulfates play in PFAS destruction?

Advanced oxidation reactors use persulfate radicals to break the strong carbon-fluorine bonds in PFAS, allowing compliant discharge of treated water.

Page last updated on: