Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.10 Billion |

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

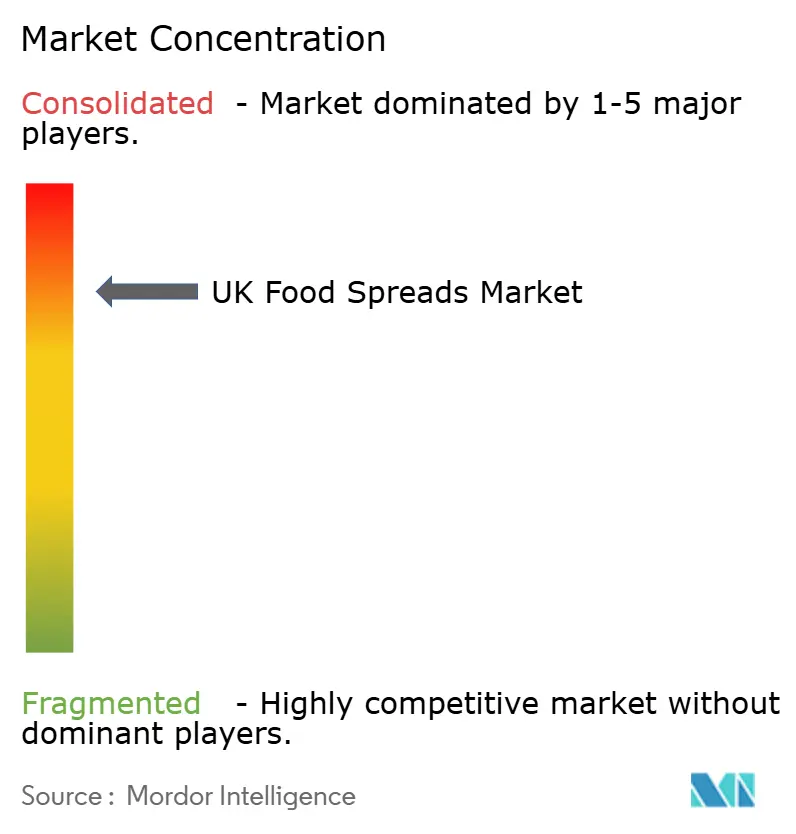

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Food Spreads Market Analysis by Mordor Intelligence

The United Kingdom Food Spreads Market size was valued at USD 1.10 billion in 2025 and estimated to grow from USD 1.15 billion in 2026 to reach USD 1.41 billion by 2031, at a CAGR of 4.28% during the forecast period (2026-2031). This growth trajectory reflects the market's resilience despite economic pressures, as consumers increasingly view food spreads as affordable indulgences that offer versatility across multiple consumption occasions. The market's expansion is being propelled by the dual forces of premiumization and health consciousness, with consumers willing to pay more for products that deliver on taste, quality, and nutritional benefits. The growing breakfast culture in the UK, combined with continuous innovation in flavors and premium ingredients, is reshaping the food spreads landscape. Manufacturers are responding to consumer demands by introducing new flavor variants and incorporating high-quality ingredients, while the increasing popularity of breakfast occasions provides multiple opportunities for spread consumption throughout the day. As the market continues to evolve, the combination of innovative product development and changing consumer preferences positions for sustained growth and diversification in the coming years.

Key Report Takeaways

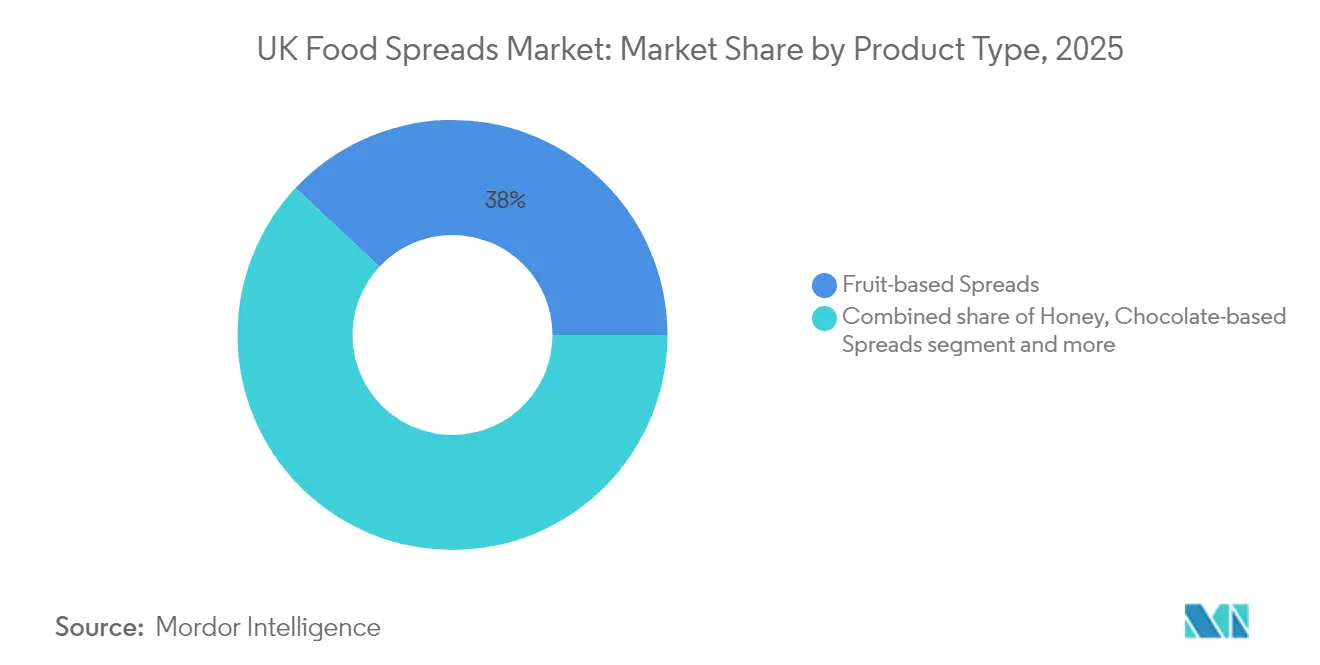

- By product type, fruit-based spreads led with 38.03% of the UK food spreads market share in 2025; nut and seed variants are projected to grow at a 6.55% CAGR through 2031.

- By nature, the conventional segment accounted for 71.78% of the UK food spreads market size in 2025, whereas organic spreads are expected to register a 9.56% CAGR between 2026-2031.

- By packaging type, jars dominated with a 41.76% revenue share in 2025, while sachets and pouches are set to expand at a 6.98% CAGR to 2031.

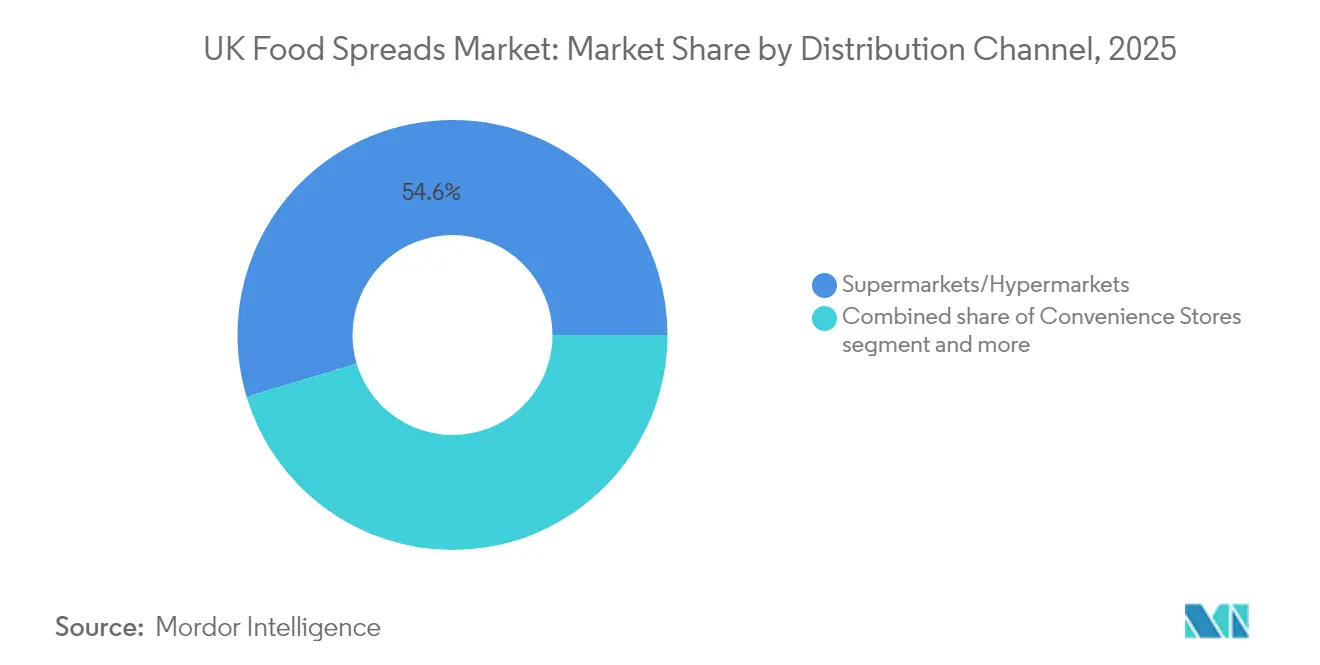

- By distribution channel, supermarkets/hypermarkets held a 54.63% share of the UK food spreads market in 2025; online retail is anticipated to climb at a 9.52% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Food Spreads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing popularity of breakfast culture increases spread consumption | +1.2% | National, with stronger impact in urban areas | Medium term (2-4 years) |

| Busy lifestyles increase the preference for convenient and versatile food options | +0.8% | National, particularly in metropolitan regions | Short term (≤ 2 years) |

| Innovation in flavors and premium ingredients attracts new consumers | +1.0% | National, with early adoption in London and Southeast | Medium term (2-4 years) |

| Expansion of vegan and organic product lines drives market growth | +0.7% | National, with concentration in urban centers | Long term (≥ 4 years) |

| Convenience packaging formats encourage on-the-go usage | +0.5% | National, stronger in urban areas | Medium term (2-4 years) |

| Strong retail infrastructure supports wide product availability | +0.4% | National, with rural areas catching up | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing popularity of breakfast culture increases spread consumption

The resurgence of breakfast as a critical meal is fundamentally reshaping the UK food landscape. This trend extends beyond traditional toast applications, as consumers incorporate spreads into breakfast bowls, smoothies, and baked goods. This perspective is particularly evident among younger demographics who consider morning nutrition fundamental to their wellness routines, creating opportunities for spreads with specific functional benefits such as protein enhancement or energy provision. The breakfast trend's sustainability is reinforced by home-based consumption patterns established during pandemic lockdowns, which have continued even as work routines normalize. Manufacturers are responding to this shift by developing innovative spread formulations that cater to specific dietary preferences, including plant-based and reduced-sugar options. Additionally, the growing emphasis on breakfast has led to increased retail shelf space dedicated to morning-focused spreads, reflecting the market's adaptation to evolving consumer preferences.

Busy lifestyles increase the preference for convenient and versatile food options

The increasing employment rates and busy lifestyles are reshaping consumer food preferences, particularly in favor of convenient and versatile options. This time compression in modern households has elevated the strategic importance of versatile food products, particularly food spreads, which serve multiple culinary functions. The market is adapting to these changing consumer needs by expanding beyond traditional bread applications, with food spreads gaining popularity as cooking ingredients, dessert components, and snack complements. The food spreads market has evolved to meet consumer demands through innovative product formulations that offer enhanced functionality and convenience, including squeezable packaging and portion-controlled formats. According to UK Labour Market Statistics, the employment rate for people aged 16-64 reached 75.1% in February to April 2025, with 34.01 million people aged 16 and above in employment, marking an increase of approximately 667,000 over the previous year [1]Source: UK Parliament Library, “Labour Market Statistics,” parliament.uk . Additionally, the integration of food spreads into meal preparation has become more prevalent, with consumers utilizing these products as quick flavor enhancers and nutritional supplements in various recipes.

Innovation in flavors and premium ingredients attracts new consumers

Innovation in flavors is driving the market's premiumization trend, creating a two-tier market where value offerings coexist with premium variants. Consumers demonstrate increased willingness to pay more for specialty products, particularly heritage and flavored spreads that offer distinctive flavor profiles, ethical sourcing credentials, or nutritional advantages. The premium segment has witnessed significant growth due to consumers' evolving taste preferences and increasing focus on high-quality ingredients. This shift has encouraged manufacturers to invest in research and development to create unique flavor combinations and artisanal production methods. In March 2025, Hilltop Honey expanded its product portfolio by introducing trendy spreads, including sweet and salty, cocoa honey, chai spiced, and whipped and pink flavors. This continuous flavor innovation and consumer preference for premium offerings indicates sustained growth potential.

Expansion of vegan and organic product lines drives market growth

The plant-based revolution is fundamentally altering the UK food spreads landscape, as consumer preferences shift toward vegan and organic food products. This transition from niche to mainstream has prompted manufacturers to expand their product portfolios with new plant-based alternatives across various food categories. The growing demand for plant-based spreads is driven by health-conscious consumers seeking alternatives to traditional dairy-based products, as well as increasing awareness of environmental sustainability. The British consumers are willing to pay premium prices for high-quality plant-based spreads that match the taste and texture of conventional options. The expansion of plant-based offerings has also led to increased competition among manufacturers, resulting in improved product formulations and innovative packaging solutions. Arla Foods launched a plant-based Lurpak spread in the UK and Denmark in August 2024, offering consumers a dairy-free alternative within the Lurpak brand portfolio. This trend indicates a significant transformation in the food spreads market, with plant-based options becoming increasingly integral to product development strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High competition from private-label brands pressures pricing | -0.6% | National, particularly in discount retail channels | Medium term (2-4 years) |

| Health concerns over sugar and fat content reduce traditional spread usage | -0.8% | National, with stronger impact in urban and affluent areas | Long term (≥ 4 years) |

| Increasing allergy awareness limits nut-based spread consumption | -0.3% | National | Medium term (2-4 years) |

| Regulatory constraints on labeling and health claims add complexity | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High competition from private-label brands pressures pricing

Economic pressures are accelerating the shift toward private label products in food spreads, creating margin compression for branded manufacturers who must demonstrate distinctive value propositions to justify premium pricing. This trend is particularly pronounced in staple segments like fruit spreads, where product differentiation is challenging and price sensitivity is high. The private label threat is intensifying as retailers enhance their own-brand offerings with premium cues, clean labels, and sustainability credentials that previously distinguished national brands. The regulatory environment is further disrupting the market, driving reformulation efforts across both branded and private label segments as manufacturers recalibrate their value propositions. These market dynamics pose significant challenges for manufacturers, potentially limiting their ability to maintain profit margins and invest in product innovation. The competitive landscape has become increasingly complex as manufacturers face pressure to innovate while simultaneously managing cost structures and maintaining market share. Additionally, changing consumer preferences toward healthier and more sustainable options have compelled both national brands and private labels to adapt their product portfolios, further straining operational resources and development capabilities.

Health concerns over sugar and fat content reduce traditional spread usage

The food industry faces significant challenges due to increasing consumer scrutiny of sugar and fat content in products. According to the British Nutrition Foundation (May 2024), ultra-processed foods (UPF) constitute 51-68% of caloric intake in UK diets and are increasingly linked to obesity, type 2 diabetes, and cardiovascular diseases [2]Source: British Nutrition Foundation, “Ultra-Processed Foods Position Statement,” nutrition.org.uk . This health awareness is reflected in consumer behavior, as a 2024 Food Standards Agency survey indicates that 54% of consumers are more likely to purchase reduced sugar products [3]Source: Food Standards Agency, “Consumers and Sugar Intake,” food.gov.uk. Consumers regularly examine food labels for nutritional information, particularly calories, fat, and sugar content. These trends are compelling manufacturers to carefully balance product indulgence with health considerations in their formulations. However, reformulating products while maintaining taste, texture, and consumer acceptance remains a significant challenge for manufacturers. The complexity of this challenge is further heightened by varying regional taste preferences and regulatory requirements across different markets. Additionally, manufacturers must consider the cost implications of alternative ingredients and processing methods while ensuring their products remain commercially viable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Health-Conscious Shifts Redefine Preferences

Fruit-based spreads hold a dominant 38.03% market share in 2025, supported by traditional breakfast consumption patterns and their natural ingredient perception. However, the segment faces volume decline as consumers become increasingly conscious of sugar content in traditional jams. This trend is particularly evident in developed markets where health-conscious consumers are actively seeking alternatives with reduced sugar content. Manufacturers like B Healthy Limited, Locco are responding by expanding their product portfolio in low-sugar and sugar-free variants, incorporating natural sweeteners and fruit concentrates.

Nut and seed-based spreads are experiencing rapid growth, with a projected CAGR of 6.55% from 2026-2031. This growth stems from their high protein content and alignment with plant-based diets. Products featuring natural, minimally processed ingredients have gained substantial market acceptance. The increasing adoption of these spreads in snacking applications has further accelerated their market penetration. The category has witnessed significant innovation in flavor combinations and ingredient profiles, including the introduction of specialty nuts and superseeds. The versatility of these spreads, from breakfast applications to recipe ingredients, has contributed to their expanding consumer base across different demographic segments.

By Nature: Organic Growth Outpaces Conventional Segment

The conventional segment holds a 71.78% market share in 2025, driven by established brands, extensive distribution networks, and competitive pricing. The segment maintains its dominant position by delivering consistent quality and familiar taste profiles that align with traditional consumer preferences. The conventional segment's market leadership is further reinforced by its strong brand recognition and consumer trust built over decades. These products benefit from economies of scale in production and established relationships with retailers, enabling manufacturers to maintain competitive price points. Additionally, conventional spreads continue to dominate household penetration rates due to their widespread availability across various retail channels and their role as pantry staples.

The organic food spreads segment is projected to grow at a CAGR of 9.56% during 2026-2031, exceeding the overall market growth rate. This expansion stems from increasing consumer preference for natural, clean-label products and environmentally sustainable options. The growth trajectory is supported by rising health consciousness and increasing disposable income among consumers. The segment's growth is further accelerated by expanding retail shelf space dedicated to organic products and increasing investment in organic farming practices by manufacturers. Moreover, the introduction of innovative organic spread variants and flavors, coupled with enhanced marketing efforts highlighting their health benefits, continues to attract new consumer segments.

By Distribution Channel: Online Growth Disrupts Traditional Retail

Supermarkets and hypermarkets dominate sweet spreads distribution with a 54.63% market share in 2025. These retail formats maintain their strong position through extensive store networks and comprehensive product displays. The physical store environment enables consumers to inspect products, review nutritional content, and make spontaneous purchase decisions. Regular promotional activities and strategic shelf placement in these stores enhance product visibility and drive sales. Additionally, the ability to cross-merchandise food spreads with complementary products like bread and baked goods strengthens their retail performance.

Online retail is experiencing the highest growth among distribution channels, with an expected CAGR of 9.52% during 2026-2031. The digital channel is transforming purchasing patterns by offering convenience, broader product selection, and direct-to-consumer distribution options that circumvent traditional retail limitations. E-commerce platforms provide detailed product information, customer reviews, and competitive pricing comparisons that aid consumer decision-making. The integration of subscription services and automated reordering systems further enhances the appeal of online food spread purchases.

By Packaging Type: Convenience Drives Format Innovation

Jars continue to dominate the market with a 41.76% share in 2025, leveraging their established consumer trust, shelf stability, and premium visual appeal. While jars maintain their strong position, they face increasing competition from sachets and pouches, which are experiencing rapid growth at a 6.98% CAGR (2026-2031). This growth is primarily attributed to changing consumer preferences for on-the-go consumption and portion control, supported by advancements in recyclable materials. The widespread acceptance of jars is further reinforced by their ability to preserve product quality and extend shelf life effectively.

The packaging landscape is diversifying with various formats catering to specific consumer needs. Tubs offer a balanced solution with resealable features that maintain product freshness, while cups, cans, and tetra packs serve distinct usage occasions. The industry is also advancing through the integration of intelligent systems for food quality monitoring, which aims to extend shelf life and minimize waste, reflecting the sector's focus on innovation and sustainability. Furthermore, there is a growing demand for packaging solutions that incorporate smart indicators to monitor temperature fluctuations and product freshness.

Geography Analysis

The UK food spreads market demonstrates significant regional variations in consumer preferences and purchasing behaviors. Urban centers, particularly London and the Southeast, serve as early adoption hubs for premium and innovative products. Consumers in these metropolitan areas show higher acceptance of natural nut butters and plant-based alternatives, driven by increased health consciousness and environmental awareness. Northern regions exhibit stronger preferences for traditional spreads, including jams and marmalades, reflecting established consumption patterns. Coastal regions show distinct seasonal variations in spread consumption, with higher sales of lighter options during summer months.

The regulatory landscape adds complexity to regional market dynamics, as devolved administrations implement distinct health policies. England has established restrictions on HFSS (High in Fat, Sugar, and Salt) product promotions in prominent store locations, while Wales is introducing similar measures through the Food Regulations 2025. Scotland's anticipated comparable legislation creates a multi-layered regulatory environment that requires manufacturers to adapt their strategies across national boundaries. These variations in regulatory frameworks have prompted manufacturers to develop region-specific product formulations and marketing approaches. Local authorities also maintain different interpretations of national guidelines, necessitating careful consideration of compliance requirements in each area.

The evolution of retail infrastructure and changing consumer habits further influence the geographic market landscape. The rise in home working has increased domestic food consumption, expanding food spreads consumption beyond traditional breakfast occasions. Additionally, improved digital connectivity has enhanced online retail penetration in rural areas, providing better access to specialty products. These combined factors necessitate targeted approaches to product development, pricing, and promotion across different regions. The emergence of specialized food delivery services has created new distribution channels for premium spreads in both urban and suburban areas.

Competitive Landscape

The UK food spreads market exhibits a highly consolidated structure, with multinational corporations maintaining dominant positions through their economies of scale, established distribution networks, and strong brand recognition. These large companies benefit from extensive manufacturing capabilities and efficient supply chains. However, the market dynamics are evolving as smaller, specialized producers enter the space, introducing innovative products and challenging traditional players. The market structure reflects a distinct segmentation between mass-market manufacturers focusing on cost-effectiveness and widespread availability, and premium producers targeting specific consumer segments with unique product formulations, organic ingredients, and sustainability certifications.

Major corporations, including Unilever PLC, Ferrero International SA, The Hain Celestial Group, Flora Food Company, and The J. M. Smucker Company, primarily shape the competitive landscape. These established companies maintain significant market share through extensive product portfolios and strong retail presence. In response to changing consumer preferences, these companies are actively innovating their product offerings. A notable example is Ferrero's strategic initiative to introduce a plant-based version of its popular Nutella spread, launched in September 2024, demonstrating the industry's adaptation to evolving consumer demands.

The market presents substantial growth potential in addressing the intersection of indulgence and health consciousness. Consumer demand is increasingly focused on products that deliver traditional taste satisfaction while incorporating healthier ingredients and improved nutritional content. This trend creates opportunities for manufacturers to develop innovative formulations that maintain the desired taste profiles and texture while reducing sugar content, incorporating natural ingredients, and enhancing nutritional value. The food spreads category particularly demonstrates strong potential for products that successfully balance indulgence with health-conscious attributes, responding to growing consumer awareness of nutritional considerations.

UK Food Spreads Industry Leaders

Unilever Plc

Ferrero International SA

The Hain Celestial Group

The J. M. Smucker Company

Flora Food Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Pip & Nut launched a Chocolate Hazelnut Spread with significantly less sugar, responding to consumer demand for healthier indulgence options. This product innovation exemplifies the market trend toward improved nutritional profiles while maintaining sensory appeal

- May 2025: Sweet Freedom has introduced Choc Pot Hazelnot, a plant-based and nut-free alternative to traditional chocolate hazelnut spreads. The product is manufactured in a nut-free facility, providing a safe option for consumers with nut allergies while maintaining the characteristic chocolate-hazelnut taste profile.

- October 2024: Lactalis expanded its Seriously Spreadable product line by introducing a black pepper cheese spread variant. The product comes in fully recyclable packaging to meet consumer demand for sustainable packaging solutions.

- May 2024: Kavli introduced whipped cheese spreads in the United Kingdom, featuring two variants: classic Cheddar and Cheddar & Chorizo. The product launch expands the company's presence in the cheese spread category.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom food spreads market as all factory-produced sweet spreads, honey, fruit preserves, chocolate-based, nut and seed-based, plus dairy or cheese spreads, sold through retail and food-service channels, valued at manufacturer gate and expressed in constant 2025 USD.

Scope exclusion: table butter, margarine, and savory yeast extracts are outside our scope.

Segmentation Overview

- By Product Type

- Honey

- Chocolate-based Spreads

- Fruit-based Spreads

- Nut and Seed-based Spreads

- Dairy and Cheese Spreads

- Other Product Types

- By Nature

- Conventional

- Organic

- By Packaging Type

- Jars

- Tubs

- Sachets/Pouches

- Others

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

Detailed Research Methodology and Data Validation

Primary Research

We interviewed category buyers at leading supermarket groups, brand managers at national and craft spread producers, ingredient brokers, and dieticians across England, Scotland, Wales, and Northern Ireland. These discussions confirmed prevailing pack sizes, emerging flavor formats, online price points, and the pace at which organic and plant-based variants penetrate shelves. Insights from these calls filled data gaps and shaped realistic scenario bounds.

Desk Research

Mordor analysts gathered foundational figures from tier-one public sources such as the Office for National Statistics household food expenditure tables, HMRC trade codes for honey and nut pastes, the Food & Drink Federation production bulletins, Soil Association organic sales audits, and peer-reviewed nutrition journals. Company filings, trade press like The Grocer, and product-launch intelligence from Mintel GNPD completed the landscape.

Paid repositories, D&B Hoovers for company revenues and Dow Jones Factiva for deal news, supplied additional granularity. The sources listed illustrate the range used; many more were reviewed to cross-check facts, reconcile units, and clarify definitions.

Market-Sizing & Forecasting

A top-down demand pool was built from household breakfast occasion frequency multiplied by average spread portion size and retail price, adjusted for food-service share and import leakage. Bottom-up supplier roll-ups and sampled ASP multiplied by volume checks fine-tuned totals. Key variables like disposable income per capita, obesity-related sugar reduction targets, organic shelf share, e-commerce penetration, and new SKU launch counts feed a multivariate regression and ARIMA overlay that projects values to 2030. Where artisanal producers lacked disclosure, volumes were inferred from craft-market audit ratios before being absorbed into overall totals.

Data Validation & Update Cycle

Outputs run through sequential variance checks, peer review, and senior analyst sign-off. Before publication, fresh trade data are screened to capture material events. Reports refresh annually, with interim mini-updates when pricing shocks or policy shifts occur.

Why Mordor's UK Food Spreads Baseline Is Trusted

Published estimates often diverge because firms apply different product baskets, channel mixes, and currency bases.

Our disciplined scope, yearly refresh, and dual-path modeling limit such drift for clients who need a stable decision anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.10 B | Mordor Intelligence (2025) | - |

| USD 1.50 B | Regional Consultancy A (2024) | Includes butter and margarine; uses retail receipts without producer price rebasing |

| USD 1.60 B | Trade Journal B (2024) | Adds industrial bulk volumes and applies straight-line CAGR without variable testing |

These contrasts show that Mordor's careful scope setting, variable-based forecasting, and update cadence deliver a balanced, transparent baseline clients can rely on.

Key Questions Answered in the Report

What is the current value of the UK food spreads market?

The UK food spreads market is valued at USD 1.15 billion in 2026.

Which product segment is growing fastest through 2031?

Nut and seed-based spreads are projected to post the highest CAGR at 6.55%, driven by protein content and plant-based appeal.

How fast is online retail expanding in this category?

The online channel is forecast to rise at a 9.52% CAGR from 2026-2031, the quickest among distribution formats.

Which packaging format is expected to see notable gains?

Sachets and pouches should advance at a 6.98% CAGR as consumers desire portion control and on-the-go convenience.

Why are private-label spreads gaining ground?

Retailers are upgrading own-label recipes and packaging while keeping prices low, enticing value-seeking shoppers.

Page last updated on: