Healthcare M2M Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

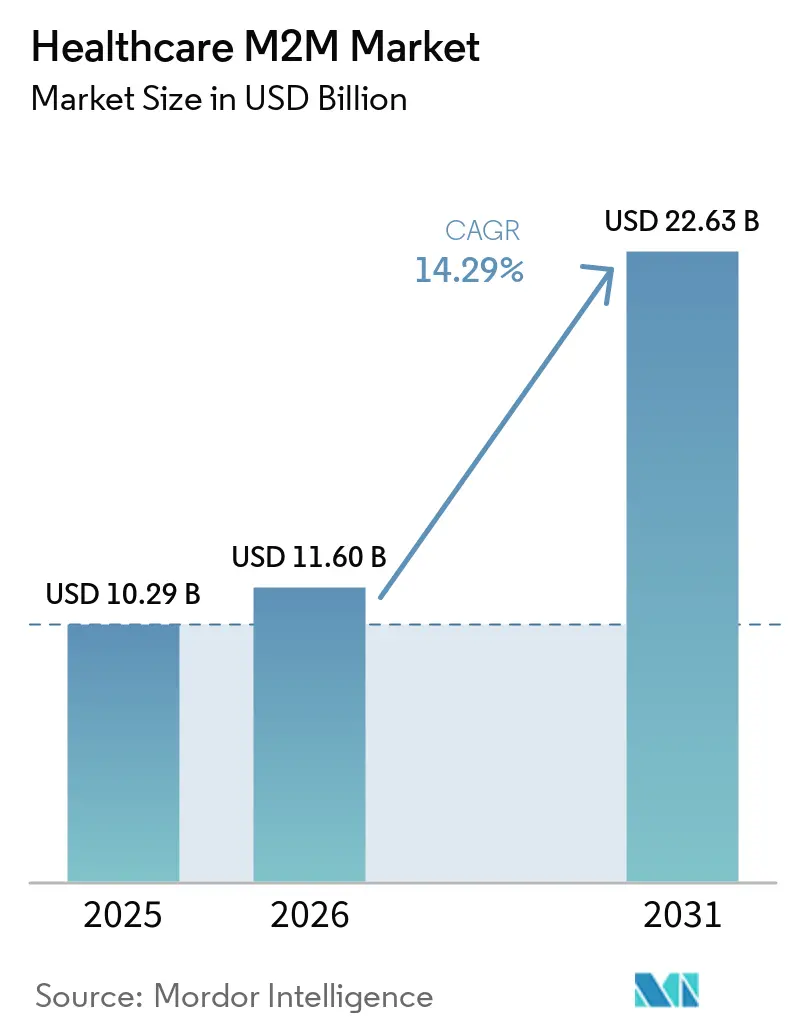

| Market Size (2026) | USD 11.60 Billion |

| Market Size (2031) | USD 22.63 Billion |

| Growth Rate (2026 - 2031) | 14.29% CAGR |

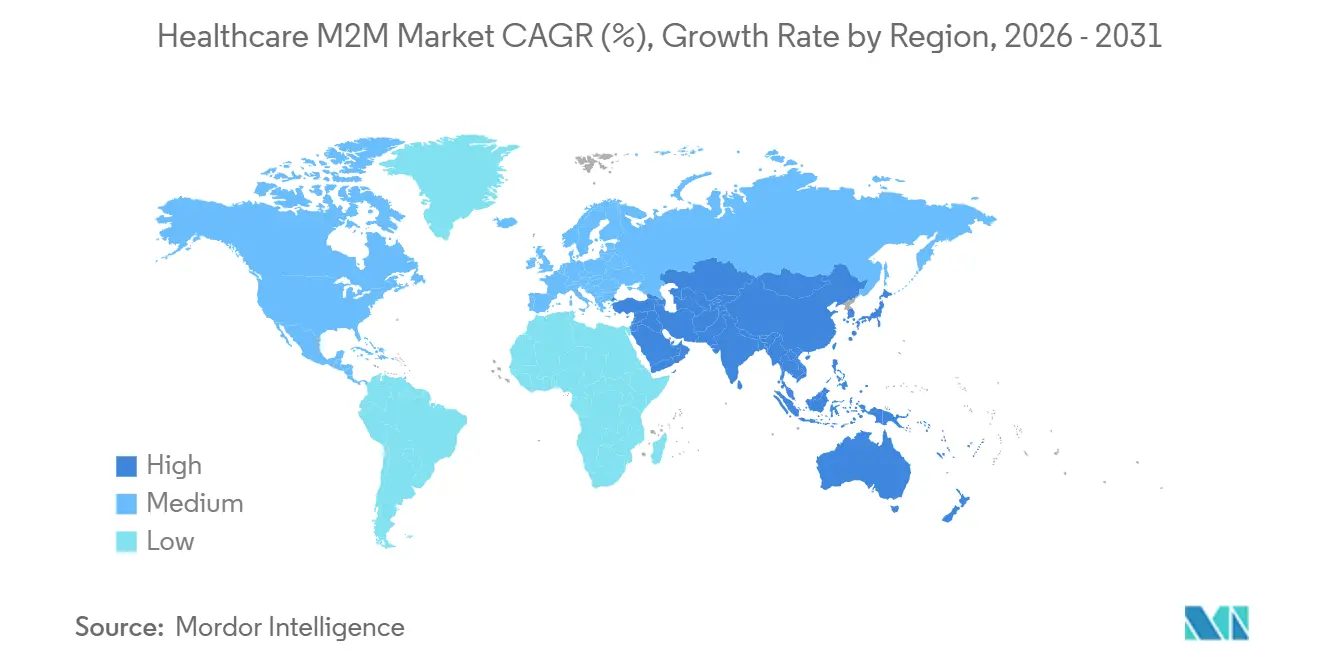

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

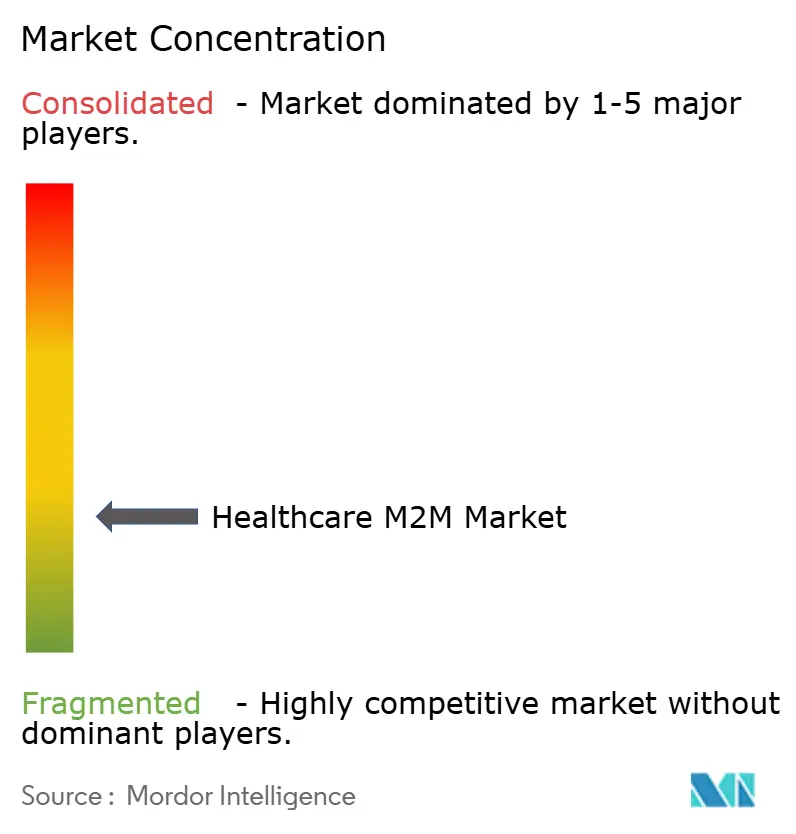

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare M2M Market Analysis by Mordor Intelligence

The Healthcare M2M Market size is expected to grow from USD 10.29 billion in 2025 to USD 11.60 billion in 2026 and is forecast to reach USD 22.63 billion by 2031 at 14.29% CAGR over 2026-2031.

Heightened reimbursement for Remote Patient Monitoring (RPM) and Remote Therapeutic Monitoring, the phase-out of 2G/3G networks, and hospital digitization programs are converting machine-to-machine connectivity from experimental pilots into mainstream clinical infrastructure. Insurers now pay monthly fees for device setup, data transmission, and clinical interpretation, while private 5G and edge platforms deliver millisecond-level latency for telemetry and surgical video. Device makers, carriers, and cloud providers are responding with eSIM profiles, secure-boot chipsets, and FHIR-native software layers that shrink onboarding cycles from months to weeks. Asian public health programs, notably India’s eSanjeevani and China’s rural tele-imaging network, demonstrate that scalable cellular backbones can bridge specialist shortages and chronic disease surveillance gaps.

Key Report Takeaways

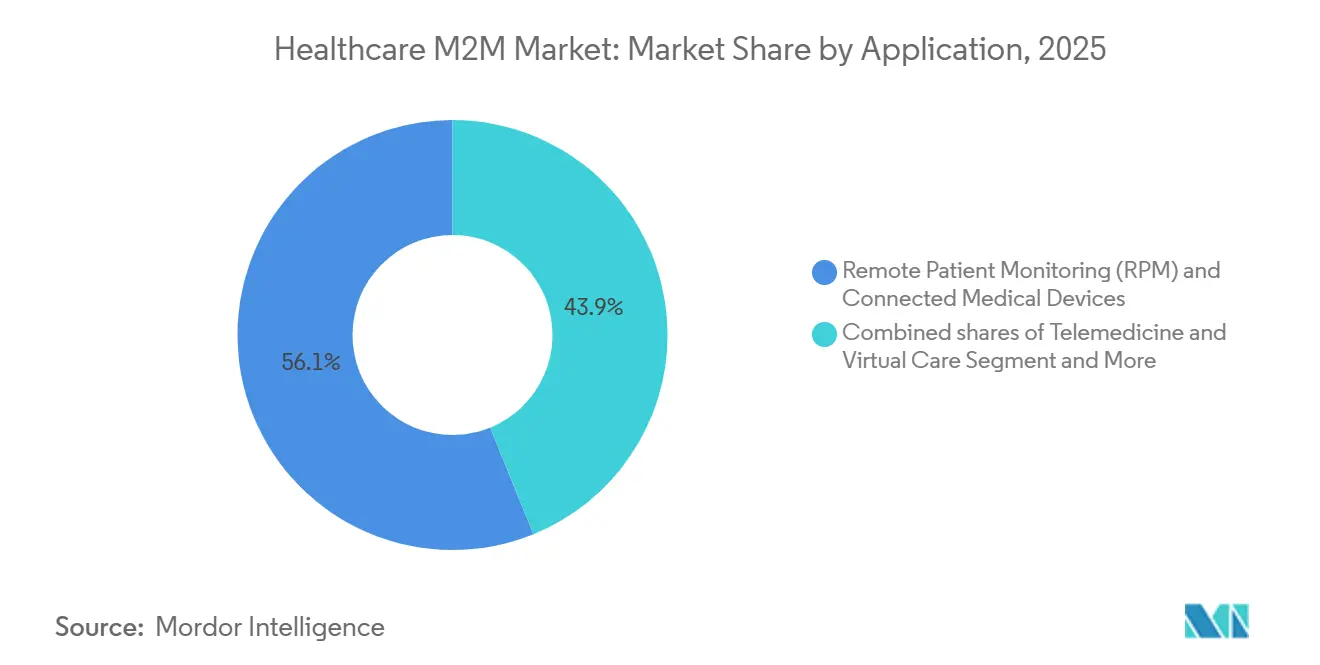

- By application, remote patient monitoring and connected medical devices led the Healthcare M2M market with 56.14% market share in 2025, and the telemedicine & virtual care segment is projected to advance at a 16.56% CAGR through 2031.

- By connectivity, cellular 4G/LTE/5G accounted for 37.91% of the Healthcare M2M market size in 2025, and Zigbee/Z‑Wave/Thread is forecast to expand at 15.31% CAGR to 2031.

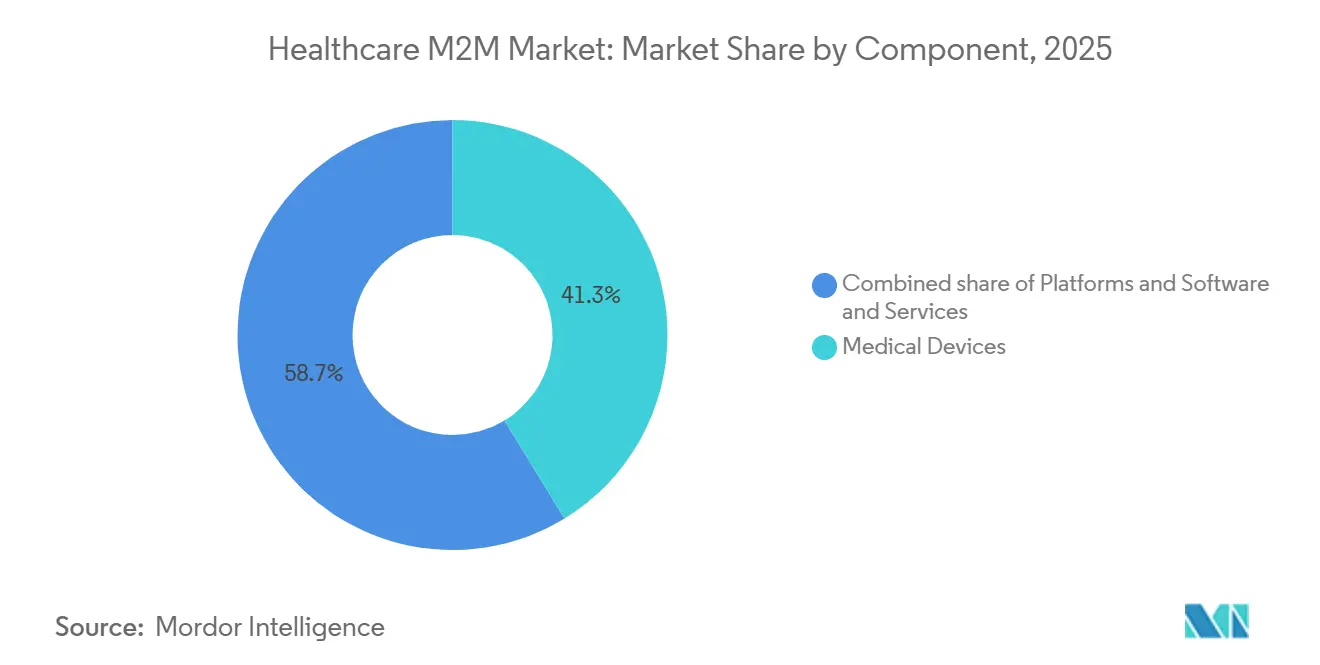

- By component, medical devices accounted for 41.29% of the Healthcare M2M market in 2025, while platforms & software posted the fastest CAGR of 16.24% through 2031.

- By end user, hospitals and clinics captured 48.90% Healthcare M2M market share in 2025; homecare patients registered the highest projected CAGR of 16.01% to 2031.

- By geography, North America retained 37.65% of global revenue in 2025, whereas Asia-Pacific is the fastest-growing geography with a 16.71% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare M2M Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement expansion for RPM/RTM and virtual care | +3.2% | North America, early EU adopters | Short term (≤ 2 years) |

| Rising chronic disease burden and aging at-home care needs | +2.8% | Global, pronounced in APAC | Long term (≥ 4 years) |

| Proliferation of connected devices, wearables, and cloud/AI analytics | +2.5% | Global, led by North America & APAC | Medium term (2-4 years) |

| Hospital digitization for operational efficiency | +2.1% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Private 5G and edge deployments enabling deterministic connectivity | +1.9% | North America, Nordic Europe, select APAC metros | Medium term (2-4 years) |

| Decentralized clinical trials using regulated eSource data | +1.8% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Expansion For RPM/RTM And Virtual Care

Permanent U.S. CMS billing codes 99453-99458, and 98975-98981 convert what were pandemic-era pilot projects into predictable monthly revenue for providers. Private U.S. insurers mirror these codes, while France reimburses Dexcom ONE+ for insulin-treated Type 2 diabetes, prompting other EU payers to re-evaluate wearable coverage. India pilots RPM reimbursement under Ayushman Bharat to target rural hypertension, and initial data suggest per-patient monitoring costs fall below USD 5 per month.

Such policies upstream device demand and accelerate platform roll-outs that aggregate data into EHRs through FHIR interfaces. The upshot is a near-term boost in North America and a pipeline of adoption across Asia-Pacific once reimbursement frameworks mature.

Rising Chronic Disease Burden And Aging At-Home Care Needs

Japan’s senior population hit 29.3% in 2024, and South Korea’s reached 19.2%, straining institutional care capacity. India counts 62 million diabetes patients, with non-communicable diseases causing 52% of annual deaths. China processed 68 million county-level remote imaging cases in 2025, demonstrating how 5G links rural clinics to specialists. Low-cost LTE-M modules with 10-year batteries are now standard in glucometers and fall detectors, enabling continuous surveillance without burdensome power constraints. Collectively, demographic and epidemiologic pressures will propel sustained Healthcare M2M market growth throughout the forecast horizon.

Proliferation Of Connected Devices, Wearables, And Cloud/AI Analytics

Abbott’s Libre Assist and Dexcom’s AI coaching illustrate the pivot from raw data to predictive interventions delivered in natural language. ResMed’s Smart Comfort CPAP self-tunes using 100 million nights of anonymized data, indicating a shift among device makers toward vertically integrated analytics stacks that capture software revenue. Quectel’s BG770A-GL combines LTE Cat-1 and GNSS, enabling fall detection and geofencing in a single SKU. These innovations shorten clinical response times and raise patient engagement, reinforcing the Healthcare M2M market’s value proposition.

Hospital Digitization for Operational Efficiency

Verizon's private 5G at AdventHealth and Tampa General collapses three parallel wireless overlays, trimming nurse walking time by 15% and speeding bed turnover. Oulu University Hospital streams 4K surgical video over sub-10 ms links, enabling remote intraoperative consults[1]Nokia, “Oulu University Hospital Deploys Private 5G Network for Smart Healthcare,” nokia.com. RFID and BLE tags track pumps and wheelchairs, meeting FDA-mandated Unique Device Identifier requirements and minimizing asset shrinkage. Such efficiencies reduce length of stay and free nursing hours for direct care, sustaining double-digit ROI on connectivity budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity, privacy, and compliance costs | -1.8% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Interoperability and legacy integration complexity | -1.5% | Global, pronounced in U.S. EHR landscape | Medium term (2-4 years) |

| 2G/3G sunsets driving costly migrations | -1.2% | Europe, North America, select APAC | Short term (≤ 2 years) |

| Battery longevity and power constraints | -0.9% | Global, critical for implantables | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity, Privacy, And Compliance Costs Across Expanded Attack Surface

The 2024 Change Healthcare ransomware event and Ascension Health breach revealed vulnerabilities in infusion pumps and telemetry hubs connected via M2M gateways[2]U.S. Department of Health and Human Services, “Change Healthcare Ransomware Attack,” hhs.gov. New FDA cybersecurity rules add USD 0.5-2 million to each platform’s validation costs and compress launch timelines.

The EU’s forthcoming Cyber Resilience Act introduces 24-hour incident reporting and third-party audits, compelling module vendors like Quectel to embed hardware root-of-trust mechanisms. Vendors lacking security budgets risk exclusion from hospital formularies, tempering near-term Healthcare M2M market growth.

Interoperability And Legacy Integration Complexity

Only 30% of U.S. hospitals can query all six TEFCA networks, forcing device makers to juggle multiple interfaces. FHIR is mandated in new EHR certification, yet radiology and lab systems still speak HL7 v2, necessitating middleware translators that add 6-12 months to deployments. China’s telemedicine standards aim for unified protocols, but provincial roll-outs vary, complicating cross-border device data exchange. As a result, even FHIR-ready devices must coexist with decades-old systems, raising integration costs and deployment risk within the Healthcare M2M market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Telemedicine Pulls Ahead

Remote Patient Monitoring (RPM) and connected medical devices still brought in a majority-share 56.14% of application revenue in 2025. Even so, Telemedicine & Virtual Care is set to expand the fastest, rising 16.56% annually through 2031. Several shifts explain the jump. First, Washington made pandemic telehealth waivers permanent, giving hospitals and clinics reliable reimbursement for behavioral health, chronic care, and specialty visits. Second, big public platforms prove that virtual care carries real weight. India’s eSanjeevani, for example, has already logged 360 million visits, handling 7 out of 10 routine primary-care cases without requiring an office appointment.

Inside hospitals, wireless patient monitoring is spreading thanks to low-energy Bluetooth gear that lets a single nurse oversee more beds. Philips’ long-term “equipment-as-a-service” deal with Hoag Hospital even bundles hardware, maintenance, and upgrades into a single subscription fee, turning hefty capital outlays into manageable operating costs. Although still small, medication-adherence tools are catching the eye of drug makers. ResMed’s Propeller Health sensor clips onto an inhaler, time-stamps each puff, and pushes the data to the cloud—handy proof for asthma and COPD trial sponsors eager to show payers that patients really take their meds.

By Connectivity Technology: Smart-Home Mesh Hits Its Stride

Classic cellular, 4G, LTE, and 5G, remains the largest slice, accounting for 37.91% of connectivity revenue in 2025, buoyed by smartphone ubiquity and the retirement of 2G/3G gear. Yet the brightest growth story belongs to short-range mesh protocols. Zigbee, Z-Wave, and Thread should grow 15.31% annually through 2031 as aging-in-place programs outfit homes with motion sensors, door contacts, and fall detectors. Matter, the interoperability standard finalized in 2024, lets a single hub pull data from assorted devices, smart speakers, lights, and glucose meters, without multiple gateways.

Governments with aging demographics are leaning in. Japan is subsidizing Thread-based fall sensors that alert caregivers within seconds, and South Korea has similar incentives. LTE-M and NB-IoT keep growing in low-power trackers and pill dispensers that send only a trickle of data but need batteries to last years. Wi-Fi still rules bedside monitors, but hospitals increasingly add private 5G layers for life-critical traffic because Wi-Fi 6E hand-offs can lag. Bluetooth Low Energy dominates wearables, and the new LE Audio spec even streams directly to hearing aids, blurring the line between medical and consumer tech.

By Component: Software Becomes the Profit Engine

Hardware still leads the money race: medical devices delivered 41.29% of 2025 revenue. Even so, Platforms & Software should outpace every other piece, growing 16.24% annually through 2031 as firms trade one-off device sales for recurring analytics fees. Abbott’s and Medtronic’s data-sharing deals show the shift: glucose data itself is becoming a commodity, but algorithms that predict trouble win premium pricing. Cloud giants are quick to capitalize—Azure hosts Medtronic’s workloads, while AWS runs Philips’ monitoring back-end.

GE HealthCare and Medtronic’s 2026 tie-up integrates continuous glucose data directly into hospital records, creating stickier software subscriptions. Service contracts that wrap hardware, connectivity, and support into a single monthly bill are gaining favor, too; Philips’ 10-year bundle with Hoag Hospital moves upkeep costs off hospital balance sheets. Governments are also turning up the heat on data standards. China’s 2025 rules require telemedicine networks to adopt unified exchange protocols, complete with blockchain audit trails, nudging every provincial health exchange onto modern platforms.

By End User: Homecare Takes the Growth Crown

Hospitals and clinics still spent nearly half 48.90% of every Healthcare M2M dollar in 2025, but home-based patients are the breakout story, projected to climb 16.01% a year to 2031. Permanent U.S. RPM and RTM reimbursement turns continuous monitoring into a billable service, rewarding systems that keep patients out of the ER. India’s eSanjeevani and national health ID program show how remote care scales in low-bandwidth settings, funneling chronic-disease data from rural homes into centralized dashboards.

Consumer-friendly sensors broaden the pool. Dexcom’s over-the-counter Stelo CGM reaches pre-diabetics and wellness users, while Insulet’s Omnipod 5 won clearance for the 30 million-plus Type 2 population. Asset-tracking gates help ambulatory centers meet FDA device-label rules, but their total spend still trails the swelling homecare market.

Inpatient networks are expensive, private 5G can cost USD 2-5 million per campus, so only large systems can afford them. A homecare kit needs little more than a modem and a smartphone. That low entry cost lets vendors reach millions of households. Abbott’s AI glucose coach aims to slash costly hypoglycemic ER visits, and value-based care contracts now share those savings with providers.

Geography Analysis

North America accounted for 37.65% revenue in 2025, underpinned by CMS reimbursement clarity and dense private 5G pilots. Early outcomes from AdventHealth show notable reductions in nurse walking time, validating capital outlays and spurring copycat deployments. FDA cybersecurity rules raise entry barriers but also weed out sub-scale suppliers, nudging consolidation within the Healthcare M2M market. Canada and Mexico harmonize policies, creating a contiguous regulatory bloc that simplifies regional roll-outs.

Asia-Pacific is the fastest-growing theatre, with a 16.71% CAGR, propelled by China’s 300 medical LLMs and India’s 360 million-strong teleconsultation backbone. Japan and South Korea subsidize home-based monitoring to offset aging demographics, while 5G penetration across APAC reaches 18%, enabling edge AI at community clinics. Regional partnerships on quantum-AI cardiology trials hint at leapfrogging opportunities that could reorder vendor hierarchies.

Europe is growing steadily as MDR-mandated post-market surveillance makes embedded telemetry table stakes. Belgium and Finland prove sub-10 ms private 5G is feasible even in smaller hospitals, encouraging wider EU adoption. Middle-East Gulf states deploy kiosk-based telemedicine over 5G to remedy physician shortages, whereas South America’s progress hinges on Brazil’s subsidized data-plan program that targets Amazon basin chronic-disease hotspots.

Competitive Landscape

The Healthcare M2M market remains fragmented, with the top players holding a significant combined share, fostering rapid innovation cycles. Abbott and Dexcom commoditize glucose data but differentiate through AI coaching; Medtronic and GE HealthCare chase interoperability, embedding Simplera CGM streams into EMRs to lock in hospital workflows. Verizon and AT&T leverage carrier scale to bundle connectivity and compliance, whereas module suppliers Quectel and Telit jockey to certify Cyber Resilience Act-ready chipsets.

Cloud hyperscalers vie for backend dominance: Azure wins Medtronic, AWS secures Philips, and Google courts startups with Healthcare API credits. Pharmaceutical sponsors bankroll adherence sensors to capture real-world evidence, creating a fresh battleground where device, data, and drug intersect. Net result: competition pivots from hardware margins to data rights, algorithmic IP, and secure over-the-air update pipelines, elements that together define durable advantage in the Healthcare M2M market.

Healthcare M2M Industry Leaders

Abbott Laboratories

Dexcom, Inc.

Medtronic Plc

GE HealthCare

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Medtronic and GE HealthCare linked Simplera CGM data with hospital EMRs

- February 2026: FDA issued final cybersecurity guidance, mandating software bills of materials.

- February 2026: Verizon and Aeris integrated SGP.32 eSIM provisioning into ThingSpace.

Global Healthcare M2M Market Report Scope

As per the scope of the report, healthcare Machine-to-Machine (M2M) technology refers to the automated exchange of data between medical devices and central systems without human intervention. This ecosystem typically consists of networked sensors that record physiological data, such as heart rate or blood glucose levels, and transmit it via wired or wireless channels like 5G, Wi-Fi, or cellular networks to software applications that convert it into usable information for physicians.

The healthcare M2M market is segmented by application, connectivity technology, component, end user, and geography. Based on applications, the market is segmented into remote patient monitoring (RPM) and connected medical devices, telemedicine & virtual care, inpatient wireless patient monitoring, clinical operations & workflow management, asset & staff tracking, medication adherence & connected drug delivery, and other applications. By connectivity technology, the market is segmented into cellular (4G/LTE/5G), LPWA (LTE-M, NB-IoT), Wi‑Fi, Bluetooth Low Energy (BLE), Zigbee/Z‑Wave/Thread, and RFID/NFC. By component, the market is medical devices, platforms & software, and services. By end users, the market is segmented into hospitals & clinics, homecare patients, ambulatory surgical centers, diagnostic & imaging centers/labs, and other end users.

By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Remote Patient Monitoring (RPM) and Connected Medical Devices |

| Telemedicine & Virtual Care |

| Inpatient Wireless Patient Monitoring |

| Clinical Operations & Workflow Management |

| Asset & Staff Tracking |

| Medication Adherence & Connected Drug Delivery |

| Other Applications |

| Cellular (4G/LTE/5G) |

| LPWA (LTE-M, NB-IoT) |

| Wi‑Fi |

| Bluetooth Low Energy (BLE) |

| Zigbee/Z‑Wave/Thread |

| RFID/NFC |

| Medical Devices |

| Platforms & Software |

| Services |

| Hospitals & Clinics |

| Homecare Patients |

| Ambulatory Surgical Centers |

| Diagnostic & Imaging Centers/Labs |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Remote Patient Monitoring (RPM) and Connected Medical Devices | |

| Telemedicine & Virtual Care | ||

| Inpatient Wireless Patient Monitoring | ||

| Clinical Operations & Workflow Management | ||

| Asset & Staff Tracking | ||

| Medication Adherence & Connected Drug Delivery | ||

| Other Applications | ||

| By Connectivity Technology | Cellular (4G/LTE/5G) | |

| LPWA (LTE-M, NB-IoT) | ||

| Wi‑Fi | ||

| Bluetooth Low Energy (BLE) | ||

| Zigbee/Z‑Wave/Thread | ||

| RFID/NFC | ||

| By Component | Medical Devices | |

| Platforms & Software | ||

| Services | ||

| By End User | Hospitals & Clinics | |

| Homecare Patients | ||

| Ambulatory Surgical Centers | ||

| Diagnostic & Imaging Centers/Labs | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will Healthcare M2M connectivity spending grow through 2031?

Total outlays are projected to rise from USD 11.60 billion in 2026 to USD 22.63 billion by 2031, reflecting a 14.29% CAGR.

Which application contributes the largest revenue today?

Remote Patient Monitoring and connected medical devices accounted for 56.14% of 2025 revenue and should remain the dominant segment.

What connectivity option is preferred for mission-critical hospital telemetry?

Private cellular (4G/LTE/5G) leads due to guaranteed quality of service and simplified eSIM provisioning.

Why is Asia-Pacific the fastest-growing region?

Government-backed 5G roll-outs, large telemedicine platforms like eSanjeevani, and aging demographics drive a 16.71% CAGR from 2026 to 2031.

Page last updated on: