Healthcare Navigation Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.25 Billion |

| Market Size (2031) | USD 17.61 Billion |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Navigation Platform Market Analysis by Mordor Intelligence

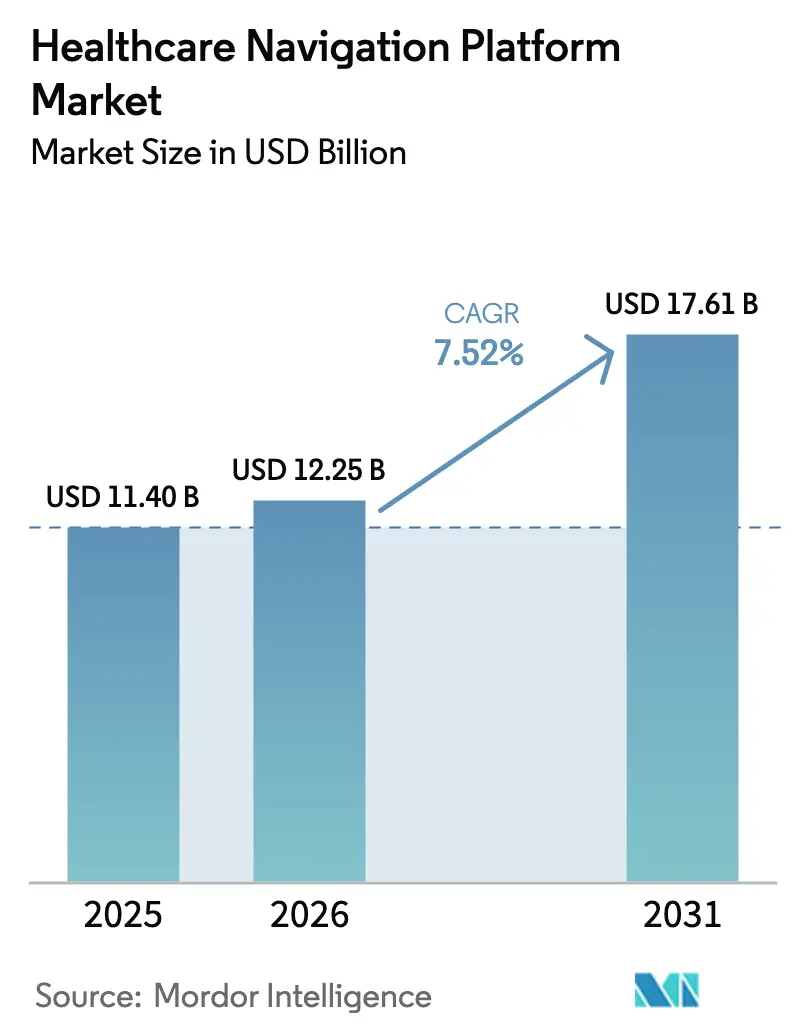

The Healthcare Navigation Platform Market size was valued at USD 11.40 billion in 2025 and is estimated to grow from USD 12.25 billion in 2026 to reach USD 17.61 billion by 2031, at a CAGR of 7.52% during the forecast period (2026-2031).

The current expansion reflects payer, employer, and health-system moves away from reactive phone centers toward AI-enabled, omnichannel guidance that steers members to the right care setting at the exact moment of choice. Employers now consolidate once-fragmented point solutions into unified platforms, while payers embed navigation into their digital front doors to defend their star ratings. Platform vendors are also gaining tailwinds from government-led digital health mandates and the broader shift to value-based contracts that reward coordinated care. Cloud economics, rising FHIR API adoption, and generative-AI personalization further accelerate uptake as organizations seek scalable infrastructure capable of ingesting claims, clinical, and social-determinant data in real time.

Key Report Takeaways

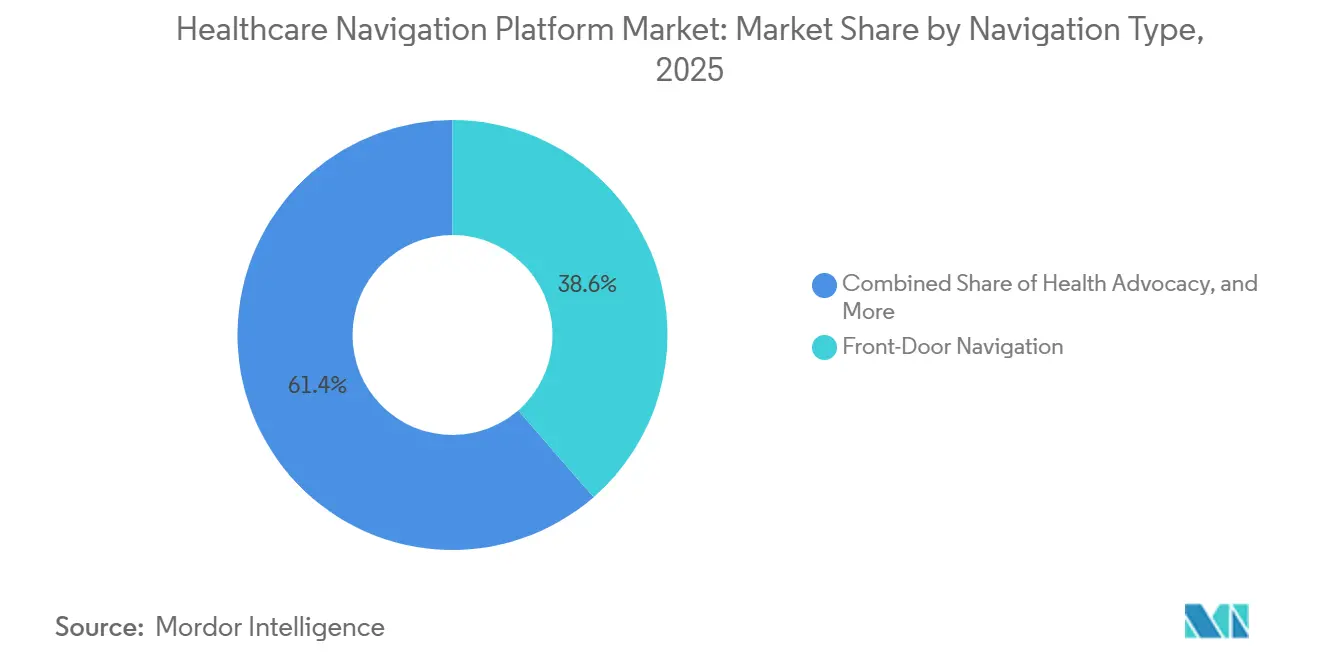

- By navigation type, Front-Door Navigation led with 38.55% revenue share in 2025; Condition-Specific Vertical Navigation is forecast to expand at an 11.25% CAGR through 2031.

- By deployment mode, Cloud-Based solutions held 69.23% of the Healthcare Navigation Platform market share in 2025, while on-premises-to-cloud migration is advancing at a 10.15% CAGR through 2031.

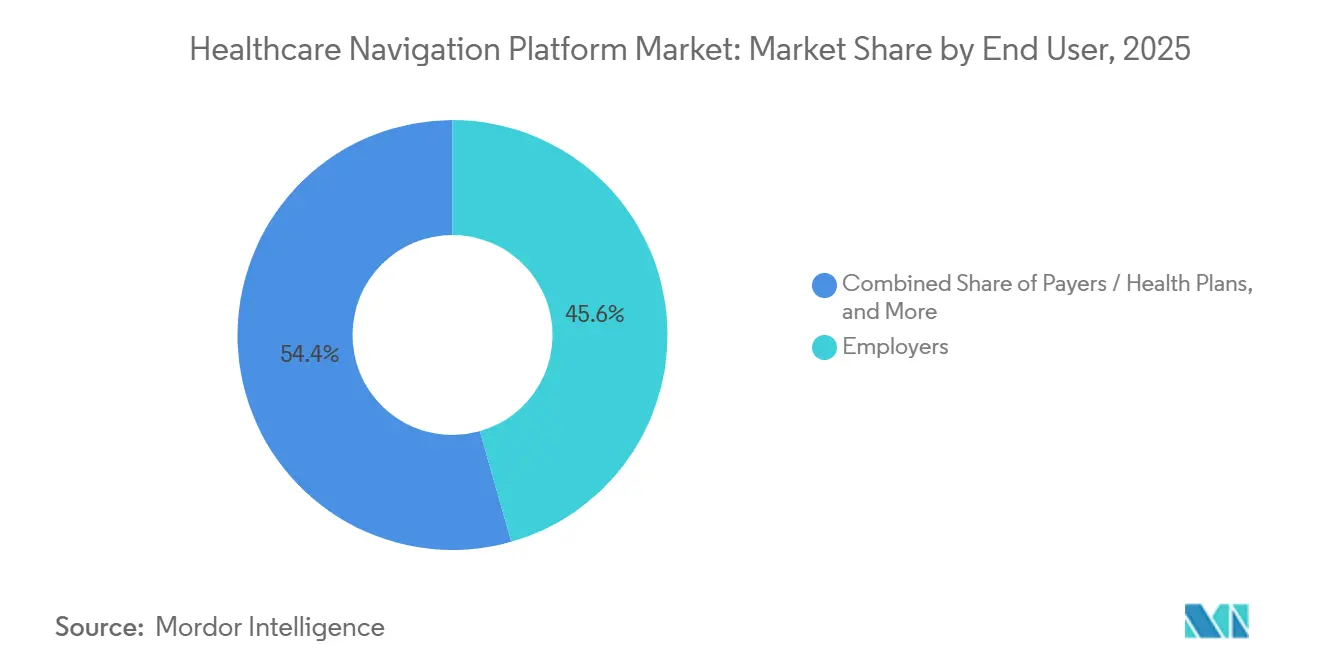

- By end user, employers accounted for 45.63% of the Healthcare Navigation Platform market in 2025, and payers are advancing at a 12.15% CAGR through 2031.

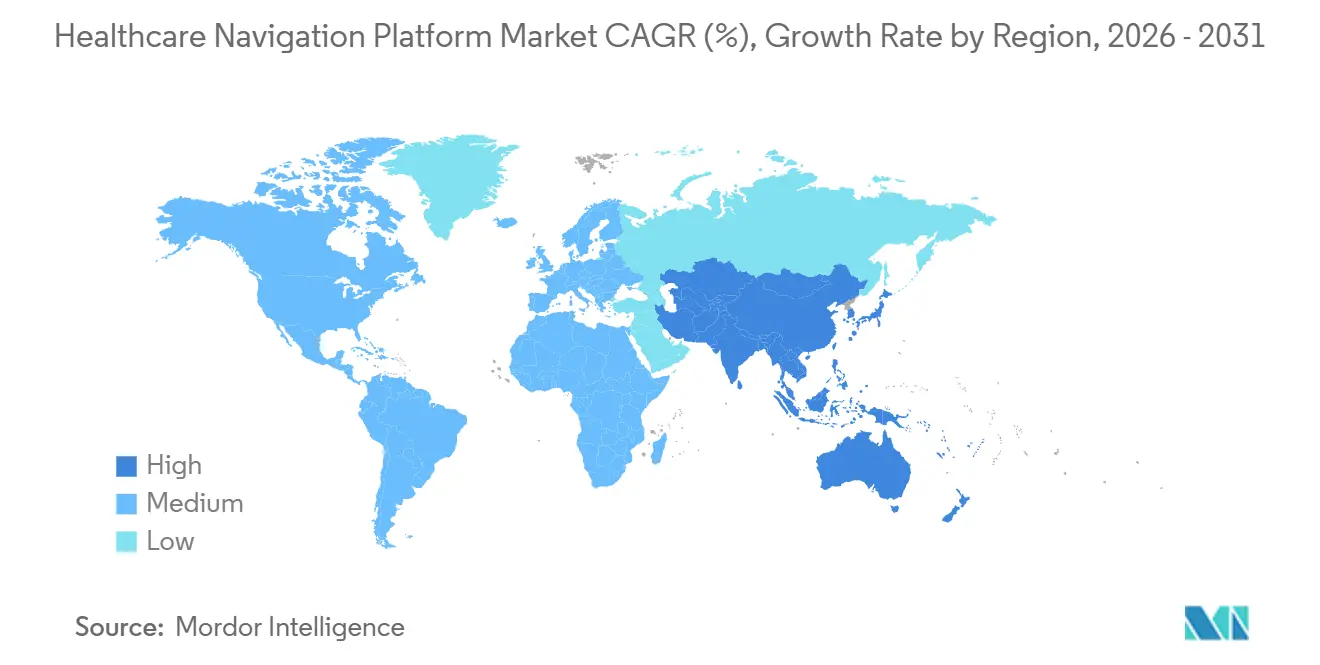

- By geography, North America commanded 45.25% revenue share in 2025; Asia-Pacific is forecast to grow at a 12.82% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Navigation Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Employer Demand for Integrated Benefit Navigation Solutions | +1.8% | North America, with early adoption in Western Europe | Medium term (2-4 years) |

| Shift To Value-Based Care Models Rewarding Coordinated Navigation | +2.1% | Global, led by North America; APAC pilots emerging in Australia, Singapore | Long term (≥ 4 years) |

| Payer Push for Digital Front-Door Experiences | +1.6% | North America & EU, expanding to Middle East health insurers | Short term (≤ 2 years) |

| AI-driven Personalization Improving Engagement | +1.4% | Global, with concentrated R&D in North America and select APAC hubs | Medium term (2-4 years) |

| State Medicaid Waivers Funding Navigation for SDoH Integration | +0.9% | United States (state-level), limited international parallel | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Employer Demand For Integrated Benefit Navigation Solutions

Large U.S. employers have made integrated navigation a budget imperative. The Business Group on Health 2025 survey showed that 73% of jumbo employers contract with a single navigation vendor, up from 58% in 2023, because unified platforms cut conflicting guidance across medical, pharmacy, and mental-health programs[1]Business Group on Health, “2025 Large Employer Health Care Strategy Survey,” BusinessGroupHealth.org. The 2025 Kaiser Family Foundation survey reported 12% lower specialty-referral spend for firms deploying integrated navigation and a nine-point jump in member satisfaction[2]Kaiser Family Foundation, “2025 Employer Health Benefits Survey,” KFF.org. Mid-market employers with 500–5,000 employees are now aligning with this model as CFOs demand a measurable return on investment. Navigation adoption also dovetails with a broader “benefits-as-a-platform” strategy that connects pharmacy-benefit managers, telemedicine providers, and specialty networks through a single front end. The resulting reduction in vendor sprawl simplifies contracting, eases security audits, and enhances the user interface, reinforcing the Healthcare Navigation Platform market growth trajectory.

Shift To Value-Based Care Models Rewarding Coordinated Navigation

Accountable care organizations and risk-bearing provider groups now treat navigation as a lever for hitting quality benchmarks. CMS reported that ACOs using navigation lowered emergency department visits by 14% and generated average shared savings bonuses of USD 1.8 million in 2025. A joint playbook from the American Medical Association, AHIP, and NAACOS underscores the importance of real-time data sharing through navigation platforms to close care gaps [3]American Medical Association et al., “Health Data Sharing in Value-Based Care Playbook,” AMA-Assn.org. The Commonwealth Fund documented that Medicaid programs with embedded navigation increased postpartum follow-up by 22% and improved HbA1c control by 17%[4]Commonwealth Fund, “Medicaid Managed Care Quality Measures Analysis,” CommonwealthFund.org. Australia, Singapore, and other APAC health systems are piloting bundled payments that reward general practitioners for using navigation to reduce duplicate imaging. These payment reforms lock navigation into care-delivery economics, sustaining Healthcare Navigation Platform market expansion over the long term.

Payer Push For Digital Front-Door Experiences

Commercial and government insurers are embedding navigation in their mobile apps to protect star ratings, retain employer contracts, and cut call-center load. J.D. Power’s 2025 member study found 87-point satisfaction gains when plans provided AI chatbots and personalized care recommendations. A 2024 HealthEdge poll showed that 68% of payers have rolled out or piloted conversational AI, with early movers cutting call-center contacts by 30% in six months. Star-rating methodology now scores digital-channel responsiveness, creating an immediate incentive. International precedents reinforce the trend: the NHS App accumulated 35 million users by late 2025, proving that large-scale digital front doors can shift patient behavior. Collectively, these factors keep the Healthcare Navigation Platform market adoption high in the short term.

AI-Driven Personalization Improving Engagement

Generative AI lets platforms parse longitudinal claims, clinical notes, and sentiment cues to create hyper-relevant care paths. A 2024 Nature Medicine study found that members who received AI-tailored suggestions were 26% more likely to complete preventive screenings and 19% less likely to miss specialist appointments. Google Health research on physician-tuned large language models demonstrated near-human empathy in message responses, suggesting scalable, high-touch support. Stanford randomized trials found that AI-drafted messages cut clinician documentation time by 12 minutes per encounter, freeing capacity for complex care. Yet safety monitoring remains vital, as a 2024 JAMA analysis flagged occasional omission of critical alerts. Despite caveats, AI continues to raise engagement metrics, boosting the Healthcare Navigation Platform market CAGR contribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Data Sources Limiting Single-View-of-Member | -1.2% | Global, acute in North America | Medium term (2-4 years) |

| Privacy Concerns over Longitudinal Behavioral Data | -0.7% | North America and EU | Short term (≤ 2 years) |

| Slow EHR-API Uptake among Mid-Size Provider Groups | -0.9% | North America, mirrors issues in Europe and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Data Sources Limiting Single-View-Of-Member

Navigation vendors face persistent data silos across clinical, claims, and pharmacy systems. A 2024 JAMA study reported 8.3% patient-matching error rates in regional health information exchanges, leading to missed hospitalizations within navigation recommendations. The ONC’s 2023 report to Congress showed 31% of hospitals reporting information blocking, often tied to EHR vendors charging high API fees. Multi-payer environments intensify fragmentation, forcing platforms to develop proprietary normalization engines that add latency and cost. Vendors compensate through master-patient-index algorithms, yet the lag undercuts real-time triage and diminishes perceived value. These factors shave 1.2 percentage points from the forecast Healthcare Navigation Platform market CAGR.

Privacy Concerns Over Longitudinal Behavioral Data

Members worry that navigation insights on app usage and sentiment could influence underwriting or be sold. SAMHSA’s 2024 update to 42 CFR Part 2 aligned substance-use-disorder consent with HIPAA, but state Medicaid systems still enforce stricter rules. A National Council for Mental Wellbeing survey found 54% of behavioral-health providers were uncertain about compliance when sharing data with navigation vendors. Multiple U.S. states enacted privacy statutes in 2024–2025 that classify health data as sensitive and demand opt-in consent. The upcoming European Health Data Space will tighten purpose limitation, challenging longitudinal profiling techniques. These headwinds trim 0.7 percentage points from the growth of the healthcare navigation platform market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Navigation Type: Verticals Capture High-Cost Cohorts

Condition-Specific Vertical Navigation is projected to grow at an 11.25% CAGR between 2026 and 2031, well above the Healthcare Navigation Platform market average. Front-Door Navigation still generated the largest revenue in 2025, with a 38.55% share, serving as the initial triage layer that guides members to benefits, directories, or virtual urgent care. Oncology and musculoskeletal programs drive vertical growth by bundling care coordination, second-opinion access, and cost-transparency tools that directly influence high-cost decisions. A 2024 Journal of Managed Care & Specialty Pharmacy study found that oncology navigation reduced total care costs by 21% compared with matched cohorts. Vertical navigation vendors also integrate behavioral health, diabetes, and maternal care modules, which reduces referral leakage for payers. Front-Door Navigation growth is moderating as payers embed basic symptom checkers directly into first-party mobile apps, compressing stand-alone vendor contracts. General Navigation, focused on benefit inquiries, faces commoditization; EHR vendors now bundle similar features. Musculoskeletal navigation is in strong demand among employers, with Hinge Health reporting a 32% drop in orthopedic surgery rates among engaged members. Behavioral health navigation gains momentum as parity enforcement tightens and payers integrate mental health with chronic-disease management, achieving 19% higher follow-up rates after psychiatric discharge.

Continued vertical traction lifts engagement metrics as patients receive condition-specific coaching, curated provider networks, and personalized digital therapy content. Employers cite measurable ROI when surgical avoidance and medication adherence improve. Payers appreciate integrated reporting dashboards that feed directly into value-based contract analytics. As adoption scales, the segment’s contribution to the Healthcare Navigation Platform market size is projected to rise steadily, whereas generalist solutions plateau. For vendors, portfolio breadth across multiple clinical verticals has emerged as a competitive differentiator that attracts large multipayer contracts and international expansion opportunities.

By Deployment Mode: Cloud Moves From Advantage To Default

Cloud-Based deployments accounted for 69.23% market share in 2025 and are forecast to grow at a 10.15% CAGR through 2031, reflecting elastic compute economics and native API architectures. Subscription pricing aligns vendor incentives with active member engagement, reducing the large upfront license fees typical of on-premise contracts. Cloud environments enable weekly feature releases, automatic security patching, and rapid integration of generative AI capabilities, such as real-time benefit checks or appointment-scheduling chatbots. A 2024 HIMSS study noted that 71% of health systems planned at least one major cloud migration within 24 months, with care coordination ranked top use case.

On-premises deployments persist among risk-averse provider systems and federal agencies subject to data-residency rules. The U.S. Department of Veterans Affairs continues to self-host its patient portal stack due to FedRAMP constraints affecting 9 million users. Hybrid models gain traction in Europe, where platforms host member-facing layers in regional clouds while storing clinical data on local servers to meet GDPR requirements. Security remains a gating factor; a 2024 HealthEdge survey showed 48% of payers citing ransomware risk as a barrier to full cloud migration. Despite hurdles, the continued swing to cloud will enlarge the Healthcare Navigation Platform market size among subscription players, while legacy on-premise share declines.

By End User: Payers Accelerate Under Star-Rating Pressure

Employers accounted for 45.63% revenue in 2025, reflecting early adoption and ongoing efforts to shrink specialty-care leakage. Growth has begun to plateau as large enterprises have already contracted with vendors, leaving penetration gaps mainly in the mid-market. Payers and health plans are the fastest-growing segment, projected to grow at a 12.15% CAGR through 2031, driven by CMS Star Ratings that reward member experience and care-gap closure. Payer adoption also rises because navigation can steer members to in-network facilities, improving medical-loss ratios. Government programs are mandating beneficiary-support systems that mirror employer benefits, adding regulatory pull in Medicaid and Medicare Advantage plans.

Provider uptake lags due to tighter capital budgets and integration complexity, though value-based payment contracts push hospitals to implement enterprise-wide navigation. An American Hospital Association 2024 survey reported 29% system-wide deployment, with remaining facilities employing departmental point solutions. Direct-to-consumer models remain a niche, yet some vendors pilot freemium apps monetized through referral fees or pharmaceutical partnerships. Overall, payer momentum is set to lift their Healthcare Navigation Platform market share substantially across the forecast horizon.

Geography Analysis

North America maintained a 45.25% share in 2025, supported by mature employer self-insurance, intense payer competition, and advanced EHR penetration. Growth moderates as large employers and national payers approach saturation, and future expansion relies on mid-market employer penetration plus Medicaid managed-care requirements. CMS rules that elevate digital engagement metrics keep the region ahead in functionality, while state Medicaid 1115 waivers fund social determinants navigation pilots in North Carolina, Oregon, and California, providing budget support.

Asia-Pacific delivers the highest CAGR at 12.82% through 2031, propelled by large-scale digital health mandates. India’s Ayushman Bharat Digital Mission reached 500 million registrations by late 2025, creating a national health-ID spine that navigation vendors can tap for claims and clinical data. China’s revised Internet Hospital regulations clarify reimbursement, prompting insurers and health systems to roll out patient-centered navigation portals. Australia and Japan fund telehealth and remote-monitoring programs that include navigation features, and regional big-tech firms partner with insurers to bundle chat-based triage inside messaging apps.

Europe shows mid-single-digit growth. The United Kingdom’s NHS App acts as a de facto front door for 35 million users, yet incomplete hospital-EHR integration limits longitudinal navigation. Germany’s Digital Healthcare Act fast-tracks reimbursable digital applications, and 58 DiGA solutions were approved by mid-2025, several of which embed navigation layers. France pilots regional navigation portals to reduce GP workload and appointment bottlenecks. GDPR drives hybrid hosting architectures, shaping vendor deployment choices.

The Middle East and Africa plus South America remain emerging markets. Private insurers in Gulf Cooperation Council states integrate navigation to differentiate employer group products, while public systems lag amid infrastructure gaps. Brazil launched a national telemedicine platform in 2024 to serve rural patients and private insurers overlay navigation to divert members from emergency rooms. These regions exhibit high long-term potential once interoperability improves, adding optionality for vendors seeking first-mover advantage in less competitive landscapes.

Competitive Landscape

The Healthcare Navigation Platform market is moderately fragmented. No player holds dominance because buyer segments vary by employer size, payer integration depth, and provider EHR environment. Horizontal platforms such as Quantum Health address employers, payers, and providers through a unified stack. Vertical specialists like Hinge Health focus on musculoskeletal care, while embedded solutions from EHR vendors such as Epic Systems integrate navigation directly into clinician workflows.

Publicly filed 10-K statements reveal that multi-segment vendors achieve 22% higher gross margins than single-segment peers because platform R&D costs amortize across larger revenue bases. Payer-owned platforms are growing as insurers prefer end-to-end control over data and the member experience. Generative-AI startups challenge incumbents with low-cost chat interfaces that can be white-labeled by payers or employers.

Technology differentiation hinges on API breadth, AI-driven risk scoring, and outcome attribution dashboards. Vendors filing AI-related patents increased 37% year over year in 2024, signaling an algorithmic arms race. Interoperability capabilities remain a key competitive axis. Platforms able to normalize FHIR and non-FHIR data streams into a single member record win contracts where health systems still run multiple EHR instances. Pricing models are shifting to performance-based fees tied to avoided costs or quality metrics, placing pressure on vendors that cannot prove ROI.

Market consolidation pressure is visible in recent deals. Quantum Health acquired Embold Health in early 2025 to bring provider-quality analytics in-house and launched Care Finder later that year. Bamboo Health introduced Bamboo Bridge in December 2025, adding behavioral-health navigation to its real-time intelligence platform. EHR vendors continue to roll out free navigation modules, squeezing standalone vendors on price. Nevertheless, white-space exists in Medicaid managed-care plans, mid-market employers, and APAC government contracts, suggesting sustained opportunity for differentiated players.

Healthcare Navigation Platform Industry Leaders

Accolade

Brightside Health

Buoy Health

Castlight Health

Quantum Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Bamboo Health launched Bamboo Bridge, an AI-enabled behavioral health navigation platform for high-need patients, integrating curated provider networks and expert navigators.

- September 2025: Quantum Health extended Care Finder by Embold Health to all clients, enhancing its navigation suite with integrated provider-quality search capabilities.

Global Healthcare Navigation Platform Market Report Scope

As per the report's scope, healthcare navigation platforms are digital solutions designed to guide patients, caregivers, and employers through the complex healthcare system. They integrate benefits, provider networks, cost transparency, and personalized support to help users make informed decisions about care. By combining technology with human assistance, these platforms improve access, reduce administrative burden, and enhance overall patient experience.

The healthcare navigation platforms market segmentation includes navigation type, deployment mode, end user, and geography. By navigation type, the market is segmented into front-door navigation, health advocacy, condition-specific vertical navigation, and general navigation. By deployment mode, the market is segmented into cloud-based and on-premise. By end user, the market is segmented into employers, payers/health plans, providers/health systems, government & public programs, and individuals / direct-to-consumer. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Front-Door Navigation |

| Health Advocacy |

| Condition-Specific Vertical Navigation |

| General Navigation |

| Cloud-Based |

| On-Premise |

| Employers |

| Payers / Health Plans |

| Providers / Health Systems |

| Government & Public Programs |

| Individuals / Direct-to-Consumer |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Navigation Type | Front-Door Navigation | |

| Health Advocacy | ||

| Condition-Specific Vertical Navigation | ||

| General Navigation | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By End User | Employers | |

| Payers / Health Plans | ||

| Providers / Health Systems | ||

| Government & Public Programs | ||

| Individuals / Direct-to-Consumer | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 valuation for Healthcare Navigation Platform solutions?

The Healthcare Navigation Platform market size is USD 12.25 billion in 2026.

How fast is the sector expected to expand through 2031?

Revenue is projected to reach USD 17.61 billion by 2031, implying a 7.52% CAGR.

Which navigation type is growing quickest?

Condition-Specific Vertical Navigation is forecast at an 11.25% CAGR from 2026-2031.

Why are payers investing heavily in navigation platforms?

CMS Star Ratings and value-based contracts reward member experience and care-gap closure, making navigation essential.

Which region offers the highest growth upside?

Asia-Pacific leads with a projected 12.82% CAGR through 2031, spurred by national digital-health mandates.

What deployment model dominates new contracts?

Cloud-based platforms held 69.23% share in 2025 and continue to expand due to elastic scaling and rapid feature release.

Page last updated on: