Patient Experience Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.40 Billion |

| Growth Rate (2026 - 2031) | 11.93% CAGR |

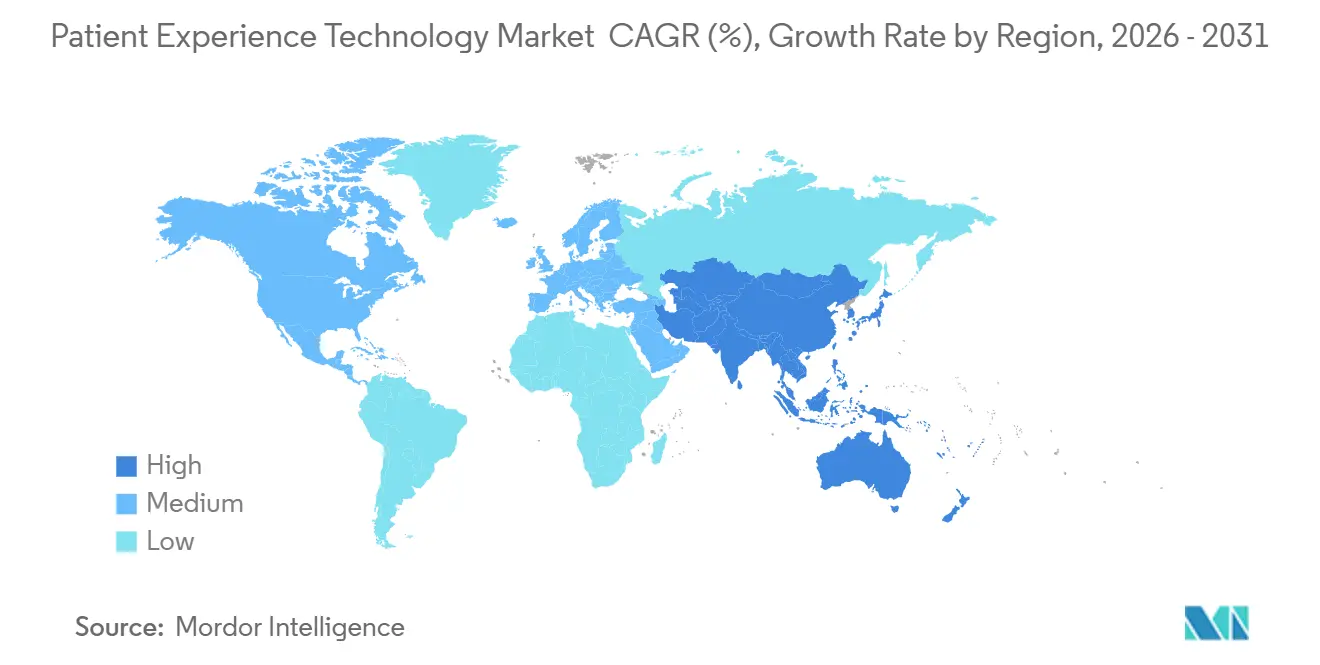

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

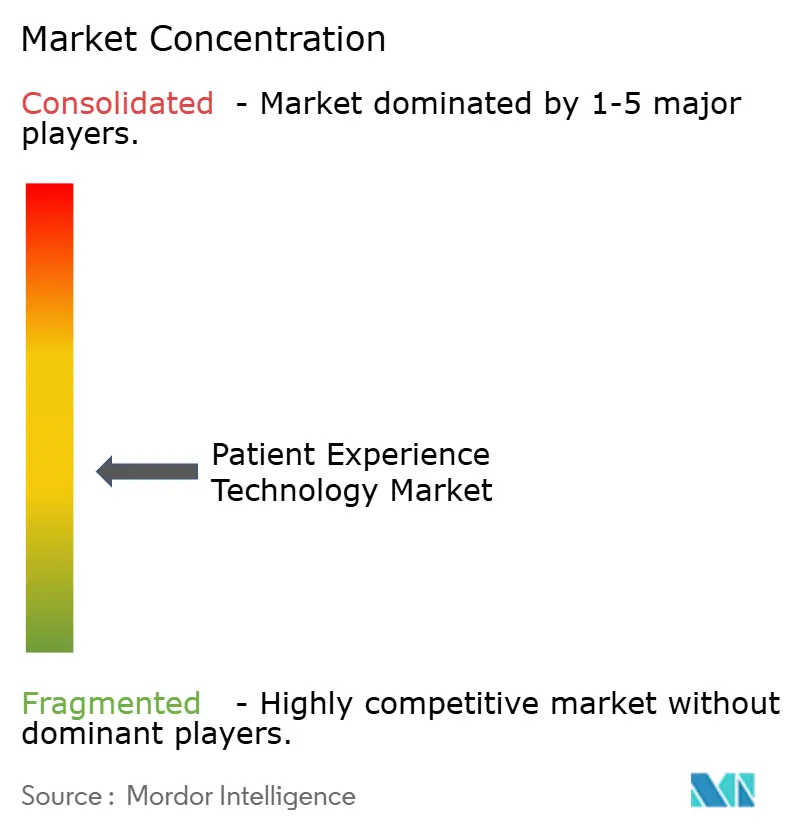

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Experience Technology Market Analysis by Mordor Intelligence

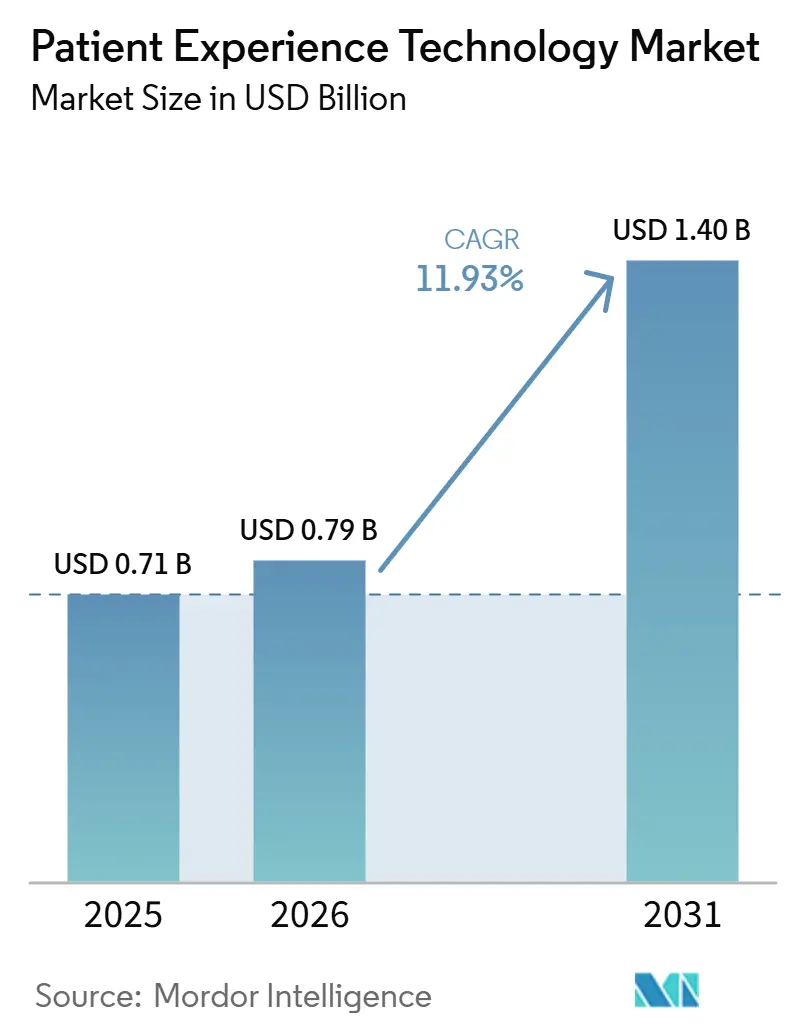

The Patient Experience Technology Market size is projected to be USD 0.71 billion in 2025, USD 0.79 billion in 2026, and reach USD 1.40 billion by 2031, growing at a CAGR of 11.93% from 2026 to 2031.

The market is moving beyond simple digitization because providers now use digital identity, self-service access, and persistent communication channels to manage a larger share of the care journey. Portal messages rose 153% between 2020 and 2025, while telephone calls declined 6% across more than 2,000 hospitals and 47,000 clinics, which shows that patient behavior has shifted toward digital touchpoints at scale. This change is expanding between-visit care activity and is pushing health systems to redesign staffing, triage, and communication workflows around higher digital volumes. Medicare reimbursement rules and federal interoperability standards keep spending on the patient experience technology market close to core revenue and compliance priorities rather than optional innovation budgets. AI-enabled scheduling, outreach, and navigation tools are also making the patient experience technology market more scalable, while creating better conditions for platform consolidation and broader enterprise buying decisions.

Key Report Takeaways

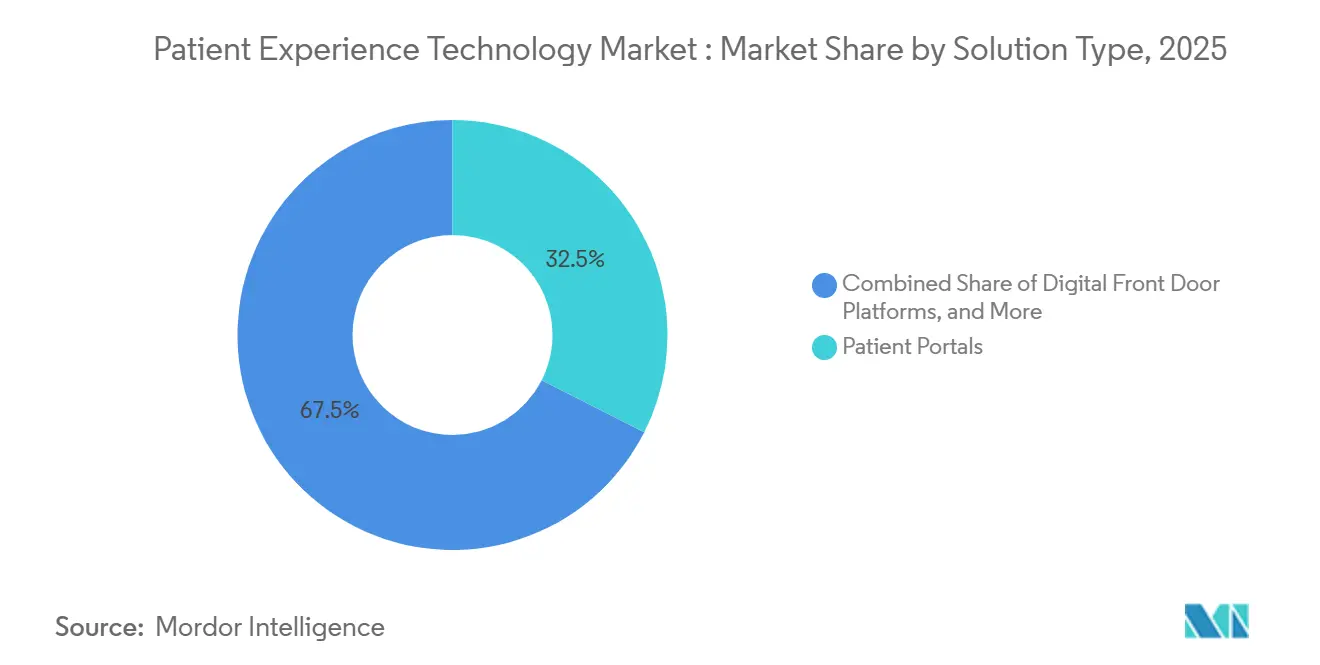

- By solution type, patient portals held 32.47% of revenue in 2025, while digital front door platforms recorded the fastest projected CAGR at 12.89% through 2031 in the patient experience technology market.

- By deployment mode, cloud-based solutions accounted for 62.58% of revenue in 2025, while on-premise solutions posted the highest expected CAGR at 13.61% through 2031 in the patient experience technology market.

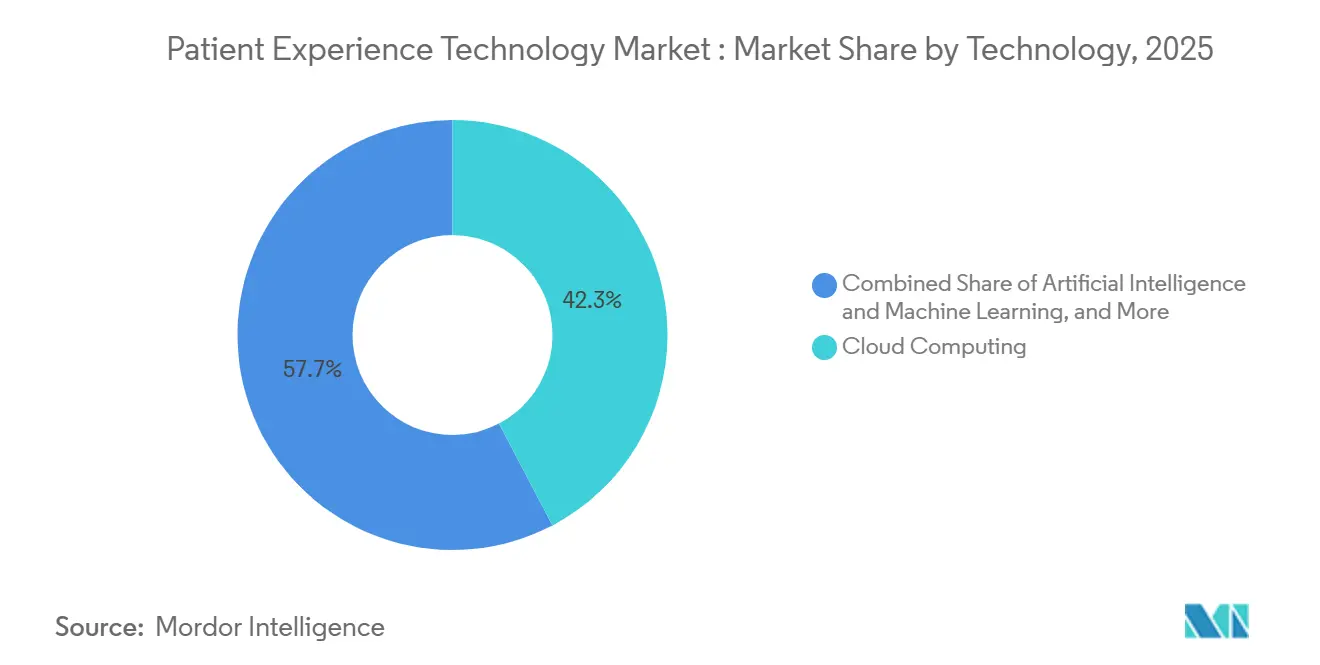

- By technology, cloud computing led with 42.31% share in 2025, while AI and machine learning is forecast to expand at a 14.24% CAGR through 2031 in the patient experience technology market.

- By application, patient communication and engagement represented 33.26% of revenue in 2025, while appointment management is projected to grow at a 14.78% CAGR through 2031 in the patient experience technology market.

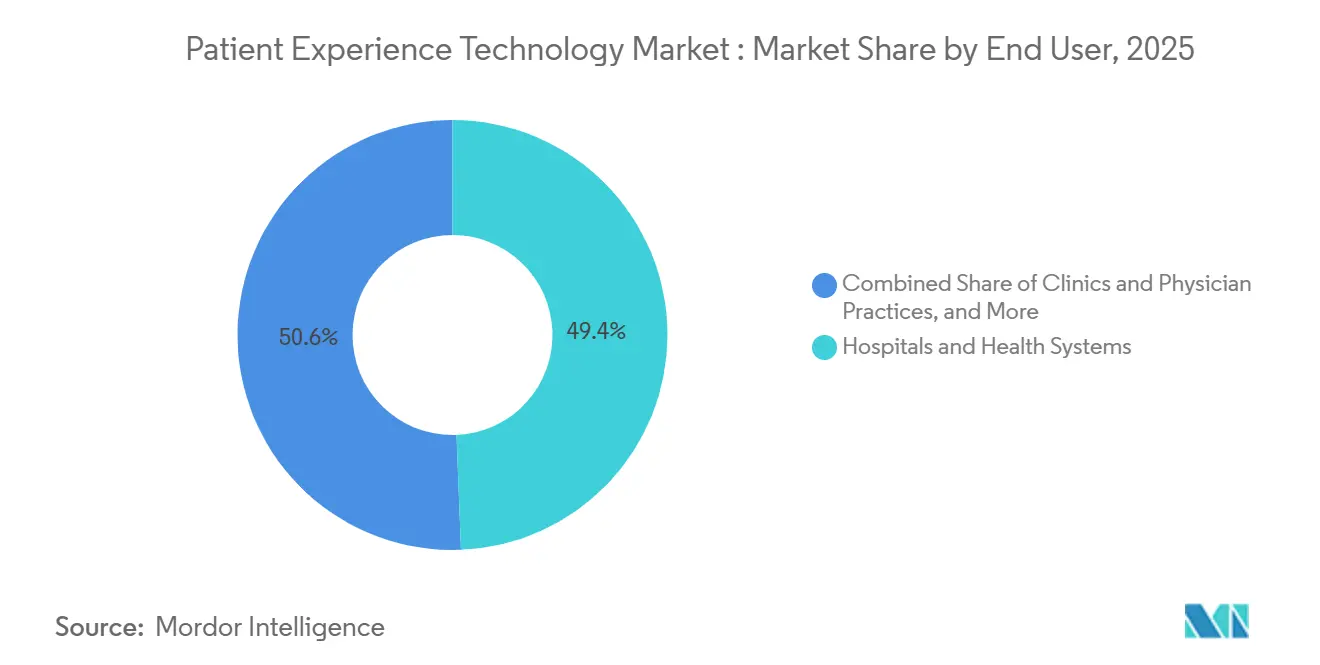

- By end user, hospitals and health systems held 49.37% of revenue in 2025, while clinics and physician practices are expected to advance at a 15.26% CAGR through 2031 in the patient experience technology market.

- By geography, North America captured 40.36% share in 2025, while Asia-Pacific is forecast to register the fastest CAGR at 16.58% through 2031 in the patient experience technology market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Patient Experience Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Digital Patient Access and Self-Service Workflows | +3.2% | Global, concentrated in North America and APAC | Short term (≤ 2 years) |

| Value-Based Care Incentives Linked to Patient Experience Scores | +2.4% | North America, expanding to EU | Medium term (2-4 years) |

| Expansion of AI-Enabled Patient Interaction and Triage | +2.8% | Global | Short term (≤ 2 years) |

| Rising Need to Reduce Contact-Center Dependency in Health Systems | +1.5% | North America and EU | Short term (≤ 2 years) |

| Growth of Closed-Loop Feedback Across Care Journeys | +1.1% | North America, APAC | Medium term (2-4 years) |

| Interoperability Pressure from EHR and Portal Consolidation | +1.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Digital Patient Access and Self-Service Workflows

Patients are now initiating a larger share of scheduling, follow-up, messaging, and records access through digital channels, and that is forcing providers to rebuild the access layer of care around self-service tools. A June 2026 study covering more than 2,000 hospitals and 47,000 clinics showed that portal messages increased 153% between 2020 and 2025, while phone calls fell 6% over the same period. The same study also noted that 30% of 140 million active Epic users sent a portal message to a clinician in the first quarter of 2025, which shows how quickly messaging has become part of routine care activity rather than a niche option. For the patient experience technology market, that behavior shift means digital traffic is not replacing every in-person encounter, but it is increasing the amount of work that happens between visits. Federal data exchange efforts are reinforcing this direction because TEFCA had surpassed 500 million exchanged records by February 2026, which supports more portable patient data and makes digital access expectations easier to meet across systems.[1]“Insights Condition, Individuals' Access to Electronic Health Information Through Certified Health IT v.4,”

Value-Based Care Incentives Linked to Patient Experience Scores

Payment design is making patient experience technology harder for hospitals to delay because patient satisfaction performance affects reimbursement in a direct way. CMS continues to withhold 2% of base Medicare inpatient payments and redistribute that pool through the Hospital Value-Based Purchasing Program, which keeps HCAHPS results tied to financial performance.[2]“HCAHPS: Patients' Perspectives of Care Survey,” The FY 2025 IPPS Final Rule also finalized modified HCAHPS scoring for FY 2027 through FY 2029 and confirmed that the updated survey will be integrated into VBP from the FY 2030 program year.[3]“FY 2025 Hospital Inpatient Prospective Payment System Final Rule,” That multi-year compliance path is compressing buying cycles in the patient experience technology market because providers are upgrading feedback, communication, and service recovery tools before the updated scoring regime becomes fully embedded. The same payment logic is widening beyond large inpatient hospitals, which supports demand from ambulatory providers and smaller care sites that increasingly need measurable patient engagement performance to support payer and contract relationships.

Expansion of AI-Enabled Patient Interaction and Triage

AI is moving from pilot use into routine front-end patient communication, which is raising the value of automation across triage, prep, billing support, and navigation. Oracle Health launched a new AI-driven EHR for ambulatory providers in August 2025 with voice-first interaction, semantic AI, and agentic capabilities, and the company said full acute care functionality is planned for 2026.[4]“Oracle Ushers in New Era of AI-Driven Electronic Health Records,” A July 2026 study in npj Digital Medicine found that conversational AI for pre-procedural patient preparation delivered patient satisfaction comparable to staff-delivered preparation, which supports broader use of AI for routine communication tasks. WHO Europe also reported in April 2026 that 63% of EU member states now use AI chatbots for patient engagement, which signals that the technology has moved into normal operating practice in many settings. In the patient experience technology market, that combination of provider adoption and clinical validation is shortening the path from symptom question to guided action, while making AI a core part of workflow design rather than a side feature.

Rising Need to Reduce Contact-Center Dependency in Health Systems

Health systems are under pressure to lower the volume of routine phone traffic because call-heavy models are costly, slow, and difficult to scale during scheduling spikes or post-discharge demand. As patients shift toward portals, text, and automated workflows, the patient experience technology market is increasingly centered on tools that can resolve simple requests without keeping staff tied to repetitive queue management. That shift matters because scheduling, intake, reminders, and billing questions can often be handled with consistent digital workflows, while staff time is better reserved for urgent cases and more complex coordination. Vendors that first solve scheduling deflection and self-service access are also gaining a path into adjacent workflows such as billing outreach, referral follow-up, and recovery support. This is turning contact-center automation into an entry point for broader platform expansion across the patient experience technology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Cost Across Fragmented Clinical Systems | -1.8% | Global, acute in North America | Short term (≤ 2 years) |

| Data Privacy, Consent Management, and Cybersecurity Exposure | -1.4% | Global | Medium term (2-4 years) |

| Workflow Adoption Resistance Among Clinicians and Front-Desk Staff | -1.0% | Global | Medium term (2-4 years) |

| Limited ROI Visibility for Smaller Provider Organizations | -0.7% | North America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Cost Across Fragmented Clinical Systems

Many providers still operate across multiple scheduling, billing, EHR, portal, and identity systems, and that makes deployment more complex than a simple software purchase. The integration burden is not limited to APIs because health systems also need patient identity alignment, consent controls, workflow mapping, and governance rules before a new platform can operate smoothly. In the patient experience technology market, vendors with certified or mature connections into major clinical systems have a practical advantage because they reduce implementation friction and shorten time to value. This issue is especially important for mid-sized providers that may be able to afford licensing costs but not the broader technical work that sits behind a full rollout. As a result, total ownership cost in the patient experience technology market often diverges sharply from subscription pricing, which slows some buying decisions and favors vendors with stronger ecosystem fit.

Data Privacy, Consent Management, and Cybersecurity Exposure

Patient engagement platforms collect communication preferences, appointment history, personal identifiers, and often some clinical context, which makes them sensitive systems from both a privacy and security standpoint. HHS showed the financial and operational risk clearly when it announced a USD 600,000 HIPAA settlement with PIH Health after a phishing-related breach and required a 2-year corrective action plan. That kind of enforcement raises the bar for vendors and providers that want to expand AI-driven communication without weakening transparency, consent management, or breach response controls. The patient experience technology market also faces added pressure because these platforms often sit across several systems and channels, which increases the number of points where data governance can fail. Smaller vendors can find it especially difficult to absorb the cost of compliance, security hardening, and model oversight while still competing on price.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Portals Anchor Demand as Digital Front Doors Redefine Access

Patient portals held 32.47% of the patient experience technology market share in 2025, while digital front door platforms are projected to post the fastest patient experience technology market size growth at 12.89% through 2031. Portals remain central because they already sit at the point where many patients look for test results, prescription refills, appointment details, and secure messaging. The strong installed base also means providers are more willing to expand around portals than replace them outright, especially when new tools can extend scheduling, intake, and messaging through familiar interfaces. In the patient experience technology market, that supports steady revenue from mature portal products even as buyer attention shifts toward broader front-end orchestration. The growth of digital front door platforms comes from the need to pull fragmented access functions into one consumer-facing layer rather than asking patients to move across separate systems for each task.

Patient communication platforms and appointment scheduling tools are gaining weight because providers now need to act on demand in real time instead of only responding after a patient reaches the clinic. Rising portal volume and the broader move toward between-visit engagement have increased the value of a unified workflow that can route requests, confirm appointments, and guide patients to the right level of care. That is why the patient experience technology market is rewarding vendors that can connect messaging, navigation, reminders, and access management in a single operating layer. The logic is straightforward because fragmented point tools create handoff gaps, while integrated access platforms reduce friction for both patients and staff. Over time, solution competition is likely to center less on standalone features and more on how well each platform manages the full entry path into care.

By Deployment Mode: Cloud Dominates While On-Premise Gains Specialized Ground

Cloud-based solutions accounted for 62.58% of the patient experience technology market size in 2025, while on-premise solutions are forecast to expand at a 13.61% CAGR through 2031. Cloud remains the leading deployment mode because providers value lower upfront infrastructure needs, faster update cycles, and easier scaling during spikes in messaging, scheduling, and outreach demand. Those benefits fit the day-to-day reality of the patient experience technology market, where interaction volumes can change quickly and where interface updates matter to patient satisfaction. Cloud deployment also supports multi-site organizations that want one common communication layer across hospitals, clinics, and affiliated physician groups. For many providers, the cloud model is the simplest path to rolling out new features without creating long local upgrade cycles.

On-premise growth remains strong because some health systems and public health environments still place a high priority on data residency, direct infrastructure control, and strict internal governance. Germany’s electronic patient record moved to an opt-out model in January 2025, which reflects how national policy is pushing digital engagement forward while keeping close attention on data handling rules. That tension keeps room open in the patient experience technology market for on-premise deployments where public cloud use is constrained or politically sensitive. Hybrid models also continue to make sense for providers that still rely on legacy local clinical systems but want cloud-native patient-facing tools at the outer layer. This means deployment competition is less about one model replacing another and more about matching architecture to the regulatory and operational profile of each buyer.

By Technology: AI and Machine Learning Moves from Pilot to Production

Cloud computing represented 42.31% of revenue in 2025, while AI and machine learning is set to grow at a 14.24% CAGR through 2031 in the patient experience technology market. Cloud computing still forms the technical base of many platforms because messaging, workflow orchestration, storage, and interoperability all depend on stable and scalable data infrastructure. Even so, buyer attention is shifting toward AI because automation now affects how patients ask questions, receive instructions, complete intake, and move through follow-up tasks. In the patient experience technology market, this makes AI and machine learning the clearest growth engine among technology layers. The important change is that providers increasingly expect systems to interpret context and manage multi-step work rather than only send reminders or trigger simple rules.

Oracle’s 2025 launch of an AI-driven EHR and its planned expansion into acute care in 2026 show that major platform suppliers now see AI-enabled interaction as a built-in requirement rather than an optional module. Clinical validation is also improving because npj Digital Medicine reported patient satisfaction results for conversational AI preparation that were comparable with staff delivery. WHO Europe’s finding that 63% of EU member states use AI chatbots for patient engagement confirms that adoption has spread across mainstream health systems. Experience analytics is also gaining relevance as providers try to move from delayed feedback review toward more predictive service design, which gives data and AI a more direct link inside the patient experience technology market. Together, these shifts show that production AI is becoming a structural layer of the patient experience technology market rather than a limited experiment.

By Application: Communication Leads as Appointment Automation Scales Rapidly

Patient communication and engagement accounted for 33.26% of revenue in 2025, while appointment management is projected to deliver the fastest patient experience technology market size growth at 14.78% through 2031. Communication remains the largest application because nearly every provider needs messaging, reminders, digital outreach, and service updates across the care path. At the same time, appointment management is accelerating because access bottlenecks, no-shows, waitlist handling, and rescheduling pressure all have immediate operating consequences. In the patient experience technology market, these two applications increasingly overlap because outreach, scheduling, and follow-up now happen in one connected workflow rather than separate systems. The commercial logic is strong because the same platform that sends a reminder can also recover an open slot, route a patient to another location, or trigger next-step communication.

Luma Health said its Spring 2026 release added operational AI capabilities for no-show recovery, clinical results follow-up, and automated waitlist outreach, and the company reported that its AI workflows had saved 2.5 million staff hours and handled more than 350,000 care-related next steps. Artera also said its Flows Agents completed 94% of conversations without staff intervention across 42 million annual sessions, which shows how much mature communication automation can absorb at scale. Patient satisfaction measurement is also moving toward faster and more continuous feedback loops because reimbursement and service recovery depend on more timely signals Care coordination and navigation should keep gaining importance as providers use automation to reduce routine load and reserve staff time for higher-value follow-up work. That pattern suggests application growth in the patient experience technology market will favor platforms that connect communication, access, and coordination instead of optimizing only one step.

By End User: Hospital Systems Anchor Revenue as Clinics Accelerate

Hospitals and health systems held 49.37% of revenue in 2025, while clinics and physician practices are expected to grow at a 15.26% CAGR through 2031 in the patient experience technology market. Hospitals remain the largest buyer group because they face the strongest reimbursement pressure, the largest communication volumes, and the broadest need for integration across departments and sites. Their scale also makes workflow delays and patient dissatisfaction more costly, which supports enterprise platform purchases. In the patient experience technology market, large health systems still anchor revenue because they buy across scheduling, portal, intake, outreach, and measurement functions at once. They also set the pace for vendor selection standards around interoperability, compliance, and service reliability.

Clinics and physician practices are growing faster because AI-enabled engagement tools are becoming easier to deploy without a large internal IT team. NextGen Healthcare introduced NextGen Navigator in September 2025, using Luma Health technology to answer inbound calls, manage scheduling, reduce abandonment, and escalate complex cases to staff when needed. Phreesia said in its fiscal 2026 results that its platform supported more than 180 million patient visits, which shows how deeply digital intake and engagement platforms have penetrated ambulatory workflows. Diagnostic and specialty settings also present room for expansion because they need frequent reminders, prep instructions, and follow-up communication but often still rely on manual processes. As these settings digitize, the patient experience technology market should see more spending from smaller care sites that need fast deployment and clear workflow payback.

Geography Analysis

North America held 40.36% of the patient experience technology market share in 2025. The region leads because the United States directly ties part of hospital reimbursement to patient experience performance, which keeps engagement technology close to revenue protection and service improvement priorities. Federal interoperability policy is also raising the operating baseline because the HTI-4 Final Rule established FHIR-based API certification criteria that support data access and exchange across the vendor ecosystem. This gives the patient experience technology market a stronger technical foundation in North America than in many other regions. Large provider systems and ambulatory networks also create a deep demand base for scheduling, intake, communication, and patient feedback tools.

Europe remains an important growth region because policy and digital health modernization continue to push providers toward better patient access and more connected records. Germany’s electronic patient record moved to an opt-out approach in January 2025, which marks a meaningful policy step toward broader digital participation. WHO Europe also reported that 63% of EU member states use AI chatbots for patient engagement, which shows that patient-facing automation is no longer confined to pilot programs. For the patient experience technology market, Europe offers a mix of strong public-sector demand, tighter governance expectations, and varied national implementation speeds. That creates room for both scaled platforms and country-specific deployment models.

Asia-Pacific is forecast to record the fastest patient experience technology market size growth at 16.58% through 2031. The region is benefiting from large-scale public digital health programs, rising patient volumes, and stronger demand for mobile-first access models. Providers across Asia-Pacific are also moving through different stages of adoption, which creates opportunities ranging from basic digital access layers to more advanced AI-enabled engagement. In the patient experience technology market, this keeps Asia-Pacific as the clearest high-growth geography even though maturity levels and procurement patterns differ widely across countries.

Competitive Landscape

The patient experience technology market has a concentrated top layer but remains fragmented across the mid-tier, where many vendors still focus on a narrow part of the care journey. A major strategic move came in May 2026 when Qualtrics completed its USD 6.8 billion acquisition of Press Ganey Forsta, combining broader experience management tools with a large healthcare-specific database across more than 41,000 facilities. That deal strengthens the role of data depth and predictive analytics in the patient experience technology market because it links patient experience measurement more closely with operational action. It also raises the competitive bar for vendors that only provide survey collection or isolated messaging tools. Scale now matters more because buyers increasingly want one platform that can connect access, communication, measurement, and workflow automation.

Another important shift is the expansion of large health IT platforms into patient-facing engagement functions. Oracle Health achieved CMS Aligned Network status in April 2026 and positioned itself to support standards-based data sharing across CMS networks and QHINs. Oracle had already launched its new AI-driven ambulatory EHR in August 2025, and its plan to add full acute care functionality in 2026 points to a broader strategy that joins clinical systems with patient communication and workflow tools. This matters in the patient experience technology market because native functionality from major platform vendors can reshape buying decisions for hospitals that prefer tighter integration. Vendors that are not embedded in core clinical workflows will need stronger specialization, faster deployment, or clearer ROI to defend their position.

Mid-scale specialists are still competitive when they solve a specific workflow gap with clear operating value. RevSpring’s September 2025 agreement to acquire Kyruus Health is a good example because it aims to combine provider data, search, scheduling, price transparency, and payments into one connected patient journey. Luma Health and NextGen Healthcare also show how workflow-focused automation is moving deeper into scheduling and contact-center activity at both health system and ambulatory levels. The patient experience technology market still has open space in areas such as post-acute outreach, multilingual engagement, and cross-payer coordination, but the direction of competition is clearly moving toward broader, better-connected platforms.

Patient Experience Technology Industry Leaders

Artera

Epic Systems Corporation

GetWellNetwork, Inc.

Medallia, Inc.

Oracle Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Qualtrics completed its USD 6.75 billion acquisition of Press Ganey Forsta, assembling the world's largest proprietary healthcare experience AI dataset across more than 41,000 healthcare facilities and the majority of US hospitals. The transaction, the largest technology acquisition in Utah history, enables the combined platform to shift patient experience management from retrospective survey measurement to predictive AI-driven simulation of patient behaviors and outcomes.

- April 2026: Luma Health's Spring 2026 release introduced new Operational AI capabilities, including conversational AI no-show recovery, automated clinical results follow-up, and batched waitlist outreach that fills open slots automatically. The platform's AI workflows had collectively saved 2.5 million staff hours and handled over 350,000 care-related next steps at the time of release.

- April 2026: Oracle Health achieved CMS Aligned Network status, enabling standards-based patient health data sharing across CMS networks and Qualified Health Information Networks (QHINs). Oracle simultaneously announced capabilities to eliminate paper-based check-in at the point of care, advancing its interoperability-as-a-platform strategy.

- September 2025: RevSpring announced a definitive agreement to acquire Kyruus Health, combining Kyruus's provider data, search, scheduling, and price transparency capabilities with RevSpring's patient engagement and payments platform. The acquisition targets creation of a unified digital experience from patient care-access search through to final payment settlement.

Global Patient Experience Technology Market Report Scope

As per the scope of the report, the patient experience technology market comprises digital solutions designed to improve patient interactions, accessibility, communication, and overall healthcare journey across care settings. It includes technologies such as patient portals, digital front-door platforms, patient communication systems, appointment scheduling solutions, feedback management tools, and AI-enabled engagement platforms. These solutions help healthcare providers enhance patient satisfaction, streamline access to care, and deliver more personalized, patient-centered healthcare experiences.

The patient experience technology market is segmented by solution type, deployment mode, technology, application, end user, and geography. By solution type, the market is segmented into patient portals, digital front door platforms, patient communication platforms, appointment scheduling and access management solutions, and others. By deployment mode, the market is segmented into cloud-based solutions, on-premise solutions, and hybrid solutions. By technology, the market is segmented into artificial intelligence and machine learning, cloud computing, data analytics and experience analytics, and others. By application, the market is segmented into patient communication and engagement, appointment management, patient satisfaction measurement, care coordination and navigation, and others. By end user, the market is segmented into hospitals and health systems, clinics and physician practices, diagnostic and specialty care centers, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Patient Portals |

| Digital Front Door Platforms |

| Patient Communication Platforms |

| Appointment Scheduling and Access Management Solutions |

| Others |

| Cloud-Based Solutions |

| On-Premise Solutions |

| Hybrid Solutions |

| Artificial Intelligence and Machine Learning |

| Cloud Computing |

| Data Analytics and Experience Analytics |

| Others |

| Patient Communication and Engagement |

| Appointment Management |

| Patient Satisfaction Measurement |

| Care Coordination and Navigation |

| Others |

| Hospitals and Health Systems |

| Clinics and Physician Practices |

| Diagnostic and Specialty Care Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Patient Portals | |

| Digital Front Door Platforms | ||

| Patient Communication Platforms | ||

| Appointment Scheduling and Access Management Solutions | ||

| Others | ||

| By Deployment Mode | Cloud-Based Solutions | |

| On-Premise Solutions | ||

| Hybrid Solutions | ||

| By Technology | Artificial Intelligence and Machine Learning | |

| Cloud Computing | ||

| Data Analytics and Experience Analytics | ||

| Others | ||

| By Application | Patient Communication and Engagement | |

| Appointment Management | ||

| Patient Satisfaction Measurement | ||

| Care Coordination and Navigation | ||

| Others | ||

| By End User | Hospitals and Health Systems | |

| Clinics and Physician Practices | ||

| Diagnostic and Specialty Care Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected growth outlook for patient experience technology through 2031?

The patient experience technology market is projected to grow from USD 0.79 billion in 2026 to USD 1.40 billion by 2031 at a 11.93% CAGR.

Which solution category leads revenue today?

Patient portals led with 32.47% share in 2025 because they remain the main digital access point for results, refills, and secure messaging.

Which application area is expanding the fastest?

Appointment management is forecast to grow at a 14.78% CAGR through 2031 as providers automate scheduling, no-show recovery, and waitlist handling.

Why does North America lead adoption?

North America held 40.36% share in 2025 because reimbursement rules, interoperability policy, and large provider networks support sustained digital engagement spending.

How is AI changing patient-facing workflows?

AI is moving into routine prep, navigation, and communication, and WHO Europe reported that 63% of EU member states now use AI chatbots for patient engagement.

Which end users are driving new expansion?

Hospitals and health systems remain the largest buyers at 49.37% share, while clinics and physician practices are growing faster at a 15.26% CAGR as tools become easier to deploy.

Page last updated on: