Patient Referral Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

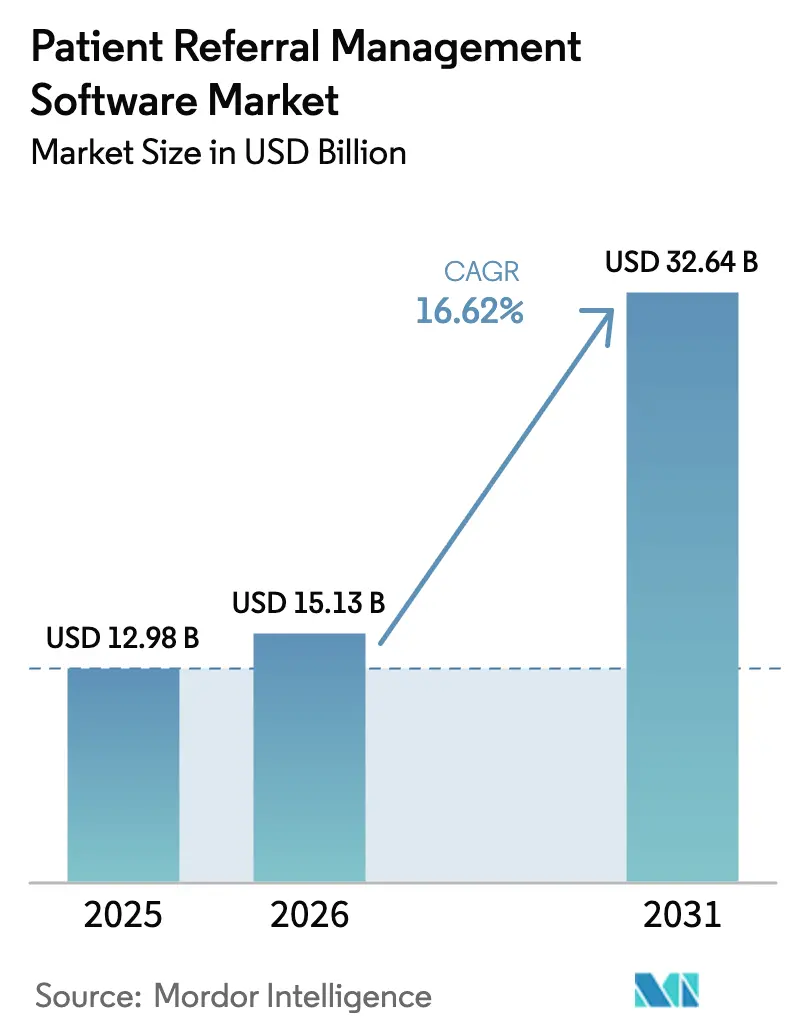

| Market Size (2026) | USD 15.13 Billion |

| Market Size (2031) | USD 32.64 Billion |

| Growth Rate (2026 - 2031) | 16.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Referral Management Software Market Analysis by Mordor Intelligence

The patient referral management software market size was valued at USD 12.98 billion in 2025 and estimated to grow from USD 15.13 billion in 2026 to reach USD 32.64 billion by 2031, at a CAGR of 16.62% during the forecast period (2026-2031). Strong demand for streamlined care coordination, mandatory interoperability rules, and the rapid digitization of health systems underpin this expansion. Digital transformation programs that embed AI routing and real-time data exchange have begun to reduce administrative waste, while the rising prevalence of chronic diseases keeps specialist referrals on a steep upward curve. Providers view modern referral software as a core requirement for value-based contracts that link reimbursement to outcomes. Competitive intensity remains moderate as incumbent EHR platforms defend installed bases against nimble AI-driven entrants.

Key Report Takeaways

- By delivery mode, web & cloud-based platforms commanded 79.10% of 2025 revenue and are expanding at the overall 16.62% patient referral management software market CAGR through 2031.

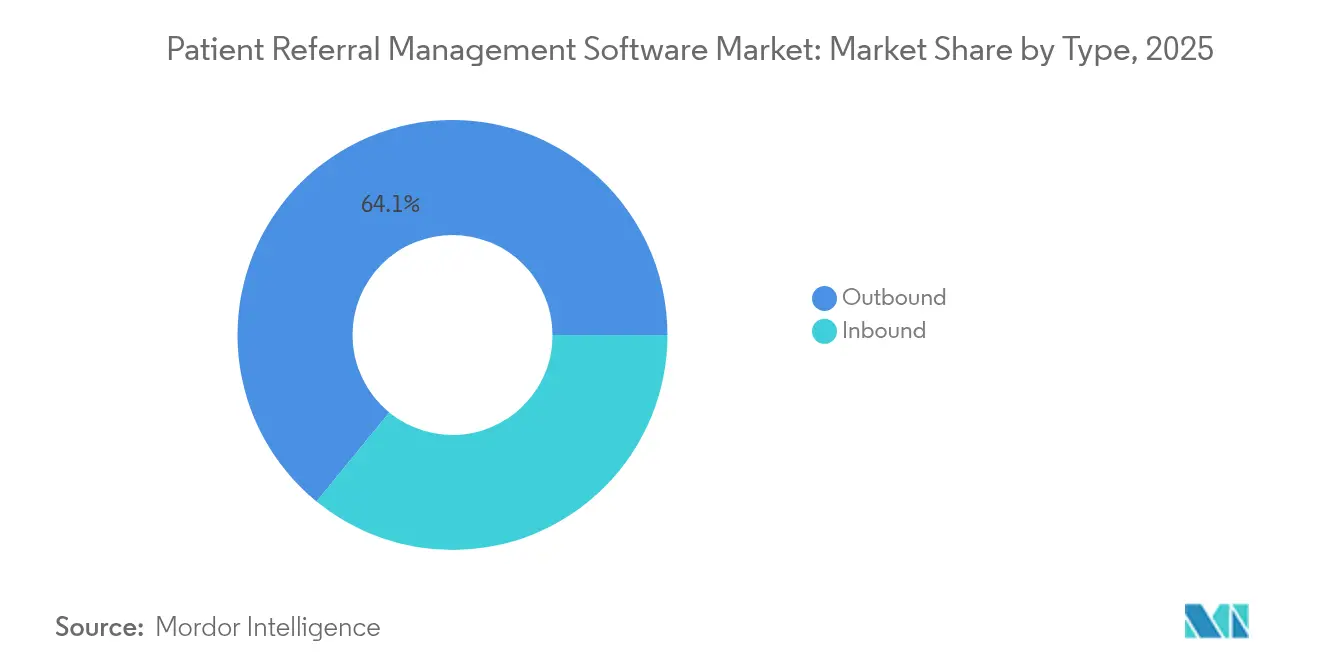

- By referral type, outbound workflows accounted for 64.10% of the patient referral management software market size in 2025 and are advancing at an 17.98% CAGR to 2031.

- By component, software held 71.80% of revenue and is rising at a 18.74% CAGR, highlighting demand for tightly integrated digital stacks.

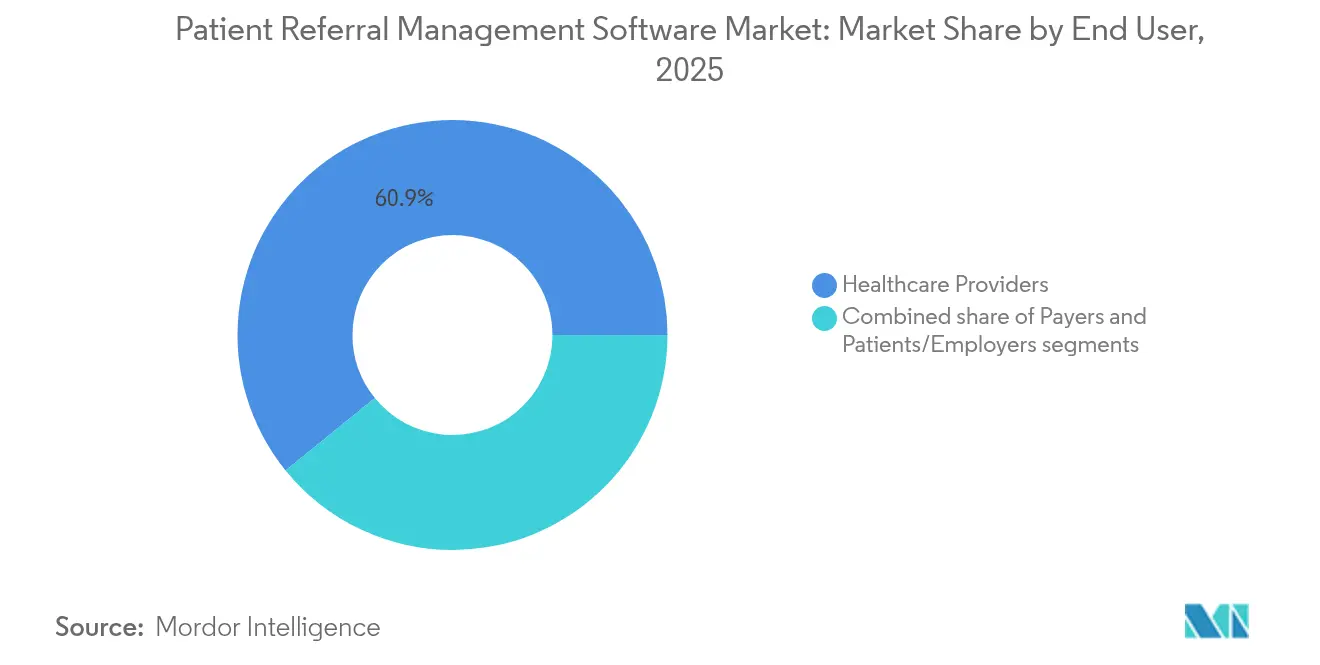

- By end user, healthcare providers led with 60.85% share in 2025, while the patients/employers segment posts the quickest 18.92% CAGR as consumer-centric tools proliferate.

- By referral specialty, specialist care captured 56.20% share, whereas rehabilitation & home-health referrals record the highest 18.15% CAGR over the forecast period.

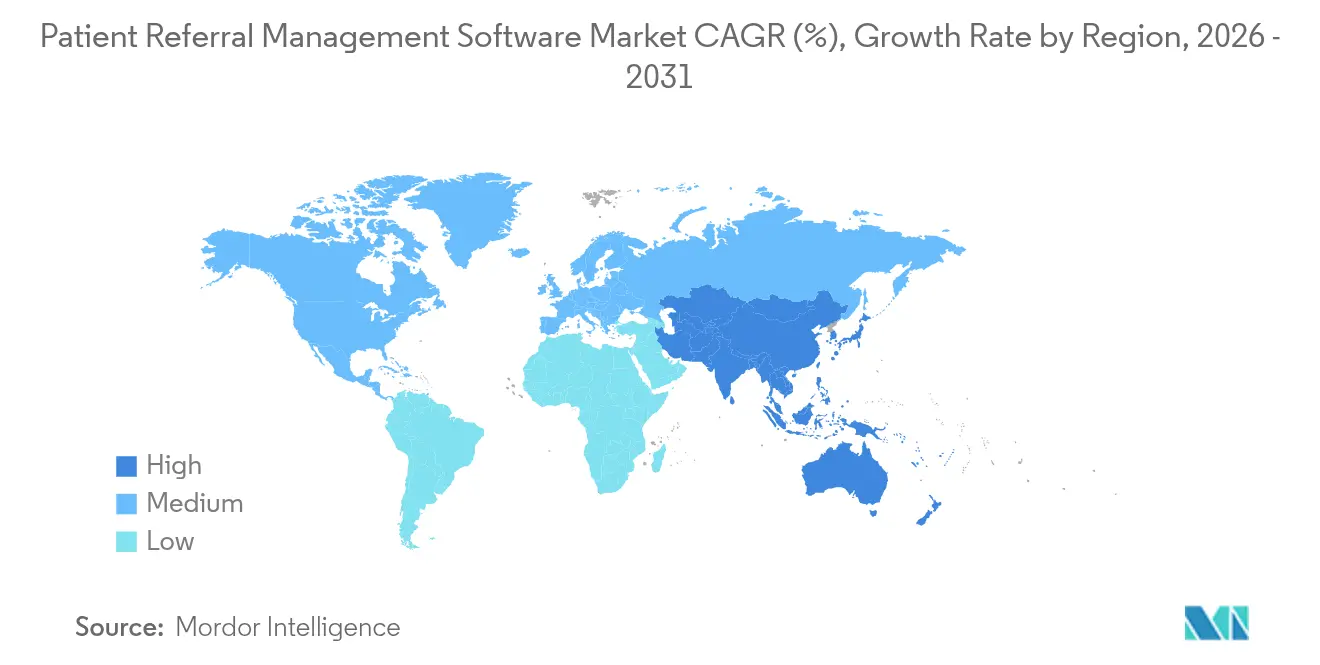

- By geography, North America retained 43.20% of global spend in 2025, while Asia-Pacific delivers the fastest 17.12% CAGR on the back of virtual primary care pilots and payer IT incentives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Patient Referral Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating healthcare digital transformation | +3.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing focus on care coordination efficiency | +2.8% | Global, especially United States | Short term (≤2 years) |

| Rising chronic disease prevalence requiring specialist referrals | +2.1% | Global, highest in aging economies | Long term (≥4 years) |

| Expansion of telehealth and virtual care ecosystems | +1.9% | North America and Asia-Pacific | Medium term (2-4 years) |

| Growing emphasis on value-based care and outcome tracking | +1.7% | North America, expanding to Europe and Asia-Pacific | Medium term (2-4 years) |

| Government incentives for health information exchange | +1.4% | North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerating Healthcare Digital Transformation

Hospital and clinic leadership continue to pour investment into referral automation, with Germany alone allocating more than USD 4 billion under the Hospital Future Act to modernize digital infrastructure. Epic Systems introduced over 100 AI features in 2024 that route referrals automatically and surface specialist availability without manual lookup. Historical data show that 45% of referred patients failed to attend their appointments, a gap now closing as AI tools send automated reminders and enable virtual triage. Hospitals deploying complete digital suites report 20% reductions in readmissions and 30% lower administrative expenses. Health systems thus view end-to-end referral platforms as foundational for boosting quality scores under value-based reimbursement programs.

Increasing Focus on Care Coordination Efficiency

The Medicare Shared Savings Program expanded in January 2025 to cover 53.4% of Traditional Medicare beneficiaries inside accountable care arrangements. These financial incentives pressure providers to eliminate fax-based handoffs that slow patient access. Modern platforms integrate insurance verification, real-time scheduling, and clinical decision support in a single workflow. Luma Health’s AI engine, for example, cut manual fax processing times to seconds and triggered automatic reminders that reduce leakage to competing systems. Closed-loop functionality also accelerates diagnosis and boosts referring-provider satisfaction, making efficiency a direct strategic lever.

Rising Chronic Disease Prevalence Requiring Specialist Referrals

Integrated care pathways for diabetes and cardiovascular disease now depend on sophisticated referral coordination, as multidiscipline teams manage therapy plans over long horizons. French data show 76% of general practitioners infrequently refer diabetes patients to specialists because of long queues, underscoring unmet need. Tele-rehabilitation trials for heart-failure patients delivered equivalent clinical outcomes to in-person programs, proving remote follow-up can be seamlessly embedded into referral platforms. Systems that layer risk stratification onto referral lists now report lower A1c levels across enrolled populations. As aging populations inflate chronic disease incidence, scalable referral management becomes critical for controlling long-term costs.

Expansion of Telehealth and Virtual Care Ecosystems

Nearly 20% of general-practice consultations in Australia took place remotely in 2024, saving travel time while keeping quality stable[1]Productivity Commission, “Advancing telehealth services,” pc.gov.au. Emergency departments have begun using natural-language processing to redirect low-acuity cases to urgent-care centers, achieving 84.1% compliance and trimming congestion. China’s pilot internet-based family-doctor model now links EHRs to teleconsults and referral scheduling, easing pressures on urban hospitals. Mobile-device prescribing inside EHRs lets clinicians monitor vitals remotely and receive automated alerts when thresholds are crossed. Such developments expand entry points into the patient referral management software market and create new pathways that must be orchestrated alongside traditional in-person services.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability challenges with legacy health IT systems | -2.3% | Global, acute in fragmented markets | Medium term (2-4 years) |

| Data security and privacy compliance burdens | -1.8% | Global, stricter in EU and United States | Short term (≤2 years) |

| Budget constraints among small and rural providers | -1.5% | Rural regions worldwide | Short term (≤2 years) |

| Organizational resistance to workflow change | -1.2% | Global, cross-provider settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Challenges with Legacy Health IT Systems

Legacy IT silos hinder seamless referral data flow when platforms cannot consume standards such as HL7 FHIR. Rural facilities in the United States show only 64% EHR adoption versus 74% in urban centers, widening digital gaps that obstruct patient transitions. Multi-site oncology centers in the Netherlands flagged 95 interface issues across DICOM and HL7 links, illustrating the integration complexity[2]IOP Publishing, “Interoperability issues in multi-site oncology,” iopscience.iop.org. Providers therefore face high integration costs that often stretch beyond annual budget cycles, slowing platform roll-outs and tempering near-term growth momentum.

Data Security and Privacy Compliance Burdens

The forthcoming 2025 HIPAA Security Rule update will require annual risk analyses, carrying an aggregate first-year price tag of USD 9 billion for U.S. providers[3]National Association of Counties, “HIPAA Security Rule cost impact,” naco.org. AI modules embedded inside referral workflows must navigate complex de-identification routines and heightened vendor-contract standards. The 21st Century Cures Act introduces monetary disincentives for information blocking, further tightening compliance oversight. Smaller practices lacking dedicated security teams may defer advanced referral projects, potentially widening the digital divide across provider tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Strategic Emphasis on Outbound Coordination

Outbound referrals held 64.10% of the patient referral management software market share in 2025, and the segment is forecast to post an 17.98% CAGR, making it the pivotal growth engine within the patient referral management software market. Providers leverage outbound workflows to retain visibility over patient journeys and to align specialists with value-based quality metrics. AI-enabled provider directories provide real-time match recommendations, reducing leakage and speeding up appointments.

Inbound referrals serve specialty groups seeking to maximize capacity through automated triage. Modern platforms rank incoming requests by clinical urgency and insurance fit, raising utilization without overbooking. Health systems report that balanced two-way orchestration lowers no-show rates and lifts referring-physician satisfaction. Together, these dynamics keep type-based innovation at the center of the wider patient referral management software market.

By Component: Software-First Adoption

Software applications accounted for 71.80% of revenues in 2025, reflecting decisive provider migration toward configurable platforms that sit on top of enterprise EHRs. This segment is projected to expand at a 18.74% rate through 2031, reinforcing its structural lead within the patient referral management software market. Health systems prefer single-sign-on modules that embed scheduling, prior authorization, and analytics in the same screen.

Services—including implementation, change management, and training scale in tandem with software rollouts. Providers often re-engineer clinical workflows and train multidisciplinary teams during go-live phases. Although the services' share is smaller, it remains indispensable for turning license purchases into measurable performance gains. The software-services mix thus underlines the platform orientation of the patient referral management software market.

By Delivery Mode: Cloud Acceleration

Web and cloud deployments captured 79.10% of total spend in 2025, demonstrating that scalability, real-time updates, and ease of integration outweigh concerns over off-premise hosting. Vendors push frequent upgrades that enhance AI matching and telehealth routing without downtime, a benefit difficult to replicate on local servers—cloud delivery, therefore, anchors the most significant slice of the patient referral management software market share.

On-premise systems persist inside government hospitals and academic centers that must meet stringent data sovereignty rules. Hybrid architectures, in which sensitive images remain onsite while referral metadata lives in the cloud, offer a transitional path. As more regulators endorse secure cloud frameworks, adoption barriers continue to erode, reinforcing SaaS dominance in the patient referral management software market.

By End User: Providers Still Dominate but Consumer Segments Surge

Hospitals, integrated delivery networks, and specialty clinics generated 60.85% of 2025 revenue, confirming that clinical organizations remain the locus of referral decision-making. Complex risk contracts make end-to-end visibility an operational necessity.

Patients and employers, though smaller today, exhibit a 18.92% CAGR and represent a pivotal demand frontier. Employer navigation programs now furnish staff with self-service referral portals that list cost and quality metrics. Payers also fund referral technologies to ensure network adequacy and to control out-of-network spending. This diversification broadens the addressable universe for the patient referral management software market.

By Referral Specialty: Specialist Care Retains Scale, Rehabilitation Leads Growth

Specialist care drew 56.20% of 2025 revenues, underscoring the high volume of cardiology, orthopedics, and oncology handoffs that require nuanced triage protocols. AI risk-scoring tools guide primary physicians to the correct subspecialist, raising throughput and optimizing clinic schedules.

Rehabilitation and home-health workflows are projected to grow 18.15% annually, buoyed by post-acute bundles that reimburse outcomes over episodes rather than on service counts. Remote monitoring devices feed data back to care teams, prompting dynamic referral updates. Diagnostic and imaging services also gain ground as providers adopt AI-driven image analysis that slots into referral algorithms. These specialty trends combine to broaden the clinical scope of the patient referral management software market.

Geography Analysis

North America controlled 43.20% of global revenue in 2025, thanks to federal interoperability mandates such as TEFCA and the Medicare Shared Savings expansion that tie payment to quality coordination. Epic Systems added 176 hospitals to its EHR roster during the year, pushing its domestic footprint to 42.3% of acute beds and reinforcing its influence over regional referral workflows. Canada anticipates annual savings of up to CAD 26 billion (USD 20 billion) from AI-enhanced digital health, a figure that underpins future referral platform funding. Mexico’s public-private telehealth pilots extend market reach but face infrastructure gaps that temper near-term growth.

Europe advances on the back of Germany’s EUR 4 billion Hospital Future Act grants that require patient portals by 2025. The European Health Data Space will standardize FHIR-based data exchange and open cross-border referral routes, fostering a single digital market for vendor platforms. The UK’s Booking and Referral Standard lets primary and acute providers share slots in real time, improving patient experience and reducing wait lists. France and Spain show unmet needs where long specialist queues depress referral volumes, indicating future upside.

Asia-Pacific posts the highest 17.12% CAGR through 2031, with China piloting virtual primary care that integrates specialist referrals via standardized APIs. India’s insurance-funded health stack embeds claims and referral metadata in unified records, spurring demand for cloud-first platforms that can scale nationwide. Australia’s My Health Record now connects allied providers to a single longitudinal chart, opening new referral orchestration points. Japan and South Korea leverage mature broadband and policy support to accelerate digital pathways, even though reimbursement frameworks differ across markets. Collectively, regional regulators view referral automation as central to aging-population care planning, validating long-run demand for the patient referral management software market.

Competitive Landscape

Market structure remains moderately concentrated, dominated by EHR titans yet open to disruption. Epic Systems links 625 hospitals to TEFCA-compliant exchanges and released more than 100 AI workflows during 2024, consolidating its role as default referral hub. Oracle Health lost 74 client hospitals as reliability concerns prompted some systems to reassess their roadmap.

Challengers raise sizable war chests to carve out workflow niches. Innovaccer closed a USD 275 million Series F in January 2025 to deepen AI risk models and payer-provider data pipes. Kyruus touts USD 196 million in venture backing and aligns accurate provider directory data with scheduling APIs that slot into large EHRs. Luma Health automates intake fax queues with computer vision that offsets staffing shortages, while Ribbon Health positions its data layer as the definitive provider identity graph.

White-space opportunities center on rural hospitals, specialty-specific modules, and international markets where local EHR penetration is lower. Vendors that deliver measurable throughput gains and prove cybersecurity compliance are best placed to outflank legacy systems. The competitive narrative therefore turns on speed of innovation and the ability to broker data across heterogeneous networks.

Patient Referral Management Software Industry Leaders

Epic Systems

Oracle Health (Cerner)

Altera Digital Health (Allscripts)

Kyruus

Conifer Health Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Epic Systems unveiled healthcare-specific ERP modules at HIMSS 2025 that integrate workforce, finance, and materials management with AI agents for routine tasks.

- January 2025: Innovaccer raised USD 275 million in Series F funding to expand utilization management and prior authorization tools while eyeing strategic acquisitions.

- December 2024: HEALWELL agreed to acquire Orion Health to combine AI capabilities with established health-information exchange infrastructure.

- August 2024: Epic Systems announced more than 100 new AI functions, including automated claims submission and patient messaging, across its EHR platform.

- April 2024: Kaiser Permanente and Geisinger combined to form Risant Health, a new entity focused on IT-enabled value-based care.

Global Patient Referral Management Software Market Report Scope

As per the report's scope, patient referral management software refers to a specialized digital tool designed to streamline and optimize the process of referring patients between healthcare providers, such as primary care physicians, specialists, hospitals, clinics, and other healthcare facilities. This software facilitates the efficient and effective transfer of patient information, medical records, and treatment plans from one healthcare provider to another, ensuring patient care coordination and continuity.

The patient referral management software market is segmented by type, deployment mode, end-user, and geography. By type, the market is segmented into inbound and outbound. In terms of deployment mode, the market is segmented into cloud & web-based, and on-premise. By end-user, the market is segmented into healthcare providers, payers, and other end-users. The market is segmented by geography into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the segments mentioned above.

| Inbound |

| Outbound |

| Software | Stand-Alone Referral Portals |

| Integrated EHR Modules | |

| Services |

| On-Premise |

| Web & Cloud-Based (SaaS) |

| Healthcare Providers | Hospitals & IDNs |

| Specialty Clinics & ASCs | |

| Federally Qualified Health Centers (FQHCs) | |

| Payers | Private Health Insurance |

| Public / Government Programs | |

| Patients / Employers |

| Specialist Care |

| Diagnostic & Imaging |

| Rehabilitation & Home-Health |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Inbound | |

| Outbound | ||

| By Component | Software | Stand-Alone Referral Portals |

| Integrated EHR Modules | ||

| Services | ||

| By Delivery Mode | On-Premise | |

| Web & Cloud-Based (SaaS) | ||

| By End User | Healthcare Providers | Hospitals & IDNs |

| Specialty Clinics & ASCs | ||

| Federally Qualified Health Centers (FQHCs) | ||

| Payers | Private Health Insurance | |

| Public / Government Programs | ||

| Patients / Employers | ||

| By Referral Specialty | Specialist Care | |

| Diagnostic & Imaging | ||

| Rehabilitation & Home-Health | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast revenue for the patient referral management software market in 2031?

The patient referral management software market is projected to reach USD 32.64 billion by 2031.

Which delivery mode leads current adoption?

Web & cloud-based platforms hold 79.10% share and dominate new deployments.

Which user segment is growing quickest?

The patients and employers segment is advancing at a 18.92% CAGR through 2031.

Why are outbound referrals important for providers?

Outbound workflows let providers guide patients to in-network specialists and meet quality targets tied to value-based contracts.

Which region is set to grow fastest?

Asia-Pacific shows the highest 17.12% CAGR through 2031 owing to virtual care pilots and payer-driven IT mandates.

How do interoperability rules affect market demand?

TEFCA and similar policies compel providers to invest in compliant platforms, driving sustained market growth.

Page last updated on: