Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

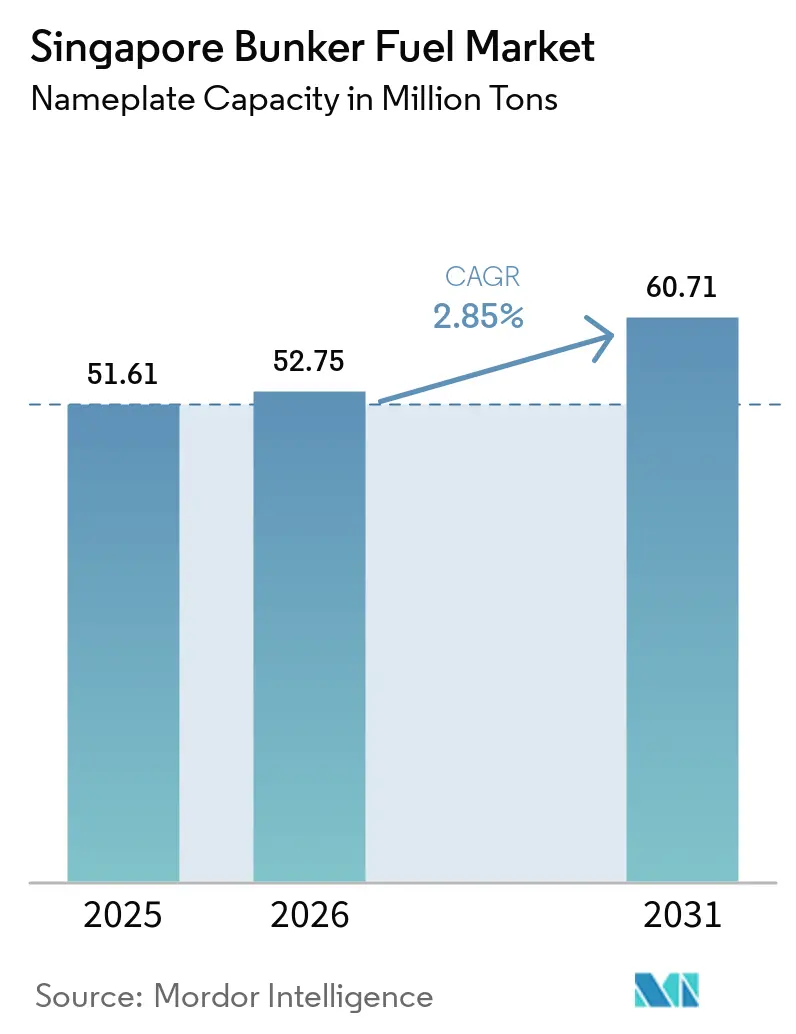

| Base Year Market Size (2025) | 51.61 Million tons |

| Market Volume (2026) | 52.75 Million tons |

| Market Volume (2031) | 60.71 Million tons |

| Growth Rate (2026 - 2031) | 2.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Bunker Fuel Market Analysis by Mordor Intelligence

The Singapore Bunker Fuel Market size in terms of nameplate capacity is projected to be 51.61 million tons in 2025, 52.75 million tonnes in 2026, and reach 60.71 million tonnes by 2031, growing at a CAGR of 2.85% from 2026 to 2031. This moderate trajectory conceals a strategic re-positioning from pure volume supplier to enabler of the maritime energy transition. Singapore’s record 54.92 MT of bunker sales in 2024 reflected Red Sea conflict diversions that routed Far East–Europe traffic around the Cape of Good Hope, adding roughly 8,500 nautical miles per voyage and lifting fuel demand. Government incentives are catalyzing liquefied natural gas (LNG), methanol, and biofuel uptake, while mandatory electronic bunker delivery notes (eBDNs) introduced in April 2025 compress information asymmetry and narrow bid-ask spreads. At the same time, scrubber-equipped vessels have revived high-sulfur fuel oil (HSFO) consumption whenever the HSFO–VLSFO price differential exceeds USD 150 per ton, underlining the market’s price-responsive nature. Competitive intensity remains elevated as oil majors, independent traders, and shipping-line captive suppliers vie for share in a hub where no single player exceeds 12% supply share.

Key Report Takeaways

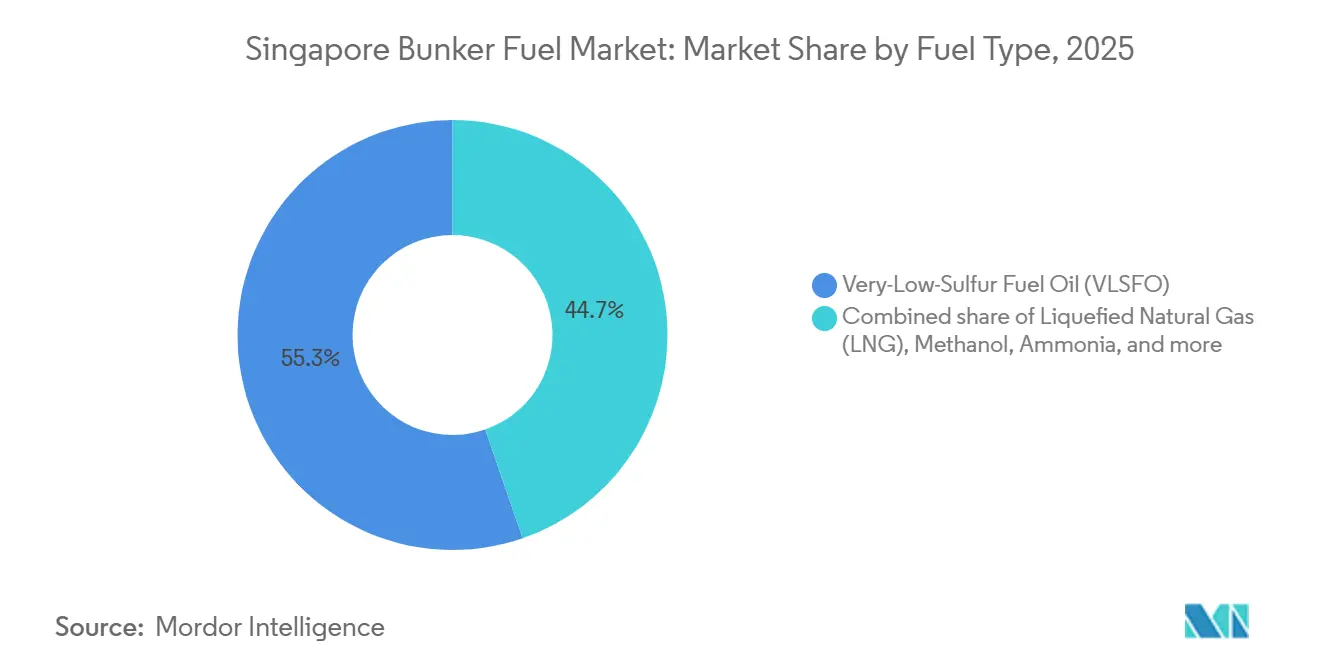

- By fuel type, very-low-sulfur fuel oil (VLSFO) led with a 55.3% share of the Singapore bunker fuel market in 2025, while LNG is forecast to grow at a 28.9% CAGR through 2031.

- By bunkering method, ship-to-ship operations held 41.1% of the Singapore bunker fuel market share in 2025, whereas LNG barge-to-ship deliveries are set to expand at a 28.1% CAGR between 2026 and 2031.

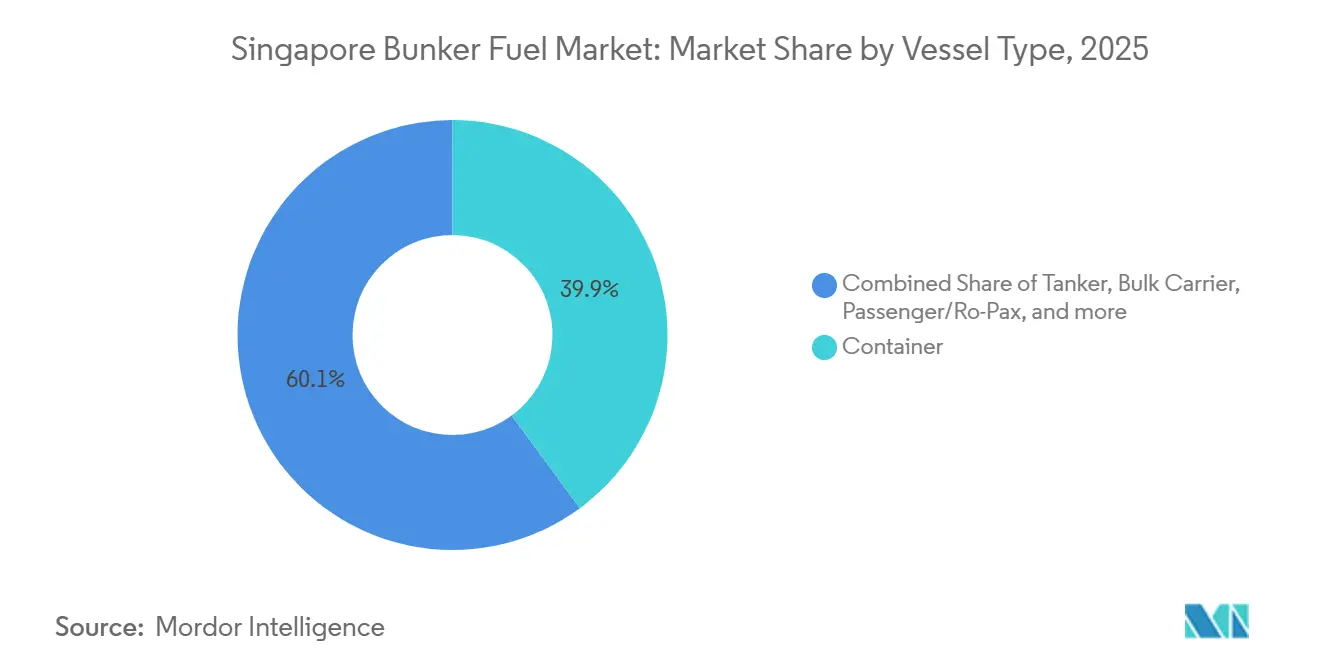

- By vessel type, container ships captured 39.9% of the Singapore bunker fuel market size in 2025, and passenger plus Ro-Pax ferries represent the fastest-growing segment at a 5.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Bunker Fuel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IMO 2020 sulfur-cap compliance boosting VLSFO demand | +0.6% | Global, with Singapore as primary APAC hub | Medium term (2-4 years) |

| Singapore's position as the world's largest bunkering hub | +0.5% | National, with spill-over to Southeast Asia | Long term (≥ 4 years) |

| Rising container throughput from e-commerce-driven trade | +0.4% | Global, concentrated in APAC-Europe lanes | Short term (≤ 2 years) |

| Government incentives for LNG bunkering infrastructure | +0.8% | National, with demonstration effects for regional ports | Medium term (2-4 years) |

| Emerging bio-/e-fuel bunkering pilots under Green Ship Programme | +0.3% | National, early-mover advantage in APAC | Long term (≥ 4 years) |

| Digital bunkering platforms lowering transaction costs | +0.2% | National, with potential replication in regional hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IMO 2020 Sulfur-Cap Compliance Boosting VLSFO Demand

The IMO’s 0.50% sulfur ceiling, active since January 2020, pushed VLSFO to a 55.3% share in 2025 and simultaneously triggered an HSFO rebound as scrubber economics improved when the HSFO–VLSFO spread touched USD 150-180 per ton in late 2024. Scrubber payback periods fell below 18 months for fuel-intensive VLCCs and capesize bulkers, motivating owners to fund retrofits even amid freight-rate volatility. Suppliers must now carry parallel VLSFO and HSFO inventories, inflating working-capital needs by roughly 15-20% compared with pre-2020 practice. The IMO’s 2023 GHG strategy requiring 5-10% emission cuts by 2030 accelerates interest in LNG and methanol, likely tapering VLSFO’s dominance beyond 2028. Maersk’s successful 2023 ship-to-ship methanol bunkering in Singapore shows the technical feasibility of alternatives, yet methanol’s lower energy density forces compromises on cargo capacity.

Singapore’s Position as the World’s Largest Bunkering Hub

The port sold 54.92 MT of fuel in 2024, equaling about 18% of global marine demand and benefitting from 24/7 operations and over 50 licensed suppliers.[1]Maritime and Port Authority of Singapore, “Port Statistics 2025,” mpa.gov.sg Red Sea diversions boosted Asia–Europe voyages via the Cape, adding 8,500 nautical miles and 33% more fuel burn, translating into an extra 2-3 MT of bunkering volume. Jurong Island’s land scarcity restricts storage expansion to roughly 20.5 million cubic meters, nudging some buyers toward Malaysia’s Port Klang and Indonesia’s Batam when space constraints pinch. Regional refinery build-outs in India and Vietnam could erode as much as 5-8% of Singapore’s share by 2030 unless the city-state sustains its alternative-fuel lead. The Green Ship Programme’s 2024 payouts for 460,000 ton of LNG and 880,000 ton of biofuels underscore the pivot to future fuels that aims to cement hub relevance over the long run.

Rising Container Throughput from E-Commerce-Driven Trade

Container throughput climbed to 41.12 million TEUs in 2024, up 3.8% year-on-year, as e-commerce favored frequent, smaller shipments and shortened dwell times. Average vessel calls increased 7% in 2024, heightening demand for rapid ship-to-ship deliveries of 1,000-3,000 ton in under six hours. Ultra-large container vessels (ULCVs) over 24,000 TEU now account for 15% of global capacity and require as much as 6,000 ton per call, reinforcing Singapore’s advantage in deep-water anchorages suited to concurrent multi-barge fueling. CMA CGM’s 153-vessel alternative-fuel orderbook and its first methanol-powered vessel call in March 2025 illustrate container lines’ early pivot toward dual-fuel fleets.[2]CMA CGM Group, “Alternative-Fuel Fleet Commitments,” cmacgm-group.com Geopolitical shocks remain a wildcard: the return of some Suez Canal traffic in 2025 clipped H1 bunker volumes by about 2-3%, showing the segment’s vulnerability to route shifts.

Government Incentives for LNG Bunkering Infrastructure

Expanded in 2024, the MPA’s Green Ship Programme reimburses up to 30% of incremental LNG bunkering costs and 50% for zero-carbon fuels, quadrupling LNG sales to 460,000 ton in 2024. FueLNG, Keppel, and Shell’s joint venture, deployed two 7,500-cubic-meter dual-fuel barges that cut waiting times by roughly 40%. Shell’s June 2024 purchase of Pavilion Energy has vertically integrated LNG supply chains from liquefaction to delivery, an edge that most regional competitors lack. The programme reduces perceived fuel-availability risk, encouraging Maersk’s order of 20 dual-fuel vessels aimed at 15-20% alternative-fuel consumption by 2030. Methane-slip concerns nevertheless spur interest in bio-LNG and synthetic variants that may feature in future incentive rounds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility compressing trader margins | -0.4% | Global, with acute impact on independent traders | Short term (≤ 2 years) |

| Decarbonisation shift toward ammonia & methanol alternatives | -0.3% | Global, with early adoption in Europe and Singapore | Long term (≥ 4 years) |

| Land-scarce storage expansion limitations | -0.2% | National, with competitive pressure from regional hubs | Medium term (2-4 years) |

| Stricter mass-flow-meter enforcement raising OPEX | -0.3% | National, with potential replication in APAC ports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility Compressing Trader Margins

Brent crude oscillated between USD 70 and USD 90 per barrel in 2024, squeezing bunker-trader margins to 3-5% from the 6-8% typical in 2020-2022 as suppliers struggled to pass cost swings to shipowners on quarterly contracts. Maersk’s average bunker expense fell to USD 569 per ton in Q1 2025, down 9% year-on-year, yet price transmission lagged crude by four to six weeks, spotlighting timing mismatches.[3]Maersk A/S, “Q1 2025 Interim Report,” maersk.com Independents lacking upstream integration must pre-fund inventories 30-45 days ahead, exposing them to spikes that can erase quarterly profit. An HSFO price rally in October 2024 widened the HSFO–VLSFO spread to USD 150-180 per ton, prompting a 15% uptick in scrubber-equipped calls but forcing suppliers to widen bid-ask spreads by 5-7% to manage risk. Hedging remains limited for smaller firms because margin calls tie up scarce working capital.

Decarbonisation Shift Toward Ammonia & Methanol Alternatives

The IMO’s 2050 net-zero target is redirecting capital toward ammonia and methanol, raising the risk that VLSFO and MGO assets become stranded IMO.ORG. MPA shortlisted Keppel and Sembcorp-SLNG-led consortia in July 2024 to develop at least 0.1 MT per annum of ammonia capacity, but commercial service is improbable before 2028, given safety and regulatory hurdles. Ammonia’s toxicity means bunkering barges need double-walled tanks and vapor detection, inflating capex by 40-50% over LNG vessels. Only three methanol-capable barges operate in Singapore today, and TFG Marine’s 2024 lease of four more vessels will take at least two years to commission.[4]TFG Marine, “Decarbonisation Update 2024,” tfgmarine.com Energy-density penalties, methanol holds 50% and ammonia 40% of conventional fuel’s energy per cubic meter, force vessel redesigns that sacrifice cargo space, delaying broad adoption until economics and regulations align.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Dual-Track Growth in Conventional and Alternative Fuels

The Singapore bunker fuel market size for very-low-sulfur fuel oil reached 29.2 MT in 2025, corresponding to a 55.3% share as vessels complied with the IMO 2020 sulfur cap. LNG volumes, though starting from a small base, are rising at a 28.9% CAGR through 2031 on the back of 460,000 tons sold in 2024 and the arrival of additional LNG bunker barges. HSFO rebounded in 2024 when the price gap to VLSFO widened, with scrubber-fitted ships capturing savings and cutting payback periods below 18 months. Methanol, biofuels, and ammonia collectively remain below 2% today, yet regulatory clarity and pilot infrastructure signal an inflection from 2028 onward.

Longer term, alternative fuels are expected to challenge VLSFO dominance as shipowners future-proof fleets against impending carbon levies. The Singapore bunker fuel market is therefore likely to exhibit a dual-track profile: stable demand for conventional fuels through 2028, overlapped by accelerating uptake of LNG, methanol, and advanced biofuels thereafter. Feedstock constraints on waste-oil-based biodiesel and safety questions around ammonia keep supply tight, but early movers in these niches could secure premium margins once regulation mandates zero-carbon fuels.

By Bunkering Method: Ship-to-Ship Retains Lead but LNG Barges Surge

Ship-to-ship services accounted for 41.1% of 2025 volumes, reflecting their ability to deliver 1,000-3,000 tons within six hours while vessels remain at anchorage. Port-to-ship methods, usually by truck or pipeline, cater to smaller craft but are losing ground as ultra-large vessels favor faster offshore fueling. The Singapore bunker fuel market share for LNG barge-to-ship deliveries is small today, yet expanding at a 28.1% CAGR, supported by FueLNG’s dual-fuel fleet that cuts waiting times by 40%. Portable tank solutions occupy a sub-3% niche because higher per-ton costs outweigh flexibility advantages.

Future sales mix will likely tilt further toward specialized LNG, methanol, and ammonia barges as dual-fuel vessels proliferate. Digital platforms that integrate real-time mass-flow-meter data and eBDNs favor ship-to-ship operations where connectivity is easiest. Complying with SS 648:2024, suppliers invested in cloud-linked meters and documentation to gain operational efficiency that small truck-based vendors struggle to match.

By Vessel Type: Containers Dominate, Passenger Ferries Accelerate

Container vessels consumed 39.9% of total fuel in 2025 as Singapore handled 41.12 million TEUs, and ultra-large container ships demanded single-call loads of up to 6,000 tons. Tankers and bulk carriers together represented roughly one-third of volumes, yet their slower adoption of alternative fuels reflects longer asset lives and lower freight earnings. The Singapore bunker fuel market size for passenger and Ro-Pax ferries was modest but is rising at a projected 5.2% CAGR as cruise lines refit fleets with LNG and methanol systems to meet emission-control-area rules.

This growth underscores a broader modal shift, where short-haul routes prioritize low-carbon options because storage requirements are less punitive. Operators such as Stena Line and Color Line are retrofitting ferries, providing a blueprint for Singapore–Indonesia and Singapore–Malaysia corridors. The segment’s rising share may diversify overall demand away from container reliance, cushioning the market against cyclical swings in global liner trade.

Geography Analysis

Singapore alone recorded 54.92 MT of sales in 2024, equating to about 18% of world marine fuel demand, thanks to its central position on Europe-Asia and transpacific routes. Red Sea hostilities diverted nearly one-third of Asia–Europe traffic around the Cape of Good Hope, temporarily adding 2-3 MT of incremental demand. Although partial resumption of Suez transit trimmed H1 2025 volume by 2-3%, the episode highlighted Singapore’s role as a shock absorber for route disruptions.

Regional refinery projects in India and Vietnam could capture 5-8% of Singapore bunker fuel market share by 2030 if they replicate the island’s service levels and alternative-fuel infrastructure. Jurong Island storage is near its 20.5 million-cubic-meter limit, and Vopak’s 2024 shift of tanks toward biofuels removed 3-5% of conventional capacity, encouraging some shipowners to top up in Port Klang or Batam when queues lengthen. However, Singapore’s first-mover advantage in LNG, methanol, and ammonia bunkering, plus mandatory digital transparency, underpins its premium hub status.

The Maritime and Port Authority’s plan to commission at least 0.1 MT per annum of ammonia capacity by 2028, coupled with steady incentives for LNG and biofuels, suggests that the Singapore bunker fuel market will remain the Asia-Pacific benchmark through the 2030s, even if incremental volume growth migrates to neighboring ports.

Competitive Landscape

Fragmentation defines the current supplier roster: Equatorial Marine Fuel, TFG Marine, and Sinopec headed the 2023 rankings, yet none exceeded a 12% share. Oil majors such as Shell, TotalEnergies, BP, and Chevron compete alongside traders like Vitol and Glencore and corporate arms such as Maersk Oil Trading. Shell’s June 2024 acquisition of Pavilion Energy has strengthened its LNG supply chain, while TotalEnergies delivered Singapore’s first B100 biodiesel cargo in August 2024, expanding its low-carbon footprint. Stricter mass-flow-meter and eBDN rules raise OPEX by 8-12% for smaller operators, signaling a likely reduction from more than 50 licensed suppliers today to perhaps 30-35 by 2030.

White-space opportunities revolve around methanol and ammonia. TFG Marine’s 2024 lease of four methanol barges positions it to serve Maersk’s growing dual-fuel fleet, while Chevron’s hybrid-electric barge offers emission savings during bunkering. Blockchain-based traceability pilots led by Maersk and IBM aim to verify biofuel sustainability, yet fewer than 5% of transactions use the technology today owing to interoperability hurdles. Scale players armed with digital platforms are therefore best placed to capture share as transparency erodes historical relationship moats.

Singapore Bunker Fuel Industry Leaders

Exxon Mobil Corporation

Shell plc

BP p.l.c.

TotalEnergies SE

PetroChina Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NYK Line, Golden Island, and Yara Clean Ammonia announced a partnership to develop low-carbon ammonia bunkering services in Singapore. This initiative seeks to establish a dependable ammonia fuel supply chain at the world's largest bunkering port, contributing to maritime decarbonization and strengthening Singapore's role as a hub for advanced marine fuels.

- March 2025: The Maritime and Port Authority of Singapore (MPA) rolled out Port Marine Circular No. 04 of 2025, outlining fresh mandates for conventional bunker tankers transporting biofuel blends and MARPOL Annex I cargoes in Singapore's port.

- March 2025: Singapore unveiled Technical Reference 129 (TR 129) for methanol bunkering. This initiative sets a framework to ensure the safe and efficient adoption of methanol as a sustainable marine fuel.

- March 2025: Singapore's Maritime and Port Authority (MPA) has begun accepting applications for licenses to provide methanol as a marine fuel. This move comes on the heels of Singapore finalizing its methanol bunkering licensing framework and standards.

Singapore Bunker Fuel Market Report Scope

Bunker fuel, often referred to as bunker oil, is a heavy, low-grade fuel primarily used to power large ships and select aircraft. The term "bunker" harks back to early steamships, where storage areas for coal were termed bunkers. Derived as a residual product from crude oil refining, bunker fuel is typically thick and tar-like, known in the industry as Heavy Fuel Oil (HFO). This viscosity necessitates heating for pumping. Traditionally high in sulfur content, the industry is witnessing a shift towards cleaner and lighter marine fuels.

The Singapore bunker fuel market is segmented by fuel type, bunkering method, and vessel type. By fuel type, the market is segmented into high-sulfur fuel oil (HSFO), very-low-sulfur fuel oil (VLSFO), ultra-low-sulfur fuel oil (ULSFO), marine gas oil (MGO), liquefied natural gas (LNG), methanol, bio-/synthetic fuels, ammonia, and other fuel types. By bunkering method, the market is segmented into ship-to-ship, port-to-ship, LNG barge-to-ship, and portable tanks and containers. By vessel type, the market is segmented into container vessels, tankers, bulk carriers, general cargo vessels, passenger/Ro-Pax vessels, and offshore and specialized vessels. For each segment, the market sizing and forecasts are provided on the basis of volume (million tons).

By Fuel Type

| High-Sulfur Fuel Oil (HSFO) |

| Very-Low-Sulfur Fuel Oil (VLSFO) |

| Ultra-Low-Sulfur Fuel Oil (ULSFO) |

| Marine Gas Oil (MGO) |

| Liquefied Natural Gas (LNG) |

| Methanol |

| Bio-/Synthetic Fuels |

| Ammonia |

| Other Fuel Types |

By Bunkering Method

| Ship-to-Ship |

| Port-to-Ship (Truck/Pipeline) |

| LNG Barge-to-Ship |

| Portable Tanks and Containers |

By Vessel Type

| Container |

| Tanker |

| Bulk Carrier |

| General Cargo |

| Passenger/Ro-Pax |

| Offshore and Specialized |

| By Fuel Type | High-Sulfur Fuel Oil (HSFO) |

| Very-Low-Sulfur Fuel Oil (VLSFO) | |

| Ultra-Low-Sulfur Fuel Oil (ULSFO) | |

| Marine Gas Oil (MGO) | |

| Liquefied Natural Gas (LNG) | |

| Methanol | |

| Bio-/Synthetic Fuels | |

| Ammonia | |

| Other Fuel Types | |

| By Bunkering Method | Ship-to-Ship |

| Port-to-Ship (Truck/Pipeline) | |

| LNG Barge-to-Ship | |

| Portable Tanks and Containers | |

| By Vessel Type | Container |

| Tanker | |

| Bulk Carrier | |

| General Cargo | |

| Passenger/Ro-Pax | |

| Offshore and Specialized |

Key Questions Answered in the Report

How large is the Singapore bunker fuel market in 2026?

It totals 52.75 MT in 2026 and is forecast to reach 60.71 MT by 2031, reflecting a 2.85% CAGR.

Which fuel commands the largest share of bunkering sales?

VLSFO leads with a 55.3% share in 2025, owing to IMO 2020 sulfur rules.

What fuel type is growing fastest?

LNG bunkering sales are rising at a 28.9% CAGR through 2031, supported by government incentives and new barge capacity.

Which bunkering method dominates operations?

Ship-to-ship fueling accounts for 41.1% of 2025 volume thanks to quick offshore transfers.

What is the main restraint on market growth?

Oil-price volatility squeezes trader margins, cutting profitability for suppliers lacking upstream integration.

Page last updated on: