Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

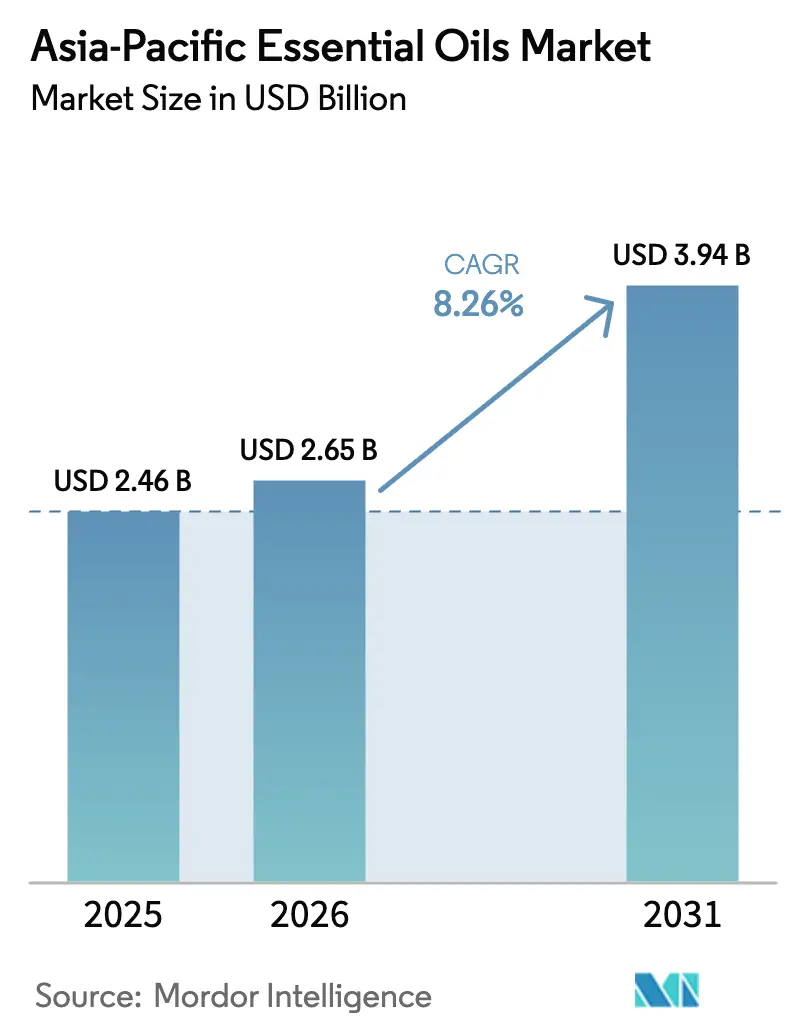

| Base Year Market Size (2025) | USD 2.46 Billion |

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 3.94 Billion |

| Growth Rate (2026 - 2031) | 8.26% CAGR |

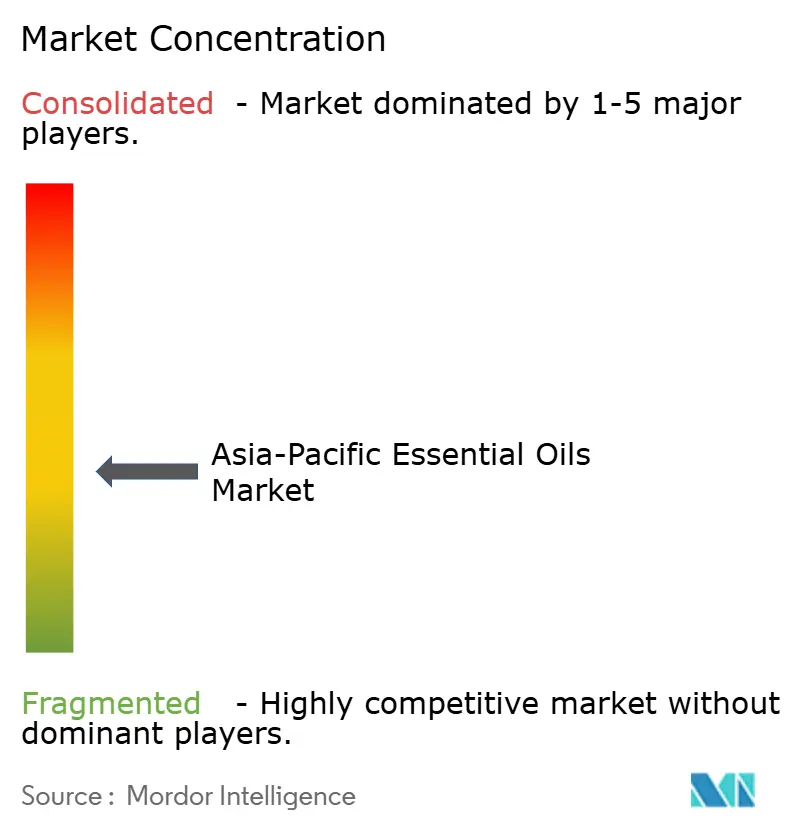

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Essential Oils Market Analysis by Mordor Intelligence

The Asia-Pacific Essential Oils Market size is expected to increase from USD 2.46 billion in 2025 to USD 2.65 billion in 2026 and reach USD 3.94 billion by 2031, growing at a compound annual growth rate (CAGR) of 8.26% over 2026-2031. This growth is influenced by multiple factors, including the implementation of stricter regulations on synthetic additives, a rise in consumer awareness regarding ingredient transparency, and the increasing institutional adoption of aromatherapy practices and clean-label products. China continues to dominate the market in terms of scale, driven by its production of citrus-peel and menthol-based essential oils. Meanwhile, Japan is emerging as the fastest-growing market in the region, primarily due to its rapidly aging population. Regulatory reforms, such as restrictions on the use of microplastics and requirements for fragrance disclosure, are further accelerating the transition toward plant-based inputs. Companies that operate with vertically integrated models, managing processes from farming and distillation to formulation, are achieving significant profit margins. Additionally, advancements in extraction technologies, including cold-press methods and supercritical carbon dioxide (CO₂) extraction, are reducing residue risks, enhancing the positioning of premium products, and encouraging the adoption of botanical solutions across various industries, including food, cosmetics, and household products.

Key Report Takeaways

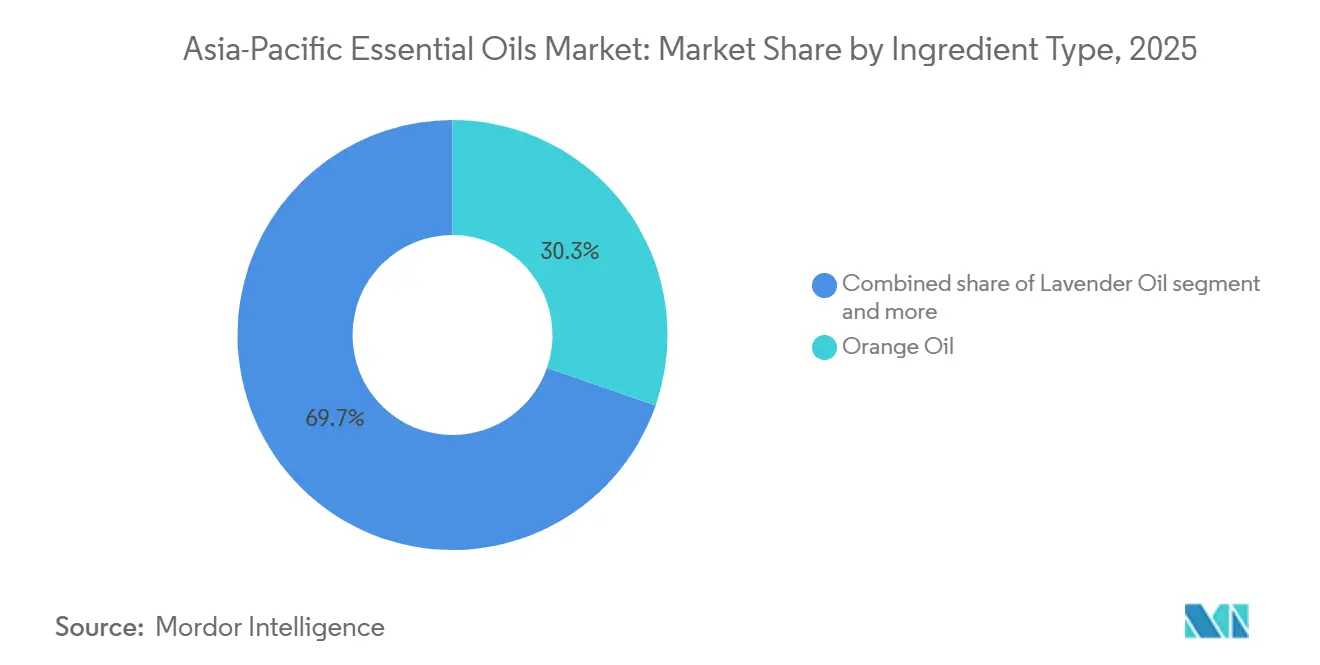

- By ingredient type, orange oil led with 30.31% of the Asia-Pacific essential oil market share in 2025, while lavender oil recorded the highest forecast growth at 8.72% CAGR through 2031.

- By source, flower extracts accounted for 35.08% of the Asia-Pacific essential oil market size in 2025 and are set to advance at a 9.00% CAGR to 2031.

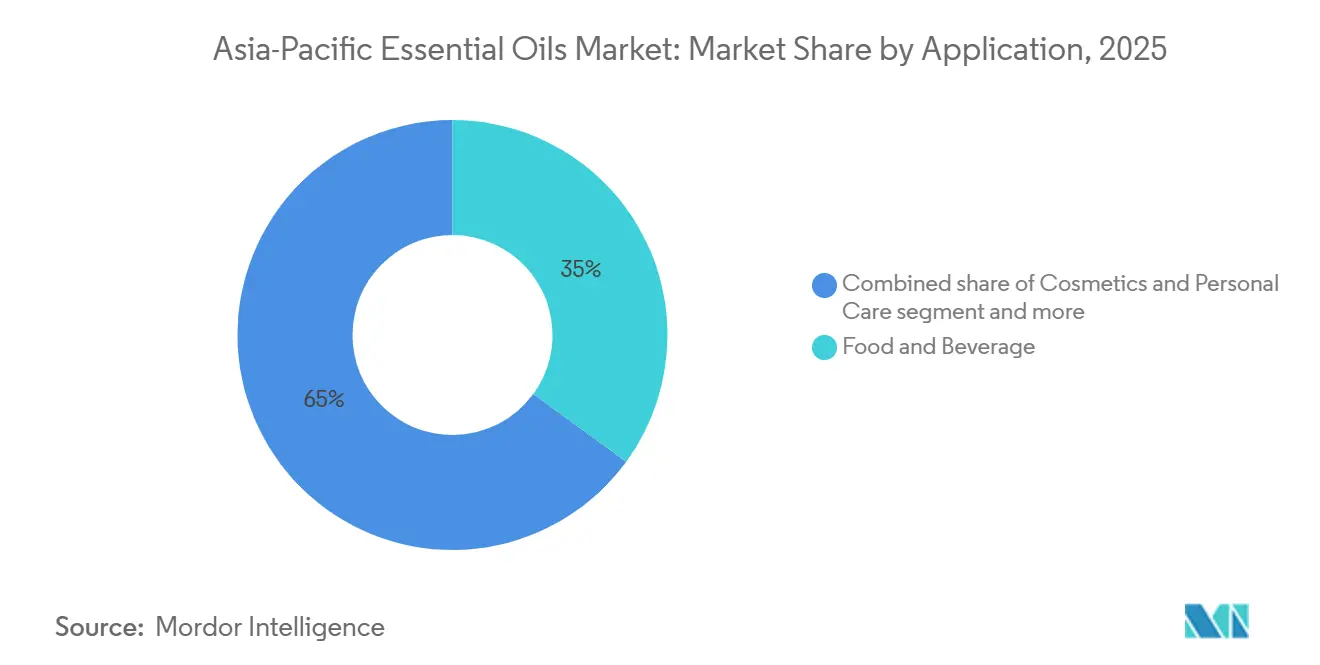

- By application, food and beverage represented 35.03% of segment revenue in 2025; cosmetics and personal care is poised to grow at a 9.62% CAGR through 2031.

- By geography, China commanded 37.21% of 2025 revenue, whereas Japan is expected to expand at a 9.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Essential Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for natural and organic ingredients across consumer products | +1.5% | China, India, Southeast Asia with spillover to Japan and Australia | Medium term (2-4 years) |

| Rapid expansion of aromatherapy and wellness practices | +1.3% | Japan, South Korea, urban centers in China and India | Long term (≥4 years) |

| Increasing use of essential oils in natural and clean beauty formulations | +1.4% | South Korea, Japan, China, with export-driven growth in Thailand | Medium term (2-4 years) |

| Rising awareness of therapeutic and functional benefits in traditional medicine | +1.0% | China, India, Indonesia, with Traditional Chinese Medicine and Ayurveda hubs | Long term (≥4 years) |

| Innovation in flavors for food and beverage applications | +1.2% | China, Japan, Australia, Singapore, with regulatory push in packaged goods | Short term (≤2 years) |

| Shift toward chemical-free household and home-care products | +0.9% | Australia, Singapore, Japan, with eco-certification uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing preference for natural and organic ingredients across consumer products

Consumer goods manufacturers across the Asia-Pacific region are making significant changes to their personal care, food, and household product lines by replacing synthetic fragrances and preservatives with steam-distilled essential oils. This transition has been driven by regulatory requirements in countries like China and South Korea, which now mandate full ingredient disclosure on cosmetic labels. In 2024, China's National Medical Products Administration expanded its cosmetic-ingredient negative list to include 27 synthetic musks and phthalates. As a result, brands have started using essential oils such as geranium, rose, and sandalwood in premium skincare products. Similarly, in 2025, India's Bureau of Indian Standards revised its specifications for organic essential oils under Indian Standard 210, introducing stricter residue limits for pesticides and heavy metals. While these changes have increased compliance costs, they have also provided a competitive edge for National Accreditation Board for Testing and Calibration Laboratories (NABL)-accredited distillers by ensuring higher quality standards. At the same time, there is a growing awareness among the middle class about ingredient safety. A survey conducted in 2025 found that 68% of urban Chinese consumers checked cosmetic labels for natural claims before making a purchase. This preference for natural ingredients is not limited to cosmetics but also extends to the food and beverage industry. For instance, clean-label mandates in Australia and Singapore have encouraged beverage manufacturers to replace artificial citrus flavors with cold-pressed orange and lemon oils, offering both flavor authenticity and marketing appeal. Additionally, organic certification schemes such as United States Department of Agriculture (USDA) Organic and European Union (EU) Organic are gaining popularity in export-oriented markets. Indian and Thai distillers are increasingly investing in these certifications to access premium price points in markets like Japan and Australia.

Rapid expansion of aromatherapy and wellness practices

The adoption of aromatherapy is growing significantly across Japan, South Korea, and urban China, driven by an aging population, workplace stress reduction programs, and its integration into traditional wellness practices. In Japan, the Ministry of Health, Labour and Welfare approved 12 new essential-oil-based aromatherapy products for over-the-counter sale in 2025, recognizing their role in reducing stress and improving sleep among the aging population. In South Korea, the wellness tourism sector, which attracted 4.2 million visitors in 2025, now includes essential-oil massages and diffuser experiences in 73% of spa facilities, incorporating oils such as lavender, eucalyptus, and peppermint into hospitality services. In China, the State Administration of Traditional Chinese Medicine endorsed aromatherapy as a complementary approach in its 2024 guidelines for integrative health clinics, prompting provincial governments to subsidize essential-oil diffusers in eldercare facilities across Jiangsu and Zhejiang provinces. Meanwhile, India's Ayurvedic wellness centers, which numbered over 8,000 in 2025, are increasingly incorporating steam-distilled oils such as sandalwood, vetiver, and jasmine into therapeutic treatments, supported by research from the Council of Scientific and Industrial Research's Central Institute of Medicinal and Aromatic Plants. Additionally, direct-selling networks such as doTERRA and Young Living expanded their distributor bases in Southeast Asia by 18% in 2025, leveraging social media education and home-party models to make aromatherapy more accessible beyond urban elite markets.

Increasing use of essential oils in natural and clean beauty formulations

Korean and Japanese beauty brands are incorporating essential oils into anti-aging serums, cleansers, and sheet masks to comply with microplastic bans and address consumer demand for transparent ingredient lists. In 2024, South Korea's Ministry of Food and Drug Safety banned microbeads in rinse-off cosmetics and extended the restrictions to leave-on products in 2025. This regulatory shift has led formulators to replace synthetic exfoliants and preservatives with essential oils such as tea tree, lavender, and rosemary, which provide antimicrobial and antioxidant benefits. In Japan, major cosmetic companies like Shiseido and Kao introduced 34 new essential-oil-infused product lines in 2025, focusing on cold-pressed yuzu, hinoki cypress, and camellia oils sourced from domestic farms to support "Made in Japan" premiumization strategies. Meanwhile, China's C-beauty market, which recorded a 22% year-on-year growth in 2025, prominently features essential oils as key ingredients in brands like Florasis and Proya, leveraging Traditional Chinese Medicine themes with ginseng, goji, and osmanthus extracts. In Thailand, contract manufacturers, responsible for 40% of ASEAN's private-label cosmetics, reported a 29% increase in essential-oil procurement in 2025, driven by export demand from Australia and Singapore, where clean-beauty retail channels have expanded shelf space for natural formulations. Regulatory standards such as ISO 9235 for oleoresins and ISO 4730 for essential-oil nomenclature provide quality benchmarks that facilitate cross-border trade, reducing formulation risks for multinational brands entering the region.

Rising awareness of therapeutic and functional benefits in traditional medicine

Traditional medicine systems in the Asia-Pacific region are increasingly adopting essential oils into clinical practices, driven by government support and research that highlights their antimicrobial, anti-inflammatory, and pain-relieving properties. The World Health Organization's 2024 Traditional Medicine Strategy emphasized essential oils as proven interventions for respiratory infections and stress-related disorders. This has encouraged health ministries in countries like China, India, and Indonesia to include aromatherapy in primary care guidelines [1]Source: World Health Organization, “WHO Traditional Medicine Strategy 2024-2034,” who.int. For example, India's Ministry of Ayurveda, Yoga and Naturopathy, Unani, Siddha, and Homeopathy (AYUSH) allocated INR 120 crore (USD 14.4 million) in 2025 to promote research on essential oils in Ayurvedic formulations. Research conducted at the All India Institute of Medical Sciences has shown the effectiveness of eucalyptus and peppermint oils in managing symptoms of chronic obstructive pulmonary disease. Similarly, China's State Administration of Traditional Chinese Medicine published a 2025 compendium that identified 47 essential oils for therapeutic use, such as sandalwood for reducing anxiety and ginger oil for improving digestion, enabling licensed Traditional Chinese Medicine practitioners to prescribe them. In Indonesia, the National Agency of Drug and Food Control approved 19 essential-oil-based Jamu products in 2025, combining traditional formulations with modern extraction methods to meet export standards for markets like Malaysia and Singapore. Clinical studies have further validated these developments, including a 2025 study in the Journal of Ethnopharmacology that demonstrated tea tree oil's effectiveness against antibiotic-resistant Staphylococcus aureus, which has supported its use in hospital infection-control protocols across Australia and New Zealand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs and volatile raw material prices | -1.1% | India, China, Indonesia, with climate-sensitive lavender and citrus regions | Short term (≤2 years) |

| Quality control problems, adulteration, and dilution in the supply chain | -0.8% | China, India, Southeast Asia, with spot-market concentration | Medium term (2-4 years) |

| Limited standardization of grades, specifications, and certification schemes | -0.6% | ASEAN economies, with fragmented national regulations | Long term (≥4 years) |

| Competition from cheaper synthetic fragrances and flavors | -0.9% | Indonesia, Thailand, Philippines, with price-sensitive consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs and volatile raw material prices

Essential-oil production continues to face significant cost pressures due to labor-intensive harvesting, energy-intensive distillation processes, and climate-induced yield variability, which disrupt supply chains and reduce margins for distillers. In 2024, lavender cultivation in China's Xinjiang region and India's Kashmir valley experienced yield declines of 18% and 23%, respectively, caused by unseasonal frost and erratic monsoon patterns. These factors drove spot prices for lavender oil from USD 45 per kilogram in January 2024 to USD 68 per kilogram by December 2025. Citrus-peel oil production, which depends on by-product streams from juice manufacturing, remains susceptible to fluctuations in fruit prices. A drought in 2025 in China's Jiangxi province reduced orange harvests by 14%, tightening the supply of cold-pressed orange oil and increasing prices by 22% year-on-year. Additionally, steam-distillation energy costs, which constitute 30 to 40% of production expenses, rose sharply in 2025. Natural gas and electricity tariffs increased by 12% and 9%, respectively, in India and Indonesia, further squeezing margins for small-scale distillers who lack access to renewable energy infrastructure. Labor scarcity adds to these challenges, particularly for crops like jasmine, rose, and ylang-ylang, which require 200 to 300 person-hours per hectare for hand-harvesting. Wage inflation in Thailand and Vietnam, where agricultural labor costs rose by 8% in 2025, forced some growers to abandon low-yield plots. These conditions benefit vertically integrated players who manage cultivation, distillation, and formulation processes, while creating significant barriers for new entrants and commodity traders reliant on spot markets.

Quality control problems, adulteration, and dilution in the supply chain

Adulteration remains a significant issue in the Asia-Pacific essential oil trade, with chromatography audits identifying synthetic additives, carrier-oil dilution, and species substitution that undermine product quality and erode brand trust. The International Organization for Standardization (ISO) Technical Committee 54, which oversees essential oil standards, reported 127 cases of adulterated lavender oil in 2024. These cases included samples blended with synthetic linalool and linalyl acetate to mimic authentic lavender profiles [2]Source: ISO Technical Committee 54, “Adulteration Reports 2024,” iso.org. Similarly, in 2025, the Bureau of Indian Standards (BIS) found that 34% of lemon oil samples tested contained added limonene or terpene fractions. This practice is primarily driven by price differences, as cold-pressed citrus oils are priced at USD 18 per kilogram, compared to isolated terpenes at USD 6 per kilogram. In China, spot markets in Guangzhou and Shanghai, which account for 40% of the regional essential oil trade, do not require third-party testing. This lack of regulation enables brokers to mix lower-cost oils, such as eucalyptus, into peppermint or spearmint without disclosure. Advanced detection methods like gas chromatography-mass spectrometry (GC-MS) and nuclear magnetic resonance (NMR) spectroscopy, which are highly effective in identifying adulteration, remain underutilized outside Australia and Japan due to the high cost of equipment, which exceeds USD 150,000 per laboratory. In India, the National Accreditation Board for Testing and Calibration Laboratories (NABL) accredited only 23 essential oil testing facilities as of 2025, which is insufficient to monitor the 4,800 distilleries operating in states such as Uttar Pradesh, Tamil Nadu, and Kerala. This gap in quality control reduces buyer confidence, particularly among multinational flavor and fragrance companies that require ISO 4730-compliant certificates of analysis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Citrus Dominance Meets Floral Acceleration

Advancements in cold-press extraction methods and the utilization of by-products have enabled orange oil to account for 30.31% of the ingredient type segment in 2025. Lavender oil, on the other hand, is projected to grow at a compound annual growth rate (CAGR) of 8.72% through 2031, driven by increased cultivation in China and India. Orange oil benefits from its integration with citrus juice production, where peel waste from China's 7.5 million metric tons of orange production in 2025 is used in cold-press mills. This process yields d-limonene-rich oil at a lower cost compared to standalone distillation methods [3]Source: USDA Foreign Agricultural Service, “China Citrus Annual Report 2025,” fas.usda.gov. Food and beverage applications account for 58% of orange oil consumption, with beverage manufacturers in Japan and Australia replacing synthetic citrus esters to comply with clean-label requirements. Lavender oil's growth is supported by expanded cultivation in Xinjiang, where 12,000 hectares began production in 2024 and 2025, and in Kashmir, where state subsidies facilitated the planting of 3,400 hectares. These developments have reduced import dependence and lowered procurement costs for domestic aromatherapy brands.

Peppermint oil and spearmint oil, primarily used in pharmaceutical and oral-care applications, are witnessing growth driven by increasing demand for menthol in India's cough-drop and analgesic-balm industries. Eucalyptus oil, sourced mainly from Australia's 28,000 hectares of plantation forests, is expanding due to its antimicrobial applications in household cleaners and pharmaceutical inhalants. Tea tree oil, a niche segment concentrated in New South Wales and Queensland, is growing as Korean and Japanese cosmetic brands include it in acne treatments and scalp-care products, bolstered by clinical studies demonstrating effectiveness against Propionibacterium acnes. Lemon oil, rosemary oil, and geranium oil support fragrance and flavor applications where distinct sensory profiles command premium pricing in specialized formulations.

By Source: Flower Extraction Leads on Premium Positioning

Flower-based sources accounted for 35.08% of the source segment in 2025 and are projected to grow at a CAGR of 9.00% through 2031. This growth is attributed to advancements in steam-distillation efficiency and the premium pricing of extracts such as rose, jasmine, and ylang-ylang. Rose oil, requiring 4,000 kilograms of petals to produce 1 kilogram of oil, is priced at over USD 300 per kilogram, making it a luxury ingredient in high-end perfumery and anti-aging cosmetics. In 2025, India's Kannauj region and China's Gansu province collectively produced 2,800 kilograms of rose oil, utilizing solar-powered distillation units that reduced energy costs by 18% while maintaining the ester profiles demanded by European and Japanese buyers. Jasmine oil, harvested at night to preserve its volatile compounds, is used in perfumery and aromatherapy, with Thailand and India exporting 1,200 kilograms in 2025 at an average price of USD 180 per kilogram. Ylang-ylang oil, distilled in Indonesia and the Philippines.

Leaf-based sources, including eucalyptus, tea tree, and peppermint, constituted a significant portion of the segment and are experiencing notable growth. This growth is supported by Australia's plantation-forestry model, which ensures consistent yields and facilitates mechanized harvesting. Bark-based sources, primarily cinnamon from Indonesia and Sri Lanka, accounted for a smaller portion of the segment and are growing steadily, driven by their use in food flavoring and pharmaceutical applications. Root-based sources, such as vetiver and ginger, represented another portion of the segment and are expanding, although growth is limited by labor-intensive harvesting processes and multi-year cultivation cycles. Other sources, including seeds, peels, and resins, made up the remaining portion of the segment. Oils such as nutmeg, clove, and frankincense serve niche markets in fragrance and traditional medicine applications.

By Application: Food Maturity Versus Cosmetics Acceleration

In 2025, food and beverage applications accounted for 35.03% of the application segment, driven by clean-label mandates in packaged snacks and beverages. However, cosmetics and personal care applications are projected to grow at a compound annual growth rate (CAGR) of 9.62% through 2031, outpacing other end-use segments. This growth is attributed to Korean and Japanese brands reformulating anti-aging serums with tea tree, lavender, and geranium oils to comply with microplastic bans. In China, beverage manufacturers, who produced 180 million liters of flavored sparkling water in 2025, transitioned from synthetic citrus esters to cold-pressed orange and lemon oils due to a 2024 regulation requiring "natural flavor" claims to be substantiated with botanical extracts. Japan's functional beverage market, valued at USD 8.2 billion in 2025, incorporated peppermint and ginger oils into energy drinks and wellness shots, leveraging their thermogenic and digestive properties to differentiate from caffeine-based formulations. Australia's craft beverage segment, which grew by 31% in 2025, utilized essential oils in botanical gins, kombucha, and cold-brew coffee, with distillers sourcing native lemon myrtle and Tasmanian pepperberry oils to create terroir-driven flavor profiles.

Aromatherapy applications, including diffusers, massage oils, and spa treatments, captured 22% of the segment in 2025 and are expected to grow at a CAGR of 8.9%, driven by Japan's aging population and South Korea's wellness tourism sector. Pharmaceutical applications, which include cough syrups, analgesic balms, and antimicrobial ointments, held an 18% share of the segment in 2025 and are projected to grow at a CAGR of 7.7%. This growth is supported by clinical validation of eucalyptus and tea tree oils in respiratory and dermatological therapies.

Geography Analysis

China is expected to lead the regional essential oils market with a 37.21% share in 2025. This leadership is attributed to its dual role as the largest producer and consumer of essential oils in the region. The country's production is supported by citrus-peel processing activities in Jiangxi and Hunan provinces. A significant portion of the locally produced essential oils is utilized by the domestic cosmetics market, which continues to grow steadily. Additionally, food and beverage applications accounted for a notable share of consumption, driven by clean-label regulations that require the use of natural flavoring in packaged goods. Furthermore, the State Administration of Traditional Chinese Medicine in China included aromatherapy as a complementary modality in its 2024 guidelines for integrative health clinics, encouraging provincial governments in Jiangsu and Zhejiang provinces to subsidize essential-oil diffusers for eldercare facilities.

Japan is projected to exhibit the fastest growth in the regional essential oils market, with a compound annual growth rate (CAGR) of 9.43% through 2031. This growth is supported by demographic trends, as a significant portion of Japan's population was aged 65 and older in 2025. The aging population has driven demand for aromatherapy products that address issues such as sleep disorders, cognitive decline, and chronic pain. In 2025, the Ministry of Health, Labour and Welfare approved 12 new essential-oil-based aromatherapy products for over-the-counter sale, recognizing their effectiveness in reducing stress and improving sleep. Additionally, Japan's cosmetics industry, which generated substantial revenue in 2025, has increasingly incorporated essential oils such as cold-pressed yuzu, hinoki cypress, and camellia oils into anti-aging serums and cleansers. These efforts align with "Made in Japan" premiumization strategies, which emphasize high-quality, locally sourced ingredients.

India accounted for a significant share of essential oil production in 2025, primarily due to its menthol and mint-oil production in Uttar Pradesh, which supplied a majority of the global demand for menthol. Despite this strong production capacity, the domestic essential-oil market in India remains underpenetrated, presenting opportunities for further growth and development. In 2025, India’s menthol production, along with other essential oils, contributed to a total output of 18,400 metric tons. The country’s production capabilities highlight its potential to expand its presence in the global essential oils market, particularly as demand for natural and sustainable products continues to rise.

Competitive Landscape

The Asia-Pacific essential oil market is moderately fragmented, comprising multinational corporations, regional distillers, and small-scale producers. Prominent players include multinational flavor and fragrance companies such as Givaudan SA, Symrise AG, and Takasago, along with direct-selling networks like doTERRA International, LLC and Young Living. Regional distillers, including Synthite Industries and VedaOils, as well as numerous small-scale producers in countries such as China, India, and Indonesia, further enhance the market's diversity. Multinational companies often adopt vertical integration strategies, overseeing the entire supply chain from upstream cultivation through contract farming to midstream distillation in owned facilities and downstream formulation. For instance, Givaudan's 2025 acquisition of a 40% stake in a Chinese lavender cooperative in Xinjiang secures an annual supply of 1,200 metric tons.

Direct-selling companies like doTERRA and Young Living adopt asset-light models, outsourcing distillation to third-party processors while focusing on distributor recruitment and consumer education. In 2025, doTERRA's distributor base in the Asia-Pacific region grew by 18%, reaching 420,000 members across Japan, South Korea, and Australia. Meanwhile, Young Living introduced 14 new product SKUs in Malaysia and Singapore, incorporating essential oils into household cleaners and personal-care products. Similarly, Symrise expanded its Indonesian clove-oil sourcing network to include 800 smallholder farms, integrating agronomic support and quality assurance to maintain consistent volume and purity. These strategies highlight the diverse approaches adopted by companies to strengthen their market presence.

Regional distillers differentiate themselves through organic certification, terroir branding, and positioning their products for therapeutic benefits. For instance, Synthite Industries achieved USDA Organic and European Union (EU) Organic certifications in 2025 for its mint and spice-oil operations in Kerala. This accomplishment not only highlights product quality but also enables premium pricing in export markets. The market is also witnessing emerging opportunities, such as biotechnology-derived essential-oil analogs. Fermentation platforms can produce rose and sandalwood molecules at costs 40% lower than traditional botanical extraction methods. Additionally, precision agriculture is gaining traction, with Indian and Chinese growers utilizing technologies like soil-moisture sensors and drone-based pest monitoring. These advancements have led to stabilized yields and a 15% reduction in input costs, enhancing efficiency and sustainability in the region.

Asia-Pacific Essential Oils Industry Leaders

doTERRA International, LLC

Young Living Essential Oils, LC

Ultra International

Givaudan SA

Symrise AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Young Living launched Wyld Notes, a sister company that offered five 100% natural fine fragrances and a first-of-its-kind affiliate program. The hybrid model complemented Young Living’s direct selling system, targeted Millennials and Gen Z, and expanded its reach into the fast-growing fine fragrance market.

- October 2024: BO International, based in Gurugram, India, was awarded Kosher certification by SM Certification Services. This certification recognized the company's compliance in manufacturing essential oils, carrier oils, and personal care products, ensuring adherence to Kosher standards and quality requirements.

- April 2024: BMV Fragrances Pvt. Ltd., Noida, India, received HACCP certification from United Kingdom Global Certification for manufacturing and supplying perfumery compounds, natural and synthetic essential oils, resinoids, and absolutes.

Asia-Pacific Essential Oils Market Report Scope

Essential oils are liquid extracts derived from various beneficial plants and other sources through the distillation process. The Asia-Pacific Essential Oils Market is categorized based on ingredient type into lavender oil, orange oil, eucalyptus oil, peppermint oil, spearmint oil, lemon oil, rosemary oil, geranium oil, tea tree oil, and other product types. By source, the market is segmented into flowers, leaves, bark, roots, and others. Based on application, the market is divided into food and beverages, aromatherapy, pharmaceuticals, cosmetics and personal care, and other application types. Geographically, the market is segmented into China, India, Japan, Australia, Indonesia, South Korea, Thailand, Singapore, and the rest of Asia-Pacific. The market sizing has been done in value terms in USD and volume in liters for all the abovementioned segments.

By Ingredient Type

| Lavender Oil |

| Orange Oil |

| Eucalyptus Oil |

| Peppermint Oil |

| Spearmint Oil |

| Lemon Oil |

| Rosemary Oil |

| Geranium Oil |

| Tea Tree Oil |

| Other Oils |

By Source

| Flowers |

| Leaves |

| Bark |

| Roots |

| Others |

By Application

| Food and Beverage |

| Aromatherapy |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Others |

By Geography

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Ingredient Type | Lavender Oil |

| Orange Oil | |

| Eucalyptus Oil | |

| Peppermint Oil | |

| Spearmint Oil | |

| Lemon Oil | |

| Rosemary Oil | |

| Geranium Oil | |

| Tea Tree Oil | |

| Other Oils | |

| By Source | Flowers |

| Leaves | |

| Bark | |

| Roots | |

| Others | |

| By Application | Food and Beverage |

| Aromatherapy | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Others | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific essential oil market in 2026?

The Asia-Pacific essential oil market size is USD 2.65 billion in 2026 and is forecast to reach USD 3.94 billion by 2031.

Which ingredient holds the largest share of sales?

Orange Oil leads, accounting for 30.31% of 2025 revenue.

What is the fastest-growing application for essential oils?

Cosmetics and personal care products are set to expand at a 9.62% CAGR through 2031.

Which country is growing quickest?

Japan posts the highest national CAGR at 9.43% over the forecast period.

Page last updated on: