Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

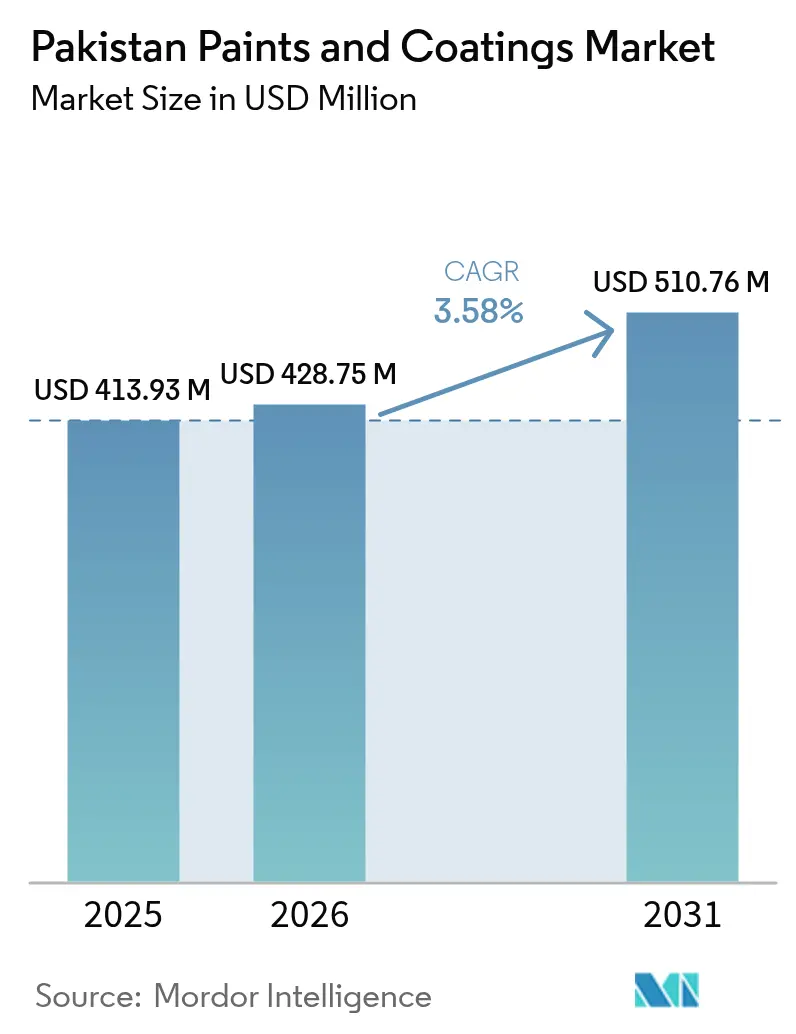

| Base Year Market Size (2025) | USD 413.93 Million |

| Market Size (2026) | USD 428.75 Million |

| Market Size (2031) | USD 510.76 Million |

| Growth Rate (2026 - 2031) | 3.58% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Paints And Coatings Market Analysis by Mordor Intelligence

Pakistan Paints And Coatings Market size in 2026 is estimated at USD 428.75 million, growing from 2025 value of USD 413.93 million with 2031 projections showing USD 510.76 million, growing at 3.58% CAGR over 2026-2031. Moderate yet steady growth reflects the country’s return to macro-economic stability, supported by a 4.2% GDP growth outlook and a contained inflation target of 7.5% that preserves consumer purchasing power. CPEC Phase 2 investments, accelerated Special Economic Zone roll-outs, and a Rs 1,000 billion Federal PSDP allocation are widening the opportunity set for protective, road-marking, and maintenance coatings. Simultaneously, the import duty structure that favors water-borne inputs—such as 0% on ethylene glycol—reinforces a long-term technological shift toward environmentally compliant, low-VOC systems.

Key Report Takeaways

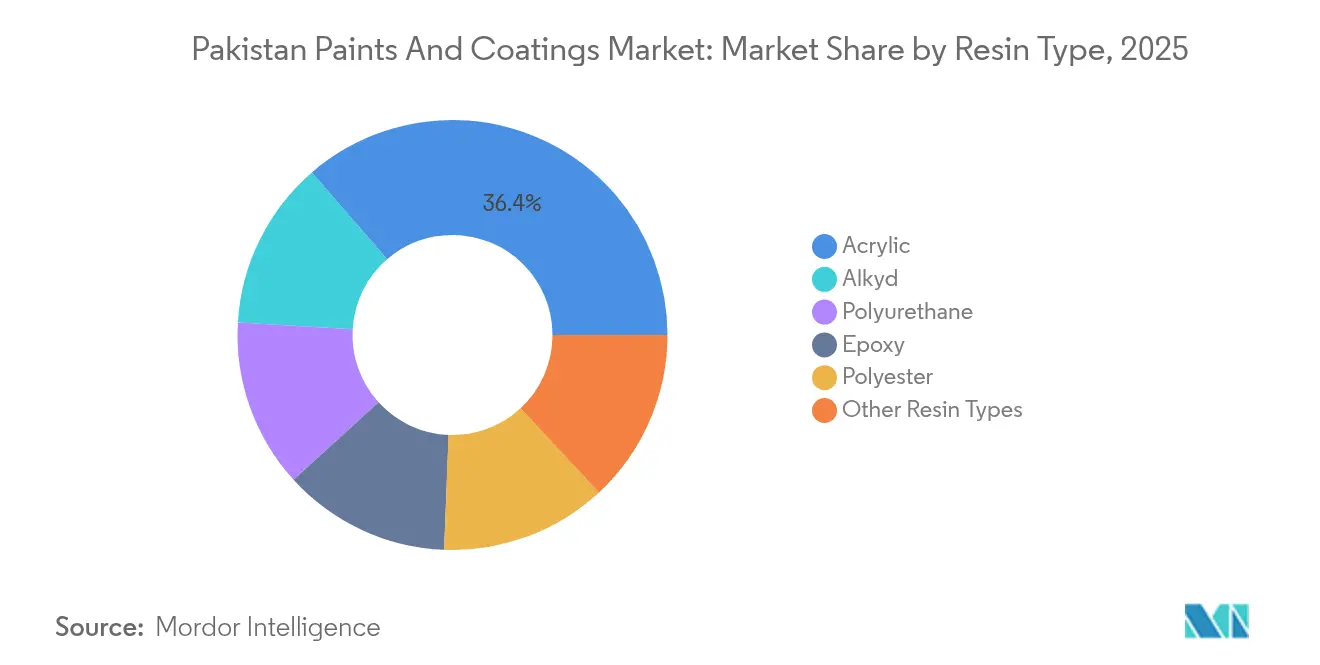

- By resin type, acrylic products captured 36.35% of Pakistan paints and coatings market share in 2025 and is forecasted to grow at a CAGR of 4.93% through 2031.

- By technology, water-borne systems accounted for 49.58% of the Pakistan paints and coatings market size in 2025 and are forecast to grow at a 4.81% CAGR through 2031.

- By end-user, architectural coatings commanded 64.42% of the Pakistan paints and coatings market size in 2025 and are projected to register the fastest 5-year CAGR at 3.92%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Govt-backed affordable housing and infra boom | +1.2% | National, Punjab and Sindh urban centers | Medium term (2-4 years) |

| Rapid urbanization spurring decorative demand | +0.8% | National; Karachi, Lahore, Islamabad | Long term (≥ 4 years) |

| Shift toward low-VOC water-borne coatings | +0.6% | National; regulated industrial zones | Medium term (2-4 years) |

| Appliance and 2/3-wheeler boom lifts powders | +0.4% | National; manufacturing hubs | Short term (≤ 2 years) |

| E-commerce and onsite tinting widen reach | +0.3% | Urban centers with strong digital networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Backed Affordable Housing and Infrastructure Boom

Federal support for subsidized housing and the PKR 328 billion earmarked for transport infrastructure in the 2025-26 PSDP are expanding coating demand across residential, road, and public‐works projects[1]Staff, “Federal Budget 2025-26 to be presented,” tribune.com.pk. CPEC Phase 2, which now features five industrial corridors and an operational Rashakai SEZ, is translating into sizable protective-coating opportunities for bridges, power plants, and heavy equipment. Steel capacity expansion from 4 million t to 9 million t, negotiated under Sino-Pak agreements, further raises consumption of high-performance anti-corrosion systems. Budgeted fiscal surpluses and USD 14.3 billion in foreign-exchange reserves strengthen public-investment execution, cushioning demand from cyclical setbacks. Amid these programs, Pakistan paints and coatings market participants that align supply chains, tinting services, and credit terms with large contractors are positioned to outpace sector averages.

Rapid Urbanization Spurring Decorative Demand

A 40.1% urbanization rate and a 3.8% rise in construction GDP in FY 2025 sustain city-center residential starts and renovation spending. Karachi, Lahore, and Islamabad record increased remittance inflows—USD 32 billion in 2025—that lift discretionary incomes for home improvement and premium finishes. While national cement output contracted 7.2%, selective demand in high-density neighborhoods preserved order books for decorative producers focused on mid- to high-end emulsions. Diamond Paints’ expansion of integrated manufacturing at Sunder Industrial Estate illustrates how local champions capture this trend through responsive lead-time and color-matching capabilities. The push toward healthier indoor environments is also nudging buyers toward low-VOC, odor-free options, advancing the long-run transition to water-borne chemistries.

Shift Toward Low-VOC Water-Borne Coatings

Punjab Environmental Quality Standards enforce strict emission ceilings that are raising compliance costs for solvent-based manufacturers and accelerating water-borne adoption. Independent testing in Karachi found 40% of solvent paints exceeding the 100 ppm lead limit, intensifying regulatory scrutiny and consumer distrust. Scientific work on styrene-acrylic façade coatings demonstrated dirt-resistant performance that matches or outperforms traditional alkyds, validating broader market acceptance. As petrochemical volatility still inflates solvent-raw-material costs, the relative total-cost advantage of water-borne lines is improving, particularly for export-oriented textile and appliance plants subject to international audits. Producers that invest in modular dispersion units and automated tinting for water-borne SKUs are therefore expected to gain share within the Pakistan paints and coatings market.

E-Commerce and Onsite Tinting Widen Reach

Mobile-first consumers in Pakistan’s urban corridors now benefit from 82 million broadband SIMs and a maturing branchless-banking ecosystem that enable direct-to-home paint retailing. Brighto Paints’ automatic tinting kiosks and “model shops” illustrate how local brands replicate multinational retail standards at lower cost while extending into GCC export markets that delivered Rs 400 million in sales in 2024. Portable tinting units further minimize waste by in-situ color matching, reducing returns and boosting contractor loyalty. Online platforms also bypass fragmented wholesalers, improving margin capture and order visibility for capacity planning. Manufacturers that integrate ERP-linked e-stores and live inventory feeds are therefore winning shelf space in the Pakistan paints and coatings market’s long-tail geographies.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and petro-chemical prices | -0.9% | Global supply chain; all Pakistani regions | Short term (≤ 2 years) |

| Energy shortages and high tariffs | -0.7% | Punjab and Sindh industrial belts | Medium term (2-4 years) |

| Large informal sector undercutting prices | -0.5% | Urban and peri-urban retail clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy Shortages and High Tariffs

Capacity payments of PKR 2.8 trillion to idle plants keep industrial tariffs between 13 and 17.5 US cents/kWh, double some regional peers, eroding cost competitiveness for local resin and dispersion lines[2]Editors, “Critical evaluation of textile industry,” nipapeshawar.gov.pk . Gas revisions and frequent load shedding drive smaller firms toward diesel gensets that raise unit costs and emissions. Textile exporters losing regionally competitive energy tariffs offer a cautionary parallel for paint formulators dependent on consistent heat for batch reactors and curing ovens. Government proposals to privatize loss-making Discos and to retire furnace-oil capacity promise relief beyond 2027, yet near-term uncertainty is delaying capex in high-efficiency roasting or recovery systems. Larger integrated players that deploy solar or waste-heat recovery retain a structural margin edge within the Pakistan paints and coatings market.

Large Informal Sector Undercutting Prices

The informal economy’s USD 457 billion gross value and 72.5% share of non-farm employment enable sub-scale paint shops to bypass taxes, environmental audits, and labor compliance, allowing price points up to 25% below organized brands. Occupational-safety studies reveal inadequate personal-protective equipment and unregulated solvent use in informal spray-painting, underscoring public-health concerns and reputational risk for the sector. As formal producers spend on wastewater treatment, lead-free pigments, and ISO certifications, price wars compress margins and disincentivize research and development. Digitized invoicing and tax amnesties may eventually entice small operators into the formal fold, yet enforcement resources remain thin, prolonging competitive distortions in the Pakistan paints and coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Drives Innovation

Acrylic resins held a 36.35% of overall revenue, and is projected to rise at a 4.93% CAGR through 2031, reflecting their versatility across both decorative and industrial categories. The segment’s strength lies in superior UV resistance, color retention, and ease of formulation into water-borne dispersions that satisfy emerging environmental rules. Domestic research and devlopment has already delivered styrene-acrylic façade emulsions with proven dirt resistance on par with European benchmarks. Alkyd offerings remain relevant for metal maintenance but face gradual share loss as regulators tighten VOC and lead limits. Imports of polymeric MDI for polyurethane systems draw only 5% duty, facilitating niche growth in high-durability floor and oil-and-gas coatings that capture rising industrial capex.

Second-tier resin families—epoxies and polyesters—address protective and powder applications, respectively, and benefit from tariff preferences that encourage local blending. Polyester uptake is synchronized with powder-coating capacity aimed at appliances and two-wheelers, while epoxy primers protect critical infrastructure such as pipelines and bridges being delivered under CPEC. As multinational and domestic formulators increasingly publicize product EPDs (Environmental Product Declarations), acrylic adoption will deepen, reinforcing its leadership within the Pakistan paints and coatings market.

By Technology: Water-Borne Systems Lead Environmental Transition

In 2025, water-borne lines generated 49.58% of sector revenue, outpacing solvent systems as Pakistan Environmental Protection Act audits gain momentum. The sub-segment is forecast at a 4.81% CAGR to 2031, supported by 0% import duty on ethylene glycol and institutional buyers’ preference for low-odor top-coats in schools and hospitals. Solvent-borne demand endures in heavy-duty marine and automotive refinishes but slips as supply chains improve for high-flash water-reducible alkyds.

UV-cured and solvent-free hybrids remain embryonic yet garner pilot projects among furniture exporters targeting European compliance. Pakistan’s customs framework incentivizes early adopters through IOCO quotas and duty drawbacks, encouraging incremental capex in UV lines. As regulatory enforcement tightens, the commercial case for water-borne and powder formats strengthens, positioning them as twin growth engines.

By End-User Industry: Architectural Segment Drives Market Growth

Architectural coatings earned 64.42% of sector revenue in 2025 and are projected to grow at a 3.92% CAGR through 2031 on the back of Rs 5 billion in subsidized housing loans and rising urban renovation cycles. Decorative emulsions and exterior textures dominate volume, with premium sheens gaining traction as disposable incomes rise.

Wood-finish demand correlates with the furniture cluster in Chiniot and Gujrat, while industrial formulations protect machinery in emerging SEZs along CPEC routes. Transportation and packaging sub-segments remain specialized but benefit from railway modernization and food-and-beverage capacity additions such as Murree Brewery’s ongoing PET bottle investments. Overall, diversified demand anchors resilience in the Pakistan paints and coatings market.

Geography Analysis

Punjab is driven by Lahore’s manufacturing belt and the presence of integrated plants like the 13-acre Diamond Paints complex in Sunder Industrial Estate. Karachi’s port logistics make Sindh the import gateway for titanium dioxide and specialized additives, and its vast urban housing stock underpins decorative volumes despite slower industrial expansion. Local formulators exploit proximity to container terminals to minimize demurrage and offer faster delivery into Baluchistan and KPK.

Khyber Pakhtunkhwa emerges as a high-growth node after the Rashakai SEZ became operational on 247 acres, hosting textiles, packaging, and light-engineering tenants that source protective and floor coatings. . Rail and road upgrades on the Western Route further lower freight costs for paint distributors extending north-west. Baluchistan contributes modest revenue today but holds potential in marine and oil-storage coatings tied to Gwadar’s master plan, which includes 300 MW of new generation capacity and expanded berths. Northern urban clusters, Islamabad-Rawalpindi and Faisalabad, benefit from civil-service housing allowances and export-oriented textile mills, respectively, creating steady mid-grade decorative demand. In aggregate, regional dynamics confirm a dual core of Punjab and Sindh with emerging peripheries under CPEC, shaping supply-chain footprints in the Pakistan paints and coatings market.

Competitive Landscape

Pakistan paints and coatings market features consolidation amongst major players. Multinationals AkzoNobel, Nippon Paint, and Berger Paints leverage proprietary resins and branded tinting systems, while domestic leaders Diamond Paints and Brighto Paints compete on localized formulations and agile distribution. AkzoNobel’s 25-acre Faisalabad hub integrates decorative, coil, and protective lines and signals a pivot toward capacity consolidation in South Asia following its announced divestment of Indian decorative assets to JSW Group. Strategic investments in digital color tools, ERP-linked inventory, and training academies for painters improve brand stickiness, while ESG disclosures and ISO-14001 certifications unlock procurement from multinational construction firms. Over the forecast period, analysts expect selective consolidation as energy and compliance costs favor scale, thereby raising entry barriers in the Pakistan paints and coatings market.

Pakistan Paints And Coatings Industry Leaders

AkzoNobel N.V.

Berger Paints Private Limited

Brighto Paints

Diamond Paints

Nippon Paint Pakistan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: AkzoNobel initiated a strategic review of its South Asian decorative portfolio, considering partnerships, joint ventures, and divestments to sharpen its focus on high-scale core markets.

- February 2024: AkzoNobel inaugurated a 25-acre multifunctional coatings plant in Faisalabad, integrating a forested buffer zone for biodiversity conservation.

Pakistan Paints And Coatings Market Report Scope

Paint is any pigmented liquid, liquefiable or solid putty composition that, when applied to a substrate in a thin layer, turns into a solid film. It is most often used to protect, color, or provide texture. A coating is a coating that is applied to the surface of an object, usually referred to as a substrate. The purpose of applying a coating can be decorative, functional, or both. Coatings can be applied as liquids, gases, or solids, e.g. powder paints. The Pakistani paints and coatings market is segmented by resin, technology, and end-user industry. On the basis of resin, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. On the basis of technology, the market is segmented into waterborne and solvent-borne. On the basis of end-user industry, the market is segmented into architectural, automotive, wood, industrial coatings, transportation, and packaging. For each segment, the market sizing and forecast have been done based on revenue (in USD million).

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

| Powder |

| Others (UV cured and Solvent free) |

By End-user Industry

| Architectural |

| Automotive |

| Wood |

| Industrial Coatings |

| Transportation |

| Packaging |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder | |

| Others (UV cured and Solvent free) | |

| By End-user Industry | Architectural |

| Automotive | |

| Wood | |

| Industrial Coatings | |

| Transportation | |

| Packaging |

Key Questions Answered in the Report

What is the current value of Pakistan's paints and coatings sector?

The Pakistan paints and coatings market size stands at USD 428.75 million as of 2026.

How fast is the sector expected to grow?

Mordor Intelligence forecasts a 3.58% CAGR, lifting value to USD 510.76 million by 2031.

Which resin family leads volume sales?

Acrylic resins hold 36.35% share owing to versatility and compatibility with water-borne systems.

Why are water-borne formulations gaining ground?

Stricter VOC limits under PEPA and lower import duties on key inputs favor water-borne chemistry.

Which end-use category dominates demand?

Architectural coatings represent 64.42% of total revenue, supported by subsidized housing and urban renovation.

What key challenge could slow sector growth?

Volatile titanium-dioxide and energy costs pose the largest near-term margin risks.

Page last updated on: