Global Pain Management Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

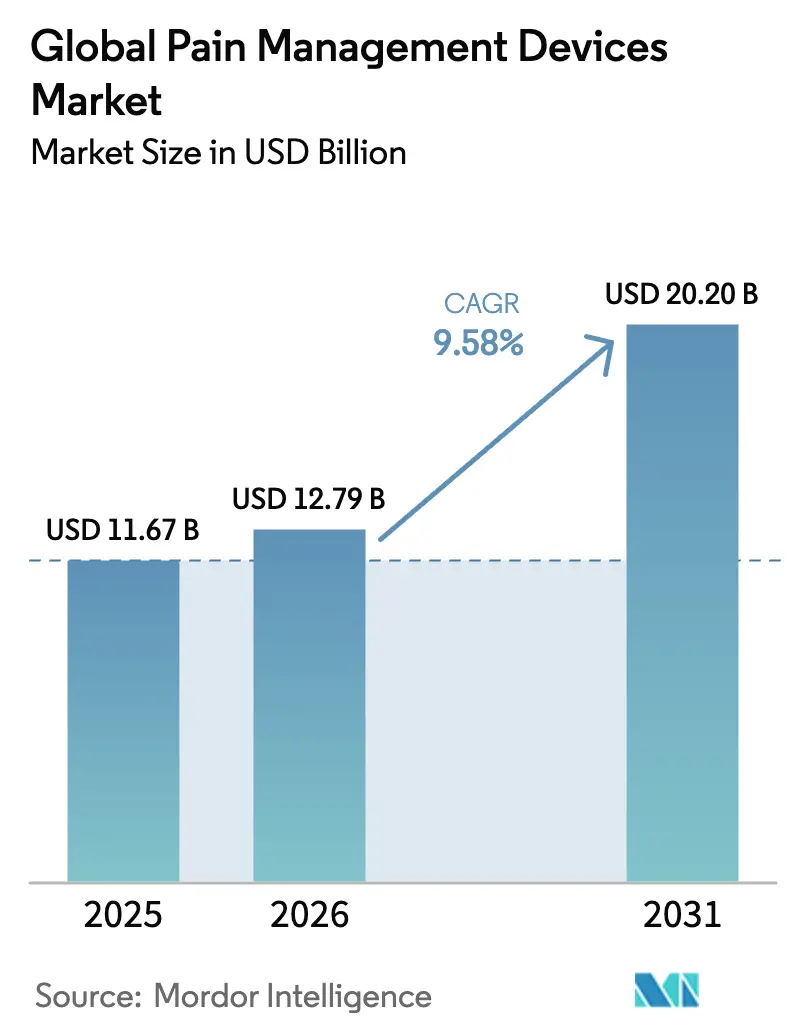

| Market Size (2026) | USD 12.79 Billion |

| Market Size (2031) | USD 20.2 Billion |

| Growth Rate (2026 - 2031) | 9.58% CAGR |

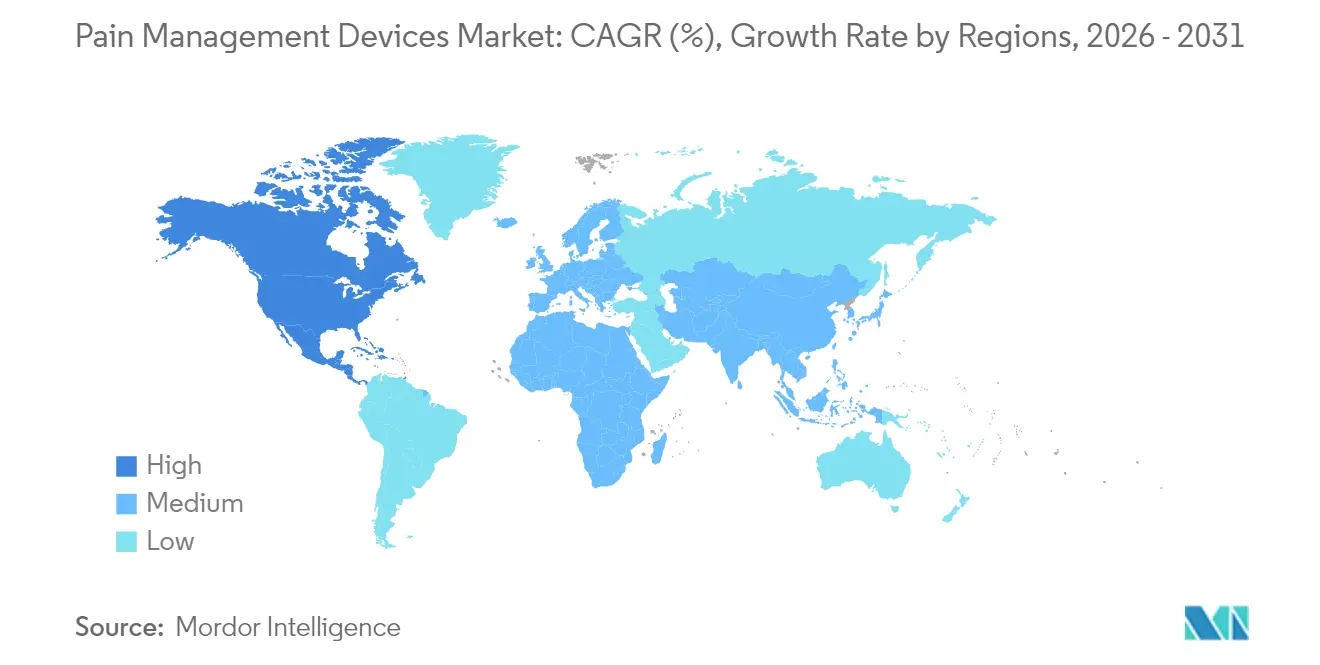

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Pain Management Devices Market Analysis by Mordor Intelligence

Pain management devices market size in 2026 is estimated at USD 12.79 billion, growing from 2025 value of USD 11.67 billion with 2031 projections showing USD 20.2 billion, growing at 9.58% CAGR over 2026-2031. This trajectory is propelled by an ageing global population, broader reimbursement for neurostimulation, and rapid progress in closed-loop systems that fine-tune stimulation in real time. Neurostimulation devices currently dominate, helped by landmark FDA approvals for adaptive spinal cord stimulators, while ablation systems gain momentum through minimally invasive radiofrequency platforms that promise pain relief lasting up to two years. North America leads adoption amid favorable Medicare policies, whereas Asia-Pacific grows the fastest on the back of Japan’s structured chronic-pain programs and expanding hospital capacity. Intensifying consolidation—typified by Globus Medical’s buyout of Nevro—couples with venture funding for wearable stimulators, deepening both competitive stakes and product innovation. Persistent chip and battery shortages continue to test manufacturers, yet AI-enabled algorithms and sensor ecosystems point to a future of fully personalized pain therapy.

Key Report Takeaways

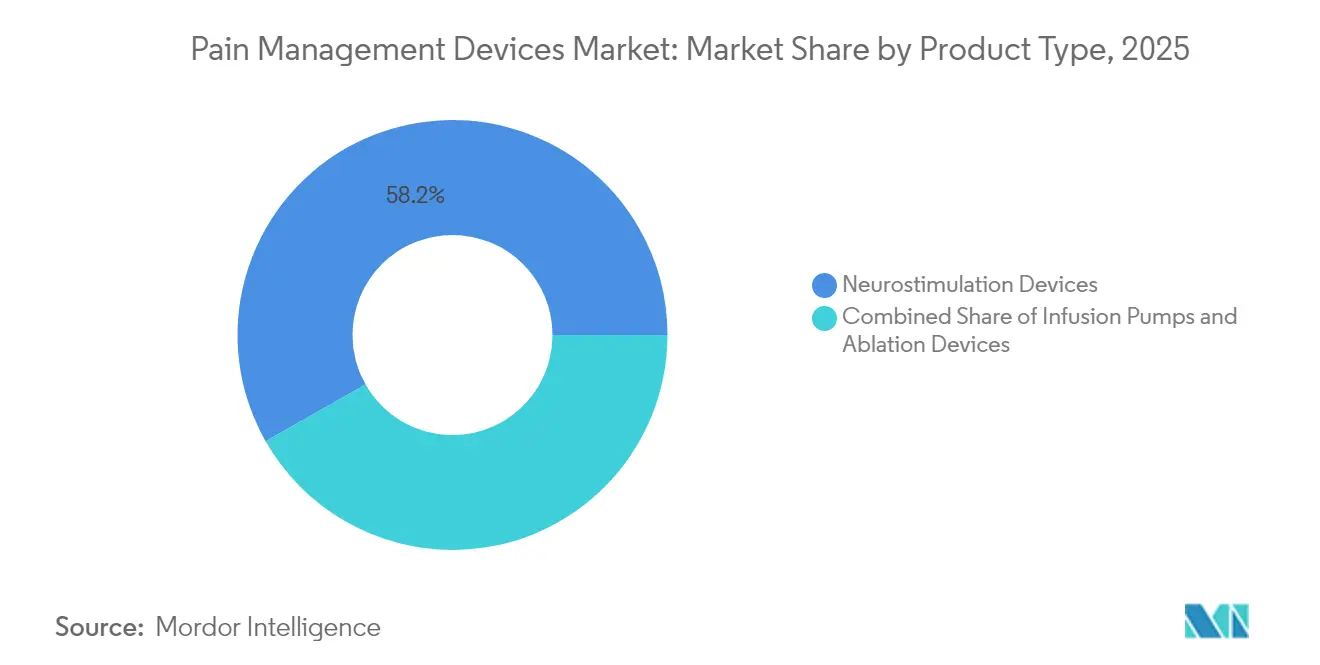

- By product type, neurostimulation devices led with 58.23% of pain management devices market share in 2025; ablation devices are projected to expand at a 10.17% CAGR to 2031.

- By application, neuropathic pain accounted for 32.08% share of the pain management devices market size in 2025, while cancer pain is advancing at a 10.62% CAGR through 2031.

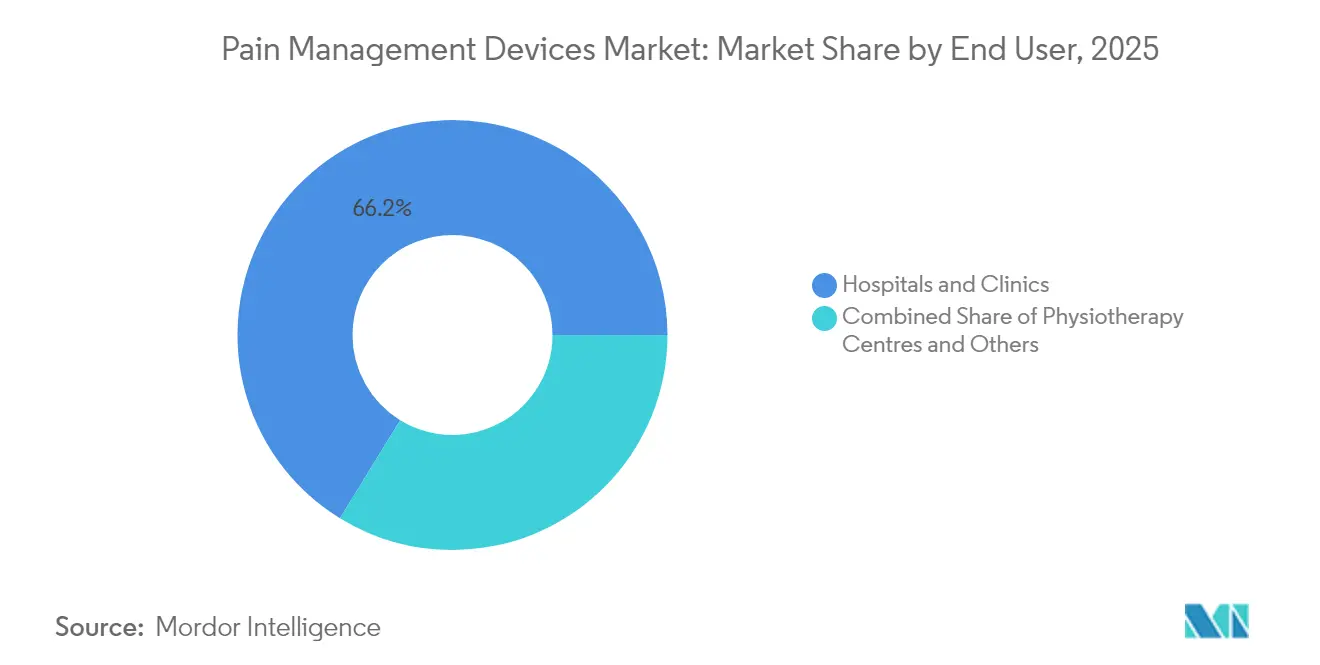

- By end-user, hospitals and clinics held 66.23% of the pain management devices market share in 2025; physiotherapy centers record the highest projected CAGR at 10.47% to 2031.

- By geography, North America commanded 43.10% of the pain management devices market in 2025; Asia-Pacific is expected to register an 11.52% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pain Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic pain & ageing population | +2.1% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Technological advances in neuromodulation | +1.8% | Global, led by North America & Europe | Medium term (2-4 years) |

| Favourable reimbursement for SCS | +1.4% | North America primary, expanding to Europe | Short term (≤ 2 years) |

| AI-driven closed-loop stimulation algorithms | +1.2% | North America & Europe, early APAC uptake | Medium term (2-4 years) |

| Wearable–implantable sensor ecosystems | +0.9% | Global, fastest in North America | Medium term (2-4 years) |

| VC surge in peripheral nerve stimulation startups | +0.6% | North America & Europe, spillover to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Pain & Ageing Population

Chronic pain now affects one in four adults in the United States, with prevalence climbing from 12.3% in those aged 18-29 to 36.0% among seniors, a demographic tilt that widens the addressable base for the pain management devices market. The economic toll exceeds USD 725 billion per year for chronic pain care, strengthening cost-effectiveness arguments for device-based interventions that lower long-term drug reliance. Japan reports 22.5% adult prevalence and a 2 trillion yen annual burden, prompting the health ministry to fund multidisciplinary pain centers that emphasize non-pharmacologic modalities [1]Ministry of Health, Labour and Welfare Japan, “Policy Initiatives for Chronic Pain Management,” mhlw.go.jp. Rural populations show higher pain incidence than urban peers, an imbalance that device-guided home programs can help close by reducing travel needs for follow-up therapy.

Technological Advances in Neuromodulation

Closed-loop neurostimulation shifts treatment from fixed settings to adaptive pulses that respond to evoked compound action potentials hundreds of times per second. Medtronic’s Inceptiv system cut overstimulation reports in 93% of study participants while halving low-back pain for 82% within six months[2]Medtronic, “Inceptiv Spinal Cord Stimulation System FDA Approval,” medtronic.com . Nevro’s AI-enhanced platform, cleared in 2024, learns individual neural patterns to refine energy delivery, elevating responder rates in trial cohorts. Progress in neuromorphic chips, bioresorbable electrodes, and full-body 3 T MRI-conditional leads widens clinical utility and underpins the premium pricing that sustains high R&D reinvestment.

Favourable Reimbursement for SCS

Medicare’s July 2023 decision to cover spinal cord stimulation for painful diabetic neuropathy instantly opened access for 11 million beneficiaries and set a reference point for commercial insurers. Average payments of USD 1,070 for trial leads and USD 3,726 for permanent systems at ambulatory surgical centers improve provider economics, while new CPT codes streamline billing workflows. Early European adopters, notably Germany’s statutory funds, are assessing similar coverage, signalling a broader reimbursement tailwind that undergirds growth in the pain management devices market.

AI-driven Closed-loop Stimulation Algorithms

Artificial intelligence now predicts pain cycles and pre-emptively adjusts stimulation, converting therapy from reactive to proactive care. Multimodal devices matching implant data with smartwatch metrics have shown correlation with subjective pain diaries, allowing closed-loop triggers that curb symptom flares. In auricular vagus nerve stimulation, AI-optimized timing improved heart-rate variability beyond conventional duty cycles, pointing to broader autonomic benefits in chronic pain cohorts.

Wearable–Implantable Sensor Ecosystems

Next-generation platforms integrate surface electrodes, implant telemetry, and cloud dashboards, creating persistent data loops that fine-tune programming between clinic visits. Battery-free stimulators leveraging inductive power or ultrasonic energy eliminate pulse-generator replacements, reducing surgical burden and life-cycle cost. Such ecosystems expand indications into postoperative, paediatric, and sports-injury pain, further widening the pain management devices market addressable pool.

VC Surge in Peripheral Nerve Stimulation Start-ups

Series A to E rounds topping USD 100 million across multiple firms in 2024-2025 underline investor belief that less-invasive percutaneous leads will move therapy earlier in care pathways. Start-ups focus on miniaturized pulse generators and dissolvable anchors, aiming to deliver two-week outpatient procedures at a fraction of traditional spinal implants, thereby lowering entry costs and accelerating market penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for pharmaceuticals | -1.6% | Global, strongest in emerging markets | Long term (≥ 4 years) |

| High implantation cost & limited implanters | -1.9% | Global, acute in emerging markets | Medium term (2-4 years) |

| Insurer scrutiny over explantations | -1.1% | North America & Europe, expanding | Medium term (2-4 years) |

| Chip & battery supply-chain constraints | -1.3% | Global, highest in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Preference for Pharmaceuticals

Opioids and NSAIDs remain first-line pain therapies in many health systems because they are inexpensive and widely prescribed, delaying device uptake despite acknowledged long-term drawbacks. Emerging markets, where reimbursement for implants is nascent, sustain higher drug reliance, muting early demand for advanced neuromodulation.

High Implantation Cost & Limited Implanters

Comprehensive procedure expenses for spinal cord stimulation can reach USD 70,000, a hurdle compounded by scarce trained surgeons in rural regions. Revision events cost an added USD 15,000-25,000, and an explantation rate near 10% prompts payors to scrutinize value propositions. Simplified peripheral systems and targeted training fellowships are easing barriers but the constraint persists.

Insurer Scrutiny over Explantations

Clinical studies attribute 38% of explants to inadequate pain relief and 29% to device complications, leading insurers to require prior authorization and documented conservative-therapy failure before approving implantation. Some policies now demand algorithm-guided programming audits to validate optimal use before permitting explant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Neurostimulation Dominance Drives Innovation

The pain management devices market size reached USD 11.67 billion in 2025, of which neurostimulation captured 58.23% pain management devices market share in 2025. Closed-loop spinal cord stimulators differentiate through adaptive dosing that halves overstimulation complaints while granting full-body MRI access, features now standard in leading systems. Peripheral nerve stimulators stretch indications to postoperative joints and migraines, aided by outpatient-friendly implants the size of a credit card that house inductive coils. Ablation platforms, advancing at a 10.17% CAGR, leverage cooled RF probes that create larger lesions without charring, producing two-year median relief for facet-mediated back pain. Infusion pumps remain essential for refractory cancer pain, dispensing intrathecal morphine that achieves 87.5% opioid discontinuation at one month, thereby underscoring the multi-modality nature of the pain management devices industry.

Innovation clusters around AI enhancement, with onboard processors parsing compound action potentials thousands of times per minute to tailor amplitude and pulse width. Lead materials shift toward segmented silicone overmoulds that conform to epidural anatomy and cut revision risk. Convergent ecosystems pair implants with wearable accelerometers, enabling automatic posture-based stimulation adjustments that sustain analgesia during daily activities.

By Application: Neuropathic Pain Leadership Amid Cancer Pain Surge

Neuropathic disorders, notably painful diabetic peripheral neuropathy, topped application demand by accounting for 32.08% of 2025 revenue. The pain management devices market size for neuropathic pain is forecast to grow at upper-single-digit rates through 2031 as Medicare coverage expands. Trials show 70% responder rates versus 6% for best-medical-therapy, a differential that emboldens guideline writers to recommend neuromodulation earlier in algorithms. Cancer pain emerges fastest at a 10.62% CAGR, propelled by increasing survivorship and the opioid-sparing benefit of intrathecal pumps. Musculoskeletal pain continues to rely on radiofrequency ablation of genicular, sacroiliac, and basivertebral nerves, reaching more active-age cohorts. Niche indications such as phantom-limb and complex regional pain syndrome attract novel bioresorbable stimulators that dissolve after six months, avoiding explant surgery and lowering infection exposure, a design that resonates with value-based care priorities within the pain management devices market.

By End-User: Hospital Dominance Challenged by Physiotherapy Growth

Hospitals and clinics held 66.23% pain management devices market share in 2025, anchored by operating rooms equipped for fluoroscopy and the presence of multidisciplinary teams. Large centers increasingly embed AI dashboards that integrate imaging, programming, and outcomes, shortening programming visits by 30% and improving staff productivity. Nevertheless, physiotherapy centers log a 10.47% CAGR by adopting non-invasive pulsed-radiofrequency and high-energy shockwave modalities that require no implantation and can be bundled into rehabilitation packages. Expansion of remote-programming platforms enables post-operative adjustments from patients’ homes, reducing hospital touchpoints and widening the end-user base to ambulatory surgery centers and even private practices, trends that diversify distribution within the pain management devices market.

Geography Analysis

North America, representing 43.10% of global revenue in 2025, benefits from Medicare’s broadened coverage, robust private-payor alignment, and a mature clinician base accustomed to implantable technologies. The United States anchors R&D pipelines, with the FDA granting breakthrough-device designation to multiple AI-driven stimulators in 2024, accelerating time-to-market and reinforcing the region’s supply-side advantage. Canada follows with growing provincial reimbursements for peripheral stimulation, while Mexico’s cross-border medical travel supports neuromodulation procedure volumes.

Europe displays steady, policy-guided uptake governed by the Medical Device Regulation 2017/745, which enforces post-market surveillance and clinical-data verification for every implant class . Germany and the United Kingdom lead implant counts, yet southern states—Italy and Spain—embrace ablation as a cost-contained alternative. The UK’s National Institute for Health and Care Excellence is reviewing outcome-based pricing for closed-loop stimulators, potentially modelling value contracts that could echo across EU payor systems. EUDAMED database roll-out augments transparency for physicians and importers, smoothing device traceability across borders.

Asia-Pacific is the fastest-growing territory, with an 11.52% CAGR through 2031. Japan’s health ministry funds multidisciplinary pain centers, channelling public insurance toward device-guided therapy that offsets an estimated 2 trillion yen annual burden. China’s National Medical Products Administration has streamlined Class III device reviews, shortening domestic approval windows to under nine months, which encourages multinationals to localize assembly lines. India’s nascent reimbursement environment still leans on out-of-pocket spending, but pilot inclusion of spinal stimulators in public insurance schemes signals future gains. Australia and South Korea, already early adopters of high-density waveforms, extend regional best practices through professional-society training programs.

Middle East & Africa and South America together remain under 10% of 2024 turnover yet show double-digit expansion as private hospitals import turnkey pain-care suites, often staffed by visiting surgeons from Europe and North America. Government initiatives to cut opioid dependency enhance acceptance of device-based solutions, positioning both regions as long-range opportunities for the pain management devices market.

Competitive Landscape

The pain management devices market is moderately concentrated, with Medtronic, Boston Scientific, Abbott, and the newly merged Globus Medical-Nevro. Medtronic leverages versatile closed-loop algorithms across its Inceptiv spine platform and its Evolve workflow software, creating cross-selling synergy with intrathecal pumps. Boston Scientific emphasizes waveform versatility in WaveWriter stimulators that allow simultaneous tonic and burst patterns, a differentiator in patients with complex pain phenotypes. Abbott capitalizes on proprietary design for full-body MRI-compatibility and remote programming via Bluetooth-enabled smart devices.

The Globus Medical acquisition of Nevro in 2025 adds high-frequency 10 kHz waveforms to an orthopedic hardware suite, opening bundled value propositions for hospitals managing spine fusions and stimulators under one vendor. Saluda Medical advances evoked-potential sensing leads that auto-calibrate output in real time and targets European expansion under the CE-mark framework. Smaller players such as SPR Therapeutics and electroCore focus on less-invasive peripheral and vagus pathways, underwritten by venture funding that exceeded USD 100 million across top start-ups in 2024-2025.

Strategic themes coalesce around digital integration—cloud dashboards, predictive analytics, and wearable-implant harmony. Companies also hedge supply-chain risks by dual-sourcing semiconductors and designing battery-free architectures. Partnerships with university labs accelerate biomarker discovery, enabling real-time titration that may unlock value-based reimbursement models centered on objective functional gains rather than subjective pain scores.

Global Pain Management Devices Industry Leaders

Abbott

Baxter International Inc

Nevro Corp

DJO Global LLC

Stim Wave Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Zynex Inc obtained FDA clearance for the TensWave non-invasive pain therapy device.

- September 2024: Nevro Corp began limited US release of HFX iQ with AdaptivAI, an adaptive spinal cord stimulation platform

- April 2024: Medtronic plc received FDA approval for the Inceptiv closed-loop rechargeable spinal cord stimulator for chronic pain.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, according to Mordor Intelligence, defines the pain management devices market as global revenue generated from neurostimulation, electro-analgesia, infusion, and radio-frequency ablation systems that are cleared for clinical pain relief across hospitals, physiotherapy centers, and home settings.

Scope exclusion: We do not include veterinary equipment, beauty-oriented massagers, or disposable consumables such as catheters.

Segmentation Overview

- By Product Type

- Neurostimulation Devices

- Infusion Pumps

- Ablation Devices

- By Application

- Musculoskeletal

- Cancer Pain

- Neuropathic Pain

- Facial Pain & Migraine

- Others

- By End-User

- Physiotherapy Centres

- Hospitals & Clinics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed pain clinicians, biomedical engineers, hospital procurement leads, and regional distributors across North America, Europe, and Asia Pacific. These exchanges validated average selling prices, refined penetration assumptions, and confirmed refresh rates for capital equipment.

Desk Research

We began with public datasets that map pain prevalence and device uptake, such as WHO Global Health Estimates, CDC National Center for Health Statistics, Eurostat discharge files, and UN Comtrade codes 901890 and 901819. Regulatory filings on the US FDA 510(k) and EU MDR portals helped trace launch timelines, while peer-reviewed articles in Pain and The NEJM clarified clinical adoption curves. Financial disclosures, SEC 10-Ks, investor decks, and reputable press added revenue splits and pipeline clues. Paid repositories, including D&B Hoovers and Dow Jones Factiva, supported company benchmarking and news verification. This list is indicative; many further data points were consulted for cross-checks and historical continuity.

Market-Sizing & Forecasting

A top-down and bottom-up blend was applied. We first sized treated patient pools by indication and region, multiplied them by device utilization, and blended ASPs. Results were then corroborated with sampled supplier roll-ups and channel checks to temper totals. Key variables like chronic pain prevalence, neurostimulation penetration, reimbursement shifts, procedure volumes, device replacement cycles, and currency trends feed a multivariate regression forecast. Where granular bottom-up data were absent, weighted regional proxies agreed during expert calls and bridged the gaps.

Data Validation & Update Cycle

We run iterative variance reviews. Outputs are squared against customs tallies, hospital capex surveys, and select vendor revenues. Models pass two analyst reviews and refresh annually, with interim updates triggered by major regulatory or M&A events.

Why Mordor's Pain Management Devices Baseline Commands Industry Confidence

We recognize published market values often diverge; differing product baskets, geographic reach, price bases, and update cadences usually explain the gaps.

Key gap drivers include exclusion of infusion pumps, outpatient channels left untracked, spot-rate currency conversions, and shorter historical back-tests adopted by some publishers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.67 bn (2025) | Mordor Intelligence | |

| USD 7.65 bn (2024) | Global Consultancy A | Omits infusion pumps; relies solely on hospital billing data |

| USD 5.10 bn (2024) | Industry Portal B | Counts only Class III devices, five-region scope |

| USD 3.77 bn (2024) | Global Consultancy C | Uses list prices without ASP adjustment; limited historical base |

Our disciplined scope selection, transparent variable mapping, and scheduled updates give decision-makers a balanced, reproducible baseline that sits between optimistic shipment tallies and conservative hospital spend snapshots.

Key Questions Answered in the Report

How big is the Global Pain Management Devices Market?

The Global Pain Management Devices Market size is expected to reach USD 12.79 billion in 2026 and grow at a CAGR of 9.58% to reach USD 20.2 billion by 2031.

Which product segment generates the highest revenue?

Neurostimulation leads, holding 58.23% of 2025 revenue, backed by widespread adoption of closed-loop spinal cord stimulators.

Who are the key players in Global Pain Management Devices Market?

Abbott, Baxter International Inc, Nevro Corp, DJO Global LLC and Stim Wave Technologies are the major companies operating in the Global Pain Management Devices Market.

Which is the fastest growing region in Global Pain Management Devices Market?

Asia-Pacific shows the highest CAGR at 11.52% between 2026-2031, mainly due to expanding Japanese and Chinese demand.

Which region has the biggest share in Global Pain Management Devices Market?

In 2025, the North America accounts for the largest market share in Global Pain Management Devices Market.

Page last updated on: