Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 0 Billion |

| Market Size (2030) | USD 0 Billion |

| Growth Rate (2025 - 2030) | 3.50% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Contract Logistics Market Analysis by Mordor Intelligence

The Latin America Contract Logistics Market is expected to register a CAGR of greater than 3.5% during the forecast period.

Latin America's contract logistics landscape is undergoing significant transformation, driven by substantial infrastructure investments and regional economic integration initiatives. In 2023, Brazil unveiled plans to invest approximately USD 343.6 billion under the Growth Acceleration Program to enhance roadways, railways, and airport infrastructure. The "Routes for Integration" initiative, backed by approximately USD 50 billion from development banks, aims to establish comprehensive transportation routes fostering South American integration and development. These investments encompass infoways, hydroways, roadways, railways, ports, airports, and electricity transmission lines, demonstrating a concerted effort to modernize the region's supply chain management infrastructure.

The region is experiencing a dramatic shift in consumer behavior and retail logistics, particularly evident in the e-commerce sector. With over 50 million Latin Americans making their first online purchases in recent years, the demand for sophisticated warehousing and distribution logistics solutions has surged. This transformation has led to significant investments in logistics infrastructure, with Brazil commanding around 50% of the total industrial market share, followed by Mexico, Colombia, Chile, and Argentina. Major logistics providers are expanding their capabilities, as exemplified by DHL's launch of its DHL Fulfillment Network in Brazil, featuring 13 fulfillment centers and 55 transportation hubs, showcasing advanced warehouse management systems.

Nearshoring has emerged as a pivotal trend reshaping the region's contract logistics landscape. According to industry projections, nearshoring is expected to drive demand for up to 8 million square meters of industrial space in Mexico by 2027. Foreign direct investment (FDI) flows to Latin America and the Caribbean reached a remarkable USD 208 billion in 2022, marking a 51% increase driven by heightened demand for commodities and essential minerals. Brazil, in particular, witnessed a 70% rise in FDI, reaching USD 86 billion, while Mexico secured USD 35 billion in investments, emphasizing the role of integrated logistics in facilitating these developments.

The industry is witnessing rapid technological advancement and sustainability initiatives across the region. Major logistics providers are investing in cutting-edge facilities, as demonstrated by CEVA Logistics' inauguration of Colombia's first carbon-neutral warehouse in Bogotá, featuring energy and water-saving technologies, solar panels, and advanced recycling programs. In Brazil, the chemical industry achieved sales of USD 187 billion in 2022, with industrial chemicals, fertilizers, and crop protection chemicals leading the sector, highlighting the growing importance of specialized logistics solutions for handling complex cargo. These developments are driving the adoption of advanced warehouse management systems, logistics automation technologies, and sustainable practices across the contract logistics sector.

Latin America Contract Logistics Market Trends and Insights

Growing E-commerce and Digital Transformation

The rapid expansion of e-commerce in Latin America has become a fundamental driver for contract logistics services, with major investments reshaping the logistics landscape. In March 2024, MercadoLibre announced a record investment of USD 4.6 billion in Brazil, with logistics taking center stage in their strategic plans. This investment includes the development of new distribution centers and the enhancement of their technological capabilities, demonstrating the growing demand for sophisticated logistics solutions. The company's focus on logistics infrastructure highlights the critical role of contract logistics in supporting the region's digital commerce evolution.

The transformation of consumer behavior has led to significant changes in logistics requirements, particularly in warehouse positioning and last-mile delivery solutions. Major logistics providers like DHL Supply Chain have responded by launching innovative services such as the DHL Fulfillment Network (DFN) in Brazil, featuring multiclient warehouses and comprehensive e-commerce infrastructure consisting of 13 fulfillment centers, 55 transportation hubs, and 800 vehicles. This evolution in logistics infrastructure is further supported by the implementation of advanced technologies, including big data management systems that optimize fulfillment speeds and improve accuracy in delivery operations, enhancing overall supply chain management.

Understand The Key Trends Shaping This Market

Download PDF

Automotive Sector Expansion and Manufacturing Growth

The automotive sector's robust growth in Latin America has emerged as a crucial driver for contract logistics services, particularly in manufacturing powerhouses like Mexico and Brazil. In 2024, significant investments in the automotive sector are driving demand for specialized logistics services, exemplified by Volvo Group's announcement of a new heavy-duty truck manufacturing plant in Mexico. This expansion is complemented by other major investments, such as Nissan's USD 575 million enhancement of its Resende plant in Rio de Janeiro for the production of new SUV models and turbo engines.

The expansion of manufacturing activities has led to increased demand for sophisticated transportation management solutions, particularly in cross-border operations. This is evidenced by recent developments such as DP World's innovative 53-foot intermodal container solution for vehicle transport between Mexico and the United States, which can accommodate up to six vehicles per container compared to the conventional four-vehicle capacity. The solution is projected to facilitate the transportation of an additional 30,000 finished vehicles between trading partners, demonstrating the growing sophistication of automotive logistics solutions in the region.

Infrastructure Development and Government Initiatives

Government-led infrastructure initiatives across Latin America are significantly driving the growth of contract logistics services. Colombia's announcement in September 2023 to invest over USD 24.9 billion in rail, port, river, and road infrastructure projects exemplifies the region's commitment to improving logistics capabilities. The comprehensive plan encompasses 31 projects, including the revival of 1,800 kilometers of rail networks, construction of 15 new highways, modernization of five airports, and enhancement of river and port systems, creating new opportunities for logistics service providers.

Brazil's ambitious infrastructure development program has become a major catalyst for the logistics sector. The government's Growth Acceleration Program, with planned investments of USD 343.6 billion, focuses on strengthening the nation's roadways, railways, and airports. This is complemented by strategic initiatives like the "Routes for Integration" program, backed by approximately USD 10 billion from development banks, aimed at establishing comprehensive transportation routes and fostering South American integration. These investments are creating new corridors for logistics operations and enhancing the efficiency of existing supply chain services.

Rising Foreign Direct Investment and Cross-Border Trade

The surge in foreign direct investment across Latin America has become a significant driver for contract logistics services, creating new opportunities and demanding more sophisticated supply chain services. Major logistics firms are expanding their operations to meet this growing demand, as evidenced by Ryder System's recent expansion at the US-Mexico border, including a new 228,000-square-foot multiclient warehouse and cross-dock facility in Laredo, Texas. This expansion is directly responding to the increasing nearshoring trend and growing cross-border trade volumes.

The investment landscape is further enriched by strategic partnerships and facility expansions across the region. In March 2024, A.P. Moller-Maersk's partnership with Bandai Namco to establish a distribution center in Mexico City exemplifies how foreign investment is driving the need for specialized logistics solutions. Similarly, CEVA Logistics' inauguration of Colombia's first carbon-neutral warehouse in Bogota, spanning 15,000 square meters, demonstrates how investment in warehousing services is evolving to meet both operational and sustainability requirements. These developments are complemented by the expansion of logistics networks, with companies like Blue Water establishing new offices in strategic locations such as Santiago, Chile, to better serve the growing cross-border trade demands.

Segment Analysis

Outsourced Segment in Latin America Contract Logistics Market

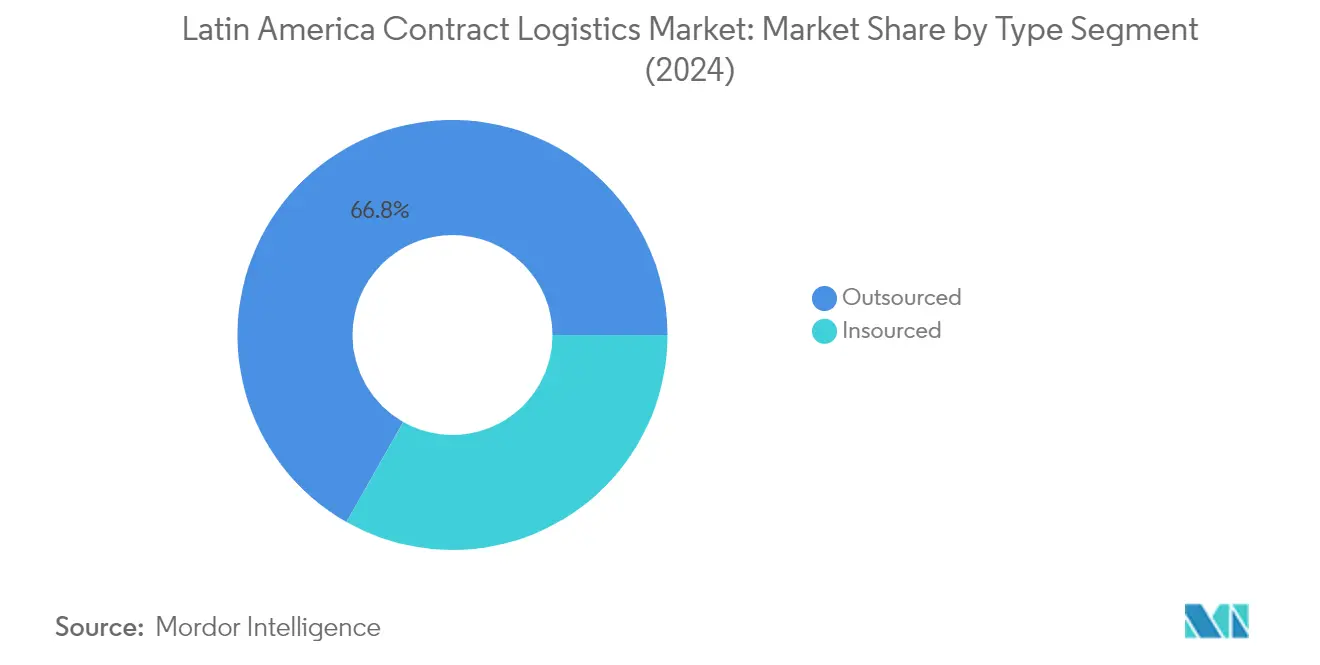

The outsourced segment dominates the Latin American contract logistics market, commanding approximately 67% of the total market share in 2024. This segment's prominence is driven by companies increasingly focusing on their core competencies while entrusting logistics operations to specialized third-party logistics providers. The segment's growth is further propelled by the rapid expansion of the Latin American manufacturing sector, emphasis on cost efficiency, and increasing technology supply chain integrations. Major players like A.P. Moller-Maersk, Bollore Logistics, DHL, CEVA Logistics, and GEODIS are actively expanding their presence in the region through strategic investments and partnerships. For instance, in March 2024, Maersk partnered with Bandai Namco to establish a distribution center in Mexico City, while CEVA Logistics unveiled Colombia's first carbon-neutral warehouse in Bogota, demonstrating the segment's continued evolution and modernization.

Insourced Segment in Latin America Contract Logistics Market

The insourced segment represents a significant portion of the Latin American contract logistics market, offering companies greater control and visibility over their logistical operations. This approach enables organizations to directly oversee their transportation, warehousing, and distribution activities, ensuring tighter integration with other business functions and compliance with internal policies and quality standards. In the transportation industry, while the trend of logistics outsourcing to third-party logistics providers has gained popularity, some companies prefer to maintain in-house logistics operations for better control over their supply chain. Retailers in the fashion and food industries have particularly embraced this model, building their own warehouses to maintain direct oversight of their operations. The segment continues to evolve with companies investing in modern facilities and technologies to enhance their internal logistics capabilities.

Segment Analysis: By End User

Food & Beverage Segment in Latin America Contract Logistics Market

The Food and Beverage segment has emerged as a dominant force in the Latin American contract logistics market, commanding approximately 17% of the market share in 2024. This significant market position is driven by the increasing complexity of food supply chains, stringent safety regulations, and the growing demand for temperature-controlled logistics solutions. The segment's strength is particularly evident in major markets like Brazil and Mexico, where expanding retail networks and changing consumer preferences have necessitated sophisticated logistics operations. The rise of e-commerce in the food sector, coupled with the need for specialized handling and storage facilities, has further cemented the segment's importance. Contract logistics providers in this segment are increasingly investing in advanced warehousing solutions, cold chain infrastructure, and technology-driven tracking systems to ensure product integrity throughout the supply chain.

Healthcare & Pharmaceutical Segment in Latin America Contract Logistics Market

The Healthcare and Pharmaceutical segment is demonstrating remarkable growth potential, projected to expand at approximately 6% CAGR from 2024 to 2029. This accelerated growth is primarily driven by the increasing complexity of pharmaceutical supply chains, stringent regulatory requirements, and the growing demand for specialized healthcare logistics solutions. The segment's expansion is further fueled by the rising healthcare expenditure across Latin America, particularly in countries like Brazil, Mexico, and Colombia. Contract logistics providers are increasingly investing in temperature-controlled facilities, specialized handling equipment, and advanced tracking systems to meet the exacting requirements of pharmaceutical transportation and storage. The growing focus on healthcare accessibility and the expansion of healthcare infrastructure across the region are creating new opportunities for logistics providers specializing in this sector.

Remaining Segments in Latin America Contract Logistics Market

The market's remaining segments, including Industrial Machinery & Automotive and Chemicals, each play vital roles in shaping the overall contract logistics landscape. The Industrial Machinery & Automotive segment is characterized by complex supply chains and the need for specialized handling capabilities, particularly in manufacturing hubs across Mexico and Brazil. The Chemicals segment demands specialized safety protocols and regulatory compliance measures, requiring logistics providers to maintain specific certifications and handling capabilities. These segments collectively contribute to the market's diversity and demonstrate the varied nature of contract logistics requirements across different industries in Latin America. Each segment presents unique challenges and opportunities for logistics providers, driving innovation in areas such as specialized transportation, storage solutions, and safety protocols.

Geography Analysis

Contract Logistics Market in Brazil

Brazil dominates the Latin American contract logistics landscape, commanding approximately 37% of the market share in 2024. The country's continental scale and emerging economy status have driven substantial investments in expanding both logistics and social infrastructure. While historically favoring highways over railways due to industrialization policies from the 1960s, Brazil has recently pivoted toward more cost-effective and sustainable transportation modes. The nation has increasingly embraced private investments, transitioning from government-managed construction and maintenance to concessions and public-private partnerships (PPPs). This shift has proven crucial in enhancing the country's logistics matrix, though significant room for improvement remains. Infrastructure projects in Brazil undergo meticulous planning and structuring, often requiring up to four years to reach the bidding phase. The Brazilian National Development Bank (BNDES) has evolved its role, moving beyond merely financing infrastructure projects to providing comprehensive advisory services to all levels of government on project planning.

Contract Logistics Market in Mexico

Mexico's contract logistics market demonstrates remarkable dynamism, projected to grow at approximately 5% annually from 2024 to 2029. The country's strategic position and robust manufacturing sector have created a thriving environment for logistics operations. Companies are increasingly adopting nearshoring strategies, leading to heightened investments in logistics distribution near the Mexican border. The country's pivotal role in nearshoring is evidenced by its leading position as an importer at 14.8% according to U.S. Census Bureau data. The logistics landscape in Mexico encompasses comprehensive end-to-end processes, from production to the final point of sale, integrating traditional logistics with sophisticated supply chain management. Companies specializing in contract logistics not only handle goods movement but also engage in supply chain design, facility planning, warehousing services, transport, order processing, payment collection, inventory management, and customer service operations.

Contract Logistics Market in Colombia

Colombia's contract logistics sector demonstrates significant potential for growth, supported by substantial infrastructure investments and strategic development initiatives. The country has announced plans to invest over 100 trillion pesos in rail, port, river, and road infrastructure projects, aiming to catalyze economic growth across diverse communities. Despite its population of approximately 50 million, Colombia faces challenges with underdeveloped roadways, ports, and airports, which impact international trade endeavors. The government's comprehensive vision encompasses 31 projects, including the revival of 1,800 kilometers of rail networks, construction of 15 new highways, modernization and expansion of five airports, and strengthening of river and port systems. These initiatives are designed to not only enhance transportation infrastructure but also serve as cornerstones for economic growth, job creation, and improved regional connectivity.

Contract Logistics Market in Other Countries

The contract logistics landscape across other Latin American countries presents a diverse and evolving market environment. Countries like Chile, Peru, Argentina, and other Central American nations are witnessing transformation in their logistics sectors, driven by technological advancement and changing consumer demands. These markets are characterized by varying levels of infrastructure development, regulatory frameworks, and economic conditions that influence the logistics landscape. The integration of digital logistics solutions and automation is gradually reshaping traditional logistics operations across these regions. While some countries focus on modernizing their port facilities, others are investing in inland transportation networks and warehousing services capabilities. The varying geographical terrains and economic priorities of these nations have led to the development of unique logistics solutions tailored to local market needs and challenges.

Competitive Landscape

Top Companies in Latin America Contract Logistics Market

The Latin American contract logistics market is characterized by the strong presence of global players like DHL, DB Schenker, Kuehne + Nagel, and CEVA Logistics, who have established robust regional networks. These industry leaders are driving market evolution through continuous investment in digital transformation initiatives, including warehouse automation systems and advanced tracking solutions. Companies are increasingly focusing on developing specialized solutions for high-growth sectors like e-commerce, automotive, and healthcare, while simultaneously expanding their geographical footprint through strategic partnerships and facility expansions. The competitive landscape is being reshaped by sustainability initiatives, with major players investing in green warehousing solutions and eco-friendly transportation options. Market leaders are also strengthening their positions through value-added supply chain services, including supply chain consulting, inventory optimization, and customized logistics solutions tailored to regional requirements.

Market Consolidation Drives Regional Growth Strategy

The Latin American contract logistics market exhibits a mix of global logistics conglomerates and regional specialists, with international players holding dominant market positions through their extensive networks and technological capabilities. Market consolidation is increasingly evident as larger players pursue strategic acquisitions to enhance their service portfolios and geographic coverage, particularly in key markets like Brazil and Mexico. The competitive dynamics are further influenced by the presence of local players who leverage their market knowledge and established relationships to serve specific industry verticals or regional markets. Recent years have witnessed a surge in merger and acquisition activities, with global players acquiring local companies to strengthen their market presence and expand their service offerings.

The market structure is evolving with the entry of technology-driven logistics providers and the expansion of e-commerce giants into logistics services, creating new competitive pressures for traditional players. Global logistics companies are establishing strategic partnerships with local entities to enhance their last-mile delivery capabilities and warehouse networks. The competitive landscape is also being shaped by increasing investments in infrastructure development and modernization of logistics facilities, particularly in major economic centers. Market participants are differentiating themselves through specialized industry expertise, technological integration, and the ability to provide integrated logistics solutions.

Innovation and Adaptability Drive Market Success

Success in the Latin American contract logistics market increasingly depends on companies' ability to adapt to rapidly evolving customer requirements and technological advancements. Incumbent players are focusing on strengthening their market position through investments in digital platforms, automation technologies, and sustainable logistics solutions. Companies are also expanding their service portfolios to include specialized offerings for high-growth sectors while developing customized solutions for local market requirements. The ability to provide integrated logistics solutions, coupled with strong regional networks and local market expertise, has become crucial for maintaining competitive advantage. Market leaders are increasingly emphasizing operational excellence and cost optimization while maintaining service quality and reliability.

For new entrants and emerging players, success hinges on identifying and serving niche market segments while building strategic partnerships to expand their service capabilities. Companies must navigate regulatory complexities across different countries while maintaining operational efficiency and service consistency. The market presents opportunities for players who can effectively address the growing demand for specialized logistics services in sectors like pharmaceuticals, automotive, and retail. Success factors also include the ability to manage end-user concentration risks through diversified client portfolios and industry focus. Companies must also consider potential regulatory changes affecting cross-border trade and environmental compliance while developing their market strategies. The role of fourth-party logistics and 4PL logistics providers is becoming increasingly significant as they offer comprehensive solutions that integrate multiple logistics service provider capabilities.

Latin America Contract Logistics Industry Leaders

DB Schenker

DHL Supply Chain

CH Robinson

FedEx

GEODIS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2020: CEVA Logistics Mexico was appointed to operate a new dedicated warehouse to support IKEA Mexico's operations in the country. This facility opening is an extension of the existing successful global partnership between CEVA and the world's largest furniture retailer.

- June 2020: CEVA Logistics won an extension to its contract with Volkswagen for the operation of the company's auto spares center at Vinhedo in Brazil.

Latin America Contract Logistics Market Report Scope

Contract logistics refers to the outsourcing of resource management tasks to a third-party company. Contract logistics companies handle activities such as designing and planning supply chains, designing facilities, warehousing, transporting and distributing goods, processing orders and collecting payments, managing inventory, and even providing certain aspects of customer service.

The report provides a complete background analysis of the Latin American contract logistics market, which includes an assessment of the economy, emerging trends by segments and regional markets, significant changes in market dynamics, market overview, and company profiles. The report also covers the impact of COVID - 19 on the market.

The Latin American contract logistics market is segmented by type (outsourced and insourced), end user (manufacturing and automotive, consumer goods and retail, hi-tech, healthcare and pharmaceuticals, and other end users), and country (Mexico, Brazil, Colombia, Chile, and Rest of Latin America).

By Type

| Insourced |

| Outsourced |

By End User

| Industrial Machinery and Automotive |

| Food and Beverage |

| Chemicals |

| Other End Users |

By Geography

| Mexico |

| Brazil |

| Colombia |

| Chile |

| Rest of Latin America |

| By Type | Insourced |

| Outsourced | |

| By End User | Industrial Machinery and Automotive |

| Food and Beverage | |

| Chemicals | |

| Other End Users | |

| By Geography | Mexico |

| Brazil | |

| Colombia | |

| Chile | |

| Rest of Latin America |

Key Questions Answered in the Report

What is the current Latin America Contract Logistics Market size?

The Latin America Contract Logistics Market is projected to register a CAGR of greater than 3.5% during the forecast period (2025-2030)

Who are the key players in Latin America Contract Logistics Market?

DB Schenker, DHL Supply Chain, CH Robinson, FedEx and GEODIS are the major companies operating in the Latin America Contract Logistics Market.

What years does this Latin America Contract Logistics Market cover?

The report covers the Latin America Contract Logistics Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Latin America Contract Logistics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: