Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 218.37 Billion |

| Market Size (2026) | USD 229.11 Billion |

| Market Size (2031) | USD 290.73 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Packaging Market Analysis by Mordor Intelligence

The China packaging market size is projected to be USD 218.37 billion in 2025, USD 229.11 billion in 2026, and reach USD 290.73 billion by 2031, growing at a CAGR of 4.88% from 2026 to 2031. Continued e-commerce expansion, mandatory green-packaging rules, and cold-chain infrastructure upgrades are lifting baseline demand for corrugated boxes, flexible mailers, and insulated shippers. Large platform operators are redesigning ship-from-supplier workflows, which reduces empty space per parcel yet raises the technical sophistication of every layer of the China packaging market. Domestic mills keep adding containerboard and pulp capacity to hedge raw-material swings, while global converters are consolidating to secure scale economies, raw-material leverage, and geographic reach inside the China packaging market.

Key Report Takeaways

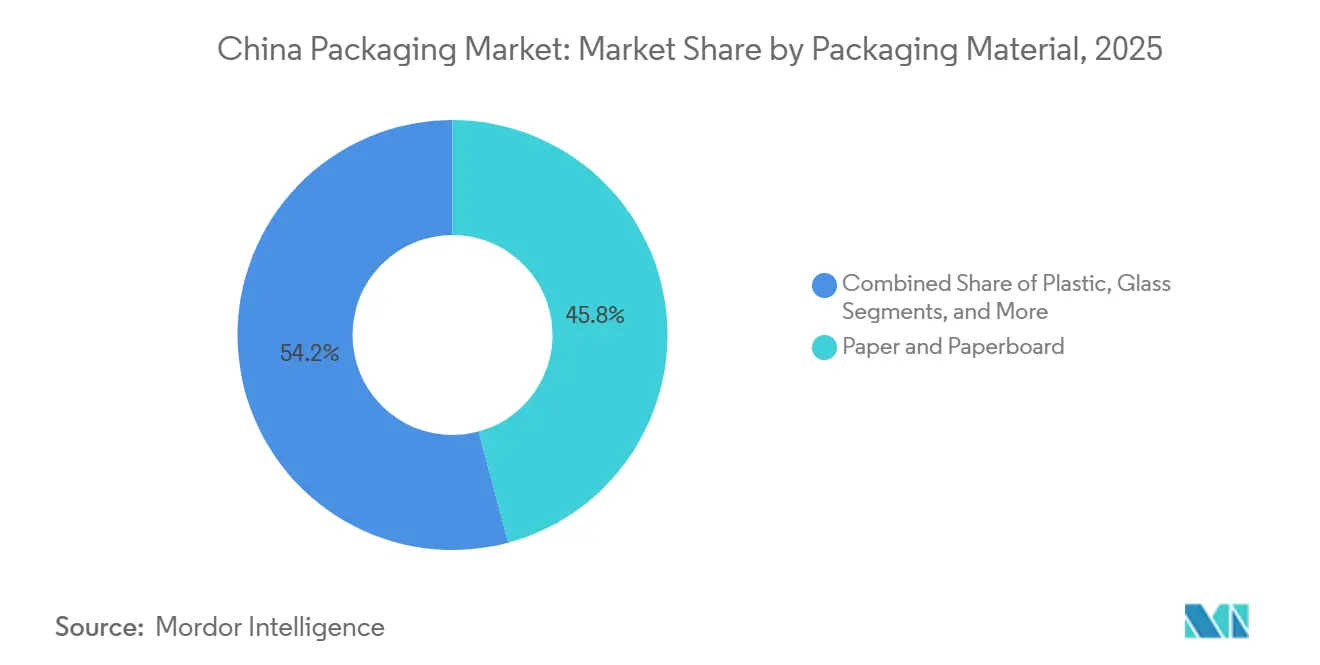

- By packaging material, paper and paperboard held 45.83% of the China packaging market share in 2025, whereas plastics will deliver the quickest expansion with a 4.93% CAGR through 2031.

- By packaging type, primary formats accounted for 51.48% of value in 2025, while secondary formats are forecast to log a 5.03% CAGR to 2031.

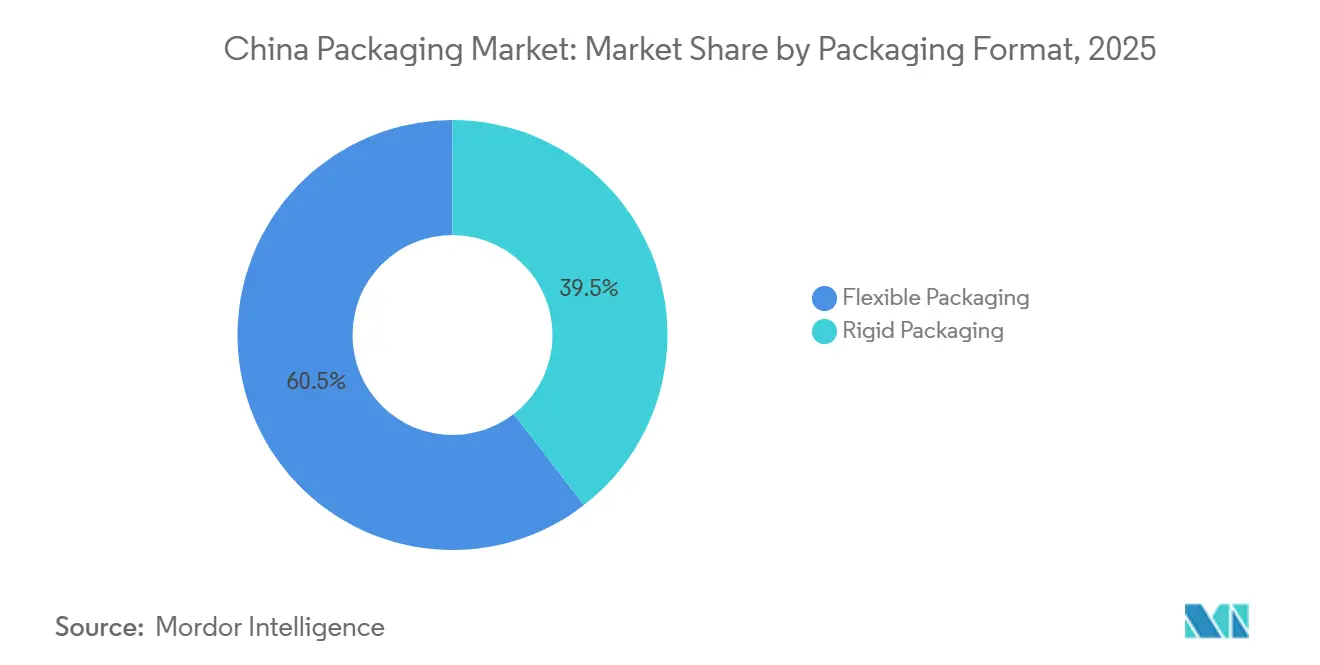

- By packaging format, flexible solutions commanded 60.48% of the China packaging market size in 2025; the same segment is advancing at a 5.11% CAGR.

- By end-user industry, food and beverages led with a 33.91% revenue share in 2025; healthcare and pharmaceutical applications are growing fastest at a 5.08% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Growth of E-Commerce Parcel Volume | +1.2% | National, with concentration in Yangtze River Delta, Pearl River Delta, and Beijing-Tianjin-Hebei cluster | Short term (≤ 2 years) |

| Demand Spike for Sustainable Paper-Based Formats | +0.9% | National, driven by tier-1 and tier-2 cities; spillover to tier-3 cities by 2028 | Medium term (2-4 years) |

| Convenience Ready-to-Drink Food Packaging Adoption | +0.6% | Urban centers (Beijing, Shanghai, Guangzhou, Shenzhen, Chengdu); expanding to lower-tier cities | Medium term (2-4 years) |

| Pharmaceutical Cold-Chain Expansion | +0.7% | National, with early gains in Shanghai, Suzhou, Guangzhou biopharmaceutical clusters | Long term (≥ 4 years) |

| IoT-Enabled Track and Trace Packaging Rollout | +0.4% | Pilot deployments in Yangtze River Delta and Pearl River Delta; national rollout post-2028 | Long term (≥ 4 years) |

| Ultra-Low-Temperature Bio-Pharma Logistics Packaging | +0.3% | Shanghai, Beijing, Guangzhou biomanufacturing hubs; limited provincial reach before 2029 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth Of E-Commerce Parcel Volume

Parcel throughput climbed from 199 billion pieces in 2025 to a targeted 214 billion in 2026, a scale that already eclipses combined U.S. and EU totals.[1]China Daily staff, “China's Parcel Delivery Volume Reaches 199 Billion Pieces in 2025,” China Daily, chinadaily.com.cn Logistics platforms are eliminating in-warehouse repacking by synchronizing supplier carton dimensions with sorting-center equipment, thereby raising demand for shelf-ready secondary boxes with a higher unit value. Rural e-commerce programs rolled out to 1,212 county-level cities in 2025, expanding the addressable base for the China packaging market far beyond coastal megacities. The State Post Bureau now requires 95% of parcels to use recyclable or degradable materials by 2026, which bumps corrugated-box costs by roughly 8% but accelerates the adoption of water-based adhesives and paper tapes.

Demand Spike For Sustainable Paper-Based Formats

Binding green-packaging targets mandate a 40% reduction in single-use plastics versus 2020 by 2030. Nine Dragons Paper is spending RMB 6 billion (USD 828 million) on a Chongqing complex that will deliver 1.7 million tonnes annually of recycled containerboard by 2027.[2]RISI editorial team, “Nine Dragons Paper Announces Major Expansion in Chongqing,” Fastmarkets RISI, risiinfo.com Century Sunshine Paper launched a RMB 20.2 billion (USD 2.79 billion) coated-paperboard project designed to displace polyethylene-laminated cartons. Closed-loop programs using reusable plastic totes can cut greenhouse-gas emissions 63% after 50 rotations, yet deployment remains limited to metropolitan pilot circles, trimming corrugated use by less than 2% of parcel volume.[3]China Dialogue contributors, “China Wrestles with Packaging Waste,” China Dialogue, chinadialogue.net

Convenience Ready-To-Drink Food Packaging Adoption

Urban consumers favor shelf-stable drinks that fit on-the-go lifestyles, fueling uptake of polyethylene terephthalate bottles, aseptic cartons, and retort pouches. Local and global beverage brands are commissioning high-speed aseptic lines that can switch between tea, dairy, and functional drinks without chemical clean-in-place, cutting changeover time from 45 minutes to 20 minutes. Store-brand and livestreaming promotions push smaller pack sizes, which increases the number of units shipped per sales dollar and multiplies demand for lightweight flexible formats within the China packaging market.

Pharmaceutical Cold-Chain Expansion

Cold-chain volume reached 192 million metric tonnes in the first half of 2025, up 15.2% year on year. National Medical Products Administration rules require temperature validation for every shipment, prompting the rise of phase-change materials and vacuum-insulated panels that keep biologics at 2 °C to 8 °C for 120 hours. The emergence of cell and gene therapies requiring storage at minus 80 degrees Celsius is pushing converters to develop vacuum-insulated panels and phase-change materials that extend payload duration from 48 hours to 120 hours, a capability demonstrated by only 12 domestic suppliers as of December 2025.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic Ban and Extended Producer Responsibility Rules | -0.5% | National, with stricter enforcement in Shanghai, Beijing, Shenzhen; uneven provincial compliance | Short term (≤ 2 years) |

| Volatile Pulp and Polymer Feedstock Costs | -0.8% | National, affecting all material segments; coastal mills more exposed to import-price swings | Short term (≤ 2 years) |

| Patchy Provincial Recycling Infrastructure | -0.3% | Inland provinces (Henan, Anhui, Jiangxi) lag coastal regions by 3-5 years in collection rates | Medium term (2-4 years) |

| Reusable Tote Pilots Eroding Urban Corrugated Demand | -0.2% | Beijing, Shanghai, Hangzhou, Shenzhen pilot zones; limited rural penetration before 2029 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-Ban and Extended-Producer-Responsibility Rules

Shanghai’s deposit-return program for polyethylene terephthalate bottles achieved a 68% recovery rate within six months, but inland Jiangsu has yet to finalize its framework, complicating nationwide compliance. The State Post Bureau's June 2025 regulation banning non-degradable plastic mailers for e-commerce parcels by 2026 is accelerating the shift to paper-based alternatives, but degradable plastics certified under GB/T 20197 standards cost 40-60% more than conventional polyethylene, a premium that small online merchants are reluctant to absorb, restraining profit transfer into the China packaging market.

Volatile Pulp and Polymer Feedstock Costs

Bleached hardwood kraft pulp fell from USD 600 per tonne in January 2024 to USD 495 in July 2025, then bounced to USD 540 by December 2025, pressuring converters locked into fixed pricing.[4]RISI price desk, “BHKP Prices Fall to Record Low in China,” Fastmarkets RISI, risiinfo.com Polyethylene followed a 12.5% swing across the same window, tied to crude-oil volatility and refinery shutdowns. Large mills countered by hiking containerboard prices RMB 100-150 per tonne, but mid-tier players saw operating margins slide to 5.7%. This volatility stems from overcapacity in Brazilian and Indonesian pulp mills, which flooded the Chinese market in mid-2025, and subsequent production curtailments that tightened supply by year-end.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: Paper Leadership Faces Plastic Momentum

Paper and paperboard held 45.83% of the China packaging market size in 2025, led by over 50 million tonnes per year of domestic containerboard capacity. Nine Dragons Paper alone operated 28.9 million tonnes by mid-2025, ensuring scale supply to Alibaba and JD.com distribution networks. Corrugated demand continues to concentrate around coastal shipping hubs, yet expansion projects in Chongqing and Hubei show inland appetite for capacity

Plastic is the fastest-growing material at a 4.93% CAGR, reflecting pouch adoption for ready-to-drink beverages and blister packs for pharmaceuticals. Flexible resins offer down-gauging potential and transparency but remain exposed to crude-linked cost swings. Glass retains a niche in baijiu and premium beverages, while metal cans stabilize shelf life in energy drinks, keeping a loyal base in urban convenience channels. Together, alternative materials sit below 5% by value, yet bio-based polymers derived from sugarcane are edging into cosmetics as brand owners pursue renewable content credence.

By Packaging Type: Secondary Formats Capture Efficiency Upside

Primary layers represented 51.48% of the China packaging market in 2025, but secondary formats are pacing ahead at a 5.03% CAGR. Walmart China and Carrefour mandated shelf-ready secondary packaging for 78% of dry-grocery SKUs in 2025, a shift that transfers box-opening and shelf-stacking tasks from store employees to upstream suppliers, cutting labor hours per store by an estimated 12%. This trend is reshaping converter strategies; Lee and Man Paper reported that shelf-ready corrugated boxes commanded a 15% price premium versus standard shipping containers in fiscal 2025, contributing to a 38-47% increase in net profit guidance

Converters receive a 15% price premium on shelf-ready corrugated, protecting margins against pulp volatility. Tertiary stretch-film and strapping track baseline logistics growth but face dilution in closed-loop networks using 2.3 million reusable totes installed by JD Logistics. Reverse-logistics costs and size standardization barriers slow tote penetration beyond megacities, ensuring a runway for conventional shrink film inside the China packaging industry.

By Packaging Format: Flexible Solutions Dominate And Accelerate

Flexible formats delivered 60.48% of the China packaging market share in 2025 and are expanding at a 5.11% CAGR through 2031. Stand-up pouches for dairy products, sauces, and pet food offer 30-40% weight savings compared to rigid bottles, reducing logistics costs and greenhouse gas emissions per unit delivered.

The April 2025 merger of Amcor and Berry Global created a flexible-packaging leader with USD 23 billion in annual sales and 400 facilities globally and a sharpened focus on emerging Asia. Rigid glass and polyethylene terephthalate hold ground in carbonated drinks and alcohol, where gas barrier and pressure requirements persist. Aseptic-carton pioneer Tetra Pak is estimated to hold a considerable share of ambient dairy packaging but faces price competition from local challenger Greatview Aseptic Packaging, which blends domestic service with lower equipment costs.

By End-User Industry: Healthcare Surges Past Food On Biologics Build-Out

Food and beverages supplied 33.91% of revenue in 2025, aligned with digital grocery growth and impulse snack consumption. Ready-to-drink teas and functional beverages leverage ambient distribution packs that align with just-in-time urban supply chains. Energy drinks, led by brands such as Red Bull China and Eastroc Beverage, experienced significant growth in retail sales in 2024, favoring aluminum cans that convey premium positioning and offer recycling infrastructure in urban centers.

Healthcare and pharmaceutical demand is climbing at 5.08% CAGR as China aims to capture 20% of global biologics output by 2030. Shanghai’s cluster now hosts 47 contract development and manufacturing organizations needing minus-80 °C shippers and serialized labels compliant with draft national track-and-trace rules. Beauty and personal-care brands pursue premium glass and airless pumps, and industrial users gravitate to standardized corrugated or returnable crates to shave cycle time.

Geography Analysis

The Yangtze River Delta and Pearl River Delta together generated a considerable share of the China packaging market in 2025, benefiting from dense manufacturing bases, high e-commerce penetration, and superior port access. Shanghai alone piloted Extended Producer Responsibility and achieved a 68% bottle-return rate within half a year, demonstrating regulatory pull on converter investment. Clustering of pharmaceutical and electronics plants in Suzhou and Ningbo boosts orders for anti-static films and cold-chain shippers.

Inland provinces such as Henan, Anhui, and Sichuan saw double-digit parcel growth, with 1,212 county service centers coming online in 2025. Recycling rates, however, vary widely- Zhejiang recovers 82% of packaging waste versus 34% in Gansu- forcing brand owners to budget 15-20% more for nationwide EPR compliance. Nine Dragons Paper’s Chongqing mill, due in 2027, positions the firm to supply fast-growing western catchments.

Remote western regions such as Xinjiang and Tibet remain underpenetrated, with per-capita packaging spend below 30% of that of their coastal peers. Belt and Road freight corridors are opening small but strategic export channels for converters, enabling them to ride outbound volumes into Central Asia while backhauling recycled fiber. Such flows diversify revenue streams and soften dependence on core eastern seaboards.

Competitive Landscape

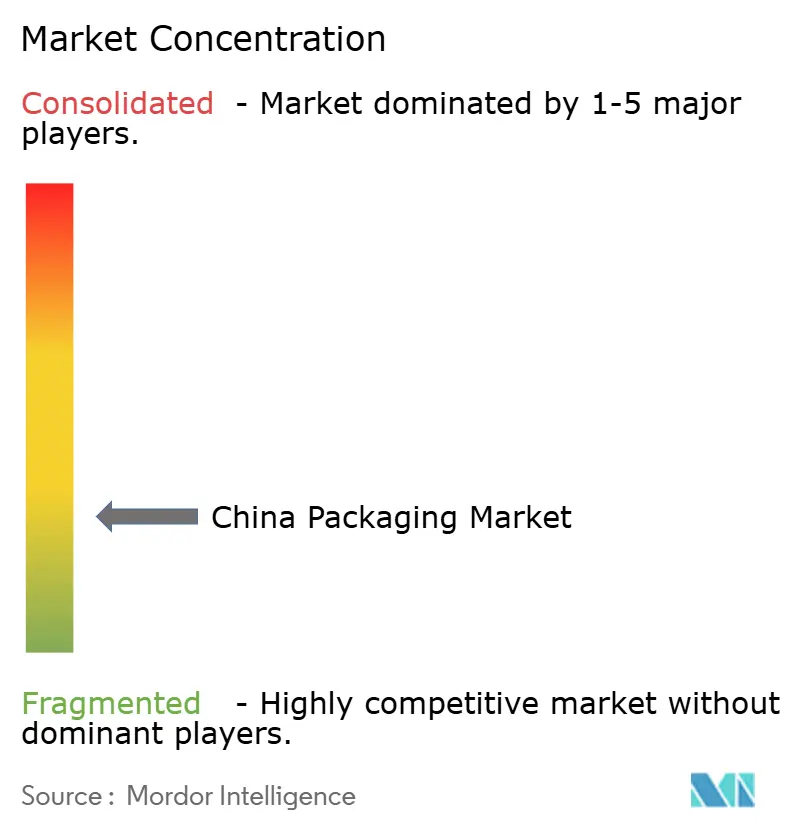

The China packaging market remains fragmented; the five largest suppliers made up a considerable share in 2025. Containerboard is anchored by Nine Dragons Paper, Lee and Man Paper, and Shanying International, which together account for around 18% of linerboard and medium capacity. Scale enables them to negotiate pulp contracts and curb margin erosion via synchronized downtime, such as the 270,000-tonne production halt during Lunar New Year 2026.

State capital is reshaping metal packaging. China Baowu Steel bought China Packaging and Materials Company for HKD 7.65 billion (USD 978 million) in 2024, uniting upstream steel supply with can manufacturing and securing roughly 17% domestic share. Overseas expansion is also gaining momentum, Jihong Group opened a USD 45 million UAE plant in February 2026 to offset softening cigarette volumes at home.

Global consolidation is redrawing flexible-packaging supply maps. The Amcor and Berry Global union promises USD 650 million in synergies and deeper penetration of the China packaging market, while International Paper’s tie-up with DS Smith concentrates corrugated heft in trans-regional trade lanes. Technology plays on the horizon include IoT labels and minus-80 °C shippers, niches served by fewer than 15 qualified domestic providers, offering high-margin refuge from commodity cycles.

China Packaging Industry Leaders

Amcor Plc

Nine Dragons Paper (Holdings) Ltd.

Lee and Man Paper Manufacturing Ltd.

YUTO Packaging Technology Co., Ltd.

Hexing Packaging Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Jihong Group started up a USD 45 million UAE facility producing 24 million cigarette cases a year, the converter’s first Middle East site.

- January 2026: Nine Dragons Paper scheduled a 270,000-tonne maintenance shutdown across January-February, which tightened supply and lifted domestic linerboard prices.

- December 2025: UPM and Sappi formed a graphic-paper joint venture, freeing pulp that will be diverted into global packaging grades.

- December 2025: Shanying International received a RMB 70 million (USD 9.7 million) subsidy for its green recycling plant, expected to process 2 million tonnes of recovered paper by 2027.

China Packaging Market Report Scope

Packaging is the process of enclosing or protecting products using containers to facilitate distribution, identification, storage, promotion, and use. The packaging industry in China is showing growth trends across various end-user industries, driven by increasing urbanization, rising disposable incomes, and changing consumer preferences. The food and beverage, e-commerce, and healthcare sectors mainly contribute to the expansion of China's packaging industry.

The China Packaging Market Report is Segmented by Packaging Material (Plastic, Paper and Paperboard, Glass, Metal, and Other Materials), Packaging Type (Primary Packaging, Secondary Packaging, and Tertiary Packaging), Packaging Format (Rigid Packaging and Flexible Packaging), and End-User Industry (Food and Beverages, Healthcare and Pharmaceutical, Beauty and Personal Care, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Packaging Material

| Plastic |

| Paper and Paperboard |

| Glass |

| Metal |

| Other Materials |

By Packaging Type

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

By Packaging Format

| Rigid Packaging |

| Flexible Packaging |

By End-User Industry

| Food and Beverages |

| Healthcare and Pharmaceutical |

| Beauty and Personal Care |

| Industrial |

| Other End-User Industries |

| By Packaging Material | Plastic |

| Paper and Paperboard | |

| Glass | |

| Metal | |

| Other Materials | |

| By Packaging Type | Primary Packaging |

| Secondary Packaging | |

| Tertiary Packaging | |

| By Packaging Format | Rigid Packaging |

| Flexible Packaging | |

| By End-User Industry | Food and Beverages |

| Healthcare and Pharmaceutical | |

| Beauty and Personal Care | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the China packaging market?

The market is valued at USD 229.11 billion in 2026, on its way to USD 290.73 billion by 2031.

How fast is flexible packaging growing in China?

Flexible formats are advancing at a 5.11% CAGR through 2031, reflecting their 60.48% share in 2025.

Which material leads market share in China’s packaging sector?

Paper and paperboard hold the top position with a 45.83% share as of 2025.

Why is secondary packaging gaining traction among retailers?

Shelf-ready secondary boxes cut in-store labor by roughly 12%, prompting a forecast 5.03% CAGR to 2031.

What drives the surge in pharmaceutical packaging demand?

Expansion of biologics manufacturing and cold-chain logistics is pushing healthcare packaging at a 5.08% CAGR to 2031.

Page last updated on: