Over-The-Air (OTA) Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.35 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Over-The-Air (OTA) Testing Market Analysis by Mordor Intelligence

The Over-The-Air Testing Market size was valued at USD 2.23 billion in 2025 and is estimated to grow from USD 2.35 billion in 2026 to reach USD 3.01 billion by 2031, at a CAGR of 5.08% during the forecast period (2026-2031).

This growth trajectory is shaped by an installed base of far-field chambers that still accounts for 48% of revenue, a 13.4% annual expansion in software-centric platforms that automate test orchestration, and rapid uptake of satellite non-terrestrial network validation. Demand rises in tandem with 5G New Radio rollouts, healthcare wearables, and private-5G factories, while capital-intensive chamber builds and a scarcity of millimeter-wave expertise temper adoption. Competitive intensity is sharpening as OEM-owned labs and pay-per-test providers offer alternatives to traditional certification houses, pushing incumbents toward integrated hardware-software offerings and regional capacity additions.

Key Report Takeaways

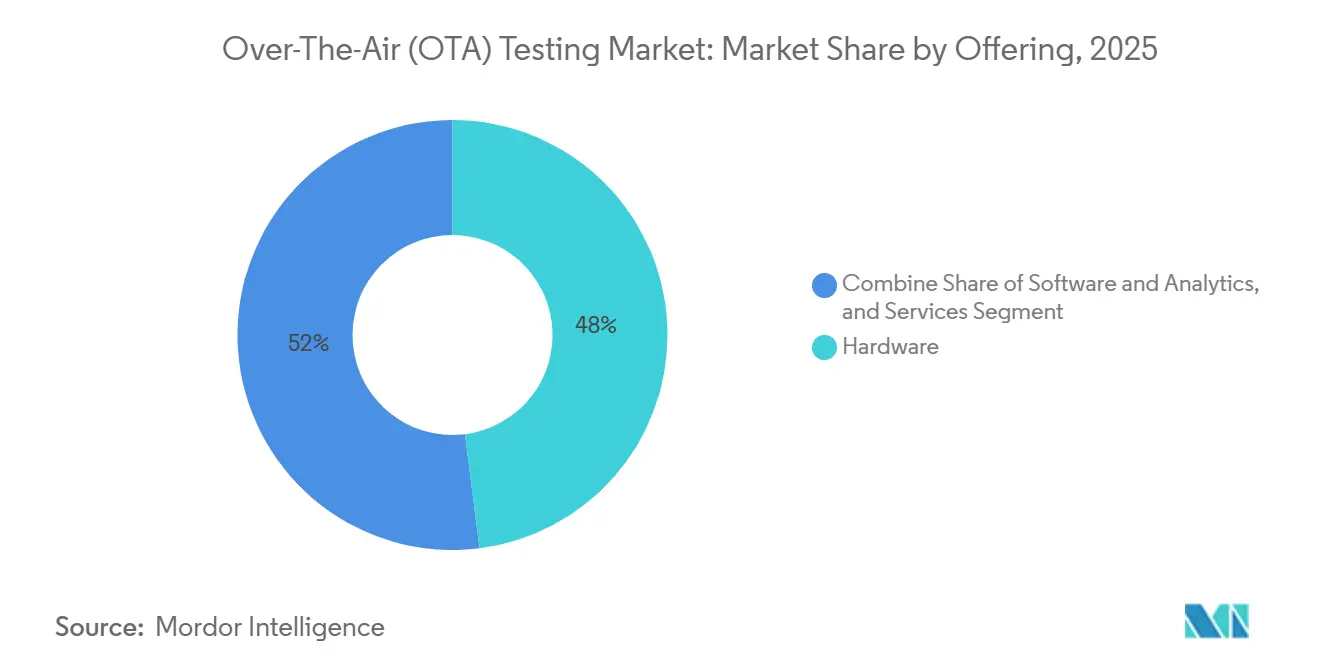

- By offering, software and analytics platforms led with 5.99% CAGR through 2031, while hardware maintained 48% revenue share in 2025.

- By technology, 5G New Radio captured 37.5% revenue share in 2025; satellite non-terrestrial networks are projected to grow at 6.21% CAGR to 2031.

- By test type, conformance and certification held 33.2% of Over-The-Air testing market share in 2025, whereas interoperability testing is advancing at a 5.78% CAGR to 2031.

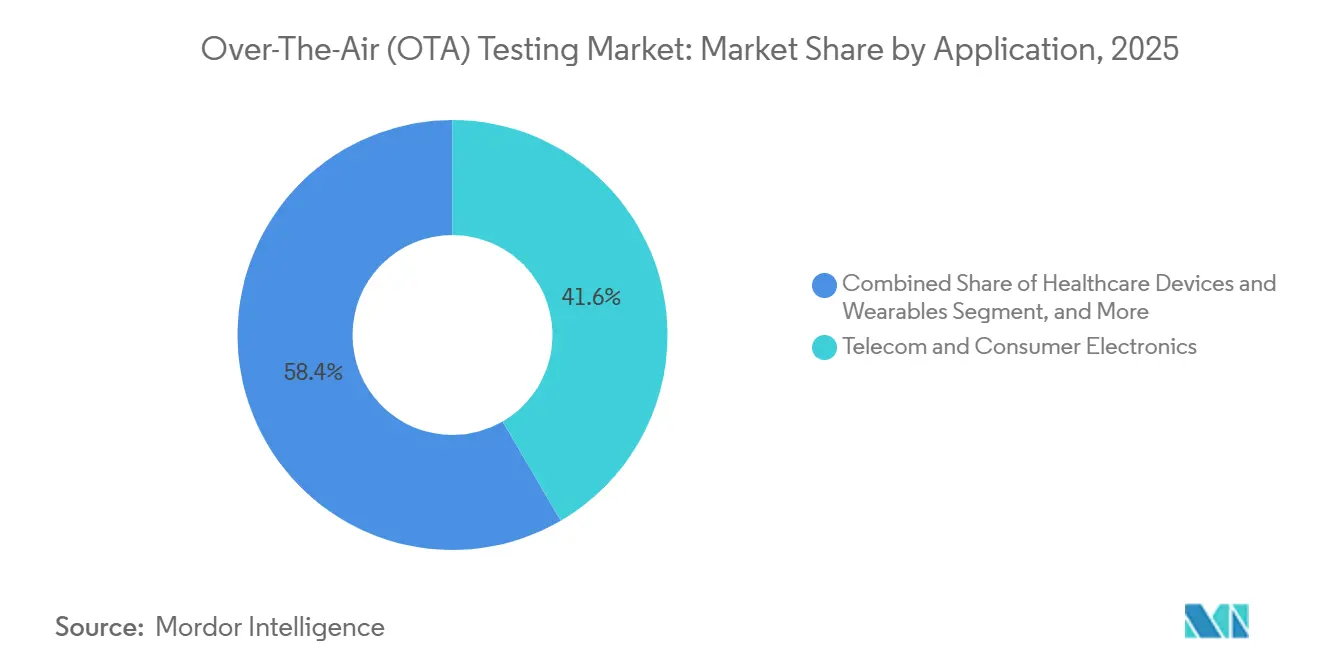

- By application, telecom and consumer electronics commanded 41.6% of the Over-The-Air testing market size in 2025; healthcare wearables are expanding at 6.05% CAGR through 2031.

- By test environment, far-field chambers retained 38.9% revenue share in 2025, while near-field systems are forecast to rise at 5.85% CAGR to 2031.

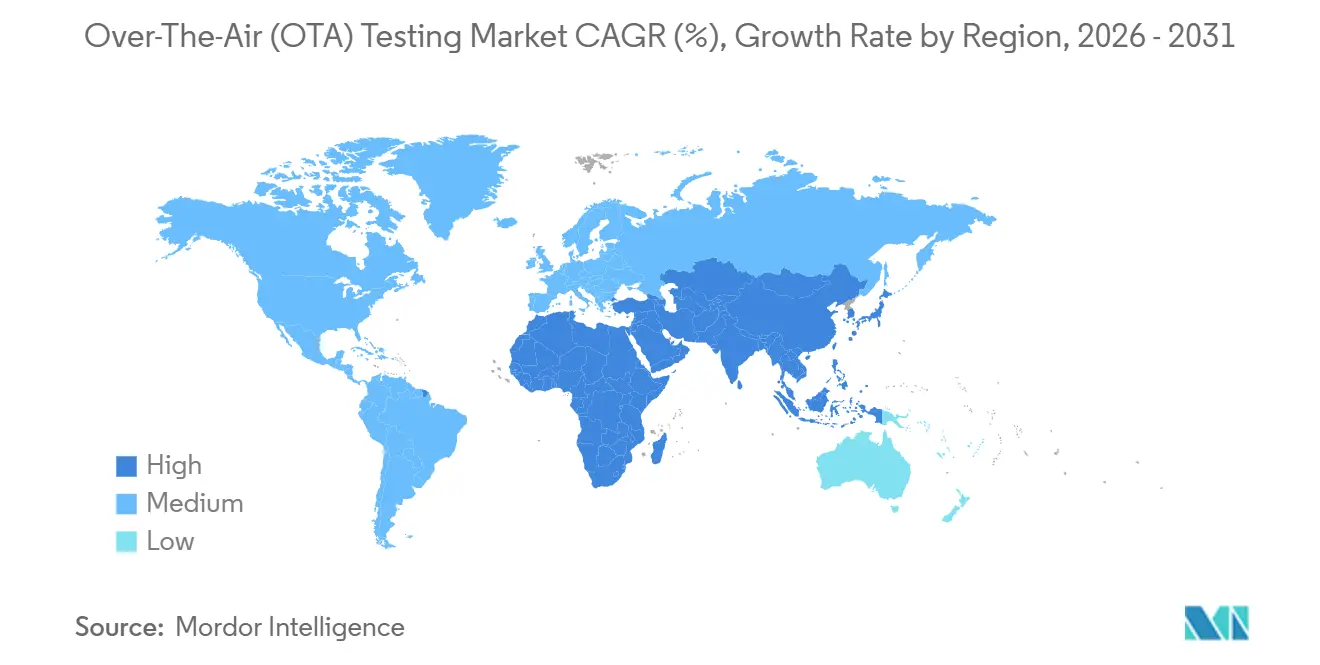

- By geography, Asia Pacific led with 32.4% revenue share in 2025 and is growing at 5.56% CAGR, the fastest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Over-The-Air (OTA) Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G Non-Standalone and Stand-Alone Deployments Requiring New Conformance Protocols | +1.20% | Global, with concentration in Asia Pacific and North America | Medium term (2-4 years) |

| Surging OTA Compliance Demand for mmWave and Massive-MIMO Antennas in Consumer Devices | +1.00% | North America, Europe, Asia Pacific core markets | Short term (≤ 2 years) |

| Automotive OEM Shift to Software-Defined and V2X Connectivity Platforms in North America | +0.80% | North America, with spill-over to Europe | Medium term (2-4 years) |

| Industrial Private-5G Roll-outs in Europe for Smart Factories Requiring Robust RF Validation | +0.60% | Europe, expanding to Asia Pacific manufacturing hubs | Long term (≥ 4 years) |

| Rapid Certification Cycles Mandated by CTIA and GCF for IoT Modules Below USD 10 BOM | +0.70% | Global, particularly Asia Pacific device ecosystem | Short term (≤ 2 years) |

| Accelerating Satellite-to-Device Direct-Link Constellations Necessitating New Near-Field OTA Protocols | +0.90% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Non-Standalone and Stand-Alone Deployments Requiring New Conformance Protocols

Stand-alone 5G cores reached mass-market status in 2025 as more than 300 operators enabled network slicing and low-latency services. Third Generation Partnership Project Release 17 introduced test cases for 64-stream massive-MIMO above 3.5 GHz, compelling laboratories to install dual-polarized probe arrays capable of simultaneous sampling.[1]3GPP, “Release 17 Specifications,” 3gpp.org The Cellular Telecommunications Industry Association tightened its OTA 5.9 specification to include radiated spurious-emission checks at frequencies beyond 52.6 GHz, forcing device makers to upgrade legacy fixtures. With non-stand-alone architectures being phased out, smartphone vendors are compressing dual-mode validation windows, migrating budgets to stand-alone-specific instrumentation, and fragmenting demand across captive design-center labs.[2]Ericsson, “5G Networks and Services,” ericsson.com

Surging OTA Compliance Demand For mmWave And Massive-MIMO Antennas in Consumer Devices

Flagship phones now integrate up to 16 phased-array elements, each requiring total radiated power and isotropic sensitivity sweeps over 360-degree azimuth and 180-degree elevation planes. Federal Communications Commission rules for 24.25-29.5 GHz bands extend chamber occupancy by 40% versus sub-6 GHz tests, straining global capacity.[3]FCC, “Equipment Authorization,” fcc.gov Apple’s 2025 millimeter-wave launches sparked a surge of over-the-air orders from contract manufacturers, pushing lead times for multi-probe systems beyond 18 months. Concurrently, China Mobile’s 192-element base stations require reciprocity calibration, creating demand for portable near-field scanners that validate beamforming without service downtime.

Accelerating Satellite-To-Device Direct-Link Constellations Necessitating New Near-Field OTA Protocols

AST SpaceMobile’s September 2025 voice call to an unmodified handset and Starlink’s FCC-approved supplemental coverage exemplify a shift toward direct-to-device services. 3GPP non-terrestrial test cases now include beam tracking below 30-degree elevation and Doppler shifts above 40 kHz, scenarios that challenge conventional far-field chambers. Certification bodies issued their first type-approval under the new annex in December 2025, confirming market readiness and stimulating investment in compact ranges with orbital-motion emulators.

Automotive OEM Shift to Software-Defined and V2X Connectivity Platforms in North America

General Motors plans to equip all post-2027 models with Cellular Vehicle-to-Everything modems, Ford’s BlueCruise relies on real-world multipath replay, and the National Highway Traffic Safety Administration proposes mandatory basic safety messages for model-year 2029 vehicles. These moves redirect validation budgets toward over-the-air replay chambers able to emulate urban and highway fading profiles, shifting demand from static conformance rigs to dynamic scenario testbeds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Anechoic and Reverberation Chambers Discouraging Adoption by Tier-2 Labs | -0.90% | Global, particularly acute in South America and Africa | Long term (≥ 4 years) |

| Technical Skill Scarcity for mmWave Near-Field-to-Far-Field Transform Algorithms | -0.60% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Lack of Harmonised Global Standards for LPWAN OTA Testing Delaying Market Convergence | -0.40% | Global, fragmented across regional certification bodies | Long term (≥ 4 years) |

| Supply-Chain Volatility of RF Absorber Materials Inflating Test Infrastructure Costs | -0.50% | Global, with supply concentrated in North America and Europe | Short term (≤ 2 years) |

| Rising Cyber-Security Concerns over Remote OTA Testbed Connectivity in Shared Facilities | -0.30% | North America and Europe automotive and defense sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Anechoic and Reverberation Chambers Discouraging Adoption by Tier-2 Labs

A 5-meter millimeter-wave chamber costs USD 2.5-4 million, while reverberation rooms run USD 0.8-1.2 million, outlays that emerging-market labs struggle to justify at sub-60% utilization. The International Electrotechnical Commission’s 2024 stirrer-efficiency revision shortened refurbishment cycles, tightening return-on-investment timelines. Consequently, Latin American and African test centers outsource to global networks, increasing lead times and concentrating revenue among the top five certification houses.

Technical Skill Scarcity For mmWave Near-Field-To-Far-Field Transform Algorithms

Fewer than 200 engineers worldwide master spherical near-field transforms, modal-expansion theory, and fast Fourier transforms on non-uniform grids. Keysight field-support tickets for millimeter-wave troubleshooting jumped 65% year-over-year, and only 120 engineers completed Rohde and Schwarz’s certification course in 2025. The skills gap elevates dependence on automated alignment routines that remain in pilot phase, slowing throughput at a time of mounting demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Reshape Hardware-Centric Workflows

The Over-The-Air testing market size for hardware stood at 48% of total revenue in 2025, reflecting entrenched investments in anechoic chambers, compact ranges, and instrument stacks. Software and analytics platforms, however, are expanding at a 5.99% CAGR as cloud-hosted orchestration tools slash report-generation time and correlate multi-site measurements in real time. Continuous-integration pipelines now call test scripts through application programming interfaces, turning chambers into on-demand assets rather than static fixtures.

Services round out the category, with OEMs outsourcing Cellular Vehicle-to-Everything validation to specialist labs that package conformance, electromagnetic compatibility, and safety submissions into unified campaigns. The momentum behind software-defined radio instrumentation further erodes discrete hardware demand, as a single reconfigurable transceiver can span sub-6 GHz and millimeter-wave bands. This shift favours vendors capable of bundling code libraries, analytics dashboards, and remote-access controls with modular enclosures, positioning them for recurring revenue streams as subscription models replace one-off equipment sales.

By Technology: Satellite Non-Terrestrial Networks Outpace Legacy Protocols

5G New Radio commanded 37.5% share in 2025, underlining its status as the baseline for modern handset launches and fixed-wireless access points. Yet satellite direct-link services represent the fastest-growing slice, advancing at 6.21% CAGR and forcing laboratories to integrate orbital-motion emulators, high-dynamic-range Doppler sources, and low-elevation beam trackers. Long-Term Evolution and machine-type evolutions remain staples in industrial Internet-of-Things segments where decade-long lifecycles demand relentless backward compatibility.

Conversely, second- and third-generation cellular protocols fade as operators reform spectrum, though certification houses still process late-cycle devices destined for emerging markets. Wi-Fi 6, Wi-Fi 7, Bluetooth low energy, and ultra-wideband round out the roster, with coordinated beamforming and 320-MHz channels driving fresh over-the-air requirements. Laboratories capable of multi-protocol, multi-band validation under a single roof stand to capture cross-technology synergies that legacy single-band facilities cannot match.

By Test Type: Interoperability Validation Gains Momentum

Conformance and certification accounted for 33.2% of 2025 revenue, reflecting their non-optional status for market access. Interoperability testing, however, emerges as the fastest-expanding subset at 5.85% CAGR, propelled by open radio access network disaggregation and non-terrestrial roaming scenarios that demand seamless handoffs across heterogeneous infrastructure.

Antenna performance testing remains the technical foundation, covering total radiated power, isotropic sensitivity, and effective isotropic radiated power metrics across full spherical sweeps. Production-line screening of telematics units and wearables rounds out the mix, with automotive suppliers moving toward 100% radiated checks to cut field-failure rates. Convergence pressures are pushing certification bodies to bundle conformance and interoperability in unified campaigns, forcing labs to maintain both regulatory rigor and real-world scenario expertise.

By Application: Healthcare Wearables Drive Fastest Expansion

Telecom and consumer electronics held 41.6% share in 2025 as smartphones, tablets, and hotspots marched through mandatory Cellular Telecommunications Industry Association and Global Certification Forum gates. Healthcare wearables represent the fastest-growing pocket, expanding at 6.05% CAGR on the back of Food and Drug Administration pre-market filings for remote patient monitoring devices operating in protected telemetry bands.

Automotive and transportation applications benefited from Cellular Vehicle-to-Everything mandates, while industrial smart-factory deployments used private-5G networks to validate ultra-reliable low-latency communication for robots and programmable logic controllers. Aerospace and defense remained niche yet lucrative, driven by anti-jamming and frequency-hopping test requirements. Smart-home segments lagged due to fragmented Matter-over-Thread standards, but harmonization efforts could unlock new demand once certification pathways coalesce.

By Test Environment: Near-Field Systems Capture Compact-Device Demand

Far-field anechoic chambers retained 38.9% revenue share in 2025, anchoring regulatory submissions that still favour classical quiet zones. Near-field systems, however, are rising at 5.85% CAGR thanks to their small footprint and rapid scan times for electrically small devices such as wearables. Compact antenna test ranges cater to automotive suppliers needing plane-wave illumination without 10-meter chambers, while reverberation rooms service high-volume Internet-of-Things modules under statistical field distributions.

Hybrid facilities that fuse far-field, near-field, and reverberation capabilities into modular enclosures remain premium investments, but they future-proof capacity against shifting protocol suites. Vendors that package multi-mode chambers with unified control software are best placed to ride this transition, especially as Release 18 test cases demand flexible setups able to validate terrestrial-to-satellite roaming in a single campaign.

Geography Analysis

Asia Pacific held 32.4% of 2025 revenue and is projected to expand at a 5.56% CAGR through 2031, buoyed by China’s certification pipeline that cleared more than 1,200 5G smartphones in 2025 and India’s Telecommunications Engineering Centre fast-track for domestic brands. Local device makers increasingly house captive labs to cut lead times yet still rely on external providers for millimeter-wave validation until homegrown expertise matures. Government incentives in South Korea and Japan further elevate regional demand by subsidizing non-terrestrial test infrastructure.

North America ranked second as automotive OEMs funnelled budgets into Cellular Vehicle-to-Everything validation and the Federal Communications Commission enforced stringent millimeter-wave emissions limits. Captive labs mushroomed around Detroit and Silicon Valley, but independent certifiers sustained volumes by specializing in replay chambers that emulate real-world multipath and Doppler. Canada contributed incremental growth via private-5G deployments in resource extraction sites that require ruggedized device validation.

Europe posted steady gains anchored by smart-factory rollouts in Germany, France, and the Nordics that mandate over-the-air verification of time-sensitive networking controllers. Reverberation chambers gained traction for industrial Internet-of-Things modules, while satellite non-terrestrial tests clustered in Munich and Toulouse. South America saw modest momentum led by Brazil’s 5G launches, yet a paucity of accredited labs funnelled certifications to North American facilities, elongating schedules. Middle East and Africa remain nascent, though the African Telecommunications Union’s mutual-recognition framework could catalyse regional capacity as spectrum auctions proceed.

Regulatory Landscape

OTA testing requirements are shaped by telecom equipment authorization rules, industry certification programs, and fast-moving 3GPP-driven conformance methods. In the United States, the Federal Communications Commission (FCC) tightened oversight of the certification ecosystem in August 2025 by adopting rules that require recognized Telecommunications Certification Bodies (TCBs), test labs, and accreditation bodies to certify they are not owned or controlled by prohibited entities and to report 5% or greater equity or voting interests. This increases due diligence burdens for cross-border lab networks.

In May 2026, the FCC advanced a Second Further Notice of Proposed Rulemaking that considers prohibiting recognition of test labs and TCBs located in non-Reciprocal Territories, bringing geopolitics and reciprocity into lab selection and capacity planning. On the technical side, 3GPP updates continue to raise the bar for radiated measurements, including March 2026 updates to 3GPP specifications for enhanced OTA test methods for NR FR1 TRP/TRS and newer methodologies described in Release 19 technical reports for FR2 multi-panel scenarios. In parallel, CTIA and PTCRB procedures (for example NAPRD03 updates) increasingly require clearer justifications and tighter controls around MIMO OTA changes in lab reports.

Competitive Landscape

The top five equipment vendors and top three certification providers controlled roughly 60% of global revenue in 2025, indicating moderate concentration. Keysight Technologies, Rohde and Schwarz, and Anritsu anchor the equipment tier with broad instrumentation portfolios integrated into software automation suites. Chamber specialists ETS-Lindgren and Microwave Vision Group compete on modular designs that shorten lead times for emerging bands. Certification giants SGS, Intertek, and Bureau Veritas race to add millimeter-wave and satellite capabilities as OEMs build in-house labs.

Emerging disruptors such as BluFlux and CETECOM promote cloud-connected pay-per-test services that lower entry barriers for startups, while VIAVI Solutions leverages machine-learning routines to cut chamber occupancy time by 25%, boosting asset utilization. White-space opportunities loom in reconfigurable intelligent surfaces and terahertz-band testing, where measurement uncertainty still impedes commercial roll-out. Competitive advantage is shifting toward vendors that can bundle hardware, orchestration software, analytics, and certification under subscription models that mirror agile development cycles.

Incumbents counter disruption through acquisitions: Spirent’s 2025 purchase of Labforge integrated continuous-integration hooks into over-the-air workflows, while Microwave Vision Group’s Orbit FR deal halved chamber footprints for vehicle-mounted antennas. Overall, price competition remains secondary to time-to-certificate, with laboratories commanding premiums for guaranteed slot access during device launch windows.

Over-The-Air (OTA) Testing Industry Leaders

Intertek Group plc

Bureau Veritas S. A.

Anritsu Corporation

Rohde & Schwarz GmbH & Co KG

Keysight Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is opening around higher-complexity radiated validation, where labs and vendors combine chambers, emulation, and software orchestration to support massive MIMO, beamforming, and emerging terrestrial-satellite test cases within a single workflow. A clear sign of investment is VIAVI Solutions expanding its VALOR Automated Lab-as-a-Service facility in Chandler, Arizona (April 2025) with an RF-shielded anechoic chamber supporting massive MIMO and beamforming OTA validation, reflecting the market shift from single-purpose conformance rigs to multi-vendor, multi-layer OTA validation.

Opportunities also exist in scalable, programmable, end-to-end OTA platforms that reduce manual reconfiguration across 4G, 5G, and Wi-Fi, helping address throughput constraints created by compressed device release cycles and limited mmWave expertise. Spirent Communications introduced its Landslide E20 OTA solution (June 2025) as a rackmount, scalable platform for carrier-grade labs, reinforcing demand for automation-centric test environments. On the standards roadmap, ongoing 3GPP work items and technical reports targeting OTA method enhancements for NR, including FR1 TRP/TRS refinements and FR2 OTA Phase 3 study activity, expand what must be validated over the air, supporting demand for near-field systems, chamber upgrades, and cloud-managed test orchestration that can keep pace with new test cases and multi-protocol coexistence requirements.

Recent Industry Developments

- June 2026: Rohde & Schwarz supplied BTL Laboratory in Taiwan with an R&S TS8991 OTA test system designed to be compliant with CTIA certification requirements. The installation strengthens accredited OTA capacity in Asia Pacific and supports regional device makers that need faster access to certification-grade radiated testing for advanced wireless features.

- March 2026: Rohde & Schwarz acquired Software Radio Systems (SRS), adding software-defined mobile communications capabilities to its test and measurement portfolio. The acquisition increases in-house depth in programmable radio and software stacks used in 5G, non-terrestrial networking, and AI-assisted testing workflows that are increasingly coupled to OTA validation.

- December 2024: Rohde & Schwarz and ETS-Lindgren partnered to offer integrated OTA testing solutions for next-generation wireless technologies. By combining instrumentation and chamber infrastructure into coordinated offerings, the partnership supports faster deployment of turnkey test environments for labs upgrading to new bands and more complex antenna systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The OTA testing market is defined as revenues earned from testing wireless devices and antennas over the air to verify radiated performance and compliance in real operating conditions. This includes hardware setups, the relevant related software, and testing services.

Scope exclusions: It excludes device manufacturing revenues and general lab testing that is not based on radiated OTA measurements (such as purely conducted tests).

Segmentation Overview

- By Offering

- Hardware

- Chambers (Anechoic, Reverberation, Compact Range)

- Instrumentation (Signal Generators, Spectrum Analysers, Controllers)

- Software and Analytics

- Services

- Testing and Certification Services

- Consulting and Integration

- Hardware

- By Technology

- 5G NR (Sub-6 GHz and mmWave)

- LTE, LTE-A and LTE-M

- UMTS and WCDMA

- GSM and CDMA

- Wi-Fi 6, Wi-Fi 7 and Wi-Fi HaLow

- Bluetooth and UWB

- LPWAN (NB-IoT, LoRaWAN, Sigfox)

- By Test Type

- Antenna Performance (TRP, TIS, EIRP, EIS)

- Conformance and Certification

- Compatibility and Inter-operability

- Production and End-of-Line

- By Application

- Telecom and Consumer Electronics

- Automotive and Transportation

- Industrial and Manufacturing IoT

- Aerospace and Defense

- Healthcare Devices and Wearables

- Smart Home and Building Automation

- By Test Environment

- Far-Field Anechoic Chambers

- Compact Antenna Test Range

- Near-Field Systems

- Reverberation Chambers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia Pacific

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map market context and anchor the major demand signals that drive OTA testing spend. We relied on public sources such as ITU and national telecom regulator releases for spectrum and rollout context, 3GPP and IEEE standards documentation for test requirements, and FCC and ETSI guidance for certification and compliance cues.

For demand pacing, we reviewed sources such as GSMA device and mobile ecosystem updates, customs and trade statistics where relevant for test equipment movement, and peer reviewed papers that discuss TRP and TIS measurement practices. Company filings, investor presentations, and credible press were also checked to understand product launches, test capacity expansions, and regional investment cycles. Select paid subscriptions were used only for structured company financials, patent landscaping, and news tracking, so we would not miss smaller public signals. The desk sources listed are illustrative only, and we used many other public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased for OTA testing, and what gets bundled into adjacent wireless testing budgets. We spoke with lab operators, test service teams, device makers, and component suppliers across APAC, EMEA, and the Americas. The goal was to confirm pricing ranges, utilization patterns, and the split between in-house labs and outsourced testing, and then to sanity check assumptions used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 47% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 29% |

| Smaller Players: 17% | Managers: 48% | Americas: 24% |

Market-Sizing & Forecasting

Market size is built using a top-down and bottom-up approach. We use standards-led test requirements and device rollout intensity to reconstruct the addressable OTA testing demand pool, then cross-check against selective supplier and lab revenue approximations. Practically, we start from wireless device shipment momentum and the expected share of devices that go through OTA validation for each major technology generation, then translate that demand into testing spend using typical test cycles and pricing.

Key inputs include the pace of 5G NR and LTE deployments, the mix of device categories that require radiated testing (for example automotive connectivity modules versus consumer devices), lab capacity additions such as new chambers and CATR systems, compliance activity linked to certification pathways, and typical ASP movement for services as test complexity increases. Where data is thin, we handle gaps through ranges agreed in interviews, then select conservative midpoints and run sensitivity checks.

Forecasting is done using scenario analysis supported by simple multivariate regression. Spend is tied to explanatory variables such as device shipment outlook, 5G penetration, and test complexity indicators, and then adjusted based on expert expectations about certification intensity and outsourcing trends. The final forecast is reviewed region by region so mix shifts between APAC, EMEA, and the Americas are retained in the global total.

Data Validation & Update Cycle

Validation is done through multiple checks so the market total stays consistent with real-world signals. We compare model outputs against independent indicators such as lab utilization commentary, certification and compliance activity levels, and large capex announcements for chambers and test systems. These checks help flag values that change too fast or too slow.

When anomalies show up, assumptions are revisited and respondents are re-contacted to confirm whether the issue is a one-off event or a structural change in testing mix. Before sign-off, the model and logic are reviewed by analysts in steps to ensure calculations, unit conversions, and regional rollups align. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery pass so clients receive the latest view.

Mordor Intelligence's Ota Testing Market Size Versus Other Published Estimates

Published OTA testing market numbers often vary because the line between OTA-only work and broader wireless testing is drawn differently, and not every estimate handles services, software, and lab hardware in the same way. Timing also affects totals, since base year selection and currency conversions can shift a USD figure even when the story is similar.

The main gap comes from whether adjacent activities, like general RF conformance work that is not radiated OTA, are included in the market, and how aggressively pricing is assumed to rise as 5G and complex antennas spread. Some sources also use a different base year and apply a faster growth curve without clearly tying it back to lab capacity, utilization, and certification volumes. That can inflate near-term totals compared with how Mordor Intelligence counts OTA testing spend tied to TRP and TIS type measurements.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.35 B (2026) | |

| Industry Publisher A | USD 2.62 B (2026) | Uses a broader interpretation of OTA testing that can blend in non-radiated wireless testing services, and applies a higher assumed price uplift as complexity rises. This increases the 2026 total. |

| Global Research Firm B | USD 2.37 B (2025) | Anchors the model on a different base year and may not fully normalize for year-to-year currency timing. The implied growth curve is less clearly linked to lab capacity additions and utilization checks. |

Overall, the spread is mostly explained by scope and starting-year choices, rather than disagreement about the core demand drivers. By keeping the sizing tied to observable testing requirements, capacity signals, and interview-validated pricing ranges, the output is easier to trace and repeat when the market is updated.

Key Questions Answered in the Report

What is the growth outlook for the Over-The-Air testing market to 2031?

The market is projected to rise from USD 2.35 billion in 2026 to USD 3.01 billion by 2031, advancing at a 5.11% CAGR.

Which segment is expanding the fastest?

Satellite direct-to-device non-terrestrial network testing posts the quickest growth at 6.21% CAGR through 2031.

Why is software becoming more important in Over-The-Air validation?

Cloud-based orchestration, automated reporting, and analytics cut certification cycles and support agile device releases, pushing software revenue to a 13.4% CAGR.

How are healthcare wearables influencing demand?

Food and Drug Administration pre-market filings for wireless telemetry drive a 6.05% CAGR in healthcare wearable testing, the fastest among applications.

What regions lead Over-The-Air test demand?

Asia Pacific commands the largest share at 32.4% and grows the fastest at 5.56% CAGR, backed by high device-certification volumes in China and India.

Page last updated on: