Osmometers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

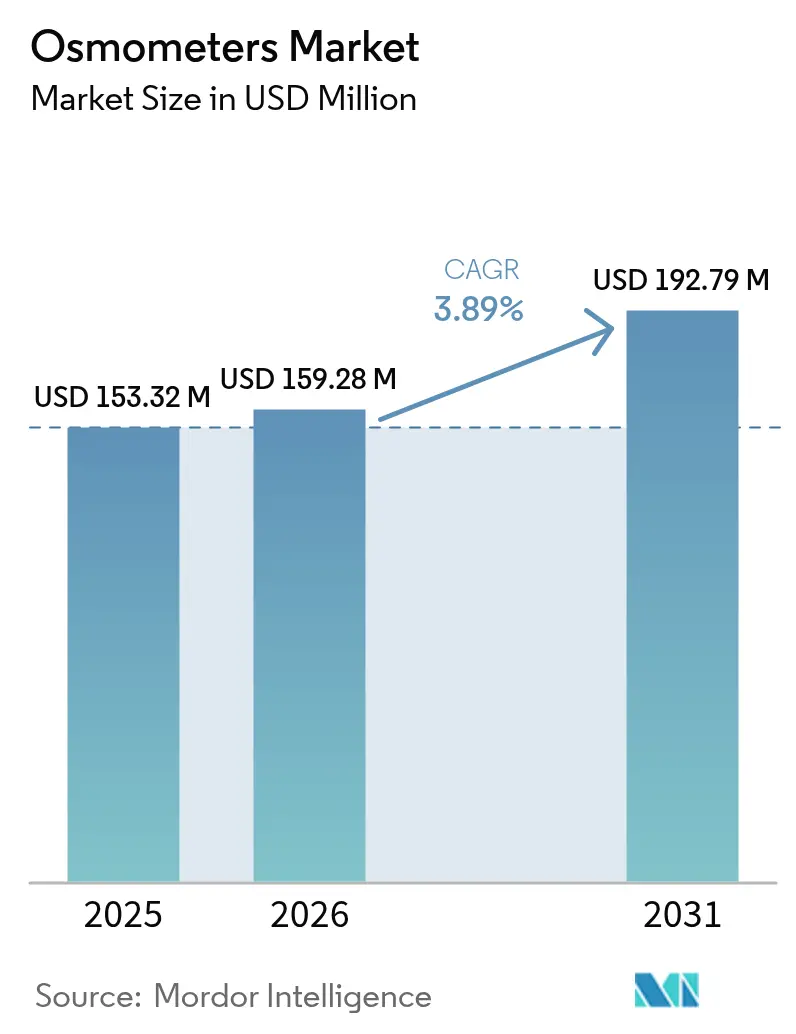

| Market Size (2026) | USD 159.28 Million |

| Market Size (2031) | USD 192.79 Million |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Osmometers Market Analysis by Mordor Intelligence

The osmometers market size is expected to grow from USD 153.32 million in 2025 to USD 159.28 million in 2026 and is forecast to reach USD 192.79 million by 2031 at 3.89% CAGR over 2026-2031. Demand is buoyed by laboratory automation, stricter compliance rules and biopharma’s tilt toward high-concentration biologics, even as device approvals take longer under the European Union Medical Device Regulation (EU MDR). Strategic combinations—such as Advanced Instruments’ pending USD 2.2 billion purchase of Nova Biomedical—underline an industry pivot toward integrated analytical platforms able to navigate complex global regulations. Meanwhile, the new EU rule that forces manufacturers to pre-alert regulators six months before supply interruptions is reshaping risk-management playbooks for every major supplier. In North America, continued clinical infrastructure investment supports stable replacement demand, while Asia-Pacific’s modernization push drives above-trend unit growth and fuels competition from impedance-based, point-of-care (POC) newcomers.

Key Report Takeaways

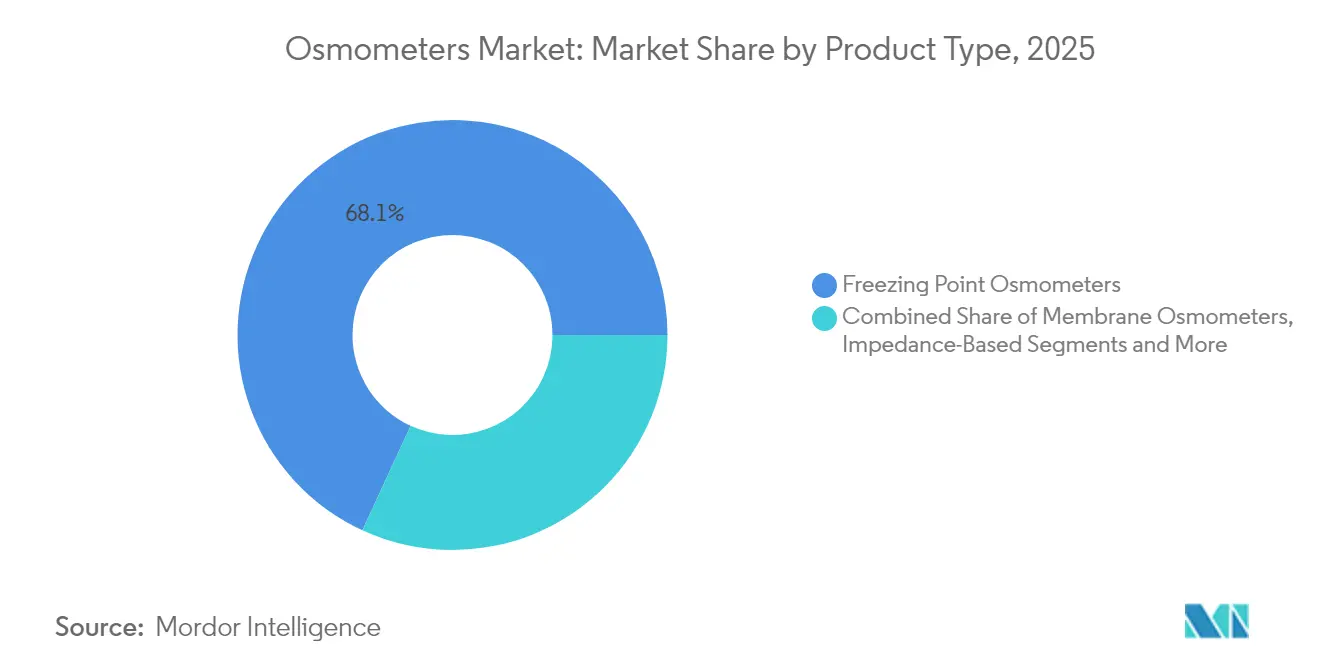

- By product type, freezing point instruments led with 68.12% of the osmometers market share in 2025; impedance-based systems are on course to expand at a 7.29% CAGR to 2031.

- By sampling capacity, single-sample units commanded 59.74% of the osmometers market size in 2025, whereas multi-sample models are projected to post an 7.64% CAGR through 2031.

- By application, clinical testing retained 52.88% share of the osmometers market in 2025, but pharmaceutical and biotech use-cases are forecast to rise at an 7.92% CAGR through 2031.

- By end user, hospitals accounted for 46.08% share in 2025; biopharma manufacturers are expected to record a 6.39% CAGR to 2031.

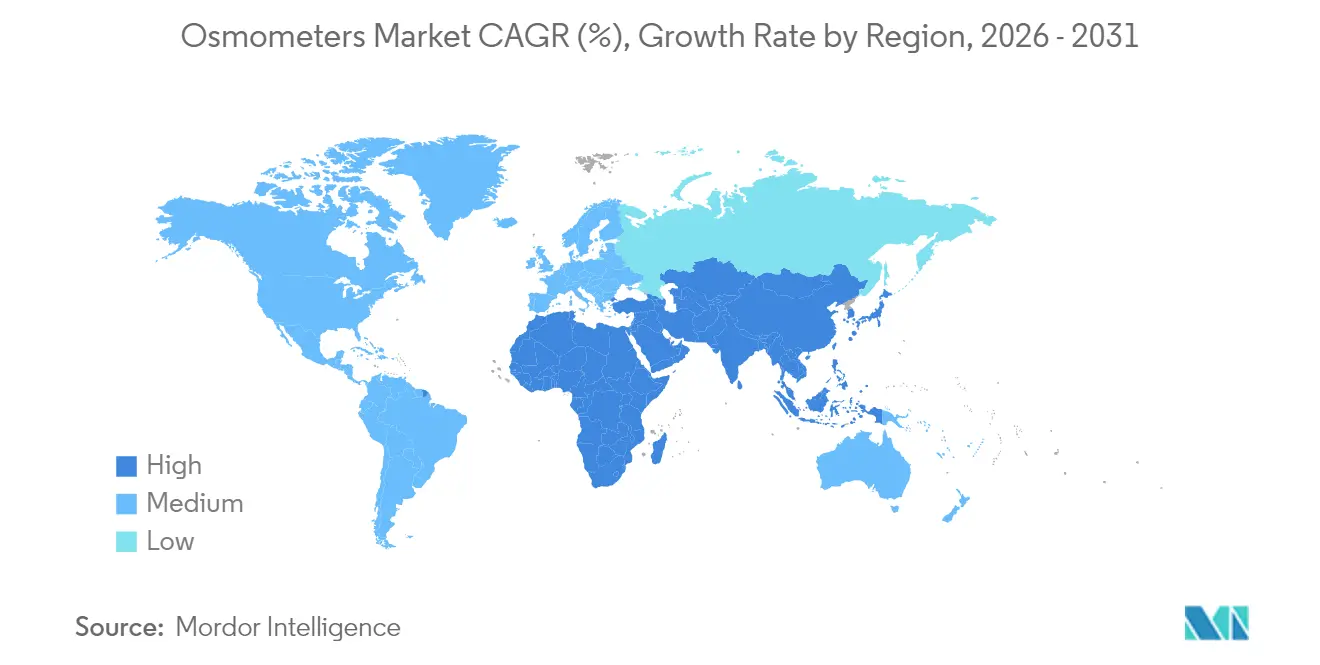

- By geography, North America captured 37.35% of the osmometers market size in 2025, while Asia-Pacific is advancing at a 7.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Osmometers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements & automation | +1.2% | Global (early North America & EU) | Medium term (2-4 years) |

| Growing R&D spend & disease burden | +0.8% | Global (developed markets) | Long term (≥ 4 years) |

| Biopharma shift to high-concentration biologics | +1.1% | North America & EU, spreading to APAC | Medium term (2-4 years) |

| Portable impedance-based devices for home renal care | +0.7% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Regulatory push for in-process osmolality testing | +0.9% | EU & North America, with APAC following | Short term (≤ 2 years) |

| LIS-integrated QA in food & beverage plants | +0.5% | EU & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements & Automation

European laboratories are adopting fully automated osmometry workcells that link directly with analytical LC-MS, chemistry analyzers and laboratory information systems, shrinking manual steps and minimizing cross-contamination risks. A province-wide CoreLIMS roll-out in Northern Ireland has shown how seamless integration allows real-time osmolality data to flow into blood-bank and microbiology modules, improving traceability across 1,200 sample points per day. Vendors now position “connected” osmometers that generate HL7-formatted results in under 60 seconds, a capability that resonates with hospitals chasing zero-waste, high-throughput operations. The osmometers market is thus witnessing higher average selling prices tied to software, cyber-security updates and remote diagnostics bundles. Adoption is sharpest in North America’s core reference labs, but EU-based networks are narrowing the gap through region-funded digital health programs.

Growing R&D Spend & Disease Burden

Global R&D outlays in advanced therapies push osmolality to the front line of process analytics, with recent trials showing adeno-associated virus titers jump 22% when producers orchestrate timed osmolality shifts mid-culture. Chronic kidney disease prevalence, now topping 9% of the EU adult population, heightens need for decentralized kidney-function screens that depend on rapid urine osmometry. Nova Biomedical’s CE-marked creatinine/eGFR meter pairs osmolarity and kidney markers in a two-minute test, enabling rural physicians to triage patients without central lab support. High disease burden therefore amplifies the osmometers market’s clinical installed base and shifts procurement criteria toward devices that blend speed, analytical depth and ergonomic design.

Biopharma Shift To High-Concentration Biologics

As mAb concentrations approach 250 mg/mL, freezing-point instruments suffer “failure-to-freeze” artifacts, triggering longer cycle times and reruns that squeeze batch release schedules.[1]Alona Teran, Sabaha Khakoo, Rahul Rajan Kaushik, and William Callahan, “Nonideal Colligative Properties in High-Concentration mAb Solutions,” BioProcess International, bioprocessintl.com Vapor-pressure and dual-method platforms now achieve coefficient of variation under 1.5% at viscosities beyond 30 cP, helping formulation chemists meet subcutaneous delivery targets without diluting actives. European contract development and manufacturing organizations are standardizing on in-line osmometry inside continuous bioreactors, turning osmolality into a release-by-exception parameter and spurring upgrades that lift unit sales across mid-capacity lines.

Portable Impedance-Based Devices For Home Renal Care

Wearable bioimpedance patches that read extracellular resistance in 30-second bursts have correlated within ±2% of dialysate ultrafiltration volumes in multicenter hemodialysis trials.[2]Frida Bremnes et al., “Measuring Fluid Balance in End-Stage Renal Disease with a Wearable Bioimpedance Sensor,” BMC Nephrology, bmcnephrol.biomedcentral.com Because sensors use microliter sample volumes, they dovetail with tele-nephrology apps, permitting continuous hydration alerts that address fluid overload risk between clinic visits. Prototype urine-dipstick add-ons have registered 89.9% accuracy versus standard freezing-point osmometers, signalling readiness for over-the-counter expansion.[3]Yanhong Zhang, “Urine Osmolality Assessment Through the Integration of Urea Hydrolysis and Impedance Measurement,” Lab Chip, pubs.rsc.org Asia-Pacific innovators, backed by digital-health grants, are first movers, but EU MedTech sandbox schemes are accelerating cross-border CE marking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intrinsic accuracy/throughput limits | -0.6% | Global (high-volume labs) | Medium term (2-4 years) |

| Shortage of skilled operators | -0.4% | EU & North America | Long term (≥ 4 years) |

| Cryoscopic sensor supply-chain risks | -0.5% | Global (EU regulatory burden) | Short term (≤ 2 years) |

| Emerging non-contact T-measurement alternatives | -0.3% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intrinsic Accuracy/Throughput Limits

Freezing-point cycles surpass three minutes when protein loads exceed 150 mg/mL, throttling daily capacity inside mega-labs that already run 800 million tests annually. Vapor-pressure devices improve accuracy but require long equilibration; thus they seldom slot into STAT benches where 15-minute turnaround is non-negotiable. This trade-off steers some buyers to non-contact refractive sensors, eroding addressable share in rapid-response niches.

Shortage Of Skilled Operators

Vacancy rates for certified chemistry technologists in EU reference labs climbed to 18% in 2025, a gap worsened by curriculum lag on instrument automation. Training a new technician on calibration, error codes and probe maintenance for a multi-sample osmometer takes 160 hours, an investment many mid-sized hospitals find hard to spare.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Freezing Point Dominance Faces Impedance Innovation

Freezing point instruments retained 68.12% of 2025 osmometers market share, underpinned by decades of clinical trust and clear regulatory acceptance. Impedance systems, though only a fraction of today’s osmometers market size, are growing at 7.29% CAGR thanks to portable designs that suit critical care, dialysis and veterinary applications. Vapor-pressure units occupy a narrow high-concentration biologics niche where their performance premium offsets slower cycle times. Manufacturers now bundle maintenance contracts, remote firmware pushes and auto-calibration features to keep compliance costs predictable.

Technology updates echo industry moves toward connectivity and service. Impedance devices achieve 95.5% accuracy with sub-20 µL samples—critical for newborn screening and animal health—and plug directly into Bluetooth-enabled patient apps, expanding the osmometers industry footprint in decentralized setting. Freezing-point leaders respond by embedding barcode scanners, reagent-lot traceability and AI-based quality control alerts that slash out-of-spec reruns. Vapor-pressure suppliers focus on stainless-steel wetted paths and 21 CFR Part 11 audit trails that attract gene-therapy CDMOs.

By Sampling Capacity: Multi-Sample Automation Drives Efficiency

Single-sample analyzers held 59.74% of the osmometers market in 2025 as clinics and emergency rooms favored lower purchase prices and easy workflows. Yet multi-sample versions, climbing at 7.64% CAGR, now ship with robotic load drawers and LIS hubs that process up to 90 tubes per hour—features North American mega-labs deem essential for value-based reimbursement targets. The osmometers market size for high-throughput units should therefore outpace historical averages over the forecast as hospitals redesign core labs around modular automation.

European sites adopt 24-place racks with smartphone-style touchscreens, allowing one technologist to oversee parallel electrolyte, glucose and osmolality tests. In rural health centers, compact single-sample devices persist, but vendors refresh them with cloud logging, simplified QC and one-button maintenance. This balanced demand keeps both categories relevant yet sharply differentiated on throughput and connectivity.

By Application: Pharmaceutical Growth Outpaces Clinical Stability

Clinical diagnostics anchored 52.88% of the osmometers market share in 2025, a base likely to grow modestly as population aging and chronic-disease screening expand test menus. Pharmaceutical and biotech labs, however, will deliver an 7.92% CAGR, lifting their slice of osmometers market size because continuous manufacturing and high-concentration formulations require in-line osmolality monitoring to preserve product integrity. Industrial food testing gains momentum under stricter EU isotonic beverage rules, while academic labs propel exploratory work on hybrid sensing.

The pharmaceutical surge concentrates in gene therapy and next-generation antibodies where precise osmolality control correlates with yield and potency. Hospitals expand POC menus, integrating creatinine-plus-osmolality meters that trim discharge times after contrast imaging. Together these trends diversify revenue streams and cushion cyclical swings in capital budgets.

By End User: Biopharma Manufacturers Accelerate Adoption

Hospitals preserved a 46.08% stake in 2025, reflecting entrenched lab infrastructure and broad chemistry panels that include osmolality. Biopharma plants, expanding at 6.39% CAGR, upgrade to hygienic, in-line probes as regulators intensify scrutiny of critical quality attributes, keeping osmolality front and center. Diagnostic service chains buy mid-tier benchtop units to service satellite clinics, while universities pilot impedance wearables, ensuring innovation flow.

FDA rules on laboratory-developed tests broaden the validation burden, steering drug makers toward turnkey platforms with cradle-to-grave data integrity. Hospitals, facing staffing shortages, lean on auto-QC and e-learning modules to shorten technologist onboarding, shaping future purchase criteria.

Geography Analysis

North America kept 37.35% of global osmometers market share in 2025 as reimbursement stability and high test volumes underpinned steady upgrades. The region benefits from the deepest base of CLIA-certified labs and a dense biopharma corridor that values process analytical technology. Asia-Pacific, compounding at 7.41% CAGR, benefits from national health insurance expansions, aggressive biologics capacity build-outs and rising adoption of bedside testing in China, India and South Korea. Europe, while hampered by regulatory bottlenecks, leverages automation uptake and strong vaccine pipelines to maintain competitive parity. Middle East and Africa remain nascent but secure double-digit unit growth where hospital build programs pair with local device assembly incentives.

Government subsidies in Singapore, Korea and China tilt capex toward high-throughput, 21 CFR Part 11-ready osmometers that future-proof regulatory filings. EU MDR’s protracted certification cycles delay some product launches, but also create white-space for nimble suppliers with pre-notified-body strategies. Across all regions, demand gravitates toward platforms that compress workflow, integrate data streams and reduce total cost of ownership.

Competitive Landscape

The osmometers market is moderately fragmented but consolidating fast as players pursue integrated analytics portfolios. Advanced Instruments’ USD 2.2 billion takeover of Nova Biomedical unlocks a combined installed base exceeding 35,000 analyzers across 100 countries, pooling freezing-point pedigree with rapid POC technology. Bruker’s USD 942 million move for ELITechGroup adds clinical chemistry and molecular testing breadth that complements osmometry workflows. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s filtration arm signals a tilt toward full upstream-to-downstream process analytic suites, embedding osmolality within PAT toolboxes.

Market leaders differentiate through automation expertise, SaaS-style service contracts and regulatory consultancy that demystifies EU MDR and US FDA filings. Anton Paar courts beverage and pharma users with Ultratap 500 Series tap-density aids that share common UI and calibration protocols with its PBA osmometer line. Niche entrants target impedance sensors for home renal care, banking on consumer-grade electronics to unseat legacy benchtop incumbents. Competitive intensity thus hinges on speed of portfolio integration, strength of digital ecosystems and agility in meeting evolving regional compliance timelines.

Osmometers Industry Leaders

Advanced Instruments LLC

Precision Systems Inc.

ELITechGroup

ARKRAY, Inc.

Nova Biomedical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Advanced Instruments announced a USD 2.2 billion deal to acquire Nova Biomedical, creating a combined life-science tools platform.

- February 2025: Thermo Fisher Scientific struck a USD 4.1 billion agreement to buy Solventum’s purification and filtration unit, bolstering PAT capabilities aligned with osmometry.

- January 2025: Advanced Instruments launched OsmoPRO MAX, an automated freezing-point osmometer aimed at boosting clinical lab productivity.

Global Osmometers Market Report Scope

As per the scope of the report, an osmometer is an analytical instrument that is used for the estimation of the osmotic pressure of various solutions, colloids, and compounds. These instruments are also used in measuring sugars or salts in urine solutions. The osmometers market is segmented by product type (freezing point osmometers, vapor pressure osmometers, membrane osmometers), sampling capacity (single-sample osmometers and multi-sample osmometers), application (clinical, pharmaceutical, and biotech, and other applications), end user (hospitals, laboratories, and diagnostic centers, and other end users), and geography (North America, Europe, Asia-Pacific, and the rest of the world). The report offers the value (in USD million) for the above segments.

| Freezing Point Osmometers |

| Vapor Pressure Osmometers |

| Membrane Osmometers |

| Impedance-Based (Others) |

| Single-sample Osmometers |

| Multi-sample Osmometers |

| Clinical |

| Pharmaceutical & Biotech |

| Industrial & Food QC |

| Research & Academic |

| Hospitals |

| Diagnostic & Laboratory Centers |

| Biopharma Manufacturers |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Freezing Point Osmometers | |

| Vapor Pressure Osmometers | ||

| Membrane Osmometers | ||

| Impedance-Based (Others) | ||

| By Sampling Capacity | Single-sample Osmometers | |

| Multi-sample Osmometers | ||

| By Application | Clinical | |

| Pharmaceutical & Biotech | ||

| Industrial & Food QC | ||

| Research & Academic | ||

| By End User | Hospitals | |

| Diagnostic & Laboratory Centers | ||

| Biopharma Manufacturers | ||

| Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Osmometers Market?

The Osmometers Market size is expected to reach USD 159.28 million in 2026 and grow at a CAGR of 3.89% to reach USD 192.79 million by 2031.

What is the current size of the osmometers market?

The osmometers market stands at USD 159.28 million in 2026 and is on track to reach USD 192.79 million by 2031.

Which product type dominates the osmometers market?

Freezing point instruments lead with 68.12% share in 2025, although impedance-based devices are the fastest-growing category at a 7.29% CAGR.

Why is Asia-Pacific the fastest-growing region for osmometers?

Healthcare modernization, expanding biopharmaceutical capacity and rapid adoption of point-of-care testing push Asia-Pacific to a 7.41% CAGR, outpacing other regions.

How is regulation affecting osmometry demand?

EU MDR certification delays and new FDA guidelines mandating in-process osmolality tests drive laboratories to upgrade to compliant, automated instruments.

What are the key growth applications for osmometers?

Beyond core clinical use, high-concentration biologics manufacturing, cell-gene therapy production and isotonic beverage quality control are major growth engines.

Page last updated on: