Organ 3D Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 190.48 Million |

| Market Size (2031) | USD 340.53 Million |

| Growth Rate (2026 - 2031) | 12.31 % CAGR |

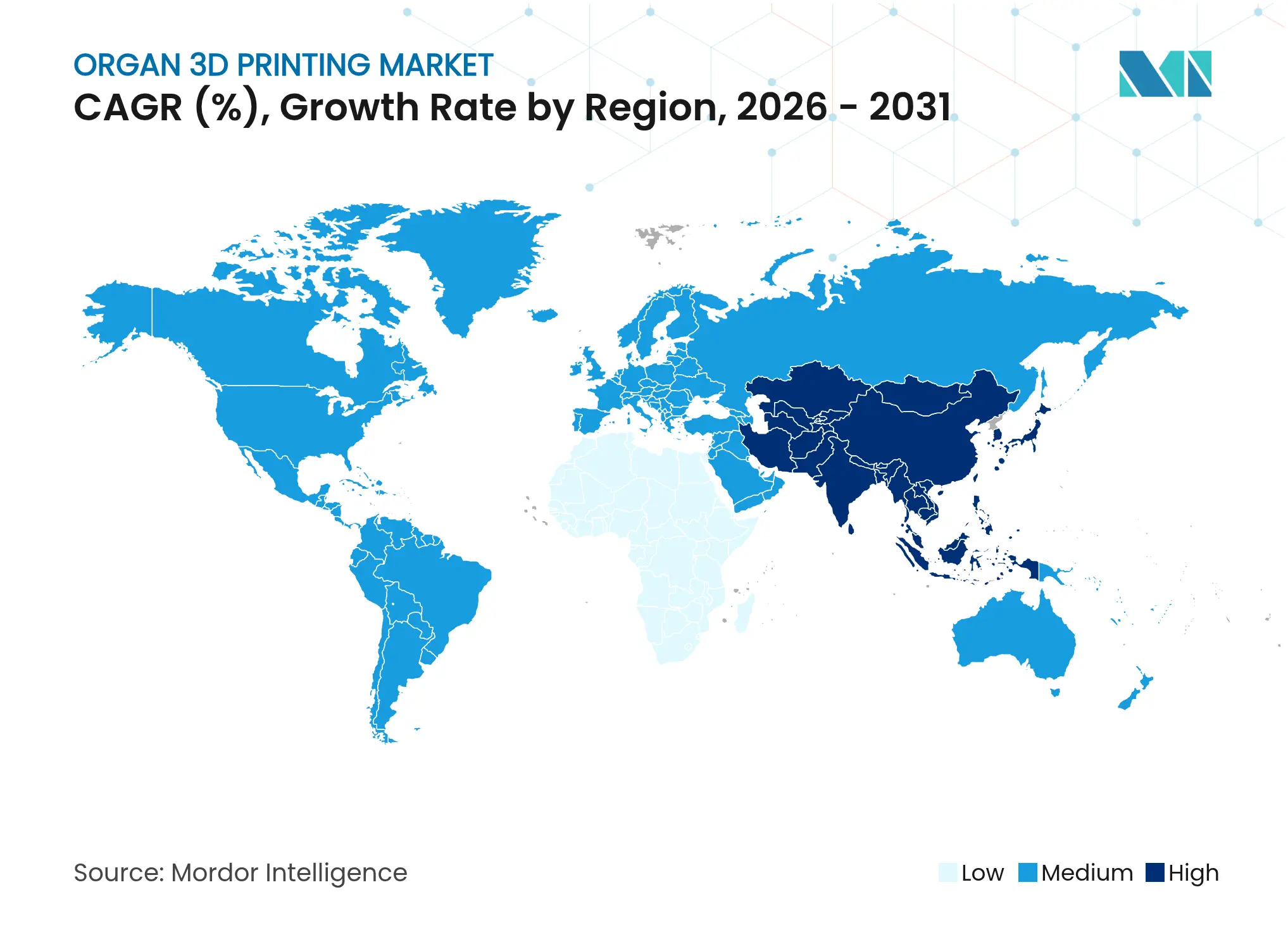

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

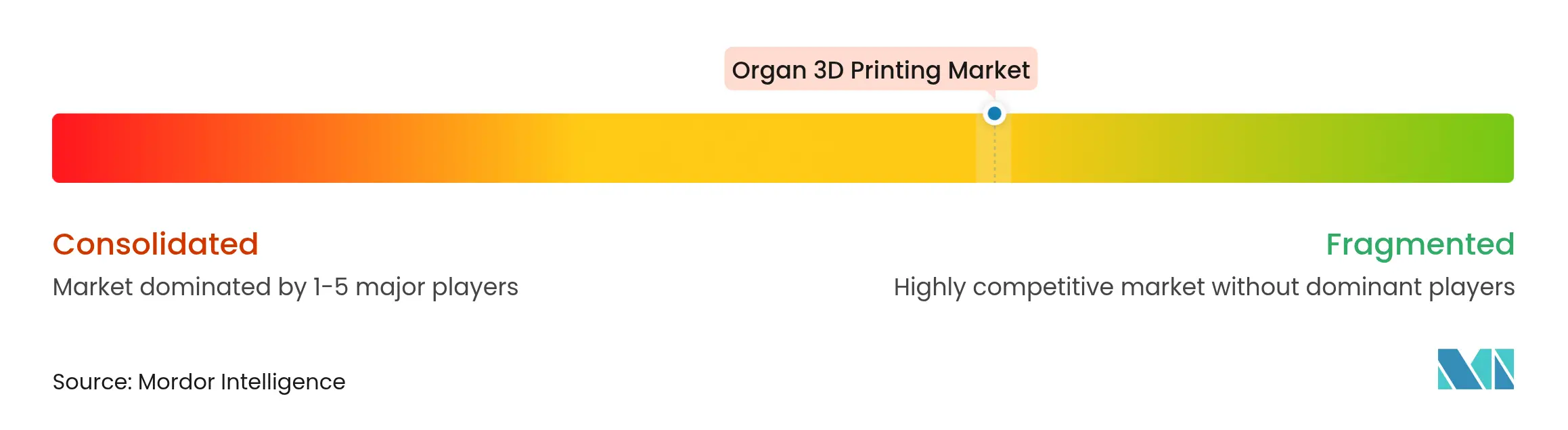

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Organ 3D Printing Market Analysis by Mordor Intelligence

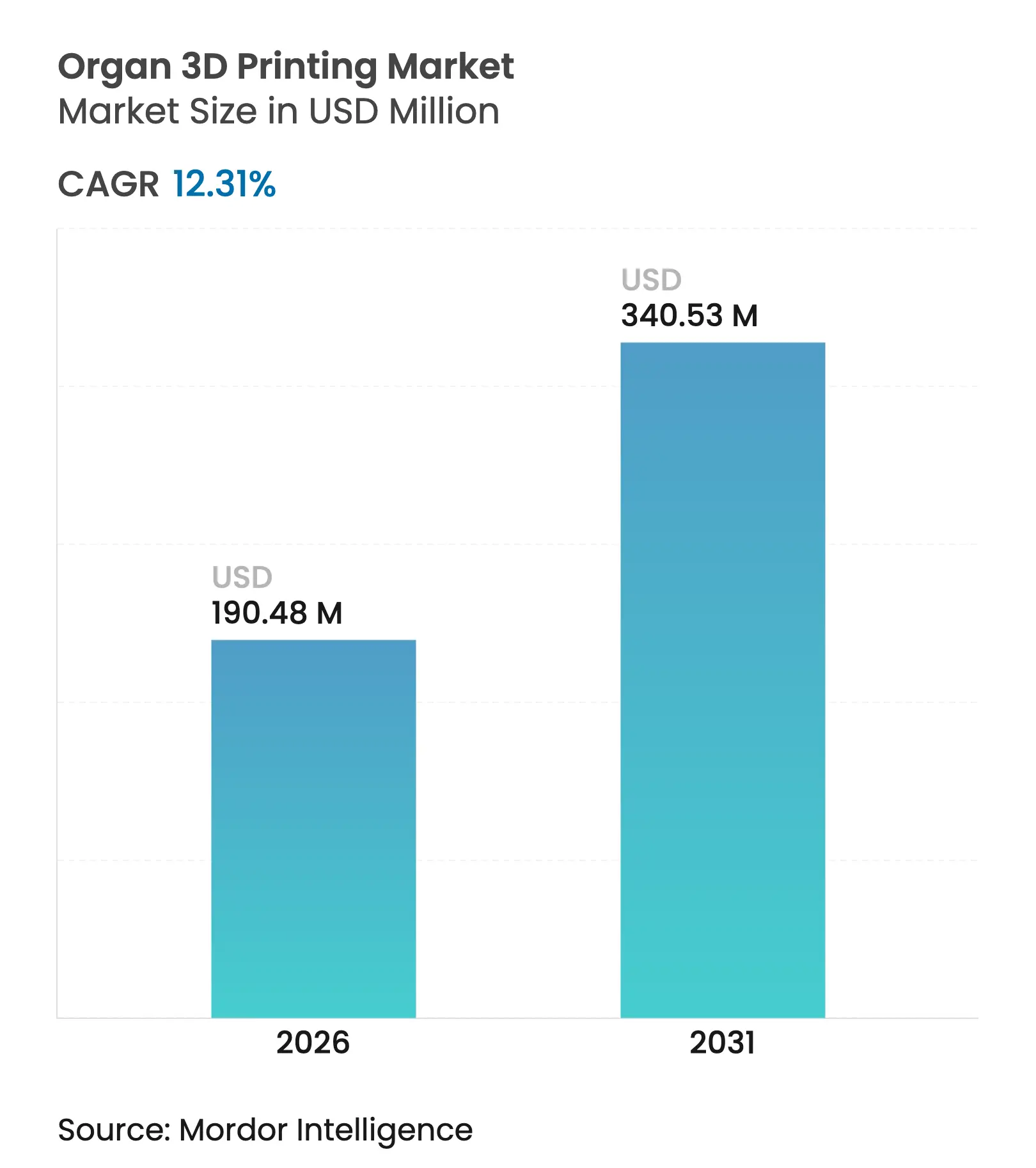

The Organ 3D Printing market size was valued at USD 169.6 billion in 2025 and estimated to grow from USD 190.48 billion in 2026 to reach USD 340.53 billion by 2031, at a CAGR of 12.31% during the forecast period (2026-2031). Artificial intelligence is accelerating efficiency by 60% in bio-ink formulation, while microgravity manufacturing delivers four-fold gains in tissue strength, collectively moving the Organ 3D Printing market toward routine clinical deployment. Space-based bioprinting, AI-guided parameter control, and regulatory sandboxes in Asia-Pacific are reshaping commercial strategies and lowering time-to-approval. Hardware innovation now centres on volumetric and holographic techniques that reduce build times from weeks to hours, directly boosting throughput. Meanwhile, recurring revenue from consumables is outpacing hardware sales, signaling a fundamental shift in value capture across the Organ 3D Printing market.

Key Report Takeaways

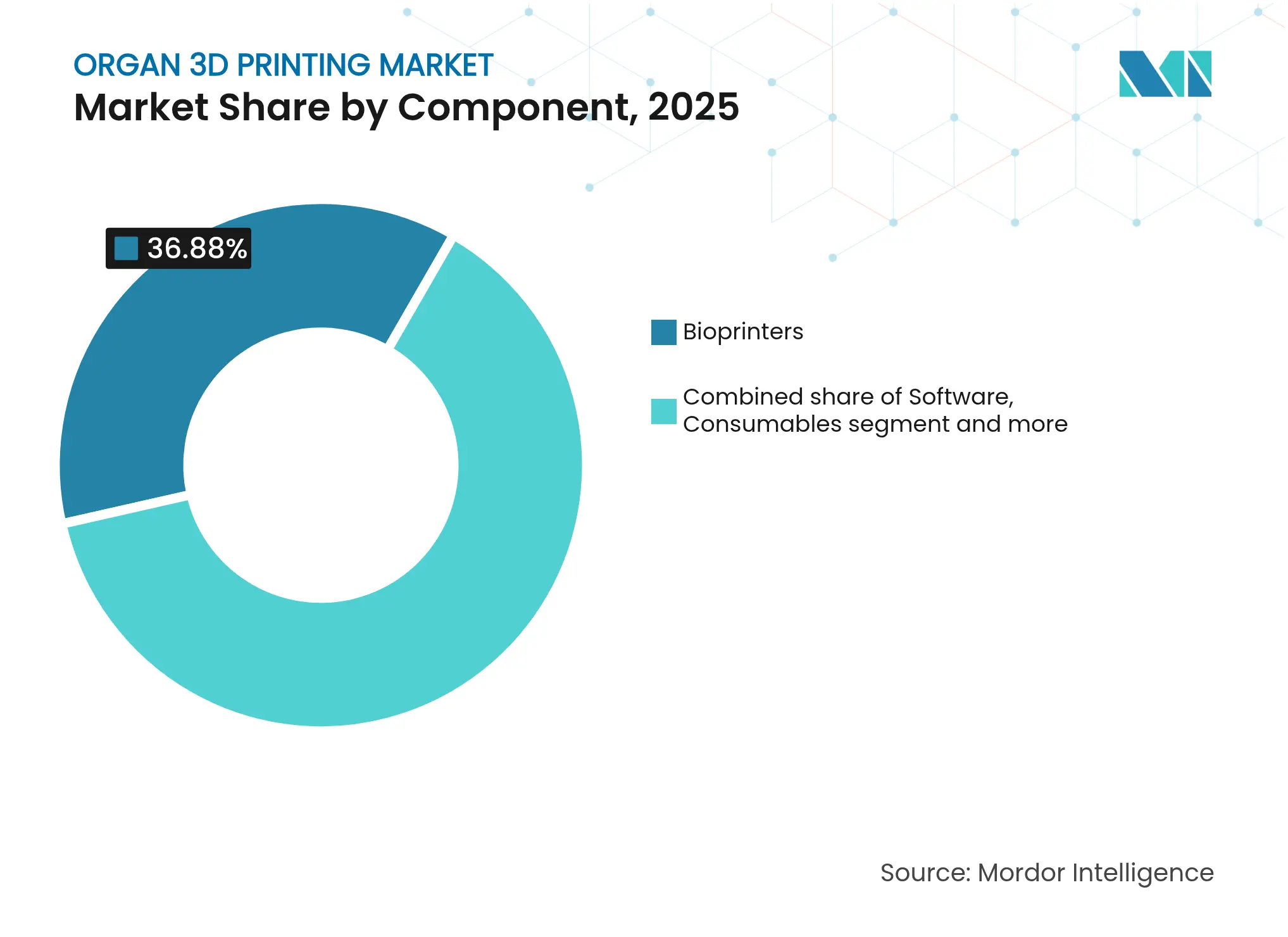

- By component, bioprinters held 36.88% of the Organ 3D Printing market share in 2025, whereas consumables are advancing at a 13.82% CAGR through 2031.

- By organ type, liver dominated with 37.74% share of the Organ 3D Printing market size in 2025; heart is projected to grow at 16.11% CAGR during 2026-2031.

- By application, transplantation commanded 38.02% of the Organ 3D Printing market size in 2025, while regenerative medicine led with a 15.34% CAGR outlook.

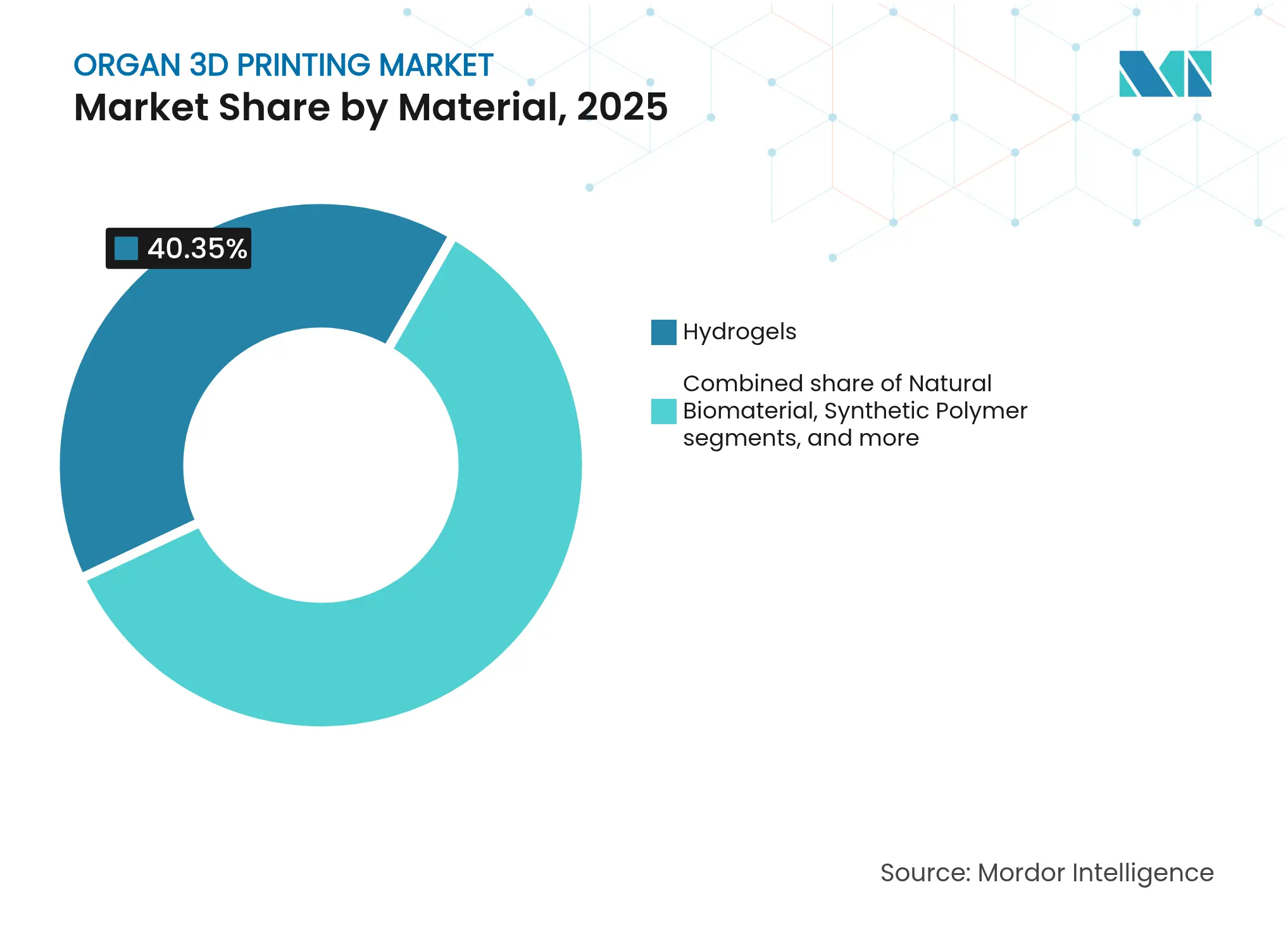

- By material, hydrogels captured 40.35% share, and natural biomaterials are expanding at 13.96% CAGR.

- By technology, extrusion accounted for 51.43% share; laser-assisted platforms are rising at 14.22% CAGR.

- By source of cells, autologous approaches held a 36.21% share; induced pluripotent stem cells (iPSCs) are climbing at a 15.65% CAGR.

- By end-user, hospitals and transplant centres secured a 38.37% share, whereas academic institutes are growing at a 14.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organ 3D Printing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Technological advances in bioprinting hardware and

bio-inks

Technological advances in bioprinting hardware and

bio-inks

| +3.2% | Global | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+3.2%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Medium term (2-4 years)

|

Rising demand for organ transplants

Rising demand for organ transplants

| +2.8% | Global | Long term (≥ 4 years) | |||

Increasing funding and partnerships in regenerative

medicine

Increasing funding and partnerships in regenerative

medicine

| +2.1% | North America & EU | Medium term (2-4 years) | |||

AI-driven bio-ink optimization

AI-driven bio-ink optimization

| +1.9% | Global | Short term (≤ 2 years) | |||

Asia-Pacific regulatory sandboxes enabling clinical pilots

Asia-Pacific regulatory sandboxes enabling clinical pilots

| +1.3% | Asia-Pacific | Medium term (2-4 years) | |||

Microgravity bioprinting breakthroughs

Microgravity bioprinting breakthroughs

| +0.8% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Technological Advances in Bioprinting Hardware & Bio-Inks

Volumetric, holographic, and direct sound printing techniques now produce entire organ[1]Vidhi Mathur, “Volumetric Additive Manufacturing for Cell Printing,” ACS Biomaterials Science & Engineering, pubs.acs.org structures in hours, avoiding prolonged cell stress and elevating viability. Self-healing hydrogels repair micro-fractures after extrusion, while embedded electrospun fibers raise nutrient diffusion by 40%. These advances shorten maturation cycles, bridge vascularization gaps, and push the Organ 3D Printing market toward therapeutic production.

Rising Demand for Organ Transplants

More than 103,000 patients[2]Pradyun Iyer, “Avenues and Future Prospects Of 3D Bioprinting,” International Journal for Multidisciplinary Research, ijfmr.com were on United States waiting lists in 2025, intensifying the pull for printed alternatives that remove donor scarcity and could save USD 500,000 per patient in lifetime care costs.

Increasing Funding & Partnerships in Regenerative Medicine

Capital is shifting from platform plays to application-specific ventures. CollPlant and Stratasys are pursuing regenerative breast implants, which are aimed at a USD 3 billion niche, while Pandorum Technologies raised USD 11 million for corneal therapy.

AI-Driven Bio-Ink Optimization

Machine-learning systems now self-calibrate extrusion pressure[3]Washington State University, “Self-improving AI Method Increases 3D-Printing Efficiency,” ScienceDaily, sciencedaily.com, temperature, and cross-linking in real time, lifting print accuracy and democratizing access for smaller clinics that lack specialist staff.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of equipment and GMP-grade materials

High cost of equipment and GMP-grade materials

| -2.4% | Global | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-2.4%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Medium term (2-4 years)

|

Vascularization and tissue-maturation hurdles

Vascularization and tissue-maturation hurdles

| -1.8% | Global | Long term (≥ 4 years) | |||

Fragmented bio-ink intellectual-property landscape

Fragmented bio-ink intellectual-property landscape

| -1.2% | North America & Europe | Medium term (2-4 years) | |||

Supply bottlenecks for pharma-grade hydrogel polymers

Supply bottlenecks for pharma-grade hydrogel polymers

| -0.9% | Developed markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Equipment & GMP-Grade Materials

Full-scale systems still list between USD 200,000 and USD 1 million, while pharma-grade hydrogels remain 10–15 times pricier than research formulations, limiting Organ 3D Printing market penetration in cost-sensitive regions.

Vascularization & Tissue-Maturation Hurdles

Replicating capillary networks under 200 µm is technically unresolved[4]Huang N.F., “Overcoming Bottlenecks in Vascular Regeneration,” Nature Communications Biology, nature.com ; embedded sacrificial printing increases complexity and cost, and bioreactor conditioning often exceeds eight weeks, delaying throughput and revenue.

Segment Analysis

By Component: Recurring Consumables Drive Future Growth

Bioprinters captured 36.88% of the Organ 3D Printing market size in 2025, showing early capital build-out. Consumables, however, are growing at 13.82% CAGR as installed systems raise continuous demand for proprietary bio-inks and growth factors. The Organ 3D Printing market size tied to consumables is projected to eclipse hardware revenue by 2031, supported by platforms such as BLI’s BioLoom that bundle printers with subscription materials. Software is becoming critical as AI modules enhance accuracy and reduce waste.

Demand for consumables signals a strategic pivot from one-off equipment sales to annuity-like supply models. Suppliers investing in exclusive hydrogels can secure pricing power and customer lock-in, an approach mirrored in the Organ 3D Printing industry’s shift toward service-enabled platforms.

Note: Segment shares of all individual segments available upon report purchase

By Organ Type: Liver Leads, Heart Accelerates

Liver retained 37.74% of the Organ 3D Printing market share in 2025, thanks to its simple lobular architecture and regenerative propensity. Heart constructs, aided by 4D shape-morphing breakthroughs, are forecast to post a 16.11% CAGR, reflecting rising cardiac demand and maturing bio-ink technology. Kidney remains commercially attractive due to the dialysis bridge; skin, bone, and cartilage provide nearer-term regulatory pathways.

The emerging cardiac focus redefines research priorities, channeling investment into electromechanical synchronization and thick-tissue perfusion. Companies that perfect contractile myocardium stand to unlock the largest untapped segment of the Organ 3D Printing market.

By Application: Transplantation Dominates but Regenerative Medicine Grows Fast

Transplantation held a 38.02% share of the Organ 3D Printing market size in 2025, driven by donor shortages and high rejection costs. Regenerative medicine is expanding 15.34% CAGR as tissue patches, wound matrices, and reconstructive implants reach commercial maturity. Drug discovery platforms remain lucrative because they circumvent transplant regulations and deliver quick wins.

Regulatory leniency for skin and cartilage applications enables early cash flows that finance long-cycle organ programs. Hybrid business strategies pairing near-term tissue products with long-range organ goals are gaining traction across the Organ 3D Printing industry.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Material: Hydrogels Dominate While Natural Biomaterials Surge

Hydrogels delivered 40.35% of the Organ 3D Printing market share in 2025 through unmatched biocompatibility. Natural biomaterials are growing 13.96% CAGR as pure collagen and gelatin formulations achieve clinical-grade purity. Synthetic polymers retain value in load-bearing constructs but face biocompatibility trade-offs.

The material mix is becoming application-specific. Natural matrices suit vascularized organs, while composite polymers power orthopedic builds. Portfolio breadth will be vital for suppliers courting varied Organ 3D Printing market segments.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Extrusion Maintains Volume Leadership; Laser-Assisted Gains Precision

Extrusion methods held 51.43% of the Organ 3D Printing market share in 2025, owing to their versatility and scalability. Laser-assisted platforms are advancing at a 14.22% CAGR because they deliver the micro-architectural accuracy required for capillary fidelity. Holographic direct sound printing could compress production times by 20x, an innovation with game-changing potential.

Future platforms will blend modalities to marry speed, detail, and material breadth, reinforcing competitiveness within the Organ 3D Printing market.

By Source of Cells: Autologous Dominates; iPSCs Show High Upside

Autologous cells, through a perfect immunogenic fit, owned 36.21% of the Organ 3D Printing market size in 2025. iPSCs are scaling 15.65% CAGR following microgravity-enhanced reprogramming research on the International Space Station. Allogeneic sources enable off-the-shelf products but carry rejection risks.

Scalable iPSC supply chains promise to cut lead times and costs, making them pivotal to longer-term Organ 3D Printing market growth once vascular and maturation barriers fall.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End-User: Hospitals Lead; Academia Fuels Innovation

Hospitals controlled 38.37% of the Organ 3D Printing market share in 2025, reflecting clinical use cases. Academic institutes are rising 14.86% CAGR as they pilot disruptive bioprinting protocols and train personnel. Pharmaceutical firms exploit mini-organs for screening, while contract research organizations provide outsourced capacity.

End-user diversity spreads revenue risk and encourages specialized product offerings, sustaining a robust Organ 3D Printing market.

Geography Analysis

North America held 39.88% Organ 3D Printing market share in 2025 and is climbing 11.35% CAGR, driven by ARPA-H’s PRINT program and FDA-backed device clearances that normalize regulatory pathways. Strong venture capital, a deep patent pool, and NASA’s microgravity research create a virtuous innovation cycle.

Europe is growing 11.92% CAGR, balancing strict MDR safety mandates with strategic EU grants. Companies such as CollPlant prosper through niche applications like regenerative implants, though complex legal layers can slow first-in-human trials.

Asia-Pacific is the fastest-moving region, with a 15.2% CAGR. India’s revised toxicology rules, China’s provincial sandbox schemes, and Japan’s material science leadership combine to open large-scale clinical pilots with reduced approval times.

The Rest of the World is accelerating 13.01% CAGR as Middle Eastern health investments and South American medical tourism adopt bio-printed tissues to compensate for organ import limits. Flexible oversight in these regions can speed early revenue while global standards evolve.

Competitive Landscape

Market Concentration

Few active firms jostle within a fragmented Organ 3D Printing market, yet only a handful—CELLINK, Organovo, 3D Systems—have moved beyond prototype organs. Competition is pivoting from hardware arms races toward integrated ecosystems combining printers, proprietary bio-inks, and AI orchestration. High-impact moves include CollPlant-Stratasys’ breast implant alliance and Enovis’ EUR 800 million acquisition of LimaCorporate for titanium lattice know-how.

Emerging challengers leverage 4D shape-morphing and microgravity-validated bio-inks, carving differentiated moats. Patent fragmentation both empowers start-ups and complicates scale, forcing firms to negotiate cross-licenses or concentrate on narrowly defined indications.

With recurring consumables driving margins, market leaders are racing to lock clinicians into end-to-end platforms that bundle printers, AI software, and subscription materials, echoing razor-and-blade economics across the Organ 3D Printing industry.

Organ 3D Printing Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: University of Galway researchers achieved contractile human heart tissue using 4D shape-morphing bioprinting.

- October 2024: University of Galway researchers achieved contractile human heart tissue using 4D shape-morphing bioprinting.

- August 2024: CollPlant and Stratasys began pre-clinical work on regenerative collagen breast implants.

- September 2023: Enovis acquired LimaCorporate for EUR 800 million (USD 864 million) to enhance 3D-printed titanium orthopedics.

Table of Contents for Organ 3D Printing Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Technological Advances in Bioprinting Hardware & Bio-Inks

- 4.2.2Rising Demand for Organ Transplants

- 4.2.3Increasing Funding & Partnerships in Regenerative Medicine

- 4.2.4AI-Driven Bio-Ink Optimization

- 4.2.5APAC Regulatory Sandboxes Enabling Clinical Pilots

- 4.2.6Micro-Gravity Bioprinting Breakthroughs

- 4.3Market Restraints

- 4.3.1High Cost of Equipment & GMP-Grade Materials

- 4.3.2Vascularization & Tissue-Maturation Hurdles

- 4.3.3Fragmented Bio-Ink Intellectual-Property Landscape

- 4.3.4Supply Bottlenecks for Pharma-Grade Hydrogel Polymers

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers/Consumers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Component

- 5.1.1Bioprinters

- 5.1.2Software

- 5.1.3Consumables

- 5.1.4Other Components

- 5.2By Organ Type

- 5.2.1Bone & Cartilage

- 5.2.2Heart

- 5.2.3Kidney

- 5.2.4Liver

- 5.2.5Skin & Soft-tissue Grafts

- 5.2.6Vascular Constructs

- 5.2.7Other Organs

- 5.3By Application

- 5.3.1Organ Transplantation

- 5.3.2Drug Testing & Development

- 5.3.3Regenerative Medicine

- 5.3.4Prosthetics & Implants

- 5.3.5Other Applications

- 5.4By Material

- 5.4.1Hydrogels

- 5.4.2Natural Biomaterials

- 5.4.3Synthetic Polymers

- 5.4.4Metals & Metal-ceramic Composites

- 5.4.5Ceramics & Bio-glass

- 5.4.6Other Materials

- 5.5By Technology

- 5.5.1Extrusion-based Bioprinting

- 5.5.2Ink-jet Bioprinting

- 5.5.3Laser-assisted Bioprinting

- 5.5.4Other Technologies

- 5.6By Source of Cells

- 5.6.1Autologous Cells

- 5.6.2Allogeneic Cells

- 5.6.3Induced Pluripotent Stem Cells (iPSCs)

- 5.6.4Xenogeneic Cells

- 5.7By End-User

- 5.7.1Hospitals & Transplant Centres

- 5.7.2Academic & Research Institutes

- 5.7.3Biotechnology & Pharmaceutical Companies

- 5.7.4Other End-Users

- 5.8By Geography

- 5.8.1North America

- 5.8.1.1United States

- 5.8.1.2Canada

- 5.8.1.3Mexico

- 5.8.2Europe

- 5.8.2.1Germany

- 5.8.2.2United Kingdom

- 5.8.2.3France

- 5.8.2.4Italy

- 5.8.2.5Spain

- 5.8.2.6Rest of Europe

- 5.8.3Asia-Pacific

- 5.8.3.1China

- 5.8.3.2Japan

- 5.8.3.3India

- 5.8.3.4Australia

- 5.8.3.5South Korea

- 5.8.3.6Rest of Asia-Pacific

- 5.8.4Rest of the World

- 5.8.4.1Middle East and Africa

- 5.8.4.2South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Competitive Benchmarking

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.13D Bio Corp

- 6.4.23D Bioprinting Solutions

- 6.4.33D Systems Inc.

- 6.4.4Advanced Solutions Life Sciences

- 6.4.5Aspect Biosystems Ltd.

- 6.4.6BiomimX

- 6.4.7CELLINK (BICO Group)

- 6.4.8CollPlant Biotechnologies

- 6.4.9Desktop Metal (EnvisionTEC US LLC)

- 6.4.10LifeNet Health (Cyfuse Biomedical)

- 6.4.11Nivalis Group (RegenHU)

- 6.4.12nScrypt Inc.

- 6.4.13Organovo Holdings Inc.

- 6.4.14Pandorum Technologies Pvt. Ltd.

- 6.4.15Poietis

- 6.4.16Prellis Biologics

- 6.4.17Rokit Healthcare

- 6.4.18Shining 3D

- 6.4.19United Therapeutics (LungBioTech)

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Organ 3D Printing Market Report Scope

As per the scope of the report, a 3D-printed organ is a replica of bodily tissue crafted using a 3D bioprinter. The artificial organ or tissue is printed using a bioink. The bioink is developed to support cells in building the function and structure of the natural organ it is mimicking.

The organ 3D printing market is segmented into component, application, materials, technology, end-user, and geography. By component, the market is segmented into hardware and software. By application, the market is segmented into organ transplantation, drug testing and development, regenerative medicine, prosthetics and implants and other applications. Other applications include - disease modelling and surgical training models, among others. By materials, the market is segmented into hydrogels, biomaterials, metals, ceramics, and other materials. Other materials include living cells and polymers, and others. By technology, the market is segmented into extrusion-based bioprinting, inkjet-based bioprinting, laser-based bioprinting and other technologies. Other technologies include stereolithography and magentic levitation and others. By end-user, the market is segmented into hospitals and clinics, academic and research institutes and biotechnology and pharmaceutical companies. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizing and forecasts have been done on the basis of value (in USD).