Dairy Cattle Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

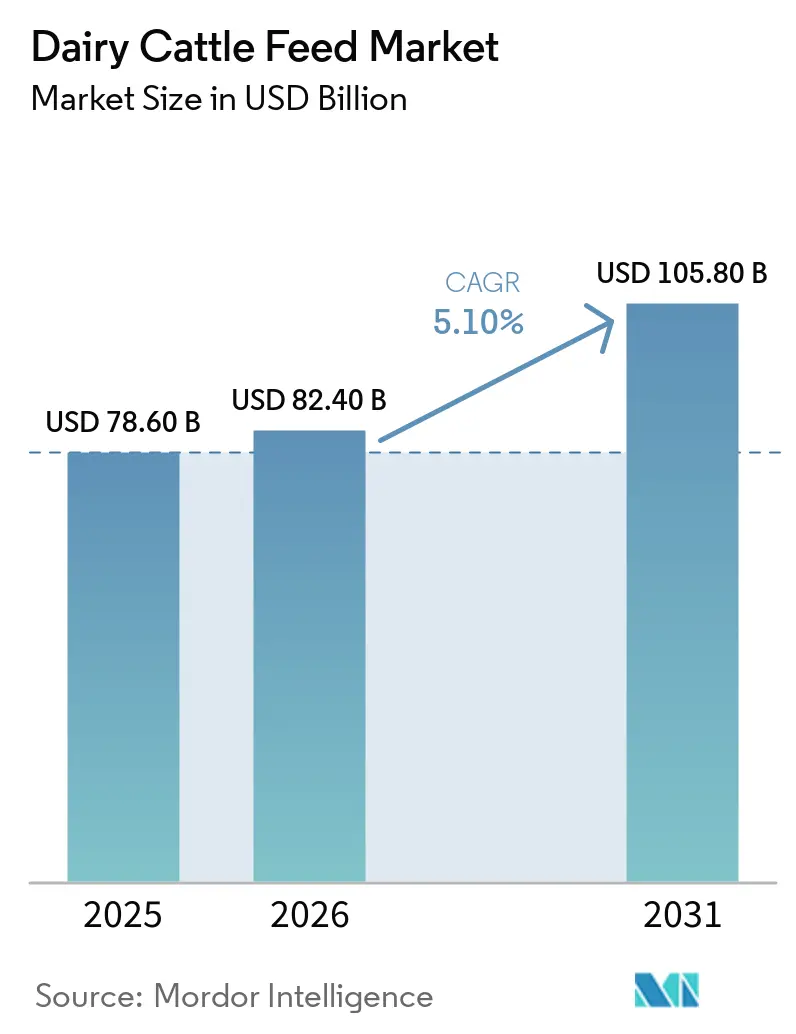

| Market Size (2026) | USD 82.40 Billion |

| Market Size (2031) | USD 105.80 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dairy Cattle Feed Market Analysis by Mordor Intelligence

The dairy cattle feed market size is projected to grow from USD 78.6 billion in 2025 to USD 82.4 billion in 2026 and USD 105.8 billion by 2031, with a CAGR of 5.1% from 2026 to 2031. Persistent cost inflation for inputs such as corn, soybean meal, vitamins, and functional additives is driving producers to adopt formulation strategies that enhance energy density, reduce enteric methane emissions, and maintain milk component premiums. Demand is particularly strong among large herds of 1,000 cows or more, where operators have the financial resources and data infrastructure to implement precision feeding software and in-line sensors, reducing feed waste and labor costs. Functional additives, including 3-nitrooxypropanol for methane reduction, probiotics for rumen stability, and protected amino acids for achieving milk-protein targets, have become essential due to their alignment with supermarket greenhouse-gas scorecards and voluntary carbon credit programs. Additionally, feed mills are adapting ingredient workflows to meet stricter pesticide-residue regulations, zero-deforestation soy certifications, and supplier audits extending to palm kernel and cassava plantations.

Key Report Takeaways

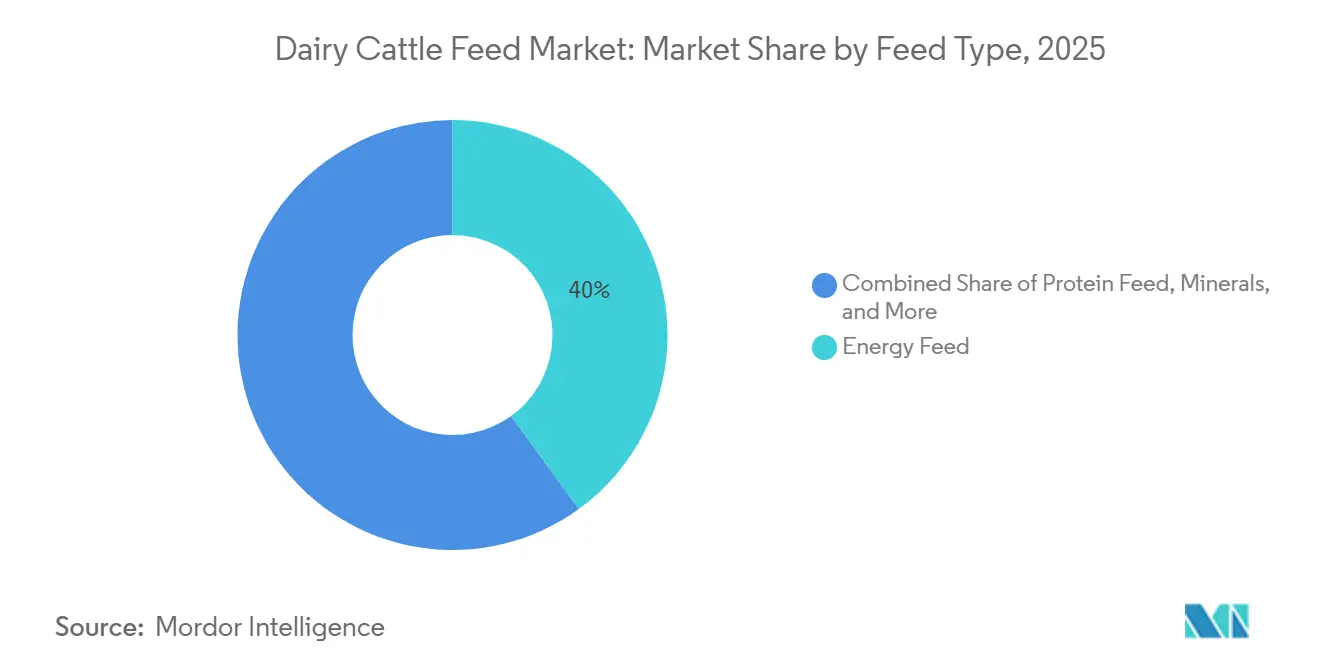

- By feed type, energy feed led with the largest 40% of the dairy cattle feed market share in 2025, while the functional additives market size is advancing at the fastest 8.9% CAGR from 2026 to 2031.

- By form, pellets held the largest 46% of the dairy cattle feed market share in 2025, whereas the total mixed ration (TMR) market size is expanding at the fastest 9.7% CAGR from 2036 to 2031.

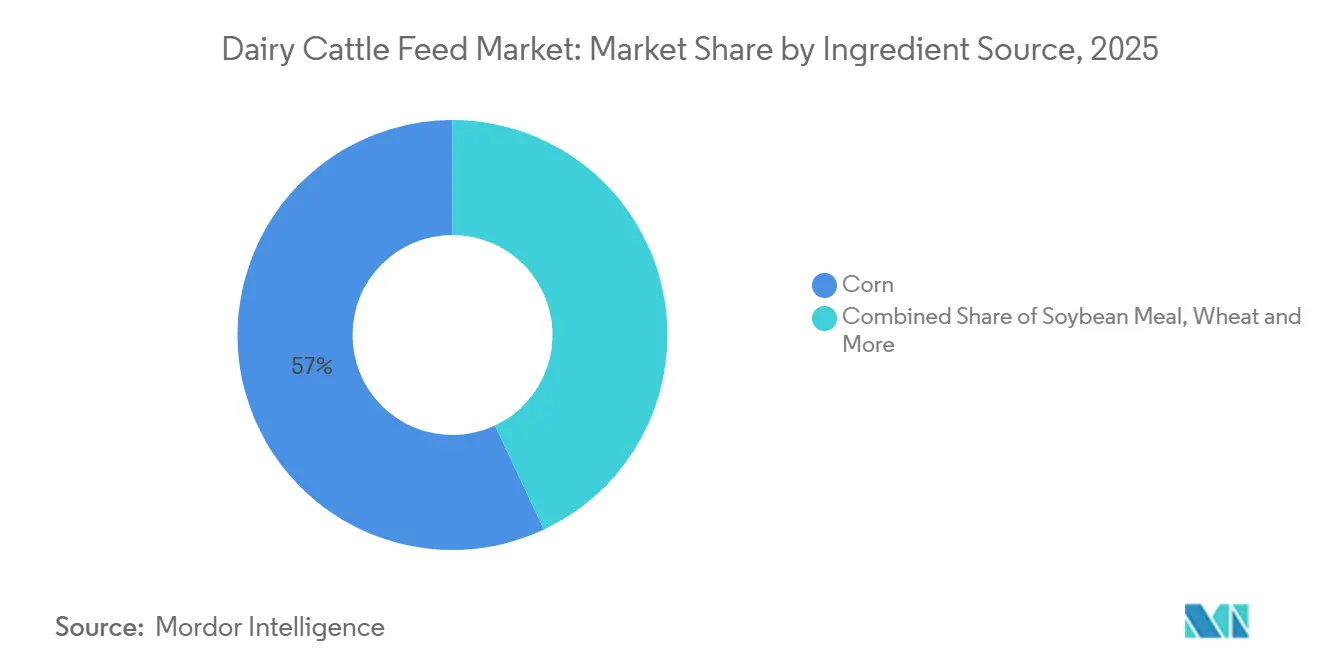

- By ingredient source, corn accounted for the largest 57% of the dairy cattle feed market share in 2025, and the soybean meal market size is growing at the fastest 7.9% CAGR from 2026 to 2031.

- By lifecycle stage, lactating cow rations commanded the largest 48% of the dairy cattle feed market share in 2025, and the calf starter market size is rising fastest at a 9.1% CAGR from 2026 to 2031.

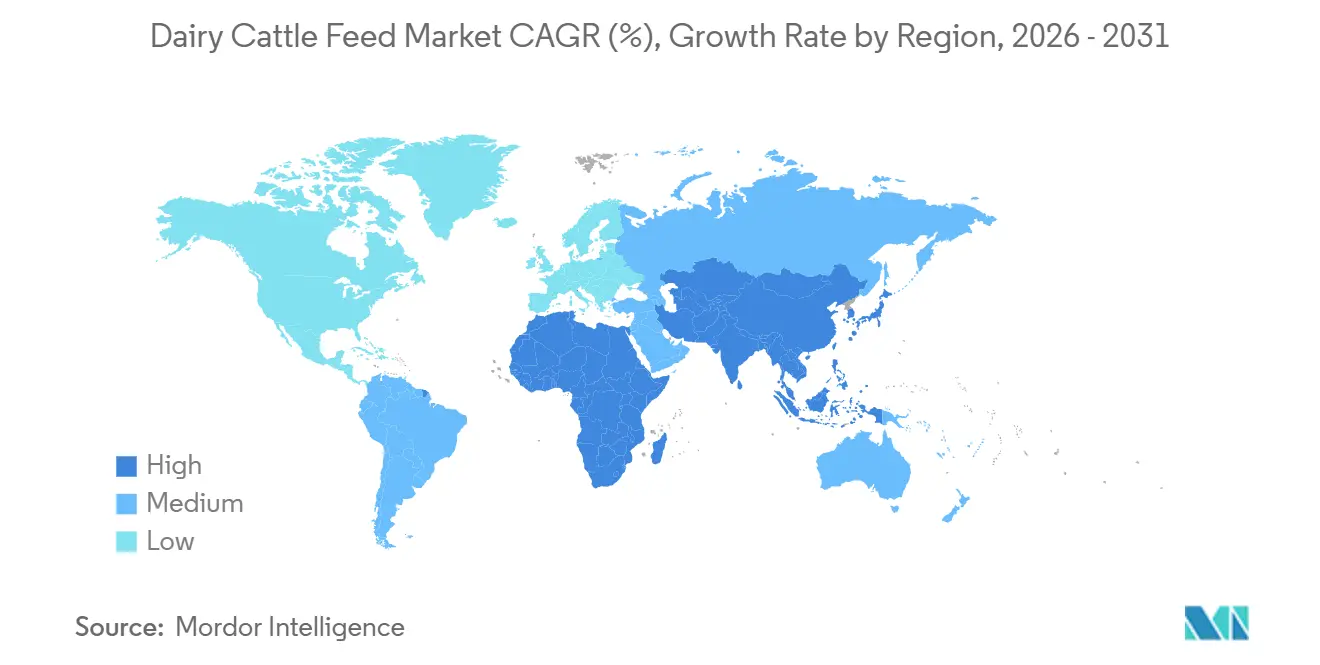

- By geography, North America accounted for the largest 29% of the dairy cattle feed market share in 2025, and the Asia-Pacific market size is rising fastest at a 7.4% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dairy Cattle Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing intensification of dairy farms in emerging economies | +1.2% | Asia–Pacific and South America | Medium term (2-4 years) |

| Adoption of precision-feeding software and IoT ration sensors | +0.8% | North America, Europe, and Australia | Medium term (2-4 years) |

| Surge in functional dairy demand for A2 and lactose-free products | +0.6% | Global with early gains in developed markets | Short term (≤ 2 years) |

| Volatility-hedging contracts for feed corn and soybean meal | +0.5% | Major grain-importing regions | Short term (≤ 2 years) |

| Carbon-credit programs rewarding low-methane dairy herds | +0.7% | North America, Europe, and Oceania | Long term (≥ 4 years) |

| On-farm insect bioconversion of manure into high-protein feed | +0.3% | Pilot sites in Europe and Asia–Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Intensification of Dairy Farms in Emerging Economies

The growth of dairy cattle farming in India is increasing the demand for ruminant and compound cattle feed, driven by rising herd productivity and structured feeding practices. According to the Government of India, milk production totaled 247.87 million metric tons in 2024–25, a 3.58% increase from 239.30 million metric tons in 2023–24, reflecting the expansion of organized dairy systems and larger herd sizes[1]Source: Government of India, Press Information Bureau (PIB), pib.gov.in. This growth underscores the need for nutritionally balanced ruminant feed to maintain productivity levels. As dairy farms transition to commercial operations with enhanced feed management practices, the use of formulated cattle feed is projected to increase, supporting sustained growth in the dairy cattle feed market.

Adoption of Precision-Feeding Software and IoT Ration Sensors

According to a study by the National Institutes of Health, the growth of dairy farms and larger herd sizes have increased the complexity of animal monitoring, resulting in challenges related to health, welfare, and productivity. The study emphasizes that precision livestock farming (PLF) employs sensors to monitor individual animals in real time, facilitating improved herd management and performance optimization[2]Source: Tangorra et al., “Internet of Things (IoT): Sensors Application in Dairy Cattle Farming,” National Institutes of Health (NIH), pmc.ncbi.nlm.nih.gov . These systems incorporate IoT technologies, including cloud computing and machine learning, to enable data-driven decision-making in dairy operations.

Surge in Functional Dairy Demand for A2 and Lactose-free Products

According to the National Institutes of Health, approximately 68% of the global population experiences lactose malabsorption, leading to a significant rise in demand for lactose-free dairy products. This change in consumer preferences is prompting processors to focus on milk composition and develop specialized dairy products. Consequently, dairy farms are implementing advanced feeding strategies to regulate lactose levels and enhance milk quality. The increasing emphasis on functional dairy products, such as lactose-free milk, is driving the adoption of precision nutrition and feed additives, thereby boosting demand for high-quality cattle feed designed for specific production objectives.

Volatility-Hedging Contracts for Feed Corn and Soybean Meal

Fluctuations in feed grain prices are prompting the increased use of risk management strategies within the dairy cattle feed market. Data from the University of Illinois, based on United States Department of Agriculture-linked information, indicates that corn futures rose from USD 4.69 per bushel on February 27, 2026, to USD 4.90 per bushel on March 13, 2026, highlighting short-term price volatility [3]Source: University of Illinois, “Projected Prices and Volatility Factors for 2026,” farmdocdaily.illinois.edu . This variability affects feed cost structures and profit margins for dairy producers. Consequently, feed manufacturers and farmers are increasingly adopting forward contracts and hedging tools to stabilize input costs, secure a consistent supply, and sustain profitability in dairy operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating phytosanitary import barriers on feed ingredients | -0.6% | Asia–Pacific, Middle East, and North Africa | Short term (≤ 2 years) |

| Antibiotic-use scrutiny tightening medicated-feed approvals | -0.4% | North America and Europe | Medium term (2-4 years) |

| Margin squeeze from alternative milk uptake | -0.3% | North America and Europe | Medium term (2-4 years) |

| Smallholder credit limitations in Africa and South Asia | -0.5% | Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Phytosanitary Import Barriers on Feed Ingredients

Increasingly stringent phytosanitary regulations are restricting global trade in feed ingredients, significantly affecting the supply availability for the dairy cattle feed market. The United States Department of Agriculture reports that the European Union's proposed stricter pesticide residue limits could impact agricultural exports worth over USD 5.4 billion annually [4]Source: United States Department of Agriculture Foreign Agricultural Service (USDA FAS), “EU Proposes to Reduce MRLs to Limit of Quantification for Pesticides on Imported Products through Food and Feed Omnibus Package,” fas.usda.gov. These regulatory measures raise compliance costs and restrict market access for exporters. Consequently, feed manufacturers encounter supply disruptions and price challenges, emphasizing the importance of diversified sourcing strategies and flexible procurement practices.

Antibiotic-Use Scrutiny Tightening Medicated-Feed Approvals

The Food and Drug Administration (FDA) Guidance 273, finalized in 2023, mandates feed manufacturers to submit updated duration-of-use data, leading to longer approval timelines. In Europe, regulations on cross-contamination enforce stringent limits on permissible therapeutic doses, necessitating either dedicated production lines or comprehensive cleaning procedures. These regulatory demands increase pressure on mill capacity, complicating efforts to sustain operational efficiency while adhering to evolving safety standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feed Type: Functional Additives Extend Value Capture

Energy feed led with the largest 40% of the dairy cattle feed market share in 2025, while the functional additives market size is advancing at the fastest 8.9% CAGR from 2026 to 2031. Producers are increasingly focusing on 3-nitrooxypropanol, as an investment in this additive can be offset through carbon credits and reduced methane-related milk levies. While energy feeds continue to dominate the dairy cattle feed market in terms of size, their share is gradually declining as feed mills allocate budgets toward probiotics, live yeast, and protected amino acids. Start-ups focusing on rumen microbiome modulation are entering a space previously dominated by medicated crumbles.

In practical ration formulation, enzymes and direct-fed microbials are combined with coated methionine to enhance protein efficiency. Functional additives could capture a significant market share if regulatory bodies accept prescription-like marketing strategies. Energy feeds will remain a key component, but are projected to shift toward local grain by-products when corn prices reach export-parity levels. This trend underscores the dairy cattle feed market's transition toward nutrient density over simple calorie content.

By Form: TMR Automation Drives Adoption

Pellets held the largest 46% of the dairy cattle feed market share in 2025, whereas the total mixed ration (TMR) market size is expanding at the fastest 9.7% CAGR from 2036 to 2031. Robotic mixers that weigh, blend, and deliver feed with high precision are driving advancements in the dairy cattle feed market. Large herds increasingly rely on Total Mixed Ration (TMR) robots to address staffing challenges caused by persistent labor shortages. As a result, the market for TMR components is expanding, particularly in regions where energy efficiency contributes to improved carbon scorecards, attracting interest from milk buyers.

While demand for crumble and mash feed remains steady in calf and heifer diets, its growth is limited. Conversely, the introduction of advanced TMR nutrient sensors, which transmit detailed data such as Neutral Detergent Fiber (NDF) and starch content to cloud-based dashboards, is transforming feed into a data-driven product. Feed mills capable of providing both the physical feed blend and accompanying data insights are positioned to benefit significantly in this evolving market.

By Ingredient Source: Soybean Meal Gains on Protein Fortification

Corn accounted for the largest 57% of the dairy cattle feed market share in 2025, and the soybean meal market size is growing at the fastest 7.9% CAGR from 2026 to 2031. The focus on achieving significant average daily gain in calf starters has intensified competition in protein sources. The premium for European Union-certified deforestation-free soy has increased, leading mills to explore partial substitutions with alternatives such as insect oil cake, canola, and palm kernel expeller. These developments indicate a shift towards diversifying protein sources in the dairy cattle feed market, reducing dependence on any single legume.

Alfalfa hay, wheat, and cassava chips are key components for fulfilling energy and fiber requirements in regions where local agronomic conditions allow their cultivation. These feed ingredients play a crucial role in supporting livestock nutrition and ensuring optimal productivity. Additionally, forward contracts and parametric weather insurance for corn and soy have become integral to mill–farmer agreements, addressing financial aspects in feed formulations to reduce risks and maintain stability in the supply chain.

By Lifecycle Stage: Calf Starter Innovations Drive Early Performance

Lactating cow rations commanded the largest 48% of the dairy cattle feed market share in 2025, and the calf starter market size is rising fastest at a 9.1% CAGR from 2026 to 2031. Early-stage nutrition is increasingly emphasized in dairy cattle feed, with calf starter formulations playing a significant role in rumen development and long-term productivity. Research highlights that calf starters generally contain 18% or more crude protein to promote growth and microbial activity in the developing rumen. The growing adoption of structured calf feeding programs and earlier transitions from milk to starter feed are driving demand for high-quality, digestible formulations.

Dry-cow and transition feeds are recognized for their role in balancing minerals to prevent milk fever and ketosis. Key components such as protected choline, chromium, and magnesium salts are increasingly emphasized, highlighting the growing acknowledgement of the critical impact of the pre- and post-calving period on a cow's productivity. Although the market size for these transition products is relatively small, it benefits from stable margins due to the significant technical support required and the specialized nature of these feeds.

Geography Analysis

North America is projected to account for 29% of the dairy cattle feed market share in 2025. States such as California, Wisconsin, Idaho, and Texas represent significant demand centers, supported by regional mills that provide Total Mixed Ration (TMR) startups and cloud-based analytics. Canada’s quota system stabilizes milk payments, which in turn balances feed budgets. Meanwhile, Mexico leverages its proximity to surplus ingredients from the United States, fostering a strong cross-border logistics network. Archer-Daniels-Midland Company (ADM) and Alltech, Inc. Akralos venture, launched in February 2026, highlights the region's focus on scaling operations and integrating technical services.

The Asia-Pacific market is projected to grow at a 7.4% CAGR from 2026 to 2031, making it the fastest-growing region. Government initiatives supporting cold-chain infrastructure and genotyping are increasing the demand for higher feed specification requirements. These programs aim to enhance the efficiency and quality of feed production, ensuring compliance with evolving industry standards. Although Australia and Japan are regarded as mature markets, they maintain a strong demand for feed traceability and functional additives that meet consumer expectations for sustainability, reflecting a growing emphasis on transparency and environmental responsibility.

Europe is navigating challenges such as stagnant milk production, stringent climate policies, and competition from plant-based alternatives. Carbon footprint considerations and residue limits are influencing ingredient choices, encouraging the use of regional grains and deforestation-free soy certifications. Eastern Europe remains a promising area for expansion, as demonstrated by ForFarmers’ recent activities in Poland. South America benefits from cost advantages associated with pasture-based systems but is increasingly adopting confinement diets to capture export opportunities.

Competitive Landscape

The market is moderately concentrated with major players includes Cargill, Incorporated, Archer-Daniels-Midland Company (ADM), Nutreco N.V. (SHV Holdings N.V.), Land O’Lakes, Inc., and De Heus Voeders B.V. Cargill, Incorporated’s feed production expansion in Punjab and Archer-Daniels-Midland Company’s joint operation with Alltech, Inc., in February 2026 illustrate how scale dovetails with proximity to growth nodes. Nutreco N.V.’s Skretting-style digital tools, Land O’Lakes, Inc.’s Truterra carbon monetization, and De Heus Voeders B.V.’s multi-country Southeast Asian spree reflect varied paths to the same end game to integrate feed, data, and sustainability into one farmer contract.

New entrants focus on digital ration optimization or low-methane solutions rather than bricks-and-mortar mills. According to Performance Livestock Analytics, Inc., its bunk monitoring systems are deployed across more than 4,000 sites, capturing data that can later feed into bespoke additive packages. Meanwhile, ingredient specialists such as Lallemand Inc., Evonik Industries AG, BASF SE, and DSM-Firmenich AG race to patent yeast, amino acids, and vitamins that tolerate high-temperature pelleting and still express in the rumen.

White-space remains in insect protein, methane vaccines, and seaweed derivatives. According to ArkeaBio, the company raised approximately USD 45.5 million in 2026 to develop a single-shot methane vaccine that could undercut daily additive dosing. Symbrosia is scaling its seaweed-based feed solutions for large-scale livestock applications, supported by trials demonstrating significant methane reduction potential across cattle systems, with ongoing commercialization efforts progressing toward 2026.

Dairy Cattle Feed Industry Leaders

Cargill, Incorporated

Archer-Daniels-Midland Company (ADM)

Nutreco N.V. (SHV Holdings N.V.)

Land O’Lakes, Inc.

De Heus Voeders B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: De Heus Voeders B.V.'s acquisition of CJ Feed and Care enhances its feed production and distribution network across Asia. This development bolsters the supply of feed in rapidly growing livestock markets. The acquisition addresses the increasing demand for nutritionally optimized cattle feed, driven by the expansion of intensive dairy and livestock farming systems.

- February 2026: Cargill, Incorporated inaugurated a dairy feed plant in Wazirabad, Punjab, India, with an investment of INR 300 crore (USD 36 million) and an annual production capacity of 400,000 metric tons. This facility is Cargill's largest dairy feed plant in South Asia and its second in Punjab.

- February 2026: Archer-Daniels-Midland Company (ADM) and Alltech, Inc. introduced Akralos Animal Nutrition. Leveraging formulation expertise and distribution networks, Akralos aims to deliver advanced, performance-focused cattle feed solutions, addressing the increasing demand from the market.

Global Dairy Cattle Feed Market Report Scope

Dairy cattle feed is a balanced nutritional formulation designed to fulfil the dietary requirements of milk-producing cattle. It aids in milk production, promotes animal health, and improves feed efficiency during various stages of growth and lactation. The dairy cattle feed market report is segmented by feed type (energy feed, protein feed, minerals, vitamins, functional feed, and others), form (pellets, crumbles, mash, total mixed ration, and others), ingredient source (corn, soybean meal, wheat, alfalfa, and others), lifecycle stage (calf starter, heifer grower, lactating cow ration, dry cow ration, and others), and geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Energy Feed |

| Protein Feed |

| Minerals |

| Vitamins |

| Functional Additives |

| Others |

| Pellets |

| Crumbles |

| Mash |

| Total Mixed Ration (TMR) |

| Others |

| Corn |

| Soybean Meal |

| Wheat |

| Alfalfa |

| Others |

| Calf Starter |

| Heifer Grower |

| Lactating Cow Ration |

| Dry Cow Ration |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Italy | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Feed Type | Energy Feed | |

| Protein Feed | ||

| Minerals | ||

| Vitamins | ||

| Functional Additives | ||

| Others | ||

| By Form | Pellets | |

| Crumbles | ||

| Mash | ||

| Total Mixed Ration (TMR) | ||

| Others | ||

| By Ingredient Source | Corn | |

| Soybean Meal | ||

| Wheat | ||

| Alfalfa | ||

| Others | ||

| By Lifecycle Stage | Calf Starter | |

| Heifer Grower | ||

| Lactating Cow Ration | ||

| Dry Cow Ration | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of global dairy cattle feed by 2031?

The dairy cattle feed market is projected to reach USD 105.8 billion by 2031.

Which feed type is expanding fastest?

Functional additives are growing at an 8.9% CAGR as producers target methane cuts and milk-quality premiums.

Why is total mixed ration gaining ground over pellets?

Automated TMR systems slash labor and energy costs while ensuring consistent nutrient delivery, driving a 9.7% CAGR through 2031.

Which region shows the quickest growth in feed demand?

Asia–Pacific market size is projected to grow at the fastest 7.4% CAGR from 2026 to 2031.

Page last updated on: