Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 35.52 Billion |

| Market Size (2026) | USD 39.52 Billion |

| Market Size (2031) | USD 67.41 Billion |

| Growth Rate (2026 - 2031) | 11.27% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Tourism Market Analysis by Mordor Intelligence

The Southeast Asia tourism market size is expected to grow from USD 35.52 billion in 2025 to USD 39.52 billion in 2026 and is forecast to reach USD 67.41 billion by 2031 at 11.27% CAGR over 2026-2031. This pace firmly places the Southeast Asia tourism market among the world’s fastest-expanding visitor economies, outstripping the growth rates in most other regions. The momentum in Southeast Asia's tourism market is driven by three key factors: streamlined visa reforms that have minimized travel barriers, the strategic network expansion by low-cost carriers resulting in reduced airfares, and the consistent growth in disposable incomes across a substantial consumer base. These drivers collectively enhance both origin and destination options, diversify revenue channels, and reinforce confidence in the market's ability to withstand future disruptions. Accommodation services remain the primary revenue generator; however, digital travel services, particularly dynamic packaging and in-destination activities, are capturing an increasing share of consumer spending as mobile platforms dominate the search, booking, and review processes. The MICE (Meetings, Incentives, Conferences, and Exhibitions) segment is witnessing a resurgence, with corporate planners finalizing long-delayed events. Simultaneously, leisure tourism continues to serve as the foundation, supporting employment within the hospitality sector across the region.

Key Report Takeaways

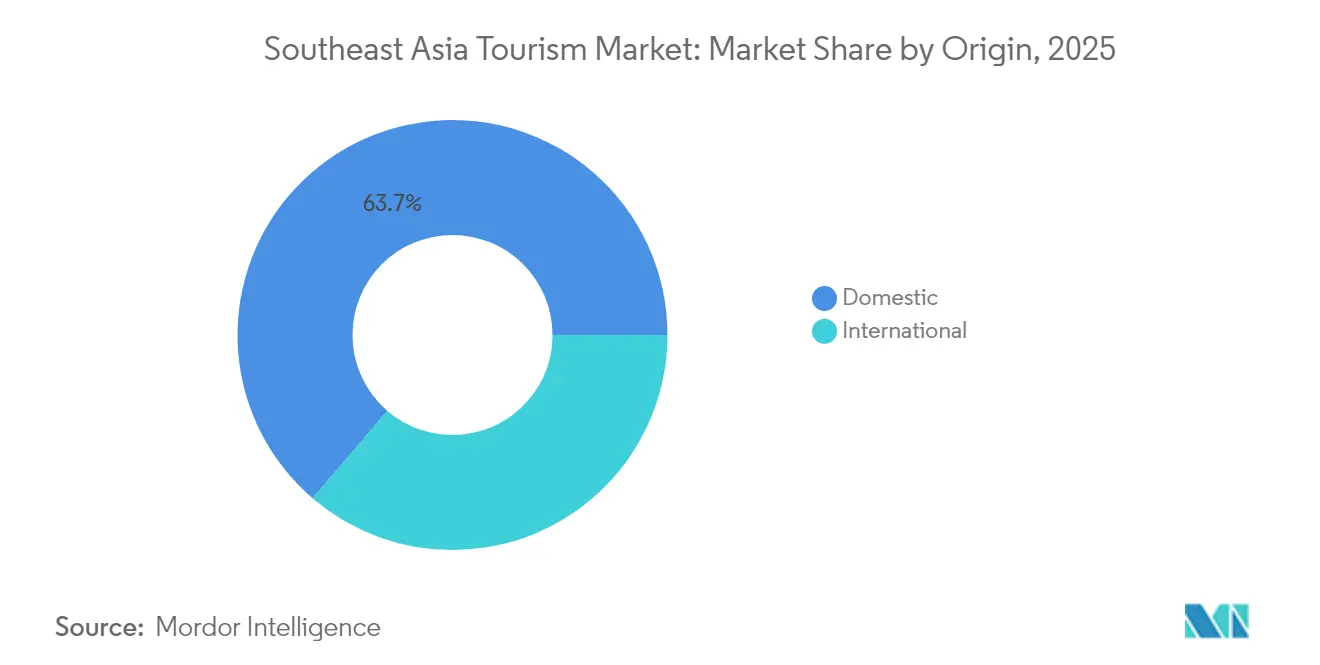

- By origin, domestic travel contributed 63.72% of the Southeast Asia tourism market share in 2025, whereas international arrivals are forecast to grow at an 11.05% CAGR through 2031.

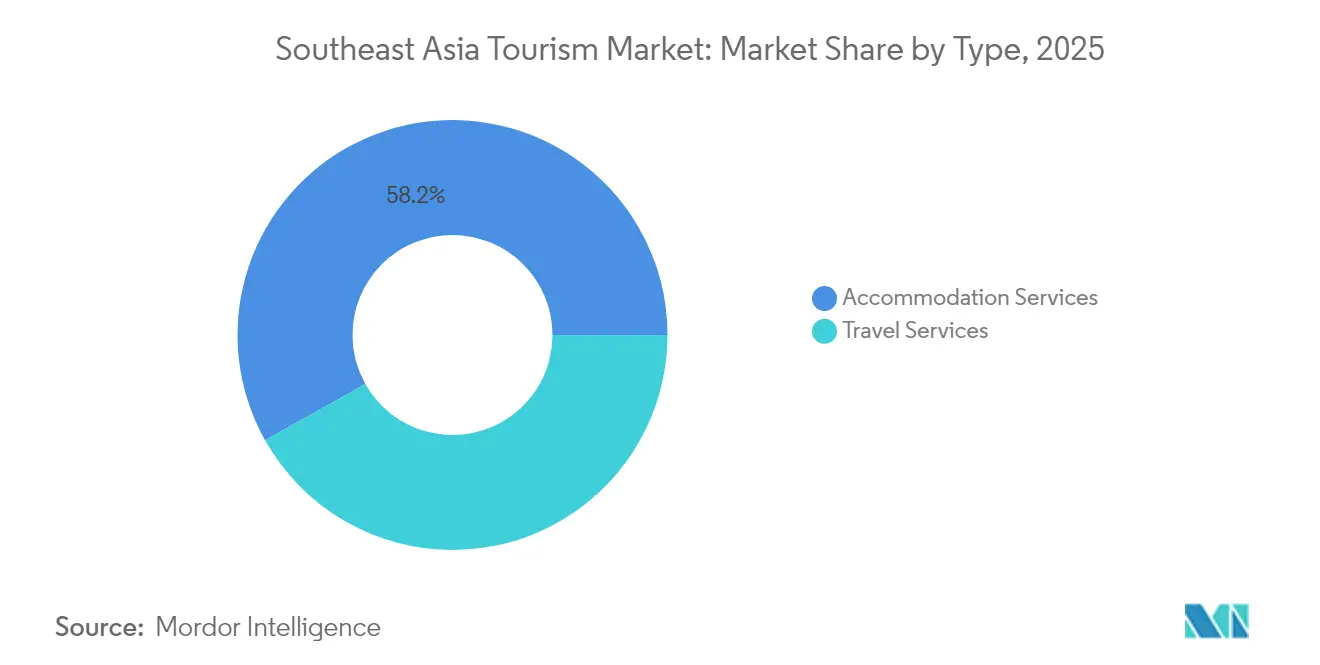

- By type, accommodation services held 58.15% of the Southeast Asia tourism market size in 2025; travel services are set to expand at a 12.01% CAGR during the same period.

- By purpose, leisure accounted for 46.89% of the Southeast Asia tourism market size in 2025, while the MICE segment is advancing at a 13.92% CAGR to 2031.

- By geography, Thailand commanded 19.06% of the Southeast Asia tourism market share in 2025, and Vietnam is projected to log the fastest 13.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Visa liberalization & e-visa rollouts | +2.1% | Global, with early gains in Thailand, Vietnam, Malaysia | Medium term (2-4 years) |

| Expansion of low-cost carrier (LCC) networks | +1.8% | ASEAN core, spill-over to secondary cities | Short term (≤ 2 years) |

| Rising disposable income of the intra-regional middle class | +1.5% | ASEAN domestic markets, China-ASEAN corridor | Long term (≥ 4 years) |

| Digital-nomad visa schemes and long-stay demand | +1.2% | Thailand, Malaysia, Philippines, Vietnam | Medium term (2-4 years) |

| Heritage-conservation PPPs catalysing cultural tourism | +0.9% | Vietnam, Cambodia, and Indonesia heritage sites | Long term (≥ 4 years) |

| Early adoption of crypto-payments in select destinations | +0.4% | Thailand (Phuket), Singapore, Malaysia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Visa Liberalization & E-Visa Roll-outs Drive Regional Integration

Southeast Asian policymakers now treat seamless entry as the linchpin of competitiveness, and the recent wave of exemptions illustrates collective intent. Thailand doubled visa-free stays to 60 days for 93 nationalities and introduced the Destination Thailand Visa that grants 180-day renewable residence to remote workers. Vietnam has enhanced its business environment by extending 45-day visa waivers for 12 European countries until 2028 and implementing digital systems to streamline approval processes for other markets[1]TAT Newsroom, “Thailand Targets High-Value Travellers to Fuel Long-haul Tourism Growth,” tatnews.org . Malaysia has strategically enhanced its tourism inflow by implementing long-term visa waivers for Chinese visitors, while the Philippines has introduced a digital-nomad permit aimed at attracting the global remote workforce. These policy measures have streamlined application processes and reduced compliance costs, resulting in extended visitor stays and increased expenditure. Collectively, these initiatives strengthen Southeast Asia's position as a leading and accessible multi-country tourism destination.

Expansion of Low-Cost Carrier Networks Transforms Regional Connectivity

Ten budget airlines secured Thai operating certificates in 2024, multiplying city-pair frequencies and linking previously isolated locales such as Mae Sot and Trang. AirAsia Group inaugurated cross-border routes that bypass capital hubs, Cebu Pacific partnered with Traveloka to penetrate mobile-first consumers, and Singapore Airlines deepened joint scheduling with Scoot to fill off-peak slots. Airlines in Southeast Asia are strategically responding to shifting traveler preferences, resulting in notable market changes. A substantial reduction in average round-trip fares, coupled with increased passenger traffic at secondary airports, highlights the region's expanding network density and enhanced geographic accessibility. The establishment of dedicated low-cost carrier (LCC) terminals in key cities such as Bangkok, Jakarta, and Ho Chi Minh City has optimized operational efficiency by reducing turnaround times. This operational improvement enables tighter scheduling, maintaining profitability despite lower fare yields. The availability of cost-effective and frequent flights provides the Southeast Asia tourism market with the flexibility to capitalize on demand driven by spontaneous travel decisions, particularly among millennials and first-time travelers.

Rising Disposable Income of the Intra-Regional Middle Class Fuels Domestic Demand

The middle-income population within ASEAN has experienced substantial growth since 2010, with forecasts indicating sustained expansion. Wage increases in key markets such as Indonesia, the Philippines, and Vietnam are driving demand for weekend city getaways, festival-related tourism, and culinary experiences. Additionally, Thailand's domestic tourism revenue now constitutes a significant share of total travel income, enhancing the Southeast Asia tourism market's ability to withstand external challenges. In 2024, Vietnam recorded 110 million domestic travellers, with a noticeable shift from hostel accommodations to boutique stays, which contributed to an increase in average daily expenditure. The increasing outbound travel activity among Chinese and Indian middle-class consumers is contributing to sustained year-round occupancy rates. This trend highlights the role of income-driven demand in supporting both travel volumes and revenue generation, even before accounting for long-haul travel arrivals.

Digital-Nomad Visa Schemes Capture Long-Stay Tourism Premium

Thailand leads with its 180-day Destination Thailand Visa that targets online professionals who often outspend leisure visitors two-to-one. The Philippines offers a renewable 12-month remote-work permit, and Vietnam drafts multi-entry visas of up to 36 months for retirees and knowledge workers[2]VietnamPlus, “Tourism Sector Thriving in 2024,” en.vietnamplus.vn . These strategies effectively transform short-term tourists into semi-residents, addressing low-season demand gaps while bolstering the sustainability of local businesses such as cafes, co-working spaces, and language schools. Furthermore, long-term visitors play a pivotal role in enhancing the destination's visibility by sharing their experiences online. This activity generates a network effect, attracting similar demographic groups and solidifying Southeast Asia's position as a preferred destination for individuals pursuing location-independent lifestyles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political instability & travel advisories | -1.6% | Myanmar, regional spill-over effects | Short term (≤ 2 years) |

| Infrastructure bottlenecks in Tier-2/3 cities | -1.2% | Indonesia, Philippines, Vietnam secondary cities | Medium term (2-4 years) |

| Overtourism-driven visitor caps at heritage sites | -0.8% | Bali, Hoi An, Angkor heritage corridors | Long term (≥ 4 years) |

| Climate-risk insurance cost spikes for airlines & resorts | -0.7% | Coastal regions, typhoon-prone areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Political Instability Creates Regional Tourism Disruption

Myanmar’s dramatic visitor collapse after the 2021 coup eliminated a once-promising destination and disrupted Mekong multi-country circuits. Cruise lines rerouted to avoid off-limit ports, and insurers raised premiums on regional itineraries that traverse contested waters. Sporadic protests in Malaysia and Indonesia occasionally trigger foreign travel advisories, leading to last-minute cancellations that squeeze small operators with thin cash reserves. Political risk, therefore, remains an unpredictable drag on the Southeast Asia tourism market, prompting businesses to invest in scenario planning and diversified source markets.

Infrastructure Bottlenecks Constrain Secondary-Destination Development

Operational delays at Long Thanh International Airport are intensifying capacity constraints in Ho Chi Minh City, highlighting the need for accelerated infrastructure upgrades. Similarly, the ongoing development of Indonesia's Nusantara is projected to alleviate congestion in Java, but its full impact is not expected to materialize until 2028. In the Philippines, inefficiencies in ferry scheduling and inadequate road networks are disrupting the seamless connectivity required for island-hopping tourism, thereby limiting the sector's growth potential. Furthermore, unreliable access to water and electricity in tier-3 cities is deterring hotel investments, as investors face challenges in securing stable utility services. These infrastructure bottlenecks are constraining the average length of stay and curbing tourist spending, thereby restricting the ability of Southeast Asia's tourism market to distribute economic benefits beyond primary gateway destinations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Origin: Domestic Resilience Anchors Market Stability

The domestic channel retains a 63.72%, proving a shock absorber when borders closed. Stimulus vouchers in Thailand and Indonesia funded hotel discounts and free attraction passes, sustaining labour in provincial economies. Vietnam reported 110 million domestic trips in 2024, with a significant shift observed in consumer behaviour. Mid-scale hotels experienced an increase in occupancy rates, indicating a trend where local travellers are opting for higher-quality accommodations. This development highlights a growing preference among domestic tourists to upgrade their lodging choices, reflecting an evolution in spending patterns and travel preferences within the market. A similar pattern emerged in Malaysia, where domestic trips to Penang and Kota Kinabalu doubled quarter-on-quarter, pushing room rates up despite moderate volumes. The Southeast Asia tourism market thus benefits from a vast internal customer base that backstops employment and public revenues.

International travel, though currently smaller, advances faster on an 11.05% trajectory. China's tourism sector has demonstrated a significant recovery, approaching pre-pandemic performance levels. Concurrently, extended visa waivers have encouraged European travelers to prolong their stays, contributing to increased tourism revenue. Long-haul travelers are generating higher daily expenditures compared to domestic tourists, thereby enhancing foreign-exchange inflows and strengthening the economic impact of international tourism. The introduction of digital-nomad visas is mitigating the effects of seasonality by transforming peak-period visitors into consistent, year-round contributors to the tourism economy. Furthermore, the adoption of simplified e-visa platforms is reducing customer acquisition costs for marketers, improving operational efficiency. By 2031, the Southeast Asia tourism market is expected to achieve greater financial stability through a balanced mix of domestic and international tourist flows, ensuring more predictable cash cycles and sustainable growth.

By Type: Travel Services Innovation Drives Segment Transformation

Accommodation retains the lion’s 58.15% share, underpinned by quarterly RevPAR gains at major chains. Asset-light franchises reduce capital exposure, allowing rapid flag planting in Bali, Da Nang, and Khanom. The adoption of sustainable retrofitting solutions, such as solar roofs and low-flow plumbing systems, is increasingly recognized for its ability to reduce operational energy costs while meeting the heightened environmental, social, and governance (ESG) standards demanded by corporate stakeholders. Concurrently, boutique brands operating within Southeast Asia's tourism market are strategically focusing on localized design approaches. By incorporating materials like reclaimed wood and indigenous textiles, these brands are effectively addressing the growing consumer demand for authentic and culturally resonant experiences.

Travel services enjoy a 12.01% CAGR as digital intermediaries scale. Traveloka’s API deal with Malaysia Airlines lets customers bundle flights, lounges, and travel insurance in two clicks. Tiket.com has partnered with Accor, integrating hotels into a unified loyalty wallet. This move aims to boost repeat bookings through targeted push notifications. Additionally, ancillary products like concert tickets, theme-park passes, and micro-insurance are enhancing the company's take rate, thereby reducing the profitability gap with accommodation providers. Furthermore, AI chatbots are streamlining service costs, while machine-learning recommender engines are improving conversion rates. These advancements underscore the pivotal role of data leverage in shaping the competitive landscape of Southeast Asia's tourism market.

By Purpose: MICE Tourism Emerges as Premium Growth Driver

Leisure still fills planes and seaside resorts, but yield growth relies on higher-value niches. MICE bookings now pace at 13.92% CAGR, supported by new convention halls in Bangkok, Kuala Lumpur, and Ho Chi Minh City. The Philippines has been granted the opportunity to host the ASEAN Tourism Forum in 2026, positioning the country as a key player in regional tourism initiatives. Concurrently, Cambodia forecasts significant growth in its MICE (Meetings, Incentives, Conferences, and Exhibitions) sector by 2025, reflecting the increasing importance of business tourism in the region. The Southeast Asia tourism market is further strengthened by the inclusion of weddings and religious gatherings, which contribute to demand during traditionally low seasons, thereby enhancing market resilience and purpose diversification.

The resurgence of corporate travel is driving an uptick in mid-week hotel occupancy rates, as businesses increasingly shift from virtual to hybrid meeting formats. This trend is further supported by the acceleration of regional trade, prompting suppliers to prioritize in-person plant visits. Medical tourism is also gaining traction in Thailand and Malaysia, underpinned by the presence of JCI-certified hospitals, which enhance the credibility and appeal of healthcare services in these countries. Additionally, educational exchanges are contributing to the utilization of dormitory facilities in key hubs such as Singapore and Kuala Lumpur. The growing popularity of esports tournaments, exemplified by the Mobile Legends event scheduled for the 2025 SEA Games, is attracting millennial audiences and diversifying the tourism market's demographic reach. This broadening of travel purposes mitigates demand volatility and establishes a more stable revenue foundation for the Southeast Asia tourism market, extending its growth potential beyond the traditional focus on beach holidays.

Geography Analysis

Thailand has established itself as a leader in airport revenue generation within Southeast Asia, driven by consistent and strategic infrastructure investments over the years. These investments include the expansion of airport capacity through the addition of runways and satellite terminals at key locations such as Bangkok and Phuket. Furthermore, the introduction of the "Destination Thailand" visa has strategically positioned the country as an attractive destination for digital professionals. This initiative has facilitated the growth of co-working hubs in cities like Chiang Mai and Phuket, further enhancing Thailand's appeal as a hub for remote work and business activities. Partnerships with Alipay+ make cashless payments ubiquitous, and a pending gambling law could unlock integrated resorts that redirect outbound Thai bettors home. Despite saturation risk at core beaches, new product themes, wellness retreats in Nakhon Si Thammarat, soft-adventure circuits in Phatthalung, spreading visitors inland, and preserving carrying capacity.

Vietnam's tourism sector has demonstrated significant growth, achieving a robust 13.22% expansion, as the country intensifies efforts to attract foreign tourists by 2030. Infrastructure improvements, such as expressway upgrades, have reduced travel time between Hanoi and Ha Long to two hours, enhancing accessibility to key destinations. In Hoi An, a UNESCO World Heritage site, authorities are implementing advanced crowd-management technology to regulate visitor flow and optimize ticket revenue generation. The government's visa waiver policy for European travelers has positively impacted the market by increasing the average length of stay and expenditure per visitor. Furthermore, the ongoing review of multiple-entry visa policies is expected to attract high-value segments, including retirees and yacht owners. Hotel development pipelines are increasingly concentrated in emerging coastal provinces such as Quy Nhon and Phu Quoc, signaling a strategic shift to diversify accommodation supply beyond the established hub of Danang.

Indonesia chases a 16 million foreign-visitor goal, pairing visa waivers for Brazil and Turkey with five “Super Priority Destinations” such as Lake Toba and Labuan Bajo that receive ring-fenced infrastructure budgets. Malaysia secures Chinese market stickiness via visa exemptions until 2036 and promotes eco-tourism in Sabah’s Danum Valley. Singapore positions itself as the region’s high-yield gateway, integrating cruise terminals, Changi Airport, and world-class events, while leveraging technology to cap manpower costs. The Philippines blends domestic strength with inbound MICE prospects, using upgraded Cebu and Boracay facilities to host ASEAN Tourism Forum 2026. Cambodia and Laos participate in Greater Mekong Sub-region marketing to tap shared circuits, thus ensuring that every ASEAN member plays a role in the expanding Southeast Asia tourism market.

Competitive Landscape

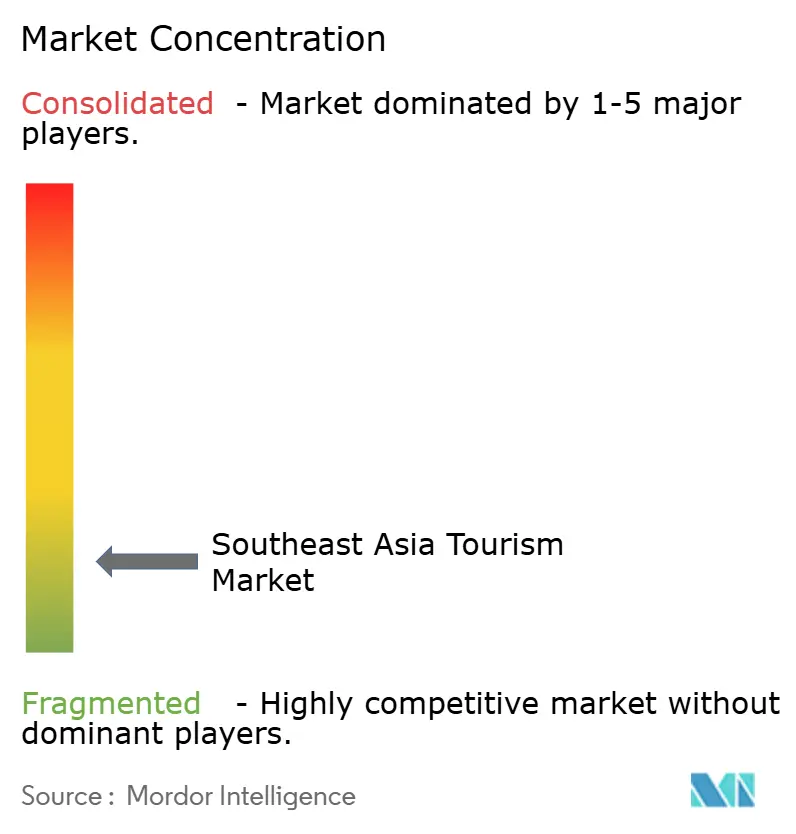

The tourism market in Southeast Asia demonstrates a fragmented structure, with the leading players collectively holding a relatively small market share. Companies such as Traveloka and Agoda are actively competing to enhance customer loyalty by integrating innovative features, including buy-now-pay-later (BNPL) financing options and multi-currency digital wallets, to differentiate their offerings. AirAsia Group is diversifying its revenue streams by incorporating fintech solutions, such as foreign-exchange cards and ride-sharing services, into its ecosystem, thereby reducing its reliance on seat sales. Similarly, Singapore Airlines is leveraging strategic joint ventures with Scoot and Vistara to strengthen its wide-body traffic network, enabling the airline to secure a competitive position in the profitable long-haul travel segment.

Sunway Hotels has strategically aligned with the Global Hotel Alliance to leverage its extensive loyalty program, enabling access to a broad customer base and enhancing cross-promotional opportunities. Within the Southeast Asia tourism market, boutique hotel chains are increasingly adopting culturally inspired designs to differentiate themselves from established international brands. This approach not only strengthens their market positioning but also contributes to a more diverse and competitive industry landscape.

Technological partnerships intensify. Accor ports inventory to tiket.com, accessing 20 million monthly active users. Traveloka allies with Malaysia Airlines and Singapore Tourism Board to co-fund digital campaigns and share customer analytics. ESG credentials now influence corporate RFPs: Singapore pursues ISO 20121 certification for events, and Thailand’s “Green SEA Games” initiative pre-qualifies suppliers that meet carbon baselines. Esports tourism emerges as a niche battleground, with Mobile Legends: Bang Bang integrated into SEA Games 2025 underpinned by new sponsorship revenue. Players agile enough to weave sustainability, technology, and experience curation will seize margin leadership as the Southeast Asia tourism market passes USD 60 billion by decade-end.

Southeast Asia Tourism Industry Leaders

Singapore Airlines

AirAsia Group

Agoda (Booking Holdings)

Traveloka

Garuda Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sunway Hotels & Resorts joined Global Hotel Alliance and GHA DISCOVERY loyalty programme, integrating 11 properties across Malaysia, Vietnam, and Cambodia into the network serving 30 million members, Hospitality Net.

- November 2024: ONYX Hospitality Group and Malaysia’s Equatorial Group signed a joint venture for EQ Phuket luxury hotel project with THB 2.5 billion investment, featuring 180 units on Kata Beach with 2028 opening target Hospitality Net.

- November 2024: Accor forged a global strategic partnership with Indonesian OTA tiket.com, integrating over 490 Asian hotels across 17 brands into tiket.com’s booking platform, with worldwide expansion planned by 2025.

- September 2024: Traveloka and Malaysia Airlines signed a regional strategic partnership MoU at the MATTA Fair Kuala Lumpur, combining the airline network with the technology platform for enhanced travel experiences.

Southeast Asia Tourism Market Report Scope

The South East Asia Travel and Tourism industry report covers information about the countries in the region, the type of travel, and the mode of travel. Additionally, the report will cover insights on Online travel market in the region, driver and restrains to the market. The report will also cover information on some of the major players active in the region.

By Origin

| Domestic |

| International |

By Type

| Accommodation Services |

| Travel Services |

By Purpose

| Leisure |

| Business |

| Visiting Friends & Relatives (VFR) |

| Religious |

| Meetings-Incentives-Conferences-Exhibitions (MICE) |

| Other Purposes |

By Geography

| Indonesia |

| Thailand |

| Malaysia |

| Singapore |

| Philippines |

| Vietnam |

| Rest of Southeast Asia |

| By Origin | Domestic |

| International | |

| By Type | Accommodation Services |

| Travel Services | |

| By Purpose | Leisure |

| Business | |

| Visiting Friends & Relatives (VFR) | |

| Religious | |

| Meetings-Incentives-Conferences-Exhibitions (MICE) | |

| Other Purposes | |

| By Geography | Indonesia |

| Thailand | |

| Malaysia | |

| Singapore | |

| Philippines | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large could visitor spending become in Southeast Asia by 2031?

The region’s receipts are forecast to reach USD 67.41 billion by 2031, powered by an 11.27% CAGR.

Which destination shows the strongest medium-term growth?

Vietnam leads with a projected 13.22% CAGR through 2031, driven by visa reforms and infrastructure upgrades.

What share of tourism receipts come from domestic travelers?

Domestic journeys account for 63.72% of total spending, giving the market a stable revenue floor.

Why is the MICE segment critical now?

MICE arrivals grow at 13.92% CAGR and spend more per day than leisure tourists, lifting average yields.

How will gambling legalization affect Thailand’s positioning?

Casino-integrated resorts could attract high-roller segments and diversify Thailand’s product mix beyond beach leisure.

Is the competitive field easy for new entrants?

Yes, with the top firms holding a small share, the market remains open to innovators and niche specialists.

Page last updated on: