Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 258.03 Billion |

| Market Size (2026) | USD 283.03 Billion |

| Market Size (2031) | USD 449.45 Billion |

| Growth Rate (2026 - 2031) | 9.69% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Online Travel Market Analysis by Mordor Intelligence

The North America Online Travel Market size was valued at USD 258.03 billion in 2025 and estimated to grow from USD 283.03 billion in 2026 to reach USD 449.45 billion by 2031, at a CAGR of 9.69% during the forecast period (2026-2031).

Momentum comes from always-connected consumers, rapid mobile adoption, and new payment choices that shorten the path from inspiration to purchase. Mobile bookings already account for 57% of all online reservations, underscoring how smartphones have become the control center for trip planning. Airline New Distribution Capability (NDC), the spread of short-term rentals, and flexible “buy now, pay later” (BNPL) options are widening product choice and nudging transaction values upward. At the same time, state-level rules on home-sharing, stubbornly high merchant fees, and persistent cybersecurity risks work as brakes on what is otherwise a high-velocity expansion of the North America online travel market.

Key Report Takeaways

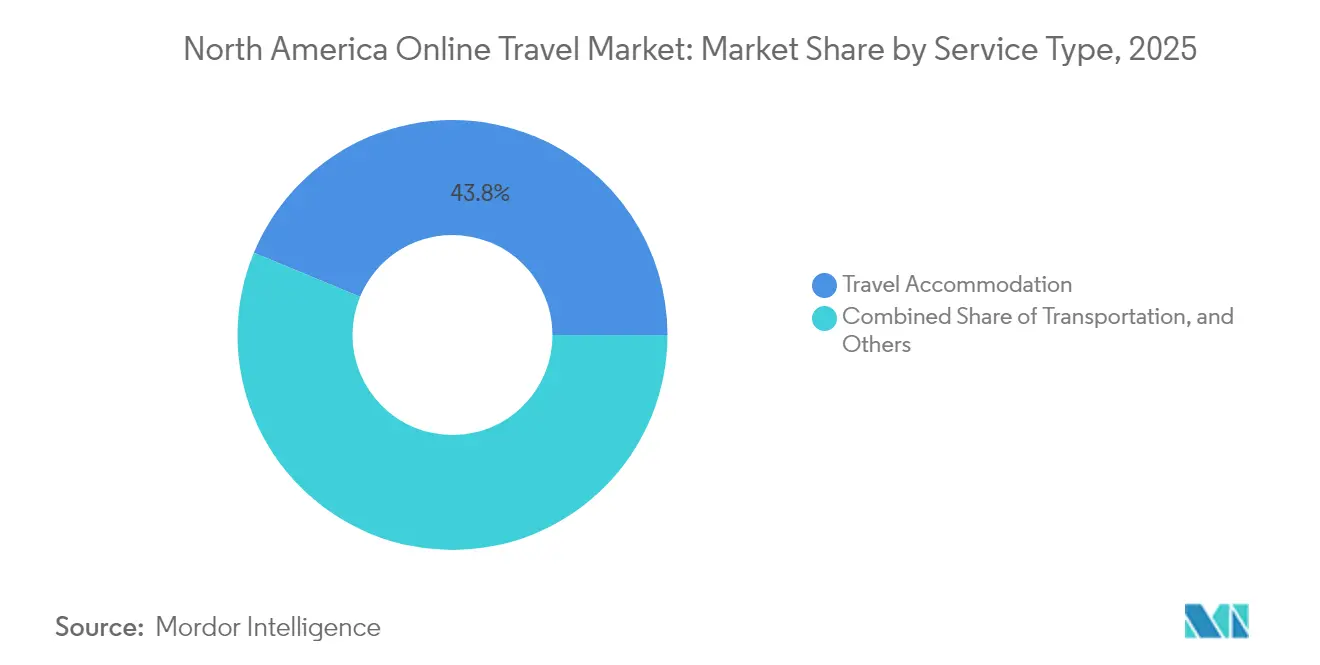

- By service type, travel accommodation led with 43.75% of the North America online travel market share in 2025, while vacation packages are forecast to grow at a 10.39% CAGR through 2031.

- By device, smartphones captured 56.18% of bookings in 2025; desktop remains important, yet mobile is projected to post an 11.55% CAGR to 2031 in the North America online travel market.

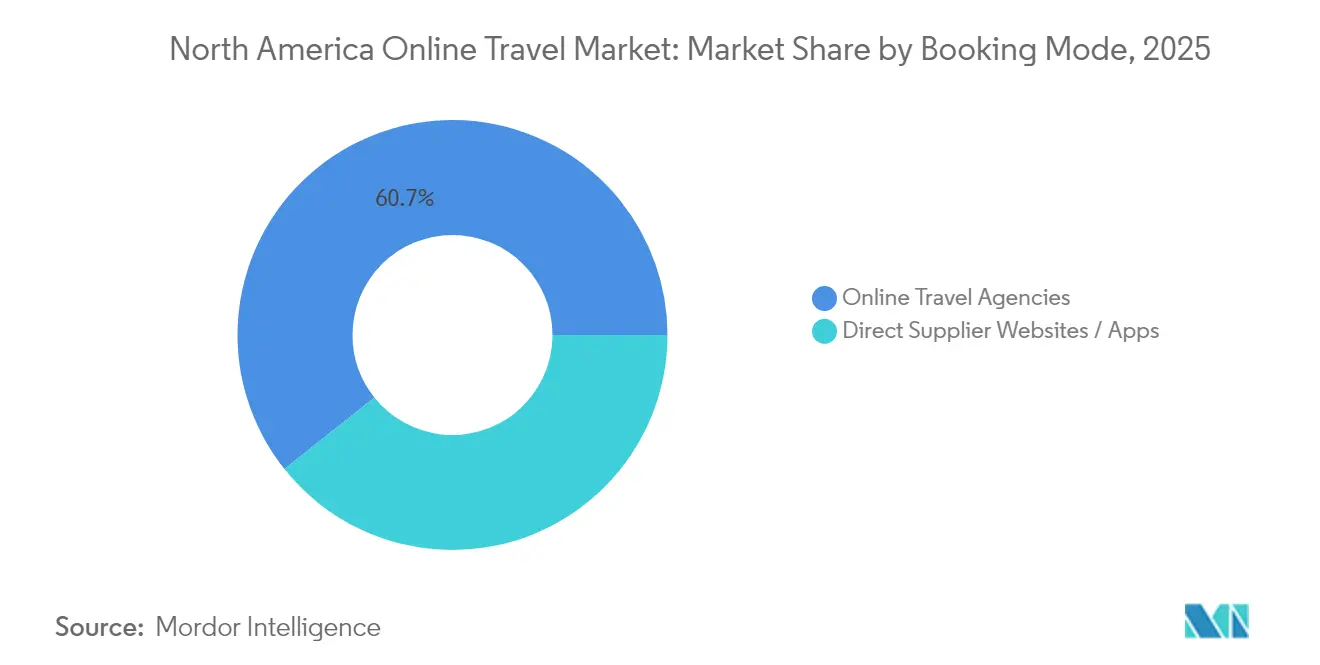

- By booking mode, online travel agencies held 60.72% share of the North America online travel market size in 2025, whereas direct supplier apps are set to expand at a 8.97% CAGR to 2031.

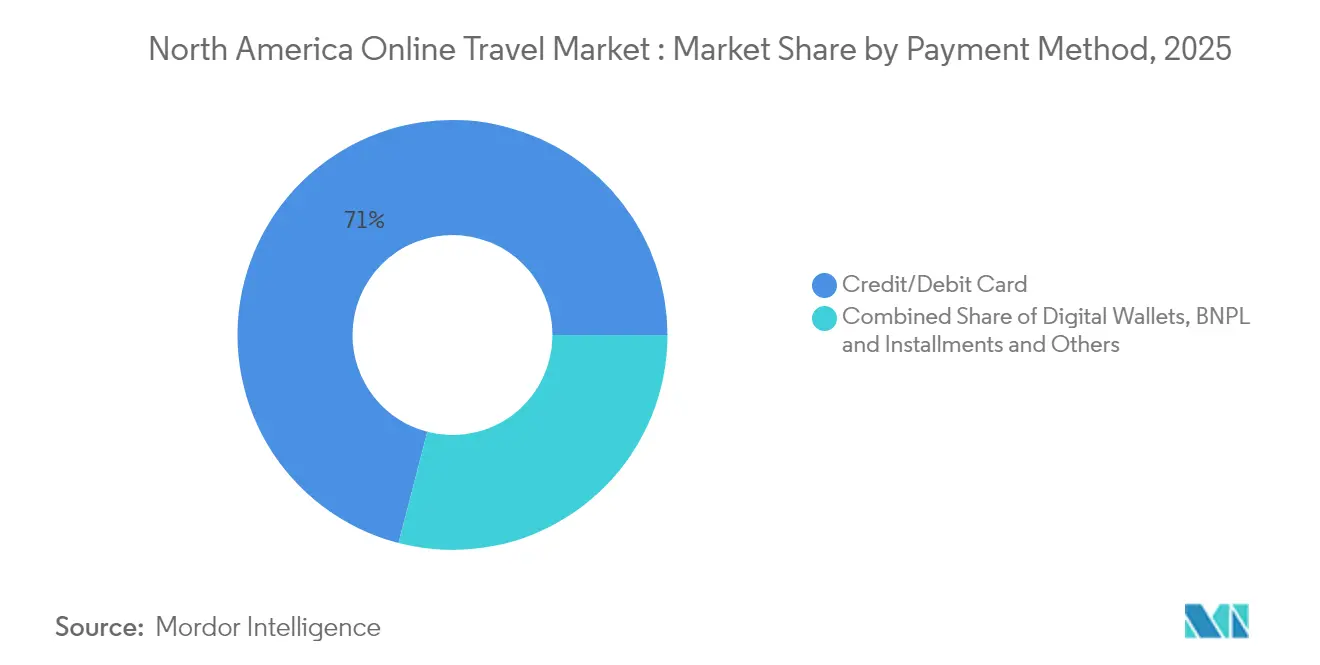

- By payment method, credit/debit cards retained 70.96% revenue share in 2025, but BNPL is the fastest-growing option with an 17.48% CAGR expected through 2031.

- By purpose of travel, leisure accounted for 67.34% of total spend in 2025 and is advancing at an 10.12 % CAGR.

- By age group, millennials commanded 44.72% of bookings in 2025; generation Z is the quickest riser with an 11.08% CAGR.

- By geography, the United States dominated with 80.95% share in 2025, while Mexico is forecast to post the region’s fastest 8.62% CAGR.

- The five largest players—Expedia Group, Booking Holdings, Airbnb, TripAdvisor, and Hopper—collectively held major market share in 2024, signaling a highly concentrated competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Online Travel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone-Led Shift to In-App Bookings Across U.S. | + 2.0% | United States, with spillover effects in Canada and Mexico | Medium term (2-4 years) |

| Airline NDC Adoption Enabling Personalized Offers | + 1.5% | North America, with strongest impact in the U.S. | Medium term (2-4 years) |

| Rising Popularity of Short-Term Rentals in Canada | + 1.2% | Canada, with influence on U.S. border regions | Short term (≤ 2 years) |

| Buy-Now-Pay-Later (BNPL) Integration Boosting Conversion in Mexico | + 1.8% | Mexico, with growing adoption in the U.S. | Short term (≤ 2 years) |

| AI-Powered Trip Planning Tools Elevating User Engagement | + 1.4% | North America, led by U.S. urban centers | Medium term (2-4 years) |

| Government Easing of Border Restrictions & Canada eTA Uptake | + 0.8% | Canada-U.S. border regions, Mexico-U.S. travel corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smartphone-Led Shift to In-App Bookings Across the United States

Mobile channels already capture 57% of transactions, and usage is climbing 12.2% each year. Younger cohorts drive the surge: Millennials hold a 45.11% share, and Generation Z bookings rise nearly 12% annually. Mobile interfaces support impulse reservations, location-based upselling, and richer ancillary sales that desktops rarely match. Strong 4G/5G coverage and 85% national mobile internet penetration provide the infrastructure base [1]Source: U.S. Department of Commerce, “NTIA Internet Use Survey,” commerce.gov. As a result, the North America online travel market benefits from greater engagement, longer session times, and higher attach rates for excursions and insurance.

Airline NDC Adoption Enabling Personalized Offers

By deploying NDC, carriers push real-time, tailored bundles that lift ancillary revenue per passenger by 15% [2]Source: U.S. Department of Transportation, “Airline Ancillary Revenue Statistics 2024,” transportation.gov. Dynamic pricing widens fare classes while offering seat selection, lounge access, and carbon offsets inside one screen. OTAs and metasearch engines increasingly carry this enriched content, making NDC a network effect across the North America online travel market. Airlines able to combine loyalty data with NDC pipelines report sharper yield management and lower distribution costs, reinforcing competitive advantages that ripple through allied segments such as insurance and vacation packaging.

BNPL Integration Boosting Conversion in Mexico

BNPL & Installments usage is growing at an 18.25% CAGR, the fastest of any travel payment tool. For mid-to-high-value vacation packages—already the quickest service-type segment—split payments ease sticker shock and pull forward bookings. Banco de México notes a 43% annual jump in alternative-payment transaction volume. Mexican suppliers adopting BNPL see higher cart conversion and longer lead times, which helps optimize inventory and airfare yield. The effect extends across the North America online travel market as U.S. platforms pilot similar offers to stay competitive in price-sensitive segments..

AI-Powered Trip Planning Tools Elevating User Engagement

Generative AI now curates itineraries, predicts real-time crowding, and auto-rebooks disrupted segments. Large agencies disclose technology spending up 32% in 2024. Conversational search lowers friction, while machine-learning pricing engines fine-tune offers by time-of-day and proximity. Suppliers using AI personalize promotions at scale, pushing higher conversion and loyalty metrics that feed back into the North America online travel market growth loop.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-Level Restrictions on Short-Term Rentals in U.S. Cities | -1.0% | Major U.S. urban centers (New York, San Francisco, Boston) | Medium term (2-4 years) |

| High Merchant & Interchange Fees Raising Cost Pressures | -0.8% | North America, with highest impact in the U.S. | Long term (≥ 4 years) |

| Cybersecurity & Data-Privacy Breaches Eroding Consumer Trust | -1.2% | North America, particularly affecting large OTAs | Medium term (2-4 years) |

| Airline Capacity Constraints Driving Price Volatility | -0.9% | Major U.S. and Canadian air travel hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

State-Level Restrictions on Short-Term Rentals in U.S. Cities

More than 70 metropolitan areas revised home-sharing laws between 2022 and 2024. Licensing caps and zoning bans thin inventory in top demand hubs, crimping the 44.10% accommodation segment. Hosts pivot to suburban zones, altering search patterns and length-of-stay norms inside the North America online travel market. Platforms divert marketing spend into compliant listings, slowing expansion and raising acquisition costs in regulated locales.

High Merchant and Interchange Fees Raising Cost Pressures

Payment processing charges remain stubbornly high, particularly on cross-border card transactions. OTAs absorbing these fees face a margin squeeze and often pass costs on through service charges, dampening price elasticity. The burden weighs heavier on low-cost carriers and value-based lodging suppliers, eroding competitiveness versus cash-heavy rivals. Over time, elevated fee structures may accelerate supplier push toward direct channels, reshaping revenue flows across the North America online travel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Bundled Experiences Propel Vacation Package Upswing

The travel accommodation segment commanded 43.75% of revenue in 2025, cementing its role as the anchor of the North America online travel market. Deep property inventory, from branded hotels to alternative rentals, keeps comparisons easy and prices transparent. At the same time, Vacation Packages are projected to advance 10.39% annually through 2031, outpacing every other service type. Personalized packaging engines blend flights, lodging, and on-ground activities, raising perceived value and pushing average order size higher. The “North America online travel market size” benefits as bundling drives cross-sell opportunities that lift overall spend per passenger.

Vacation packages also allow suppliers greater yield control by shifting inventory in shoulder seasons, smoothing revenue volatility that historically affected standalone hotel or air bookings. OTAs leverage machine-learning insights to tailor itineraries around traveler personas, shortening search time and lifting satisfaction scores. Transportation remains steady as multimodal search gains traction, with the U.S. Bureau of Transportation Statistics citing a 28% rise in online multimodal reservations in 2024. Ancillary categories—tours, insurance, experiences—embrace contextual selling; push notifications timed to weather or local events encourage incremental spend, adding depth to the North America online travel market.

By Device Type: Mobile Booking Supremacy Continues to Expand

Mobile accounted for 56.18% of all bookings in 2025, growing at a 11.55% CAGR into the next decade. That dominance shapes app interface priorities, from one-tap payment to biometric login. Gen Z contributes the fastest motor, boosting traffic and advocating social-media driven discovery that converts directly inside apps. The “North America online travel market size” sees incremental growth as richer in-app functionalities drive ancillary attachment rates and loyalty enrollments.

Desktops persist for multi-stop or high-value itineraries where larger screens aid comparison. Tablets play a research role, often seeding intent that later closes on smartphones. Suppliers experiment with QR code triggers at airports and attractions to capture real-time upsell moments. Continuous design optimization for smaller screens keeps bounce rates in check, preserving funnel efficiency across the North America online travel market.

By Booking Mode: Direct Channels Seek Margin Relief

Online travel agencies retained a 60.72% share of the North America online travel market in 2025, yet direct supplier channels are gaining ground with an anticipated 8.97% CAGR. Major hotel chains sharpen loyalty program benefits—free Wi-Fi, room-type upgrades, app-only rates—to entice repeat usage. Airlines similarly encourage app downloads with push-upgrade offers and automated re-accommodation features during irregular operations.

OTAs counter by embedding virtual agents, same-page insurance quotes, and multi-supplier vacation bundles that direct channels cannot easily replicate. The result is an innovation race that improves consumer choice and compresses booking friction. As supplier apps proliferate, marketing cost per acquisition could drop, allowing reallocation toward product development, a net positive for the North America online travel market.

By Purpose of Travel: Leisure Demand Steers Product Innovation

Leisure trips represented 67.34% of the booking value in 2025. Experiences now outpace material goods in household priority, a trend most visible among Millennials and Gen Z. Suppliers respond by curating local, authentic excursions ranging from farm-to-table dining to street art walks. Customizable cancellation windows and fully refundable codes satisfy risk-averse consumers, widening conversion.

Business travel grows with an 8.54% annual expansion expected through 2031, important even as remote work shifts company policies. Hybrid schedules spawn “bleisure” extensions, lengthening stays and adding weekend nights that pump incremental revenue. Meetings meanwhile migrate toward secondary markets with lower costs and looser restrictions, redistributing spend across a wider geography. This flexibility keeps demand resilient and enriches supply diversity inside the North America online travel market.

By Payment Method: Financial Flexibility Wins Wallet Share

Credit and debit cards processed 70.96% of transactions in 2025, but BNPL models are racing ahead, projected at 17.48% CAGR. Flexible installments turn big-ticket vacations into manageable monthly outlays, enlarging the addressable audience. Digital wallets benefit from tokenization and biometric authentication, soothing cybersecurity anxieties that remain a key restraint. For cross-border itineraries, multi-currency wallets sidestep punitive FX fees and simplify reconciliation.

The surge in BNPL & Installments also yields earlier booking windows, granting airlines and hotels clearer demand visibility and better inventory controls. Alternative rails—bank transfers, vouchers, crypto—address specific traveler niches and local regulations, ensuring the North America online travel market can serve a spectrum of budgets and risk profiles.

By Age Group: Emerging Gen Z Sets New Experience Benchmarks

Millennials generated 44.72% of bookings in 2025, yet Gen Z will supply the steepest curve with nearly 11.08% annual growth. Gen Z’s ethos prizes sustainability, peer reviews, and social validation, prompting platforms to enhance eco-labels and creator-led storytelling. Generation X stays prominent for family vacations and multi-room stays, while Baby Boomers uphold premium cabin and luxury cruise demand.

Cross-generational influence is tangible: features first rolled out for digital natives—such as frictionless in-app re-booking—rapidly become baseline expected by older travelers. This democratizes innovation and pushes universal design, thereby broadening the North America online travel industry adoption across demographics.

Geography Analysis

The United States dominated the North America online travel market with 80.95% revenue share in 2025. High per-capita spend, wide broadband coverage, and an inventory spectrum spanning national parks to urban attractions make the country a self-sustaining demand engine. TSA checkpoint throughput reached 2.94 million on 24 June 2024, underscoring robust domestic air traffic even against inflation headwinds . Strength in home-market leisure travel, where 68% of trips stay within U.S. borders, cushions the sector from external shocks and fuels platform scale advantages.

Mexico, holding a smaller base, is the fastest climber, tracking a 8.62% CAGR through 2031. Infrastructure upgrades, such as new terminals at Cancún and Guadalajara, streamline airlift, while BNPL adoption lowers affordability barriers for domestic and inbound tourists. The Ministry of Tourism recorded a 12% uptick in international arrivals during 2024. Mobile booking penetration mirrors regional averages, validating cross-border scalability for app-centric models that have already matured in the United States.

Canada's online travel market continues to evolve with unique regulatory developments and changing travel patterns. The country's online travel sector is particularly influenced by the rising popularity of short-term rentals, which is reshaping the accommodation landscape and contributing to the overall dominance of the Travel Accommodation segment.

Regulatory Landscape

Regulation shaping North America online travel continues to be driven by consumer protection, accommodation taxation, and tourism-program funding across the United States, Canada, and Mexico. In Canada, Alberta raised its tourism levy from 4% to 6% for accommodation bookings made after March 31, 2026, directly affecting total trip costs and price transparency across OTA and direct booking flows.

Policy actions in 2026 also focused on destination development and permitting friction. On July 14, 2026, Alberta brought the Traveller Protection and Destination Development Act into force, setting a framework for destination marketing fees and traveler protections, while British Columbia launched an Adventure Tourism Hub in April 2026 to streamline permitting. This operational change can influence tour and activity suppliers whose inventory increasingly sells through online channels. At the federal level, Innovation, Science and Economic Development Canada announced an additional CAD 6 million for the Indigenous Tourism Fund (SITES stream) in March 2026, supporting product development that expands bookable experiences on digital platforms.

Value Chain Analysis

The value chain starts with travel suppliers (airlines, hotels and resorts, alternative lodging hosts, rail and bus operators, car rental firms, cruises, and attractions), which supply inventory, rates, and policies into distribution rails. Distribution is carried out through supplier direct websites and apps, as well as OTAs (including metasearch and affiliate partners). Airline NDC content and packaging engines increasingly shape what is merchandised and how ancillaries such as seats, bags, insurance, and activities are attached.

Beneath distribution, enablers include cloud infrastructure, identity and fraud tools, cybersecurity controls, and payments orchestration (cards, digital wallets, and BNPL). Post-booking servicing (changes, refunds, disruption handling, customer support) and reputation systems (reviews and content) then feed back into re-purchase behavior. Cost and performance bottlenecks concentrate in payments and digital resilience, with high merchant and interchange fees, particularly on cross-border card transactions, pressuring OTA take rates and encouraging suppliers to push direct-channel adoption via loyalty benefits and app-only offers. Demand-side volatility also travels through the chain: cross-border sentiment and trade-related uncertainty were flagged in 2025 surveys by the American Bus Association, National Tour Association, and Student and Youth Travel Association, while Canada-based operators reported reduced U.S.-origin bookings, tightening utilization for tours and packaged products. With mobile accounting for the majority of online reservations (56.18% in 2025 in this report), app performance, secure authentication, and uptime are gating factors for conversion and ancillary attachment across the ecosystem.

Competitive Landscape

Competition in the North America online travel market is concentrated, with the top five players jointly holding major market share. Expedia Group continues to lean on bundled package capabilities and large loyalty enrollment, Booking Holdings refines price-parity algorithms, and Airbnb scales Experiences to deepen traveler engagement beyond lodging. TripAdvisor harnesses review volume to funnel traffic into meta-search and instant booking, while Hopper deploys predictive pricing to carve out a fast-growing mobile niche.

Strategic investments trend toward vertical integration: Expedia integrates finance with point-of-sale credit, Booking acquires ground-transport tech, and Airbnb experiments with ticketed events. AI remains the common denominator, underscored by a 32% jump in technology outlays reported in collective SEC filings. This arms race targets real-time personalization, fraud mitigation, and operational efficiency.

White-space opportunities persist in luxury, eco-tourism, and niche adventure segments where dominant platforms have limited curation. Smaller specialists differentiate via deep local supplier relationships and purpose-driven branding. Still, high customer-acquisition costs and platform fee structures often push independents toward partnership or acquisition, further reinforcing the scale advantages enjoyed by incumbents within the North America online travel market.

North America Online Travel Industry Leaders

Expedia Group, Inc.

Booking Holdings Inc.

Airbnb, Inc.

TripAdvisor LLC

Hopper Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities center on expanding engagement beyond a single booking into full-trip orchestration, using AI and deeper partner integrations to increase attachment of activities, ground transport, and protection products within the same funnel. Company actions in 2026 show how this whitespace is being pursued, including Expedia Group's Explore 26 effort to introduce new AI-powered traveler experiences and its expanded ecosystem capabilities, such as tighter integration with ride-hailing (Uber) to keep more trip steps inside the app. On the supply side, InterContinental Hotels Group completed an eight-year core systems overhaul, including a new reservation platform and AI-enabled revenue management, which supports cleaner pipes for personalized offers and more consistent availability and pricing across direct and third-party channels.

Payments flexibility and compliant data usage remain practical conversion levers in a market where credit and debit cards still led with 70.96% share in 2025 in this report, while BNPL is the fastest-growing payment method within the same scope. The Affirm and UATP partnership announced in May 2025 expands airline BNPL enablement, supporting higher-value itineraries and packages that benefit from installment economics. At the same time, short-term rental rules across major U.S. cities and new tourism tax mechanics, including Alberta's 2026 levy change, have turned policy monitoring into a product requirement. Platforms increasingly need to invest in listing compliance, fee disclosure, and localized pricing logic, which creates openings for tools and partnerships that reduce regulatory overhead for suppliers and intermediaries.

Recent Industry Developments

- July 2026: Expedia Group ran a one-day Summer Flash Deal on July 7, 2026, offering up to 50% off select hotels for travel through December 31, 2026. The promotion highlights how major OTAs use time-boxed pricing events to stimulate demand and compete with direct supplier channels, while also filling inventory in defined travel windows.

- May 2026: Airbnb announced its 2026 Summer Release, adding new service categories such as car rentals, grocery delivery, airport pickups, and curated FIFA World Cup 2026 experiences. Expanding into trip logistics and event-linked experiences can increase opportunities to capture more of the traveler wallet beyond accommodation and to deepen engagement inside the app.

- May 2025: Affirm and UATP announced a partnership to enable pay-later options across airline merchants. The collaboration expands BNPL availability within airline checkout flows, supporting conversion for higher-ticket trips and establishing a route for broader installment-payment adoption across online travel platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the online travel market in North America covers the value of travel bookings completed through digital channels, including airline and other transport tickets, lodging stays, and online holiday bundles paid through websites or mobile apps.

Scope exclusions: Offline travel agency bookings, corporate travel management service fees, and travel-related insurance that is sold separately outside the booking flow are excluded.

Segmentation Overview

- By Service Type

- Transportation

- Air Travel

- Bus & Coach Travel

- Rail Travel

- Car Rental

- Cruise

- Travel Accommodation

- Hotels & Resorts

- Alternative Lodging / Rentals

- Vacation Packages

- Others (Activities, Travel Insurance, Ancillary)

- Transportation

- By Device Type

- Desktop / Laptop

- Mobile (Smartphone)

- Tablet

- By Booking Mode

- Online Travel Agencies (OTAs)

- Direct Supplier Websites / Apps

- By Purpose of Travel

- Leisure

- Business

- By Payment Method

- Credit / Debit Card

- Digital Wallets

- BNPL & Installments

- Other (Bank Transfer, Cash, Crypto)

- By Age Group

- Generation Z (18-24)

- Millennials (25-40)

- Generation X (41-56)

- Baby Boomers (57-75)

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market perimeter and to anchor major demand signals that can be checked year over year. We relied on public sources such as the U.S. National Travel and Tourism Office releases, Statistics Canada travel and tourism tables, and Banco de Mexico tourism statistics, followed by airline and airport traffic indicators published by industry bodies and airports.

To avoid building estimates on one narrow data series, travel price and activity signals were cross-checked using sources such as the U.S. Bureau of Labor Statistics CPI travel components, U.S. Bureau of Transportation Statistics air passenger data, and government border entry datasets. These were complemented with company annual reports, earnings call transcripts, investor presentations, and trusted press coverage, plus selective use of paid subscriptions for company financials and a shipment-level import and export database where it helped validate travel-linked payment and device trends. The sources listed here are illustrative, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to stress-test assumptions that are not visible directly in public data, especially channel mix shifts between direct supplier sites and intermediated bookings. We spoke with online travel operators, travel suppliers, payment and booking technology participants, and travel industry advisors across the United States, Canada, and Mexico, then reconciled the feedback to tighten model inputs and remove outlier growth views.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | |

| Mid tier: 47% | Functional/Unit leaders: 29% | |

| Smaller Players: 15% | Managers: 59% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where travel demand and spending signals were reconstructed into a digital booking value pool for North America, then filtered through online penetration by major travel categories. To keep the result realistic, we corroborated totals with selective bottom-up checks, such as sampled booking value roll-ups from public company disclosures, channel checks on commission and take-rate patterns, and sanity checks using average booking value multiplied by transaction volume where data was available.

Key inputs included indicators such as air passenger volumes, lodging demand and occupancy signals, travel price inflation (airfares and lodging CPI), smartphone and mobile booking adoption, and the share of travel purchases completed through websites and apps. When inputs were missing for a country or a travel category, gaps were handled using nearest-neighbor proxies (for example, similar traveler mix and price indices), then adjusted based on interview feedback. Forecasting used scenario analysis supported by simple trend fitting on the major drivers, and the final path was accepted only after it aligned with how experts expect channel mix and travel pricing to move over the next few years.

Data Validation & Update Cycle

Validation was done by comparing model outputs against independent signals, including travel volume trends and travel price inflation, then checking that implied booking values did not drift too far from what public companies and industry bodies suggest. We also ran variance checks across the United States, Canada, and Mexico so that a single-country assumption did not silently distort the regional total.

Before sign-off, the model and assumptions go through step-by-step analyst reviews, and re-contacts are triggered when there is a large mismatch between interviews and secondary signals. The report is refreshed annually, and interim updates are made when material events occur, such as sharp travel demand shifts, large pricing changes, or policy moves that affect cross-border travel. Right before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's North America Online Travel Market Size Measured Against Other Published Estimates

Published market sizes for online travel in North America can look far apart because the underlying definition is not always the same, even when the titles sound similar. Differences usually come from what is counted as online travel, which countries are included, and whether the figures reflect booking value or only a narrower revenue stream.

Some estimates narrow the geography to the United States and Canada only, or they mix in offline agency activity through broader travel agent channels. Mordor Intelligence counts online bookings across the United States, Canada, and Mexico for transport, accommodation, and bundled packages, and it excludes offline storefront transactions and corporate travel management service fees so the number stays tied to digital checkout behavior.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 258.03 B (2025) | |

| Industry Research Publisher A | USD 166.10 B (2025) | Uses a smaller country set (United States and Canada) and may apply a tighter service scope, which lowers the booking value pool versus a full North America roll-up that includes Mexico and bundled packages. |

| Industry Publisher B | USD 229.00 B (2023) | Anchors the series to an earlier base year and applies a different inflation and recovery path, so the implied 2025 value can diverge even if the overall channel definition is similar. |

Looking across the table, the spread is mainly explained by geography coverage and by how the measured value is constructed over time. When the included countries and the booking categories are clearly stated, and the inflation and demand inputs are checked against travel volume signals, the resulting market size becomes easier to trace and repeat for planning purposes.

Key Questions Answered in the Report

What is the projected size of the North America online travel market by 2031?

The market is forecast to reach USD 449.45 billion by 2031, growing at a 9.69% CAGR.

Which service type is expanding the fastest in the North America online travel market?

Vacation Packages are projected to post a 10.39% CAGR through 2031 as travelers seek bundled, value-driven experiences.

How significant are mobile bookings today?

Smartphones accounted for 56.18% of all online travel reservations in 2025 and are still expanding at a 11.55% CAGR

Why is BNPL important for travel sellers in North America?

BNPL transactions are growing at 17.48% annually, improving conversion rates and making higher-value trips more affordable, especially in Mexico.

Page last updated on: