Waterproof Breathable Textiles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

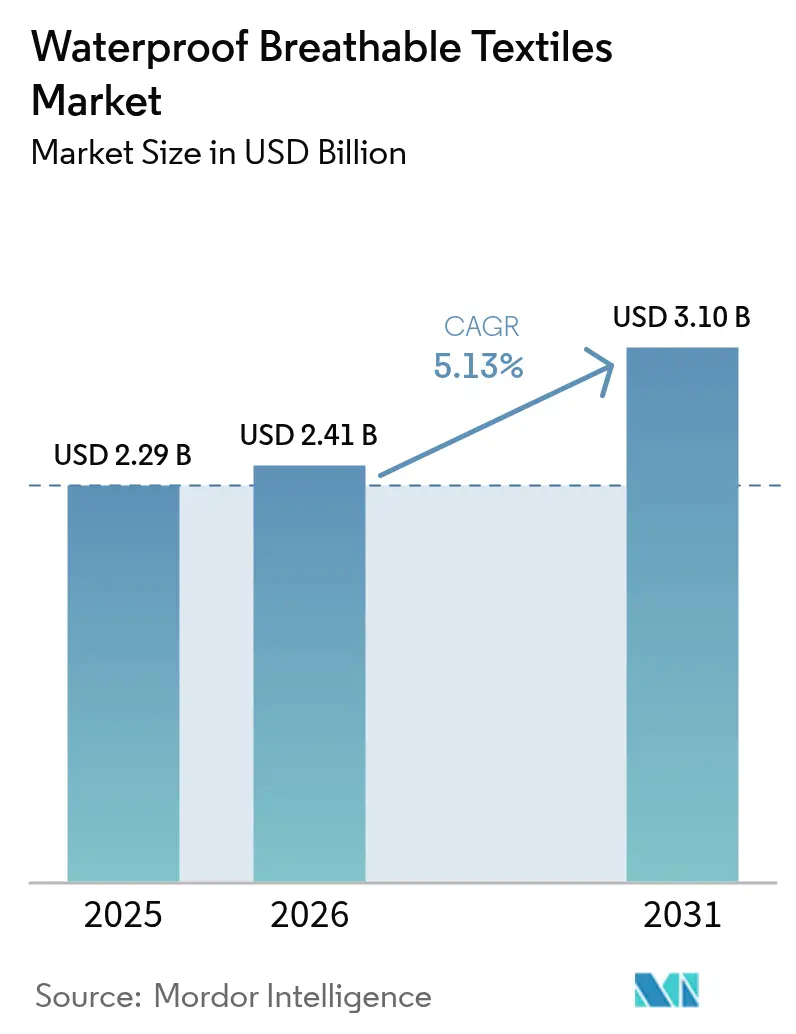

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.10 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Waterproof Breathable Textiles Market Analysis by Mordor Intelligence

The Waterproof Breathable Textiles Market size is expected to grow from USD 2.29 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 3.10 billion by 2031 at 5.13% CAGR over 2026-2031. Brands are accelerating PFAS-free chemistry adoption, premiumizing bio-based polyurethane while launching solvent-free lamination that lowers volatile-organic-compound footprints. The price of PTFE feedstocks is volatile, yet the strategic migration toward expanded polyethylene membranes and recycled-polyester substrates cushions disruption. Mass-market “gorpcore” styling folds technical shells into everyday wardrobes, widening average sell-through rates even as consumers extend gear replacement cycles. Suppliers that combine vertical integration with agile order quantities seize share from license-heavy incumbents, while near-shore production sites in Mexico, Portugal, and Vietnam compress lead times and support rapid design refreshes.

Key Report Takeaways

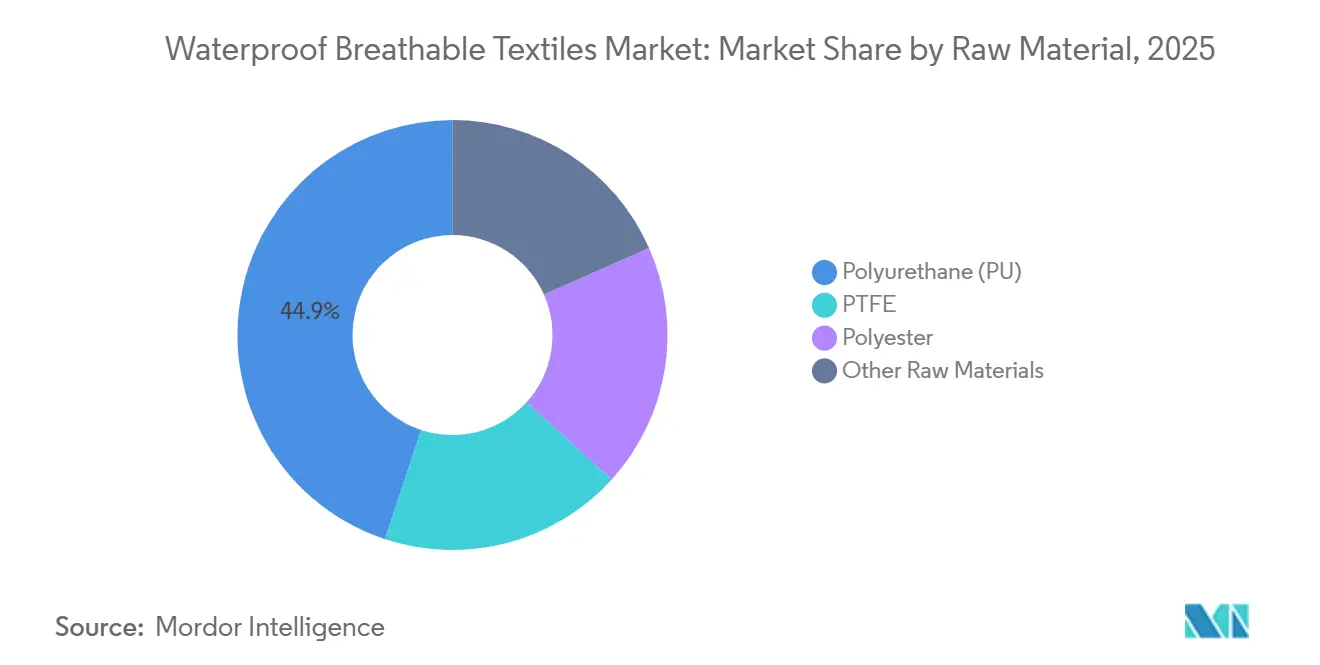

- By raw material, polyurethane captured 44.92% of the waterproof breathable textiles market share in 2025 and is projected to expand at a 5.80% CAGR through 2031.

- By textile, membrane-based constructions accounted for 64.83% of the waterproof breathable textiles market size in 2025. Coated fabrics are advancing at a 5.95% CAGR through 2031.

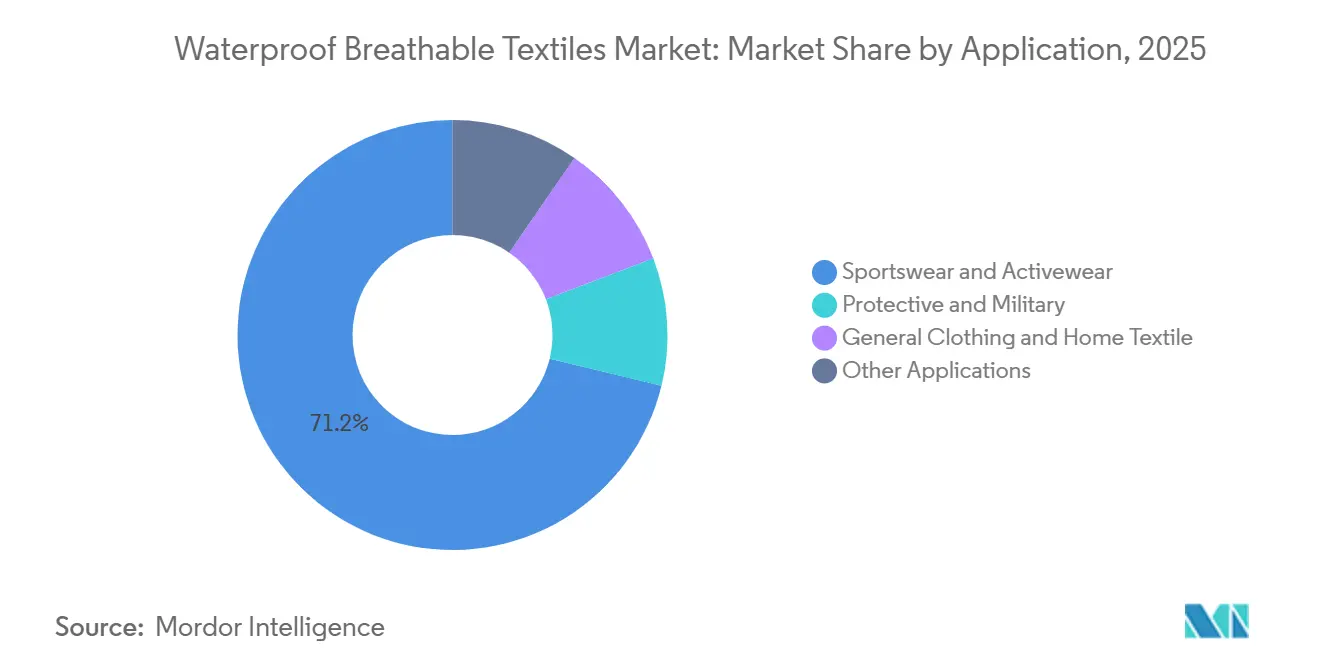

- By application, sportswear and activewear led with 71.21% revenue share in 2025. Protective and military garments are forecast to grow at a 5.87% CAGR to 2031.

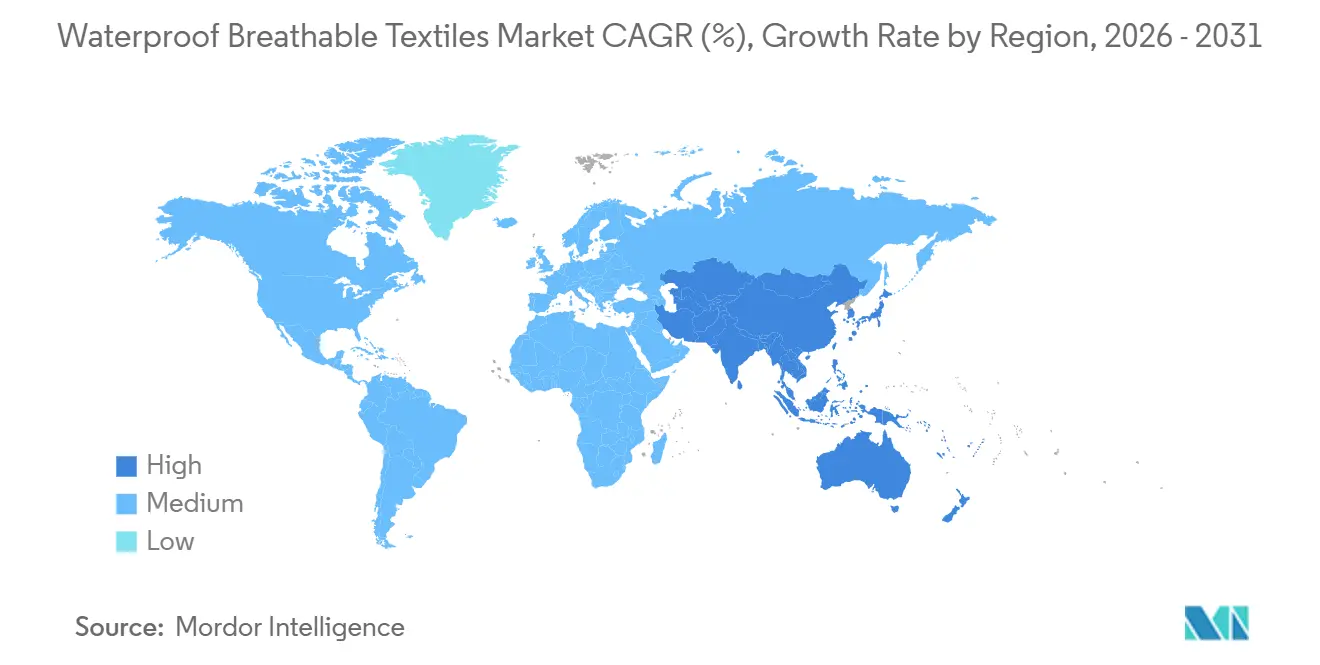

- By geography, Europe commanded 32.39% of the 2025 volume, and Asia-Pacific is set to increase at a 5.55% CAGR, the quickest among all regions, highlighting its pivotal role in the waterproof breathable textiles market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Waterproof Breathable Textiles Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from sports and outdoor apparel | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Expansion of technical protective workwear and military tenders | +0.9% | North America, Europe, ASEAN countries, the Middle East | Medium term (2-4 years) |

| Climate-resilient infrastructure boosting rain-gear sales in emerging economies | +0.7% | ASEAN core, South America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Advancements in bio-based polyurethane and solvent-free lamination technologies | +0.8% | Global, with research and development hubs in Germany, Japan, United States | Short term (≤ 2 years) |

| Micro-adventure urban outdoor trend spurring casual waterproof fashion | +1.0% | Urban centers in North America, Europe, East Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand From Sports and Outdoor Apparel

In 2024, outdoor participation surged, welcoming U.S. consumers who now prefer breathable shells over traditional cotton blends. Urban trail networks have claimed a significant share of gear purchases, integrating waterproof jackets into daily wear. Columbia’s OutDry Extreme Eco III showcases a membrane-free bonding technique, lightening the load for commuters balancing office hours and trailhead adventures[1]Columbia Sportswear, “Columbia OutDry Extreme Eco III Jacket,” columbia.com. Patagonia has successfully maintained a high hydrostatic-head rating in its H2No 3-layer system, eliminating PFAS treatments and demonstrating the feasibility of fluorine-free products. With France set to enforce a PFAS ban in 2026 and Denmark imposing restrictions in 2025, late reformulators face potential shelf-space challenges. Brands that adapt swiftly not only ensure their presence in EU retail but also command premium prices in specialty outlets.

Expansion of Technical Protective Workwear and Military Tenders

In 2025, NATO and Indo-Pacific modernization efforts led to a procurement surge. Notably, the U.K. mandated an ISO 343 Level 3 breathable outer for its VIRTUS armor refresh. Industrial standards are evolving in tandem with military needs; for instance, EN 343 Class 3 now mandates a moisture transfer of at least 15 g/m²/h, sidelining older PVC-coated nylons. Furthermore, updated ANSI/ISEA guidelines tailored for humid offshore rigs have unlocked a market potential in the Gulf of Mexico and North Sea basins. In a similar vein, Malaysia's 2025 amendments to occupational safety laws now mandate breathable rain gear on construction sites, creating a ripple effect of opportunities across ASEAN.

Climate-Resilient Infrastructure Boosting Rain-Gear Sales

ADB has rolled out a flood-resilience initiative in the Philippines, mandating waterproof workwear for infrastructure teams. This approach is now being mirrored by both Vietnam and Indonesia. Coated textiles are clinching these tenders, outbidding membrane laminates. In Brazil, the 2024 floods led to an urgent acquisition of jackets, allowing local mills to land disaster-response contracts. The African Union, through its adaptation fund, has set aside funds for rain gear for smallholder farmers in 2025, bolstering the demand for coated fabrics.

Advancements in Bio-Based Polyurethane and Solvent-Free Lamination Technologies

Waterborne PU achieves an adhesion strength while eliminating VOCs. In 2025, castor-oil polyols accounted for a significant portion of the PU feedstock, resulting in a reduction in life-cycle carbon intensity. This move aligns with SBTi targets for brands like The North Face and Jack Wolfskin. Covestro has developed a CO₂-based polyol platform that effectively sequesters industrial emissions. Pertex has introduced the Diamond Fuse process, which is solvent-free and skips adhesive layers prone to delamination, thus enhancing durability and reducing defect rates. While premium labels readily invest in sustainability, value players are biding their time, awaiting mandates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory phase-out of PFAS chemistries | -1.1% | Europe, North America, export-oriented APAC mills | Short term (≤ 2 years) |

| High processing and capital costs versus conventional fabrics | -0.6% | Global, acute in South America and MEA | Medium term (2-4 years) |

| PTFE feedstock supply-chain disruptions amid geopolitical tensions | -0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Phase-Out of PFAS Chemistries

In April 2026, ECHA imposed a restriction on PFHxA, a prevalent short-chain PFAS, impacting DWR treatments. France's 25 ppm threshold mandates testing costs, extending lead times. California's AB-1817 adds layers of complexity for brands operating across multiple regions[2]California Legislature, “California AB-1817,” leginfo.legislature.ca.gov. Silicone DWRs, needing an additional weight, incur extra costs. Gore invested significantly to retrofit its Elkton and Putzbrunn plants for ePE membrane lines, a feat beyond the reach of smaller competitors.

High Processing and Capital Costs Versus Conventional Fabrics

Each membrane lamination line comes with a high price tag, limiting entry to major players like Toray and Teijin. While coated-fabric lines demand a more modest investment, they also necessitate climate-controlled ovens, a luxury often out of reach for many in emerging markets. PU-coated polyester commands a significantly higher price compared to basic DWR-treated taffeta. This price disparity limits penetration at retail price points below USD 100. Additionally, seam-sealing adds extra cost per jacket, further widening the premium over standard water-resistant outerwear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: PU Balances Cost and Sustainability

Polyurethane accounted for 44.92% of raw-material demand in 2025 and is on course for a 5.80% CAGR, underpinning the waterproof breathable textiles market size gains in cost-sensitive and green-label segments. Its compatibility with waterborne dispersions and castor-oil polyols reduces VOCs and carbon intensity. Polyester supplies most coated-fabric substrates and is benefiting from recycled-content targets. PTFE retains relevance in alpine and defense niches despite feedstock volatility and regulatory scrutiny.

The “Other Raw Materials” bucket—polyamide, polypropylene, graphene-oxide coatings—remains small yet strategically important. Teijin’s Nanofront 700-nm fibers create waterproofness via weave density alone, lowering material costs by 20 to 25 percent. Gore’s ePE breakthrough illustrates how non-fluorinated resins can replace PTFE without losing performance, but scale-up remains capital-intensive. Brands locking long-term contracts for bio-based polyols secure margin insulation against petrochemical swings, as seen in Patagonia’s 2025 agreement with Covestro for CO₂-based PU.

By Textile: Membrane Supremacy Meets Coated-Fabric Growth

Membranes held a 64.83% share in 2025, powered by Gore-Tex’s 400-plus licensees and Sympatex’s recyclable polyester ether. Nevertheless, coated fabrics will be the fastest mover at a 5.95% CAGR through 2031. This surge is attributed to advancements in silicone-DWR chemistry, which not only enhances wash durability but also slashes costs compared to traditional laminated stacks. Meanwhile, heritage brands, with their emphasis on natural fibers and tactile comfort, are increasingly gravitating towards densely woven textiles like Ventile cotton.

Pertex Shield Air has introduced electrospun nanofibers that seamlessly merge the benefits of coated and laminated textiles. These nanofibers boast impressive hydrostatic-head ratings while maintaining a lightweight profile of under 100 g/m², all without adhering to Gore’s royalty model. Companies like Schoeller, quick to adopt PFAS-free materials, have secured a competitive edge, enjoying a lead in navigating regulatory challenges compared to rivals still in the reformulation validation phase. Mills adept at pivoting between membranes, coated fabrics, and densely woven textiles stand to not only broaden their revenue streams but also mitigate regulatory risks in the evolving landscape of waterproof breathable textiles.

By Application: Sportswear Maturity Versus Military-Workwear Upside

Sportswear and activewear owned a 71.21% share in 2025, but their volume growth decelerated as consumers opted to repair their gear instead of replacing it. To safeguard their profit margins, brands are now emphasizing sustainability, incorporating features like being PFAS-free, using recycled materials, and offering repair programs. Meanwhile, Protective and military garments are rising at a 5.87% CAGR. This surge is fueled by NATO tenders and stringent industrial safety regulations, which emphasize breathability for crews on oil rigs and in construction. The U.K. has set a precedent with the VIRTUS upgrade, a move now being mirrored by other European nations, bolstered by backing from the EU defense fund.

While general clothing and home textiles maintain a steady presence, their significance remains limited, often swayed by institutional procurement cycles. Innovations play a pivotal role in "Other Applications." For instance, when new breathable yet waterproof inserts are introduced, there's a noticeable uptick in demand for footwear linings and medical-device packaging. A prime example is trail-running shoes adopting Gore-Tex Invisible Fit, highlighting the footwear industry's shift towards lighter membranes. Suppliers who customize features—like arc-flash resistance or protection against chemical splashes—stand to secure lucrative contracts, extending their reach beyond conventional sportswear.

Geography Analysis

Europe retained 32.39% of 2025 revenue, buoyed by mature recreation habits and stringent chemical laws that pull PFAS-free innovation forward. German machinery makers, Monforts and Brückner, facilitated rapid chemistry pivots, granting EU mills a first-mover advantage. France's 2026 PFAS ban hastened brand timelines, allowing contenders like Sympatex to seize shelf space while slower rivals awaited clarity. Following Brexit, U.K. brands, despite a domestic output dip in 2025, pivoted to Canadian and Australian markets, relocating fabrication to Portugal and Turkey.

Asia-Pacific is expanding at a 5.55% CAGR, driven by investments in membrane-lamination from India, Vietnam, and Bangladesh to cater to both export and domestic demands. Toray's collaboration with MAS Holdings in Odisha underscores India's ambitions in technical fabrics, bolstered by the PLI scheme. While China commands a significant share of the global PTFE membrane capacity, it experienced a decline in waterproof-textile exports in 2025, as brands began diversifying their sourcing. Mills in Southeast Asia are gaining momentum by producing PFAS-free coated fabrics that meet EU import standards.

North America's textile and protective gear outlook is closely linked to the FY 2026 defense budget, which allocates a portion to these sectors, and the nation's outdoor-recreation economy. In 2025, Mexico drew in substantial textile investments, focusing on near-shore coating lines to meet a swift 5-day lead-time demand. While South America and the Middle East-Africa regions remain relatively small players, they occasionally surge; for instance, Brazil's procurement post-2024 floods and Saudi Vision 2030's contracts for breathable workwear highlight these climate- and construction-driven spikes. Coated fabrics are favored in these regions, attributed to their cost-effectiveness and ease of maintenance in warmer climates.

Regulatory Landscape

The regulatory environment for waterproof breathable textiles is tightening around PFAS and broader chemical transparency. Under the EU REACH framework (EC 1907/2006), substance registration and SVHC duties (including SCIP notifications above 0.1%) continue to shape formulation choices for membranes, coatings, and DWR finishes, while ECHA has advanced sector scrutiny of PFAS in textiles through its RAC and SEAC evaluations, including a RAC opinion adopted on 2 March 2026 for the TULAC sector.

Specific PFAS controls are also shifting from molecule-by-molecule management toward screening-based limits and product restrictions. The EU PFHxA restriction for consumer clothing and footwear (Regulation (EU) 2024/2462) enters into force on 10 October 2026, and Denmark has set a 50 mg/kg (50 ppm) Total Organic Fluorine limit effective 1 July 2026 for specified consumer textile and footwear applications. In parallel, the EU Ecodesign for Sustainable Products Regulation (ESPR, Regulation 2024/1781) entered into force on 18 July 2024, with textiles identified as a priority category in the first ESPR Working Plan adopted in April 2025, reinforcing traceability and product-information obligations that cascade through mills, laminators, and brands.

Value Chain Analysis

The value chain runs from upstream polymer and additive inputs (PTFE alternatives, TPU/PU systems, waterborne and solvent-free chemistries) to midstream textile formation (woven and knit substrates, membrane making and coating), then to downstream lamination, seam-sealing compatibility, garment manufacturing, and brand-led testing and certification. Performance and compliance requirements tend to concentrate influence with membrane developers and chemical suppliers, while lamination capacity and finishing know-how remain key chokepoints due to high capital intensity and narrow process windows for durable waterproofness and breathability.

Recent activity points to tighter coupling between material innovators and downstream brand programs. BASF has showcased TPU-based electrospun membrane concepts (Freeflex E 130) with Niber Technologies, and ANTA Group launched its AEROVENT ZERO PFAS-free membrane developed with Donghua University, signaling a shift toward brand-linked R&D and localized supply creation in Asia. In the sustainability and circularity layer of the chain, consortium models have also emerged for feedstock transitions, such as the July 2024 supply-chain collaboration led by Chiyoda and partners to produce sustainable polyester fibers using CO2-derived para-xylene for THE NORTH FACE in Japan, while major licensors and platform suppliers continue to steer adoption through updated laminate constructions and recycled face-textile options.

Competitive Landscape

The waterproof breathable textile market is moderately consolidated. White-space opportunity clusters around fluorine-free chemistry, bio-based feedstocks, and product take-back programs. Patent filings in electrospun membranes rose between 2023 and 2025, signaling intensified innovation aimed at undercutting Gore’s cost base. Coated segments risk commoditization; suppliers now invest in digital prints and tactile finishes to retain differentiation as silicone DWR becomes a standard feature.

Waterproof Breathable Textiles Industry Leaders

W. L. Gore & Associates Inc.

TORAY INDUSTRIES, INC.

Sympatex

schoeller Switzerland

FORMOSA TAFFETA CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace remains PFAS-free performance stacks that preserve high breathability while simplifying compliance documentation across export supply chains. Evidence in 2026 shows acceleration in non-fluorinated membrane and laminate offerings: Polartec introduced AirCore, a PFAS-free air-permeable nanofiber membrane laminate (stated MVTR exceeding 25,000 g/m2/24 h), and BASF highlighted electrospun TPU membrane approaches with Niber Technologies. Together, these launches broaden the menu of alternatives beyond legacy ePTFE architectures and create room for suppliers that can validate durability, seam-seal performance, and wash resistance at scale.

A second opportunity centers on circular and renewable feedstocks embedded into waterproof breathable constructions, with brands seeking lower-impact face textiles and polymer inputs alongside technical performance. In June 2026, W. L. Gore & Associates expanded its GORE-TEX Fabrics portfolio with laminates featuring 100% recycled textile-to-textile polyester faces, and Toray partnered with Goldwin, Neste, and Idemitsu Kosan on a renewable-nylon fiber supply chain targeted for integration into THE NORTH FACE products starting August 2026. These initiatives support traceable recycled or renewable inputs that align with emerging EU product-information requirements under ESPR, and they also enable shorter lead-time and smaller-batch manufacturing without giving up hydrostatic head and moisture management.

Recent Industry Developments

- June 2026: The company announced updates across the GORE-TEX Fabrics portfolio, including new WINDSTOPPER Stretch products, updates to GORE-TEX PACLITE, and laminates using 100% recycled textile-to-textile polyester face materials. The refresh expands PFAS-free and circular-material options that brands can specify while maintaining a premium performance positioning in membranes and laminates.

- September 2025: The company launched the next-generation GORE-TEX Pro fabric featuring an ePE membrane, eliminating intentional PFAS while targeting higher durability thresholds. The launch marked a technology shift among leading membrane platforms, accelerating downstream conversion work at mills and garment programs that depend on licensed laminate systems.

- July 2024: Chiyoda Corporation and partners (including Goldwin, Mitsubishi Corporation, Neste, SK geo centric, Indorama Ventures, and India Glycols) formed a consortium to build a global supply chain for sustainable polyester fiber using CO2-derived para-xylene for THE NORTH FACE brand in Japan. This move supports the upstream feedstock pathway for lower-impact face textiles used in technical laminates, reinforcing brand sustainability commitments that increasingly influence material selection.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the waterproof breathable textiles market covers fabric systems that block liquid water while still allowing moisture vapor to pass through, mainly used in performance apparel and protective wear.

Scope exclusions: We exclude downstream branded apparel retail value, general non-breathable waterproof fabrics, and non-textile rain protection products.

Segmentation Overview

- By Raw Material

- PTFE

- Polyester

- Polyurethane (PU)

- Other Raw Materials

- By Textile

- Densely Woven

- Membrane-based

- Coated

- By Application

- Sportswear and Activewear

- Protective and Military

- General Clothing and Home Textile

- Other Applications

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping demand context for end uses like outdoor apparel and protective clothing, then tracking how material and textile formats flow into those uses. We mainly rely on public sources such as USITC trade statistics, UN Comtrade, World Trade Organization trade indicators, and government textile or manufacturing releases to track import, export, and production direction.

To ground assumptions, we also review patent databases, peer-reviewed textile science journals, association publications for technical textiles, and public sustainability or performance standards that affect adoption. Company filings, investor presentations, and reputable press coverage are used to confirm capacity additions, shifts in product mix, and pricing direction. Where needed, we use paid subscription company financials and an import-export shipment-level database to validate supplier exposure and trade flows. These examples are not exhaustive, and other sources were also used to collect data, validate inputs, and clarify open questions.

Primary Interviews and Surveys

Primary work focuses on speaking with stakeholders across the value chain, including fabric producers, membrane and coating specialists, converters, and purchasing teams at apparel and protective clothing brands. For a global market like this, we cover APAC, EMEA, and the Americas so regional price movements, lead times, and adoption drivers can be compared, and then used to tighten assumptions where desk inputs look broad.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 19% | APAC: 38% |

| Mid tier: 42% | Functional/Unit leaders: 26% | EMEA: 37% |

| Smaller Players: 20% | Managers: 55% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where production and trade indicators for technical textile inputs are reconstructed, then filtered through the share that goes into waterproof breathable end uses across key regions. The totals are checked with selective bottom-up approximations, such as sampled price per square meter for membrane and coated formats multiplied by estimated shipment volumes, and a limited supplier roll-up for a sanity check.

Key inputs in this market include the mix shift between membrane-based, coated, and densely woven formats, changes in raw material usage (such as PTFE, polyester, and polyurethane), outdoor apparel demand cycles, and protective or military procurement activity. We also track average selling price movement linked to energy and polymer cost trends. When a variable is not consistently available by country, we handle gaps through proxy indicators such as regional trade intensity and expert-confirmed conversion ratios, and then keep the estimate conservative until it is validated.

For forecasting, scenario analysis is used so upside and downside cases can be expressed around adoption rates, price progression, and the pace of performance apparel growth. Final forecasts are aligned with what primary respondents consider realistic for capacity additions, pricing pass-through, and the timing of new fabric launches.

Data Validation & Update Cycle

Outputs are checked against independent signals such as trade values, material price direction, and visible capacity announcements, and then large variances are reviewed again before sign-off. If the model shows a jump that demand indicators do not support, we re-check the assumption, and follow up with a fresh expert touchpoint when needed.

Reports are refreshed on an annual cycle, and interim updates are made when a material event affects supply, demand, or pricing. Before delivery, the latest data points are re-screened so clients receive an up-to-date view rather than an older snapshot.

Mordor Intelligence's Waterproof Breathable Textiles Market Size Measured Against Other Published Estimates

Published market sizes for waterproof breathable textiles can differ even when the topic name looks the same, since the counted value can move based on what is treated as the textile layer versus the finished apparel outcome, and how pricing is normalized across regions. Differences also come from base year choice, currency conversion timing, and how much of the protective clothing stream is included versus left implicit.

The main gap comes from whether estimates fold in finished garment value and broader technical textiles, where Mordor Intelligence counts only waterproof breathable textile materials across raw materials, textile formats, and core applications. Pricing is kept tied to fabric-level average selling prices validated through interviews.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.41 B (2026) | |

| Global Research Publisher A | USD 2.03 B (2024) | Uses a different base year and may apply broader application coverage and pricing normalization across more countries, which can shift the implied average fabric price and total value. |

| Industry Research Outlet B | USD 2.98 B (2024) | Long-horizon forecasts often lean on higher adoption and wider technology buckets, and the 2024 value can be lifted if apparel-linked revenue and aggressive ASP progression are assumed early. |

Across the table, the spread is mainly explained by what is counted at the textile level, how ASPs are moved forward over time, and how base year and currency timing are treated. When scope is kept at fabric and membrane systems with clear end-use links, the market total stays more traceable to observable trade, pricing, and demand signals.

Key Questions Answered in the Report

How large is the waterproof breathable textiles market in 2026?

The waterproof breathable textiles market size stands at USD 2.41 billion in 2026.

What is the expected CAGR for waterproof breathable textiles through 2031?

The market is projected to grow at a 5.13% CAGR between 2026 and 2031, reaching USD 3.10 billion by 2031.

Which raw material leads current demand?

Polyurethane dominates with a 44.92% share, rising on bio-based and solvent-free momentum.

Which textile construction is growing fastest?

Coated fabrics are forecast to expand at a 5.95% CAGR as silicone DWR replaces fluorocarbons.

Which region shows the highest growth potential?

Asia-Pacific is set to grow fastest at a 5.55% CAGR thanks to investments in India, Vietnam, and Bangladesh.

How are PFAS regulations affecting suppliers?

EU and U.S. bans are accelerating shifts to ePE membranes and silicone-based DWR, raising costs but opening market share for early adopters.

Page last updated on: