DNA/RNA Extraction Kit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

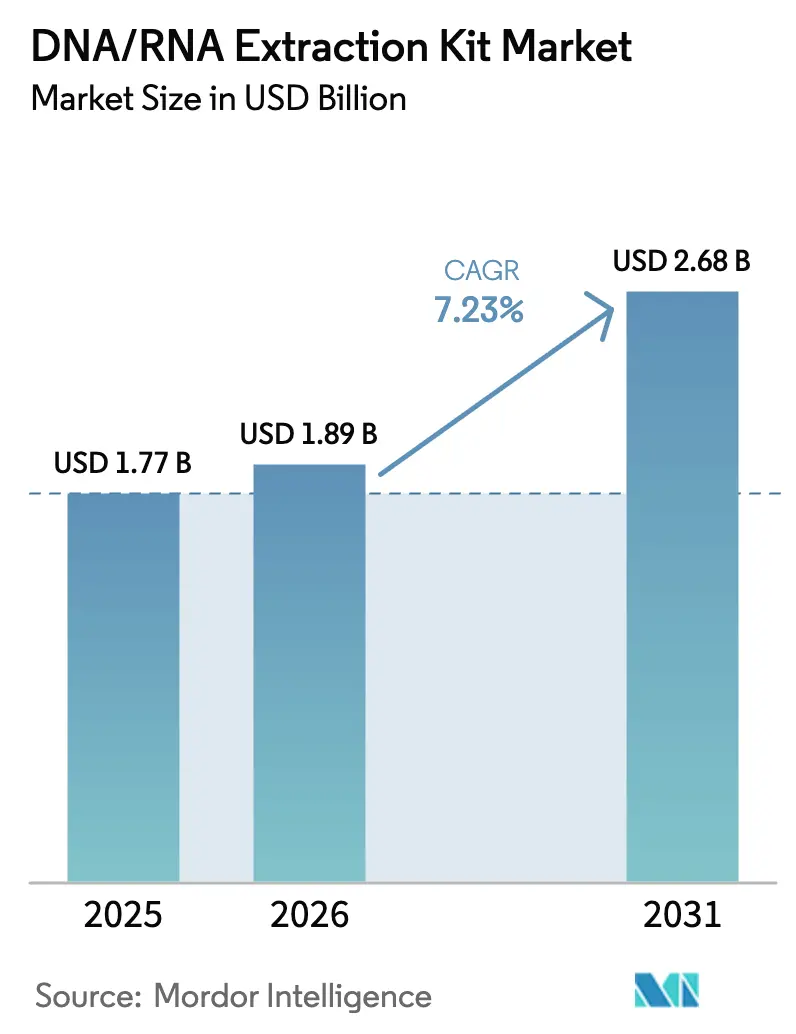

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DNA/RNA Extraction Kit Market Analysis by Mordor Intelligence

The DNA/RNA Extraction Kit Market size is expected to grow from USD 1.77 billion in 2025 to USD 1.89 billion in 2026 and is forecast to reach USD 2.68 billion by 2031 at 7.23% CAGR over 2026-2031.

This growth is driven by oncology's transition to liquid biopsies, the expansion of wastewater pathogen surveillance programs, and the increasing demand for precision medicine, which requires consistent and reliable nucleic acid purification. The adoption of magnetic-bead automation is accelerating, reducing technician time and minimizing error rates, prompting clinical laboratories to replace outdated reagent protocols. Public health authorities are institutionalizing viral RNA monitoring in wastewater, thereby expanding the application of RNA kits beyond traditional hospital use. Additionally, pharmaceutical companies are embedding validated extraction methods into drug and diagnostic submissions to streamline regulatory approvals, fostering strong vendor relationships and increasing switching costs. The competitive landscape is shaped by established players defending manual spin-column volumes, while emerging competitors promote cartridge systems that integrate extraction, library preparation, and analysis into a single consumable.

Key Report Takeaways

- By sample type, blood and plasma held 42.45% of the DNA/RNA extraction kit market share in 2025. Wastewater and environmental matrices are projected to advance at a leading 9.65% CAGR through 2031.

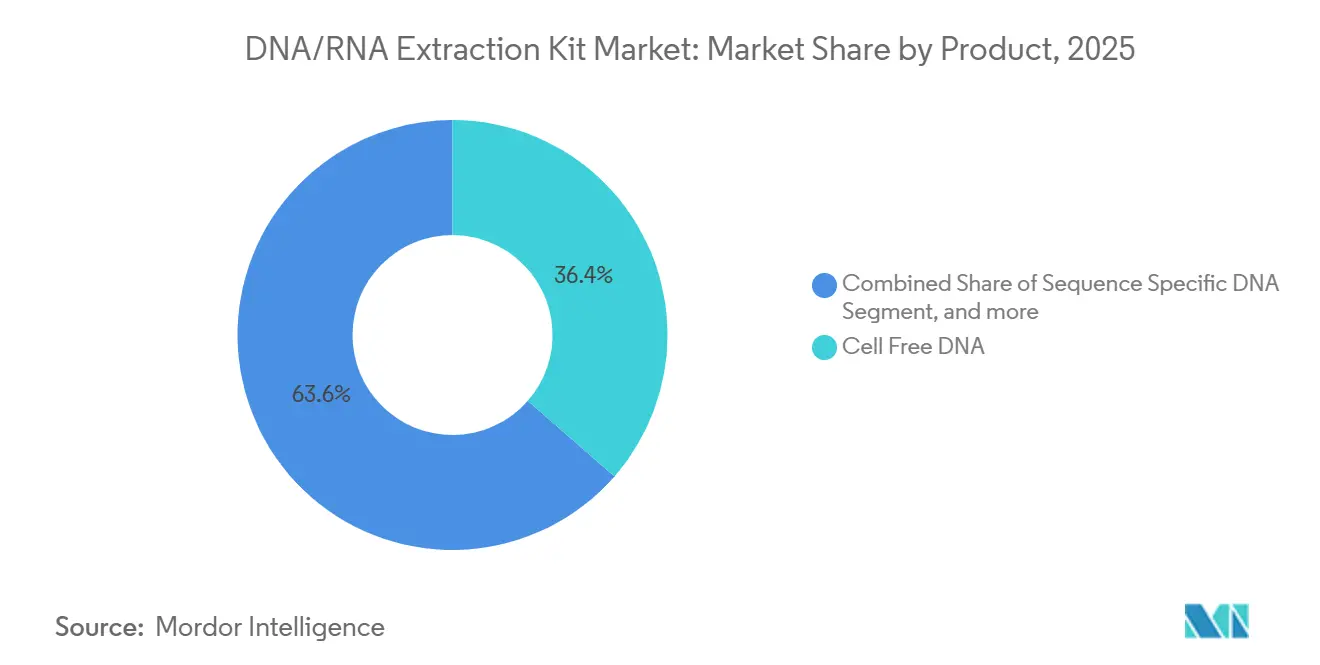

- By product, cell-free DNA kits captured 36.43% of the DNA/RNA extraction kit market size in 2025. Total RNA solutions are projected to post the fastest 9.54% CAGR between 2026 and 2031.

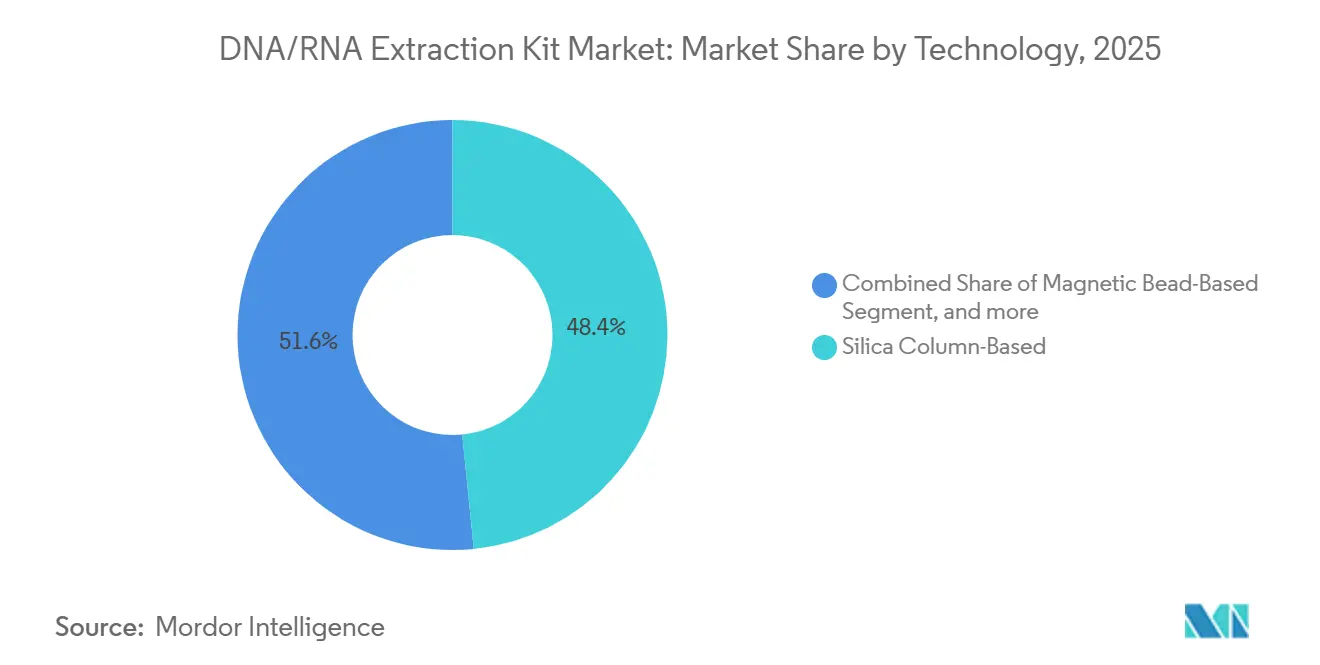

- By technology, silica columns commanded 48.43% revenue in 2025, while automated cartridges recorded a 10.01% CAGR to 2031.

- By end user, diagnostic centers contributed 41.46% revenue in 2025, whereas biotechnology and pharmaceutical firms expanded at a 10.34% CAGR through 2031.

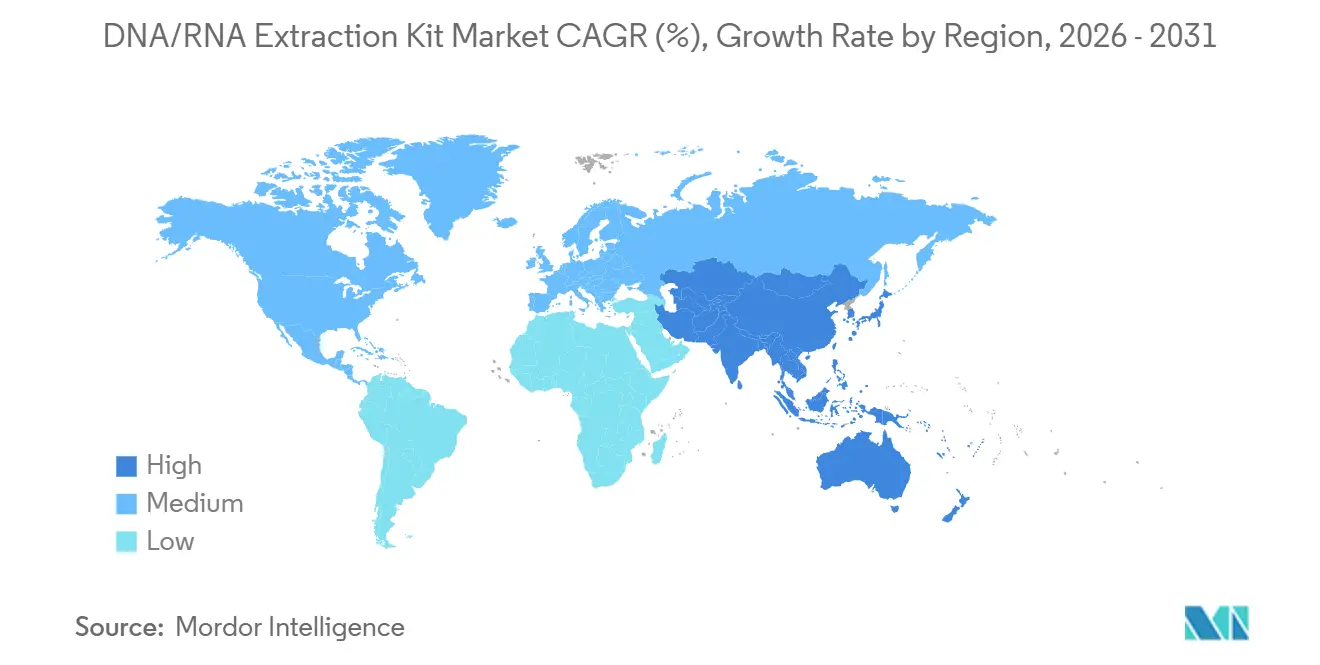

- By region, North America accounted for 42.67% revenue in 2025; Asia-Pacific is projected to grow at 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global DNA/RNA Extraction Kit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Liquid Biopsy in Oncology Diagnostics | +2.1% | North America, Europe, Global centers | Medium term (2-4 years) |

| Technological Advancements in Automated High-Throughput Extraction Platforms | +1.8% | North America, Europe, APAC (China, Japan) | Short term (≤2 years) |

| Growing Investments in Molecular Diagnostic R&D | +1.3% | United States, China, Germany, Japan | Long term (≥4 years) |

| Expansion of Precision Medicine Programs and Companion Diagnostics | +1.5% | North America, Europe, Selected APAC countries | Long term (≥4 years) |

| Increasing Use of Residential Point-of-Care Genomic Testing Kits | +0.8% | United States, United Kingdom, South Korea | Medium term (2-4 years) |

| Wastewater Epidemiology Demand for Viral RNA Surveillance | +1.2% | North America, Europe, Selected APAC cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Liquid Biopsy in Oncology Diagnostics

Guardant360 CDx received FDA approval in 2024, requiring labs to validate extraction methods that preserve plasma DNA fragments under 200 base pairs. Reference centers report a 40% year-over-year growth in liquid biopsy sample volumes, necessitating upgrades to 96-well magnetic platforms that reduce handling steps. Roche’s cfDNA kit on the cobas system captures 85% of circulating tumor DNA from 2 mL of plasma, enabling the detection of minimal residual disease at an allele frequency of 0.01%. Prenatal testing also benefits, as cell-free fetal DNA replaces invasive procedures in high-income markets. Net effect raises throughput and purity requirements that manual spin columns struggle to meet.

Technological Advancements in Automated High-Throughput Extraction Platforms

Thermo Fisher’s KingFisher Apex processes 96 samples in 30 minutes with full LIMS integration, improving traceability for ISO 15189 labs. Beckman Coulter liquid handlers pair with magnetic processors to run blood, saliva, and tissue samples simultaneously, reducing the risk of cross-contamination. Tecan’s Fluent workstation combines extraction, quantification, and normalization, cutting labor costs by 60% while holding a coefficient of variation below 5%. Leasing contracts and shared-service models ease capital barriers, widening access in mid-tier hospitals. Automation thus accelerates kit conversion from low-margin manual protocols to premium cartridges.

Expansion of Precision Medicine Programs and Companion Diagnostics

FoundationOne CDx, cleared in 2024 for 324 genes, stipulates extraction yields above 10 ng/µL from FFPE tissue, disqualifying phenol-chloroform workflows. Pharmaceutical sponsors now specify extraction reagents in Phase III biomarker studies, locking vendors into drug-diagnostic packages. QIAGEN’s therascreen EGFR test bundles its extraction kit and PCR chemistry, harmonizing results across global labs. Centralized reference networks in the United Kingdom route purified DNA to regional hospitals, demanding room-temperature stability for multi-day shipping. Tight linkage between extraction fidelity and therapeutic eligibility secures recurring kit revenue per patient.

Wastewater Epidemiology Demand for Viral RNA Surveillance

The CDC monitors over 1,200 treatment plants, driving bulk procurement of RNA kits that remove inhibitors like humic acids[1]Centers for Disease Control and Prevention, “National Wastewater Surveillance System 2025,” cdc.gov. QIAGEN’s wastewater-adapted viral RNA kit increases recovery to 70% compared to 40% for generic options. WHO guidance endorses wastewater surveillance for polio, prompting UNICEF deployments in Africa and South Asia. The private sector joins in, from agricultural firms testing soil microbiomes to environmental consultants tracking the DNA of invasive species. Non-clinical buyers often opt for cost-efficient reagent kits, thereby diversifying their channel mix and pricing tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Reagent Costs of Automated Extraction Systems | −0.9% | Global, acute in low- and middle-income countries | Short term (≤2 years) |

| Limited Skilled Workforce in Low-Resource Settings | −0.7% | Africa, South Asia, Latin America | Long term (≥4 years) |

| Regulatory Scrutiny over Microplastic Waste from Single-Use Plastics in Kits | −0.5% | European Union, Canada, Australia | Medium term (2-4 years) |

| Supply Chain Vulnerabilities for Silica and Magnetic Bead Raw Materials | −0.6% | North America, Europe reliant on Asian supply | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Reagent Costs of Automated Extraction Systems

Automated instruments cost USD 150,000–300,000, with cartridges priced at USD 200 per sample for systems like Genexus Dx, which limits viability to labs processing more than 1,000 samples per month. Manual spin columns run USD 2–5 per sample but require skilled technicians and record higher failure rates. Pay-per-use models shift capital risk to vendors but raise per-test pricing by 15%. Medicare pays USD 18 for a PCR assay, compressing margins and nudging labs toward the lowest cost extraction consumables. The resulting affordability gap stalls automation uptake in community hospitals and emerging markets.

Supply Chain Vulnerabilities for Silica and Magnetic Bead Raw Materials

Silica membranes and magnetic beads primarily originate from China and Japan. The semiconductor prioritization in 2024 delayed bead deliveries by up to 12 weeks, resulting in kit rationing. QIAGEN faced a 12% increase in raw-material costs amid tariffs and passed some of these costs on to customers. Thermo Fisher vertically integrated by buying a membrane supplier in 2024 to stabilize inputs. Meanwhile, the EU Single-Use Plastics Directive pushes vendors to switch columns to recyclable polypropylene, extending development cycles by up to 9 months[2]European Commission, “Single-Use Plastics Directive 2025,” eur-lex.europa.eu. These supply pressures threaten lead times and pricing discipline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cell-Free DNA Remains the Revenue Anchor, Total RNA Gains Momentum

Cell-free DNA kits accounted for 36.43% of product revenue in 2025, reflecting their widespread adoption for liquid biopsy and prenatal testing. Total RNA kits are growing at a 9.54% CAGR as single-cell transcriptomics and spatial assays surge, requiring integrity numbers above 8.0 for downstream library preparation[3]Nature Publishing Group, “Spatial Transcriptomics Market Uptake 2025,” nature.com. Sequence-specific DNA kits remain in legacy PCR workflows, yet they are gradually ceding share to broad-capture formats aligned with next-generation sequencing. Viral RNA and microbial DNA kits remain stable after the pandemic spike, yet they continue to support wastewater and microbiome niches. Roche’s MagNA Pure 96, QIAGEN’s RNeasy Plus, and Zymo’s Quick-DNA/RNA Miniprep illustrate how vendors differentiate via automation, purity, or co-isolation advantages.

The DNA/RNA extraction kit market size for cell-free DNA kits is projected to rise at 6.4% CAGR through 2031, while total RNA solutions advance at 9.54% and are on track to close the revenue gap by 2029. Labs now standardize on dual-protocol devices to future-proof capacity against shifting assay demand, uplifting average selling prices and service revenue.

By Sample Type: Blood Dominates Today, Wastewater Fastest Tomorrow

Blood and plasma generated 42.45% of the revenue in 2025, as clinicians rely on venipuncture for molecular diagnostics. Wastewater samples expand at 9.65% CAGR on the back of institutionalized epidemiological programs, elevating demand for high-volume RNA kits that handle PCR inhibitors. Tissue extraction remains critical for oncology pathology, while saliva and buccal swabs power consumer genomics and remote testing models. Stool, CSF, and niche matrices add fragmented incremental growth.

The DNA/RNA extraction kit market share for blood workflows is expected to decline to 37% by 2031 as wastewater and environmental use rise, balancing the sample mix. Vendors that optimize binding chemistries for turbid matrices stand to capture outsized gains in the expanding surveillance sector.

By Technology: Columns Still Lead, Cartridge Automation Surges

Silica spin columns retained a 48.43% revenue share in 2025, thanks to their low per-sample cost and broad familiarity. Cartridge and lab-on-chip platforms are projected to exhibit a 10.01% CAGR from 2026 to 2031, driven by walk-away convenience and integrated analytics. Magnetic beads underpin most high-throughput systems, while reagent-based phenol-chloroform protocols persist in grant-funded academic labs that trade safety for budget relief.

The DNA/RNA extraction kit market size for automated cartridge formats is forecast to reach USD 1.1 billion by 2031, up from USD 530 million in 2026, narrowing the gap with the column-based market. Hybrids like QIAcube Connect bridge the transition by automating traditional columns, easing buyers into higher price points without forklift replacements.

By End User: Diagnostic Laboratories Hold Lead, Pharma Drives Incremental Gains

Diagnostic centers and clinical labs generated 41.46% of revenue in 2025 from routine PCR, oncology panels, and inherited-disease testing. Biotechnology and pharmaceutical firms are logging the fastest 10.34% CAGR as they integrate extraction into biomarker discovery pipelines and companion diagnostics. Hospitals strive for timely results and adopt cartridge systems that interface seamlessly with point-of-care analyzers. Academic institutes favor versatile manual kits under constrained budgets.

The DNA/RNA extraction kit market size for pharmaceutical and biotech buyers is expected to double between 2026 and 2031, driven by regulatory guidance that links extraction quality to therapeutic labeling. Vendors that bundle consumables with regulatory support command premium pricing and longer contract tenures.

Geography Analysis

North America accounted for 42.67% of the revenue in 2025, driven by high liquid biopsy volumes, well-funded precision medicine initiatives, and reimbursement that supports companion diagnostics. Europe maintains steady demand but contends with tighter budgets that shift preferences toward cost-efficient columns, despite stricter IVDR rules. Asia-Pacific is set to grow at 8.54% CAGR, propelled by the Chinese government's genomics subsidies and India’s contract-research expansion. The Middle East and Africa remain nascent, but they benefit from donor-funded infectious disease programs. South America sees moderate gains via dengue and Zika molecular surveillance.

China earmarked USD 1.2 billion in 2024 to equip provincial hospitals with automated extraction systems, cementing supplier footholds. India’s CRO industry increased its molecular testing capacity by 35% year-over-year, favoring magnetic-bead robotics that meet Good Laboratory Practice requirements. Europe’s IVDR raises compliance hurdles and nudges smaller suppliers toward mergers or exits. North American vendors pursue vertical integration to insulate raw-material supply and protect margins in a mature region. Collectively, geographic expansion rebalances growth toward emerging Asia while reinforcing regulatory-driven stickiness in developed economies.

Competitive Landscape

Thermo Fisher Scientific, QIAGEN, and Roche collectively capture approximately 55% of the revenue, indicating a moderately concentrated market. Thermo Fisher’s vertical supply control and FDA-cleared Genexus Dx system strengthen its moat. QIAGEN leverages co-development with pharmaceutical partners to integrate its kits into regulatory filings, thereby increasing exit costs for laboratories. Roche integrates extraction with mutation assays on MagNA Pure and cobas lines to offer end-to-end oncology solutions.

Niche players carve share in specialized workflows. Zymo Research’s FFPE RNA kits deliver 30% higher yield for archived tissue studies. Promega removes xylene from tissue extraction, lowering fume-hood requirements and winning pathology accounts. Bio-Rad miniaturizes extraction into droplet-based chips to cut reagent spend in low-throughput labs. Strategic moves include Takara Bio’s USD 50 million expansion of bead manufacturing in Japan, aimed at shortening Asian lead times.

Regulatory dynamics heighten competitive barriers. FDA and IVDR approvals require validated extraction protocols, favoring incumbents with large quality teams. ISO 13485 certification supports CE marking in Europe, as achieved by Zymo Research in 2024, enabling research suppliers to enter clinical channels. The resulting structure sustains premium pricing and limits rapid commoditization.

DNA/RNA Extraction Kit Industry Leaders

Promega Corporation

F Hoffmann-La Roche AG

Qiagen N.V.

Agilent Technologies

Bio-Rad Laboratories Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Primerdesign, part of the Novacyt Group launched its exsig Mag RapidBead Pro Extraction kit. This next-generation magnetic bead-based kit allows efficient extraction of high-quality DNA and RNA from various samples. The streamlined protocol helps researchers quickly prepare samples for PCR testing without sacrificing yield or purity.

- September 2025: Xpedite Diagnostics GmbH announced the CE-IVD certification and launch of SwiftX™ Virus, a novel one-step DNA/RNA extraction kit. The kit is designed for rapid nucleic acid extraction from human serum and plasma. This breakthrough technology aims to streamline diagnostic processes and improve testing efficiency.

- April 2024: New England Biolabs (NEB) launched its Monarch Mag Viral DNA/RNA Extraction Kit. The kit is designed to improve recovery of low amounts of viral nucleic acids, enabling highly sensitive detection. It utilizes magnetic bead-based technology, which is suitable for various sample types, including saliva, respiratory swabs, and wastewater.

Global DNA/RNA Extraction Kit Market Report Scope

As per scope of the report, the DNA/RNA extraction kits are used for isolating the DNA or RNA from any cell, which can be from any animal, microbe, or plant. The primary use of these extractions is for DNA or RNA profiling of various organisms to gain a better understanding and, in some cases, to identify unknown organisms.

The DNA/RNA Extraction Kit Market is Segmented by Product (Cell Free DNA, Sequence Specific DNA, Sequence Specific RNA, Total RNA, Other Products), Sample Type (Blood & Plasma, Tissue & FFPE, Saliva & Buccal Swab, Wastewater & Environmental Samples, Other Samples), Technology (Silica Column-Based, Magnetic Bead-Based, Anion-Exchange Resin, Reagent-Based, Automated Cartridge & Lab-On-Chip), End User (Diagnostic Centers & Clinical Labs, Hospitals, Research & Academic Institutes, Biotechnology & Pharmaceutical Companies, CROs & Others), and Geography (North America, Europe, Asia-Pacific, Middle East And Africa, South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Cell Free DNA |

| Sequence Specific DNA |

| Sequence Specific RNA |

| Total RNA |

| Other Products |

| Blood & Plasma |

| Tissue & FFPE |

| Saliva & Buccal Swab |

| Wastewater & Environmental Samples |

| Other Samples |

| Silica Column-Based |

| Magnetic Bead-Based |

| Anion-Exchange Resin |

| Reagent-Based (Phenol-Chloroform, Trizol, Etc.) |

| Automated Cartridge & Lab-On-Chip |

| Diagnostic Centers & Clinical Labs |

| Hospitals |

| Research & Academic Institutes |

| Biotechnology & Pharmaceutical Companies |

| CROs & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product | Cell Free DNA | |

| Sequence Specific DNA | ||

| Sequence Specific RNA | ||

| Total RNA | ||

| Other Products | ||

| By Sample Type | Blood & Plasma | |

| Tissue & FFPE | ||

| Saliva & Buccal Swab | ||

| Wastewater & Environmental Samples | ||

| Other Samples | ||

| By Technology | Silica Column-Based | |

| Magnetic Bead-Based | ||

| Anion-Exchange Resin | ||

| Reagent-Based (Phenol-Chloroform, Trizol, Etc.) | ||

| Automated Cartridge & Lab-On-Chip | ||

| By End User | Diagnostic Centers & Clinical Labs | |

| Hospitals | ||

| Research & Academic Institutes | ||

| Biotechnology & Pharmaceutical Companies | ||

| CROs & Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the DNA/RNA extraction kit market in 2026?

The market is valued at USD 1.89 billion in 2026 and is projected to grow to USD 2.68 billion by 2031.

What is driving the fastest segment growth?

Wastewater and environmental sample kits lead with a 9.65% CAGR as agencies formalize pathogen surveillance programs.

Which technology segment is expanding quickest?

Automated cartridge and lab-on-chip platforms record a 10.01% CAGR because laboratories want walk-away workflows and reduced errors.

Which region offers the highest future growth?

Asia-Pacific shows the strongest outlook at an 8.54% CAGR thanks to government genomics funding and CRO expansion.

Who are the leading companies in this space?

Thermo Fisher Scientific, QIAGEN, and Roche jointly hold around 55% of global revenue through broad product portfolios and regulatory clearances.

What is the biggest adoption barrier for automation?

Capital cost of USD 150,000-300,000 per instrument plus premium cartridge pricing limits uptake in low-volume or resource-limited labs.

Page last updated on: