North America Outdoor Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

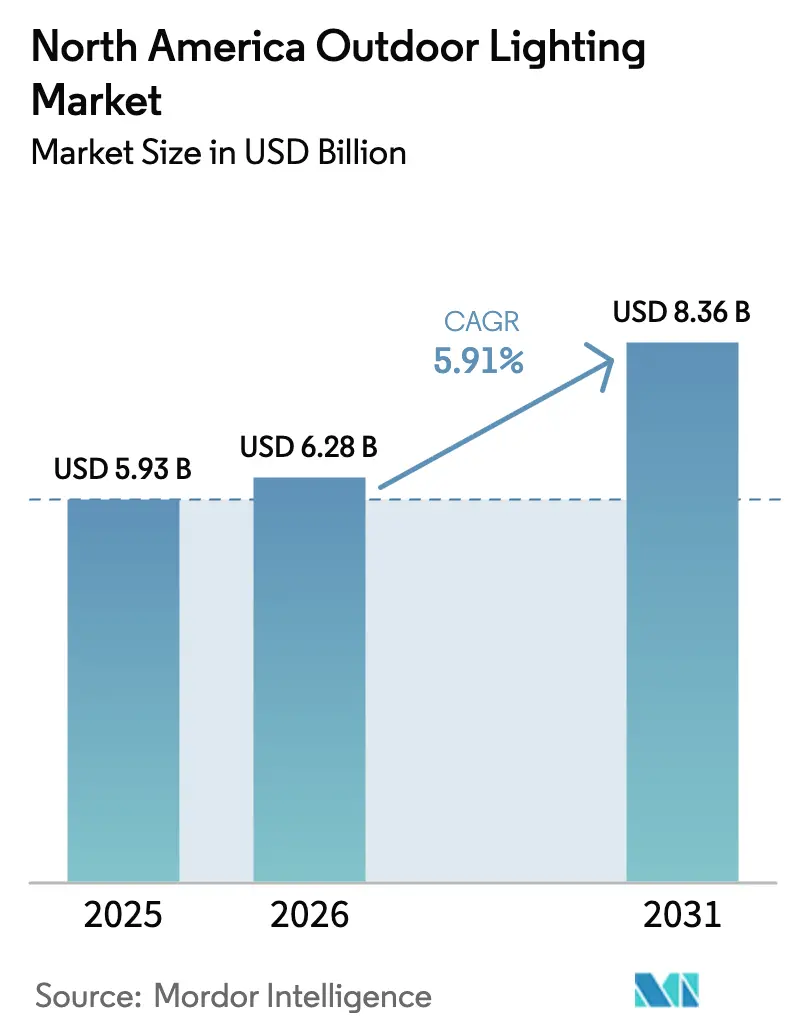

| Base Year Market Size (2025) | USD 5.93 Billion |

| Market Size (2026) | USD 6.28 Billion |

| Market Size (2031) | USD 8.36 Billion |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Outdoor Lighting Market Analysis by Mordor Intelligence

The North America outdoor lighting market size is expected to grow from USD 5.93 billion in 2025 to USD 6.28 billion in 2026 and is forecast to reach USD 8.36 billion by 2031 at 5.91% CAGR over 2026-2031. This solid expansion rests on municipal streetlight retrofits, rising federal energy-efficiency incentives, and the roll-out of smart-city programs that embed connected luminaires into broader IoT networks. As high-pressure sodium fixtures give way to LED and connected-ready systems, cities capture double-digit energy savings, while commercial property owners adopt landscape and security lighting to elevate brand experiences and site safety. Competitive intensity sharpens as incumbents add AI-driven controls and cybersecurity features, yet supply-chain swings in LED driver integrated circuits and community concerns about light pollution temper near-term momentum. Opportunities remain significant in solar-powered solutions for resilience projects, connected lighting in electric-vehicle charging hubs, and dark-sky-compliant fixtures demanded by suburban communities.

Key Report Takeaways

- By application, the residential outdoor segment held 35.12% revenue share in 2025, while commercial outdoor lighting is projected to expand at a 7.32% CAGR to 2031.

- By lighting type, LEDs commanded 79.45% of the North America outdoor lighting market share in 2025, whereas connected-ready LEDs are forecast to rise at an 7.62% CAGR through 2031.

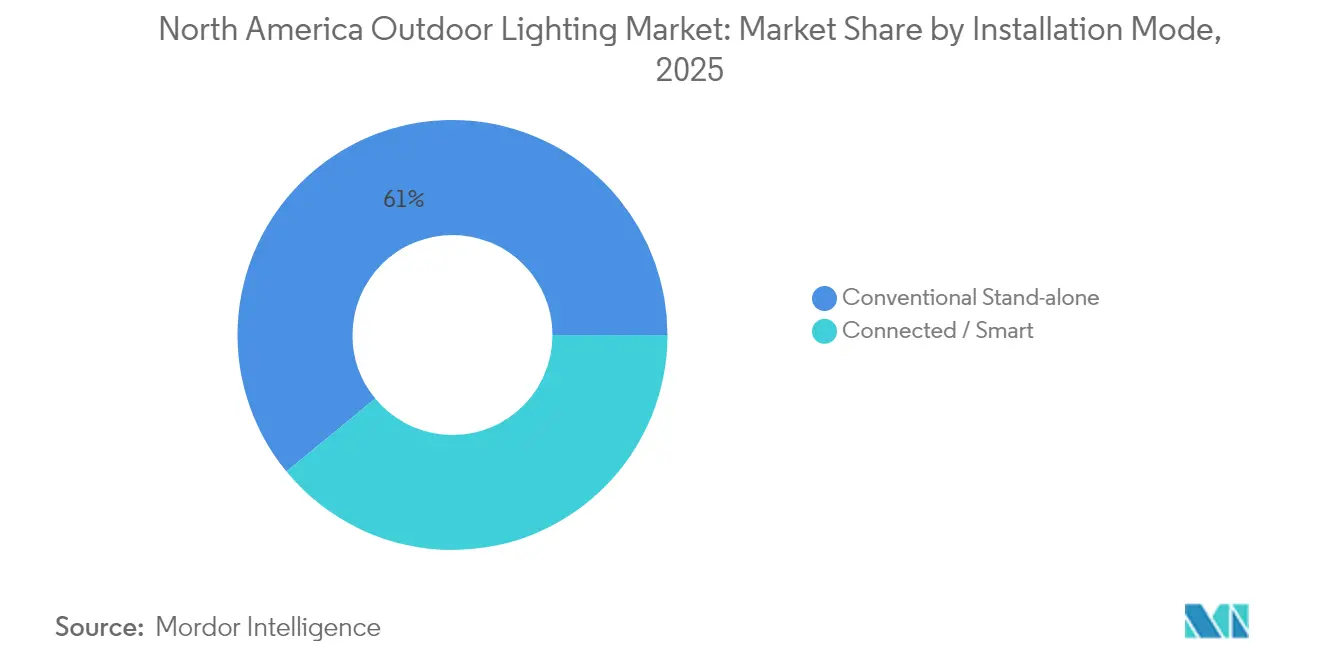

- By installation mode, conventional stand-alone systems accounted for 60.95% of the North America outdoor lighting market size in 2025; however, connected and smart installations are advancing at a 7.54% CAGR through 2031.

- By geography, the United States captured 45.35% of the regional value in 2025 and is expected to register the highest CAGR of 7.78% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Outdoor Lighting Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Energy-efficient retrofits in municipal streetlighting | +1.8% | United States, Canada, Mexico | Medium term (2-4 years) |

| Federal and state rebates accelerating LED adoption | +1.2% | United States primarily, limited Canada | Short term (≤ 2 years) |

| Smart-city mandates and IIoT integration of luminaires | +1.5% | Major metropolitan areas across North America | Long term (≥ 4 years) |

| Surge in outdoor e-mobility charging-infrastructure lighting | +0.9% | Urban centers in the United States and Canada | Medium term (2-4 years) |

| Micro-grid and resilience projects in climate-vulnerable zones | +0.6% | Coastal regions, wildfire-prone areas | Long term (≥ 4 years) |

| AI-enabled adaptive dimming for dark-sky compliance | +0.4% | North America, focus on rural and suburban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-efficient retrofits in municipal streetlighting

Large-scale LED conversions deliver 50-70% energy savings and swift paybacks for cities across the region. The City of Placentia saves USD 158,120 each year from a 3,400-fixture project and expects USD 3.1 million in lifetime benefits.[1]Source: City of Placentia, “City Streetlight LED Conversion Project,” placentia.org Edmonton completed 46,000 LED retrofits that cut greenhouse-gas emissions by 5,500 tonnes and reduced annual operating costs by USD 1.2 million. The American Council for an Energy-Efficient Economy estimates that nationwide conversion of U.S. streetlights could save 20,200 GWh annually and reduce municipal spending by USD 1 billion.[2]Source: American Council for an Energy-Efficient Economy, “Reducing Energy Use in Public Outdoor Lighting,” aceee.orgEnergy-service contracts and volume-purchase alliances shorten payback windows for smaller jurisdictions, while advanced dimming pilots in Colorado Springs reveal incremental energy reductions of 1–51% through adaptive scheduling. These robust outcomes reinforce LED retrofits as the market’s strongest growth engine through mid-decade.

Federal and state rebates accelerating LED adoption

Utility and state rebate programs offset upfront capital, enabling municipalities to deploy LED projects within constrained budget cycles. Roughly 77% of U.S. zip codes qualify for some form of lighting rebate, which lowers effective project costs and compresses payback periods to below five years in many cases.[3]Source: Signify, “Lighting Utility Rebates,” signify.com Maryland directed USD 1 million in FY 2024 grants to its Streetlight and Outdoor Lighting Efficiency initiative, while New York and Massachusetts offer tiered incentives for Clean-Energy-Community participants. National Grid finances conversions through on-bill repayment mechanisms that align debt service with realized energy savings. Oregon updated its incentive schedules in 2025, underscoring the state's continued policy support. These financial levers expedite procurement decisions, particularly in small and mid-sized cities that struggle with capital budget constraints.

Smart-city mandates and IIoT integration of luminaires

Connected luminaires form the digital backbone of emerging smart-city ecosystems. Washington, D.C. has contracted 75,000 smart streetlamps equipped with remote management and environmental sensing functions.[4]Source: inteliLIGHT, “InteliLIGHT Selected to Power Up 75k Smart Streetlamps in Washington, D.C.,” intelilight.eu Itron manages over 4 million smart fixtures worldwide, achieving 50% energy savings and 20% lower operational costs for its municipal clients. Los Angeles utilizes multi-functional poles that host Wi-Fi gateways, public safety beacons, and weather stations, transforming its lighting infrastructure into a revenue-generating urban platform. Spokane is piloting AI algorithms that predict dimming schedules based on traffic density to optimize luminaire performance. These deployments validate connected lighting as a resilient, data-rich asset class that municipalities can monetize over the long life of their assets.

Surge in outdoor e-mobility charging-infrastructure lighting

Rapid roll-outs of EV chargers generate demand for purpose-built luminaires that meet accessibility and safety criteria. The U.S. Access Board specifies illumination requirements for charging stations to ensure that all users have safe and navigable access to these spaces.[5]Source: U.S. Access Board, “EV Charging Stations Guidance,” access-board.gov NECA 413 prescribes installation practices that integrate lighting with Level 1, Level 2, and DC fast-charging equipment for consistent performance. SAE J1772 electrical and safety standards guide luminaire specification for charger canopies positioned in retail parking lots and highway corridors. As federal infrastructure funding accelerates charger deployment, lighting suppliers are enjoying a new channel whose growth parallels the broader electrification of transportation.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront CAPEX versus budget cycles | -1.4% | North America, particularly smaller municipalities | Short term (≤ 2 years) |

| Persistent supply-chain volatility in driver ICs | -0.8% | North America, dependent on Asian semiconductor supply | Medium term (2-4 years) |

| Community opposition on light-pollution grounds | -0.6% | Rural and suburban North America | Medium term (2-4 years) |

| Cyber-security risks in connected street-lights | -0.3% | Urban areas with smart-city deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX versus budget cycles

Despite favorable total-cost-of-ownership metrics, LED streetlight projects can stall when annual municipal budgets are unable to absorb large capital outlays. The U.S. Department of Energy identifies financing gaps as the top hurdle to comprehensive conversions, especially in towns with populations under 25,000. Performance contracts and vendor-backed leases align payments with energy savings, yet council approvals often prolong deal closures. Public-power utilities offer low-interest loans, though fiscal-year timing may still delay project mobilization. Volume-purchase alliances reduce fixture prices by as much as 15%, but procurement rules vary by state, adding complexity to already stretched administrative staff. These headwinds slow short-term uptake even when life-cycle economics remain compelling.

Persistent supply-chain volatility in driver ICs

The post-pandemic semiconductor landscape presents ongoing challenges for luminaire manufacturers that source driver chips from Asia. Lead times doubled in early 2025, forcing suppliers to carry elevated inventories that tie up working capital. Dialight’s USD 7.8 million judgment in a 2024 supply-agreement dispute underscores the financial risks of component shortages. Some vendors respond by dual-sourcing and redesigning drivers to accept alternative chipsets, yet qualification cycles can stretch beyond customer bid deadlines. Delays ripple through municipal retrofit schedules and create spot shortages that inflate fixture prices. Although the broader semiconductor market is normalizing, driver IC volatility remains a medium-term drag on deployment velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Application: Commercial growth outpaces entrenched residential demand

The residential segment led the North America outdoor lighting market with 35.12% revenue share in 2025 as homeowners invested in motion-sensing security lights, landscape accents, and architectural uplighting. Commercial venues, however, are scaling fastest and are projected to register a 7.32% CAGR through 2031, as retailers, hotels, and mixed-use developers utilize dynamic façade lighting to enhance brand appeal and customer safety. Retail chains are installing connected luminaires in parking lots to integrate surveillance cameras and license-plate readers, while hospitality operators are upgrading pool-deck and pathway fixtures to meet evolving guest-experience standards. Industrial facilities embrace high-output LEDs that resist vibration and extreme temperatures, reducing maintenance downtime in continuous-operation environments. Stadiums and large arenas are adopting tunable-white floodlights that meet broadcasting requirements and enable color-themed spectacles for concerts and special events.

Demand diversification underpins the North America outdoor lighting market, encouraging suppliers to tailor photometric distributions and control protocols for specific verticals. Landscape designers favor low-voltage LED bollards to accent native flora, whereas logistics campuses require high-mast poles with glare shields to comply with local ordinances. As commercial property owners pursue sustainability certifications, networked controls that provide energy dashboards become procurement differentiators. The interoperable D4i standard enables asset managers to mix and match drivers and nodes across multi-site portfolios, thereby simplifying spare parts logistics. By 2030, commercial adoption of adaptive dimming and occupancy sensing is expected to set new benchmarks that spill over into the still-dominant residential category.

By Type of Lighting: Connected LEDs redefine value proposition

LED fixtures captured 79.45% of the North America outdoor lighting market in 2025, reflecting the near-complete displacement of high-pressure sodium and metal-halide incumbents. Connected-ready LEDs represent the fastest-growing slice with an 7.62% CAGR, fueled by municipal mandates for asset-level data and predictive maintenance. Current projects demonstrate connected systems reducing truck rolls by more than 30% through remote fault detection, thereby shrinking operating budgets for public works departments. In the commercial realm, mall owners adopt Bluetooth-mesh luminaires that double as wayfinding beacons, while campuses layer Wi-Fi and environmental sensors onto existing poles to expand digital services without trenching new conduit.

The integration of AI-driven adaptive dimming can achieve energy savings of up to 80% compared to legacy systems, highlighting the widening performance gap between smart and static fixtures. Interoperability remains a top concern, and the D4i certification process gains momentum as cities insist on future-proof deployments. Vendors are rushing to integrate edge-based cybersecurity features to meet procurement clauses that reference ioXt Alliance standards.

By Installation Mode: Smart systems gain speed against conventional incumbents

Conventional stand-alone installations still account for 60.95% of the North America outdoor lighting market size, reflecting the immense installed base of fixtures that operate via photocells and fixed schedules. Yet connected and smart installations are increasing at a 7.54% CAGR, aided by the falling price of wireless nodes and cloud-based management platforms. Pacific Northwest National Laboratory has cataloged 57 distinct cybersecurity threats to networked lighting, prompting manufacturers to harden firmware and implement certificate-based authentication. Solutions like Ubicquia’s UbiCell stream 32 telemetry points, enabling utilities to verify voltage levels and detect pole knock-downs in real time, while demonstrating up to 40% energy savings.

Municipal procurement guidelines now require bidders to disclose their cybersecurity certifications, positioning the ioXt “NLC” profile at the forefront of tender requirements. These specifications help cities avoid expensive rip-and-replace scenarios if vulnerabilities surface. For rural networks where fiber is scarce, cellular-enabled photocontrols tested in Acuity Brands’ Cell Connect pilot show strong throughput even at pole-top heights, thereby bringing smart-city functionality to suburban corridors. As depreciation schedules align with fixture lifespans, many agencies plan to convert the remaining conventional stock at end-of-life, accelerating connected penetration in the outer years of the forecast.

Geography Analysis

The United States dominated the North America outdoor lighting market with a 45.35% share in 2025 and is projected to grow at an 7.78% CAGR to 2031. Chicago retrofitted more than 280,000 streetlights, forecasting savings exceeding USD 100 million over ten years. Federal grants tied to the Bipartisan Infrastructure Law, along with extensive utility rebate coverage that spans 77% of zip codes, underpin the continued momentum. Strict outdoor lighting codes in jurisdictions such as Maine drive demand for compliant fixtures that cap correlated color temperatures at 3000 K and restrict upward light output. California agencies complement those efforts with dark-sky audits that encourage adaptive dimming during low-traffic hours.

Canada ranks second in regional revenue, thanks in part to provincial programs and municipal climate goals. Edmonton’s LED conversion demonstrates tangible gains, while Hamilton, Ontario, leverages solar-powered Illumient poles to avoid costly trenching on rocky terrain. Ontario’s Save on Energy rebates cover a percentage of project costs for commercial customers, accelerating uptake in retail and industrial parks. Canadian cities are also testing hybrid smart-solar systems that maintain illumination during grid outages, thereby enhancing resilience against severe winter storms.

Mexico trails in absolute value but shows steady growth tied to industrial parks, maquiladora zones, and new suburban housing. U.S. suppliers maintain production plants south of the border, hedging tariff risks while shortening lead times for domestic orders. Mexican municipalities are experimenting with energy-as-a-service contracts structured in U.S. dollars to mitigate currency volatility. Although national incentive programs are less robust, cross-border technology transfer and competitive fixture pricing support a healthy pipeline of retrofit bids, especially in northern states with strong manufacturing clusters.

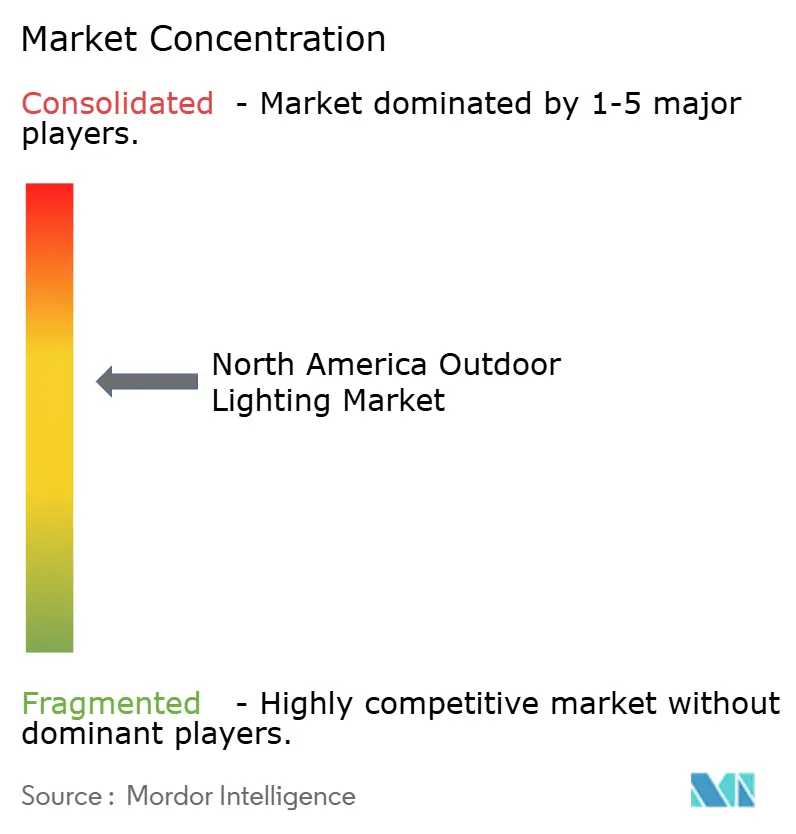

Competitive Landscape

The North America outdoor lighting market is moderately fragmented. Acuity Brands led the revenue league after posting USD 951.6 million in net sales for Q1 FY 2025, and the firm further broadened its portfolio by acquiring QSC for USD 1.2 billion to integrate advanced audio and control systems with smart luminaires. Kingswood Capital’s roll-up strategy led to the creation of Coleto Brands, which merged Kichler and Progress Lighting to form a sizable residential platform with a combined deal value of USD 256 million. Dialight’s manufacturing-supply dispute with Sanmina highlights the operational risk associated with contract electronics manufacturing.

Innovation awards reflect the competition for technological leadership. The 2024 IES Progress Report accepted 14 products each from Signify and RAB Lighting, while Acuity Brands and Green Creative earned seven selections, underscoring a focus on connected controls and bio-adaptive LEDs. Cooper Lighting Solutions garnered attention for its BioUp melanopic system, which supports circadian-friendly outdoor environments. Smaller firms are carving niches in solar-powered fixtures and dark-sky-certified optics as municipalities tighten their light-pollution rules.

Strategic moves center on partnerships with telecoms, sensor firms, and EV-charger providers to bundle services. Ubicquia collaborates with Acuity Brands on cellular photocontrols, while Clear Blue Technologies expands solar-hybrid deployments across Canadian provinces. Havells Lighting launched U.S. operations via a joint venture that includes a vertically integrated plant in South Carolina, signaling renewed competition from international entrants. With connected-ready platforms converging on common standards, differentiation increasingly hinges on integration services and cybersecurity assurances rather than core fixture performance.

North America Outdoor Lighting Industry Leaders

Signify N.V.

Acuity Brands Lighting Inc.

Eaton Intelligent Lighting (Cooper)

Cree LED Lighting

OSRAM GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Acuity Brands released IVO Deep Regressed Downlights, Lithonia Lighting REBL High Bay, and DTL Local Connect wireless photocontrols.

- January 2025: Acuity Brands completed its USD 1.2 billion acquisition of QSC, LLC, adding roughly USD 500 million in annual revenue to its Intelligent Spaces Group.

- January 2025: Coleto Brands commenced operations as the parent for Kichler and Progress Lighting after Kingswood Capital’s USD 256 million dual acquisition.

- September 2024: Kingswood Capital closed its purchase of Kichler Lighting from Masco Corporation for USD 125 million, finalizing the residential lighting portfolio build-out.

North America Outdoor Lighting Market Report Scope

| Residential Outdoor | |

| Commercial Outdoor | Retail and Hospitality |

| Offices and Business Parks | |

| Industrial and Logistics | |

| Parking Spaces | |

| Public and Street Lighting | |

| Sports and Large Area Lighting | |

| Other Type of Applications (Architectural and Landscape, Events, Galleries) |

| Traditional |

| LED |

| Conventional Stand-alone |

| Connected / Smart |

| United States |

| Canada |

| Mexico |

| By Type of Application | Residential Outdoor | |

| Commercial Outdoor | Retail and Hospitality | |

| Offices and Business Parks | ||

| Industrial and Logistics | ||

| Parking Spaces | ||

| Public and Street Lighting | ||

| Sports and Large Area Lighting | ||

| Other Type of Applications (Architectural and Landscape, Events, Galleries) | ||

| By Type of Lighting | Traditional | |

| LED | ||

| By Installation Mode | Conventional Stand-alone | |

| Connected / Smart | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current value of the North America outdoor lighting market?

The market was valued at USD 6.28 billion in 2026 and is projected to reach USD 8.36 billion by 2031.

Which country leads regional demand for outdoor lighting solutions?

The United States holds 45.35% of regional revenue and is expanding at 7.78% CAGR.

Which application segment is growing fastest?

Commercial outdoor lighting, driven by retail and hospitality upgrades, is rising at 7.32% CAGR through 2031.

How much energy can municipalities save by switching to LEDs?

Full LED conversion of U.S. streetlights could save 20,200 GWh annually and reduce municipal costs by USD 1 billion.

Page last updated on: