Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

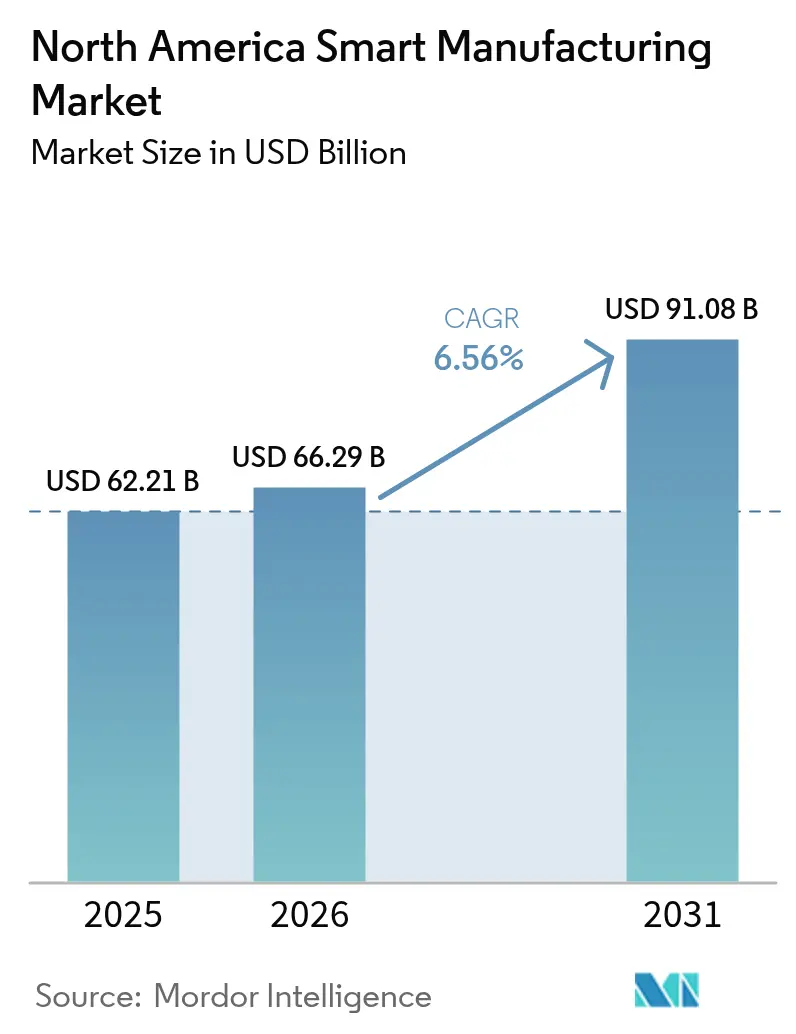

| Base Year Market Size (2025) | USD 62.21 Billion |

| Market Size (2026) | USD 66.29 Billion |

| Market Size (2031) | USD 91.08 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

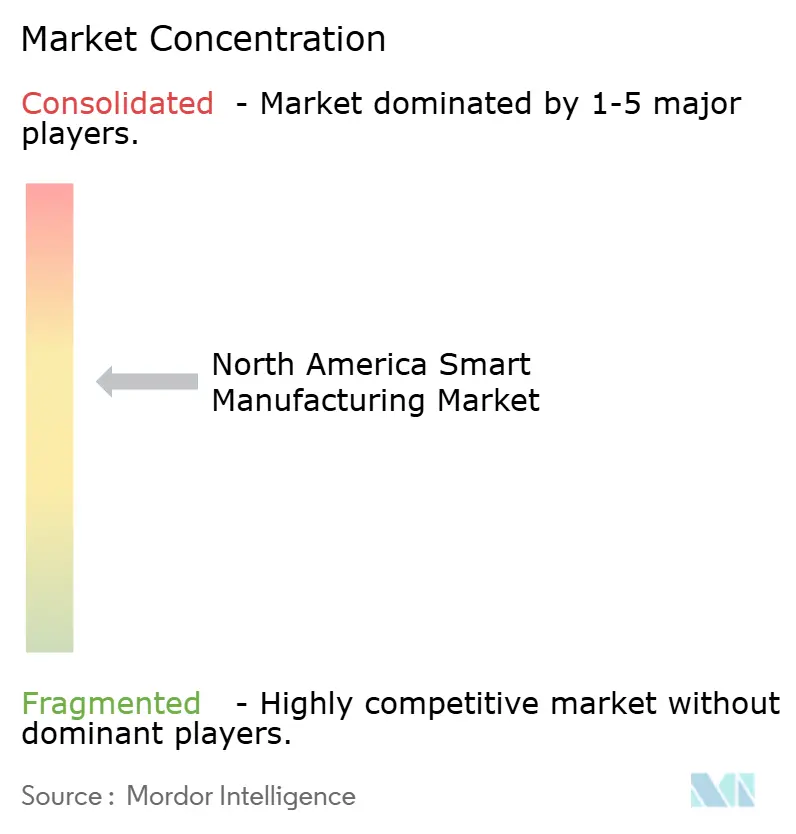

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Smart Manufacturing Market Analysis by Mordor Intelligence

The smart manufacturing market size was valued at USD 62.21 billion in 2025 and estimated to grow from USD 66.29 billion in 2026 to reach USD 91.08 billion by 2031, at a CAGR of 6.56% during the forecast period (2026-2031). Demand is shifting from isolated automation projects toward digital-first factory architectures that meld advanced analytics with cyber-physical production lines. Federal reshoring incentives, especially the CHIPS and Science Act and the Inflation Reduction Act, have converted the United States into a launchpad for greenfield facilities that embed digital twins, edge AI and time-sensitive networking from day one. Mexico is absorbing nearshoring spillovers as foreign direct investment pours into new automotive and electronics plants, while Canada is leveraging public–private 5G testbeds to attract high-value aerospace and medical device work. Together, these forces are expanding the addressable smart manufacturing market and sharpening competitive pressure on incumbent automation vendors.

Key Report Takeaways

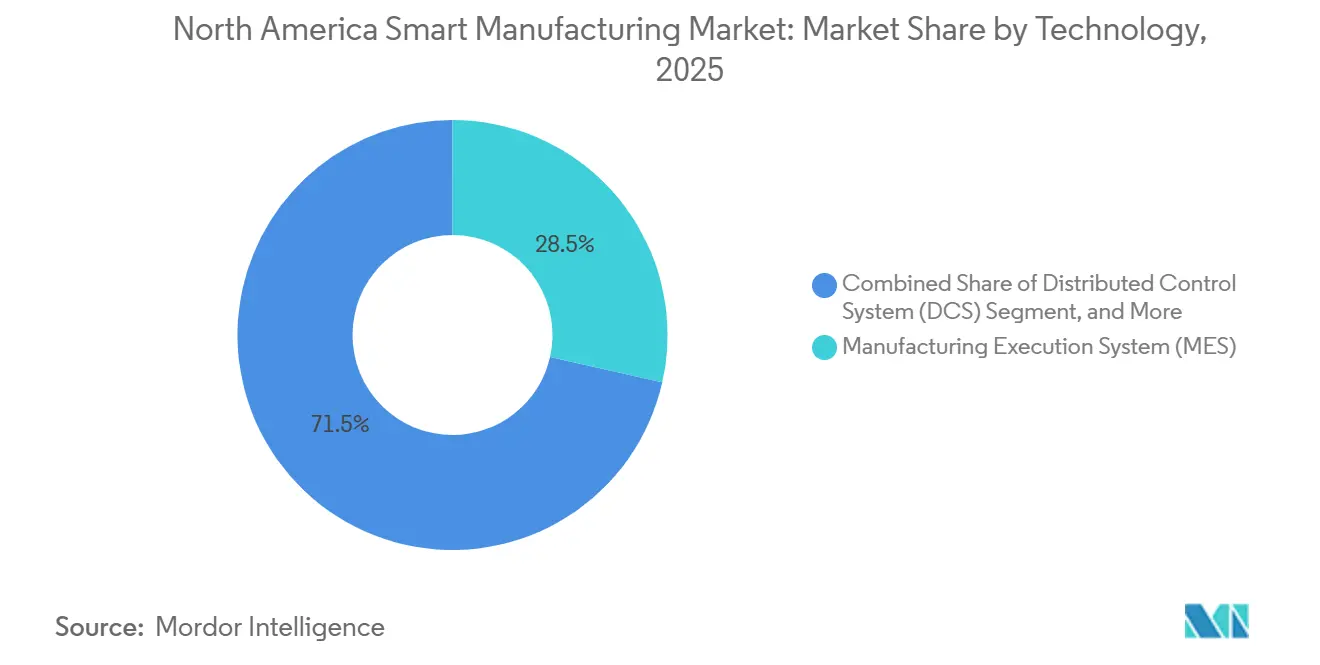

- By technology, manufacturing execution systems led with 28.53% of smart manufacturing market share in 2025; edge and cloud analytics platforms are advancing at a 7.82% CAGR through 2031.

- By component, software commanded 46.17% revenue in 2025, whereas services are forecast to grow at an 8.01% CAGR to 2031.

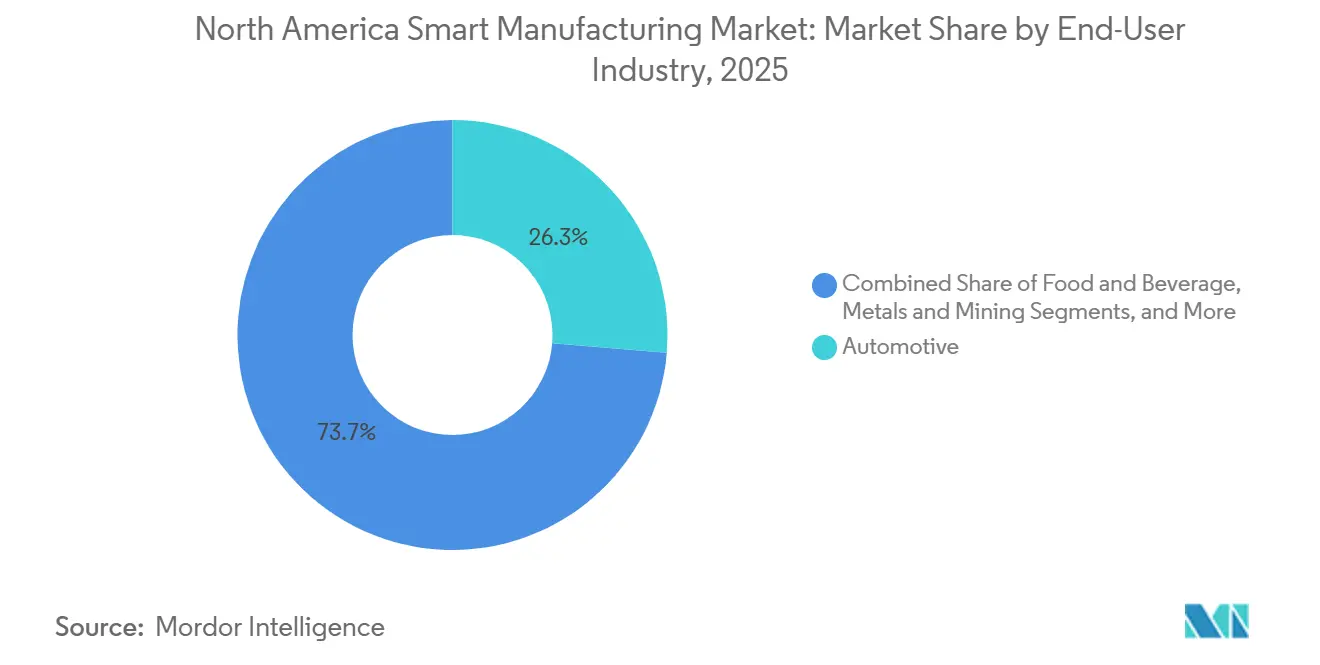

- By end-user industry, automotive captured 26.32% of 2025 demand, while pharmaceuticals and life sciences are expected to post the quickest expansion at a 7.56% CAGR.

- By deployment mode, on-premise implementations held 57.83% share in 2025, but cloud deployments are projected to climb at a 7.93% CAGR.

- By country, the United States accounted for 71.53% regional revenue in 2025, whereas Mexico is anticipated to record the fastest national growth at a 7.82% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Smart Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of AI-Enabled Edge Analytics in U.S. Discrete Manufacturing | +1.2% | United States and spillover to Canada | Medium term (2-4 years) |

| Rapid Proliferation of 5G-Powered Industrial IoT Networks across Canadian Plants | +1.0% | Canada, extending to Mexico border regions | Medium term (2-4 years) |

| Reshoring Incentives (CHIPS and Science Act, IRA) Fueling Digital-First Factories | +1.5% | United States, secondary influence on Mexico supply chains | Long term (≥ 4 years) |

| Sustainability Mandates Driving Smart Energy-Management Retrofits in Brown-Field Sites | +0.9% | United States, California and New York, Canada, Ontario and Quebec | Long term (≥ 4 years) |

| Adoption of Cyber-Physical Systems for Zero-Defect Production in Automotive Clusters | +0.8% | United States, Michigan and Ohio, Mexico, Nuevo León and Guanajuato | Medium term (2-4 years) |

| Growing Demand for Modular, Low-Code MES among SME Job-Shops | +0.7% | Midwest United States and Ontario manufacturing belts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of AI-Enabled Edge Analytics in U.S. Discrete Manufacturing

Discrete manufacturers are embedding inference engines at the network edge to reduce cloud latency and guard intellectual property. The National Association of Manufacturers showed that although 55% of firms viewed AI as strategic in 2024, only 29% reached plant-level deployment, underscoring a data-readiness gap.[1]National Association of Manufacturers, “2024 Manufacturing Outlook Survey,” nam.org Edge platforms that ship with pre-trained models for CNC tool-wear prediction and defect classification shorten proof-of-value cycles from quarters to weeks. Intel’s USD 7.86 billion CHIPS Act award for Arizona and Ohio fabs included commitments to use edge AI for wafer inspection, signaling that even semiconductor giants see local inference as indispensable. As sensor costs drop and GPU-equipped gateways proliferate, the smart manufacturing market is witnessing rapid mainstreaming of edge intelligence.

Rapid Proliferation of 5G-Powered Industrial IoT Networks across Canadian Plants

Private 5G eliminates the Ethernet umbilical cord, enabling mobile robotics, AR maintenance and real-time tracking inside sprawling factories. Hitachi Rail’s Ontario site achieved sub-10 millisecond latency by replacing fiber backhaul with a 5G standalone network. Canada’s Innovation Superclusters Initiative committed CAD 230 million (USD 170 million) to advanced-manufacturing 5G pilots by 2024, de-risking early adoption for aerospace and automotive clusters. The resulting reference sites are attracting cross-border OEMs and pushing the smart manufacturing market toward wireless, software-defined production layouts.

Reshoring Incentives Fueling Digital-First Factories

The CHIPS and Science Act and Inflation Reduction Act collectively triggered nearly USD 1 trillion of announced private manufacturing projects by late 2024. Subsidy eligibility favors sites that adopt OPC UA interoperability, digital twins and real-time energy dashboards. TSMC’s USD 6.6 billion grant and Micron’s USD 6.16 billion award both embedded smart-manufacturing KPIs in funding contracts. This regulatory scaffolding accelerates adoption in the smart manufacturing market by 18-24 months relative to organic, ROI-driven timelines.

Sustainability Mandates Driving Smart Energy-Management Retrofits

California’s Title 24 and New York’s Climate Leadership Act raise the efficiency bar for legacy plants, prompting investments in smart meters, variable-frequency drives and SCADA retrofits. The U.S. Department of Energy’s Better Plants program recorded cumulative savings of 1,100 trillion BTU by 2024 through real-time monitoring and automated load shedding.[2]U.S. Department of Energy, “Better Plants Program,” energy.gov Suppliers to multinational OEMs now treat ISO 50001 certification as table stakes, extending the smart manufacturing market beyond direct regulatory reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent OT Cyber-Insurance Premium Hikes Limiting Digital Conversions | -0.8% | United States and Canada | Short term (≤ 2 years) |

| Multi-Vendor Interoperability Gaps in Legacy PLC Install-Base | -0.6% | United States—Rust Belt, Canada—Ontario and Quebec | Medium term (2-4 years) |

| Inflation-Driven CAPEX Deferrals in Tier-2 Automotive Suppliers | -0.5% | United States—Michigan, Ohio, Indiana; Mexico—Nuevo León | Short term (≤ 2 years) |

| North American Skilled-Trades Attrition Outpacing Upskilling Pipelines | -0.7% | Rural manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent OT Cyber-Insurance Premium Hikes Limiting Digital Conversions

Cyber-insurance premiums for operational technology jumped 30% in 2024 as ransomware groups pivoted toward industrial control systems. Insurers now require network segmentation, multi-factor authentication and quarterly vulnerability scans, adding compliance costs that squeeze small and medium enterprises. Average ransomware recovery topped USD 2.73 million, excluding downtime. The expense–risk trade-off is slowing new connectivity projects and dampening spending across the smart manufacturing market.

Multi-Vendor Interoperability Gaps in Legacy PLC Install-Base

Brownfield plants often run Rockwell, Siemens, Mitsubishi and Omron PLCs that speak incompatible protocols. Upgrading each line to OPC UA can cost USD 5,000-15,000 in gateways and engineering effort. An ISA survey found 62% of North American factories operate mixed-vendor controls, and 48% rank interoperability as the top roadblock to MES upgrades. The resulting payback delays discourage retrofits, constraining the otherwise robust smart manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Edge Analytics Outpaces Foundational MES

Manufacturing execution systems delivered 28.53% of 2025 revenue, cementing their place as the orchestration core that bridges ERP with shop-floor controls. Edge and cloud analytics platforms are forecast to grow at 7.82% through 2031, the fastest rise among all technologies as manufacturers seek prescriptive models that autonomously adjust parameters mid-cycle. DCS and SCADA remain indispensable in process industries, yet are increasingly over-layered with AI to refine setpoints in real time. Human-machine interfaces are morphing into tablet and AR overlays, giving technicians contextual data during maintenance rounds. Robotics, machine vision and collaborative cobots widen the addressable smart manufacturing market as payback periods compress below 18 months.[3]ABB Ltd., “Collaborative Robots GoFa and SWIFTI,” abb.com

Discrete vendors are switching from hardware margins to cloud subscriptions that monetize analytics. Siemens expanded its Xcelerator suite with generative-AI copilots that auto-write PLC code, while Rockwell Automation unified asset management and predictive maintenance under FactoryTalk Hub. Low-code MES providers such as Tulip let production engineers build workflows without IT support, opening the smart manufacturing market to 300,000-plus North American job-shops.

By Component: Subscription Software Dominates, Services Accelerate

Software held 46.17% of total revenue in 2025, reflecting the premium on digital intelligence within the smart manufacturing market. Control devices are plateauing as deterministic logic migrates onto software-defined controllers running on industrial PCs. Services will expand at an 8.01% CAGR because vendors bundle implementation, training and continuous optimization into SaaS plans, shifting client outlays from CAPEX to OPEX. Sensors and actuators under USD 5 each enable dense instrumentation, while 5G and time-sensitive networking refresh aging fieldbuses with microsecond synchronization.

Vision systems from Cognex and Keyence run deep-learning models on-device to reach 200 parts per minute inspection rates. PTC’s Vuforia overlays AR instructions that cut mean-time-to-repair by 34% at aerospace sites. Vendors increasingly sell guaranteed uptime or throughput, aligning their success with client output and reinforcing service revenue streams inside the smart manufacturing market.

By End-User Industry: Auto Scale, Pharma Speed

Automotive users generated 26.32% of 2025 demand as ISO 26262 and ASPICE push zero-defect mandates. OEMs deploy digital twins and predictive analytics to validate weld quality and battery cell formation. Pharmaceuticals and life sciences will grow fastest at 7.56% CAGR, propelled by Drug Supply Chain Security Act serialization that obliges unit-level track and trace. Aerospace primes use digital twins to halve prototype cycles, while oil and gas refineries insert edge AI that predicts failures 72 hours in advance.

Food and beverage processors apply vision-based foreign-object detection to uphold FSMA traceability rules, and metals miners field autonomous haul trucks to cut exposure in hazardous zones. Electronics fabs maintain >95% yield via inline metrology, demonstrating that exacting verticals sustain premium demand within the smart manufacturing market. Emerging domains such as battery gigafactories and additive manufacturing present bespoke requirements that push MES customization services, lifting long-tail opportunities.

By Deployment Mode: Hybrid Tops the Adoption Curve

On-premise setups kept 57.83% share in 2025 because many firms insist on local control over IP and latency-critical loops. Cloud deployments, however, are projected to rise at a 7.93% CAGR as Azure and AWS release industry clouds loaded with connectors for leading PLC brands. Hybrid is the practical compromise; millisecond safety logic stays onsite while historical analytics and fleet benchmarking move to the cloud. Schneider Electric’s EcoStruxure exemplifies this split architecture.

Small and medium enterprises gravitate toward SaaS MES costing under USD 1,000 per month, sidestepping six-figure server purchases. Yet latency-sensitive motion control governed by IEC 61508 standards continues to resist full cloud migration. Regulatory data-residency rules in pharma and defense further shape deployment choices, ensuring that all three modes coexist throughout the smart manufacturing market.

Geography Analysis

The United States leads the smart manufacturing market with 71.53% share as of 2025. Federal subsidies tied to digital-twin metrics and domestic equipment sourcing compel greenfield fabs to adopt predictive analytics, edge AI and OPC UA interoperability from day one. Expanded EPA greenhouse-gas rules in 2026 and stricter state energy codes accelerate brownfield retrofits focused on smart meters and variable-frequency drives. Labor shortages 622,000 openings in late 2024 are nudging OEMs toward robots and collaborative systems that supplement human workers rather than displace them.

Mexico represents the fastest growth corridor at 7.82% CAGR, catalyzed by nearshoring strategies that sent FDI to record highs. Automotive suppliers in Guanajuato and Queretaro deploy bilingual MES to align with U.S. quality audits, while medical device exporters in Tijuana add serialization modules to maintain FDA compliance. Infrastructure gaps such as intermittent broadband in rural plants slow cloud analytics uptake, yet flexible labor and geographic proximity make Mexico pivotal to the North American smart manufacturing market.

Canada combines public-private funding with demographic imperatives. Private 5G networks in Ontario give AGVs sub-10 millisecond latency, and collaborative robots are filling workforce gaps as median worker age climbs past 47 years. Although higher wages curb large-scale relocation, niche sectors like aerospace and specialty chemicals thrive on advanced digital infrastructure seeded by the Innovation Superclusters Initiative. Altogether, geographic diversification underpins regional resilience and sustains demand across the smart manufacturing market.

Competitive Landscape

The smart manufacturing market is moderately consolidated. Siemens, Rockwell Automation, Schneider Electric and ABB leverage extensive installed bases in PLCs and drives, yet face revenue migration toward cloud software. Siemens’ USD 500 million expansion of its Ohio Digital Industries campus augments Xcelerator with AI copilots that propose ladder logic, while Rockwell’s FactoryTalk Hub merges asset performance and remote support under a single SaaS umbrella.

White-space innovators such as Tulip, Plex Systems and Sight Machine court the 98% of manufacturers classified as SMEs by offering low-code MES priced under USD 1,000 per month and integration kits for legacy PLCs. PTC absorbed ServiceMax for USD 1.46 billion to blend digital-twin telemetry with field-service scheduling, guaranteeing uptime outcomes to clients. NVIDIA and Intel embed inference accelerators into gateways that keep time-critical models local, minimizing latency and safeguarding IP.

OPC UA’s status as IEC 62541 provides a path to vendor-neutral data exchange, yet adoption lags because incumbents retain proprietary protocol advantages. Customers hesitate to retrofit mixed-vendor plants, extending life cycles for legacy PLCs and slowing platform convergence. Consequently, strategic positioning pivots on ecosystem openness, vertical templates and outcome-based pricing, all of which redefine value creation inside the smart manufacturing market.

North America Smart Manufacturing Industry Leaders

ABB Ltd.

Emerson Electric Co.

FANUC Corp.

General Electric Co.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Rockwell Automation and Microsoft integrated Azure OpenAI into FactoryTalk Design Studio to auto-generate ladder logic from natural-language prompts, aiming to cut engineering time by 40%.

- December 2025: Siemens committed USD 500 million to expand its Ohio Digital Industries Software campus, adding 1,000 AI-focused roles.

- November 2025: ABB acquired ASTI Mobile Robotics Group for USD 200 million, strengthening its autonomous mobile robot lineup.

- October 2025: Honeywell launched Forge Energy Optimization, promising 10-15% energy savings via machine-learning load balancing.

North America Smart Manufacturing Market Report Scope

Smart manufacturing uses computer-integrated manufacturing, high adaptability and quick design changes, digital information technology, and more adaptable technical workforce training, which includes fast changes in production levels based on demand, optimization of the supply chain, efficient production, and recyclability.

The North America Smart Manufacturing Market Report is Segmented by Technology (SCADA, DCS, HMI, MES, PLM, ERP, Robotics, Machine Vision, Edge Analytics), Component (Control Devices, Communication Infrastructure, Sensors, Machine Vision, Robotics, Software and Services), End-User Industry (Automotive, Aerospace, Oil and Gas, Chemicals, Pharmaceuticals, Food and Beverage, Metals, Electronics, Pulp and Paper, Textiles), Deployment Mode (On-Premise, Cloud, Hybrid), and Geography (United States, Canada, Mexico). Market Forecasts are Provided in Terms of Value (USD).

By Techonology

| Supervisory Control and Data Acquisition (SCADA) |

| Distributed Control System (DCS) |

| Human-Machine Interface (HMI) |

| Manufacturing Execution System (MES) |

| Product Lifecycle Management (PLM) |

| Enterprise Resource Planning (ERP) |

| Robotics and Collaborative Robots |

| Machine Vision and Quality Inspection |

| Edge and Cloud Analytics Platforms |

By Component

| Control Devices (PLC, DCS, PAC) |

| Communication Infrastructure (5G, Industrial Ethernet) |

| Sensors and Actuators |

| Machine Vision Systems |

| Robotics (Articulated, SCARA, AMR) |

| Software and Services (MES, Digital Twin, SaaS) |

By End-User Industry

| Automotive |

| Aerospace and Defense |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Chemicals and Petrochemicals |

| Pharmaceuticals and Life-Sciences |

| Food and Beverage |

| Metals and Mining |

| Electronics and Semiconductors |

| Pulp and Paper |

| Other End-User Industries (Textiles, Plastics) |

By Deployment Mode

| On-premise |

| Cloud (SaaS) |

| Hybrid |

By Country

| United States |

| Canada |

| Mexico |

| By Techonology | Supervisory Control and Data Acquisition (SCADA) |

| Distributed Control System (DCS) | |

| Human-Machine Interface (HMI) | |

| Manufacturing Execution System (MES) | |

| Product Lifecycle Management (PLM) | |

| Enterprise Resource Planning (ERP) | |

| Robotics and Collaborative Robots | |

| Machine Vision and Quality Inspection | |

| Edge and Cloud Analytics Platforms | |

| By Component | Control Devices (PLC, DCS, PAC) |

| Communication Infrastructure (5G, Industrial Ethernet) | |

| Sensors and Actuators | |

| Machine Vision Systems | |

| Robotics (Articulated, SCARA, AMR) | |

| Software and Services (MES, Digital Twin, SaaS) | |

| By End-User Industry | Automotive |

| Aerospace and Defense | |

| Oil and Gas (Upstream, Midstream, Downstream) | |

| Chemicals and Petrochemicals | |

| Pharmaceuticals and Life-Sciences | |

| Food and Beverage | |

| Metals and Mining | |

| Electronics and Semiconductors | |

| Pulp and Paper | |

| Other End-User Industries (Textiles, Plastics) | |

| By Deployment Mode | On-premise |

| Cloud (SaaS) | |

| Hybrid | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the smart manufacturing market in North America today?

It reached USD 66.29 billion in 2026 and is on track to hit USD 91.08 billion by 2031 at a 6.56% CAGR.

Which technology is growing fastest within smart manufacturing?

Edge and cloud analytics platforms are projected to rise at 7.82% a year through 2031 as firms shift from descriptive to prescriptive insights.

Why are U.S. reshoring policies important for smart factories?

CHIPS Act and Inflation Reduction Act subsidies embed digital-twin and predictive-maintenance requirements into funding terms, accelerating adoption by 18-24 months.

What is the main barrier holding back legacy plants?

Interoperability gaps among mixed-vendor PLCs inflate retrofit costs by USD 5,000-15,000 per line and delay MES upgrades.

Which country in North America is expanding the quickest?

Mexico is forecast to grow at 7.82% annually thanks to record FDI and nearshoring of automotive and electronics production.

How are cyber-insurance trends affecting digital projects?

Premiums jumped 30% in 2024, and stricter underwriting standards make it harder for small firms to justify new connectivity investments.

Page last updated on: