Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.09 Billion |

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 2.63 Billion |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Forage Seed Market Analysis by Mordor Intelligence

North America forage seed market size in 2026 is estimated at USD 2.17 billion, growing from 2025 value of USD 2.09 billion with 2031 projections showing USD 2.63 billion, growing at 3.93% CAGR over 2026-2031. A steady surge in livestock inventories, rapid commercialization of drought-tolerant genetics, and widening e-commerce access underpin a growth pattern that remains resilient in the face of weather volatility. Seed companies are channeling capital into biotechnology and microbial coatings that elevate germination on marginal soils, helping producers squeeze more protein per acre while managing water scarcity. Cost-share incentives from federal and provincial agencies lower the adoption hurdle for premium varieties while online channels shorten the supply chain, enabling small and mid-size farmers to source specialized genetics once reserved for large corporate dairies. Competitive intensity is shifting away from price and toward trait innovation, with patent filings for drought tolerance, digestibility, and herbicide resistance accelerating as climate risk mounts.

Key Report Takeaways

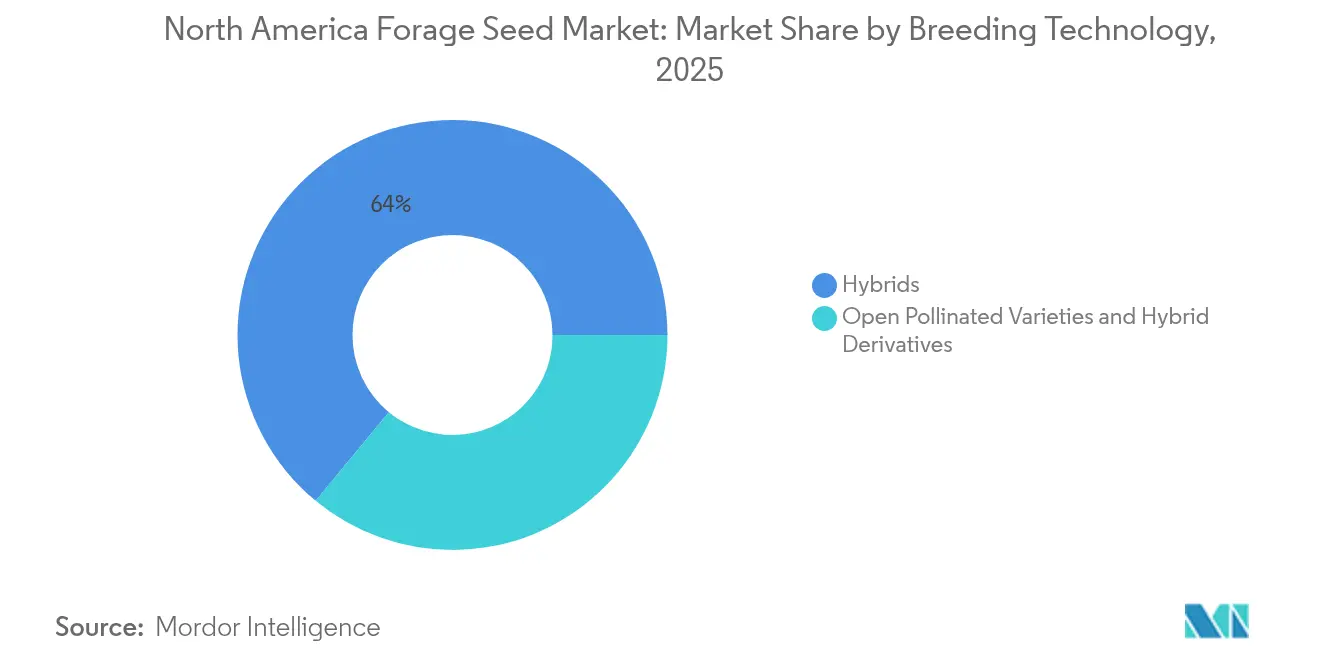

- By breeding technology, hybrids held 64.02% of the North America forage seed market share in 2025; open-pollinated varieties and hybrid derivatives are expanding at a 4.47% CAGR through 2031.

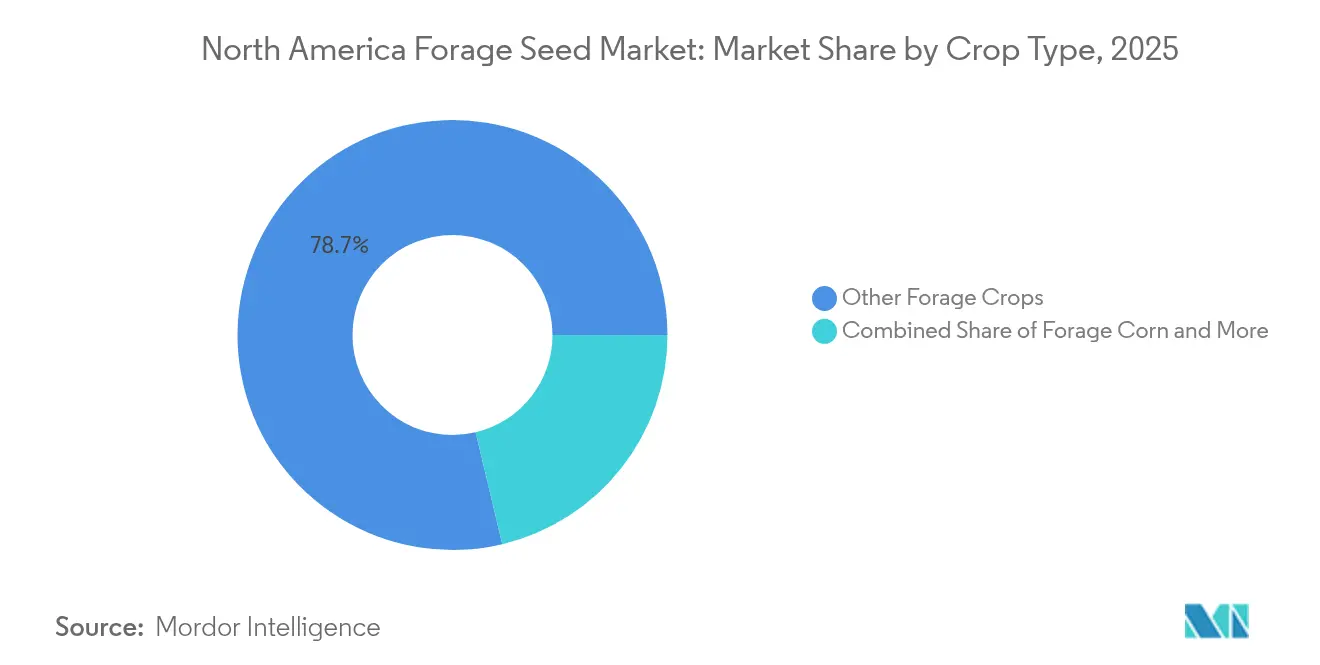

- By crop type, other forage crops accounted for 78.72% share of the North America forage seed market size in 2025, while alfalfa is growing the fastest at a 4.44% CAGR to 2031.

- By geography, Canada captured 47.18% revenue share in 2025 and is advancing at a 4.98% CAGR to 2031, the quickest pace among all countries.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Forage Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of dairy and beef livestock herds boosts demand for high-protein forage seed | +0.8% | United States, Canada core with spillover to Mexico | Medium term (2-4 years) |

| Shift toward drought-tolerant pasture systems amid rising water-stress events | +0.7% | Western United States, Prairie Canada, and Northern Mexico | Long term (≥ 4 years) |

| Broad adoption of GM herbicide-tolerant alfalfa and sorghum hybrids | +0.6% | United States, selective adoption in Canada | Short term (≤ 2 years) |

| Government cost-share programs for cover-crop/forage establishment | +0.5% | United States through USDA programs, Canada through provincial initiatives | Medium term (2-4 years) |

| Rapid growth of e-commerce seed channels reaching small and mid-size producers | +0.4% | North America with rural connectivity improvements | Short term (≤ 2 years) |

| Venture-capital–backed microbial seed coatings improving establishment on marginal soils | +0.3% | North America, with a focus on degraded agricultural lands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Dairy and Beef Herds Boosts Demand for High-Protein Forage Seed

Livestock inventory expansion across North America drives fundamental demand shifts toward protein-dense forage varieties that optimize feed conversion ratios and milk production yields. The United States Department of Agriculture (USDA) data indicate that dairy cow numbers increased 2.1% in 2024, while beef cattle operations expanded by 1.8%, creating sustained pressure for premium forage genetics[1]Source: USDA National Agricultural Statistics Service, “Livestock and Poultry Statistics,” nass.usda.gov. Because land prices keep climbing, many producers maximize nutrients per acre with elite seed genetics that furnish crude-protein levels above 20%. Organic operators face extra pressure to source certified seed, channeling more value into specialty suppliers. The North America forage seed market benefits as feedlots and dairies commit to multi-year genetics contracts to lock in supply and hedge against price swings.

Shift Toward Drought-Tolerant Pasture Systems Amid Rising Water-Stress Events

Roughly 35% of regional grasslands endured severe drought during the 2024 season, accelerating grower migration to deep-rooted alfalfa and water-efficient sorghum that retain up to 70% of anticipated yield under stress[2]Source: National Drought Mitigation Center, “North American Drought Monitor,” droughtmonitor.unl.edu. Adoption dovetails with precision irrigation programs that ration every acre-inch of water. Insurance premium discounts now reward producers who verify resilient varieties, enhancing the economic case for upgrading genetics. Seed developers respond by stacking drought tolerance with improved digestibility, a combination proving attractive to both cattle and sheep operations where weight-gain targets remain stringent.

Broad Adoption of GM Herbicide-Tolerant Alfalfa and Sorghum Hybrids

Biotechnology integration transforms weed management protocols while reducing labor costs and chemical inputs for large-scale forage operations. Herbicide-tolerant alfalfa adoption reached 85% of total alfalfa acreage in the United States by 2024, driven by glyphosate resistance that enables post-emergence weed control without crop damage. The same trend is moving into forage sorghum, where dual-trait hybrids curb broadleaf pressure and reduce chemical expenditure by up to 25%. Trait uptake is slower in Canada because of tighter regulatory reviews, but cross-border seed flows ensure availability for early adopters. As resistant weeds proliferate, tolerance traits become less a luxury and more a risk-management necessity, anchoring recurring demand for proprietary genetics.

Government Cost-Share Programs for Cover-Crop and Forage Establishment

Federal and state conservation programs provide financial incentives that reduce establishment costs and accelerate adoption of improved forage systems among cost-sensitive producers. The USDA Conservation Reserve Program allocated USD 1.8 billion in 2024 for cover crop and forage establishment, with average cost-share rates of 50-75% for approved seed varieties[3]Source: USDA Farm Service Agency, “Conservation Reserve Program Statistics,” fsa.usda.gov. Parallel provincial grants in Alberta and Saskatchewan further lower upfront spending, letting small family farms trial hybrid blends they previously considered unaffordable. Compliance rules mandate certified seed and documented establishment, pushing sales toward licensed suppliers with audit-ready traceability systems. That in turn shapes breeding pipelines by favoring varieties that meet environmental scoring metrics tied to soil-carbon retention and pollinator benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme climate volatility is causing seed-crop production swings | -0.6% | North America with particular impact on seed production regions | Short term (≤ 2 years) |

| IP-driven seed price escalation is limiting adoption by forage hay growers | -0.4% | United States and Canada with patent-protected varieties | Medium term (2-4 years) |

| Emerging herbicide resistance in forage sorghum and grass pastures | -0.3% | United States Great Plains, Canadian Prairies | Long term (≥ 4 years) |

| Tight native seed supply as prairie restoration accelerates | -0.2% | Great Plains region, Prairie Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extreme Climate Volatility Causing Seed-Crop Production Swings

Weather extremes increasingly disrupt seed production schedules and quality standards, creating supply chain instability that constrains market growth and inflates pricing volatility. The 2024 growing season experienced record temperature fluctuations across key seed production regions, with North Dakota reporting a 35% reduction in alfalfa seed yields due to late-season frost events. Similar episodes of excessive heat during pollination lowered germination quality, prompting rigorous new QC protocols. Insurers raised seed-crop coverage premiums, costs that flow downstream to end-users. Multi-regional production helps buffer supply but increases logistical complexity and inventory holding risk.

IP-Driven Seed Price Escalation Limiting Adoption by Forage Hay Growers

Intellectual property protection for advanced genetics creates pricing premiums that exceed economic thresholds for many forage hay operations, particularly those serving commodity markets with limited pricing flexibility. Patent-protected alfalfa varieties command price premiums over conventional genetics, while licensing fees for herbicide-tolerant traits add additional costs that many producers cannot justify given current hay pricing. The situation intensifies as patent portfolios expand and trait stacking increases licensing complexity, with some advanced varieties requiring multiple royalty payments that compound cost pressures. Legal frameworks governing seed patents also create uncertainty for producers regarding saved seed usage rights, further complicating adoption decisions and potentially constraining market growth in price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Maintain Scale Advantage While Diversity Gains Appeal

Hybrid cultivars accounted for 64.02% of the North America forage seed market share in 2025, underlining their status as the performance benchmark for large dairies and feedlots. Yield consistency, uniform maturity, and built-in trait packages such as herbicide tolerance and digestibility enhancement keep hybrids dominant. The North America forage seed market has seen continuous trait stacking, moving beyond weed control into drought endurance and protein boost, a progression that aligns with precision-nutrition goals. Yet open-pollinated varieties and hybrid derivatives are outpacing the category at a 4.47% CAGR, a trend reflective of cost containment and organic certification needs. Smaller ranches value the ability to save seed without infringing patents, and diversified grass-fed systems prize the genetic heterogeneity that buffers climatic shocks.

Open-pollinated expansion creates room for regional seed houses that curate locally adapted germplasm, sometimes pairing non-GM genetics with microbial coatings for better emergence on depleted soils. These entrants rarely challenge the R&D budgets of multinationals, but they secure loyalty in niche channels that transact heavily online. The hybrid camp counters by releasing lower-royalty “value” lines and introducing digital agronomy tools that fine-tune seeding rates and fertility, elevating return on every bag sold. As intellectual property regimes evolve, both models appear poised to coexist, with hybrids anchoring volume and open-pollinated types supplying flexibility within the broader North America forage seed market.

By Crop Type: Diverse Forage Blends Dominate as Alfalfa Accelerates

Other Forage Crops represented 78.72% of the North America forage seed market size in 2025, illustrating producer preference for agronomic resilience and soil-health gains. Ryegrass-clover blends, meadow brome, and chicory combos gain traction in regenerative grazing programs where biomass diversity extends grazing seasons and cuts input dependence. Seed firms now package multi-species cocktails pre-formulated for regional rainfall and soil pH, an approach resonating with conservation cost-share metrics.

Alfalfa, while a smaller slice, is expanding fastest at a 4.44% CAGR, supported by its unrivaled protein contribution to dairy rations. Breeders leverage genomics to boost digestibility and lignin reduction, enabling higher milk yields per ton of dry matter. Forage sorghum is carving out gains in low-water environments; its seed demand correlates tightly with irrigation-cut mandates in the Ogallala aquifer zone. Forage corn maintains presence in high-nutrition diets but faces competition from sorghum where water rights tighten. Altogether, crop-type momentum underscores a wider shift in the North America forage seed market toward biologically-diverse swards that better withstand climate volatility.

Geography Analysis

Canada delivered 47.18% of total revenue in 2025, making it the single largest slice of the North America forage seed market. Strong provincial incentives for pasture renovation, a consolidated dairy sector, and extensive prairie acreage converge to fuel volume. The North America forage seed market size, attributed to Canada, is expanding at a 4.98% CAGR, propelled by accelerated adoption of drought-tolerant blends as prairie summers grow hotter. Seed orders align with cost-share windows, creating predictable spring and fall surges that suppliers must stock months in advance.

The United States follows in absolute value terms; its sheer production diversity stretches from temperate Midwest hayfields to humid Southeast grass pastures. Federal conservation dollars and a robust e-commerce ecosystem support varietal experimentation, yet growth lags in Canada because of market maturity. Mexico remains a nascent but noteworthy frontier. Modernizing dairies in Chihuahua and Jalisco are trialing North American genetics, but constraints in cold-storage logistics and financing slow broader uptake. The rest of North America contributes marginally today but represents latent upside as infrastructure and rural credit access improve.

Mexico’s market is anchored in northern dairy belts where modern confinement systems crave protein-rich hay. Imports of elite alfalfa seed from suppliers in Arizona and California rise annually despite logistics bottlenecks at border warehouses. Pilot government programs now test subsidy models similar to Canadian cost-share schemes but have yet to reach scale. Longer term, improvements in cold-chain trucking and broader fintech penetration are likely to unleash pent-up demand, broadening the geographic footprint of the North America forage seed market.

Competitive Landscape

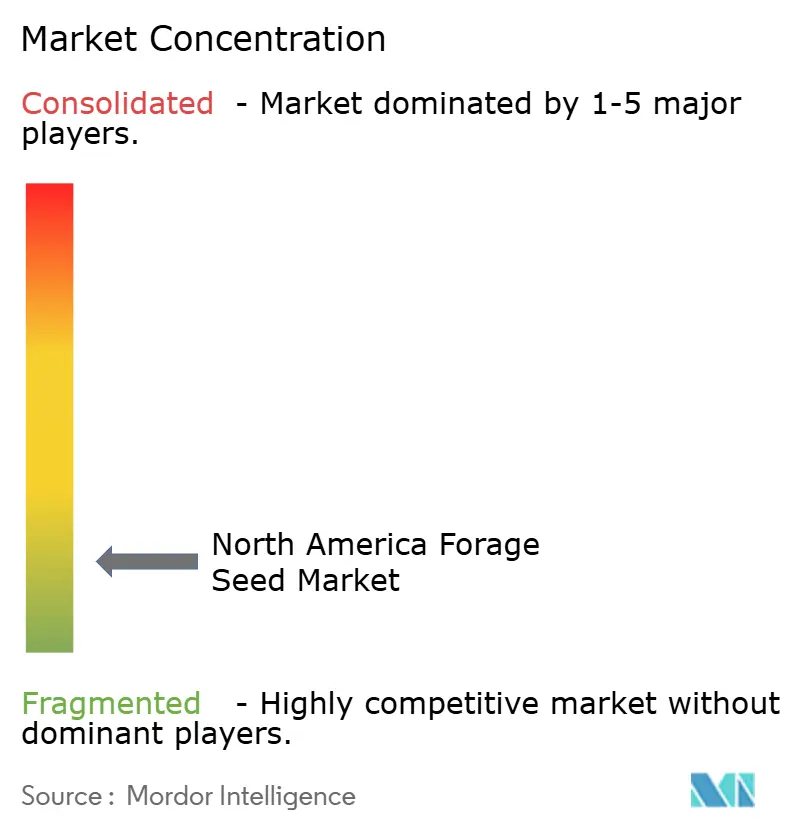

The North America forage seed market shows a fragmented structure. The top five multinational companies control a minimum share of revenue, enough to exert scale benefits but leaving room for niche entrepreneurs. Bayer AG made substantial investments in new North Dakota and Alberta plants to secure drought-tolerant alfalfa processing capacity, a move that widens the distance from smaller rivals in volume-based contract bids.

Digital disruptors, including Allied Seed and Hancock Seed, are leveraging direct-to-consumer storefronts and subscription models to chip away at regional dealer share. They often bundle microbial coatings and provide localized agronomy dashboards, differentiators that resonate with tech-savvy millennial farmers. Meanwhile, European breeders such as DLF Seeds and KWS SAAT partner with North American biotech start-ups for next-generation trait development, indicating an ecosystem that values collaborative innovation over zero-sum rivalry. Patent races continue; applications tied to drought tolerance, underscoring the strategic centrality of climate adaptation.

Regulatory developments remain a swing factor. Canada’s stricter biotech approval timelines slow cross-border trait harmonization, so multinationals stagger product launches, first entering the United States and later Canada. This sequencing forces distributors to manage dual inventories. Moderate consolidation, paired with expanding specialty niches, signals a competitive scene where both scale and specialization can thrive within the North America forage seed market.

North America Forage Seed Industry Leaders

Bayer AG

KWS SAAT SE & Co. KGaA

Land O’Lakes Inc.

DLF Seeds A/S

Corteva Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DLF Seeds A/S launched a new corporate strategy in June 2025, focusing on sustainability through seed enhancement development. The company invested in seed enhancement facilities and proprietary technology to develop seed coatings with biological and nutritional components.

- August 2022: DLF established a research station dedicated to forage, turf, and legumes across a 30-acre facility in Bangor, Wisconsin.

North America Forage Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Alfalfa, Forage Corn, Forage Sorghum are covered as segments by Crop. Canada, Mexico, United States are covered as segments by Country.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Other Traits | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

Crop Type

| Alfalfa |

| Forage Corn |

| Forage Sorghum |

| Other Forage Crops |

Country

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Other Traits | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Crop Type | Alfalfa | ||

| Forage Corn | |||

| Forage Sorghum | |||

| Other Forage Crops | |||

| Country | Canada | ||

| Mexico | |||

| United States | |||

| Rest of North America | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms