Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.54 Billion |

| Market Size (2031) | USD 39.14 Billion |

| Growth Rate (2026 - 2031) | 20.29% CAGR |

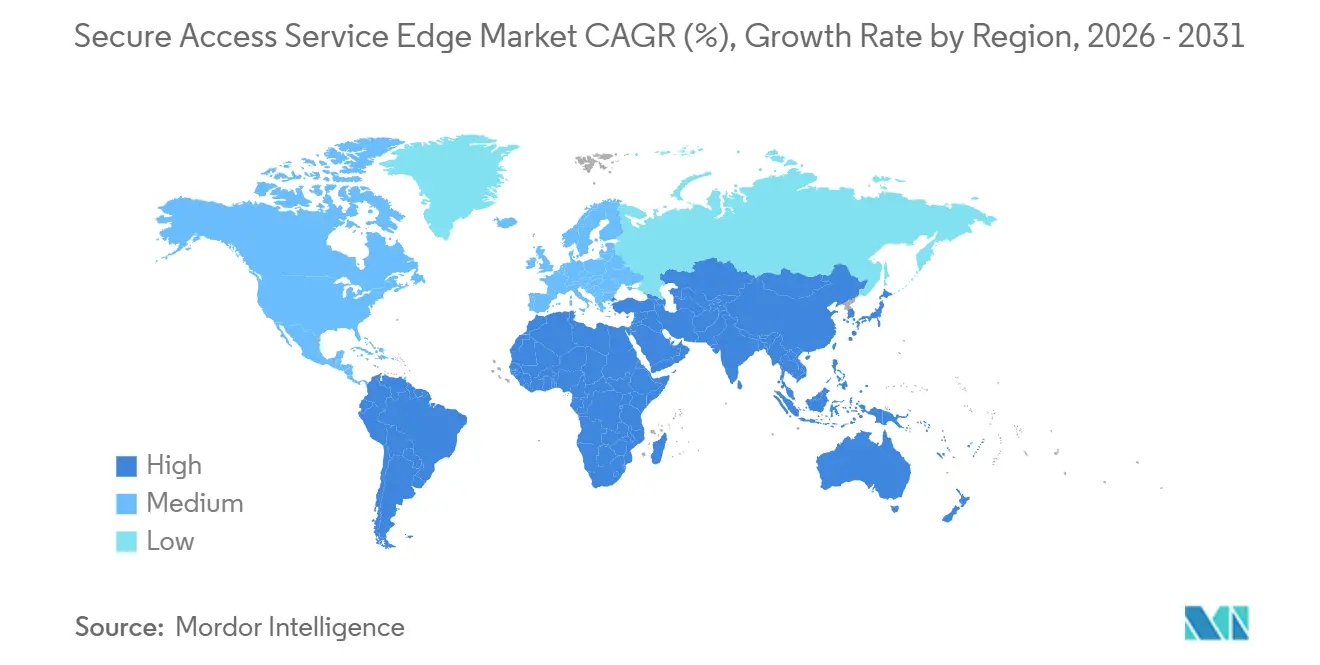

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

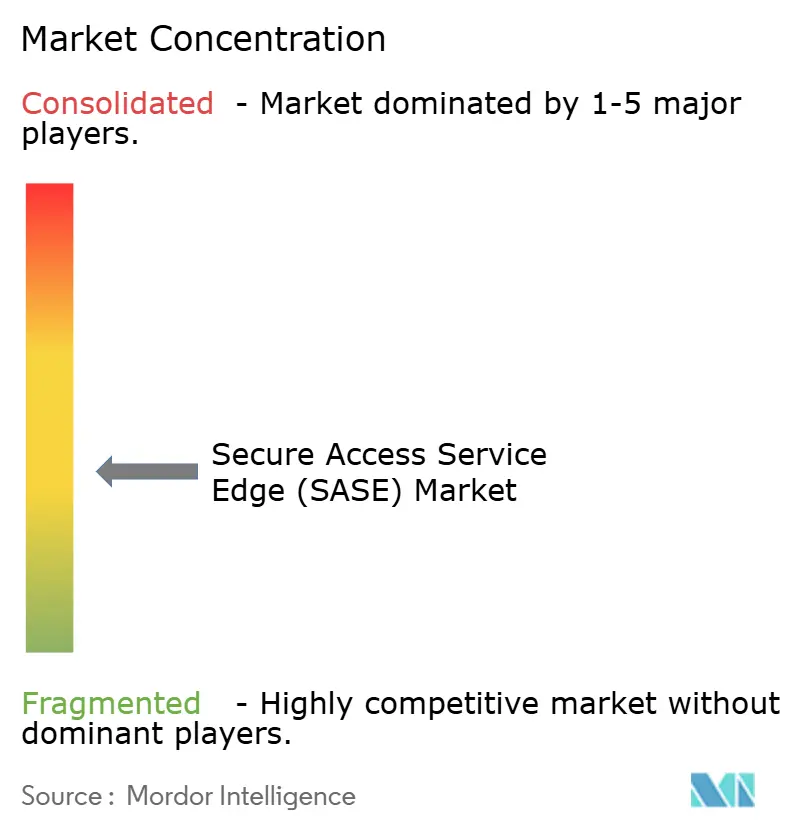

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure Access Service Edge Market Analysis by Mordor Intelligence

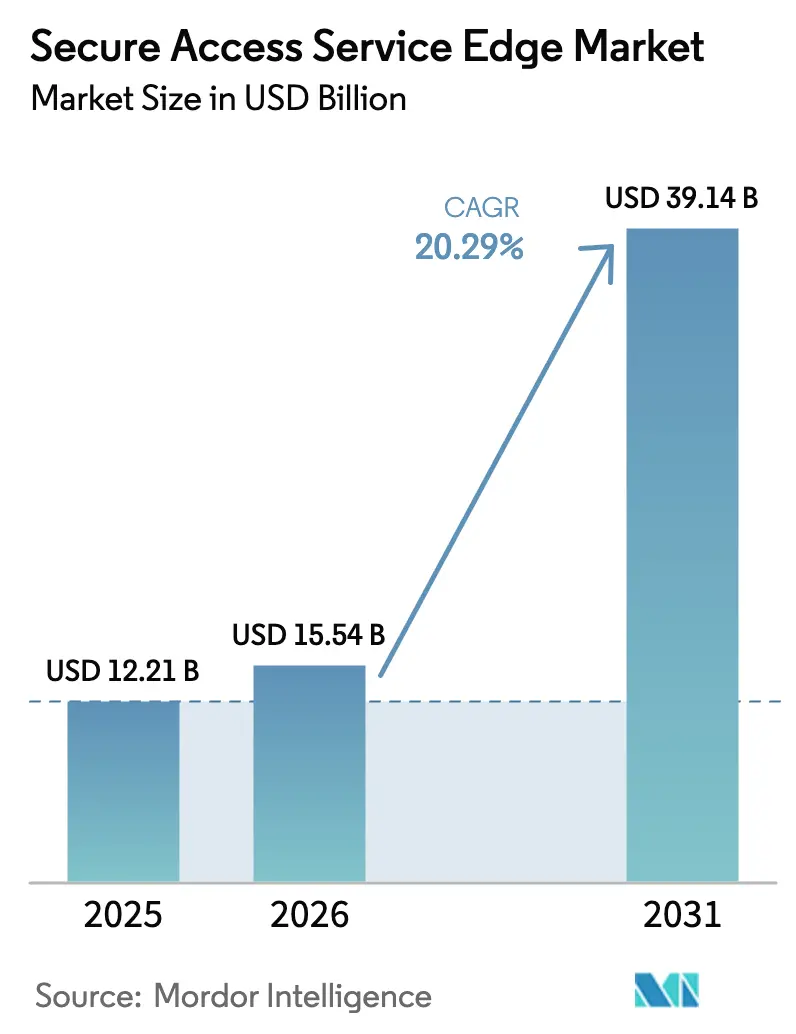

The secure access service edge market size is expected to increase from USD 12.21 billion in 2025 to USD 15.54 billion in 2026 and reach USD 39.14 billion by 2031, growing at a CAGR of 20.29% over 2026-2031. The outlook is fueled by enterprises decommissioning hub-and-spoke networks, adopting cloud-native convergence, and integrating software-defined wide-area networking with zero-trust security controls. Large technology mergers, expanding 5G rollout, and sovereign-cloud mandates are accelerating vendor investment while managed service providers bundle turnkey subscriptions that lower capital costs. Latency-sensitive industries such as financial services push silicon-based inspection, whereas data-sensitive sectors demand in-country points of presence, shaping product roadmaps across the Secure Access Service Edge (SASE) market. Vendor competition now hinges on automated policy engines, sub-50-millisecond latency guarantees, and bundled threat intelligence that trims security-operations workloads.

Key Report Takeaways

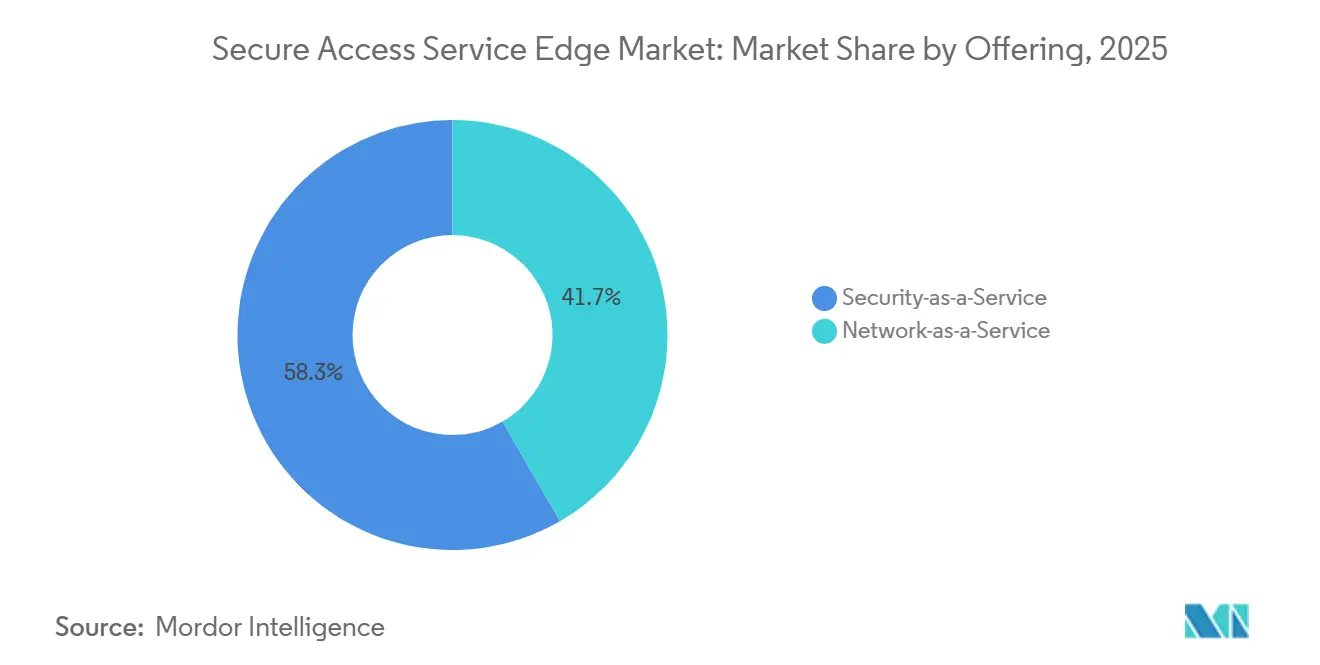

- By offering, Security-as-a-Service led with 58.34% of the secure access service edge market share in 2025, while Network-as-a-Service is forecast to expand at a 20.63% CAGR through 2031.

- By deployment mode, Cloud-Native SASE commanded a 67.53% share in 2025, whereas Hybrid SASE is projected to grow at a 20.81% CAGR to 2031.

- By organization size, large enterprises contributed 63.14% of 2025 revenue, yet small and medium-sized enterprises are expected to post a 20.66% CAGR through 2031.

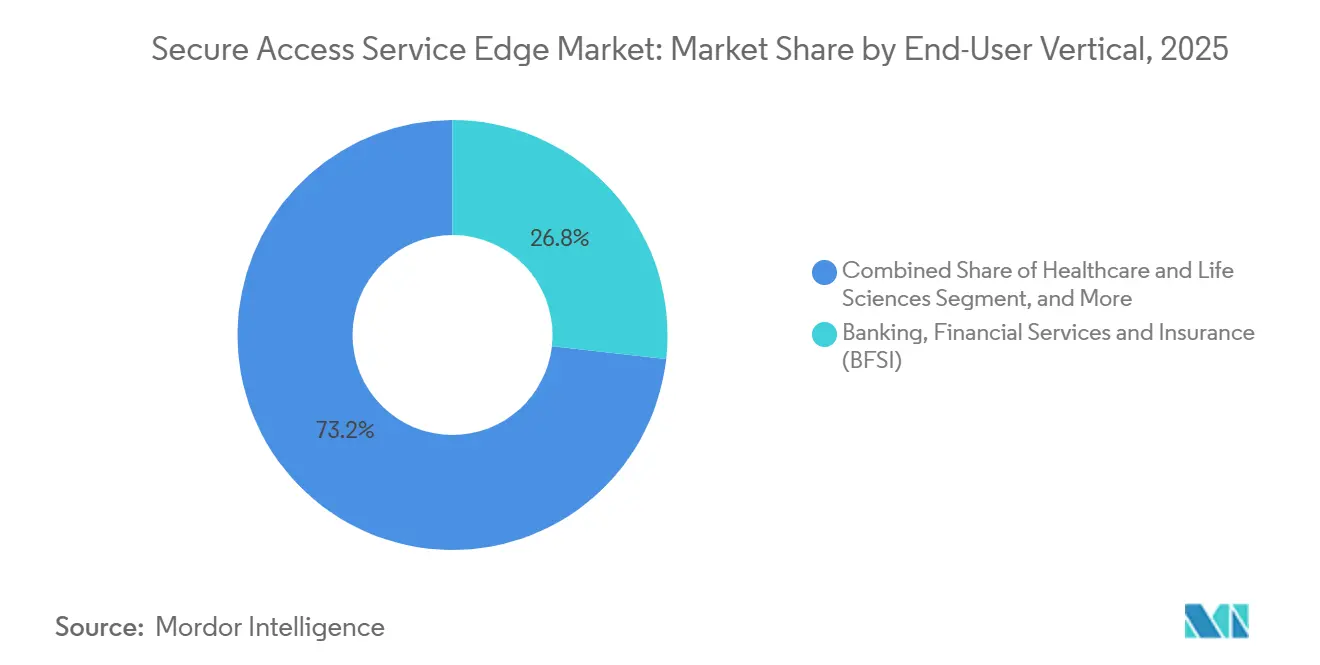

- By end-user vertical, banking, financial services, and insurance led with 26.78% of the secure access service edge (SASE) market share in 2025; healthcare and life sciences will accelerate at a 21.69% CAGR to 2031.

- By access channel, remote and mobile users held 47.91% of the SASE market share in 2025, whereas IoT and edge devices are positioned for a 20.87% CAGR through 2031.

- By geography, North America accounted for 39.76% of 2025 revenue, and Asia-Pacific will deliver the fastest 21.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Secure Access Service Edge Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convergence of SD-WAN, FWaaS, SWG, CASB and ZTNA into a Unified Cloud-Native Stack | +4.2% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Surge in Remote and Hybrid Workforce Post-2025 | +3.8% | Global, particularly North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Growing MSSP Adoption of Turnkey SASE Offerings | +3.1% | North America, Europe, with spillover to Latin America and Middle East | Medium term (2-4 years) |

| Increasing Sovereign-Cloud and Data Residency Mandates in Europe and Asia-Pacific | +3.5% | Europe, China, India, Southeast Asia, with emerging requirements in the Middle East | Long term (≥ 4 years) |

| Integration of eSIM-Native Zero-Trust SASE for Cellular IoT Fleets | +2.4% | Asia-Pacific manufacturing hubs, North America automotive, Europe industrial | Long term (≥ 4 years) |

| Chip-Level Security Offload (SmartNIC / DPU) Enabling Inline Inspection at 100 Gbps+ | +2.9% | Global, concentrated in financial services and hyperscale cloud regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convergence Of SD-WAN, FWaaS, SWG, CASB, And ZTNA Into A Unified Cloud-Native Stack

Enterprises are folding five once-separate controls into a single SASE fabric to eliminate console sprawl and policy drift, a shift that Gartner found lowers ongoing network security operating costs by 40%. With everything in one policy engine, a phishing alert in the secure web gateway can now trigger instant session revocation at the cloud-access broker and device quarantine without custom scripts, tightening the response loop to seconds.[1]PCI Security Standards Council, “PCI DSS v4.0,” pcisecuritystandards.org Vendors accelerate adoption through hyperscale alliances; Palo Alto Networks and Google Cloud pre-provision SASE nodes at the edge, enabling customers to enable micro-segmentation via APIs instead of hardware procurement, cutting rollout time from months to days. Financial institutions lead uptake because PCI DSS v4.0 demands continuous, segment-wide monitoring that multi-vendor stacks struggle to audit. As unified platforms mature, they add machine-learning policy recommendations that translate intent into rules, shrinking administrative effort for already-stretched security teams.

Surge In Remote And Hybrid Workforce Post-2025

Remote work is locked in at roughly one-third of OECD employment by 2025, dissolving the fixed perimeter that VPNs once guarded.[2]International Labour Organization, “World Employment and Social Outlook 2025,” ilo.org SASE enforces identity-centric rules regardless of network, so staff can connect from home broadband or 5G hotspots without backhauling traffic to a data center. Netskope’s agentless DLP scans SaaS uploads in real time, proving that security can run invisibly without eroding user experience. The U.S. Centers for Medicare & Medicaid Services reported a 63% jump in virtual visits between 2024 and 2025, forcing hospitals to secure clinicians’ personal devices under HIPAA. Enterprises also closed regional data centers and routed traffic directly to cloud points of presence, trimming WAN spend by more than one-third while improving SaaS latency.

Growing MSSP Adoption Of Turnkey SASE Offerings

Managed security service providers bundle SASE with 24-hour monitoring and incident response, giving mid-market firms enterprise-grade controls without staffing a security operations center. AT&T’s partnership with Palo Alto Networks lets the carrier resell Prisma SASE alongside 5G connectivity, monetizing network slices through security value rather than bandwidth pricing. Multi-tenant orchestration enables a single MSSP team to manage hundreds of customer tenants from a single console, driving economies of scale that push subscription prices below traditional firewall refresh costs. Cato Networks said 42% of its 2025 bookings came through channel partners, up from 28% a year earlier, underscoring reseller momentum. Rapid activation, often two weeks from purchase order to production, makes turnkey SASE a preferred option for mergers that must unify networks under strict regulatory deadlines.

Increasing Sovereign-Cloud And Data Residency Mandates In Europe And Asia-Pacific

Mounting localization rules force vendors to deploy inspection nodes inside national borders and escrow keys locally, turning compliance into a primary growth engine. The European Union’s Data Act now obliges cloud providers to demonstrate that foreign governments cannot compel the disclosure of EU resident data, spurring demand for SASE platforms with in-region key custody.[3]European Central Bank, “Outsourcing Guidelines for Credit Institutions,” ecb.europa.eu China’s amended Cybersecurity Law requires critical information infrastructure operators to store personal and sensitive business data onshore, prompting multinationals to run dual SASE fabrics, one for China and another for the rest of the world. India’s Digital Personal Data Protection Act sets similar constraints and ties violations to 2% of global turnover, accelerating uptake of locally hosted SASE points of presence. Saudi Arabia’s Vision 2030 earmarks USD 6.4 billion for sovereign zones, rewarding vendors that partner with domestic carriers to meet in-country processing mandates. These statutes convert regional compliance budgets into recurring SASE subscriptions, creating durable, regulation-anchored demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| In-Line Security Latency for Real-Time Applications | -1.8% | Global, acute in financial trading hubs and Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Shortage of Skilled SASE Architects and Operators | -1.6% | Global, most severe in North America and Western Europe | Medium term (2-4 years) |

| Escalating Egress Fees From SaaS Providers for Hyperscale Inspection Workloads | -1.3% | Global, concentrated in multi-cloud enterprises | Short term (≤ 2 years) |

| Proprietary Policy Languages Hindering Multi-Vendor Orchestration | -1.1% | Global, particularly affecting large enterprises with heterogeneous stacks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

In-Line Security Latency For Real-Time Applications

Deep-packet inspection and TLS decryption add 12-35 milliseconds of delay to encrypted traffic, a margin that high-frequency traders reject because microseconds matter for profit. Fortinet counters the drag by embedding NVIDIA BlueField-3 DPUs that offload inspection at 100 Gbps without taxing the CPU, but the hardware premium runs 40-60% above software-only gear. Even with silicon assist, enterprises in Asia-Pacific see congestion at cross-border exchanges that doubles end-to-end delay, so factories often bypass SASE for time-critical control lines. Cloud-native providers try to solve this with 300-plus global points of presence, yet each site needs constant capital infusion, limiting how far edge density can scale. Until inspection overhead falls below application thresholds, latency will restrain deployment in voice, video, and algorithmic trading workloads.

Shortage Of Skilled SASE Architects And Operators

The convergence of routing, cloud automation, and zero-trust security demands a talent mix in short supply. ISC2 estimated a 4.1 million-person global cybersecurity gap in 2025, with SASE roles among the hardest to fill because formal curricula lag product rollout. Fewer than 8,000 professionals worldwide held Palo Alto Networks’ specialist certification by mid-2025, far fewer than the 50,000 live deployments the vendor reported. Median salaries for SASE architects in North America hit USD 145,000 in 2025, 22% above traditional network engineer pay, inflating service providers' operating costs. The 12-to-18-month learning curve delays project value and nudges many mid-market firms toward managed services, reinforcing channel concentration and limiting customization flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Security Functions Dominate, Yet Connectivity Gains Momentum

The Secure Access Service Edge market share for Security-as-a-Service reached 58.34% in 2025, reflecting enterprise emphasis on threat prevention and data-loss controls. Financial institutions drove uptake because audits scrutinize encryption and anomaly detection more intensely than uptime. Over the forecast horizon, Network-as-a-Service is projected to post the swiftest 20.63% CAGR, propelling the SASE market as internet-based transport replaces MPLS circuits and as path-selection analytics become integral to performance tuning.

Branch consolidation also lifts network modules, as organizations close regional hubs and rely on dynamic route optimization to maintain SaaS responsiveness. Retail groups illustrate that checkout latency directly ties to customer satisfaction, so chain owners prioritize intelligent path steering even when security modules run silently in the background. Vendors that fuse deep path visibility with zero-trust policy orchestration win budget from both infrastructure and security teams, blurring the historical separation within the Secure Access Service Edge industry.

By Deployment Mode: Cloud-Native Architectures Lead, Hybrid Models Accelerate

Cloud-Native SASE captured a 67.53% share in 2025 and continues to attract greenfield adopters who skipped appliance-based firewalls entirely. Multi-tenant clouds handle millions of concurrent connections and remove customer maintenance overhead, reinforcing the Secure Access Service Edge market trajectory. Nevertheless, heavily regulated sectors turn to Hybrid SASE, forecast to grow at a 20.81% CAGR, to meet residency requirements while preserving centralized control.

European banks typically keep payment processing on-premises while forwarding web and SaaS traffic to cloud inspection nodes, balancing latency with compliance. Policy portability remains crucial, so platforms that support gradual migration without rewriting rules differentiate. Latency remains the deciding factor: cloud equalizes email and collaboration performance, but voice and video often require local inspection, sustaining demand for hybrid flexibility across the SASE market.

By Organization Size: Enterprises Dominate Spending, SMEs Drive Volume Growth

Large enterprises generated 63.14% of 2025 revenue because sprawling branch footprints and layered compliance obligations yield contract values in the multimillion-dollar range. These buyers need bespoke integrations with legacy security information and event management tools, which will contribute to sustained services revenue in the Secure Access Service Edge market. In contrast, small and medium-sized enterprises will register the fastest 20.66% CAGR through 2031, as managed service providers offer user-based monthly subscriptions that eliminate the need for hefty appliance purchases, broadening the addressable market.

Turnkey activation enables SMEs to deploy in weeks instead of quarters, a crucial advantage for professional services firms that swiftly adapt to client demands. This rapid deployment capability allows SMEs to remain competitive and responsive in dynamic market conditions. However, with a higher churn rate in this group, vendors are compelled to automate policy tuning and threat responses. These automation efforts aim to streamline operations, manage support costs, and maintain profitability while safeguarding margins in the SASE market.

By End-User Vertical: Financial Services Lead, Healthcare Surges

Financial institutions retained 26.78% of 2025 spending as payment regulators enforced zero-trust segmentation across every network segment. High-frequency traders additionally demand silicon-accelerated inspection to limit microsecond delays, pushing vendors toward DPU integration. Healthcare and life sciences post the briskest 21.69% CAGR through 2031, expanding the SASE market size for clinical workloads that synchronize electronic records and enable telehealth under HIPAA scrutiny.

Other verticals rise for distinct triggers, retail braces against supply-chain attacks, telecommunications operators embed SASE into 5G slices, and manufacturing pilots OT-aware policies that shield legacy plant networks. Government adoption remains deliberate due to procurement cycles, yet federal zero-trust mandates set 2027 deadlines, suggesting a steep ramp-up mid-forecast across the Secure Access Service Edge market.

By Access Channel: Remote Users Dominate, IoT Devices Emerge

Remote and mobile employees produced 47.91% of channel revenue in 2025, demonstrating how hybrid work hardwired zero-trust policy enforcement into daily operations. Branch offices are slow but still matter for regional support and inventory hubs. IoT and edge devices will drive a 20.87% CAGR, adding billions of authentication events to the SASE market as factories and autonomous vehicles embed eSIM-linked identities that bypass VPN overhead.

As a single plant hosts tens of thousands of sensors, platforms designed for human-user ratios become overwhelmed, surfacing scaling challenges. These challenges arise from the sheer volume of data generated by the sensors, which can strain traditional systems and hinder efficient management. In response, vendors leverage AI-driven grouping to cluster devices by behavior. This approach not only alleviates administrator fatigue by simplifying device management but also upholds least-privilege controls, ensuring robust security measures are maintained in the Secure Access Service Edge market.

Geography Analysis

North America maintained a commanding position by combining stringent federal compliance frameworks with abundant venture capital that de-risks aggressive product innovation. Public cloud providers secured FedRAMP authorizations, which drew federal agencies and defense contractors into early production pilots. Silicon-accelerated inspection gained popularity on Wall Street trading floors where microseconds define earnings. Managed service providers in the United States expanded channel reach by integrating SASE into 5G business bundles, fostering steady renewal cycles in the SASE market.

Asia-Pacific’s outlook brightens as China’s cybersecurity amendments and India’s data protection act insist upon in-country processing, compelling multinationals to build sovereign fabrics. Domestic champions such as Huawei and Tata Communications leverage regulatory familiarity to secure national projects, while U.S.-headquartered providers partner with regional data center operators to address compliance gaps. Rapid 5G expansion and mobile-first business models in Southeast Asia underpin resilient demand, keeping Asia-Pacific at the forefront of Secure Access Service Edge market growth.

Europe balances cautious procurement with progressive legislation aimed at digital sovereignty. The Data Act binds providers to strict disclosure controls, driving adoption among enterprises that must evidence compliance to auditors. Nordic countries emphasize renewable-energy-powered data centers, aligning with corporate sustainability commitments and luring inspection workloads to local points of presence. Rising cyberinsurance premiums further motivate continental businesses to deploy unified zero-trust frameworks, supporting the gradual expansion of the Secure Access Service Edge market across member states.

Competitive Landscape

The top five vendors, Palo Alto Networks, Zscaler, Cisco Systems, Fortinet, and Cloudflare, together accounted for about 42% of cloud-native deployments in 2025, indicating moderate concentration in the Secure Access Service Edge market. Strategic acquisitions intensified, including Palo Alto Networks' purchase of identity assets to natively embed privileged-access management and Cisco Systems' integration of security analytics at a USD 28 billion scale. Disruptors such as Cato Networks and Versa Networks leverage multi-tenant orchestration to underprice hardware-centric incumbents by up to 40%, winning managed service provider deals.

Technology differentiation now centers on AI-driven policy automation, edge density that caps latency below 50 milliseconds, and silicon offload for encrypted traffic at 100 gigabits per second. Vendors also align go-to-market strategies along vertical lines. Fortinet builds OT-aware modules for manufacturing, while Proofpoint focuses on email security in financial institutions. Pricing pressure mounts as channel partners negotiate steep volume discounts, compelling smaller players to consolidate or specialize in niches within the SASE industry.

The U.S. National Institute of Standards and Technology updated its zero-trust reference in 2024, enabling buyers to benchmark architectures independently of vendor marketing. That transparency lowers switching friction, amplifying competitive urgency. Overall, the ecosystem blends broad-platform giants, regional specialists, and function-focused challengers, each racing to lock in contracts before regulatory mandates make SASE compulsory across late-adopting sectors.

Secure Access Service Edge Industry Leaders

Akamai Technologies, Inc.

Broadcom Inc.

Check Point Software Technologies Ltd.

Cisco Systems, Inc.

Fortinet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Palo Alto Networks partnered with Google Cloud to embed Prisma SASE into distributed edge nodes, reducing deployment times from weeks to hours.

- November 2025: Palo Alto Networks acquired Chronosphere to integrate real-time observability metrics into dynamic security policy adaptation.

- April 2025: AT&T launched a strategic alliance with Palo Alto Networks, bundling Prisma SASE with 5G slices under the AT&T Cybersecurity label.

- April 2025: Netskope debuted DLP On Demand, an agentless data-loss prevention service that scans SaaS uploads in real time.

Global Secure Access Service Edge Market Report Scope

The Secure Access Service Edge (SASE) Report is Segmented by Offering (Network-as-a-Service (NaaS), and Security-as-a-Service (SECaaS)), Deployment Mode (Cloud-Native SASE, Hybrid SASE, On-Premise/Legacy-Integrated SASE), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises (SMEs)), End-User Vertical (Banking, Financial Services and Insurance (BFSI), Information Technology and Telecom, Retail and E-Commerce, Healthcare and Life Sciences, Government and Public Sector, Manufacturing and Industrial, Other End-User Verticals), Access Channel (Remote/Mobile Users, Branch Offices, IoT and Edge Devices), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Network-as-a-Service (NaaS) |

| Security-as-a-Service (SECaaS) |

By Deployment Mode

| Cloud-Native SASE |

| Hybrid SASE |

| On-Premise / Legacy-Integrated SASE |

By Organization Size

| Large Enterprises |

| Small and Medium-Sized Enterprises (SMEs) |

By End-User Vertical

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecom |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Manufacturing and Industrial |

| Other End-User Verticals |

By Access Channel

| Remote / Mobile Users |

| Branch Offices |

| IoT and Edge Devices |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Offering | Network-as-a-Service (NaaS) | ||

| Security-as-a-Service (SECaaS) | |||

| By Deployment Mode | Cloud-Native SASE | ||

| Hybrid SASE | |||

| On-Premise / Legacy-Integrated SASE | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises (SMEs) | |||

| By End-User Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| Information Technology and Telecom | |||

| Retail and E-Commerce | |||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| Manufacturing and Industrial | |||

| Other End-User Verticals | |||

| By Access Channel | Remote / Mobile Users | ||

| Branch Offices | |||

| IoT and Edge Devices | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the Secure Access Service Edge market in 2031?

The Secure Access Service Edge market is forecast to reach USD 39.14 billion by 2031.

Which deployment mode is growing fastest in Secure Access Service Edge solutions?

Hybrid SASE is expected to post a 20.81% CAGR through 2031 as regulated sectors bridge on-premise controls with cloud points of presence.

Why are managed service providers pivotal to Secure Access Service Edge adoption among SMEs?

MSPs bundle turnkey SASE subscriptions that eliminate hardware spending and provide 24-hour monitoring, enabling SMEs to deploy within weeks.

How do data-residency mandates influence Secure Access Service Edge vendor strategy?

Sovereign-cloud laws require in-country inspection nodes and local key escrow, prompting vendors to partner with regional telecom operators and build localized fabrics.

What technologies address latency concerns in high-speed trading environments?

Vendors integrate data processing units that offload TLS decryption and deep-packet inspection, sustaining 100 Gbps throughput without adding excessive delay.

Page last updated on: