North America Saffron Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

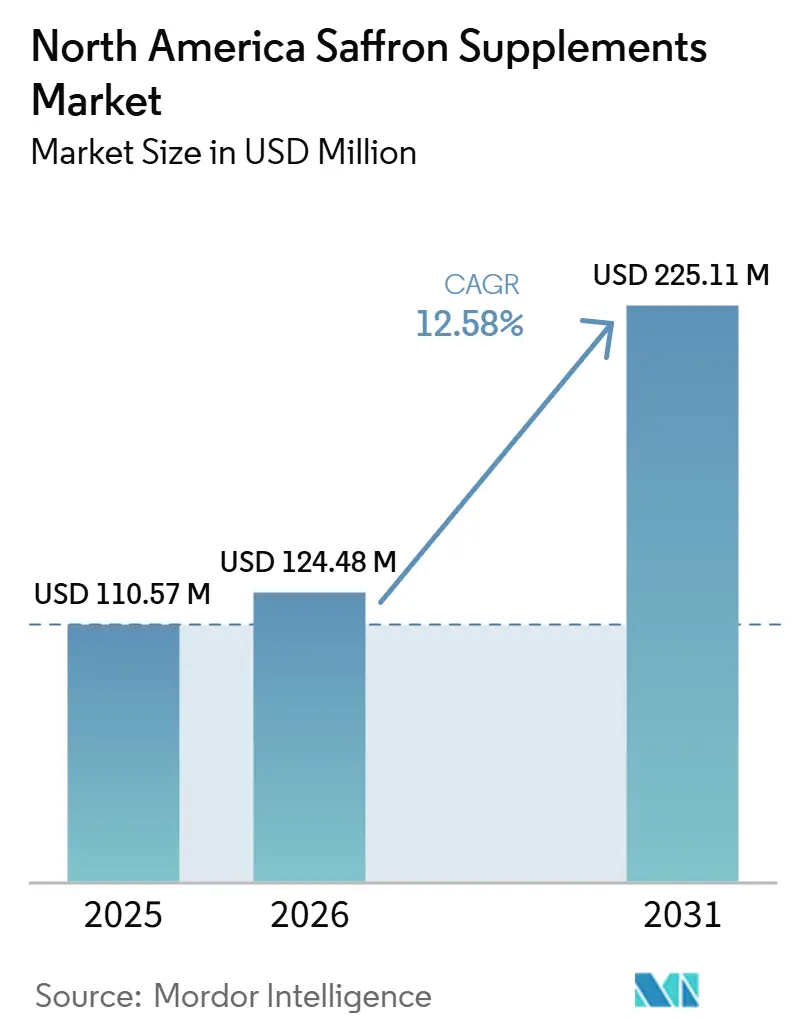

| Base Year Market Size (2025) | USD 110.57 Million |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 124.48 Million |

| Market Size (2031) | USD 225.11 Million |

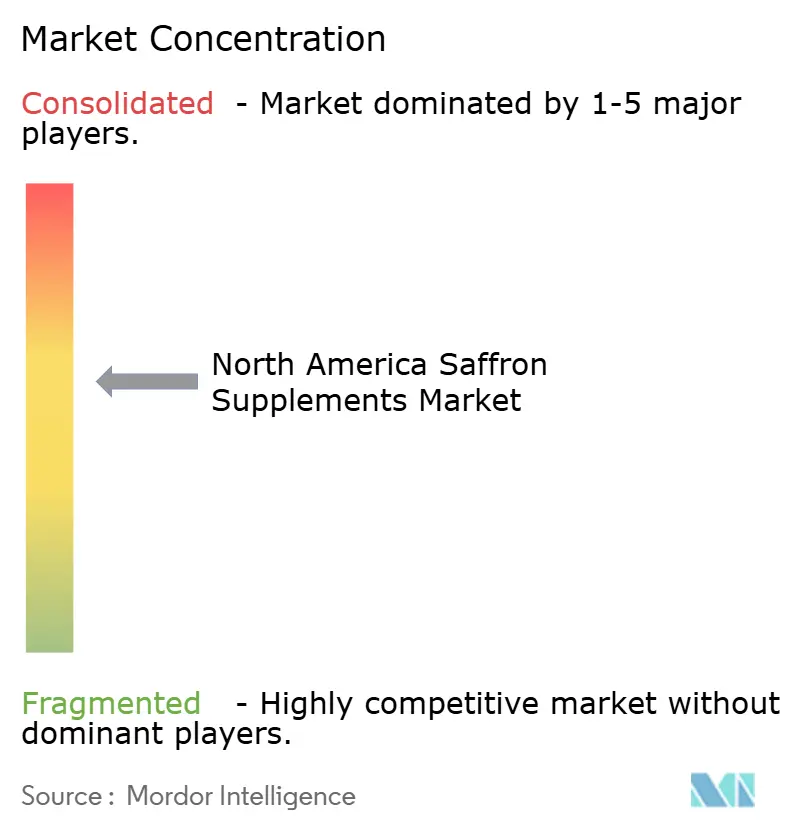

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Saffron Supplements Market Analysis by Mordor Intelligence

The North American saffron supplements market size is expected to grow from USD 110.57 million in 2025 to USD 124.48 million in 2026, and is forecast to reach USD 225.11 million by 2031 at a 12.58% CAGR over 2026-2031. Sustained validation of saffron’s mood-health benefits, rising premium positioning through organic labels, and new delivery formats such as functional gummies underpin this growth. Wider FDA authentication protocols and high-crocin extracts support brand claims, while local greenhouse projects shorten lead times and reduce spoilage. Manufacturers still grapple with Iran-centric supply chain risks, yet long-term contracts and diversified sourcing help temper volatility. Consumer-facing brands are simultaneously educating on saffron’s gut-brain pathway and bundling the botanical with complementary nutrients to capture higher average order values.

Key Report Takeaways

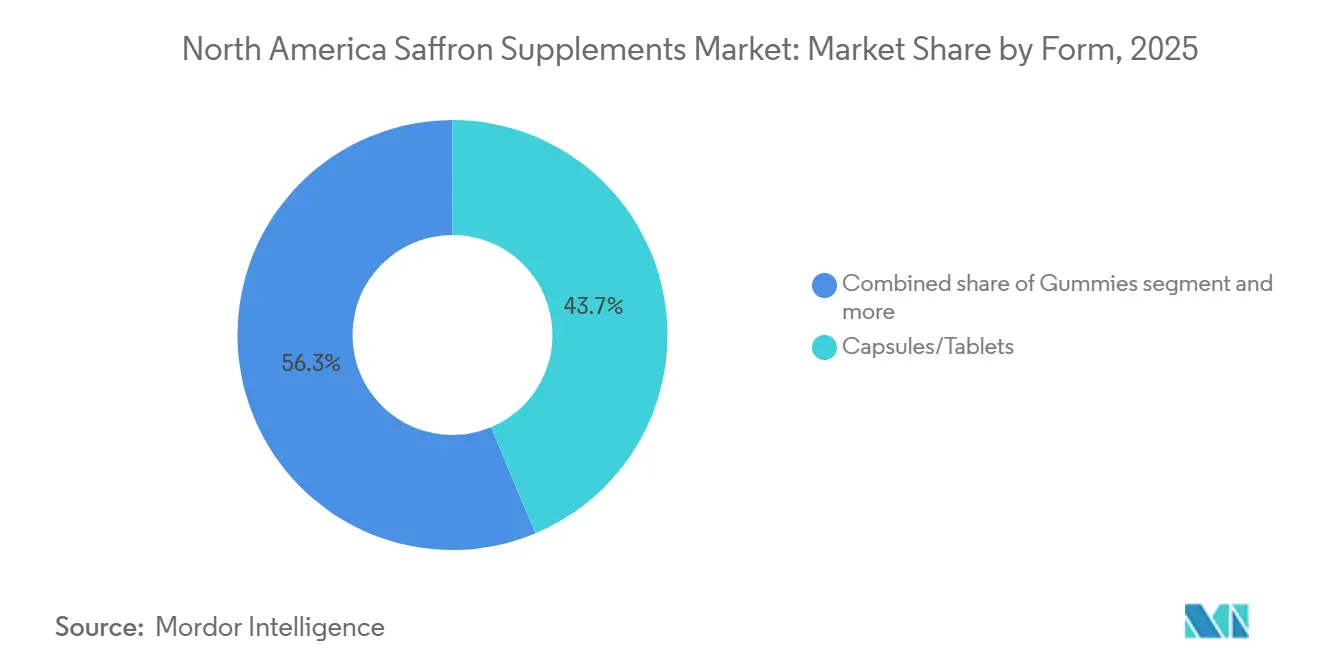

- By form, capsules and tablets accounted for 43.70% of the North America saffron supplements market share in 2025. Gummies are forecast to grow at a 13.08% CAGR to 2031, the fastest among delivery formats.

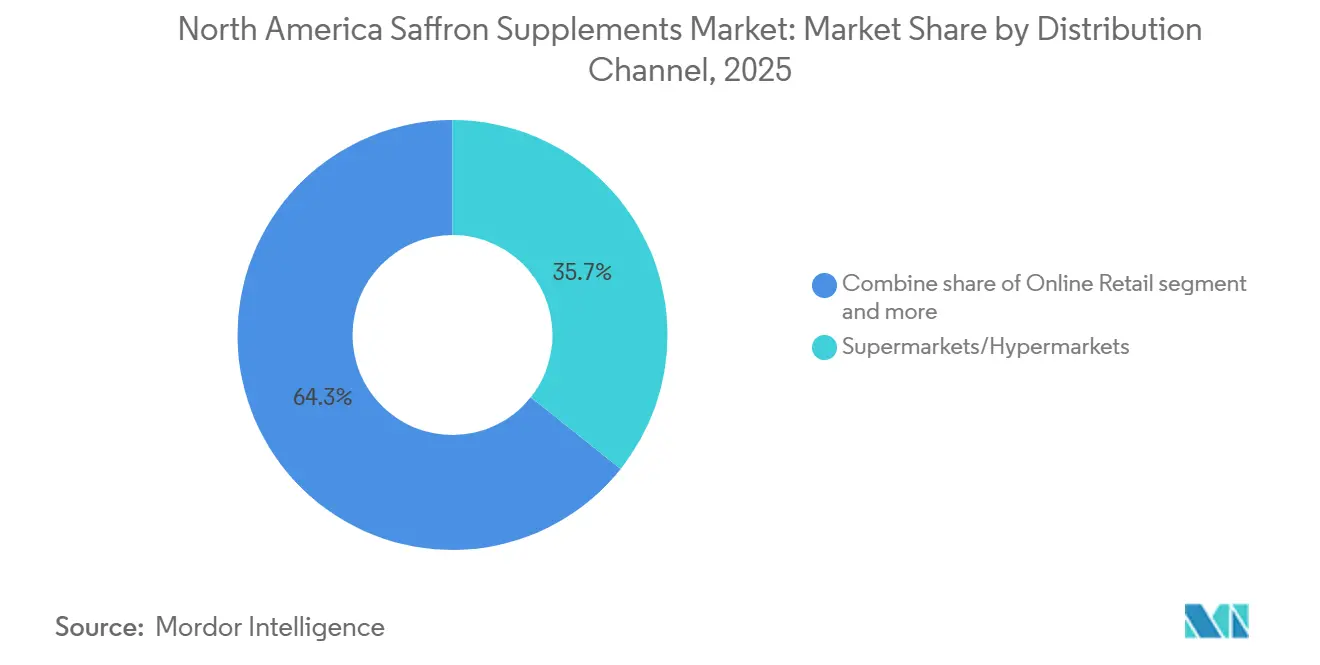

- By distribution channel, supermarkets and hypermarkets accounted for 35.66% of the North America saffron supplements market in 2025, while online retail is expected to expand at a 14.41% CAGR through 2031.

- By geography, the United States led with 77.96% revenue share in 2025, whereas Mexico is expected to post a 13.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Saffron Supplements Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for clinically validated botanical mood enhancers | +2.8% | United States, Canada, Mexico City | Medium term (2-4 years) |

| Premium positioning via organic and fair-trade traceability | +1.9% | United States, Canada coastal markets | Long term (≥4 years) |

| Expansion of plant-extract functional gummies | +2.5% | United States, Canada urban youth, Mexico emerging | Short term (≤2 years) |

| Domestic greenhouse cultivation lowering lead-times | +1.4% | Canada western provinces, southern United States | Long term (≥4 years) |

| FDA saffron authenticity protocol MPM V-8-D | +1.7% | United States with spill-over to Canada and Mexico | Medium term (2-4 years) |

| High-crocin extracts enabling smaller doses | +1.6% | North America ingredient supply chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clinically validated botanical mood enhancers

Since 2024, multiple randomized controlled trials have shown that daily doses of 28–30 mg saffron extract produce statistically significant improvements in mild-to-moderate depression, comparable in efficacy to fluoxetine but with fewer sexual side effects. Integrative psychiatrists now recommend saffron alongside therapy sessions, while naturopathic practitioners use it as a gentle, entry-level alternative for patients hesitant to try conventional medications. The gut-brain connection, where crocin metabolites influence microbiota and the kynurenine pathway, appeals to wellness-focused consumers seeking evidence-backed botanicals rather than anecdotal remedies. Pharmactive’s Affron, supported by 13 peer-reviewed studies, enables co-branded finished products to reference these trials without incurring the costs of in-house research. Short study durations, however, mean long-term safety data remain limited, prompting leading brands to develop post-market surveillance platforms that monitor adverse events in real-world use.

Premium positioning via organic and fair-trade traceability programs

USDA National Organic Program rules permit saffron extract to be included in fully certified formulas, allowing finished products to carry the organic seal and command price premiums 15-20% higher[1]Source: U.S Food and Drug Administration, "Method for the Determination of Saffron in Botanical Dietary Supplements (MPM V-8-D)", fda.gov. Lonza’s 2025 Organicaps pullulan capsule overcomes previous limitations, where gelatin and HPMC shells previously interrupted the organic chain, providing brands with a fully compliant organic pipeline in line with Capsugel, Inc. standards. Fair-trade initiatives in Afghanistan and Kashmir provide compelling social responsibility narratives, appealing to consumers who associate ethical sourcing with product quality. Blockchain tracking systems capture farm-to-capsule data, which retailers increasingly require as part of their due diligence checks. Supply remains constrained, as less than 5% of Iran’s saffron acreage meets organic standards, forcing brands to balance premium positioning with limited availability and rising costs.

Expansion of plant-extract functional gummies category

Gummy searches grew 50% year over year in 2024, with creatine gummies alone spiking 1,300% in hits, highlighting a broader shift toward candy-like supplement formats, according to the Vitamin Shoppe[2]Source: Vitamin Shoppe, "2024 Supplement Trends Report", vitaminshoppe.com. Saffron’s inherent bitterness once limited the adoption of gummies, but modern pectin formulations now mask the flavor while preserving crocin’s vibrant color. Brands leverage this by offering 10–15 mg of saffron per gummy, marketing it for daily mood support rather than acute therapy, avoiding strict FDA claim requirements. Contract manufacturers have also implemented nitrogen-flushed production lines that maintain crocin oxidation at under 5% over 18 months, thereby extending shelf life well beyond the previous 12-month limit. Meanwhile, sugar-conscious consumers are driving a second wave of reformulation, utilizing allulose or erythritol, which increases production costs but enables keto-friendly positioning.

FDA saffron authenticity protocol MPM V-8-D

The April 2024 HPLC protocol standardizes testing for crocin, picrocrocin, and safranal across third-party laboratories, closing previous gaps that allowed adulterated batches to slip through. Retailers such as CVS now require compliance with this method for shelf placement, prompting lagging brands to upgrade their quality control systems. Its alignment with ISO 3632 also reduces the need for duplicate tests when products enter Canada, resulting in up to a 15% reduction in analytical costs. In December 2025, Amazon introduced a USP-verified fast-track program, giving products that meet testing standards higher visibility in search results[3]Source: Amazon, USP Verified Supplement Fast-Track Program", amazon.com. Smaller suppliers, however, often face longer queues at accredited labs, as demand for HPLC testing surges toward year-end, extending turnaround times and increasing costs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent raw-material price volatility from Iran supply | -1.8% | Global importers, acute in North America | Short term (≤2 years) |

| Adulteration risk increasing testing overheads | -1.2% | United States, Canada, Mexico emerging | Medium term (2-4 years) |

| 2025 U.S. tariffs on solvent-based extracts | -0.9% | United States brands, minimal Canada impact | Short term (≤2 years) |

| Limited consumer awareness beyond mood benefits | -1.4% | North America mass market | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Persistent raw-material price volatility from Iran supply

Iran accounts for nearly 90% of the world’s saffron production; however, droughts and shifts in export policy can cause spot prices to fluctuate from USD 1,200 to USD 1,650 per kilogram within just a few months. Importers are often forced to maintain larger safety stocks, which ties up capital and compresses profit margins. Alternative sources from Afghanistan and Spain are priced 40-60% higher than Iranian saffron and are limited by their constrained production capacity. Vertical integration initiatives in places like New Jersey and Kashmir provide some cushioning, but reaching commercial scale is still three to five years away. With no futures or options markets for saffron, buyers must either absorb price volatility themselves or negotiate variable-rate contracts with suppliers.

Adulteration risk increasing, analytical-testing overheads

The market value of saffron is frequently undermined by the inclusion of safflower stigmas, turmeric powder, or synthetic dyes that replicate the hue of crocin. While ISO 3632 defines minimum content standards, more sophisticated adulterants, such as gardenia extract, can bypass simple UV tests, forcing brands to use LC-MS/MS in conjunction with HPLC for accurate verification. Each additional test adds approximately USD 300–500 to batch costs and delays the release timeline. Smaller companies without in-house laboratories often rely on contract testing facilities, which can experience backlogs extending beyond the typical 10-day turnaround during peak harvesting periods. DNA barcoding offers an additional layer of protection, and the American Herbal Products Association provides guidance; however, adherence to these protocols is voluntary, leaving room for less ethical importers to maintain cost advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Gummies Capture Growth While Capsules Retain Core Trust

In 2025, capsules and tablets remained the largest segment of the North American saffron supplements market, accounting for a 43.70% share, driven by consumer trust in precise dosing. This format provides high bioactive stability through oxygen-barrier shells and meets expectations for reliable medicinal delivery. Contract manufacturers often use enteric coatings to protect crocin from gastric fluids, ensuring absorption in the small intestine. Capsules also avoid sugar-related warnings under federal and state labeling laws, an increasingly important advantage as regulators tighten front-of-pack disclosures.

However, sales momentum is shifting toward gummies, which are projected to see the fastest CAGR of 13.08% through 2031, as younger consumers favor taste and convenience over traditional pills. Brands leverage smaller 10–15 mg doses to support daily mood balance without crossing therapeutic claim boundaries, while bright flavorings mask picrocrocin’s natural bitterness. Flavor houses blend berry and citrus notes that complement crocin’s color and enhance visual appeal. Sugar-free formulations using allulose or erythritol target keto and diabetic consumers, though production costs rise 20–30%. Liquids and powders serve niche markets for consumers mixing saffron with adaptogens in shakes, while innovative formats such as transdermal patches and lozenges remain experimental pending dermal absorption studies.

By Distribution Channel: Online Retail Accelerates Disintermediation

Supermarkets and hypermarkets accounted for 35.66% of the North American saffron supplements market, driven by impulse purchases and the integration of wellness sections. Strategic placement near sleep aids and functional teas encourages cross-category buying, while weekly promotions attract deal-focused shoppers. However, foot traffic growth has plateaued as consumers increasingly seek personalized digital experiences. To keep pace, physical stores are incorporating QR codes that link to clinical study summaries, aiming to replicate the depth of information available online.

Meanwhile, online retail is projected to grow at a 14.41% CAGR through 2031, outpacing all brick-and-mortar formats. Amazon’s USP-verified fast-track boosts visibility for tested products, driving higher click-through rates for compliant brands. Direct-to-consumer platforms utilize subscription bundles to enhance customer lifetime value and minimize churn. Personalization quizzes that align mood profiles with product strength have been shown to increase basket size by 25%, according to vendor dashboards. Pharmacies and specialty stores remain relevant for older consumers seeking pharmacist guidance, while practitioner dispensaries in naturopathic offices capture premium margins but grow slowly due to limited accreditation programs.

Geography Analysis

The United States dominated the region in 2025, accounting for 77.96% of North American saffron supplements revenue, supported by high per-capita supplement spending and a mature omnichannel retail landscape. The FDA’s saffron-specific testing protocol has eased authenticity concerns, prompting national chains like CVS to expand shelf space and approve larger order volumes. Amazon’s verification program adds another layer of trust to online listings, translating quality investments into greater algorithm-driven visibility. Regulatory complexity persists at the state level; however, California’s Proposition 65 extends to gummy excipients, and New York mandates disclosures of trace contaminants. To manage this variability, brands are increasingly relying on centralized compliance systems that can generate shipment-specific labels.

Canada saffron supplements market is driven by the credibility conferred by Natural Health Product Numbers. Apotex’s 2025 acquisition of CanPrev combined pharmaceutical-scale distribution with natural health expertise, expanding saffron offerings into 3,400 retail locations and strengthening pharmacist engagement. Domestic greenhouse cultivation has shortened lead times from months to weeks and enabled local sourcing claims, which resonate with the 73% of Canadian consumers who prioritize organic ingredients, according to Capsugel data. Practitioner channels remain particularly strong, as naturopathic doctors are authorized to prescribe botanicals, supporting higher per-unit pricing.

Mexico is the fastest-growing market, projected to expand at a 13.92% CAGR through 2031, as a growing middle class seeks natural wellness solutions within a retail sector valued at CAD 23.9 billion, according to Agriculture and Agri-Food Canada. COFEPRIS recognition of U.S. and Canadian regulatory dossiers reduces approval timelines by roughly 40%, easing market entry for multinational brands. At the same time, front-of-pack sugar warnings under NOM-051 favor capsule formats that avoid sweetener disclosures, limiting gummy adoption. Retail concentration in major urban centers pushes brands to partner with pharmacy chains and health-food stores to reach rural consumers, while influencer-led social commerce introduces saffron education to digitally engaged shoppers.

Competitive Landscape

The North America saffron supplements market shows moderate concentration. Legacy nutraceutical houses such as Life Extension, NOW Health Group, Nature’s Way, and Swanson Health Products combine scale purchasing power with retail volume agreements. Ingredient-branded suppliers add competitive layers; Pharmactive’s saffron and Activ’Inside’s Safr’Inside feature trademarked extraction and clinical dossiers that lift brand awareness in crowded digital marketplaces. Saffron Health Sciences widens domestic processing capacity, supplying 75% crocin extract for smaller dose sizes and avoiding import duties.

Strategic moves cluster around vertical integration, scientific validation, and omnichannel expansion. Saffron Health Sciences’ New Jersey plant enables “Made in USA” labeling that fetches 10–15% higher shelf prices in premium aisles. Apotex’s acquisition of CanPrev bridges pharmaceutical-grade manufacturing with natural health portfolios, unlocking pharmacist recommendations and insurance coverage considerations. Lonza brings organic capsules to market, letting full organic formulations finally hit shelves and tapping a segment where 54% of North American shoppers pay price premiums for organic seals.

Emerging disruptors rely on DTC subscriptions, algorithmic dosing tools, and social media education. These micro-brands offset limited budgets by piggybacking on supplier clinical trials, reducing research and developmentoutlays. Blockchain tracking pilots stay expensive at USD 50,000 - USD 100,000, so uptake concentrates among labels with annual revenue above USD 10 million. White-space exists in stacked formulas that merge saffron with omega-3s, magnesium, or B-complex vitamins, addressing multiple mood pathways while justifying 20-30% price premiums. Formulators must, however, confirm ingredient interaction data to satisfy retailer and regulatory safety prerequisites.

North America Saffron Supplements Industry Leaders

-

GNC Holdings

-

Swanson Health Products

-

Nature’s Way

-

NOW Health Group

-

Life Extension

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: NutriRise expanded its wellness portfolio in July 2026 with the launch of NutriRise Saffron 120 Caps, a saffron supplement formulated to support mood, focus, and dopamine balance. Rooted in over 3,500 years of traditional use, the supplement is marketed as a nurse-trusted botanical product designed to meet growing consumer demand for natural solutions that support emotional well-being and focus.

- October 2025: Lonza Capsugel launched Organicaps, a USDA organic-certified pullulan capsule manufactured in Greenwood, South Carolina, addressing a critical formulation bottleneck for organic saffron supplements by enabling finished products to carry full organic certification.

- February 2025: Apotex, Canada's largest pharmaceutical company, acquired CanPrev, a natural health products company with over 445 licensed products sold across 3,400 retail locations, including pharmacies, health-food stores, and naturopathic clinics. The acquisition integrates pharmaceutical-grade manufacturing capabilities with natural health portfolios, expanding distribution reach for botanical supplements, including saffron-containing formulations, and enabling cross-selling through established pharmacy channels.

North America Saffron Supplements Market Report Scope

| Gummies |

| Capsules/Tablets |

| Powders |

| Liquids |

| Others |

| Supermarkets/Hypermarkets |

| Pharmacies/Specialty Stores |

| Online Retail Stores |

| Other Distribution Channel |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Form | Gummies |

| Capsules/Tablets | |

| Powders | |

| Liquids | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Pharmacies/Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channel | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is North America saffron supplements market in 2026?

It is valued at USD 124.48 million and is set to grow at a 12.58% CAGR toward 2031.

Which form grows fastest in the region?

Gummies lead with a projected 13.08% CAGR, driven by younger consumers seeking convenient, palatable formats.

Which distribution channel is outpacing others in sales growth?

Online retail expands at a 14.41% CAGR as subscription models and amazon verification spur digital migration.

Why do brands pursue organic certification?

USDA organic seals command 15–20% premiums and assure consumers of clean, traceable supply chains.

Page last updated on: