Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

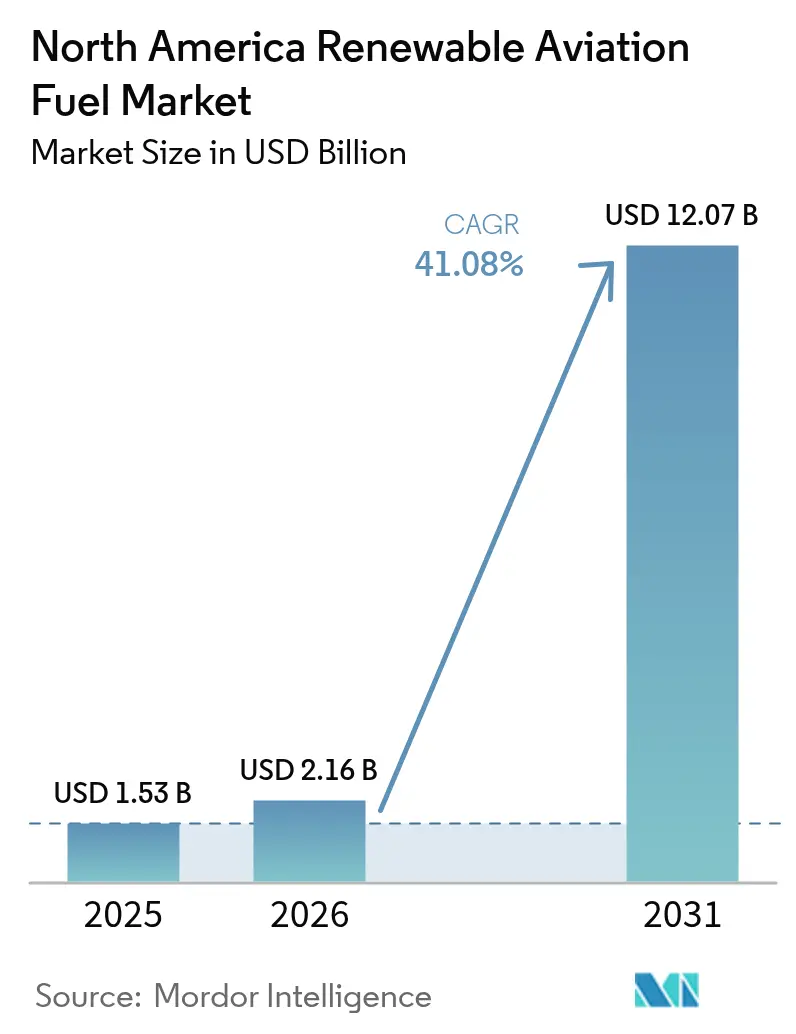

| Base Year Market Size (2025) | USD 1.53 Billion |

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 12.07 Billion |

| Growth Rate (2026 - 2031) | 41.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Renewable Aviation Fuel Market Analysis by Mordor Intelligence

North America Renewable Aviation Fuel Market size in 2026 is estimated at USD 2.16 billion, growing from 2025 value of USD 1.53 billion with 2031 projections showing USD 12.07 billion, growing at 41.08% CAGR over 2026-2031.

Policy-driven production incentives, binding airline sustainability mandates, and rapid scale-up of conversion technologies converge to narrow the price gap between sustainable aviation fuel (SAF) and conventional Jet A. Section 40B SAF Blenders Tax Credits of up to USD 1.75 per gallon now cover a significant share of production costs, tilting the investment calculus toward large-scale projects. Airlines have signed long-term offtake agreements exceeding 200 million gallons, a signal that demand visibility has reached the threshold needed for debt financing. Technology innovation reinforces the growth trajectory: HEFA remains the dominant commercial pathway, yet alcohol-to-jet (ATJ) platforms show the fastest expansion as ethanol feedstock becomes abundant, and as lifecycle emissions scoring shifts credit values in their favor. The competitive environment favors vertically integrated players that control feedstock aggregation, conversion capacity, and distribution, providing insulation against price spikes in used cooking oil and animal fats.

Key Report Takeaways

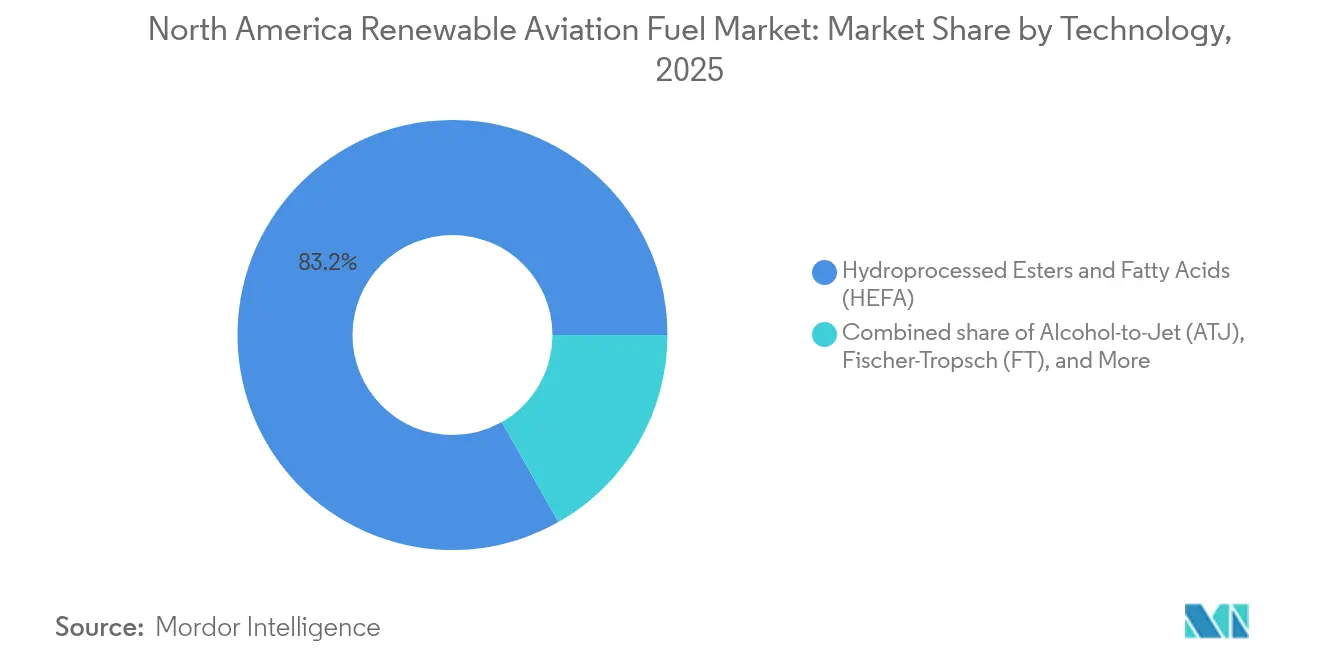

- By technology, HEFA commanded 83.20% revenue share in 2025; alcohol-to-jet is projected to advance at a 45.89% CAGR through 2031.

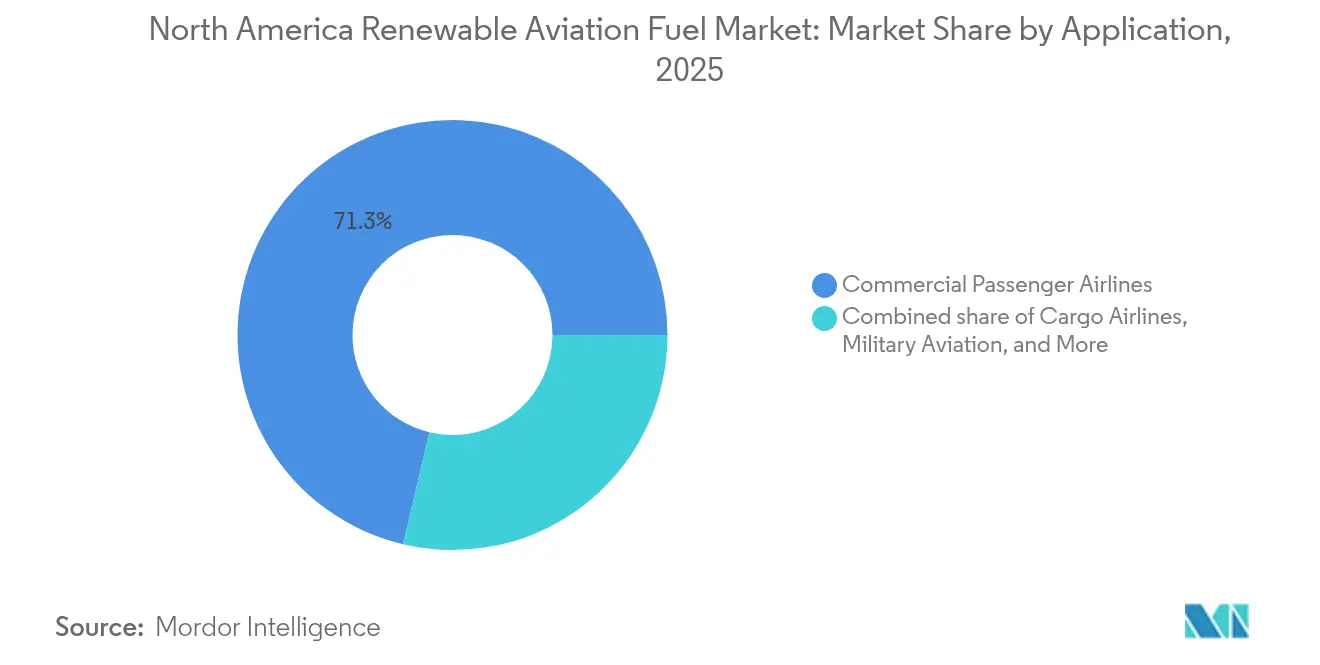

- By application, commercial passenger airlines held 71.30% of the North America renewable aviation fuel market share in 2025, while cargo aviation is forecast to expand at a 44.23% CAGR to 2031.

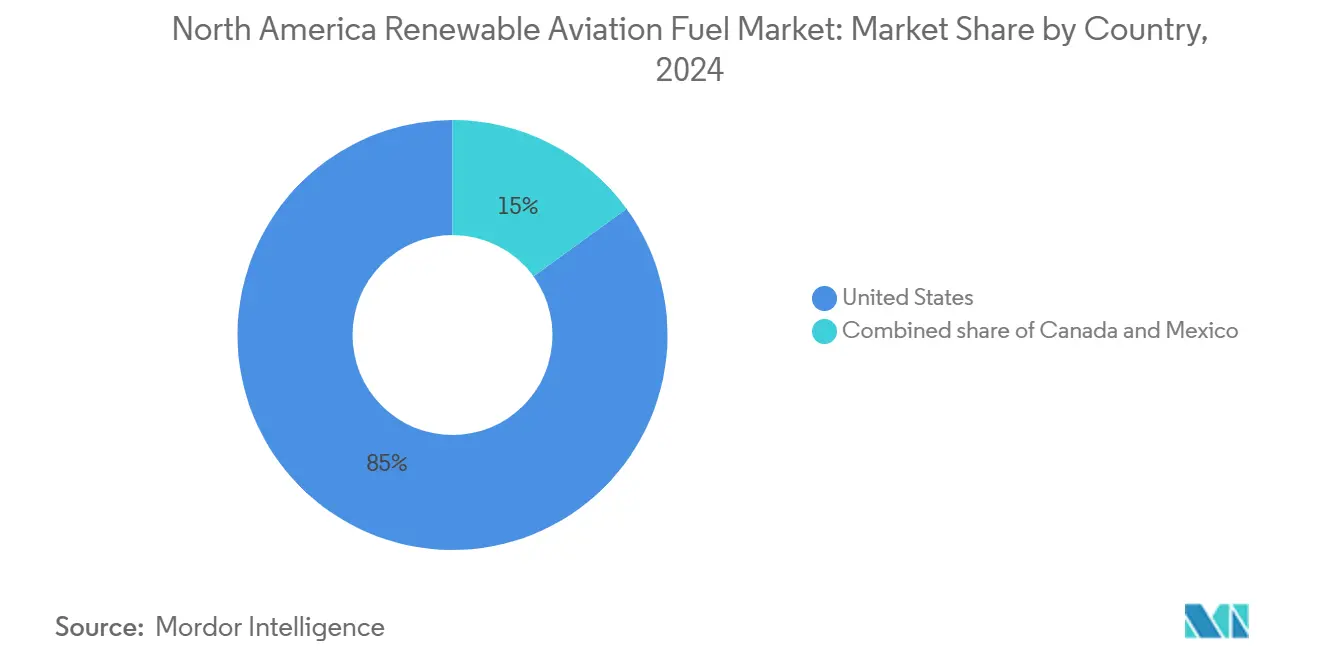

- By country, the United States captured an 84.40% share of the North America renewable aviation fuel market size in 2025 and is anticipated to climb at a 48.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Renewable Aviation Fuel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SAF tax-credits under the U.S. Inflation Reduction Act | 8.50% | United States, spillover to Canada and Mexico | Short term (≤ 2 years) |

| Net-zero pledges signed by >90% of North-American airline capacity | 6.20% | North America | Medium term (2-4 years) |

| Rising corporate "green travel" procurement programs | 4.80% | United States and Canada, emerging in Mexico | Medium term (2-4 years) |

| Emerging carbon-negative alcohol-to-jet (ATJ) pathways | 3.10% | United States, early adoption in Canada | Long term (≥ 4 years) |

| Regional airport consortia financing on-site SAF blenders | 2.70% | United States, pilot programs in Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SAF Tax-Credits Under the U.S. Inflation Reduction Act

The Inflation Reduction Act offers up to USD 1.75 per gallon for SAF achieving at least 50% lifecycle greenhouse-gas savings, a step that compresses the cost delta with fossil jet fuel and sets an economic foundation for multi-hundred-million-gallon projects. Lifecycle intensity rules tilt the advantage toward ATJ and Fischer-Tropsch designs that can meet deeper carbon cuts, hastening technology diversification across the North America renewable aviation fuel market. The shift in 2025 to Section 45Z credits layers fresh incentives for agricultural feedstock suppliers, potentially lowering ethanol input cost curves. Obligatory carbon accounting and verification increase administrative complexity, a hurdle more readily cleared by large, integrated producers. Still, the headline tax credit catalyzes offtake deals that transform airline demand into bankable cash flows, supporting the forecast 42.5% CAGR.

Net-Zero Pledges Signed by Above 90% of North-American Airline Capacity

Airlines representing over 90% of passenger capacity have committed to achieving net-zero by 2050, with interim targets that call for 10-30% SAF usage by 2030.[1]Delta Air Lines, “2025 Sustainability Report,” delta.com Delta alone has secured purchase agreements covering 200 million gallons, while United targets a 10% SAF blend within five years, thereby anchoring long-range demand curves. Military interest intensifies the pull: Lockheed Martin has cleared synthetic fuels for the F-35, F-16, and C-130 fleets, opening another sizable market segment. Binding pledges alter bargaining power, encouraging airlines to negotiate early, sometimes equity-linked, positions in upcoming facilities. The resulting demand certainty lifts lender confidence, accelerating project financial close across the North America renewable aviation fuel market.

Rising Corporate “Green Travel” Procurement Programs

Large enterprises embed Scope 3 emissions criteria into travel procurement, compelling airlines to verify SAF usage or deliver book-and-claim certificates. Neste’s “Neste Impact” service enables companies to purchase SAF attributes and report reductions in line with the Science Based Targets Initiative protocols.[2]Neste, “Neste Impact for Business Travel,” neste.com The mechanism uncouples physical delivery from environmental claims, enlarging the customer base beyond airline operators. Premium pricing narrows uptake to corporations with robust ESG budgets, yet it still enlarges the addressable pool of committed SAF buyers, indirectly boosting forward-contracted volumes that underpin plant financing.

Emerging Carbon-Negative Alcohol-to-Jet Pathways

LanzaTech and LanzaJet’s CirculAir process converts waste carbon streams into ethanol, which is then upgraded to jet fuel, resulting in lifecycle reductions exceeding 85% compared to petroleum kerosene. Freedom Pines, the USD 200 million Georgia facility, demonstrates an annual output of 10 million gallons and validates bankability for ATJ at scale. Feedstock flexibility, spanning municipal waste to industrial CO₂, tackles constraints that beset HEFA projects and qualifies for the highest Section 40B and 45Z incentives. Carbon-negative metrics unlock additional revenue through voluntary carbon markets, strengthening cash flow resilience during feedstock price swings in the North American renewable aviation fuel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock aggregation bottlenecks in the U.S. Midwest | -3.20% | United States Midwest, affecting national supply | Short term (≤ 2 years) |

| HEFA feedstock price volatility linked to renewable diesel build-out | -2.80% | North America, particularly United States | Medium term (2-4 years) |

| Lack of ASTM approval for 100% drop-in SAF use | -1.90% | North America, global implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock Aggregation Bottlenecks in the U.S. Midwest

Corn-ethanol plants operate at scales smaller than the 100-million-gallon conversion units optimal for ATJ, resulting in complex aggregation networks that increase logistics costs. Ethanol already competes with gasoline in the market, so SAF projects must compete on price, potentially introducing volatility into supply contracts. Storage and pipeline capacity in the region remain limited, resulting in additional freight expenses for coastal refineries. Co-location strategies, such as SAFFiRE’s corn-stover-to-ethanol pairing with LanzaJet technology, partially mitigate the challenge but require synchronized capital deployment. Until bottlenecks ease, the North America renewable aviation fuel market faces supply-side friction that tempers near-term growth.

HEFA Feedstock Price Volatility Linked to Renewable Diesel Build-Out

The rapid expansion of renewable diesel refineries drives demand for used cooking oil and animal fats, thereby elevating prices and squeezing margins for HEFA SAF producers.[3]Sustainable Aviation Futures, “Feedstock Price Volatility and Market Effects,” sustainableaviationfutures.com Road-fuel incentives often outbid aviation buyers, diverting feedstocks and occasionally idling SAF units. The geographic concentration of these fats in agricultural zones adds freight overhead for coastal airports. Integrated producers hedge by securing long-term supply contracts or by co-processing in existing hydrotreater assets, but smaller entrants without similar hedges face margin compression during price spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: HEFA Dominance Faces ATJ Disruption

HEFA commanded 83.20% of the North America renewable aviation fuel market share in 2025, a testament to its commercial readiness, existing hydroprocessing infrastructure, and established logistics chains. Capital requirements remain modest because facilities retrofit legacy diesel hydrotreaters, enabling projects to achieve investment-grade status faster than greenfield designs. However, feedstock scarcity and rising competition from renewable diesel refineries curb long-term scalability.

Alcohol-to-jet pathways, although nascent, are projected to post a 45.89% CAGR through 2031, the fastest in the technology stack. LanzaJet’s Freedom Pines plant validates the route’s commercial viability, while CirculAir’s waste-carbon fermentation breaks the dependence on agricultural oils, an advantage that resonates with investors seeking long-lived assets. The high tax-credit uplift for deep-carbon-cut fuels amplifies project IRRs, further shifting capital allocation toward ATJ. Fischer-Tropsch routes remain in the demonstration phase due to high capital expenditures, yet they hold promise for forestry-rich regions like British Columbia. Catalytic Hydrothermolysis Jet and Hydrothermal Liquefaction remain in pilot stages but could advance if lifecycle scores meet the upper tiers of Section 45Z thresholds within the North American renewable aviation fuel market.

By Application: Commercial Aviation Leads, Cargo Accelerates

Commercial passenger airlines accounted for 71.30% of total SAF volumes in 2025, reflecting their large fleet sizes and visible public sustainability commitments. They typically secure multi-year offtake agreements with volume escrows, swapping price certainty for supply priority. Cargo aviation, propelled by e-commerce and corporate logistics clients that demand carbon accountability, accelerates at a 44.23% CAGR to 2031. FedEx and UPS both pilot SAF at hub airports, signaling a sustained shift in procurement policy.

Military interest broadens the addressable pool. Approval for synthetic fuels in F-35, F-16, and C-130 platforms underscores the fuel’s performance under high-stress conditions, giving producers a stable offtake channel that is less price-sensitive and more security-oriented. Business aviation uptake remains limited by supply constraints at regional fixed-base operators and price premiums; however, the National Business Aviation Association documents expanding airport availability, suggesting a gradual improvement. Each application segment carries distinct demand elasticity, shaping supply contracts and influencing infrastructure build-out within the North America renewable aviation fuel market.

Geography Analysis

The United States occupies the center of gravity for production, policy, and demand. Section 40B credits, USD 291 million FAST grants, and the California LCFS jointly reduce risk for project sponsors, drawing a pipeline of >30 new plants that could push annual capacity to 3 billion gallons by 2030. Regional airport hubs, such as Delta’s Los Angeles SAF blending tank farm, reinforce local demand and shorten supply chains. State incentives add incremental margin cushions and encourage the development of distributed facilities near feedstock pools, thereby improving logistics efficiency.

Canada’s Clean Fuel Regulations mandate escalating carbon intensity reductions, pressuring carriers and fueling import demand until domestic plants come online. Air Canada’s multi-year SAF deals illustrate the policy-driven ramp-up in procurement. British Columbia’s forest waste could anchor Fischer-Tropsch deployments, complementing ethanol-rich Midwest flows into Ontario and Quebec.

Mexico’s policy framework remains formative, yet US-Mexican supply-chain integration discussions point to eventual ethanol and lipid exports that feed Gulf-Coast refineries targeting the North America renewable aviation fuel market. Infrastructure financing remains a bottleneck because Mexican airports lack blending and storage facilities, but joint-venture models under consideration mirror those already operational in the United States. Over the forecast horizon, geographic expansion hinges on policy harmonization, feedstock logistics, and cross-border capital flows that facilitate the distribution of production closer to regional demand nodes.

Competitive Landscape

Roughly 190 companies have announced SAF projects across 330 global sites, but only 18 are operating at a commercial scale, underscoring a fragmented, early-stage competitive landscape. Integrated majors such as Neste, TotalEnergies, and World Energy leverage proprietary refining assets, locked-in feedstock contracts, and direct airline partnerships to secure first-mover scale. Neste supplies carriers in San Francisco and Los Angeles, wielding book-and-claim platforms that expand its revenue base. TotalEnergies collaborates with Airbus to meet over half of the OEM’s European fuel needs, illustrating strategic alignment between airframe manufacturers and fuel suppliers.

Emerging pure-plays LanzaJet and Gevo differentiate through technology—ATJ and catalytic fermentation—targeting the tax-credit premiums accorded to deep-carbon-cut fuels. Freedom Pines validates ATJ’s bankability, while Gevo’s Net-Zero 1 project bundles power-to-x upgrades aimed at carbon-negative scores. Venture capital and airline equity appear in most new builds, a pattern demonstrated by Southwest’s USD 30 million investment in LanzaJet to secure future supply. Upstream, oilseed processors and rendering firms secure long-term offtake deals, seeking to arbitrage feedstock scarcity into negotiated pricing floors. Downstream, airports finance on-site blending modules, attracting smaller carriers that would otherwise lack access. Competitive positioning, therefore, depends on vertical integration that secures feedstock, tax-credit eligibility, and captive offtake, creating high entry barriers even in a market that outwardly appears fragmented.

North America Renewable Aviation Fuel Industry Leaders

Neste Oyj

World Energy LLC

TotalEnergies SA

Honeywell UOP (licensee capacity)

Gevo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Air France-KLM invested USD 4.7 million in DG Fuels for a Louisiana facility, securing purchase rights to 75,000 tons per year starting in 2029.

- November 2024: DG Fuels announced a Minnesota SAF plant as part of its expansion blueprint.

- June 2024: LanzaTech and LanzaJet unveiled CirculAir, a waste-carbon-to-jet technology, achieving an 85% reduction in emissions.

- April 2024: Boeing procured 9.4 million gallons of blended SAF for 2024 U.S. operations, a 60% rise year-on-year.

North America Renewable Aviation Fuel Market Report Scope

The renewable aviation fuel (RAF) market studied in the report includes the production of renewable aviation fuel. RAF is produced by blending conventional kerosene with renewable hydrocarbon. RAFs are being produced through technologies certified by the American society for testing and materials (ASTM) to reduce aviation emissions. Europe's renewable aviation fuel market is segmented by technology, application, and geography. By technology, the market is segmented into fischer-tropsch (FT), hydro-processed esters and fatty Acids (HEFA), and synthesized iso-paraffinic (SIP) and alcohol-to-jet (AJT). By application, the market is segmented by commercial and defense. The report also covers the market size and forecasts for the renewable aviation fuel market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion).

By Technology

| Fischer-Tropsch (FT) |

| Hydroprocessed Esters & Fatty Acids (HEFA) |

| Alcohol-to-Jet (ATJ) |

| Synthesized Iso-Paraffinic (SIP) |

| Catalytic Hydrothermolysis Jet (CHJ) |

| Hydrothermal Liquefaction (HTL) |

By Application

| Commercial Passenger Airlines |

| Cargo Airlines |

| Military Aviation |

| Business & General Aviation |

By Country

| United States |

| Canada |

| Mexico |

| By Technology | Fischer-Tropsch (FT) |

| Hydroprocessed Esters & Fatty Acids (HEFA) | |

| Alcohol-to-Jet (ATJ) | |

| Synthesized Iso-Paraffinic (SIP) | |

| Catalytic Hydrothermolysis Jet (CHJ) | |

| Hydrothermal Liquefaction (HTL) | |

| By Application | Commercial Passenger Airlines |

| Cargo Airlines | |

| Military Aviation | |

| Business & General Aviation | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected size of the North America renewable aviation fuel market in 2031?

The market is forecast to reach USD 12.07 billion by 2031, expanding at a 41.08% CAGR over 2026-2031.

Which technology is growing fastest in the North America renewable aviation fuel industry?

Alcohol-to-jet pathways are expanding at a 45.89% CAGR through 2031, outpacing other conversion technologies.

How do U.S. federal incentives support SAF production?

Section 40B SAF Blenders Tax Credits provide up to USD 1.75 per gallon for fuels that cut lifecycle emissions by at least 50%, significantly improving project economics.

Why is the U.S. market dominant in North America renewable aviation fuel?

A combination of federal tax credits, state-level clean-fuel standards, and a dense airline network gives the United States 84.40% market share and drives a 48.64% CAGR.

What restrains faster growth of SAF in North America?

Feedstock aggregation challenges, competition for HEFA feedstocks with renewable diesel, and limitations on 100% SAF certification presently slow deployment.

Which application segment is witnessing the highest growth rate?

Cargo aviation shows the fastest growth, advancing at a 44.23% CAGR as logistics firms demand lower-carbon freight solutions.

Page last updated on: