Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

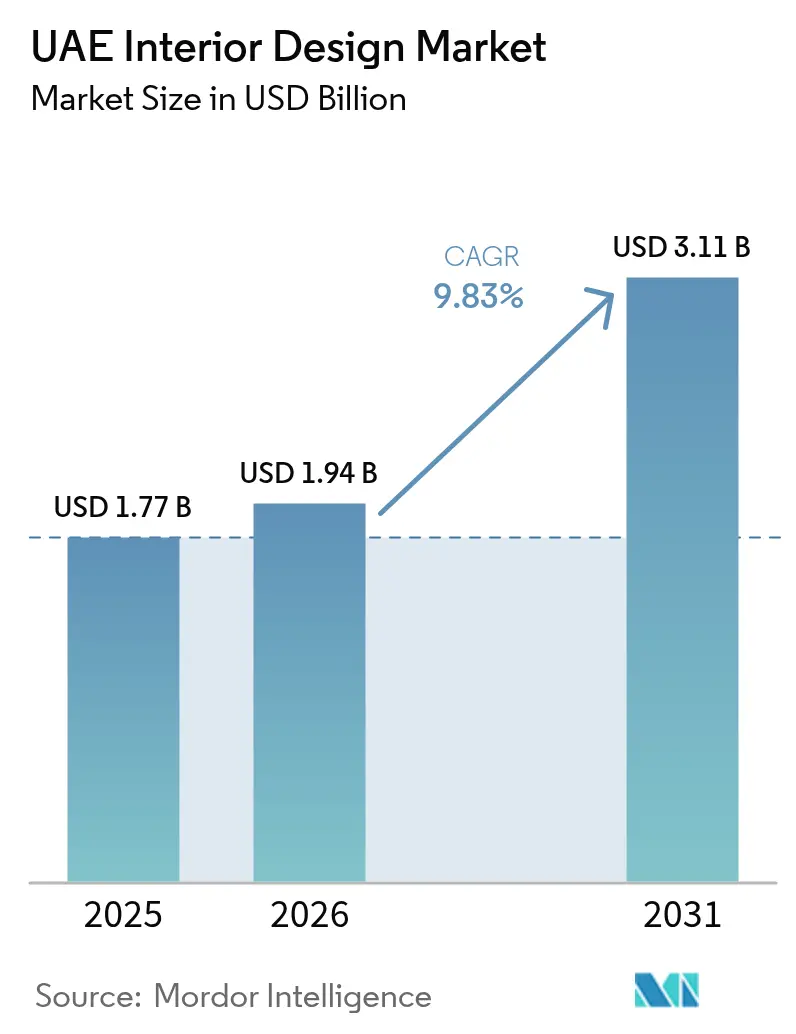

| Base Year Market Size (2025) | USD 1.77 Billion |

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 3.11 Billion |

| Growth Rate (2026 - 2031) | 9.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Interior Design Market Analysis by Mordor Intelligence

The UAE interior design market size was valued at USD 1.77 billion in 2025 and estimated to grow from USD 1.94 billion in 2026 to reach USD 3.11 billion by 2031, at a CAGR of 9.83% during the forecast period (2026-2031). Robust demand arises from record-setting residential property transactions, liberalized foreign-ownership regulations, and an extensive hospitality pipeline that spans luxury resorts, branded residences, and mixed-use mega-projects. Dubai remains the undisputed nucleus of activity, and its elevated average fit-out spend often exceeding AED 9,000 (USD 2,451.77) per square meter in premium villas continues to attract global design houses and specialist contractors. Simultaneously, retrofit mandates embedded in the Dubai 2040 Urban Master Plan are accelerating renovation cycles, while technology-driven design methods such as digital twins, BIM coordination, and 3D-printed components shorten project timelines and trim waste. Parallel advances in modular off-site interiors show early success in cost-sensitive segments, yet custom craftsmanship and experiential storytelling continue to anchor value in the premium tier of the UAE interior design market.

Key Report Takeaways

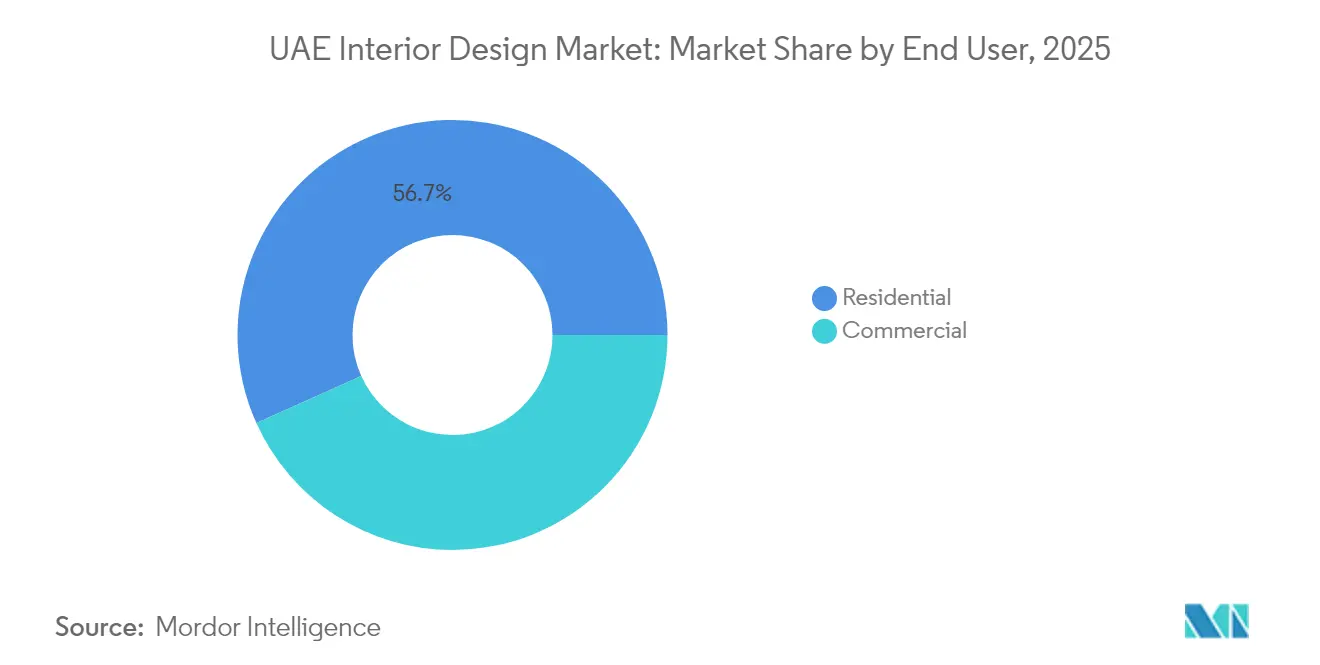

- By end-user, residential projects commanded 56.72% of the UAE interior design market share in 2025, whereas commercial fit-outs are on track to expand at a 6.86% CAGR through 2031.

- By service type, renovation and remodeling captured 68.05% of the UAE interior design market size in 2025 and are projected to rise at an 7.92% CAGR to 2031.

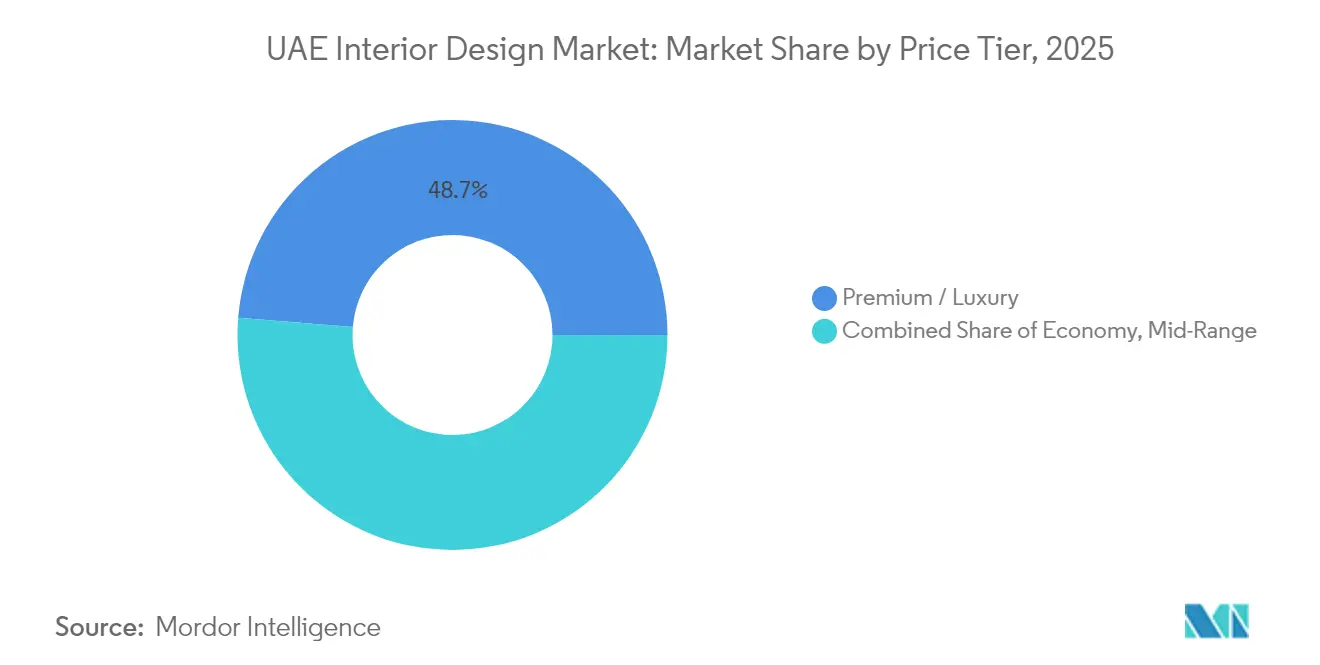

- By price tier, premium and luxury interiors led with 48.72% the UAE interior design market share in 2025 and are advancing at an 10.12% CAGR, the fastest growth across all tiers.

- By geography, Dubai accounted for 51.74% of the UAE interior design market share, expanding at a CAGR of 7.18%, the fastest-growing regional sub-market between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Interior Design Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming residential property transactions | 2.1% | Dubai core, spill-over to Abu Dhabi and Sharjah | Short term (≤ 2 years) |

| Government visa & foreign-ownership reforms | 1.8% | Global, with early gains in Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Mega-tourism & hospitality pipeline | 2.3% | Dubai & Abu Dhabi primary, Northern Emirates secondary | Long term (≥ 4 years) |

| Ultra-luxury crypto & digital-nomad demand | 1.4% | Dubai Marina, Downtown, Palm Jumeirah concentrated | Short term (≤ 2 years) |

| Dubai 2040 retrofit sustainability mandates | 1.9% | Dubai focused, Abu Dhabi following | Long term (≥ 4 years) |

| Hybrid-office experiential redesign | 1.2% | Global trend, UAE corporate districts concentrated | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Residential Property Transactions

Dubai closed Q1 2025 with 45,474 residential deals valued at AED 142.7 billion (USD 38.88 billion), marking a 22% jump in volume and a 30% surge in value versus the prior-year quarter. The ready-property slice alone generated AED 87.5 billion (USD 23.84 billion), fueling immediate customization requests as buyers push for turnkey interiors within 90-day handover windows. Off-plan sales comprise 56% of total deals and embed design-specification clauses that lock in bespoke finishes months before completion. Internal industry polling indicates that 60% of luxury buyers commission further upgrades inside the first year, funneling recurring revenue to specialist studios. Abu Dhabi mirrors the trend with a 75% leap in ready-property values, enlarging the geographic canvas for premium design. Property-tokenization pilots under the Dubai Land Department further fractionalize ownership and democratize access, stoking incremental demand for the UAE interior design market.

Government Visa & Foreign-Ownership Reforms

The Golden Visa program now grants long-term residency to investors placing AED 2 million (USD 544,217) into real estate, effectively converting foreign capital into sustained interior spending streams[2]Source: UAE Cabinet, “Integrated Regulatory Intelligence Ecosystem,” uaecabinet.ae. High-net-worth crypto entrepreneurs cite zero capital-gains taxes and rapid licensing pathways as principal reasons for relocation, and their design briefs frequently feature secure digital-asset vaults, remote-work suites, and gallery-grade art lighting. Corporate reforms that allow 100% foreign ownership outside free zones have lured multinational headquarters, elevating demand for experiential offices optimized for hybrid teams. Each headquarters fit-out typically spans 15,000–25,000 square meters and allotts 40% of budget to technology integration—another catalyst for the UAE interior design market. Importantly, one-stop regulatory clearance under the integrated regulatory-intelligence ecosystem has cut average design-approval cycles by 18%, accelerating revenue conversion for market participants.

Mega-Tourism & Hospitality Pipeline

More than USD 100 billion in hotel construction is underway, with flagships such as Aman Dubai, Janu Dubai, and Rosewood Dubai slated to open between 2027 and 2029, each earmarking AED 50–200 million (USD 13.62–54.47 million) for interiors[3]Source: Hospitality Net, “Aman Group Plans for Janu Dubai,” hospitalitynet.org. Average hotel occupancy stood at 78% in 2024, reinforcing investor appetite for differentiated guest experiences that rely heavily on sensory design, biophilic accents, and personalized digital touchpoints. Contract values at five-star properties exceed AED 17,000 (USD 4,632.42) per square meter, reflecting the premium fees that flow into the UAE interior design market. The Wynn Resort planned for Ras Al Khaimah signals a spatial diffusion of luxury demand beyond Dubai, while national ambitions to host 40 million annual visitors by 2031 ensure a multi-year pipeline of hospitality refurbishments and new builds.

Dubai 2040 Retrofit Sustainability Mandates

The Dubai 2040 Urban Master Plan obliges existing buildings to attain aggressive energy-efficiency thresholds, spurring a wave of green retrofits across Grade-A offices, retail assets, and high-rise residences. LEED-ready materials, low-VOC finishes, and smart-metering systems now feature in 35% of office projects awarded since 2024, up from 18% five years earlier. Retrofit packages routinely fold in air-quality monitoring and circadian-lighting schemes, aligning occupant-health objectives with operational-carbon goals. Because deep-retrofit projects reach 5–7-year payback periods, landlords remain highly motivated to allocate capital, injecting recurring projects into the UAE interior design market. Municipal incentive structures including expedited permitting and density bonuses further tip the economic equation in favor of sustainable interior upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fit-out material costs | -1.8% | Global supply chain impact, UAE logistics concentrated | Short term (≤ 2 years) |

| Looming residential oversupply correction | -1.2% | Dubai primary risk, Abu Dhabi secondary | Medium term (2-4 years) |

| Shortage of licensed designers post-regulation | -0.9% | UAE-wide, Dubai Municipality jurisdiction | Medium term (2-4 years) |

| Rise of off-site modular interiors | -1.1% | Technology adoption centers, cost-sensitive segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Fit-Out Material Costs

Luxury villa interiors now command AED 9,100–11,250 (USD 2,478.74–3,064.85) per square meter due to a 15–20% climb in imported timber, specialty metals, and artisanal stone since 2023. Restaurant fit-outs reach AED 19,000 (USD 5,177.93) per square meter, and quarterly swings of up to 12% in key-material indices complicate cash-flow planning. Suppliers are shortening quote validity to 14 days, pushing designers to adopt hedging clauses and provisional-sum allowances. Clients increasingly request life-cycle cost breakdowns to justify premium materials, adding complexity—but also consulting revenue—to design scopes. While larger contractors leverage bulk-buying power to cushion volatility, boutique studios struggle to protect margins, slowing project-start decisions in the UAE interior design market.

Rise of Off-Site Modular Interiors

Modular manufacturing expanded from AED 2.9 billion (USD 790.46 million) in 2020 to AED 3.4 billion (USD 926.73 million) in 2023, and projections call for nearly AED 5 billion (USD 1.36 billion) by 2029 as hospitality chains and mid-tier developers chase 25% cost savings.[4]Source: Construction Week Online, “Potential of Modular Construction in GCC,” constructionweekonline.com. ALEC subsidiary LINQ secured Dubai’s first G+6 modular license, proving regulatory openness to factory-built rooms, corridors, and MEP cores that clip together on site in half the usual time. Ji Hotels plans 10 Dubai properties built with prefabricated modules, undercutting conventional fit-out fees and siphoning share from bespoke design studios. Although ultra-luxury clients still favor handcrafted detailing that modular systems rarely replicate, the technology is steadily gaining acceptance in student housing, staff accommodation, and value-focused hospitality—segments that collectively anchor volume within the UAE interior design market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Residential Demand Anchors Growth

Residential projects accounted for 56.72% of the UAE interior design market share in 2025 as expatriate inflows, crypto-driven wealth, and Golden Visa incentives lifted buying appetite across villas and branded condos. Median villa prices advanced 20% in 2024, and rental yields rose 19%, prompting owners to inject capital into interiors that could justify premium lease rates or elevate resale positioning. The commercial slice trails but is accelerating at a 6.86% CAGR on the back of multinational headquarters migrations, with occupiers prioritizing agile collaboration zones, amenity-rich lobbies, and wellness-infused workspaces. Hybrid-office experimentation intensified through 2025, as employers shifted 30% of workstation areas into social hubs and acoustic pods—design-intensive conversions that widen addressable revenue in the UAE interior design market size. Meanwhile, co-living and senior-living pilots introduce niche sub-segments where universal-design principles, smart-home integration, and concierge-style layouts promise further upside. Collectively, these dynamics underscore a balanced yet opportunity-rich demand profile that underpins sustained investment from service providers and material suppliers.

Second-home ownership among global elites is rising, with 948 sales north of USD 4.09 million logged in 2024 and each transaction spawning AED 1–3 million (USD 272,324–816,973) in bespoke interior commissions. Abu Dhabi contributes incremental lift by funneling oil-revenues into cultural districts such as Saadiyat Grove, where museum-adjacent residences require curatorial display lighting and humidity-managed art closets. Sharjah and Ajman register a different flavor of residential growth, favoring mid-income family apartments that demand cost-efficient yet culturally resonant interiors. Whether serving penthouse buyers seeking NFT-gallery walls or extended families prioritizing prayer-room acoustics, designers are tailoring solutions across a spectrum of price sensitivities, thereby diversifying risk and expanding the overall UAE Interior Design market.

By Service Type: Renovation Commands the Majority

Renovation and remodeling seized 68.05% of UAE Interior Design market size in 2025, reflecting the maturity of the built environment and the urgency to meet new energy codes before compliance deadlines. Typical retrofit scopes now pair envelope upgrades with deep interior overhauls, driving longer project durations and higher billable hours. Tenant churn in prime offices exceeds 20% annually, translating into frequent fit-outs and an 7.92% CAGR for the renovation sub-segment through 2031. New-build activity remains strong in hospitality and mixed-use super-blocks, yet the share differential underscores the strategic importance of after-market services. Contractors are amassing design-for-manufacture competencies to fast-track retrofits using standardized components, a trend that blurs lines between renovation and modular construction.

Dubai Municipality’s Universal Design Code compels accessible upgrades across lobbies, corridors, and washrooms—an obligation that cascades into material choices, spatial layouts, and MEP rerouting. Moreover, landlords view retrofit investments as ESG accelerators capable of fetching 10-15% rent premiums, incentivizing continuous pipeline creation within the broader UAE Interior Design market. As insurance underwriters start to tie premiums to building-performance metrics, portfolio owners are pre-booking multi-year improvement cycles, offering designers recurring revenue visibility.

By Price Tier: Luxury Retains Commanding Position

Premium and luxury interiors delivered 48.72% revenue in 2025 and are tracking an 10.12% CAGR as crypto millionaires, digital nomads, and legacy family offices compete for statement properties. Top-tier projects integrate advanced security vaults, bullet-resistant glazing, biometric access, and hand-finished marquetry, pushing per-square-meter budgets higher than any other GCC market. Leisure-oriented yachts, sky mansions, and branded penthouses reinforce cross-category spending, further buoying the high end of the UAE interior design market. Mid-range demand, growing at a respectable 7%, shines in thoughtfully designed suburban communities that court professionals and young families through wellness amenities and tech-enabled efficiencies. Economy interiors, often delivered via modular packages, cater to budget hotels, student housing, and staff accommodations where cost discipline outweighs bespoke articulation.

Luxury clients increasingly insist on low-carbon materials and transparent provenance, bridging sustainability with exclusivity. Designers answer through reclaimed teak flooring, algae-based acoustic panels, and circular-economy furniture collections, thereby monetizing environmental stewardship. Smart-mirror fitness walls, AI-driven climate control, and AR-powered art curation also migrate from pilot to mainstream in this segment, underscoring technology’s role in reinforcing luxury price points and preserving the value pool inside the UAE interior design market.

Geography Analysis

Dubai preserved 51.74% of UAE Interior Design market share in 2025 and is forecast to expand at a 7.18% CAGR through 2031, propelled by AED 142.7 billion (USD 38.88 billion) in Q1 2025 real-estate transactions and a hospitality pipeline that exceeds USD 100 billion in committed capital. The emirate’s policy cocktail—spanning zero capital-gains tax, crypto-friendly frameworks, and Golden Visa residency—draws an eclectic investor base whose lifestyle requirements translate into high-margin design briefs. Dubai’s 6,500-kilometer Walk Master Plan and the Green Spine corridor further guarantee recurring retail and public-realm interiors, while 3D-printing permits unlock avant-garde façade treatments previously impossible to cost-justify. Regulatory standards enshrined in the new Dubai Building Code harmonize safety and green benchmarks, streamlining design-approval cycles and favoring firms steeped in local requirements.

Abu Dhabi contributes roughly 33.30% of national revenue and grows at 6.05% CAGR, its trajectory shaped by culture-driven placemaking, sovereign-backed infrastructure, and a deliberate push toward net-zero urbanism. Projects on Saadiyat Island and Masdar City emphasize passive-design strategies, bioswales, and micro-grid integrations that expand the consultant ecosystem beyond aesthetics into environmental engineering. Government procurement protocols reward teams combining LEED, Estidama, and WELL certification fluency, elevating the sophistication—yet also the complexity—of interior scopes. The capital’s higher average floorplates encourage experimentation with modular pod offices and multi-faith prayer rooms, spotlighting how sociocultural layers inform the UAE interior design market.

Sharjah, Ajman, Fujairah, and Umm Al Quwain jointly hold near-14.96% of revenue yet clock sturdy 5.74% growth, their value proposition rooted in affordability, cultural authenticity, and family living. Developers there prefer mid-rise typologies that foster neighborhood intimacy, steering demand toward vernacular-influenced interiors that leverage locally quarried stone, regionally woven textiles, and artisanal gypsum carvings. Ras Al Khaimah’s Wynn Resort catalyzes an upscale pivot that could lift Northern-Emirates market share above 18% by decade-end, signaling new competitive geographies for the UAE interior design market.

Competitive Landscape

Market concentration is moderate, with the top five firms—Depa Interiors, ALEC Fitout, Al Tayer Stocks, Bond Interiors, and Summertown Interiors—commanding a significant portion of total revenue. This leaves ample room for niche specialists and new entrants to compete and grow. Depa’s joint venture with Germany’s Lindner Group widens turnkey delivery capacity across airport terminals and cruise facilities, showcasing vertical-integration strategies that capture manufacturing margins while elevating technical credibility. ALEC Fitout continues to pioneer robotic pre-cutting and on-site 3D printing, shaving 12% off critical-path schedules and positioning itself for public-sector megaprojects. Al Tayer Stocks invests in proprietary wellness-analytics software that optimizes post-occupancy air quality and lighting, a differentiator as ESG metrics influence leasing decisions.

Boutique studios counter scale advantages with hyper-curation, crafting NFT-enabled art spaces and sensory-therapy suites for neurodiverse residents—offerings that secure premium pricing despite smaller backlogs. Meanwhile, material suppliers jostle for relevance via digital specification platforms that embed QR-coded provenance, enhancing transparency and reducing substitution risk. Modular-focused disruptors such as LINQ aim at cost-sensitive hospitality and staff-housing formats, enabling 40% faster delivery yet sparking debate over long-term asset differentiation versus the bespoke ethos that historically defined the UAE Interior Design market. Overall, the arms race now tilts toward tech adoption, demonstrated green credentials, and end-to-end execution muscle.

International hospitality brands, including Aman, Rosewood, and Ji Hotels, increasingly bypass general contractors to appoint design guardians that protect brand DNA across every FF&E item. This shift magnifies the importance of intellectual-property sensitivity and rapid prototype iterations, competencies that only a subset of local firms currently command. Against that backdrop, merger conversations surface among mid-tier players eager to consolidate bidding power before global design houses set up branch operations. At the same time, public-sector frameworks require Emiratization quotas and knowledge-transfer programs, weaving social objectives into competitive calculus and shaping future leadership dynamics within the UAE Interior Design market.

UAE Interior Design Industry Leaders

Depa Interiors

ALEC Fitout

Al Tayer Stocks

Bond Interiors

Summertown Interiors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Arco Group acquired Laing O’Rourke Joinery to deepen manufacturing depth across doors, wall systems, and millwork, thereby enhancing domestic supply resilience.

- January 2025: LEOS Developments unveiled Weybridge Gardens 4 in Dubailand, a project centered on wellness-oriented interiors and biophilic landscaping concepts.

- December 2024: Delano Dubai opened on Bluewaters Island with 167 guestrooms and 84 suites, each showcasing natural materials curated by Elastic Architects.

- October 2024: Dubai Executive Council ratified a new Dubai Building Code that tightens fire-safety clearances and embeds waste-diversion targets in interior fit-outs.

UAE Interior Design Market Report Scope

The report on the United Arab Emirates Interior Design Market provides a comprehensive evaluation of the industry, with an analysis of the segments in the market. The report also focuses on the exhaustive trends in production and consumption data of the product, policies, and plans. Moreover, the report also provides a competitive profile of the key interior designing players, along with regional analysis.

By End-User

| Residential |

| Commercial |

By Service Type

| New Construction |

| Renovation / Remodeling |

By Price Tier

| Economy |

| Mid-Range |

| Premium / Luxury |

By Geography

| Abu Dhabi |

| Dubai |

| Sharjah |

| Ajman |

| Ras Al Khaimah |

| Fujairah |

| Umm Al Quwain |

| By End-User | Residential |

| Commercial | |

| By Service Type | New Construction |

| Renovation / Remodeling | |

| By Price Tier | Economy |

| Mid-Range | |

| Premium / Luxury | |

| By Geography | Abu Dhabi |

| Dubai | |

| Sharjah | |

| Ajman | |

| Ras Al Khaimah | |

| Fujairah | |

| Umm Al Quwain |

Key Questions Answered in the Report

What is the forecast value of the UAE Interior Design market by 2031?

The market is projected to reach USD 3.11 billion by 2031, expanding at a 9.83% CAGR.

Which service category captures the largest revenue share?

Renovation and remodeling lead with 68.05% share, reflecting sustainability retrofits and frequent tenant churn.

Why is Dubai the primary revenue engine in this space?

Dubai accounts for 51.74% of activity thanks to record property transactions, mega-tourism pipelines, and crypto-friendly residency incentives.

How are modular interiors influencing competitive dynamics?

Factory-built modules cut delivery times by up to 40% and appeal to cost-sensitive segments, challenging traditional bespoke studios.

Which factors most threaten near-term growth?

Material-cost volatility and expanding modular adoption both exert downward pressure on project margins and traditional fee structures.

Page last updated on: