Marketing Agencies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

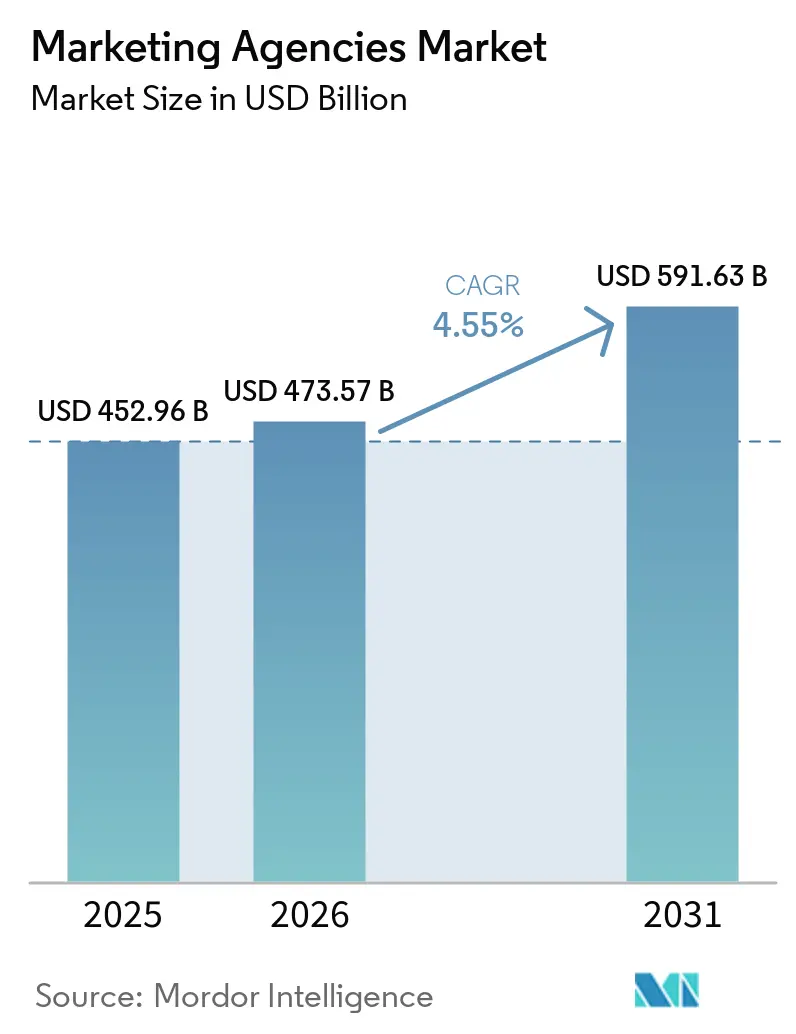

| Market Size (2026) | USD 473.57 Billion |

| Market Size (2031) | USD 591.63 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

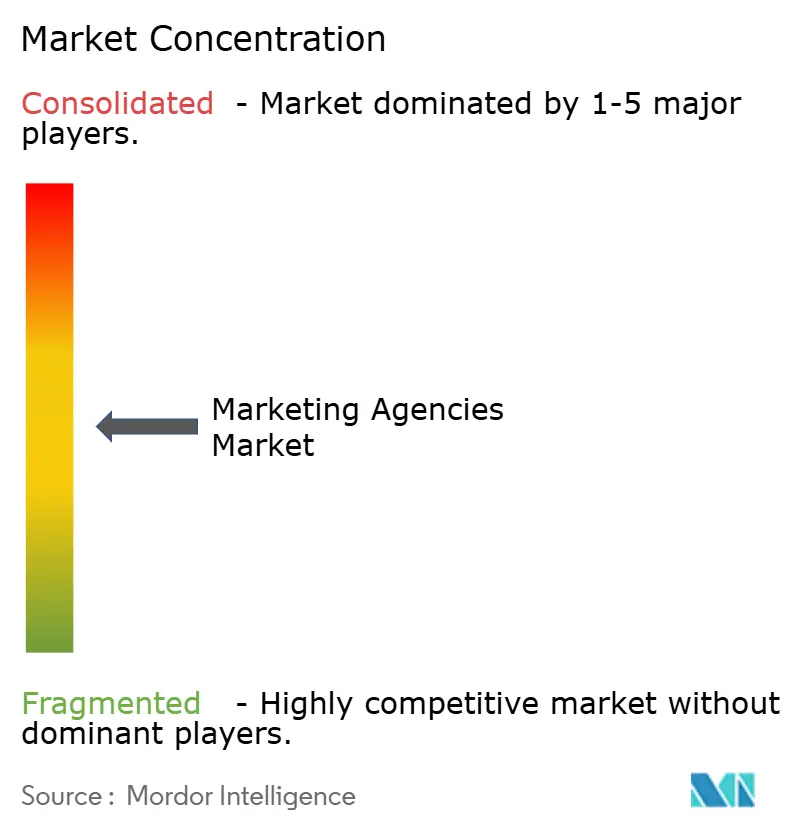

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marketing Agencies Market Analysis by Mordor Intelligence

The Marketing Agencies Market size in 2026 is estimated at USD 473.57 billion, growing from 2025 value of USD 452.96 billion with 2031 projections showing USD 591.63 billion, growing at 4.55% CAGR over 2026-2031. Heightened adoption of artificial intelligence in creative development, rapid scaling of performance-based pricing contracts, and cookie-less personalization technologies are reshaping how brands evaluate agency partnerships [1]: Digiday Staff, “Google hands Smartly creative automation brief to promote hardware range,” Digiday, digiday.com.. Agencies that combine proprietary data capabilities with outcome-linked remuneration models secure longer-term contracts, while those lacking advanced analytics face margin pressure as in-house teams expand. Competitive intensity also rises as holding companies consolidate to capture scale efficiencies, exemplified by Omnicom’s USD 13 billion acquisition of Interpublic Group that promises USD 750 million in annual cost synergies.

Key Report Takeaways

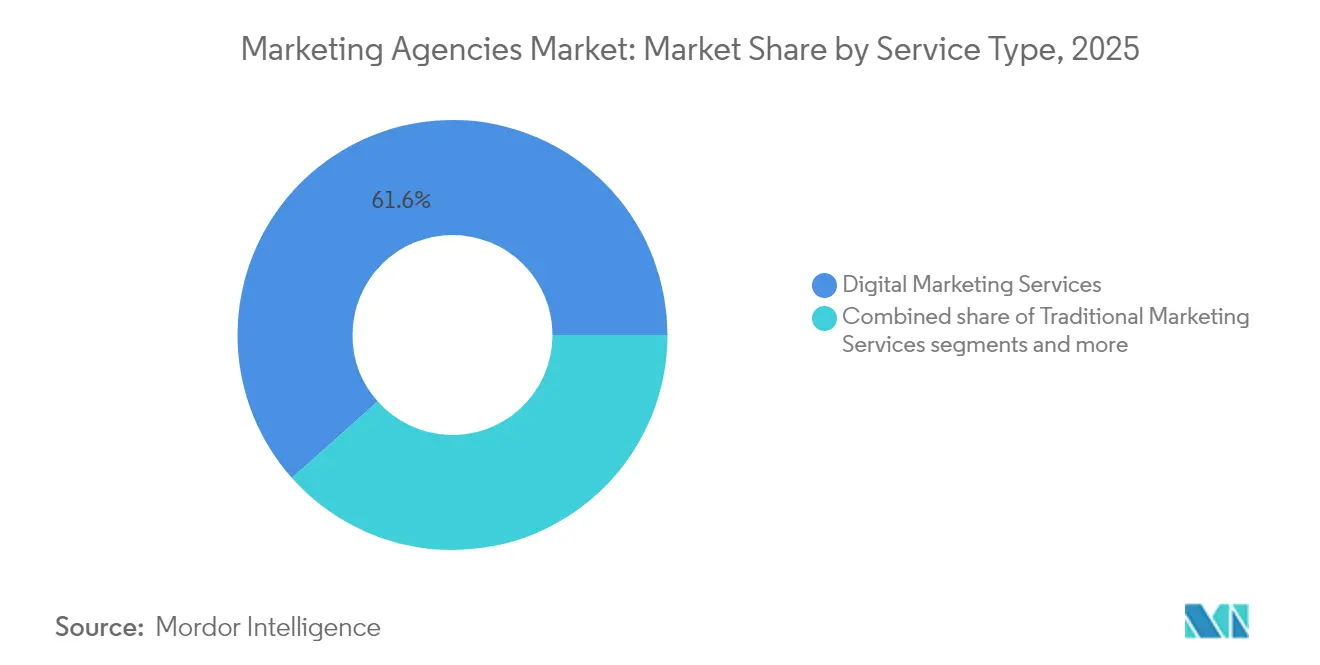

- By service type, digital marketing services led with 61.58% of the marketing agencies market share in 2025, whereas full-service agencies are forecast to expand at an 11.32% CAGR through 2031.

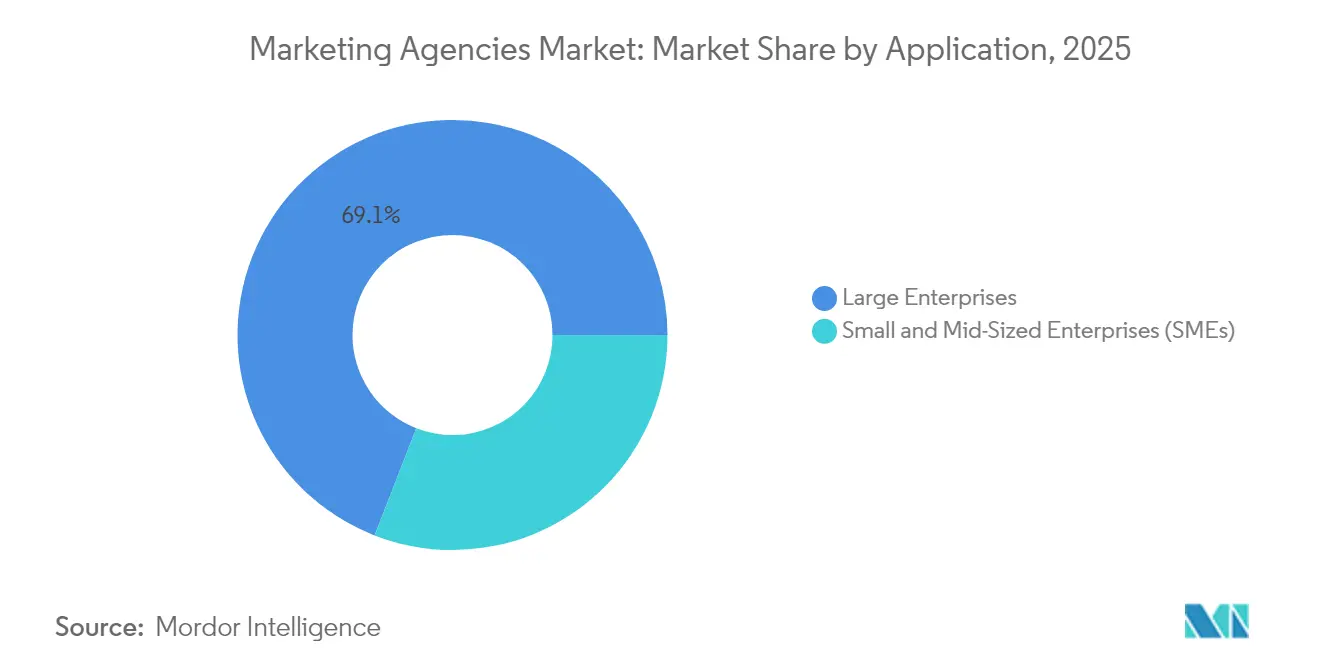

- By application, large enterprises commanded 69.10% of the marketing agencies market share in 2025, while SMEs are projected to post a 12.97% CAGR to 2031.

- By end user, retail & consumer goods accounted for 22.55% of the marketing agency market size in 2025 and public services is advancing at a 13.23% CAGR through 2031.

- By geography, North America held 36.05% of the marketing agencies market share in 2025; Asia-Pacific is set to accelerate at a 14.24% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Marketing Agencies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven campaign optimization | +1.8% | North America & Europe, spreading globally | Medium term (2-4 years) |

| Performance-based pricing models | +1.2% | North America & Europe, gaining traction in Asia-Pacific | Short term (≤ 2 years) |

| Cookieless personalization technologies | +0.9% | Global, spurred by EU & California privacy statutes | Long term (≥ 4 years) |

| B2B shift toward account-based marketing | +0.8% | Mature B2B hubs in North America & Europe | Medium term (2-4 years) |

| SME-friendly self-serve ad portals | +0.7% | Fast-growing emerging markets | Short term (≤ 2 years) |

| Retail media network proliferation | +1.0% | North America & Europe, expanding rapidly across Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-driven campaign optimization

Artificial intelligence is redefining media planning as real-time algorithms dynamically vary creative, placement, and bidding across channels to maximize return on ad spend. Google’s collaboration with Smartly illustrates this pivot: weekly generation of billions of creative signals enables the platform to automate asset selection for display, social, and video formats. Agencies deploying similar systems report double-digit efficiency gains, freeing strategists to focus on storytelling and measurement innovation. Rapid advances in large language models now allow copy, audio, and motion graphics to be versioned in minutes rather than days. Competitive stakes escalate as holding groups develop in-house AI studios to avoid reliance on external vendors. Over the medium term, performance differentials between AI-enabled and manual workflows are expected to widen, pressuring laggards to invest or risk commoditization.

Performance-based pricing adoption

Outcome-linked fee structures align agency revenue with client business results, replacing labor-hour billing with models tied to lead volume, incremental sales, or brand-lift metrics. Brands value the transparency and accountability of these contracts, leading to higher renewal rates for agencies able to prove impact. However, agencies assume greater financial risk because under-performance directly erodes margins, necessitating sophisticated forecasting and attribution frameworks. Data-rich verticals such as e-commerce, SaaS, and app marketing are quickest to adopt because conversion events are easily attributable. Market observers note that performance fees are already standard in influencer, affiliate, and direct-response television, and they are now moving into mainstream brand campaigns. Short-term growth stems from North American advertisers, yet European procurement teams increasingly pilot hybrid retainers that blend base fees with shared upside.

Cookieless personalization technologies

The phase-out of third-party cookies by major browsers compels agencies to re-engineer targeting around first-party data, contextual analysis, and privacy-safe identifiers. Investments in customer data platforms, server-side tagging, and consent management systems are soaring as marketers race to maintain relevance without violating GDPR or CCPA. Contextual artificial intelligence now categorizes page sentiment, visual composition, and metadata to infer audience intent. Agencies with deep engineering talent are gaining share because smaller rivals struggle with the capital intensity of privacy-compliant stacks. As regulatory scrutiny expands to Brazil, India, and ASEAN economies, early adopters are positioned to export their frameworks globally. Over the long run, agencies that build scalable identity graphs while respecting consumer rights will command premium valuation multiples.

Retail media network proliferation

Retailers monetize transaction data and on-site inventory by offering self-serve advertising portals that marry purchase intent with closed-loop attribution. GroupM projects global retail media spend to double from 2024 to 2027. Agencies able to integrate Amazon DSP, Walmart Connect, Target Roundel, and JD.com APIs deliver superior insights into basket composition and incremental sales. Complexity arises because each network maintains unique ad formats, reporting cadences, and fee structures, forcing agencies to build multi-tenant orchestration layers. Commerce-savvy teams that pair search optimization with creative merchandising are now securing higher margins than traditional digital shops. As new entrants from grocery chains to travel aggregators launch media platforms, agency demand for specialized retail media talent is expected to outpace supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fortune 500 in-house agency expansion | –1.5% | North America & Europe | Medium term (2-4 years) |

| Talent attrition to big-tech product teams | –0.8% | Global, concentrated in Silicon Valley & major tech hubs | Short term (≤ 2 years) |

| Data-privacy compliance cost escalation | –0.6% | EU & California, spreading worldwide | Long term (≥ 4 years) |

| Fragmented advertising measurement standards | –0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

In-house agency expansion among Fortune 500 companies

Eighty-two percent of large advertisers now operate some form of internal agency, nearly doubling since 2015[2]ANA Research Team, “Internal Agency Report,” Association of National Advertisers, ana.net. . Cost savings, faster turnaround, and closer proximity to first-party data motivate this shift. External partners increasingly win project-based or specialist assignments rather than full-funnel retainers, eroding revenue visibility for traditional shops. To defend relevance, holding groups embed cross-functional pods inside client offices, pairing strategic oversight with on-site production. Hybrid models flourish in highly regulated sectors where external expertise complements strict compliance mandates. Over the medium term, the boundary between in-house and external teams blurs, rewarding agencies that can flex resources while maintaining brand governance.

Talent attrition to big-tech product teams

Large platforms lure agency specialists with equity, higher salaries, and the opportunity to build base-layer advertising technology[3]MediaPost Staff, “AI Rips Away Manual Language Targeting From Google Ads,” MediaPost, mediapost.com. . Data scientists, full-stack engineers, and creative technologists are most vulnerable to poaching, causing wage inflation for remaining staff. Smaller independents struggle to match compensation, prompting alliances with martech vendors to access advanced capabilities on demand. Some holding companies experiment with variable-compensation pools tied to campaign performance to stem departures. Industry associations warn that persistent brain-drain could slow innovation at the agency layer, entrenching platform dominance. Short-term mitigation includes remote talent sourcing from cost-effective geographies, although cultural alignment and client-facing expertise remain gating factors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Dominates Full-Service Growth

Digital marketing services retained 61.58% of 2025 revenue, underscoring brands’ preference for measurable, omnichannel engagement models that link spend to conversion events. This dominance anchors the marketing agencies' market size baseline, yet full-service agencies exhibit the fastest growth at 11.32% CAGR because clients seek unified governance across media, content, and commerce workflows. Integration advantages manifest in consolidated data lakes that reveal cross-channel attribution, allowing holistic optimization. Meanwhile, traditional marketing services persist in experiential activations, sponsorship consulting, and print-heavy luxury verticals where physical touchpoints carry premium brand equity. The marketing agencies' market share of digital specialists is likely to plateau once AI-augmented full-service models reach scale.

Demand for predictive analytics accelerates migration toward outcome-oriented contracts, benefiting agencies that invest in proprietary dashboards covering creative viewability, path-to-purchase, and lifetime value. Conversely, firms that depend solely on third-party ad servers lose leverage as platforms offer native optimization. Leading groups respond by funneling up-skilling budgets into machine-learning labs and low-code content automation. Over the forecast horizon, the marketing agencies industry expects greater convergence between media buying and commerce enablement, compelling legacy creative boutiques to partner or merge with performance shops to safeguard relevance.

By Application: Enterprise Spending Drives SME Innovation

Large enterprises generated 69.10% of 2025 billings as complex omni-regional campaigns require specialized compliance, localization, and change-management expertise. These accounts anchor retainer revenue for holding companies, which often deploy multiple agency brands to avoid conflict and diversify perspectives. However, SMEs are set to expand at a 12.97% CAGR because platform-provided AI eliminates historical entry barriers. Self-serve portals from Google, Meta, and Amazon bundle audience insights, creative generation, and payment tools, enabling small firms to activate cross-channel plans within hours. Agencies pivot by productizing strategy modules, offering fixed-price workshops and modular creative packs to maintain affordability.

The marketing agency market size attributable to SMEs remains modest today, yet incremental growth outstrips that of large enterprises, incentivizing agencies to scale volume-driven engagement models. Freelance-first networks and crowdsourced creators complement formal agency structures, adding agility. Vertical specialists bundle lead-gen templates for real estate, hospitality, and healthcare, reinforcing differentiation. In parallel, enterprise contracts evolve toward consultative transformation mandates that go beyond campaign delivery, covering martech integration and first-party data governance.

By End User: Retail Innovation Fuels Public Sector Growth

Retail & consumer goods continued to command 22.55% of 2025 spending, leveraging deep SKU-level data to tailor promotions across search, social, and retail media. Agencies with commerce studios synchronize creative, shelf placement, and paid performance around inventory availability. First-party data clean-rooms between retailers and brands drive advanced customer lifetime value modeling that traditional media shops struggle to replicate. Public services, however, are the fastest-growing end-user cohort with a 13.23% CAGR as government bodies digitize citizen touchpoints and crisis-response communication. The marketing agencies' market size within public services expands as health ministries, city councils, and universities procure omnichannel engagement programs that meet accessibility benchmarks. Financial services and telecom maintain steady allocations for account-based marketing and loyalty orchestration, requiring agencies to master stringent data-security protocols. Manufacturing and logistics companies increasingly adopt digital twin demonstrations and B2B influencer programs to reach procurement stakeholders. The marketing agencies' market share for niche vertical boutiques rises when specialized compliance knowledge trumps scale, particularly in defense, energy, and pharmaceuticals.

Geography Analysis

North America held 36.05% of global 2025 revenue amid robust enterprise spending and mature ad-tech infrastructure. U.S. clients prioritize AI-enabled creative optimization, while Canada’s antitrust action against Google underscores regulatory momentum toward diversified ad ecosystems. Mexico’s accelerating e-commerce market attracts network agencies that pair cross-border influencer programs with localized creative studios. Europe follows as the second-largest region, with GDPR-driven privacy rigor catalyzing investment in cookieless solutions and first-party data alliances. Agencies that align with regional ESG expectations win competitive bids for sustainability-focused campaigns, especially within Germany and the Nordic states. Linguistic diversity favors hybrid talent models that combine centralized analytics hubs with country-specific creative pods.

Asia-Pacific stands out with a 14.24% forecast CAGR, propelled by mobile-centric consumption, social commerce proliferation, and rising middle-class discretionary spend. China’s marketers employ an average of 12.7 agencies per brand to navigate platform fragmentation across Alibaba, Tencent, and Douyin. India’s SME surge under the Digital India program spurs demand for vernacular content and low-data video formats. Southeast Asian markets embrace influencer-driven live-commerce, prompting agencies to cultivate creator networks fluent in local dialects. Japan’s agency landscape experiences heightened compliance scrutiny following bid-rigging investigations, forcing governance enhancements that global advertisers view favorably. Australia’s retail media boom entices U.S. holding companies to acquire boutique commerce consultancies, signaling ongoing cross-border M&A.

The Middle East and Africa represent smaller but nascent opportunities as sovereign funds finance megaprojects requiring integrated marketing for tourism, smart-city recruitment, and cultural heritage promotion. Agencies with Arabic localization capabilities and Islamic finance expertise position ahead of rivals in Qatar and Saudi Arabia. Latin America’s digital-payment revolution accelerates social-commerce campaigns across Brazil, Argentina, and Colombia, although macroeconomic volatility mandates flexible contract terms. Collectively, regional nuances reinforce the marketing agencies market’s requirement for multilingual, culturally agile service delivery.

Competitive Landscape

The marketing agencies market remains moderately concentrated, with the top five groups, WPP, Omnicom, Publicis Groupe, Interpublic Group, and Dentsu, collectively accounting for a significant portion of 2024 billings. Omnicom’s planned merger with Interpublic, valued at over USD 13 billion, is set to create the world’s largest holding entity and unlock substantial procurement and back-office synergies. WPP defends its leadership by funneling AI spend into its proprietary Open AI Studio that automates copy, imagery, and media-mix forecasting. Publicis Groupe earmarked EUR 300 million (USD 315 million) for AI acquisitions such as Mars United Commerce and influencer platform Influential to deepen commerce and creator capabilities.

Independents leverage agility and niche specialization to secure disruptive wins; for example, R/GA’s algorithm-driven brand-experience practice attracted fintech disruptors seeking unified CX design. Consulting entrants like Accenture Song and Deloitte Digital monetize digital-transformation mandates that bundle cloud migration, data-lake integration, and omnichannel creative. Competitive differentiation increasingly centers on proprietary data clean-rooms, sustainability consulting, and vertical marketplaces that match freelance creators with briefs. Talent wars intensify as agencies court machine-learning engineers and prompt designers to stay ahead of generative AI’s creative potential.

Strategic partnerships multiply: Hakuhodo Technologies now cooperates with NVIDIA to co-develop agentic AI that autonomously refines media strategy based on outcome feedback. Dentsu pursued creator-economy expansion through its House of Creators initiative that fosters Roblox talent pipelines. Technology providers reciprocate by embedding agency-oriented toolkits, as evidenced by Google’s Smartly collaboration. M&A valuations favor agencies boasting integrated commerce, influencer, and AI studios, while traditional shops without scalable tech assets face shrinking multiples. Competitive pressure therefore hinges on investment agility, data sovereignty, and the ability to translate platform innovations into measurable business lift.

Marketing Agencies Industry Leaders

WPP

Omnicom Group

Publicis Groupe

Interpublic Group

Dentsu Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Hakuhodo Technologies announced acceleration of agentic AI development in partnership with NVIDIA, leveraging AI Blueprint and NeMo-Agent-Toolkit to build autonomous ad creation and campaign optimization systems that continuously improve through operational feedback loops.

- September 2025: Google contracted Smartly to test an AI-powered creative automation platform for hardware campaigns, exploring asset automation capabilities to generate large volumes of ad variants across social, display, and video channels with improved efficiency and flexibility.

- July 2025: Publicis Groupe reported strong Q1 2025 performance with 9.4% revenue growth, supported by EUR 300 million (USD 315 million) AI investment and strategic acquisitions, including Mars United Commerce, Influential, and Adopt, to strengthen commerce and influencer marketing capabilities.

- June 2025: Dentsu Group received cease and desist orders from the Japan Fair Trade Commission related to Tokyo 2020 Olympics planning violations, with surcharge payments totaling JPY 920.71 million (USD 6.2 million) due January 2026, though the financial impact on consolidated results is expected to be minimal.

Global Marketing Agencies Market Report Scope

Marketing involves a company's strategic efforts to facilitate the buying and selling of its products or services.

The global marketing agency market is segmented by service type (digital marketing services, traditional marketing services, and full service agencies), application (large enterprises and small and mid-sized enterprises), end user (BFSI, IT and telecom, retail, public services, and manufacturing and logistics), and geography (Europe, North America, Asia-Pacific, Latin America, Middle East, and Rest of the World). The report offers market size and forecast for all the above segments in value (USD).

| Digital Marketing Services |

| Traditional Marketing Services |

| Full-Service Agencies |

| Large Enterprises |

| Small and Mid-Sized Enterprises (SMEs) |

| BFSI |

| IT and Telecom |

| Retail and Consumer Goods |

| Public Services |

| Manufacturing and Logistics |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Service Type | Digital Marketing Services | |

| Traditional Marketing Services | ||

| Full-Service Agencies | ||

| By Application | Large Enterprises | |

| Small and Mid-Sized Enterprises (SMEs) | ||

| By End User | BFSI | |

| IT and Telecom | ||

| Retail and Consumer Goods | ||

| Public Services | ||

| Manufacturing and Logistics | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for global marketing agencies in 2031?

Market value is expected to reach USD 591.63 billion by 2031, growing at a 4.55% CAGR during 2026-2031.

Which service type holds the largest share of agency spending?

Digital marketing services accounted for 61.58% of 2025 revenue due to their measurable performance and omnichannel reach.

Why are SMEs considered a high-growth customer segment for agencies?

SME demand is rising at a 12.97% CAGR because self-serve ad portals and AI tools have lowered adoption barriers, yet many businesses still require strategic guidance.

Which region is forecast to expand fastest through 2031?

Asia-Pacific is on track for a 14.24% CAGR as mobile commerce, social shopping, and digital transformation drive agency engagement.

How are privacy regulations influencing agency technology investment?

GDPR and CCPA accelerate spending on first-party data platforms, contextual AI, and consent management systems to enable cookie less targeting without breaching compliance.

What competitive strategies are leading holding companies pursuing?

Major groups are investing heavily in proprietary AI studios, commerce consulting, and creator-economy partnerships while exploring large-scale M&A to reinforce scale efficiencies.

Page last updated on: