North America Non-Dairy Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

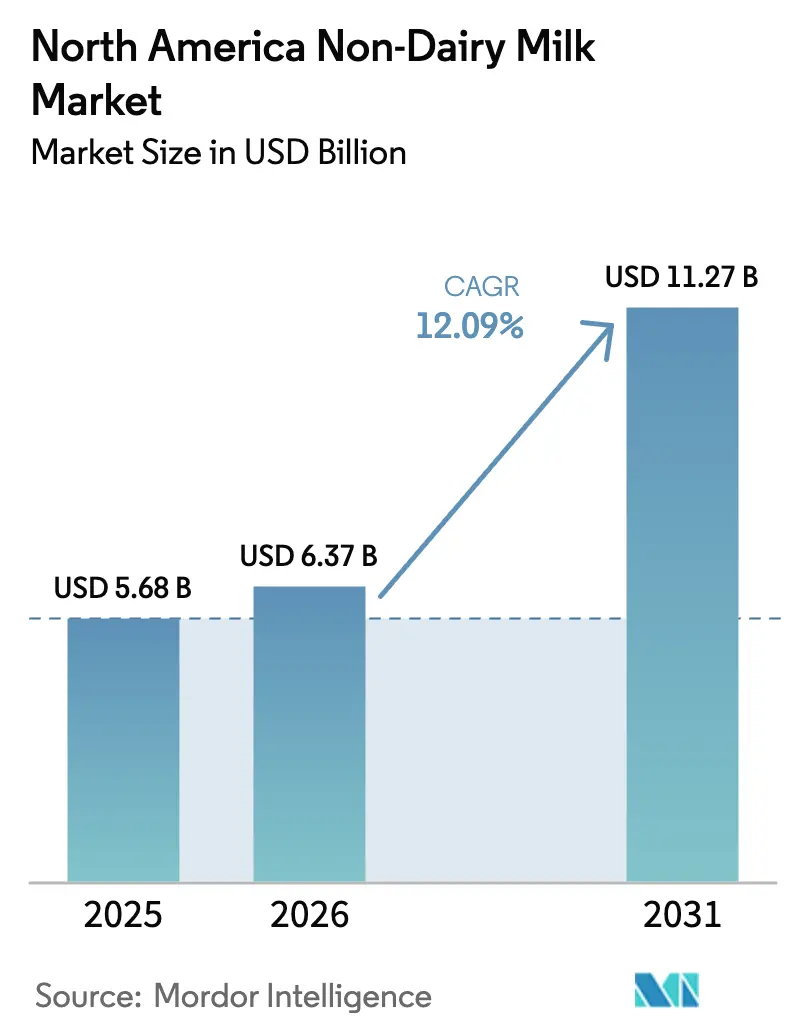

| Base Year Market Size (2025) | USD 5.68 Billion |

| Market Size (2026) | USD 6.37 Billion |

| Market Size (2031) | USD 11.27 Billion |

| Growth Rate (2026 - 2031) | 12.09% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Non-Dairy Milk Market Analysis by Mordor Intelligence

The Non-Dairy Milk market size is expected to grow from USD 5.68 billion in 2025 to USD 6.37 billion in 2026 and is forecast to reach USD 11.27 billion by 2031 at 12.09% CAGR over 2026-2031. A sustained shift toward plant-centric nutrition, heightened awareness of lactose intolerance, and clear evidence of lower environmental footprints compared with dairy are driving that expansion. Consumers in metropolitan areas are adopting premium, fortified products that promise heart and digestive benefits, while quick-service restaurants and coffee chains are scaling plant-based menus to keep pace with evolving tastes. Innovation in enzymatic processing is closing historical gaps in taste and texture, which, together with growing retail shelf space, allows new variants such as hemp and oat milk to move from niche to mainstream. Regulatory signals, including continuing United States Department of Agriculture (USDA) grants for plant-based protein research and Food and Drug Administration (FDA) clarity on labeling rules, reduce policy risk and accelerate capital flows into the category.

Key Report Takeaways

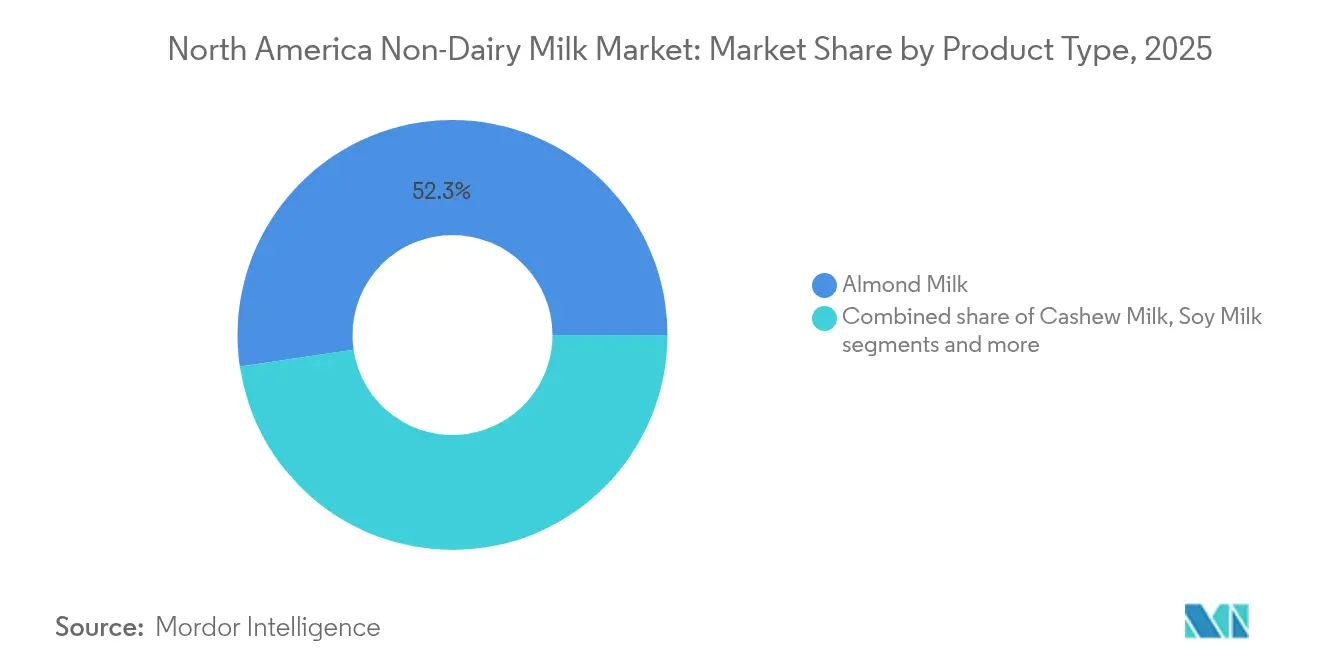

- By product type, almond milk held 52.34% of Non-Dairy Milk market share in 2025, whereas hemp milk is projected to grow at 14.06% CAGR through 2031.

- By packaging type, cartons led with 60.72% of 2025 revenue, while PET bottles are set to expand at 12.89% CAGR to 2031.

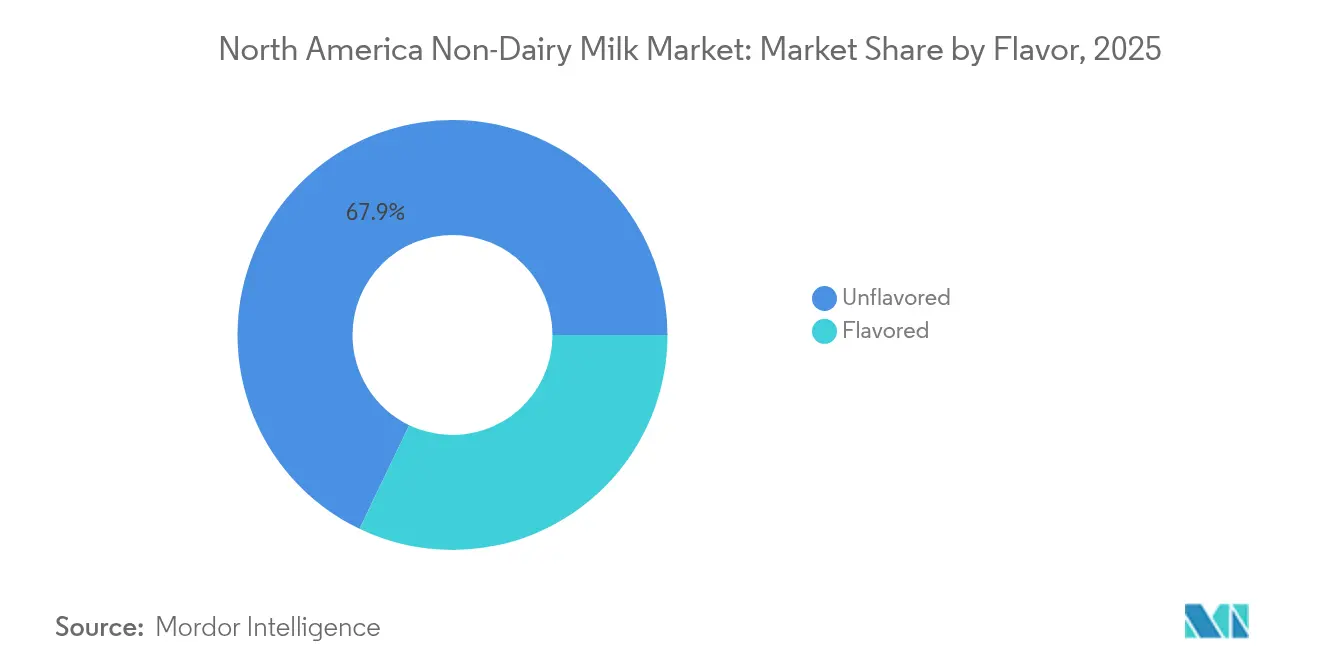

- By flavor, unflavored variants represented 67.88% of 2025 sales; flavored options are expected to advance at 13.01% CAGR during the forecast window.

- By distribution channel, off-trade accounted for 88.05% of 2025 sales, whereas on-trade is forecast to grow at 13.48% CAGR through 2031.

- By country, the United States commanded 82.98% of 2025 sales and Mexico is the fastest growing geography at 13.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Non-Dairy Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing health consciousness and wellness trends | +2.1% | North America, with stronger impact in urban centers | Medium term (2-4 years) |

| Growing prevalence of lactose intolerance and dairy allergies | +1.8% | Regional, with higher concentrations in Hispanic and Asian-American populations | Long term (≥ 4 years) |

| Rise in veganism, flexitarian, and plant-based diets | +2.4% | United States and Canada core markets, expanding to Mexico | Medium term (2-4 years) |

| High awareness of environmental sustainability and animal welfare | +1.9% | North America, particularly among millennials and Gen Z | Long term (≥ 4 years) |

| Government support for plant-based initiatives | +1.3% | United States federal and state level, Canada national programs | Short term (≤ 2 years) |

| Rising demand among younger, urban demographics | +2.2% | Metropolitan areas across United States, Canada, and Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing health consciousness and wellness trends

Health-conscious consumers are increasingly identifying non-dairy milk as functional beverages that provide targeted nutritional benefits beyond basic hydration. The American Heart Association's 2024 dietary guidelines actively promote plant-based protein sources to support cardiovascular health. This endorsement has positioned products like pea protein-enriched oat milk as wellness-oriented options rather than simple substitutes for dairy [1]Source: American Heart Association, "Plant-based proteins may help lower high blood pressure risk", heart.org. Manufacturers are leveraging this trend to implement premium pricing strategies, with organic and fortified variants commanding 30-40% higher prices compared to conventional alternatives. In urban markets, consumers are demonstrating a strong willingness to pay for products that offer perceived health advantages. As a result, functional ingredients such as probiotics, omega-3 fatty acids, and adaptogenic compounds are becoming standard features, further differentiating these products in a competitive market.

Growing prevalence of lactose intolerance and dairy allergies

Consumer interest in protein consumption continues to grow, with 71% of Americans actively seeking to increase their protein intake as highlighted by the International Food Information Council's 2024 Food & Health Survey [2]Source: International Food Information Council, “2024 Food & Health Survey,” ific.org, driving the North America non-dairy milk market as affected individuals across diverse ethnic groups including African Americans, Hispanics, Asian Americans, and Native Americans turn to fortified plant-based alternatives like almond, oat, soy, and coconut milks that deliver high protein alongside digestive comfort. Heightened health awareness prompts consumers to embrace these options for better tolerance, muscle support, and nutrition, fueling innovation in formulations that replicate dairy's creaminess while catering to vegan lifestyles and ethical preferences among younger demographics. This shift strengthens retail availability through supermarkets and online channels, establishing protein-enriched non-dairy milks as everyday essentials.

Rise in veganism, flexitarian, and plant-based diets

Rise in veganism, flexitarianism, and plant-based diets drives the North America non-dairy milk market, as according to the Good Food Institute, 59% of U.S. households purchased plant-based foods in 2024[3]Source: Good Food Institute, "U.S. retail market insights for the plant-based industry," gfi.orga figure consistent with the previous year reflecting sustained mainstream adoption for ethical, environmental, and health motivations that favor sustainable alternatives like almond, oat, soy, and coconut milks over traditional dairy. This shift expands product diversity with innovative flavors, barista blends, and fortified options tailored to clean-label and functional preferences, appealing to multicultural demographics and mainstream buyers via supermarkets, e-commerce, and specialty channels. Brands like Oatly, Califia Farms, and Lactalis capitalize on this trend through clean formulations and partnerships, transitioning non-dairy milks from niche to everyday staples amid growing retail penetration.

High awareness of environmental sustainability and animal welfare

In North America, heightened awareness of environmental sustainability and animal welfare is propelling the non-dairy milk market. Consumers are increasingly turning to plant-based alternatives such as almond, oat, soy, and coconut milks to mitigate the carbon footprint and water usage associated with dairy farming, while also addressing ethical concerns regarding livestock conditions. This shift not only resonates with the demand for clean-label products but has also spurred brands like Oatly and Califia Farms to innovate. These brands are crafting eco-sourced, low-impact formulations, and are strategically targeting ethically-conscious Millennials and Gen Z through transparent packaging and certifications. Additionally, the growing preference for non-dairy milk is driven by its perceived health benefits, including lower cholesterol levels and suitability for lactose-intolerant individuals. With expanded availability in supermarkets, e-commerce platforms, and foodservice channels, non-dairy milks have firmly established themselves as the go-to choice for those seeking sustainable daily nutrition. The increasing variety of flavors and fortified options, such as added vitamins and minerals, further enhances their appeal, making them a versatile and functional alternative to traditional dairy products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing compared to dairy milk | -1.7% | North America, particularly price-sensitive rural markets | Medium term (2-4 years) |

| Taste and texture differences vs traditional dairy | -1.4% | Regional, with regional taste preference variations | Long term (≥ 4 years) |

| Limited nutritional equivalency and fortification challenges | -0.9% | Health-conscious segments across North America | Short term (≤ 2 years) |

| Regulatory constraints on labeling and claims | -0.6% | United States federal level, varying state interpretations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium pricing compared to dairy milk

The market faces significant challenges due to premium pricing, especially when compared to traditional dairy milk. Plant-based alternatives, including almond, oat, soy, and coconut milk, consistently command higher prices. This price disparity stems from the elevated costs associated with raw materials, processing, and fortification. These higher costs make non-dairy options less accessible to budget-conscious households, particularly during periods of inflation. As a result, many price-sensitive flexitarians and mainstream consumers perceive these alternatives as luxury products rather than everyday essentials. This perception further limits their adoption. Brands actively work to address this issue by balancing their premium positioning with the need for volume growth. To achieve this, they are expanding private-label offerings and implementing cost optimization strategies. Despite these efforts, the pricing gap continues to act as a significant barrier, hindering broader market penetration and slowing the adoption of non-dairy milk products across the region.

Taste and texture differences vs traditional dairy

The market faces significant challenges due to taste and texture differences compared to traditional dairy. Consumers often find plant-based alternatives, such as almond, oat, soy, and coconut milks, to have distinct flavor profiles ranging from nutty and beany to cereal-like or watery. These products frequently exhibit thinner consistencies or grainy textures, which fail to replicate the creamy mouthfeel and neutral flavor that define traditional dairy. These sensory gaps discourage both loyal dairy consumers and occasional switchers, particularly in applications like cooking, baking, and coffee preparation. In these scenarios, issues such as separation, bitterness, or inadequate froth often compromise the performance and overall satisfaction of non-dairy options. Manufacturers have actively worked to address these shortcomings by developing innovations in emulsifiers and creating specialized barista blends. While these advancements have mitigated some concerns, the persistent differences continue to limit broader adoption among consumers who prioritize dairy-like sensory experiences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Almond Dominance Faces Hemp Innovation

Almond milk commands the largest market share at 52.34% in the North America non-dairy milk market for 2025. This dominance stems from long-standing consumer familiarity built over years of market presence. Widespread retail availability across supermarkets, online platforms, and specialty stores reinforces its position in the United States and Canada. Major brands like Silk, Almond Breeze, and Califia Farms drive loyalty through extensive distribution and consistent innovation in flavors and formulations. Almond milk's mild taste and low-calorie profile appeal to lactose-intolerant consumers and flexitarians seeking versatile dairy substitutes. Recent launches, such as shelf-stable vanilla variants with clean labels, further solidify its leadership amid rising health consciousness.

Hemp milk emerges as the fastest-growing segment with a 14.06% CAGR projected through 2031 in the North America non-dairy milk market. This rapid expansion reflects surging demand for nutrient-dense alternatives boasting complete protein profiles and omega fatty acids. Health-focused consumers prioritize these benefits, distinguishing hemp milk from less comprehensive options. North America holds a significant portion of the global hemp milk market, supporting high growth rates around 14.5% in the region. Innovations in unsweetened and fortified variants cater to wellness trends and vegan diets. The segment's trajectory signals a broader shift toward sustainable, functional beverages in competitive landscapes.

By Packaging Type: Cartons Lead While PET Bottles Surge

Traditional carton packaging holds the dominant 60.72% market share in the North America non-dairy milk market for 2025. This leadership arises from well-established supply chains that ensure efficient production and distribution across major retailers like Walmart and Kroger. Cartons provide extended shelf life, crucial for preserving freshness in plant-based beverages amid rising demand for almond and oat milks. Consumers associate cartons with superior quality and freshness, enhancing purchase decisions in supermarkets and online channels. The format's versatility supports various sizes, from single-serve to family packs, aligning with diverse household needs. Ongoing innovations, such as recyclable and aseptic cartons, further reinforce its position in a competitive landscape.

PET bottles exhibit the fastest growth at a 12.89% CAGR through 2031 within the North America non-dairy milk packaging segment. This surge stems from convenience features like resealable caps and ergonomic designs tailored for on-the-go lifestyles. Portion-controlled sizes appeal to busy professionals and fitness enthusiasts seeking portable nutrition from hemp or soy milks. PET's lightweight nature reduces shipping costs, benefiting off-trade channels that command 90% of sales. Enhanced barrier properties protect against light and oxygen, maintaining product integrity for extended periods. The shift toward PET reflects broader trends in sustainable plastics and single-use convenience amid expanding plant-based adoption.

By Flavor: Unflavored Foundation Supports Flavored Growth

Unflavored non-dairy milk varieties dominate the North America market in 2025 with a commanding 67.88% share. This large market presence is rooted in consumer preference for versatile products that suit a wide range of uses, including cooking, baking, and cereal consumption, providing consistent demand across multiple applications. The stable demand for unflavored options supports manufacturing efficiencies and simplifies retail planning, ensuring smooth supply chain operations. Consumers often favor unflavored milks for their neutral taste and adaptability to recipes, which enhances their appeal in both household and foodservice sectors. Major brands leverage this preference by offering clean-label, unsweetened formulations, which appeal to health-conscious and allergen-sensitive consumers.

Conversely, flavored non-dairy milk segments are experiencing the fastest growth, with a 13.01% CAGR projected through 2031. This robust growth is driven by continuous innovation in flavor profiles, including seasonal varieties and indulgent options that attract experiential consumers. Flavored milks increasingly incorporate functional ingredients like added vitamins, minerals, and probiotics, targeting specific nutritional needs and wellness trends. The expanding flavor portfolio enhances consumer engagement and encourages trial among younger, trend-sensitive demographics. Brands are investing in barista blends and specialty coffee pairings, further stimulating demand in retail and foodservice channels. This growth indicates a shift toward personalization and taste innovation in the evolving North American non-dairy milk market.

By Distribution Channel: Off-Trade Dominance Faces On-Trade Expansion

Off-trade channels dominate the North America non-dairy milk market with an 88.05% share in 2025, closely aligning with reports of approximately 90% dominance in the region. This commanding position reflects the core household consumption patterns of non-dairy products like almond and oat milks, which consumers stock for daily use in cereals, smoothies, and recipes. Established retail partnerships with supermarkets such as Walmart, Target, and Kroger, as well as hypermarkets and convenience stores, ensure widespread accessibility and dedicated shelf space up to 30% for plant-based options. The segment benefits from robust e-commerce growth through platforms like Amazon, further solidifying its lead amid rising at-home demand post-pandemic. Off-trade stability supports predictable inventory planning and economies of scale for major players like Silk and Califia Farms.

On-trade channels represent the fastest-growing segment at a 13.48% CAGR through 2031 in the North America non-dairy milk market. This expansion is propelled by increasing foodservice adoption in coffee shops like Starbucks, restaurants, and institutional settings including schools and corporate cafeterias seeking vegan-friendly options. Barista-blend formulations optimized for frothing and lattes drive demand, with innovations like Oatly's coffee-focused variants enhancing menu versatility. The channel captures premium pricing opportunities as consumers prioritize plant-based choices in out-of-home dining, fueled by flexitarian trends and lactose intolerance awareness. Growth accelerates through partnerships between brands and chains, expanding non-dairy presence beyond niche cafes to mainstream eateries.

Geography Analysis

The United States commands a dominant 82.98% share of the North America non-dairy milk market in 2025. This position stems from robust retail infrastructure, including major chains like Walmart, Target, Kroger, and Whole Foods, which allocate up to 30% of shelf space to plant-based options. High consumer awareness of lactose intolerance, vegan trends, and environmental sustainability drives premium product adoption among health-conscious demographics. California leads state-level consumption due to its wellness-oriented population, almond production hubs, and eco-awareness, fostering strong demand for local and organic variants. Texas and Florida exhibit rapid growth, fueled by expanding Hispanic communities embracing non-dairy alternatives and rising lactose intolerance recognition in diverse urban areas. Elevated purchasing power enables widespread access to innovative brands like Silk and Califia Farms across supermarkets and e-commerce platforms.

Mexico demonstrates the fastest growth in the region with a 13.18% CAGR through 2031 in the North America non-dairy milk market. Rising disposable incomes among urban middle-class households support premium plant-based purchases amid economic expansion. Urbanization trends concentrate demand in cities like Mexico City and Guadalajara, where modern retail formats introduce diverse almond, oat, and soy options. Cultural shifts toward Western dietary patterns, particularly among millennials and Gen Z, accelerate adoption of non-dairy milks in coffee culture and breakfast routines. Increasing health awareness around dairy allergies and sustainability appeals to younger consumers seeking functional beverages. Local brands and international entrants capitalize on this momentum through targeted marketing and flavor localization.

Canada operates as a stable mature market within North America non-dairy milk, emphasizing organic and premium segments with steady growth. Urban centers like Toronto and Vancouver drive performance, where environmental consciousness and flexitarian lifestyles boost sales of sustainable options like oat milk. Strong retail presence in Loblaws and Sobeys, alongside e-commerce, ensures accessibility for health-focused consumers. Bilingual labeling requirements and provincial health regulations necessitate compliance, favoring established brands with regulatory expertise such as Oatly and Silk. Clean-label innovations and barista blends cater to coffee shop culture prevalent in major cities. The market benefits from high vegan adoption rates and dairy sensitivity prevalence, positioning Canada as a premium niche leader.

Competitive Landscape

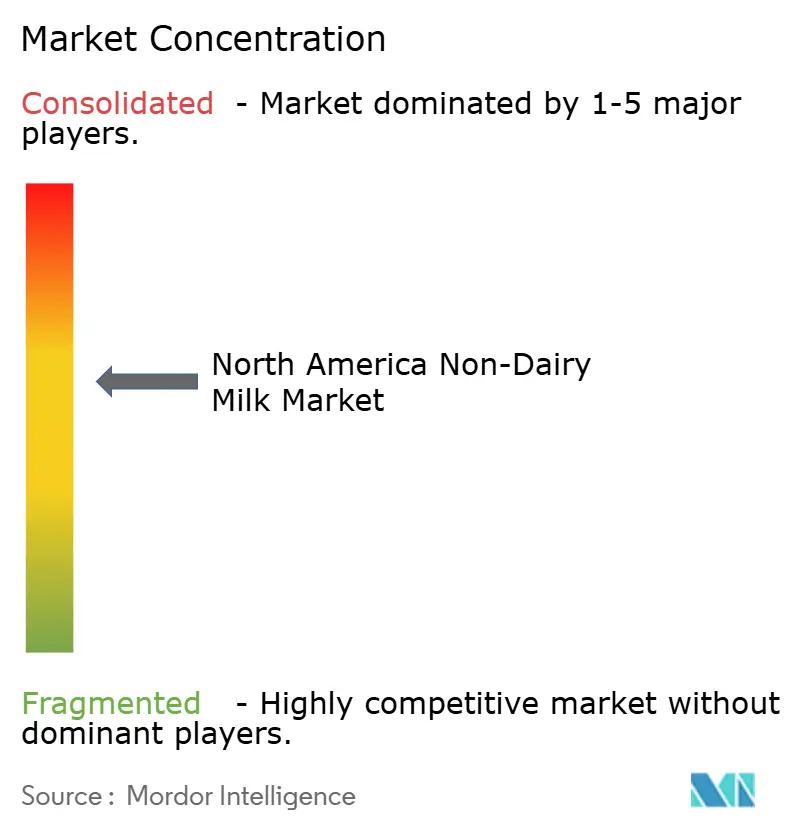

The North American non-dairy milk market presents a moderately fragmented competitive landscape, characterized by the presence of established food conglomerates, specialized plant-based brands, and emerging disruptors. Major players like Danone leverage their extensive global supply chains and distribution networks to achieve cost efficiencies and maintain a strong foothold in the market. On the other hand, pure-play brands such as Oatly and Califia Farms focus on premium positioning, emphasizing innovation and quality to command higher profit margins. This dynamic competition fosters a diverse range of offerings, catering to varying consumer preferences and dietary needs.

A key strategic trend in the market is vertical integration, with companies increasingly investing in ingredient sourcing, processing capabilities, and direct-to-consumer channels. By controlling multiple stages of the supply chain, firms aim to enhance operational efficiency and capture greater value. This approach not only reduces dependency on external suppliers but also enables companies to maintain consistent product quality and respond swiftly to market demands. Such strategies are particularly critical in a market where consumer expectations for sustainability, transparency, and nutritional value are steadily rising.

Technological advancements play a pivotal role in shaping the competitive dynamics of the non-dairy milk market. Innovations in processing techniques, such as enzymatic treatments, high-pressure processing, and specialized emulsification, are helping manufacturers create products that closely mimic the taste, texture, and nutritional profiles of traditional dairy milk. Additionally, significant research and development investments in fermentation technologies and protein extraction methods are evident through a growing number of patent filings. Precision fermentation, in particular, holds the potential to revolutionize ingredient production economics, paving the way for cost-effective and scalable solutions that could redefine the market in the coming years.

North America Non-Dairy Milk Industry Leaders

-

Blue Diamond Growers

-

Califia Farms LLC

-

Campbell Soup Company

-

Oatly Group AB

-

Daone S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Californian plant-based dairy brand Eclipse Foods has unveiled a new whole milk product, claiming it's “indistinguishable” from traditional animal-derived counterparts. Eclipse asserts that its Non-Dairy Whole Milk “truly replicates milk” by isolating proteins from peas and chickpeas and mimicking the molecular structure of dairy.

- June 2024: SunOpta announced a USD 26 million expansion of its Modesto, California facility and secured distribution agreements covering 6,700 retail locations for Dream Oatmilk Barista products. The expansion increases production capacity by 40% and strengthens SunOpta's position in the rapidly growing foodservice segment.

- February 2024: Califia Farms has unveiled its latest offering, Califia Farms Complete. This creamy plant-based milk boasts nine essential nutrients, eight grams of protein, all nine essential amino acids, and contains half the sugar found in traditional dairy milk. Crafted from a unique blend of pea, chickpea, and fava bean proteins.

North America Non-Dairy Milk Market Report Scope

Almond Milk, Cashew Milk, Coconut Milk, Hemp Milk, Oat Milk, Soy Milk are covered as segments by Product Type. Off-Trade, On-Trade are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.| Almond Milk |

| Cashew Milk |

| Coconut Milk |

| Soy Milk |

| Hazelnut Milk |

| Hemp Milk |

| Oat Milk |

| Others |

| Flavored |

| Unflavored |

| PET Bottles |

| Cans |

| Cartons |

| Others (Tetrapacks, Pouches) |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Specialist Retailers | |

| Others | |

| On-Trade |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Almond Milk | |

| Cashew Milk | ||

| Coconut Milk | ||

| Soy Milk | ||

| Hazelnut Milk | ||

| Hemp Milk | ||

| Oat Milk | ||

| Others | ||

| Flavor | Flavored | |

| Unflavored | ||

| By Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others (Tetrapacks, Pouches) | ||

| By Distribution Channel | Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | ||

| Online Retail | ||

| Specialist Retailers | ||

| Others | ||

| On-Trade | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms