Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

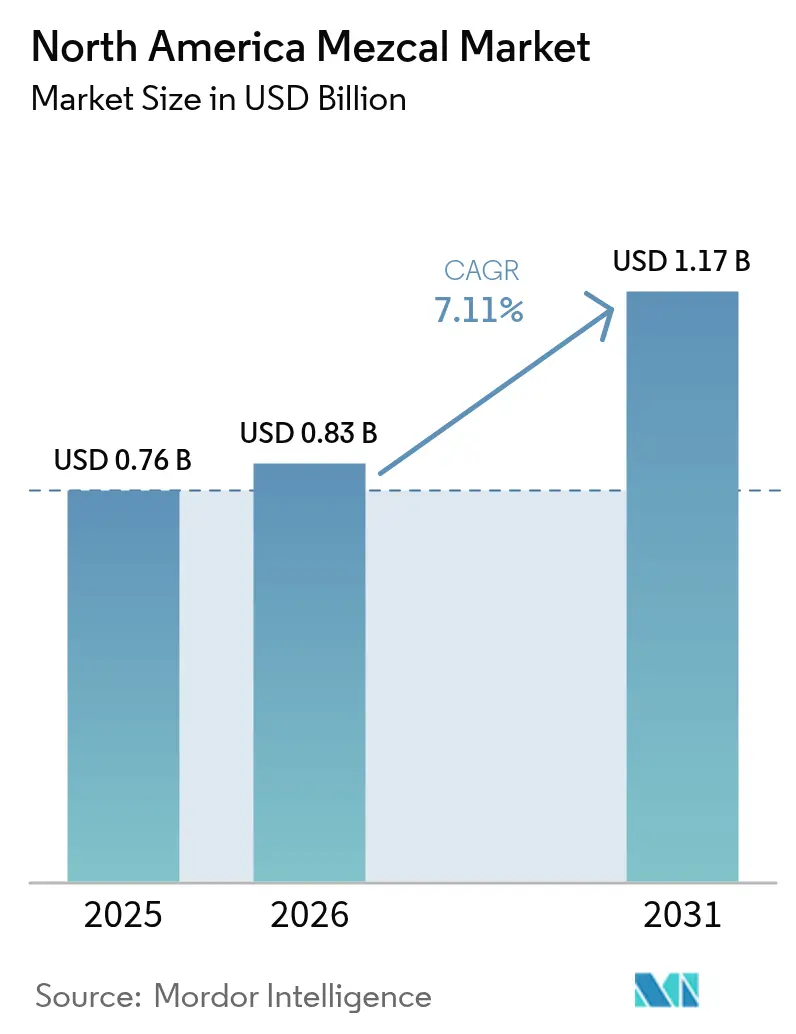

| Base Year Market Size (2025) | USD 0.76 Billion |

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

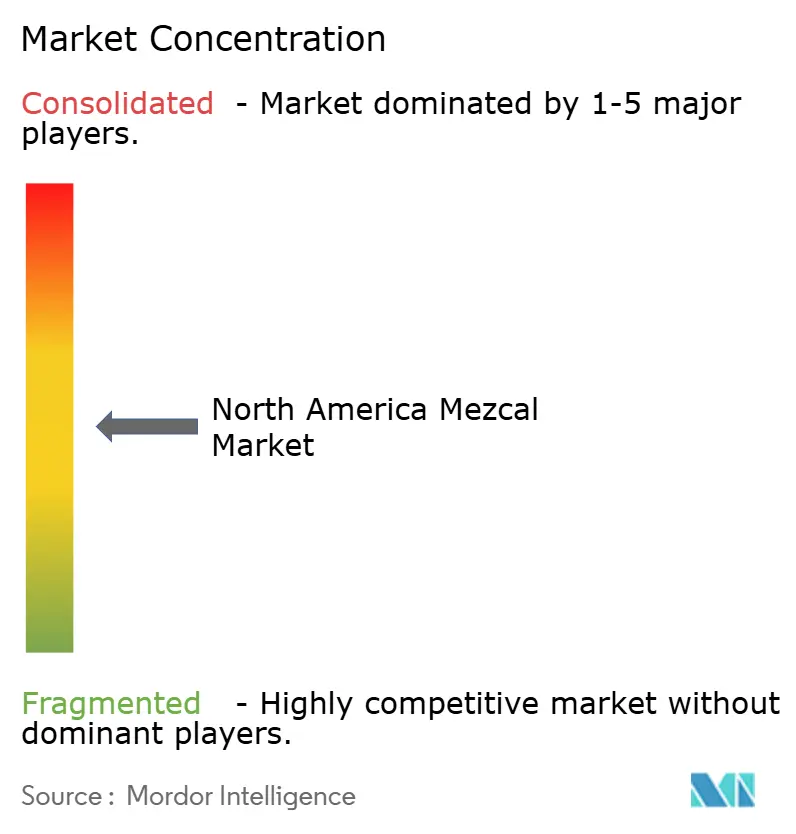

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Mezcal Market Analysis by Mordor Intelligence

The North America mezcal market size is expected to increase from USD 0.83 billion in 2026 to USD 1.17 billion by 2031, growing at a CAGR of 7.11% over 2026-2031. The region’s vibrant cocktail culture, tourism-led discovery, and sustained premiumization have helped mezcal outpace the broader spirits category. Super-premium expressions are adding incremental value as millennials and Gen Z drinkers gravitate toward products with clear provenance and artisanal narratives. U.S. distributors report that limited-release bottles priced above USD 80 sell through in fewer than six weeks, while mass-priced SKUs maintain velocity in grocery and convenience channels. Multinational acquisitions have raised brand visibility and marketing spend, narrowing the gap with tequila at the point of sale. Distribution expansion into e-commerce and specialty stores is further democratizing access, especially in secondary U.S. cities where shelf presence was minimal before 2024.

Key Report Takeaways

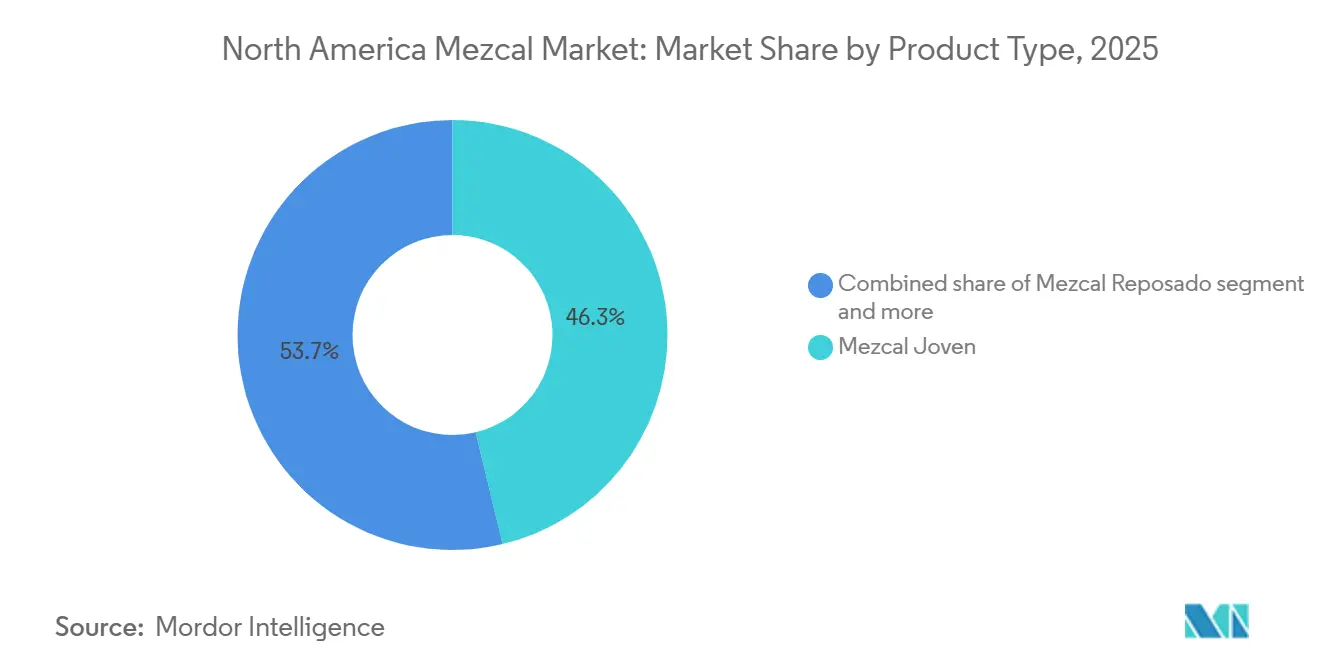

- By product type, Mezcal Joven held 46.27% of the North American mezcal market share in 2025, while Mezcal Reposado is projected to grow at an 8.93% CAGR through 2031.

- By production method, Artisanal mezcal accounted for 65.84% of the North American mezcal market size in 2025; Ancestral format is advancing at an 8.38% CAGR in the same period.

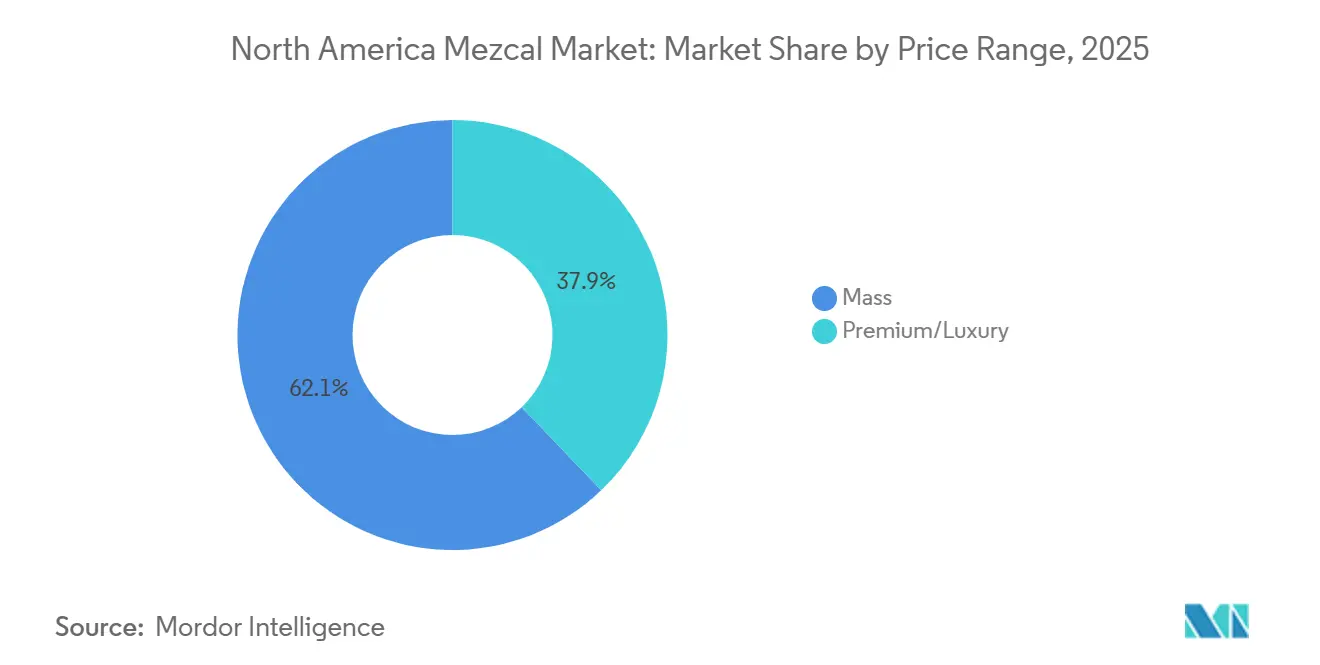

- By price range, the Premium/Luxury tier captured 37.85% the 2025 value and is forecast to expand at a 9.17% CAGR to 2031.

- By distribution channel, off-trade accounted for 68.54% of revenue in 2025, whereas on-trade is growing fastest at 7.94% through 2031.

- By geography, the United States held a 73.13% share of the North American mezcal market in 2025, and Mexico is expected to record the highest 8.07% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Mezcal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for premium and artisanal spirits | +1.9% | United States, Canada, Mexico | Medium term (2-4 years) |

| Rising popularity of craft cocktails and mixology culture | +1.6% | U.S. urban centers, Canada metros, Mexico City | Short term (≤ 2 years) |

| Increasing appreciation for authentic and heritage-driven products | +1.3% | North America-wide | Long term (≥ 4 years) |

| Mezcal tourism and experiential discovery fueling demand | +0.9% | Mexico, spillover U.S. & Canada | Medium term (2-4 years) |

| Growing interest in unique and complex flavor profiles | +1.0% | U.S. craft enthusiasts, Canada premium drinkers | Medium term (2-4 years) |

| Expanding distribution through retail and on-trade channels | +1.5% | U.S., Canada, Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Premium and Artisanal Spirits

The premiumization wave reshaping North American spirits consumption is disproportionately benefiting mezcal, as consumers allocate discretionary spend toward products with transparent provenance and craft narratives. Super-premium mezcal is forecast to grow at approximately 16% annually over the next 5 years, more than double the overall market CAGR, with the United States accounting for 86% of global super-premium mezcal volume, according to Bacardi[1]Source: Bacardi Limited, “Cocktail Trends Report 2024,” bacardilimited.com . This dynamic mirrors the broader tequila and mezcal category, which posted USD 6.7 billion in U.S. retail sales during 2024, up 2.9%, making it the only major spirits segment to register positive growth amid a flat overall market, according to the Distilled Spirits Council of the United States. High-end tequila and mezcal have expanded 1,270% since 2003, while super-premium variants surged 1,500%, underscoring a structural shift where price becomes a quality signal rather than a barrier, according to the Distilled Spirits Council of the United States. The willingness to pay premium prices is particularly pronounced among millennial and Gen Z cohorts, who prioritize authenticity and sustainability claims over brand legacy, creating an opening for smaller artisanal producers to compete on storytelling and terroir differentiation.

Rising Popularity of Craft Cocktails and Mixology Culture

Mezcal's smoky complexity and regional variability have made it a cornerstone of contemporary mixology, with 39% of global bartenders and 48% of Latin American bartenders identifying it as the top spirit to "elevate" cocktails in 2024, according to Bacardi's annual trends survey. This professional endorsement translates into on-premise velocity, as 63% of bartenders express interest in expanding mezcal usage, driving trial among consumers who might not purchase a full bottle for home consumption. The on-trade channel is growing at a 7.94% CAGR through 2031, outpacing the broader spirits market, as the post-pandemic dining and nightlife recovery sustains foot traffic in urban centers, where craft cocktail programs command premium pricing. Ready-to-drink (RTD) cocktails, which surged 16.5% to USD 3.3 billion in 2024 and now represent 14.2% of the U.S. spirits market, are beginning to incorporate mezcal as brands seek differentiation beyond vodka and tequila bases, according to the Distilled Spirits Council of the United States[2]Source: Distilled Spirits Council, “U.S. Spirits Industry Data,” distilledspirits.org. Canned formats dominate RTD with 79.8% share, offering a scalable path for mezcal producers to reach convenience-store shoppers who prioritize portability and portion control.

Increasing Appreciation for Authentic and Heritage-Driven Products

Mezcal's designation of origin (DO) status and artisanal production methods, often involving small-batch distillation in clay pots or copper stills, wild agave harvesting, and multi-generational family recipes, resonate with consumers seeking products that embody cultural heritage and resist industrialization. The Consejo Regulador del Mezcal (CRM) enforces NOM-070 standards that delineate three production categories: Artisanal (65.84% market share in 2025), Ancestral (fastest-growing at 8.38% CAGR), and Industrial, with Artisanal and Ancestral formats commanding price premiums of 30-50% over industrial variants[3]Source: Consejo Regulador del Mezcal, “NOM-070 Standards,” crm.org.mx. This regulatory framework functions as both a quality assurance mechanism and a marketing asset, as certification labels signal authenticity to buyers navigating a crowded shelf set. The heritage narrative is amplified by mezcal tourism, where distillery visits in Oaxaca and surrounding regions allow consumers to witness production firsthand; international tourist arrivals in Mexico climbed 6.8% to 19.4 million during January-May 2025, with spending reaching USD 15.9 billion, according to Datatur Mexico. These experiential touchpoints convert casual tourists into brand advocates who return home and seek out the specific labels they encountered, creating a virtuous cycle of discovery and repeat purchase.

Mezcal Tourism and Experiential Discovery Fueling Demand

The intersection of travel and spirits education is proving to be a potent demand driver, as mezcal-producing regions in Oaxaca, Guerrero, and Durango develop tourism infrastructure that positions distillery visits as cultural experiences rather than mere factory tours. International arrivals to Mexico rose 6.8% year-over-year during January-May 2025, with U.S. air passengers up 4.2% to 6.1 million and Canadian arrivals surging 11.6% to 1.6 million, according to Datatur Mexico. Average spending per visitor reached USD 404.40, reflecting a cohort willing to allocate budgets toward premium experiences, including guided tastings, palenque (distillery) tours, and agave field excursions, according to Datatur Mexico. This experiential discovery translates into post-trip purchasing behavior: travelers returning to the United States and Canada seek to replicate the sensory experience, often gravitating toward the specific brands they sampled. The phenomenon is particularly pronounced in specialty liquor stores and direct-to-consumer channels, where staff can provide tasting notes and provenance stories that mirror the on-site narrative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and certification complexity | -0.5% | Mexico (production compliance), United States and Canada (import documentation) | Long term (≥ 4 years) |

| High production and logistics costs | -0.7% | Mexico (production), United States and Canada (import and distribution) | Medium term (2-4 years) |

| Volatility in agave supply and pricing | -0.8% | Mexico (primary production), spillover to North America pricing | Short term (≤ 2 years) |

| Premium pricing limiting mass-market penetration | -0.6% | United States and Canada (price-sensitive segments) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory and Certification Complexity

Mezcal production and export are governed by NOM-070, which mandates compliance with Consejo Regulador del Mezcal (CRM) certification standards that delineate production methods (Artisanal, Ancestral, Industrial), agave species, and geographic origin across 9 Mexican states. While this regulatory framework protects authenticity and prevents adulteration, it imposes administrative burdens on small producers who lack the legal and technical resources to navigate certification audits, labeling requirements, and traceability documentation. The cost of CRM certification can exceed USD 10,000 annually for smaller palenques, a non-trivial expense when production volumes may total only a few thousand liters per year. Import into the United States and Canada requires additional compliance with TTB (Alcohol and Tobacco Tax and Trade Bureau) and CBSA (Canada Border Services Agency) regulations, including label approvals, tariff classifications, and excise tax filings, creating friction that favors larger distributors with established compliance infrastructure. This regulatory complexity constrains market entry for emerging brands and limits SKU proliferation, as distributors prioritize products with proven velocity to justify the administrative overhead.

High Production and Logistics Costs

Artisanal and Ancestral mezcal production is inherently labor-intensive, involving manual agave harvesting, underground pit roasting, stone-wheel crushing (tahona), open-air fermentation in wooden vats, and small-batch distillation in clay or copper stills. These traditional methods yield lower output per labor hour compared to industrial tequila production, where autoclaves, mechanical shredders, and column stills enable economies of scale. Labor costs in Mexico's mezcal-producing regions have risen alongside broader wage inflation, while transportation expenses have escalated due to fuel price volatility and infrastructure constraints in rural Oaxaca and Guerrero. Restaurant and bar prices in Mexico surged 28.10% year-over-year in May 2025, reflecting input cost pressures that are compressing operator margins and may dampen the willingness to stock premium mezcal pours, according to INEGI Mexico[4]Source: Instituto Nacional de Estadística y Geografía, “Consumer Price Index May 2025,” inegi.org.mx. Cross-border logistics face additional headwinds from potential tariffs on Mexican imports, which the Distilled Spirits Council of the United States has warned would be "catastrophic" for trade flows that reached USD 5.3 billion in 2024, up from USD 2.6 billion in 2020. These cost pressures disproportionately affect smaller producers who lack the purchasing power and distribution scale to absorb margin compression.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reposado Gains as Aging Softens Smoke

Mezcal Joven commanded 46.27% market share in 2025, reflecting its position as the entry point for consumers new to the category and the preferred format for bartenders crafting cocktails where unaged mezcal's bold smoke and vegetal notes provide a structural backbone. However, Mezcal Reposado is expanding at 8.93% CAGR through 2031, the fastest growth among product types, as oak barrel aging introduces vanilla, caramel, and spice notes that broaden appeal beyond the category's traditional smoky profile. Mezcal Añejo and Other Types (including Pechuga and flavored variants) occupy smaller shares but serve as margin-accretive SKUs for producers seeking to differentiate portfolios and capture ultra-premium buyers willing to pay USD 100-200 per bottle.

The Joven segment's dominance is sustained by its versatility in both on-premise and off-premise channels, where bartenders use it as a base for margaritas, Negronis, and original creations, while retail buyers appreciate its lower price point (typically USD 40-60) relative to aged expressions. Reposado's acceleration reflects a maturation of consumer palates, as repeat buyers seek complexity beyond the initial smoke-forward experience. Añejo production remains constrained by barrel availability and the opportunity cost of aging inventory for 12-24 months, limiting supply and reinforcing ultra-premium positioning. The "Other Types" category includes Pechuga mezcal, which incorporates raw chicken breast during distillation to add umami depth, and flavored variants infused with fruits or chiles, both of which appeal to adventurous consumers but face skepticism from purists who view them as departures from tradition.

By Production Method: Ancestral Commands Premium Despite Scale Limits

Artisanal Mezcal held 65.84% market share in 2025, reflecting its balance of traditional production techniques and scalability sufficient to meet distributor volume requirements. Ancestral Mezcal, the most labor-intensive format involving clay-pot distillation and manual agave crushing, is growing fastest at an 8.38% CAGR through 2031, driven by collectors and enthusiasts willing to pay premiums of 50-100% over Artisanal variants for products that embody pre-industrial methods. Industrial Mezcal, produced in autoclaves and column stills, accounts for a smaller share but serves as the entry point for mass-market brands seeking to compete on price with mainstream tequila. The Consejo Regulador del Mezcal's NOM-070 standards enforce clear delineation among these categories, with Ancestral requiring clay-pot distillation and Artisanal permitting copper stills, creating a regulatory moat that prevents industrial producers from co-opting heritage terminology.

The Artisanal segment's dominance reflects its appeal to both premium-seeking consumers and producers balancing tradition with commercial viability, as copper stills enable higher throughput than clay pots while retaining the sensory markers of craft production. Ancestral Mezcal's growth is constrained by production capacity, as clay pot distillation yields only 50-100 liters per batch compared to 500-1,000 liters for copper stills, limiting the ability to scale without compromising authenticity. Industrial Mezcal faces brand perception challenges, as consumers increasingly associate mezcal with artisanal credibility, making it difficult for industrial producers to command premium pricing or secure placement in specialty retail. The segmentation also influences geographic distribution, with Ancestral and Artisanal mezcals concentrated in Oaxaca and Guerrero where traditional palenques operate, while Industrial production is more dispersed across the 9 states within the mezcal DO.

By Price Range: Premiumization Accelerates Despite Mass Dominance

The mass price segment retained 62.15% market share in 2025, anchored by consumers seeking accessible entry points into the category and bartenders requiring cost-effective pours for high-volume cocktails. Yet the Premium/Luxury tier is expanding at 9.17% CAGR through 2031, outpacing the overall market by 2 percentage points, as high-income households allocate discretionary spend toward products with transparent provenance and limited-release cachet. This bifurcation mirrors the broader spirits market, where super-premium tequila and mezcal grew 1,500% since 2003, while mid-tier segments stagnated according to the Distilled Spirits Council of the United States. The Premium/Luxury segment's acceleration is driven by aged expressions (Reposado and Añejo), rare agave varieties (Tobalá, Tepeztate), and single-village bottlings that command retail prices of USD 80-150 and deliver gross margins of 50-60% for producers and distributors.

Mass-market mezcal faces intensifying competition from premium tequila, which has normalized at USD 50-60 price points and benefits from greater brand awareness and broader distribution. Producers targeting the mass segment must balance cost containment with quality perception, as consumers increasingly scrutinize production methods and agave sourcing even at lower price tiers. The Premium/Luxury segment's growth is concentrated in urban markets with high disposable income, New York, Los Angeles, San Francisco, Toronto, Vancouver, where specialty retailers curate portfolios of artisanal and limited-release mezcals that appeal to collectors. E-commerce platforms are democratizing access to ultra-premium expressions, enabling consumers in secondary markets to purchase bottles unavailable in local retail, though direct-to-consumer shipping remains restricted in many U.S. states due to alcohol beverage control regulations.

By Distribution Channel: Off-Trade Dominates but On-Trade Drives Discovery

Off-trade channels commanded 68.54% market share in 2025, with specialty liquor stores and others (including direct-to-consumer) growing fastest as consumers seek curated selections and expert guidance unavailable in grocery chains. On-trade channels are expanding at 7.94% CAGR through 2031, driven by post-pandemic recovery in full-service restaurants and cocktail bars where mezcal's mixology appeal justifies premium pricing and bartenders function as brand ambassadors. The bifurcation between off-trade dominance and on-trade growth reflects distinct purchase occasions: off-trade serves home consumption, gifting, and collector acquisition, while on-trade functions as a trial and education venue where consumers discover brands before seeking them in retail. Specialty liquor stores benefit from staff expertise and portfolio depth, stocking 20-50 mezcal SKUs compared to 5-10 in grocery chains, enabling them to capture enthusiasts willing to pay USD 80-150 per bottle.

Grocery chains and mass merchandisers remain cautious in expanding mezcal shelf space, as category management teams prioritize tequila's proven velocity (31.6 million 9-liter cases in 2023) and margin contribution over mezcal's nascent but growing footprint, according to the Distilled Spirits Council of the United States. On-premise velocity is strongest in urban centers with craft cocktail cultures, New York, Los Angeles, San Francisco, Chicago, Toronto, where bartenders leverage mezcal's smoky complexity to differentiate menus and command USD 14-18 cocktail prices. The on-trade channel also serves as a testing ground for new brands, as distributors use bartender feedback and pour velocity to inform retail placement decisions. Direct-to-consumer platforms are gaining traction, particularly for limited-release and single-village bottlings unavailable through traditional distribution, though regulatory constraints in many U.S. states limit scalability.

Geography Analysis

The United States anchored 73.13% of North America's mezcal market share in 2025, propelled by super-premium segment expansion, craft cocktail culture, and distribution breadth that spans specialty liquor stores, national grocery chains, and on-premise accounts in major metropolitan areas. U.S. spirits imports from Mexico surged from USD 2.6 billion in 2020 to USD 5.3 billion in 2024, with tequila and mezcal accounting for the majority of this growth, as volumes climbed from 53.7 million to 70.7 million proof gallons, according to the Distilled Spirits Council of the United States. The U.S. market captures 86% of global super-premium mezcal consumption, reflecting high disposable income, consumer willingness to experiment with craft spirits, and bartender advocacy that positions mezcal as the next frontier beyond tequila, according to Bacardi. California, New York, Texas, and Florida dominate volume, driven by large Hispanic populations, tourism inflows, and urban cocktail scenes where mezcal enjoys menu prominence. The looming threat of tariffs on Mexican imports represents a material risk, as the Distilled Spirits Council has warned that such measures would be "catastrophic" for cross-border trade flows.

Mexico is expanding at 8.07% CAGR through 2031, the fastest geographic growth rate, driven by domestic premiumization, tourism-linked discovery, and cultural pride in mezcal as a heritage product distinct from industrialized tequila. International tourist arrivals rose 6.8% to 19.4 million during January-May 2025, with U.S. visitors up 4.2% and Canadian arrivals surging 11.6%, creating a virtuous cycle where travelers discover mezcal in Oaxaca and return home as brand advocates, according to Datatur Mexico[5]Source: Datatur Mexico, “Tourism Statistics Jan-May 2025,” datatur.sectur.gob.mx . Domestic consumption is concentrated in Mexico City, Guadalajara, and resort zones (Cancún, Los Cabos, Puerto Vallarta), where rising middle-class incomes support premiumization and bars stock artisanal mezcals alongside tequila. However, restaurant and bar price inflation of 28.10% year-over-year in May 2025 is compressing operator margins and may dampen on-premise velocity, according to the INEGI Mexico. Mexico's dual role as both producer and consumer creates unique dynamics, as domestic brands compete for export allocations versus local market share, with the former offering dollar-denominated revenues that buffer peso volatility.

Canada and Rest of North America represent smaller shares but offer growth opportunities as provincial liquor boards expand mezcal listings and urban markets in Toronto, Vancouver, and Montreal develop craft cocktail scenes that mirror U.S. trends. Canadian spirits imports totaled approximately USD 1.8 billion in 2024, with agave spirits gaining share as consumers seek alternatives to whisky and vodka, as stated by Statistics Canada. Provincial regulations create fragmentation, as each liquor control board maintains distinct listing processes, pricing structures, and distribution networks, requiring producers to navigate 10 separate regulatory regimes to achieve national coverage. The Rest of North America category includes niche markets with limited current penetration but potential for future growth as mezcal awareness spreads beyond core U.S. and Mexican markets.

Regulatory Landscape

Mezcal sold across North America is anchored to Mexico's denomination of origin and NOM-070-SCFI-2016, which defines specifications for production categories (including artisanal and ancestral methods), geographic origin across nine Mexican states, and certification and labeling requirements enforced through accredited conformity assessment bodies and the sector regulator (CRM/COMERCAM in practice). This certification layer acts as a gatekeeper for export, as products generally need valid compliance documentation and seals to be commercialized as mezcal in export markets.

On the import side, the United States requires importers to hold a TTB Basic Permit under the FAA Act and to secure a Certificate of Label Approval (COLA) for bottled products, with labeling governed under 27 CFR requirements. In Canada, commercial importers must hold a Safe Food for Canadians (SFC) licence issued by CFIA, and mezcal is subject to Food and Drug Regulations requirements (including Section B.02.091), which limit modifications of imported spirits largely to adding distilled or purified water for strength adjustment. The combined effect is a multi-agency compliance pathway (CRM/COMERCAM in Mexico, TTB in the United States, CFIA and customs processes in Canada) that increases the documentation burden and favors brands and distributors with established regulatory and label-approval capabilities.

Competitive Landscape

The North America Mezcal Market registers a moderately fragmented competitive structure, characterized by multinational spirits conglomerates acquiring artisanal brands to capture heritage credibility while smaller producers leverage direct-to-consumer and specialty retail to bypass traditional distribution gatekeepers. Pernod Ricard's majority stake in Del Maguey (acquired June 2017), Bacardi's full acquisition of Ilegal Mezcal (completed September 2023), Diageo's purchase of Casa UM/Mezcal Unión (August 2021), and Campari's full buyout of Montelobos (September 2024 for USD 61.8 million) illustrate the strategic premium placed on established artisanal marques that deliver both volume growth and per-case margin expansion. These acquisitions provide multinationals with portfolio diversification beyond tequila and whisky, access to super-premium price tiers, and authenticity narratives that resonate with millennial and Gen Z consumers prioritizing craft over corporate provenance.

White-space opportunities exist in aged expressions (Reposado and Añejo), rare agave varieties (Tobalá, Tepeztate, Arroqueño), and ready-to-drink formats that democratize mezcal access for convenience-store shoppers intimidated by USD 60-80 bottle prices. Smaller artisanal producers are unsettling incumbents by securing direct distribution agreements with specialty retailers, leveraging social media to build brand awareness without traditional advertising budgets, and emphasizing single-village sourcing and transparent supply chains that appeal to ethically minded consumers.

The competitive landscape is further complicated by regulatory compliance under NOM-070 and Consejo Regulador del Mezcal standards, which function as both a quality assurance mechanism and a barrier to entry for producers lacking the legal and technical resources to navigate certification audits. Technology adoption remains limited, with most artisanal producers relying on manual processes, though some are experimenting with blockchain-based traceability to authenticate provenance and combat counterfeiting in export markets.

North America Mezcal Industry Leaders

Pernod Ricard SA

Diageo PLC

William Grant & Sons Ltd

Bacardi Limited

Davide Campari-Milano N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization and cocktail-led discovery continue to create whitespace for portfolio moves beyond core Joven, particularly in aged expressions (Reposado and Anejo) and curated, provenance-forward SKUs that perform in specialty retail and higher-end on-trade programs. A practical adjacent opportunity is mezcal-based ready-to-drink cocktails, where the U.S. spirits market has already established scale in RTD and brands are using mezcal as a differentiation lever beyond vodka and tequila bases. Retail expansion activity in 2026, such as mezcal RTD placements into Whole Foods Market doors in Southern California, underscores that shelf access for convenient formats is being used to broaden household penetration and trial outside traditional spirits aisles.

Supply chain and compliance conditions are also shaping opportunity areas. Certified mezcal production reached 6.91 million liters in 2025, down from 12.24 million liters in 2023 and a 2022 peak of 14.17 million liters, reinforcing the value of long-term agave sourcing, plantation management, and traceability programs for exporters serving the United States and Canada. On the governance side, Cofece actions related to certification-service access (fine imposed in June 2024 on the quality council for past conduct) and sustainability signaling (COMERCAM Distintivo Verde awarded to Rosaluna Mezcal in September 2025) highlight two active tracks for differentiation: credible certification access and verifiable environmental practices (for example, vinasse treatment and bagasse management) that align with premium positioning and retailer scrutiny.

Recent Industry Developments

- May 2026: Mezo Beverages expanded distribution of its ready-to-drink mezcal cocktails (Mezoritas) into 38 Whole Foods Market stores across Southern California. The move strengthens mezcal visibility in a mainstream natural and specialty retail environment and supports trial through single-serve formats that lower the entry barrier versus full bottles.

- December 2025: NOCK Tequila and Mezcal announced official distribution expansion into four major US markets: California, Illinois, New York, and Texas. This step improves route-to-market coverage in core on-trade and off-trade hubs, helping the brand compete for placements where mezcal discovery and cocktail programs are concentrated.

- July 2025: Diageo and Main Street Advisors announced a strategic joint venture to grow the Lobos 1707 Tequila portfolio worldwide, with relevance to North America as a priority market. The partnership structure adds brand-building and distribution capabilities around an agave-spirits platform, intensifying competitive pressure for independent mezcal brands seeking mindshare alongside scaled tequila portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of mezcal sold for beverage consumption across North America through on-trade and off-trade channels, reported in USD.

Scope exclusions: We exclude tequila and other agave spirits that are not labeled and sold as mezcal, and we also exclude non-beverage uses.

Segmentation Overview

- By Product Type

- Mezcal Joven

- Mezcal Reposado

- Mezcal Anejo

- Other Types

- By Production Method

- Artisanal Mezcal

- Industrial Mezcal

- Ancestral Mezcal

- By Price Range

- Mass

- Premium/Luxury

- By Distribution Channel

- On-trade

- Off-trade

- Specialty/Liquor Stores

- Others Off Trade Channels

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by locking the definition of mezcal as it is recognized in market labeling and trade reporting, and then we mapped how demand is formed across on-trade and off-trade. We referenced public sources such as the US Alcohol and Tobacco Tax and Trade Bureau for labeling rules, US International Trade Commission trade statistics for spirits movements, Statistics Canada for alcoholic beverage tables, and Mexico trade and production releases shared by official agencies. To keep the model grounded in real market behavior, we also reviewed association and institute publications on spirits and agave-based categories, along with peer-reviewed papers that discuss agave supply conditions and production constraints.

Next, we compared these signals with company filings, investor presentations, and reputable press coverage to sense-check pricing, distribution expansion, and premiumization direction. Where needed, a paid subscription covering company financials and another covering shipment-level import and export records were used to validate a few volume and pricing assumptions without relying on a single source. The sources listed here are illustrative, and many other public materials were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on gaps that desk sources do not fully explain, mainly around channel splits, realistic price ladders, and how fast premium mezcal is being adopted in key cities. We engaged with importers, distributors, on-trade buyers, and retail category managers across the United States, Canada, Mexico, and the rest of North America so the country mix did not get skewed. Where responses differed, follow-up questions were used to confirm what was counted as mezcal in practice and to adjust assumptions before totals were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | |

| Mid tier: 56% | Functional/Unit leaders: 40% | |

| Smaller Players: 19% | Managers: 48% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up combination, with the top-down side reconstructing a North America demand pool from measurable signals and then splitting it by country. The main inputs included: reported trade movement for mezcal and related spirits, on-trade versus off-trade mix, average price per liter by price range, and the pace of distribution expansion in specialty liquor and broader retail. Supply-side realities were also considered using practical indicators around agave availability and reported production constraints, since these can limit volume even when consumer interest rises.

To keep the totals realistic, we corroborated the output with selective bottom-up approximations, such as sampled revenue roll-ups where public information was available and a volume times average selling price build based on channel checks in the United States and Canada. If a bottom-up view was incomplete, the gap was handled using validated channel ratios and conservative pricing progression instead of forcing a full supplier roll-up. For forecasting, scenario analysis was used and supported by simple time-series smoothing on the key drivers, and we only shifted the curve when multiple interviewees aligned on changes in pricing, availability, or on-trade recovery.

Data Validation & Update Cycle

Validation was carried out in steps, starting with internal consistency checks so country growth rates did not conflict with trade flows, channel realities, or known supply constraints. We compared the model output with independent signals such as spirits category growth, direction of import movement, and observed price shifts, and then reviewed any variance that looked too high for a premium spirit category. Before release, another analyst checks the assumptions and recalculates key tabs so avoidable errors and unrealistic jumps are caught.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as regulatory changes that affect labeling, major pricing resets, or sustained supply shortages. Before delivery, a fresh pass is completed so clients receive an updated view aligned with the latest public data and the most recent primary feedback.

Mordor Intelligence's North America Mezcal Market Sizing Compared With Other Published Estimates

Published estimates for the North America mezcal market can differ even when the topic sounds the same at first glance. Most gaps come from how mezcal is defined versus nearby agave categories, which year is treated as the current base, and whether values reflect retail pricing, trade values, or a blended view.

Some publishers scale a regional number from a global total using a stated regional share, and some apply a faster premiumization curve that raises average price per liter early in the forecast. Those differences can widen the total when channel mix and country coverage are not checked with the same depth. Mezcal-only labeling and channel-level pricing checks are used in the model so adjacent agave spirits and overstated price jumps do not inflate the total, which is the filter applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.76 B (2025) | |

| Industry Publisher A | USD 0.71 B (2024) | Uses a different base year and a shorter horizon, and the value appears to be built from a 2024 revenue snapshot that may not fully align with base-year pricing and country mix assumptions. |

| Industry Publisher B | USD 0.96 B (2025) | Derives the regional number from a global mezcal total using a regional share, so any global scope differences, currency timing, or category overlap can carry into the North America figure without the same country-level channel checks. |

The spread across the three figures is mainly explained by base-year choice and whether the number is constructed from regional channel economics or backed out from a global share. When the value is tied back to country coverage, on-trade and off-trade splits, and realistic price per liter ranges, the result is easier to trace to inputs that can be checked and repeated over time.

Key Questions Answered in the Report

How large will North American mezcal sales be by 2031?

The market is forecast to reach USD 1.17 billion by 2031, rising at a 7.11% CAGR from 2026 levels.

Which country buys the most mezcal in North America?

The United States commands roughly 73% of regional sales, fueled by premium cocktail culture and wide retail distribution.

What is driving mezcal’s premium growth tier?

Super-premium bottles benefit from consumer demand for authenticity; tourism, craft cocktail trends, and artisanal narratives push 16% annual growth for that tier.

Why are agave prices a concern for producers?

Agave plants need up to 12 years to mature, so supply cannot quickly expand, causing price volatility that squeezes distillers’ margins.

Which production method grows fastest?

Ancestral mezcal, distilled in clay pots and crafted entirely by hand, is projected to grow at 8.38% CAGR through 2031 despite limited production runs.

Page last updated on: