Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

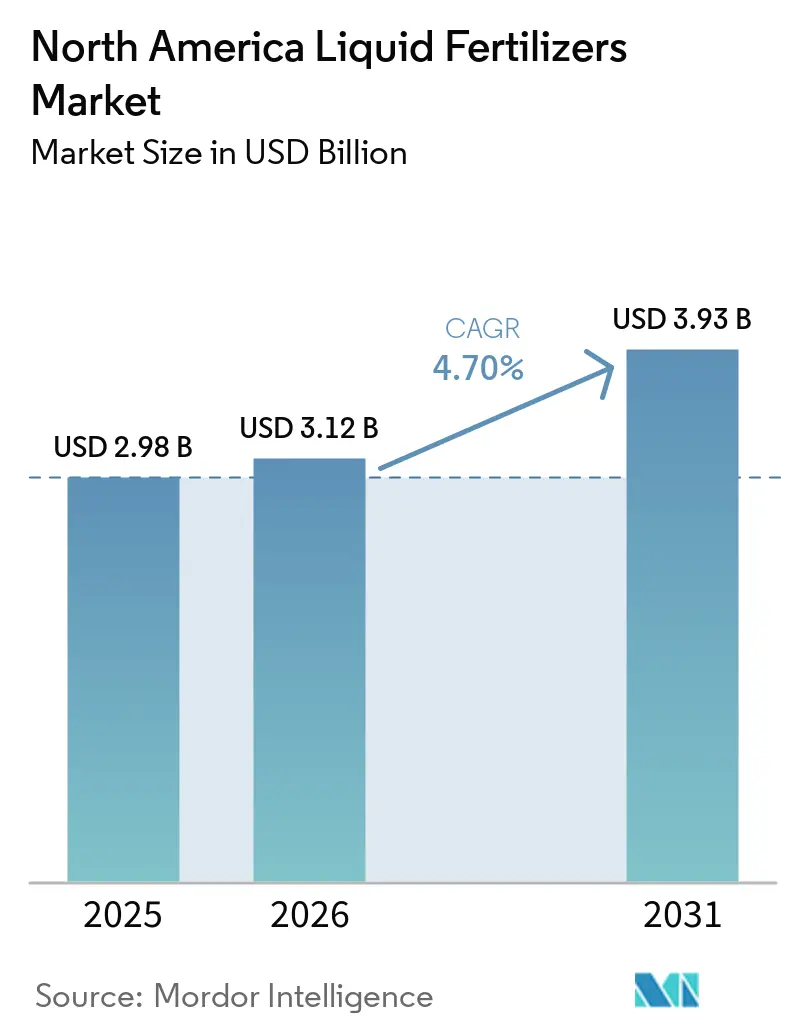

| Base Year Market Size (2025) | USD 2.98 Billion |

| Market Size (2026) | USD 3.12 Billion |

| Market Size (2031) | USD 3.93 Billion |

| Growth Rate (2026 - 2031) | 4.70% CAGR |

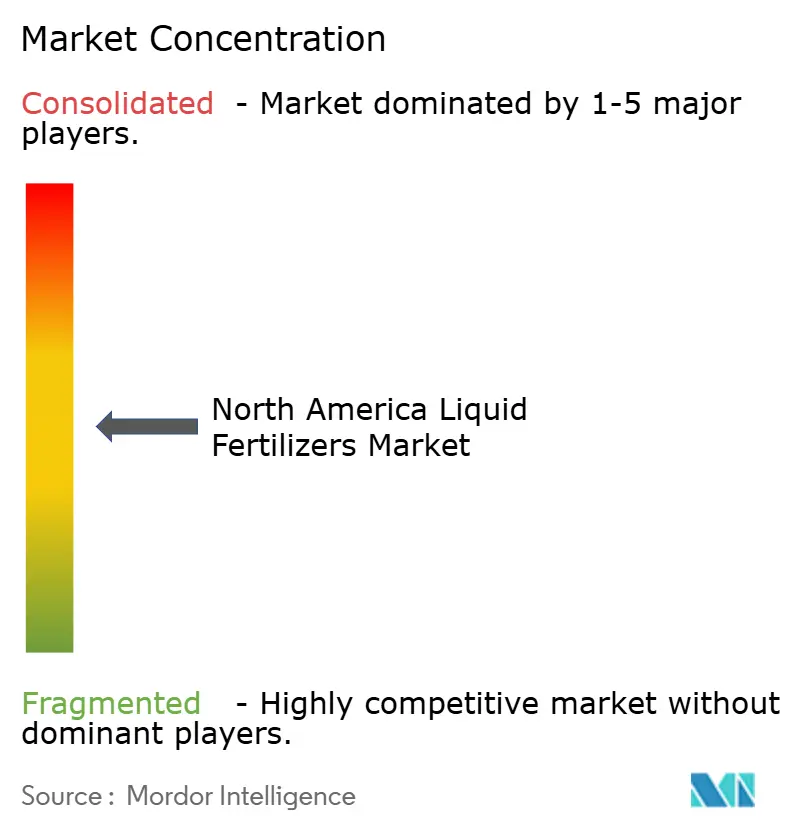

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Liquid Fertilizers Market Analysis by Mordor Intelligence

The North America liquid fertilizers market size is projected to expand from USD 2.98 billion in 2025 and USD 3.12 billion in 2026 to USD 3.93 billion by 2031, registering a 4.70% CAGR between 2026 and 2031. Demand is rising as growers shift toward precision nutrient delivery that aligns with variable-rate application protocols and tightening water-conservation rules. Nitrogen-based liquids dominated value share in 2025, but micronutrient blends are scaling faster because soil tests reveal widespread zinc, iron, and boron depletion in corn and soybean belts. Government funding under the Fertilizer Production Expansion Program is accelerating domestic capacity, while carbon-capture investments are lowering the emissions profile of major ammonia producers. Natural gas price swings and emerging per- and polyfluoroalkyl substances (PFAS) limits add cost pressure and spur the reformulation of certain chelates. Moderate supplier concentration encourages specialty formulators to enter with crop-specific liquids and biologically enhanced products.

Key Report Takeaways

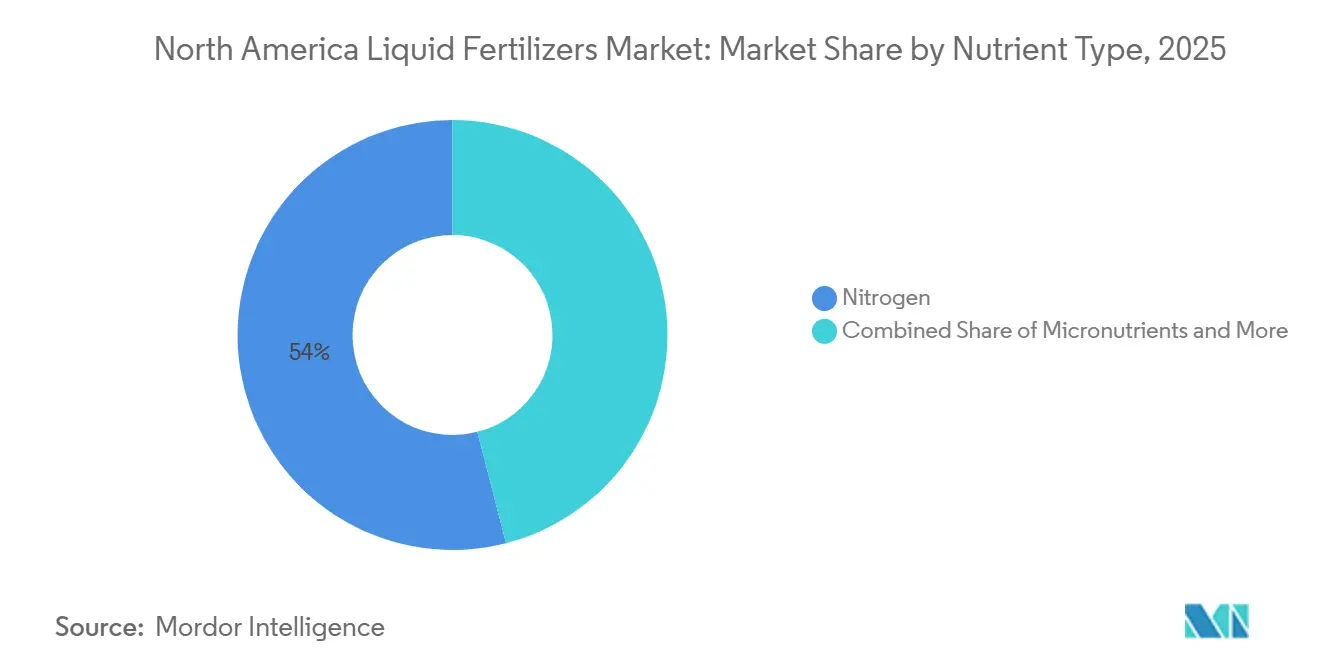

- By nutrient type, nitrogen led the segment with 54% of the North America liquid fertilizers market share in 2025, whereas micronutrients are forecast to grow at a 7.1% CAGR through 2031.

- By ingredient type, synthetic formulations held the largest segment, 72% of the North America liquid fertilizers market size in 2025, while organic liquids are advancing at an 8.1% CAGR to 2031.

- By mode of application, foliar treatments held the largest segment, 43% share of the market in 2025, yet fertigation is projected to expand at a 7.5% CAGR through 2031.

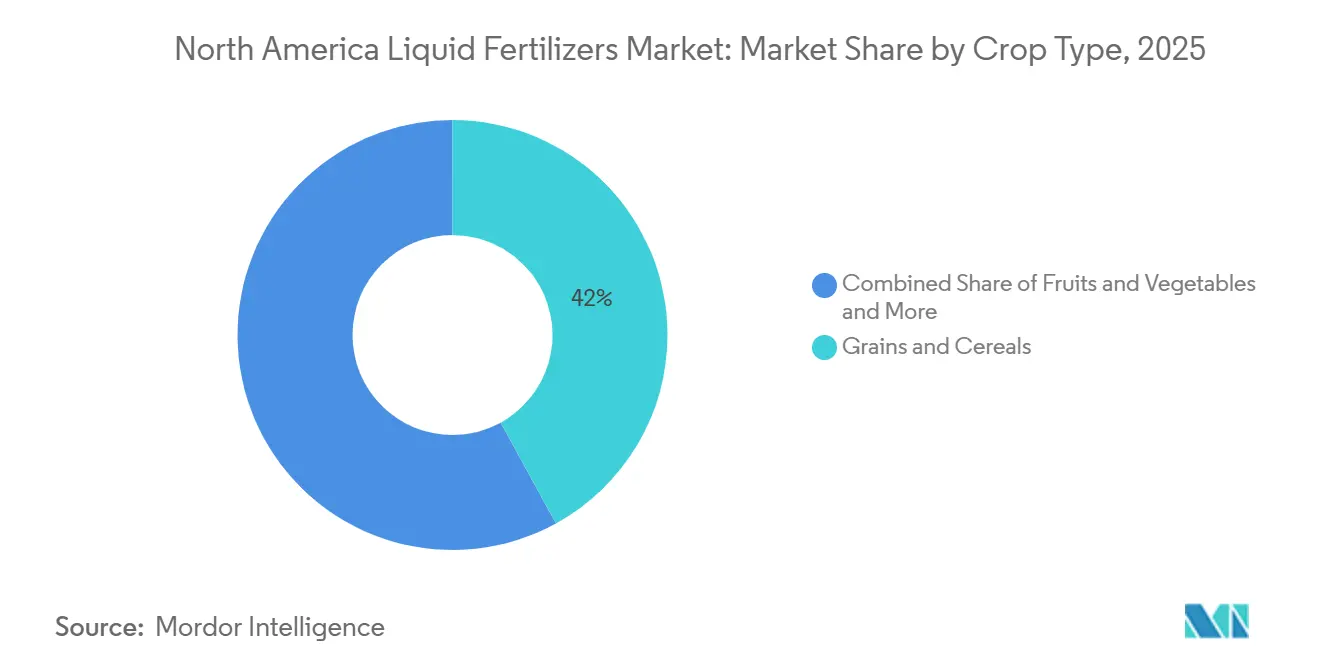

- By crop type, grains and cereals held the largest segment, 42% share of the market in 2025, and fruits and vegetables are poised for a 7.0% CAGR over 2026-2031.

- By geography, the United States dominated 77.0% of the North America liquid fertilizers market in 2025, and is projected to record the highest CAGR of 5.0% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Liquid Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-agriculture adoption accelerates demand for liquid nutrients | +1.2% | United States Corn Belt and Canadian Prairies | Medium term (2-4 years) |

| Shift to fertigation under water-scarcity programs | +1.0% | California Central Valley, Texas High Plains, and Arizona | Short term (≤ 2 years) |

| Crop-specific liquid blends launched by Tier 1 suppliers | +0.8% | United States and Canada | Medium term (2-4 years) |

| Government incentives for domestic fertilizer capacity | +0.7% | United States and Canada | Long term (≥ 4 years) |

| Growth of controlled-environment agriculture hubs | +0.6% | British Columbia, California, Arizona, and Ontario | Long term (≥ 4 years) |

| Adoption of aerial and drone foliar spraying | +0.5% | United States Great Plains and Canadian Prairies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Precision-Agriculture Adoption Accelerates Demand for Liquid Nutrients

Variable-rate equipment covers around 40% of large farms across the Corn Belt and Prairie Provinces, allowing liquids to be metered more precisely than granules[1]Source: Yara International ASA, “Fertilizer Industry Handbook 2025,” yara.com. The adoption of fertigation in high-value crops, such as fruits, vegetables, and specialty grains, is rising, particularly in water-managed regions of the United States and Canada. Liquid fertilizers are compatible with drip and pivot irrigation systems, allowing for simultaneous irrigation and nutrient delivery. This approach enhances nutrient-use efficiency while reducing the number of application passes and associated fuel costs.

Shift to Fertigation Under Water-Scarcity Programs

California’s groundwater law and similar rules in Arizona and Texas push growers toward drip and micro-irrigation that rely on soluble liquids. Multiple small fertigation doses follow crop uptake curves, cutting leaching losses and volatilization. Texas High Plains conversions lifted regional liquid sales by double digits in 2024-2025. Arizona vegetable farms documented nitrogen savings of 25% to 30% after switching from broadcast granules. Compliance deadlines make fertigation a non-negotiable transition for many producers. State and federal conservation programs, supported by agencies such as the United States Department of Agriculture Natural Resources Conservation Service (USDA NRCS), offer financial assistance for drip and micro-irrigation infrastructure. These subsidies help lower initial capital costs for growers, making fertigation systems and their associated liquid fertilizers more cost-effective while supporting objectives for water-use efficiency and nutrient management compliance.

Crop-Specific Liquid Blends Launched by Tier 1 Suppliers

Suppliers are replacing commodity Urea Ammonium Nitrate (UAN) with blends tuned for distinct crops and soils. AgroLiquid’s high-pH-tolerant iron product addresses soybean iron-deficiency chlorosis in calcareous soils. California Organic Fertilizers patented a biological nitrogen-conversion liquid for organic berries and vegetables, while ALPINE extended its potassium acetate line, which has dominated Canadian starter markets since the 1970s. Specialty formulations command premium prices, improving supplier margins. Suppliers are increasingly utilizing soil analytics, tissue testing, and digital agronomy platforms to create precise liquid blends tailored to specific field conditions. This move toward prescription-based nutrition improves crop performance while strengthening customer relationships.

Adoption of Aerial and Drone Foliar Spraying

Federal Aviation Administration (FAA) Part 137 waivers allow drones to apply 1-3 gallons per acre, opening new avenues for late-season foliar nutrition in small or saturated fields. Drones minimize soil compaction and let operators finish within scarce weather windows. Yield responses from V10 corn nitrogen top-dress via drone match ground rigs, making the service commercially viable. The emergence of specialized drone application service providers in the United States and Canada is making foliar spraying more accessible without requiring significant upfront investments. These custom applicators offer per-acre pricing models, allowing mid-sized farms to experiment with late-season liquid nutrition strategies without investing in their own drone fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of natural-gas feedstock prices | −0.6% | United States Gulf Coast and Alberta | Short term (≤ 2 years) |

| Corrosive handling and storage infrastructure costs | −0.4% | North America | Short term (≤ 2 years) |

| Per- and polyfluoroalkyl substances (PFAS) and emerging contaminant regulation pressure | −0.3% | United States and Canada | Medium term (2-4 years) |

| Cold-chain constraints for biologically enhanced liquids | −0.2% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corrosive Handling and Storage Infrastructure Costs

Urea Ammonium Nitrate (UAN) and ammonium polyphosphate require stainless tanks and corrosion-resistant pumps, which roughly doubles capex compared to dry storage solutions[2]Source: U.S. Environmental Protection Agency, “PFAS National Primary Drinking Water Regulation,” epa.gov . Secondary containment adds further expense, discouraging small dealers from stocking liquids and limiting rural service density. Liquid fertilizer systems, particularly those using Urea Ammonium Nitrate (UAN), accelerate wear on seals, valves, hoses, and pump components due to their corrosive properties. This results in more frequent replacements, increased downtime during critical application periods, and higher operating costs compared to dry fertilizer handling systems.

Cold-Chain Constraints for Biologically Enhanced Liquids

Microbe-infused liquids must be kept between 40 °F and 70 °F, yet many farm supply chains lack refrigerated warehouses. Added logistics cost of USD 0.10-0.20 per gallon deters widespread stocking, hampering adoption despite agronomic benefits. The need for temperature-controlled storage, monitoring product conditions, and implementing first-in-first-out (FIFO) inventory systems increases operational complexity throughout the supply chain. For growers, concerns regarding product efficacy due to inadequate storage or transportation conditions can undermine confidence and hinder adoption, even when significant agronomic benefits are evident.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nutrient Type: Micronutrient Momentum in Depleted Soils

Nitrogen led the segment with 54% of the North America liquid fertilizers market share in 2025, supported by large corn and wheat acreages that favor sidedress Urea Ammonium Nitrate (UAN) . Corn, wheat, and soybean acreage in the United States and Canada continues to drive significant demand for nitrogen fertilizers, particularly in liquid form, due to their quick soil absorption and compatibility with variable-rate application and fertigation systems.

Micronutrients are forecast to grow at a 7.1% CAGR through 2031, spurred by iron and zinc deficiencies across calcareous soils in the upper Midwest. The adoption of digital agronomy tools and soil-testing platforms by growers has increased demand for targeted micronutrient applications, such as zinc, iron, manganese, and boron. Unlike commodity nitrogen fertilizers, micronutrients and custom liquid blends are priced higher per gallon, providing suppliers with improved profitability and encouraging investment in research and development as well as customized formulations.

By Ingredient Type: Organic Blends Capture Specialty Crop Spend

Synthetic formulations held the largest segment, 72% of the North America liquid fertilizers market size in 2025, but expanded modestly as commodity acreage is already well penetrated. Synthetic liquid fertilizers, such as urea-ammonium nitrate (UAN), ammonium polyphosphate, and potassium nitrate, are widely used because they deliver highly concentrated nutrients in readily soluble forms. Their predictable nutrient composition enables growers to precisely match application rates to crop requirements, making them particularly suitable for large-scale grain and cereal production. Additionally, synthetic liquid fertilizers integrate effectively with variable-rate and fertigation systems, further solidifying their role in modern North American agricultural practices.

Organic liquids are advancing at a 8.1% CAGR to 2031, driven by demand from certified facilities and greenhouse vegetables that require National Organic Program compliance. Organic liquid fertilizers, derived from plant, animal, or microbial sources, are increasingly adopted for fruits, vegetables, and specialty crops. These fertilizers enhance soil health and microbial activity while aligning with regulatory and consumer-driven sustainability objectives. High-value crop growers are particularly drawn to organic liquids for their ability to deliver targeted nutrients without synthetic residues, thereby supporting both product quality and environmental sustainability.

By Mode of Application: Fertigation Gains under Water-Stress

Foliar treatments held the largest segment, 43% of the North America liquid fertilizers market share in 2025, as growers favor quick canopy uptake and compatibility with crop-protection tank mixes. Foliar liquid fertilizers offer an efficient way to address nutrient deficiencies during the growing season. Unlike soil applications, foliar treatments bypass challenges such as poor soil mobility or pH interference, allowing nutrients to be absorbed directly through the leaves. This approach is especially popular for correcting micronutrient deficiencies, such as zinc, manganese, or iron, when rapid intervention is required. Foliar applications also provide flexibility, enabling growers to optimize timing based on crop growth stages, weather conditions, and labor availability.

Fertigation is projected to expand at a 7.5% CAGR through 2031, the application of liquid fertilizers through irrigation systems, facilitates precise nutrient management aligned with plant uptake patterns, minimizing losses from leaching or volatilization. This method is particularly effective for high-value fruit, vegetable, and specialty crops, where frequent, small doses enhance yield and quality. Fertigation also supports water conservation by synchronizing nutrient delivery with irrigation schedules, thereby maximizing nutrient and water use efficiency.

By Crop Type: Fruits and Vegetables Propel High-Value Demand

Grains and cereals held the largest segment, 42% of the North America liquid fertilizers market size in 2025. Crops such as corn, wheat, and barley account for the largest share of liquid fertilizer use in North America. Their extensive cultivation areas and significant nitrogen and phosphorus requirements make liquid fertilizers, particularly Urea Ammonium Nitrate (UAN) and ammonium polyphosphate, suitable for rapid soil incorporation and precise in-season adjustments. Large-scale farms benefit from the compatibility of liquid fertilizers with variable-rate and fertigation systems, enabling efficient application tailored to plant growth stages and soil variability.

Fruits and vegetables are poised for a 7.0% CAGR over 2026-2031, although grains dominate overall usage, fruits and vegetables are increasingly adopting liquid fertilizers to meet the specific nutrient needs of high-value crops. Techniques such as foliar sprays, fertigation, and biologically enhanced liquids help growers optimize yields, address mid-season nutrient deficiencies, and enhance product quality. Custom blends, including micronutrients and organic formulations, are particularly beneficial in fruit and vegetable production, where nutrient imbalances can significantly affect both appearance and taste.

Geography Analysis

The United States accounted for 77.0% of the North America liquid fertilizer market in 2025 and is projected to register the highest CAGR of 5.0% during 2026–2031. This growth is supported by 1,700 Nutrien retail branches, which ensure efficient in-season delivery[3]Source: Nutrien Ltd., “Retail Network,” nutrien.com. Factors such as California's groundwater mandates and the depletion of the Ogallala Aquifer in Texas are driving increased fertigation installations, resulting in double-digit growth in liquid fertilizer sales across western states.

Canada ranked second in the market, driven by the adoption of seed-placed liquid starter fertilizers in Prairie no-till systems and a strong greenhouse presence in British Columbia and Ontario. Alpine Liquid Fertilizer’s established Bio-K technology has gained significant agronomic trust among canola and corn growers. Additionally, favorable natural gas prices in Alberta provided Canadian producers with a cost advantage through 2025.

Mexico is a growing market, supported by export-oriented berry and vegetable farms in Sinaloa and Michoacán that utilize drip fertigation to meet the quality standards of United States buyers. This has led to increased adoption of high-purity liquid fertilizers. However, infrastructure limitations and fragmented retail channels are constraining short-term growth. Investments in cold-chain logistics and irrigation systems are gradually addressing these challenges. The rest of North America, including select Central American nations, holds a smaller but growing share of the market. Vertical farming and greenhouse initiatives near urban centers are contributing to this growth. Additionally, regional trade agreements are facilitating cross-border movement of specialty liquid fertilizers, expanding the accessible market.

Competitive Landscape

The North American liquid fertilizer market is moderately concentrated, with the top five companies accounting for a significant market share as of 2025. Nufarm Limited leads the market by utilizing its retail network to combine agronomy services with liquid fertilizers. Yara International ASA closely integrates its foliar product lines with digital crop modeling tools. The Mosaic Company leverages its integrated phosphate mining operations to maintain a strong position. AgroLiquid and Haifa Group focus on niche categories such as micronutrients and fertigation solutions.

Key strategic initiatives in the market include vertical integration and the adoption of low-carbon production methods. For instance, CF Industries has commissioned a 2-million metric tons CO₂ capture unit, securing tax credits and enhancing its environmental, social, and governance (ESG) credentials. Additionally, emerging competitors are gaining traction by offering innovative solutions, such as drone application packages and fertigation controller software, to meet the growing demand for precision agriculture. Companies like California Organic Fertilizers and other independent players are capitalizing on patent-protected biological processes to strengthen their position in the organic fertilizer segment.

Success in the North American liquid fertilizer market increasingly hinges on the ability to develop sustainable products while maintaining cost efficiency. Established players are focusing on enhancing their market position by investing in advanced manufacturing technologies, expanding eco-friendly product portfolios, and developing integrated digital solutions for precision agriculture. The market is also placing greater emphasis on building direct relationships with end users by offering specialized agricultural advisory services and customized product solutions. Furthermore, there is a growing focus on meeting the rising demand for organic and biological liquid fertilizers.

North America Liquid Fertilizers Industry Leaders

Yara International ASA

Nufarm Limited

The Mosaic Company

Haifa Group

AgroLiquid

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AgroLiquid is strengthening its presence in the United States through the acquisition of Monty's Plant Food Company and the establishment of a new 20-acre production facility in Lake City, Florida. This expansion is intended to improve liquid fertilizer distribution in the Southeast region and integrate AgroLiquid's nutrition products with Monty's humic technology.

- September 2024: Yara North America has launched the YaraAmplix biostimulant portfolio in the United States and Canada, reinforcing its commitment to sustainable and resilient food systems. Developed over five years of research, the portfolio enhances crop resilience, nutrient uptake, crop quality, soil health, and adaptability to environmental stressors.

North America Liquid Fertilizers Market Report Scope

Liquid fertilizers are nutrient formulations in liquid form, either organic or inorganic (synthetic), designed to provide essential nutrients such as nitrogen (N), phosphorus (P), potassium (K), and micronutrients to crops, enhancing growth and productivity.

The North America Liquid Fertilizers Market is segmented by nutrient type into nitrogen, potassium, phosphate, and micronutrients, and by ingredient type into organic and synthetic. It is also segmented by mode of application into starter solution, foliar application, fertigation, injection into soil, and aerial and drone application, and by crop type into grains and cereals, pulses and oilseeds, commercial crops, fruits and vegetables, and turf and ornamentals. Geographically, the market is segmented into the United States, Canada, Mexico, and the rest of North America. The market forecasts are provided in terms of value in USD.

By Nutrient Type

| Nitrogen |

| Potassium |

| Phosphate |

| Micronutrients |

By Ingredient Type

| Organic |

| Synthetic |

By Mode of Application

| Starter Solution |

| Foliar Application |

| Fertigation |

| Injection into Soil |

| Aerial and Drone Application |

By Crop Type

| Grains and Cereals |

| Pulses and Oilseeds |

| Commercial Crops |

| Fruits and Vegetables |

| Turf and Ornamentals |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Nutrient Type | Nitrogen |

| Potassium | |

| Phosphate | |

| Micronutrients | |

| By Ingredient Type | Organic |

| Synthetic | |

| By Mode of Application | Starter Solution |

| Foliar Application | |

| Fertigation | |

| Injection into Soil | |

| Aerial and Drone Application | |

| By Crop Type | Grains and Cereals |

| Pulses and Oilseeds | |

| Commercial Crops | |

| Fruits and Vegetables | |

| Turf and Ornamentals | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How big is the North America liquid fertilizers market in 2026?

The North America liquid fertilizers market is estimated to be USD 3.12 billion in 2026.

What is the projected growth rate for liquid fertilizers across North America to 2031?

Revenue is forecast to rise at a 4.70% CAGR between 2026 and 2031.

Which nutrient category will grow fastest?

Micronutrient liquids are projected to expand at 7.1% per year through 2031.

Which country offers the highest growth potential?

United States is the fastest-growing geography because export-oriented berry and vegetable producers are investing in precision fertigation infrastructure.

Page last updated on: