North America Insulated Shipping Containers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

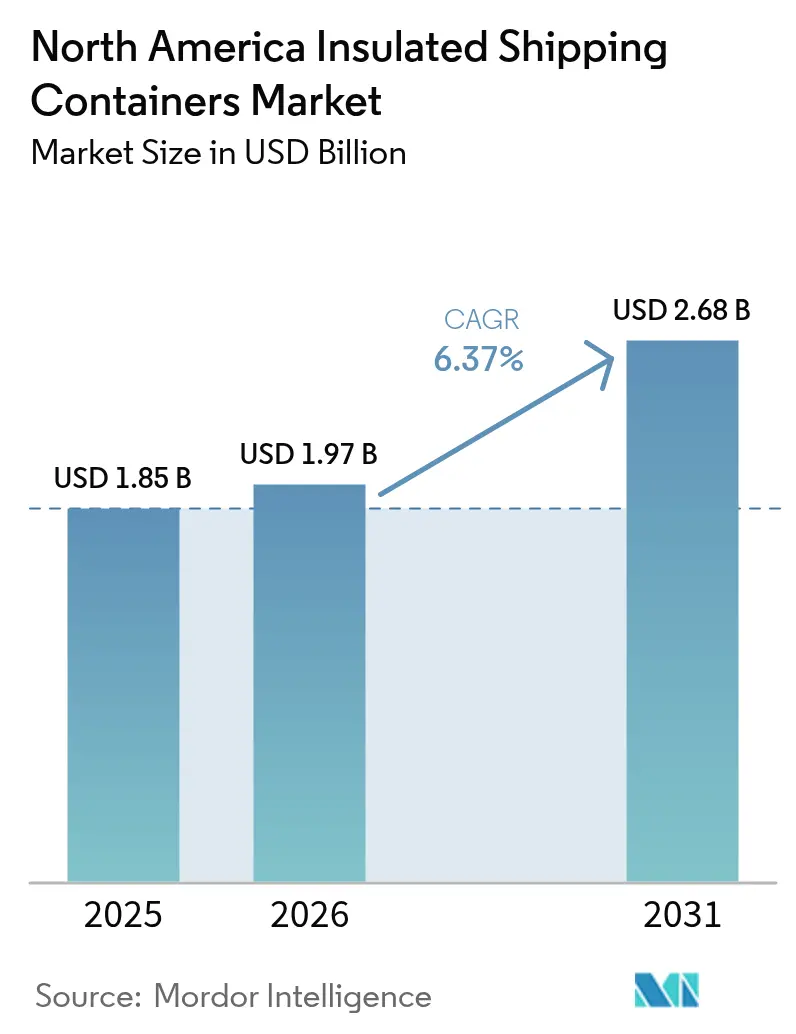

| Base Year Market Size (2025) | USD 1.85 Billion |

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 6.37% CAGR |

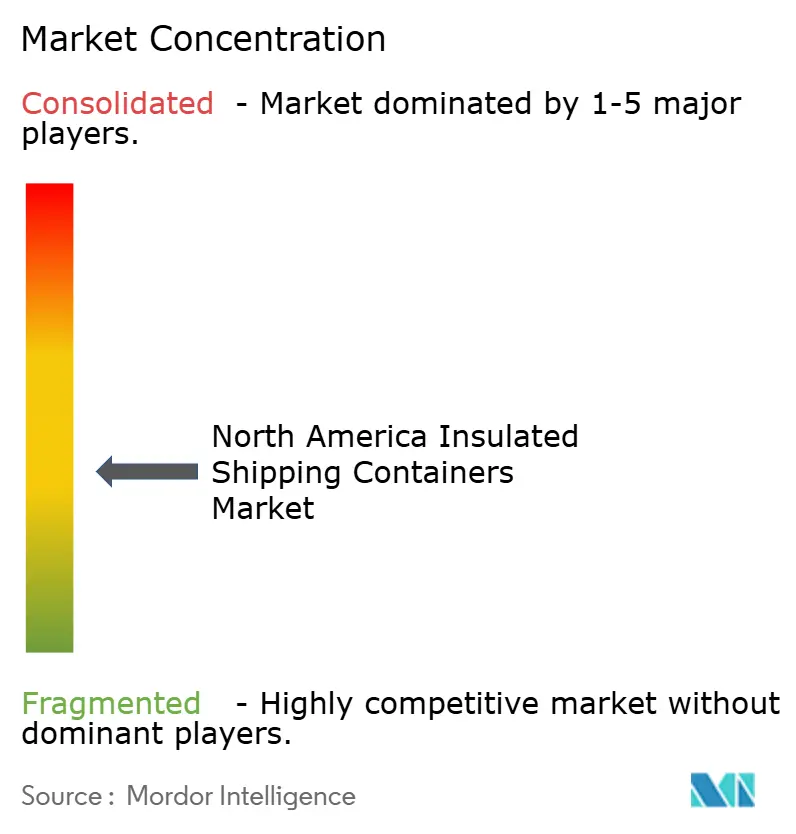

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Insulated Shipping Containers Market Analysis by Mordor Intelligence

North America insulated shipping containers market size in 2026 is estimated at USD 1.97 billion, growing from 2025 value of USD 1.85 billion with 2031 projections showing USD 2.68 billion, growing at 6.37% CAGR over 2026-2031. Pharmaceutical cold-chain investments, the surge in temperature-sensitive meal kits, and retailer sustainability mandates drive continued growth. Expanded polystyrene (EPS) maintains widespread use because of its cost advantage, yet biodegradable starch-blend foams capture rising interest as sustainability regulations tighten. Mid-capacity formats (5-20 L) hold the largest unit demand, while small formats (≤5 L) expand fastest in line with personalized medicine and direct-to-consumer food delivery. Competitive dynamics remain moderate as established suppliers such as Sonoco and TemperPack confront specialized entrants that emphasize bio-based materials and smart packaging systems.

Key Report Takeaways

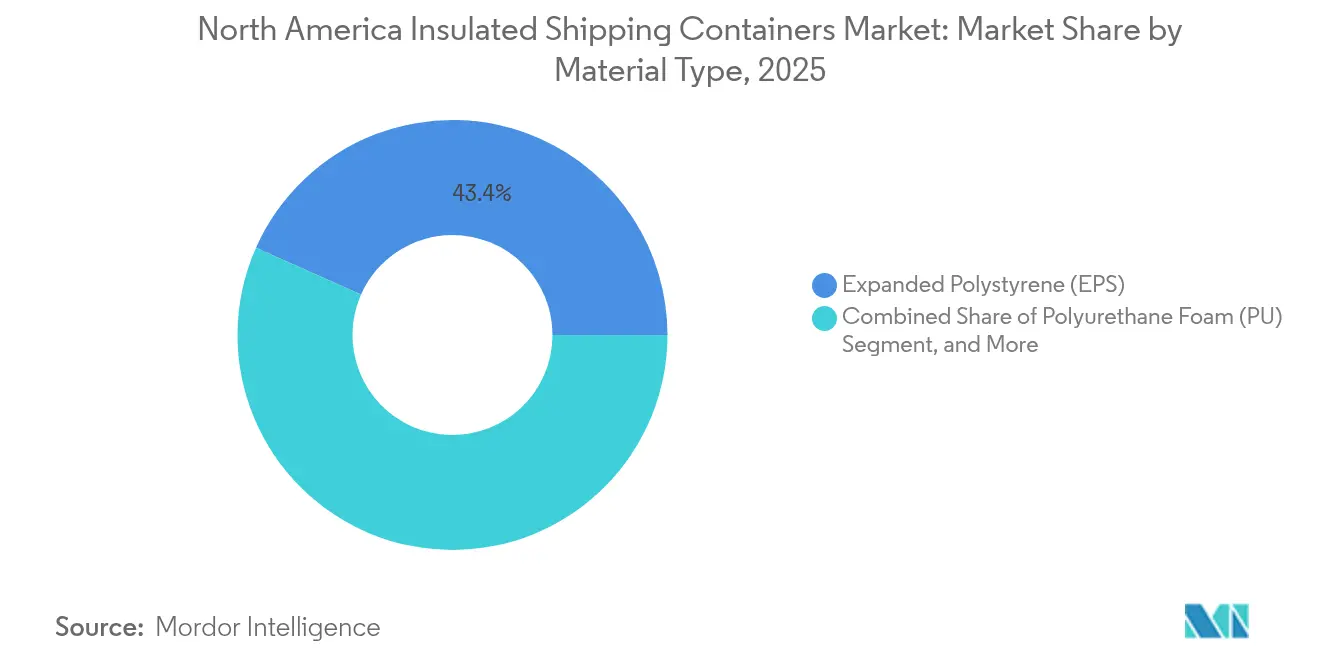

- By material type, EPS led with 43.35%of the North America insulated shipping containers market revenue share in 2025, while biodegradable starch-blend foams are expected to grow at a 6.74% CAGR through 2031.

- By end-user application, life sciences and pharmaceuticals held a 37.45% share of the North America insulated shipping containers market size in 2025; fresh meat and seafood are forecast to expand at a 6.79% CAGR to 2031.

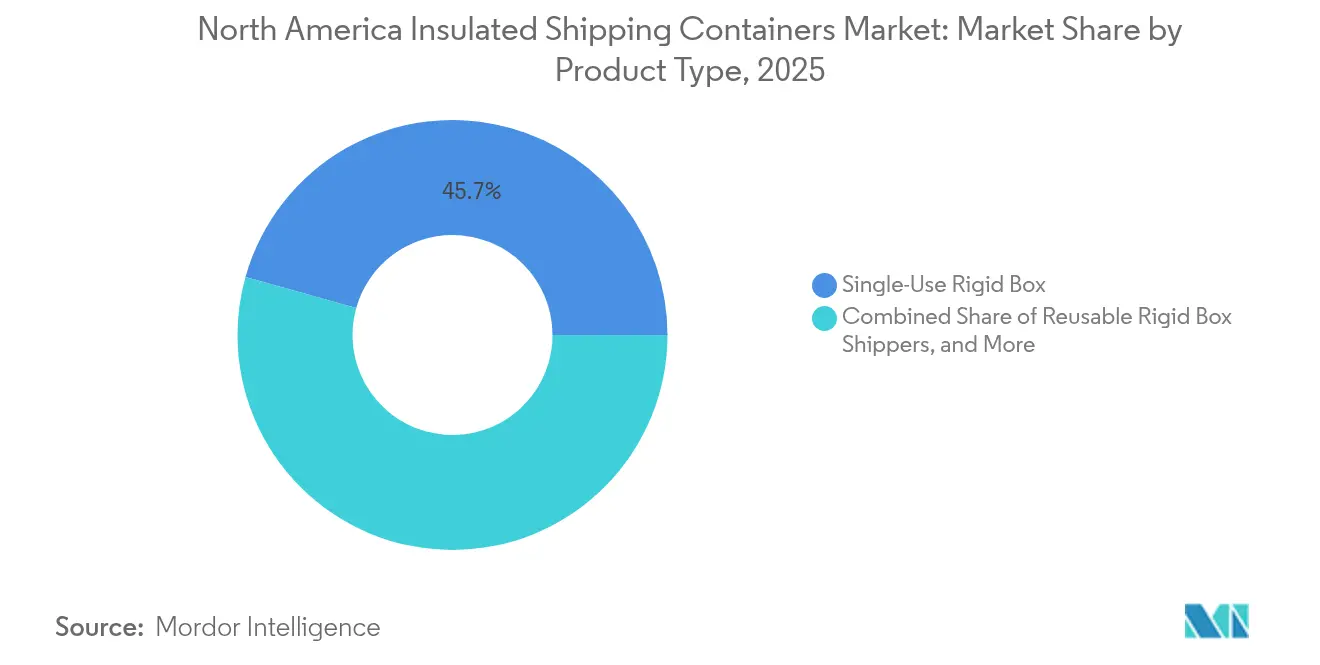

- By product type, single-use rigid boxes captured 45.65% of the North America insulated shipping containers market revenue share in 2025, whereas reusable rigid boxes posted the highest 6.86% CAGR projection to 2031.

- By capacity, the 5-20 L range accounted for 32.60% of the North America insulated shipping containers market share in 2025, while containers ≤5 L are poised for 6.55% CAGR growth to 2031.

- By country, the United States dominated with 87.65%of the North America insulated shipping containers market share in 2025; the United States records a 6.44% CAGR outlook through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Insulated Shipping Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce surge in temperature-sensitive meal kits | +1.2% | United States and Canada, urban metros | Short term (≤ 2 years) |

| Growth in pharmaceutical cold-chain expansion | +1.4% | North America, pharma hubs | Medium term (2–4 years) |

| Tightening U.S. FDA biologics stability guidance | +0.9% | United States, spillover to Canada | Medium term (2–4 years) |

| Retailer sustainability mandates for reusable shippers | +0.8% | United States and Canada | Long term (≥ 4 years) |

| USDA grants for food-loss reduction programs | +0.5% | United States agricultural zones | Long term (≥ 4 years) |

| Venture capital entering direct-to-patient logistics | +0.7% | United States healthcare clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Surge in Temperature-Sensitive Meal Kits

Temperature-sensitive meal kit services are scaling quickly and require compact, high-performance packaging that sustains 48-72-hour transit windows. Technology such as SeaWell active packaging lengthens shelf life and supports quality claims.[1]Aptar, “SeaWell Active Packaging Technology,” Aptar.com Cost-conscious operators use smaller, lighter containers that cut freight expenses, and biodegradable foams help brands communicate sustainability commitments. Adoption peaks within two years as consolidation reduces operator count, yet installed volumes of small containers keep rising. The North America insulated shipping containers market responds with thinner wall profiles that still meet last-mile thermal targets.

Growth in Pharmaceutical Cold-Chain Expansion

Biologics, cell therapies, and personalized medicine demand precise 2-8 °C shipping, expanding beyond routine vaccine lanes. Merck’s USD 1.5 billion cold-chain build-out in 2024 underscores the long-term capital push. Vacuum insulated panels (VIPs) and phase change materials (PCMs) safeguard payloads during extended transit and reduce excursion risk. Direct-to-patient delivery fuels the need for small, validated shippers with data-logging features. As distribution networks mature, the North America insulated shipping containers market embeds real-time monitoring to satisfy audit requirements across borders.

Tightening U.S. FDA Biologics Stability Guidance

Revised guidance increases documentation and continuous monitoring for temperature excursions. Packaging buyers migrate toward premium solutions that integrate sensors and secure chain-of-custody data. Cell and gene therapies are especially vulnerable, raising procurement budgets for proven containers. Validation cycles lengthen buying decisions, yet once qualified, they create sticky demand and higher margins for container vendors. Medium-term impact persists as new biologics launch pipelines remain active.

Retailer Sustainability Mandates for Reusable Shippers

Programs such as Amazon’s Climate Pledge Friendly set clear thresholds for packaging reusability. Retailers favor suppliers offering durable EPS alternatives like expanded polypropylene (EPP) that survive multiple cycles without performance loss. Container suppliers invest in automated cleaning and refurbishment to close the reuse loop, though establishing collection networks requires time. Over the long term, reusable formats shift revenue toward service-based models that include retrieval, sanitization, and redeployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cost of bio-based insulation resins | -0.8% | North America, sustainable packaging makers | Short term (≤ 2 years) |

| Limited reverse-logistics infrastructure for returns | -0.6% | United States and Canada, rural areas | Medium term (2–4 years) |

| Volatile recycled EPS feedstock availability | -0.4% | Regions with EPS recycling plants | Short term (≤ 2 years) |

| State-level EPR fees | -0.5% | United States, by state | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Cost of Bio-Based Insulation Resins

Bio-based resins cost 15-25% more than petroleum equivalents, eroding margins for eco-focused converters.[2]Chemical Week, “Bio-Based Resin Cost Analysis,” ChemicalWeek.com Limited feedstock capacity and agricultural price swings magnify volatility. Smaller vendors struggle to absorb surcharges and must pass them to customers, risking order deferrals. Technology learning curves and scale economies could narrow the gap, yet near-term headwinds remain, slowing the wholesale shift away from EPS.

Limited Reverse-Logistics Infrastructure for Returns

Reusable programs succeed only when containers return promptly for cleaning. Current return rates hover near 70%, well below breakeven for many operators. Rural and suburban routes are hardest to service because of long collection intervals. Building depots, wash lines, and tracking systems requires high capital and multi-year planning, tempering the pace at which reusable formats penetrate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: EPS Strength Meets Biodegradable Upside

Expanded polystyrene holds a 43.35% share within the North America insulated shipping containers market size in 2025 because its insulation value per dollar remains unmatched for broad food and pharma use cases. Polyurethane foam secures high-value biologics shipping through its density tunability, and EPP gains favor in reuse programs that demand higher drop resistance. Biodegradable starch-blend foams, though at a modest base, rise at a 6.74% CAGR thanks to regulatory incentives and brand stewardship. VIP and aerogel technologies serve premium payloads that justify elevated cost structures, supporting the total value pool of the North America insulated shipping containers market.

Thermal performance standards are tightening, spurred by FDA validation protocols and EPA recycling guidance. Vendors such as Sealed Air deliver thinner VIP panels that shrink package footprints by 30% while maintaining temperature hold times. EPS suppliers pilot recycled content formulations to comply with state plastics statutes. The result is an increasingly segmented material choice matrix where purchasers weigh acquisition costs against reverse-logistics savings, disposal fees, and customer sustainability expectations.

By End-User Application: Pharmaceuticals Lead, Protein Delivery Accelerates

Life sciences and pharmaceuticals account for 37.45% of North America's insulated shipping containers market share in 2025 and typically specify leak-proof, data-ready containers validated for 2-8 °C lanes. Compliance burdens extend sales cycles but also sustain premium price points and predictable reorder cadence. Direct-to-consumer protein services push fresh meat and seafood shipping, growing at a 6.79% CAGR, and require containers that balance ice-pack mass with box wall thickness to meet overnight timelines.

Meal kit operators maintain demand for mid-capacity EPS boxes fitted with gel packs, while frozen food categories sustain a baseline for rigid boxes capable of dry-ice payloads. Specialty niches like floral logistics rely on humidity-resilient liners to mitigate wilting risk. Pharmaceutical dominance is anchored in higher cost tolerance and stringent validation, even as diversified food verticals broaden the total addressable volume for the North America insulated shipping containers market.

By Product Type: Single-Use Dominates, Reuse Gains Traction

Single-use rigid boxes command 45.65% revenue share, leveraging existing fulfillment workflows that favor one-way shipments. Pouch and mailer formats extend penetration to sample drugs and meal-kit side dishes, complementing larger boxes. Reusable rigid boxes demonstrate a 6.86% CAGR as retailers enforce waste-reduction goals. IoT-enabled containers from Pelican BioThermal support asset tracking and condition monitoring.

Reusable adoption hinges on clear return on investment, influenced by container life cycle counts and reverse-logistics cost. Extended producer responsibility fees incentivize users to re-evaluate single-use spend, but contamination risks in pharma and stringent clean-room controls leave one-way boxes entrenched for many biologics programs. The North America insulated shipping containers market, therefore, develops hybrid portfolios, aligning container form factors with shipment value and regulatory tolerance.

By Capacity Range: Mid-Size Holds Lead, Small Formats Climb

Containers in the 5-20 L class represent 32.60% of shipments and fit standard vial trays and two-meal kit trays. Small packages up to 5 L grow fastest at 6.55% CAGR alongside personalized medicine and subscription food services. Large boxes from 20 L to 60 L enable bulk pharmacy replenishments and multi-meal family kits, while pallet shippers handle warehouse-level movements. Emerging aerogel linings allow smaller boxes to hit 72-hour stability targets, important for remote patient deliveries.

Optimizing cube utilization reduces freight spend and greenhouse emissions. As data analytics improves lane-specific thermal modeling, buyers increasingly right-size packages, reinforcing the multi-capacity portfolio strategy that anchors revenue resilience across the North America insulated shipping containers market.

Geography Analysis

The United States anchors the North America insulated shipping containers market with unrivaled pharma volumes and e-commerce density. Investments in direct-to-patient logistics expand small-capacity demand, and FDA stability guidance drives continuous improvement in thermal performance. Rising Extended Producer Responsibility fees encourage retailers and drugmakers to pilot reusable programs, yet success varies by state as collection infrastructure remains uneven.

Canadian growth, while from a smaller base, outpaces the region due to Health Canada alignment and widespread grocery delivery expansion. Government grants to modernize cold-chain routes in northern settlements heighten demand for high-performance containers that withstand extreme temperature gradients. Suppliers addressing Canada develop dual-certified packaging that passes both FDA and Health Canada qualification, simplifying cross-border operations.

Regional climate extremes across North America challenge container integrity from desert heat to arctic cold. This diversity spurs ongoing material R&D, particularly in phase-change media and active monitoring. Vendors able to deliver validated, geography-agnostic solutions position strongly to capture incremental share as direct-to-consumer models normalize.

Competitive Landscape

Competition is moderate, with a blend of large packaging incumbents and agile specialists. Sonoco refocused on temperature-controlled packaging after a USD 1.8 billion divestiture, reallocating capital toward smart container technologies. TemperPack channels recent USD 12 million funding into scaling biodegradable foam lines to meet retailer mandates. Meanwhile, va-Q-tec and Pelican BioThermal emphasize premium VIP solutions and IoT integration for biologics shipments.

Technology serves as a primary differentiator. IoT sensors and blockchain tracking enable shipment visibility and audit readiness, translating into higher contract win rates among pharma clients. Consolidation continues as companies seek vertical integration from material formulation through logistics management. Bioderived foams, automated cleaning systems, and predictive analytics represent active innovation frontiers. Suppliers that harmonize sustainability with total cost of ownership gain an upper hand in the North America insulated shipping containers market.

North America Insulated Shipping Containers Industry Leaders

Sonoco Products Company

Polar Tech Industries Inc.

Softbox Systems US LLC

Cryopak Industries Inc.

Insulated Products Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Sonoco Products Company completed its USD 1.8 billion industrial packaging divestiture to Toppan Holdings, refocusing resources on temperature-controlled solutions.

- August 2024: TemperPack Technologies secured USD 12 million Series B funding to expand biodegradable foam capacity.

- July 2024: Merck announced a USD 1.5 billion investment in cold-chain infrastructure, including validation labs in New Jersey and North Carolina.

- June 2024: Coldcart raised USD 6.5 million seed capital to develop an AI-powered cold-chain platform integrating smart packaging.

North America Insulated Shipping Containers Market Report Scope

Insulated containers, utilized across various industries, play a crucial role in preserving the temperature of their contents and shielding them from external weather conditions. These containers are especially vital in the transportation of fragile, perishable goods, forming an integral part of the cold chain. Their primary functions include halting germ proliferation, extending storage durations, and facilitating the local transport of temperature-sensitive items.

The North American insulated shipping container market is segmented by material type (expanded polystyrene, polyurethane foam, expanded polypropylene, and other material types), end-user application (pre-cooked food and frozen food, life sciences and pharmaceutical, fresh meat, fresh produce, bakery, plants, and flowers, and other end-user applications), and country (the United States and Canada). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Expanded Polystyrene (EPS) |

| Polyurethane Foam (PU) |

| Expanded Polypropylene (EPP) |

| Biodegradable Starch-blend Foams |

| Other Materials (VIPs, Gel Packs) |

| Life Sciences and Pharmaceutical |

| Pre-cooked and Frozen Food |

| Fresh Produce |

| Fresh Meat and Seafood |

| Bakery, Plants and Flowers |

| Other (Cosmetics, Wine, Beverages) |

| Single-Use Rigid Box Shippers |

| Reusable Rigid Box Shippers |

| Single-Use Pouch and Mailer Shippers |

| Pallet-sized Bulk Shippers |

| Upto 5 L |

| 5 - 20 L |

| 20 - 60 L |

| Greater than 60 L (Pallet) |

| United States |

| Canada |

| By Material Type | Expanded Polystyrene (EPS) |

| Polyurethane Foam (PU) | |

| Expanded Polypropylene (EPP) | |

| Biodegradable Starch-blend Foams | |

| Other Materials (VIPs, Gel Packs) | |

| By End-User Application | Life Sciences and Pharmaceutical |

| Pre-cooked and Frozen Food | |

| Fresh Produce | |

| Fresh Meat and Seafood | |

| Bakery, Plants and Flowers | |

| Other (Cosmetics, Wine, Beverages) | |

| By Product Type | Single-Use Rigid Box Shippers |

| Reusable Rigid Box Shippers | |

| Single-Use Pouch and Mailer Shippers | |

| Pallet-sized Bulk Shippers | |

| By Capacity Range | Upto 5 L |

| 5 - 20 L | |

| 20 - 60 L | |

| Greater than 60 L (Pallet) | |

| By Country | United States |

| Canada |

Key Questions Answered in the Report

How large is the North America insulated shipping containers market in 2026?

The North America insulated shipping containers market size is USD 1.97 billion in 2026.

What is the forecast growth rate for insulated shipping containers in North America?

The market is projected to expand at a 6.37% CAGR, reaching USD 2.68 billion by 2031.

Which material holds the largest share of insulated shipping containers sold in North America?

Expanded polystyrene leads with 43.35% share as of 2025.

Which end-use segment is growing fastest for insulated containers?

Fresh meat and seafood shipping posts the highest 6.79% CAGR through 2031.

What is driving the adoption of reusable insulated containers?

Retailer sustainability mandates and rising EPR fees are pushing users toward reusable formats that lower waste and long-term cost.

Which country contributes most to demand in North America?

The United States commands 87.65% of regional revenue because of its large pharmaceutical base and mature e-commerce infrastructure.

Page last updated on: