Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

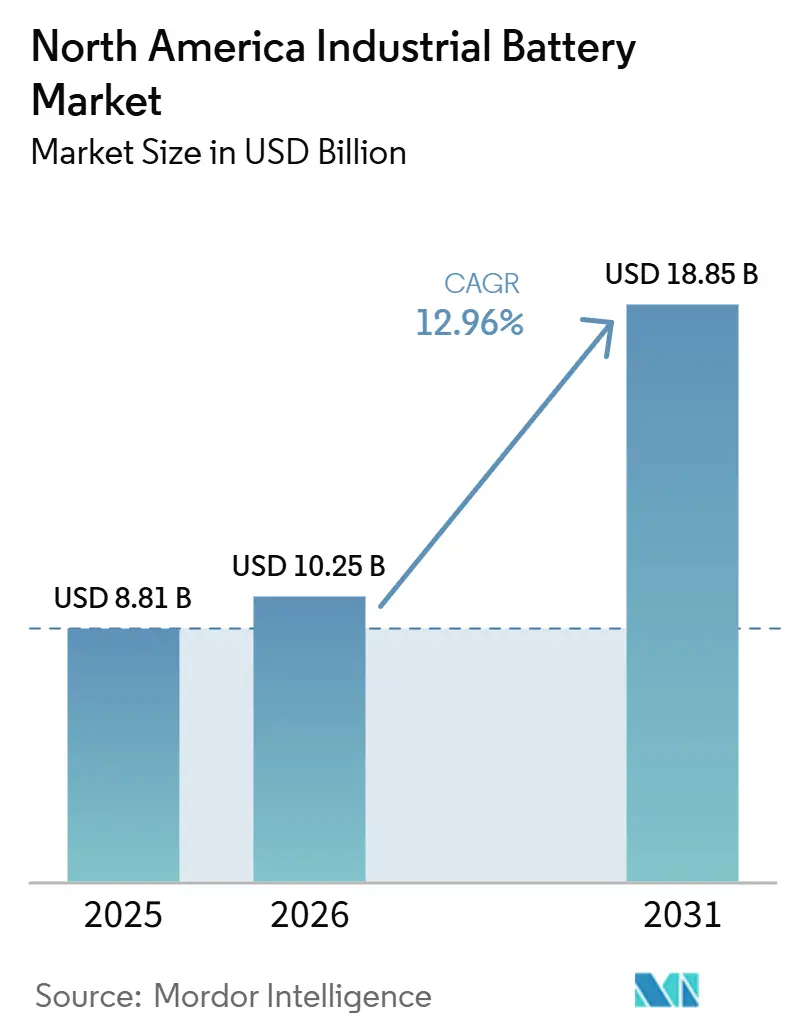

| Base Year Market Size (2025) | USD 8.81 Billion |

| Market Size (2026) | USD 10.25 Billion |

| Market Size (2031) | USD 18.85 Billion |

| Growth Rate (2026 - 2031) | 12.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Industrial Battery Market Analysis by Mordor Intelligence

The North America Industrial Battery Market size is projected to be USD 8.81 billion in 2025, USD 10.25 billion in 2026, and reach USD 18.85 billion by 2031, growing at a CAGR of 12.96% from 2026 to 2031. The North America industrial batteries market is moving beyond its traditional backup role, as batteries are now being procured as operating assets tied to warehouse uptime, grid support, and real-time power balancing across industrial sites. US domestic battery manufacturing output increased 359% in inflation-adjusted terms from 2020 to 2024, and employment in battery manufacturing reached a record 54,400 by 2024, which materially strengthened the regional supply base serving the North America industrial batteries market. The North America industrial batteries market is also benefiting from converging demand from data center expansion, warehouse automation, and federal incentives that improve project economics for localized cell and module production. Section 45X credits and the tightening foreign entity restrictions under the OBBBA are pushing producers to localize supply chains faster, which is widening the competitive gap between compliant domestic manufacturers and assemblers that still rely on imported cells in the North America industrial batteries market . The main near-term risk for the North America industrial batteries market is policy uncertainty around IRA implementation, because any disruption in incentive visibility can slow order timing for motive-power and industrial procurement programs during 2026 and 2027.[1]Congressional Research Service, “Battery Manufacturing in the United States,” Congressional Research Service, crsreports.congress.gov

Key Report Takeaways

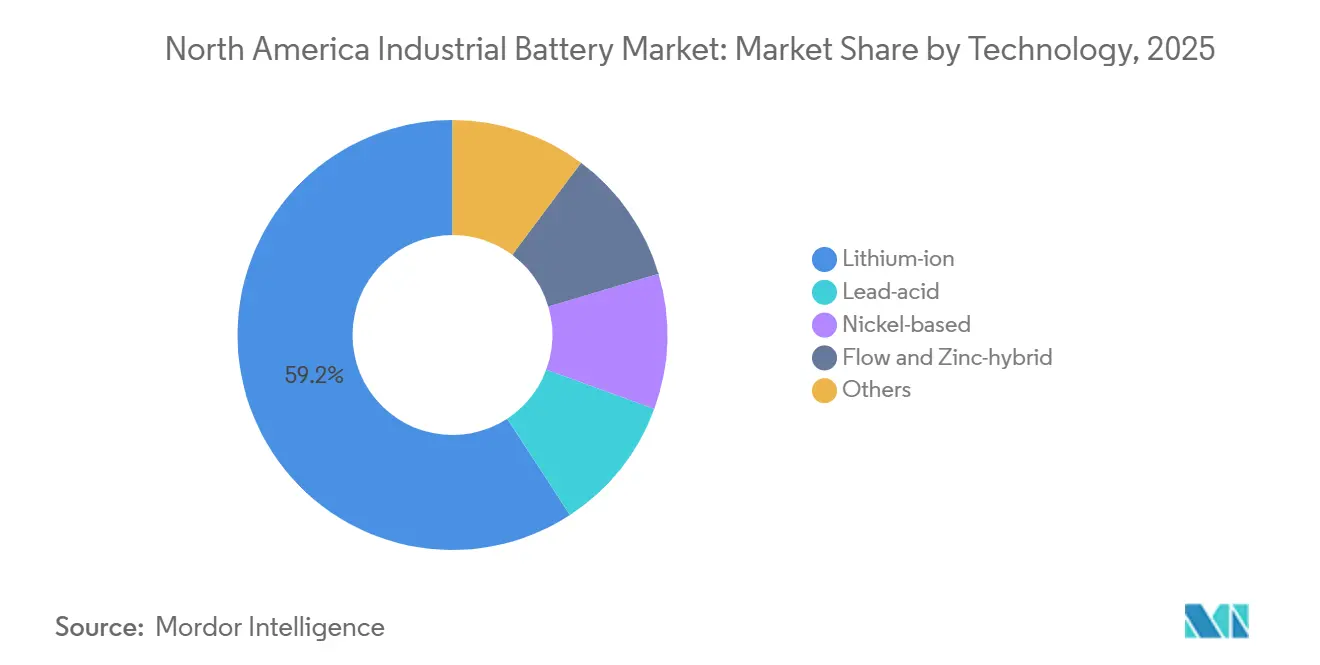

- By technology, lithium-ion held 59.2% of the North America industrial batteries market share in 2025, while Flow & Zinc-hybrid is forecast to expand at an 18.3% CAGR through 2031.

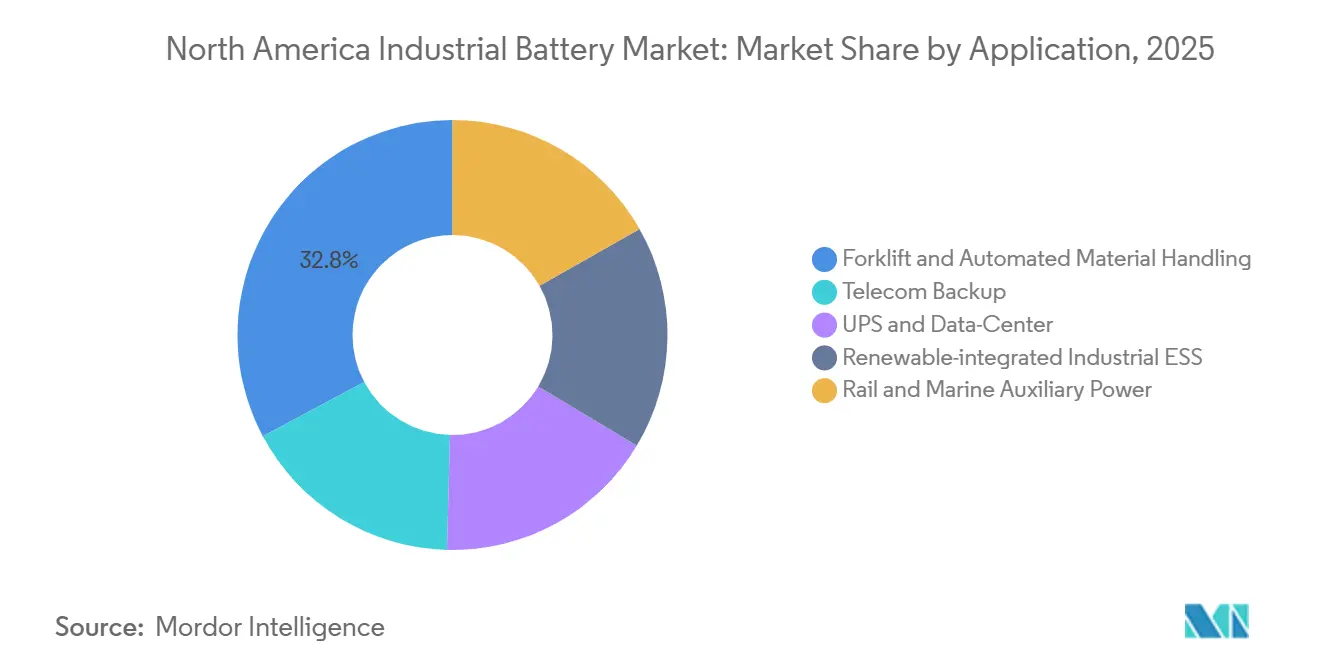

- By application, Forklift & Automated Material Handling accounted for 32.8% of the market in 2025, while Renewable-integrated Industrial ESS is projected to grow at a 19.4% CAGR through 2031.

- By geography, the United States held 75.3% of regional revenue in 2025, while Mexico is expected to record the fastest regional CAGR at 21.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Industrial Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commitment-Driven Fleet Electrification Mandates | +1.8% | US primary, Canada secondary | Short term (≤ 2 years) |

| Surging Automated-Warehouse Build-Outs Demanding 24×7 Motive-Power | +2.2% | US primary, Canada spill-over | Short term (≤ 2 years) |

| Grid-Service Battery Contracts For Data-Center Resiliency | +3.5% | US dominant, with early gains in Texas, Virginia, Arizona | Short term (≤ 2 years) |

| Declining USD Per KWh Lithium-Ion Pack Costs | +2.0% | Global supply dynamic, US primary beneficiary via domestic scale | Medium term (2-4 years) |

| OEM Shift From Flooded Lead-Acid To Maintenance-Free Chemistries | +1.5% | US and Canada | Medium term (2-4 years) |

| IRA Tax-Credit Stack For North America-Sourced Cells And Critical Minerals | +2.8% | US only | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Service "Battery-as-a-Weapon" Contracts for Data-Center Resiliency

The North America industrial batteries market is seeing data centers emerge as the most important new demand center for large-scale UPS and resiliency systems. NERC issued a Level 3 Alert on May 7, 2026, and identified AI-driven hyperscale loads as a reliability risk to the US bulk power system, which raised the value of fast-response industrial batteries in critical facilities. This shift matters because battery systems are no longer being purchased only for emergency backup, they are now being evaluated as assets that can stabilize voltage, manage short-duration load swings, and support continuity in high-density compute environments. Fluence reported a contracted backlog of USD 5.6 billion as of March 2026 and signed master supply agreements with 2 major hyperscalers in fiscal Q2 2026, showing that the North America industrial batteries market is already converting this demand into booked revenue.[2]Fluence Energy, “Quarterly Report on Form 10-Q for March 2026,” SEC EDGAR, sec.gov As a result, the North America industrial batteries market is gaining support from a use case where reliability value and potential grid-service value are being assessed together instead of separately.

IRA Tax-Credit Stack for North America-Sourced Cells and Critical Minerals

The IRA production credit framework remains one of the clearest structural supports for the North America industrial batteries market. EnerSys recognized USD 136.4 million in Section 45X credits in fiscal 2024, up from USD 17.3 million in fiscal 2023, which shows how quickly compliant domestic production can change the cost position of established manufacturers. Fluence also reported USD 10.9 million in IRA-linked cost reductions in the first half of fiscal 2026 tied to its Utah battery module manufacturing, confirming that these incentives are already influencing margin structures in the North America industrial batteries market. The OBBBA restrictions that tighten prohibited foreign entity content from 2026 through 2030 deepen this advantage, because access to federal-linked demand increasingly depends on domestic sourcing compliance rather than price alone. This is reshaping procurement decisions across the North America industrial batteries market, especially for suppliers that can offer cells, modules, and pack integration from a traceable North American base.

Surging Automated-Warehouse Build-Outs Demanding 24×7 Motive Power (AGV/AMR)

Warehouse automation is creating a high-frequency replacement cycle that continues to expand the North America industrial batteries market. Delta Electronics stated in April 2026 that its MOOV charging platform has powered more than 1 million industrial vehicles across North America and completed more than 1 billion charging cycles in 24/7 logistics environments, which shows the scale of electrified warehouse operations already in place. Exide Technologies also highlighted LFP battery systems for multi-shift AGV and AMR fleets at LogiMAT 2026, with digital diagnostics and modular battery management intended to reduce maintenance downtime in uninterrupted operations. For the North America industrial batteries market, the important point is that batteries in continuous AGV service wear faster than batteries in conventional single-shift forklift fleets, which shortens the replacement cycle and brings revenue forward for suppliers. Safety and operating standards are also strengthening buyer preference for battery systems with certified monitoring and management features, which favors established companies with deeper product validation capabilities.

Commitment-Driven Fleet Electrification Mandates

Fleet electrification rules are creating a durable policy-driven demand base for the North America industrial batteries market. California’s Advanced Clean Fleets regulation requires affected operators to shift purchasing toward zero-emission vehicles on a defined schedule, which gives battery suppliers clearer visibility into medium-term motive-power demand. This matters because regulated fleet replacement is less exposed to short-cycle swings in general industrial spending than discretionary equipment purchases. The policy framework also supports related energy storage investment, since battery-backed charging and facility energy systems can qualify under longer-dated federal incentive structures that remain available through 2034. In the North America industrial batteries market, suppliers that align product planning with regulated fleet renewal cycles are positioned to defend utilization, pricing discipline, and service revenue more effectively than suppliers that wait for spot demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity Of Regional Class-1 Nickel And Battery-Grade Manganese Refining | -1.5% | North America-wide, acute in US and Canada | Medium term (2-4 years) |

| Workplace Fire-Code Liabilities For High-Energy LFP Installations | -1.2% | US primary, Canada secondary | Short term (≤ 2 years) |

| Lead Recycling Bottlenecks Amid Tightened EPA Thresholds | -0.8% | US primary | Medium term (2-4 years) |

| Capital-Intensive Cell Manufacturing Vs Volatile Forklift Demand Cycle | -0.9% | US primary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Workplace Fire-Code Liabilities for High-Energy LFP Installations

The North America industrial batteries market faces a real execution constraint from tighter fire-code requirements around stationary storage. The 2026 edition of NFPA 855 raised the compliance threshold for many industrial installations by requiring Hazard Mitigation Analysis more broadly and reinforcing large-scale fire testing expectations for qualifying systems. Installations above 600 kWh now face stricter room design and explosion-prevention expectations, which raises project design cost and can complicate retrofits in existing warehouses and manufacturing sites. These rules do not stop deployment in the North America industrial batteries market, but they do extend approval cycles and make system selection more dependent on documentation, testing history, and installer experience. The burden is heavier for smaller suppliers, while larger integrators with tested and listed systems can move through the permitting process with fewer delays.

Lead Recycling Bottlenecks Amid Tightened EPA Thresholds

Lead recycling remains a constraint for the North America industrial batteries market, even though lead-acid demand still holds in standby and telecom uses. The EPA’s proposed NESHAP amendments for Secondary Lead Smelting were signed on September 29, 2025, and introduced new emission limits for additional hazardous air pollutants, with wet electrostatic precipitator capital costs estimated at USD 621 million for the remaining facilities. The United States now has only 11 secondary lead smelting facilities, which limits the speed at which recycled supply can expand even when downstream demand remains stable. The EPA is also developing a voluntary Extended Producer Responsibility framework for batteries, which adds future reporting and compliance cost questions for producers across chemistries. For the North America industrial batteries market, this means the lead-acid value chain still supports meaningful installed demand, but its supply-side flexibility is becoming more limited as environmental compliance tightens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Lithium-Ion Dominates While Long-Duration Chemistries Gain Structural Ground

Lithium-ion held 59.2% of the North America industrial batteries market share in 2025, which confirms that it has become the default chemistry across high-cycle industrial use cases. The North America industrial batteries industry has moved steadily in this direction for several years, as US domestic manufacturing data already showed lead-acid shipment value falling from USD 5.3 billion in 2013 to USD 2.2 billion in 2022 while non-lead-acid output rose from USD 0.7 billion to USD 16.6 billion over the same period. This shift continued through 2025 and 2026 because maintenance-free operation, better cycling performance, and stronger compatibility with automated duty cycles make lithium-ion easier to justify on a total ownership basis. EnerSys’s decision to close its Tijuana lead-acid plant and shift production to Springfield, Missouri shows how incumbent suppliers are redirecting capital toward product lines and manufacturing footprints that fit the new structure of the North America industrial batteries market.

Flow & Zinc-hybrid is projected to expand at an 18.3% CAGR through 2031, making it the fastest-growing technology group in the North America industrial batteries market. The appeal of these long-duration chemistries is strongest in industrial microgrids and renewable-linked installations where discharge duration, non-flammability, or operating flexibility can outweigh the space and cost advantages of mainstream lithium systems. This opens a wider technology mix than the headline share split suggests, because the North America industrial batteries industry is not moving toward a single chemistry for every application. Nickel-based batteries still retain relevance in temperature-variable telecom, rail auxiliary power, and other high-reliability settings where stability under harsher operating conditions remains more important than absolute cost. The practical result is that lithium-ion will continue to dominate the North America industrial batteries market by value, but long-duration and niche chemistries will capture a larger share of new projects where application needs are more specific than simple backup power.

By Application: Material Handling Anchors Revenue While Renewable ESS Reshapes Growth

Forklift & Automated Material Handling accounted for 32.8% of the North America industrial batteries market in 2025, which kept motive power as the largest application base. This position reflects a large installed fleet, routine battery replacement, and the operational reality that distribution centers cannot tolerate downtime in multi-shift environments. EnerSys reported first orders for its NexSys Air wireless AGV charger in fiscal 2024, which shows that suppliers are now selling not only batteries into this part of the North America industrial batteries market, but also the charging architecture that supports automated workflows. Telecom backup also remains an important demand layer, as distributed network build-outs continue to require compact and reliable battery systems for field power resilience.

Renewable-integrated Industrial ESS is projected to grow at a 19.4% CAGR in the North America industrial batteries market size through 2031, making it the fastest-expanding application group. Fluence reported a USD 5.6 billion contracted backlog as of March 2026, and expected 50% to 55% of that backlog to convert to revenue within 12 months, which indicates that commercial pipeline depth is already translating into near-term execution. This means the growth center of the North America industrial batteries market is shifting toward systems that sit closer to grid flexibility, renewable integration, and facility-level resiliency rather than traditional battery replacement alone. UPS and data-center demand are expanding on the same logic, because battery systems now support both continuity and power quality in increasingly load-sensitive facilities. Over the forecast period, this should reduce the share held by legacy motive-power applications even though absolute battery volumes for forklifts and automated material handling continue to rise.

Geography Analysis

The United States accounted for 75.3% of the North America industrial batteries market share in 2025, which kept it far ahead of Canada and Mexico in both demand depth and manufacturing scale. The United States remains the core of the North America industrial batteries market because it combines the region’s largest installed industrial base with the strongest mix of federal production incentives and data-center-led power reliability demand. Section 45X credits reward domestic battery cell and module output, while tightening foreign entity restrictions are increasing the value of local sourcing and traceable production chains for suppliers serving federal or incentive-linked demand. That incentive structure is already shaping capital deployment, as EnerSys recognized USD 136.4 million in Section 45X credits in fiscal 2024 and Clarios announced a USD 390 million expansion in Missouri during May 2026 with support tied to its broader US manufacturing strategy. The United States therefore remains the anchor geography for the North America industrial batteries market not only because of current revenue share, but because policy and production economics still reinforce one another more clearly there than anywhere else in the region.

Canada contributes a smaller but steady portion of the North America industrial batteries market, supported by industrial electrification goals and grid modernization needs. Demand conditions are structurally sound because remote operations, mining activity, and utility-side reliability requirements create a natural fit for maintenance-free battery systems and for longer-duration storage where diesel displacement economics are attractive. Provincial procurement frameworks and clean electricity policy direction also give storage suppliers a more stable project environment than purely discretionary industrial spending. In this setting, the North America industrial batteries market benefits from Canada more as a steady strategic contributor than as a short-term volume spike, especially in projects where reliability, duration, and critical mineral access all matter.

Mexico is expected to record the fastest regional growth at a 21.1% CAGR through 2031 in the North America industrial batteries market size. This growth profile is being driven by nearshoring-linked manufacturing investment, as OEM and battery assembly activity continues to spread across major industrial corridors such as Nuevo León, Baja California, and San Luis Potosí. Mexico’s role in the North America industrial batteries market is therefore shifting from a cost-efficient assembly location toward a broader manufacturing and battery integration platform tied to continental supply chains. That change supports both direct battery demand and the build-out of adjacent charging, storage, and industrial power systems as factories localize more of their operations. Mexico will still face policy and trade sensitivity around tariffs and foreign entity content rules, but its growth rate suggests that it remains the most dynamic expansion zone within the North America industrial batteries market over the forecast period.

Competitive Landscape

The North America industrial batteries market is moderately concentrated at the top, but it remains fragmented across mid-tier suppliers and specialized application niches. EnerSys, Clarios, East Penn Manufacturing, and C&D Technologies retain strong positions in traditional industrial, motive-power, and standby segments, while Tesla, Fluence Energy, and LG Energy Solution are more influential in ESS and data-center-linked demand. This split means the North America industrial batteries market is no longer organized around a single competitive center, because leadership now depends heavily on chemistry, application, certification depth, and domestic content compliance. Competitive advantage in the North America industrial batteries market increasingly comes from the ability to pair manufacturing footprint with incentive eligibility, rather than from price competition alone. Suppliers that can align certified products, local supply, and service capabilities are now better placed to defend margins as procurement teams apply stricter technical and sourcing screens.

EnerSys provides the clearest example of how incumbents are repositioning inside the North America industrial batteries market. The company closed its Monterrey, Mexico flooded lead-acid plant in April 2025 and later announced the closure of its Tijuana, Mexico lead-acid plant in March 2026, consolidating production into US facilities to improve economics and align better with domestic incentive structures. EnerSys also acquired Bren-Tronics in May 2024 for USD 208 million, which expanded its position in ruggedized lithium systems for military applications and reduced its exposure to more cyclical end uses. Clarios has pursued a parallel strategy through manufacturing expansion, including its Missouri investment announced in May 2026 as part of a broader long-term US manufacturing plan.

Fluence shows how quickly ESS-focused players are gaining ground in the North America industrial batteries market, with order intake of USD 2 billion year to date through May 2026 and a record contracted backlog of USD 5.6 billion. At the same time, certification and safety requirements are becoming a stronger barrier to entry, because large buyers increasingly favor UL 9540 listed systems and proven lithium safety compliance for industrial deployment. This narrows the practical field for smaller entrants that may have a valid product concept but lack the capital and testing history needed for larger commercial rollouts. The companies best placed in the North America industrial batteries market through 2031 are those that combine domestic compliance, bankable certification, and enough chemistry breadth to serve both mainstream and duration-sensitive projects.

North America Industrial Battery Industry Leaders

EnerSys

East Penn Manufacturing

Clarios

Saft Groupe SA

Panasonic Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Clarios announced a USD 390 million expansion of its 2 St. Joseph, Missouri facilities, creating 123 new jobs and retaining 936, targeting increased AGM battery production capacity as part of its broader USD 6 billion US manufacturing strategy. The investment is supported by Missouri Works Program incentives and Section 45X Advanced Manufacturing Production Credits

- May 2026: Fluence Energy reported a record contracted backlog of USD 5.6 billion, order intake of approximately USD 2 billion year-to-date, more than double the same period in FY2025, and signed master supply agreements with 2 major hyperscalers, with first data center battery orders anticipated in Q3 FY2026.

- April 2026: Delta Electronics reported that its MOOV charging platform has powered over 1 million industrial vehicles across North America, completing over 1 billion charging cycles in 24/7 logistics operations, including AGVs, AMRs, and electric forklifts.

- March 2026: EnerSys announced the closure of its Tijuana, Mexico lead-acid plant, shifting production to Springfield, Missouri, within a USD 37 million restructuring expected to generate USD 20 million in annual pre-tax benefits from FY2028.

North America Industrial Battery Market Report Scope

Industrial batteries are electrochemical devices that convert higher-level active materials into an alternate state during discharge. They are designed to last far longer than consumer batteries and are used in more challenging environments. These batteries are made for two general applications: float (or standby) duty and deep cycling (especially traction batteries for forklift trucks, etc.).

The North America Industrial Battery Market is segmented into technology, application, and geography. By technology, the market is segmented into lithium-ion, lead-acid, nickel-based, flow and zinc-hybrid, and others. By application, the market is segmented into forklift and automated material handling, telecom backup, UPS and data-center, renewable-integrated industrial energy storage systems (ESS), and rail and marine auxiliary power. By geography, the market is segmented into the United States, Canada, and Mexico. The report also covers the market size and forecasts for the industrial battery market in 3 countries across North America. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Technology

| Lithium-ion |

| Lead-acid |

| Nickel-based |

| Flow & Zinc-hybrid |

| Others |

By Application

| Forklift & Automated Material Handling |

| Telecom Backup |

| UPS & Data-Center |

| Renewable-integrated Industrial ESS |

| Rail & Marine Auxiliary Power |

By Geography

| United States |

| Canada |

| Mexico |

| By Technology | Lithium-ion |

| Lead-acid | |

| Nickel-based | |

| Flow & Zinc-hybrid | |

| Others | |

| By Application | Forklift & Automated Material Handling |

| Telecom Backup | |

| UPS & Data-Center | |

| Renewable-integrated Industrial ESS | |

| Rail & Marine Auxiliary Power | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2031 value forecast for industrial batteries in North America?

The North America industrial batteries market is forecast to reach USD 18.85 billion by 2031, rising from USD 10.25 billion in 2026 at a 12.96% CAGR.

Which battery technology leads regional demand?

Lithium-ion led with 59.2% share in 2025, reflecting its strength in high-cycle industrial applications and its fit with automated operations.

Which application is growing the fastest across industrial use cases?

Renewable-integrated Industrial ESS is the fastest-growing application, with a projected 19.4% CAGR through 2031.

Why is the United States the largest revenue contributor?

The United States held 75.3% of regional revenue in 2025 because it combines the deepest industrial installed base, strong federal incentives, and the largest data-center-led power demand pipeline.

What is driving the fastest growth in Mexico?

Mexico is projected to grow at a 21.1% CAGR through 2031, supported by nearshoring-linked manufacturing expansion and rising battery assembly activity.

What is changing competitive strategy in this space?

Supplier strategy is shifting toward domestic sourcing compliance, certified system portfolios, and application-specific product design, especially as Section 45X benefits and fire-code requirements become more important in procurement decisions.

Page last updated on: