North America Home Energy Management System (HEMS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

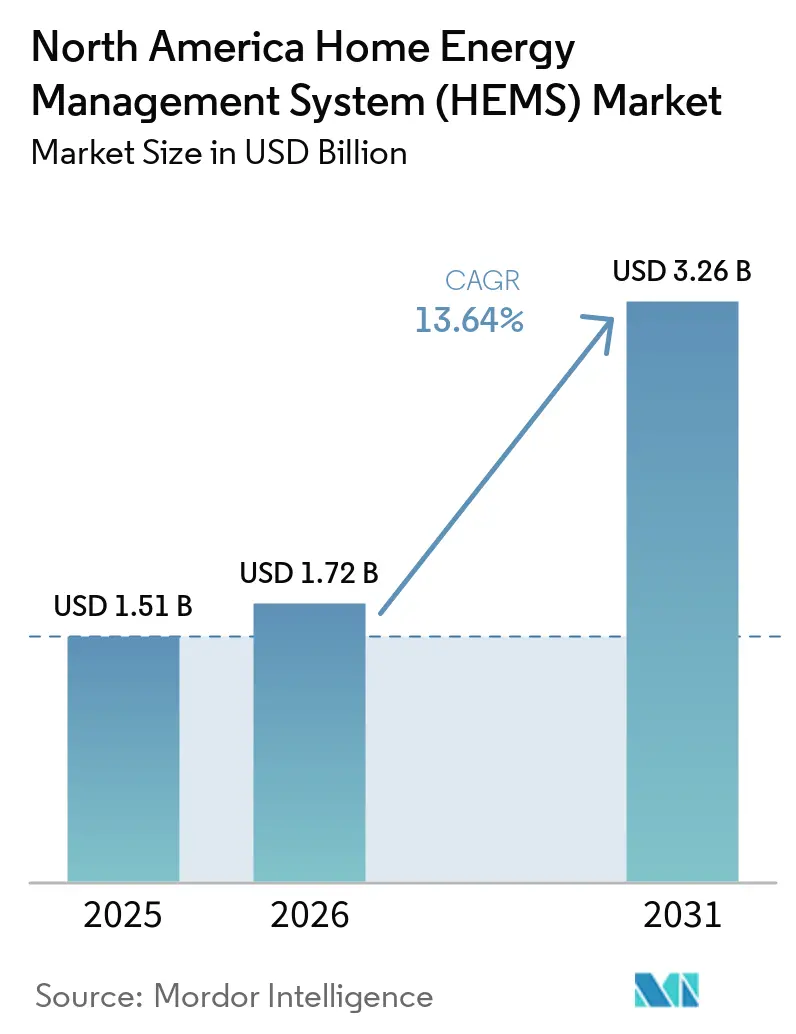

| Base Year Market Size (2025) | USD 1.51 Billion |

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 3.26 Billion |

| Growth Rate (2026 - 2031) | 13.64% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Home Energy Management System (HEMS) Market Analysis by Mordor Intelligence

The North America home energy management system (HEMS) market size is expected to grow from USD 1.51 billion in 2025 to USD 1.72 billion in 2026 and is forecast to reach USD 3.26 billion by 2031 at 13.64% CAGR over 2026-2031. The North America home energy management system market is benefiting from the combination of broad advanced metering infrastructure build-outs, a growing residential solar-plus-storage base, and utility-led demand-response activity that supports more automated household energy control. The North America home energy management system market is also moving beyond stand-alone hardware sales because software-led optimization, recurring subscriptions, and virtual power plant participation are reshaping how providers capture value. Competitive activity remains high as integrated hardware-software vendors, utility channel partners, and cloud-native platforms compete for control of the customer relationship and device stack. High upfront system costs and cybersecurity concerns still slow adoption in some households, especially where rebates are less accessible or device standards remain fragmented. Even so, expanding state-level rebate support, stronger interoperability under Matter 1.5, and deeper utility participation continue to keep the North America home energy management system market on a favorable growth path through 2031.

Key Report Takeaways

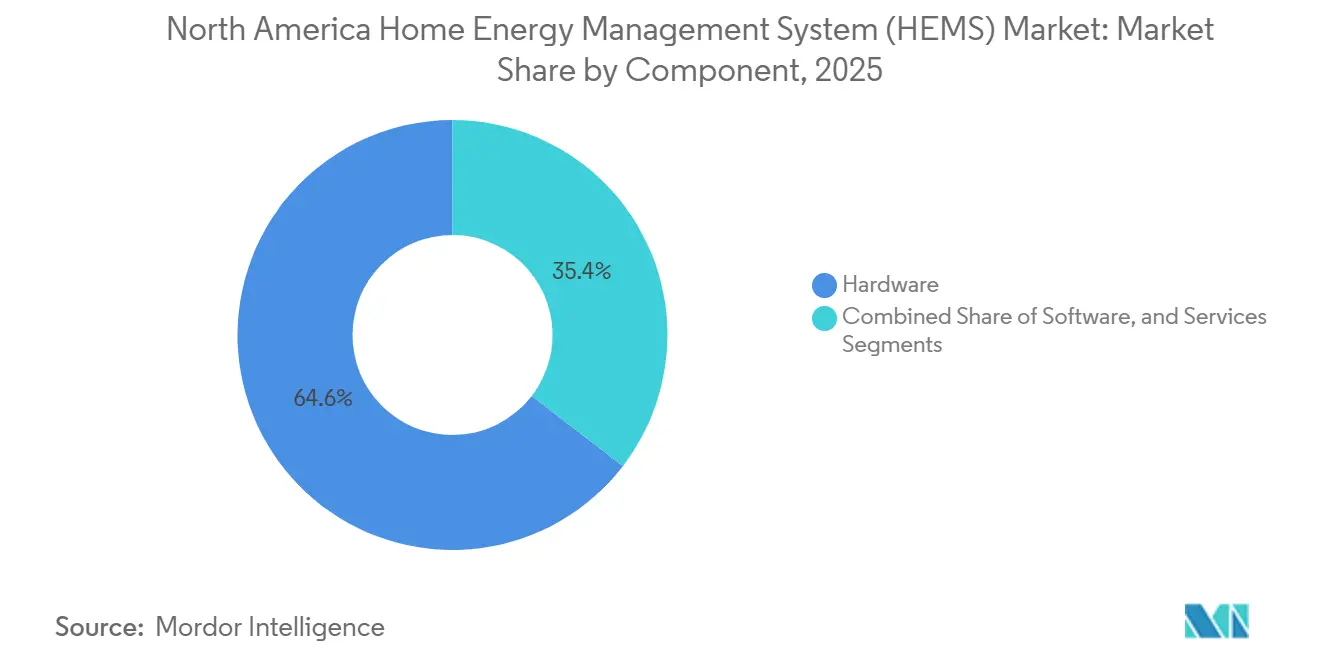

- By component, hardware led with a 64.56% revenue share of North America home energy management system (HEMS) market in 2025, while software is forecast to expand at a 14.89% CAGR through 2031.

- By communication technology, Wi-Fi held a 38.76% share in 2025, while Z-Wave recorded the highest projected CAGR at 14.21% through 2031.

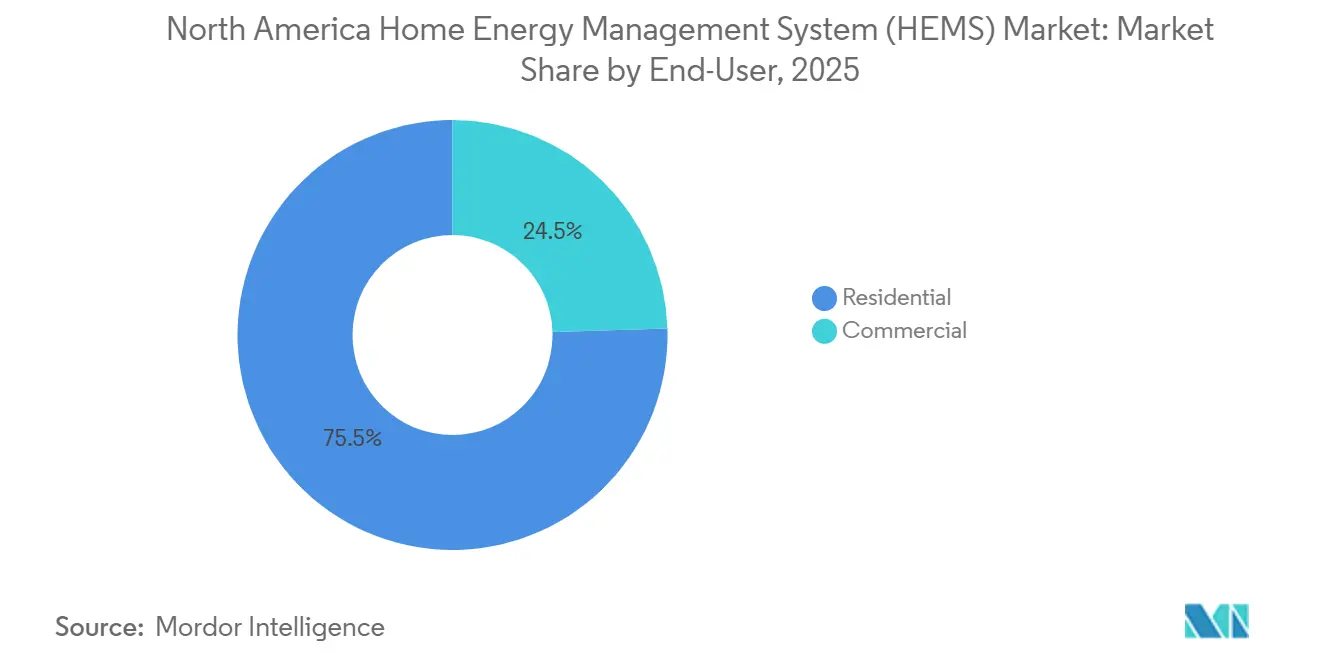

- By end-user, residential accounted for a 75.45% share of North America home energy management system (HEMS) market in 2025, while commercial is advancing at a 15.32% CAGR through 2031.

- By deployment mode, on-premises and local gateway deployments captured a 62.34% share in 2025, while cloud-hosted platforms are projected to grow at a 15.91% CAGR through 2031.

- By country, the United States held 81.89% of regional revenue of North America home energy management system (HEMS) market in 2025, while Mexico is expected to expand at a 14.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Home Energy Management System (HEMS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart Meter and AMI Saturation Supporting Real-Time Control | +3.1% | National, concentrated in investor-owned utility territories in the US, expanding to Ontario and Quebec in Canada | Short term (≤ 2 years) |

| Solar-Plus-Storage and Home Electrification Adoption | +2.6% | California, Texas, Hawaii, Florida, emerging in Arizona and Colorado | Medium term (2-4 years) |

| Utility Time-Of-Use and Dynamic Pricing Expansion | +2.2% | California, New York, Texas, Ontario in Canada, early-stage in Mexico | Medium term (2-4 years) |

| IRA-Linked Whole-Home Rebate Stacking Improving HEMS Payback | +1.6% | National in the US, concentrated in the 23 states with active HOMES and HEAR rollout as of early 2026 | Short term (≤ 2 years) |

| Insurance and Resiliency Demand for Backup-Oriented Energy Orchestration | +1.0% | California, Florida, Texas, Gulf Coast, and Southeast US | Medium term (2-4 years) |

| Matter 1.5 and Utility Signal Standardization Lowering Integration Friction | +0.8% | National, concentrated in utility service territories deploying OpenADR-integrated HEMS platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smart Meter and AMI Saturation Supporting Real-Time Control

Smart meter saturation is pushing household energy management away from simple usage visibility and toward real-time device control. In the North America home energy management system (HEMS) market, this matters because AMI data gives platforms a constant stream of household consumption signals that can support automated scheduling, load disaggregation, and tariff response. As utilities move from billing-focused infrastructure to grid-edge intelligence, the value of software that can interpret meter data and translate it into appliance-level decisions rises with it. This shift also lowers the friction of adoption because some households can receive better energy insight without adding a full set of new sensing hardware inside the home. The North America home energy management system market benefits from that lower entry barrier because it expands the addressable base for platform vendors and utility-led programs. It also strengthens the case for partnerships between utilities, software developers, and device providers that can turn existing grid infrastructure into a practical household orchestration layer.

Solar-Plus-Storage and Home Electrification Adoption

Solar-plus-storage adoption is one of the clearest demand anchors for the North America home energy management system market because households with multiple energy assets need active coordination rather than passive monitoring. The US residential storage segment grew 51% year over year in 2025, and cumulative deployments since 2019 exceeded 50GW and 144GWh, which materially expanded the installed base that can be paired with household energy control software.[1]American Clean Power Association, “U.S. Energy Storage Monitor Full Year 2025,” American Clean Power Association, cleanpower.org The same report indicates the United States is expected to deploy 500GWh of storage from 2026 to 2031, which keeps creating new integration points for home energy platforms over the forecast period. In practical terms, each new battery system raises the value of software that can optimize charging, backup priority, self-consumption, and time-based load shifting inside the home. This is why the North America home energy management system (HEMS) market is moving closer to full-stack orchestration, where thermostats, smart panels, storage systems, and connected loads operate as one coordinated energy system. The adoption of electric appliances and home electrification upgrades further deepens this need because household power flows become more complex as more flexible loads enter the home.

Utility Time-Of-Use and Dynamic Pricing Expansion

Time-of-use and dynamic pricing structures are making the value of automated control easier for households to see and easier for vendors to explain. California’s Load Management Standards require large utilities and community choice aggregators to offer dynamic electricity pricing options to all customers by 2027, which creates a clear regulatory path for wider automation uptake.[2]California Energy Commission, “Inflation Reduction Act Residential Energy Rebate Programs,” California Energy Commission, energy.ca.gov Lawrence Berkeley National Laboratory estimated in May 2026 that six categories of price-responsive equipment could reduce California peak demand by up to 8.75GW by 2030 under dynamic rate structures, with payback periods below 3 years in full dynamic pricing cases. In the North America HEMS market, those conditions favor platforms that can receive tariff signals and adjust household consumption without constant user input. That matters because price volatility alone does not create value unless the household has a system that can respond in real time across loads, storage, and backup resources. As more utilities expand these tariff models, the North America home energy management system market is likely to see stronger adoption among households that want measurable bill savings rather than basic device connectivity.

IRA-Linked Whole-Home Rebate Stacking Improving HEMS Payback

IRA-linked home energy rebates continue to improve project economics for households considering integrated energy upgrades. The US Department of Energy states that USD 8.8 billion remains available under the Home Energy Rebates program through September 2031, and 23 states had live rebate programs in early 2026. The HOMES structure is especially relevant because rebates can reach up to USD 8,000 when whole-home savings meet the required threshold, which increases the value of monitoring and verification tools inside a HEMS deployment.[3]Internal Revenue Service, “Frequently Asked Questions About Energy Efficient Home Improvements and Residential Clean Energy Property Credits,” Internal Revenue Service, irs.gov In the NA home energy management system (HEMS) market that means software is not only managing energy flows but also helping document performance in retrofit programs that reward measured savings. The preservation of HOMES and HEAR support after the end of the 25C and 25D tax credits for purchased systems at the end of 2025 also kept a meaningful rebate path in place for whole-home projects. As a result, the North America home energy management system (HEMS) market continues to benefit from policy support that reduces payback periods and makes more complete energy management stacks easier to justify across income groups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront System And Installation Costs | -2.0% | National, most pronounced in states without active rebate programs and in multi-family housing markets | Medium term (2-4 years) |

| Cybersecurity And Household Data Privacy Concerns | -1.4% | National, amplified in states with stricter consumer privacy laws such as California, Virginia, and Colorado | Medium term (2-4 years) |

| Installer Commissioning Complexity Across Multi-Vendor Home Energy Assets | -1.0% | National, concentrated in retrofit markets and utility demand-response program geographies | Short term (≤ 2 years) |

| Tariff And Program Volatility Weakening Consumer ROI Confidence | -0.7% | California, Texas, and other deregulated or incentive-heavy markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront System and Installation Costs

High upfront system cost remains the clearest barrier to mass adoption in the North America home energy management system market. A fully integrated residential setup that includes a smart panel, battery storage, thermostat, software, and EV charging can require USD 15,000 to USD 35,000 before rebates, which keeps many middle-income households on the sidelines. Installation also adds cost because circuit-level control and electrical reconfiguration often require trained electricians and platform-specific commissioning. This cost issue is more severe in multi-family settings and in markets where rebate rollout is slower or utility support is limited. It also affects product mix because households may choose a thermostat or a solar-only setup first, then delay the rest of the energy stack until financing or rebates improve. Until service-based financing and lower-cost deployment models scale more broadly, the North America HEMS market will continue to face slower conversion from consumer interest to completed installations.

Cybersecurity and Household Data Privacy Concerns

Cybersecurity risk is becoming more visible as household energy systems connect more devices, more cloud software, and more utility-facing functions. Copeland’s 2026 Smart Home Data Privacy Study found that data protection concerns rose to 29% in 2026 from 26% in 2022, while surveillance concerns increased to 19% from 16%, and 55% of respondents reported little or no understanding of how smart thermostat data is used by manufacturers.[4]Copeland, “Copeland Study Warns U.S. Homeowners’ Trust in Smart Home Data Practices Has Reached a Critical Low,” Copeland, copeland.com The IEA-4E EDNA Platform also identified firmware weaknesses, unencrypted MQTT communication, and consumer portal vulnerabilities across solar PV systems, battery storage, and EV chargers in March 2026. In the North America home energy management system market, this matters because a multi-vendor installation is only as secure as its weakest connected device. The absence of a unified federal certification standard for residential energy hardware further complicates adoption because homeowners and installers still face uneven device security expectations. That combination of low consumer trust and inconsistent device protection keeps cybersecurity as a real growth constraint for the North America home energy management system market through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Holds the Lead While Software Expands Faster

Hardware held 64.56% of the North America home energy management system market share in 2025, which reflects the still heavy role of physical equipment in total system spending. Smart thermostats remain the most common first step because they offer a visible path to energy savings and can connect later to a broader household control stack. The North America home energy management system market also continues to rely on smart electrical panels, energy storage systems, smart plugs, and in-home displays to create the physical control and sensing layer required for coordinated energy management. Rising US residential electricity prices in 2025 reinforced the need for hardware-led demand control, especially for households looking to manage peak usage more actively. SPAN strengthened that hardware case in February 2025 when it launched the SPAN Panel MAIN 40+MID and SPAN Panel MLO 48 with 25-50% more breaker spaces, while also positioning the products around avoiding 400-ampere service upgrade costs in all-electric homes.

Software is the fastest-growing component in the North America home energy management system (HEMS) market, with a 14.89% CAGR expected from 2026 to 2031. That expansion reflects the move toward AI-based load forecasting, tariff optimization, battery dispatch logic, and recurring platform subscriptions rather than one-time device revenue. The North America home energy management system market size for software is gaining support from the rising installed base of residential storage, which creates a larger pool of homes that need real-time orchestration across generation, storage, and flexible loads. Enphase reinforced this direction in February 2026 when it introduced Power Control software for IQ9 and IQ8 microinverter-based small commercial systems, showing how software can improve economics on top of an existing hardware base. Services are also expanding because multi-vendor integration, commissioning, monitoring, and managed participation in utility programs require specialized support as the installed asset base becomes more complex.

By Communication Technology: Wi-Fi Leads Today While Z-Wave Builds in Sensor-Dense Homes

Wi-Fi accounted for 38.76% of revenue in 2025 and remained the largest communication layer in the North America home energy management system market because it fits naturally into existing home broadband networks. It supports cloud-connected dashboards, remote configuration, software updates, and high-bandwidth data exchange without requiring a separate communication backbone in most homes. ZigBee continues to matter in utility-linked and meter-adjacent environments because low-power mesh communication still suits large distributed device deployments. Bluetooth maintains relevance for short-range setup and control, especially in simpler outlet-level or portable device configurations. HomePlug still serves certain retrofit cases where wiring conditions or building materials reduce the reliability of wireless links inside older homes.

Z-Wave is the fastest-growing communication protocol, with a 14.21% CAGR projected for 2026 to 2031, and it benefits from strong performance in battery-powered, multi-sensor environments. The Connectivity Standards Alliance released Matter 1.5 in November 2025, and the update added an Electrical Energy Tariff device type along with broader support that helps devices share pricing and energy data more consistently across protocols. That matters for the North America home energy management system market because interoperability reduces the risk that any one household must choose a single closed communication stack. It also allows a practical coexistence model where Wi-Fi handles high-bandwidth cloud tasks while Z-Wave supports low-power sensing and control at the edge. Matter 1.5.1, released in March 2026, further improved cross-platform device behavior and reinforced the push toward smoother multi-device compatibility.

By End-User: Residential Dominates While Commercial Adoption Picks Up

Residential represented 75.45% of the North America home energy management system market in 2025, and single-family homes remained the main adoption channel because homeowners can make upgrade decisions directly and capture the full benefit of bill savings. The strongest residential use case remains the home that combines solar, storage, smart thermostats, and circuit-level control into one coordinated system. The North America home energy management system (HEMS) market size in residential settings also benefits from the continued growth of distributed storage, since households with batteries gain more value from automation than households with only stand-alone connected devices. Multi-family housing still lags because split incentives between owners and tenants, shared metering, and building-level electrical complexity make deployment harder to standardize. That leaves a large underserved opportunity, but it also means most near-term growth still comes from owner-occupied homes with a clearer payback path.

Commercial is the fastest-growing end-user category, with a 15.32% CAGR projected through 2031, and much of that momentum comes from smaller facilities rather than large enterprise buildings. Small office and home office settings are increasingly using residential-style energy systems because they want automated demand control without the cost and complexity of a full building energy management platform. The North America home energy management system market is therefore widening into light commercial environments where operators care about utility cost control, energy visibility, and simple carbon reporting. Enphase’s February 2026 Power Control software launch for small commercial solar systems shows how vendors are adapting household-style energy logic for sub-commercial applications that were once outside the core HEMS scope. Retail and hospitality operators are also becoming more relevant as they look for portfolio-level visibility across smaller, distributed properties with lower integration budgets.

By Deployment Mode: Local Control Stays Important While Cloud Platforms Scale Faster

On-premises and local gateway deployments held 62.3% of revenue in 2025, showing that reliability and low-latency control still matter greatly in household energy systems. In the North America home energy management system market, local control retains value because households expect core functions to keep working during internet outages, especially when backup power and severe weather events are involved. This architecture is particularly important where battery switching, critical load prioritization, or local automation must continue without cloud dependency. Matter 1.5 also strengthened the logic for local responsiveness by adding support that improves direct device communication across the home network. For many homeowners, that practical resilience keeps gateway-based systems attractive even as more optimization functions move into the cloud.

Cloud-hosted platforms are expanding at the fastest pace, with a 15.9% CAGR expected from 2026 to 2031, because large-scale optimization works best when data from many homes is aggregated in one operating layer. The North America home energy management system (HEMS) market share tied to cloud-delivered value is rising as vendors monetize forecasting, tariff response, remote monitoring, software updates, and virtual power plant coordination. Enphase expanded PowerMatch across North America in May 2026, and the feature adjusts IQ Battery operation to match household power needs in real time, which illustrates the value of cloud-enabled optimization on top of connected hardware. A hybrid model is therefore becoming more attractive, with local gateways handling immediate device response while the cloud manages analytics, orchestration, and fleet-wide improvement. That balance fits the North America home energy management system market because it addresses resilience concerns without giving up the intelligence benefits of centralized data and software.

Geography Analysis

The United States held 81.89% of regional revenue in 2025, giving it the clear lead in the North America home energy management system (HEMS) market. The country benefits from the deepest residential solar ecosystem in the region, a broad utility incentive base, and faster deployment of dynamic pricing structures that reward automation. California’s Load Management Standards require large utilities and community choice aggregators to offer dynamic pricing options by 2027, and that rule is creating a direct policy pull for HEMS platforms that can respond automatically to grid signals. The US residential storage segment also grew 51% in 2025, which supports stronger HEMS demand because more households now need active coordination of batteries, tariffs, and home loads. The North America home energy management system market share remains concentrated in the United States because its policy support, installed hardware base, and utility program depth are still ahead of the rest of the region.

Canada provides a stable and mature demand base within the North America home energy management system market, led by utility-driven adoption in Ontario and Quebec. Ontario’s Independent Electricity System Operator projected provincial electricity demand rising from 151TWh in 2025 to 263TWh by 2050, which supports a long-term case for more active household load management. Adoption is steadier than in the United States, but Canada remains attractive because of its strong utility channel structure, high broadband access, and continued interest in household electrification.

Mexico is the fastest-growing country in the North America home energy management system market, with a 14.35% CAGR projected from 2026 to 2031. Growth is being supported by rising smart home penetration and a broader base of digitally connected households that can adopt home energy platforms over time. INEGI reported that 26% of Mexican households, or 10.2 million homes, had at least 1 smart connected device by 2024, marking a 31.5% year-over-year increase and establishing a stronger consumer foundation for future HEMS adoption. Mexico still trails the United States and Canada in AMI depth, so adoption currently leans more toward Wi-Fi-connected monitoring and software-led control than meter-linked tariff automation.

Competitive Landscape

The North America HEMS market is moderately concentrated in hardware and more fragmented in software and services, which creates an uneven but active competitive field. No single provider controls both the physical device layer and the software layer across the region, so competition is shaped by installer reach, utility relationships, cloud capability, and device interoperability. This has made ecosystem design more important than product breadth alone, because the winning platform increasingly needs to connect batteries, panels, thermostats, meters, and utility-facing software in one usable system. The North America home energy management system (HEMS) market is also seeing margins shift away from hardware-only models as software subscriptions and managed energy services capture a larger share of lifetime value. Providers that can combine a strong installed device base with data-driven optimization are therefore in a better position to protect revenue and hold customer engagement over time.

SPAN remains one of the clearest examples of strategic repositioning in the North America home energy management system market because it has pushed beyond smart panels and into grid-edge utility integration. In February 2025, the company expanded its panel offering with products designed for all-electric-ready homes and builder cost savings. That product strategy followed its earlier move toward utility-facing intelligence and shows how vendors are trying to sit at the intersection of household energy control and grid management. Enphase has taken a parallel route by layering software such as Power Control and PowerMatch on top of its installed hardware fleet, which strengthens customer value without relying only on new device sales.

Cloud-native and AI-led competitors are also reshaping the North America home energy management system market by focusing on orchestration rather than only equipment. Lunar Energy raised USD 232 million in February 2026 to scale home battery deployments and its Gridshare virtual power plant software platform, highlighting investor confidence in software-led household energy coordination. Matter 1.5 and Matter 1.5.1 are gradually reducing integration friction across mixed device environments, which weakens some of the lock-in once enjoyed by closed first-generation ecosystems. ecobee’s May 2025 launch of a Generac-integrated smart thermostat also showed how branded partnerships can expand reach by connecting energy management functions to established dealer and backup power channels.

North America Home Energy Management System (HEMS) Industry Leaders

SPAN.io, Inc.

Savant Systems, Inc.

FranklinWH Energy Storage Inc.

Lunar Energy, Inc.

Sense Labs, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Enphase Energy launched PowerMatch technology for IQ Battery 10C systems in the United States, including Puerto Rico, and IQ Battery 5P systems across North America, enabling real-time battery output adjustment to match household power needs, improving usable energy delivery and long-term homeowner savings.

- February 2026: Lunar Energy raised USD 232 million in total, comprising a USD 102 million oversubscribed Series D round led by B Capital and Prelude Ventures and a previously unannounced USD 130 million Series C led by Activate Capital, to scale home battery manufacturing and its AI-powered Gridshare VPP software platform.

- February 2026: Enphase Energy introduced Power Control software for IQ9 and IQ8 microinverter-based small commercial solar systems, designed to reduce interconnection costs, simplify regulatory review under California Energy Commission Rule 21, and improve project economics for previously unviable commercial installations.

- November 2025: The Connectivity Standards Alliance released Matter 1.5, adding a new Electrical Energy Tariff device type enabling standardized real-time and forecasted pricing and carbon intensity data sharing between utilities and home devices, alongside expanded EV charging coordination and TCP transport support.

North America Home Energy Management System (HEMS) Market Report Scope

The North America Home Energy Management System (HEMS) Market is Segmented by Component (Hardware (Smart Meters, Smart Thermostats, Energy Storage Systems, Smart Plugs and Outlets, In-Home Displays (IHDs), and Other Hardware), Software, Services), Communication Technology (ZigBee, Wi-Fi, Z-Wave, Bluetooth, HomePlug, and Other Communication Technologies), End-User (Residential (Single-Family Homes and Multi-Family Housing), Commercial (Small Office / Home Office, and Retail and Hospitality), Deployment Mode (Cloud-Hosted Platforms and On-Premises / Local Gateway), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Smart Meters |

| Smart Thermostats | |

| Energy Storage Systems | |

| Smart Plugs and Outlets | |

| In-Home Displays (IHDs) | |

| Other Hardwares | |

| Software | |

| Services |

| ZigBee |

| Wi-Fi |

| Z-Wave |

| Bluetooth |

| HomePlug |

| Other Communication Technologies |

| Residential | Single-Family Homes |

| Multi-Family Housing | |

| Commercial | Small Office / Home Office |

| Retail and Hospitality |

| Cloud-Hosted Platforms |

| On-Premises / Local Gateway |

| United States |

| Canada |

| Mexico |

| By Component | Hardware | Smart Meters |

| Smart Thermostats | ||

| Energy Storage Systems | ||

| Smart Plugs and Outlets | ||

| In-Home Displays (IHDs) | ||

| Other Hardwares | ||

| Software | ||

| Services | ||

| By Communication Technology | ZigBee | |

| Wi-Fi | ||

| Z-Wave | ||

| Bluetooth | ||

| HomePlug | ||

| Other Communication Technologies | ||

| By End-User | Residential | Single-Family Homes |

| Multi-Family Housing | ||

| Commercial | Small Office / Home Office | |

| Retail and Hospitality | ||

| By Deployment Mode | Cloud-Hosted Platforms | |

| On-Premises / Local Gateway | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the market size outlook for the North America home energy management system (HEMS) market?

The North America home energy management system (HEMS) market stood at USD 1.51 billion in 2025, reached USD 1.72 billion in 2026, and is projected to reach USD 3.26 billion by 2031 at a 13.64% CAGR.

Which component category currently leads revenue generation?

Hardware led revenue in 2025 with a 64.56% share, supported by strong demand for smart thermostats, smart panels, storage systems, and smart plugs.

Which deployment model is growing the fastest through 2031?

Cloud-hosted platforms are expanding the fastest, with a projected 15.91% CAGR, because AI optimization, remote updates, and VPP services work best on cloud infrastructure.

Why is the United States the largest country in this space?

The United States held 81.89% of regional revenue in 2025 because it combines a large residential solar base, deeper incentive coverage, and broader dynamic pricing adoption.

What is holding back wider household adoption?

The main barriers are high upfront system and installation costs, along with rising concerns about cybersecurity and household data privacy across connected energy devices.

Which end-user group is expanding most quickly?

Commercial applications are growing the fastest at a 15.32% CAGR through 2031, especially in small office, retail, and hospitality settings seeking simpler automated energy control.

Page last updated on: