Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

North America Fitness Ring Market is Segmented by Product Type (Basic Fitness Rings, and Smart Fitness Rings), Distribution Channel (Online Stores, and Offline Stores), Application (Health and Wellness Monitoring, Sports and Performance Analytics, and More), Price Tier (≤USD 199, USD 200-USD 399, and ≥USD400), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

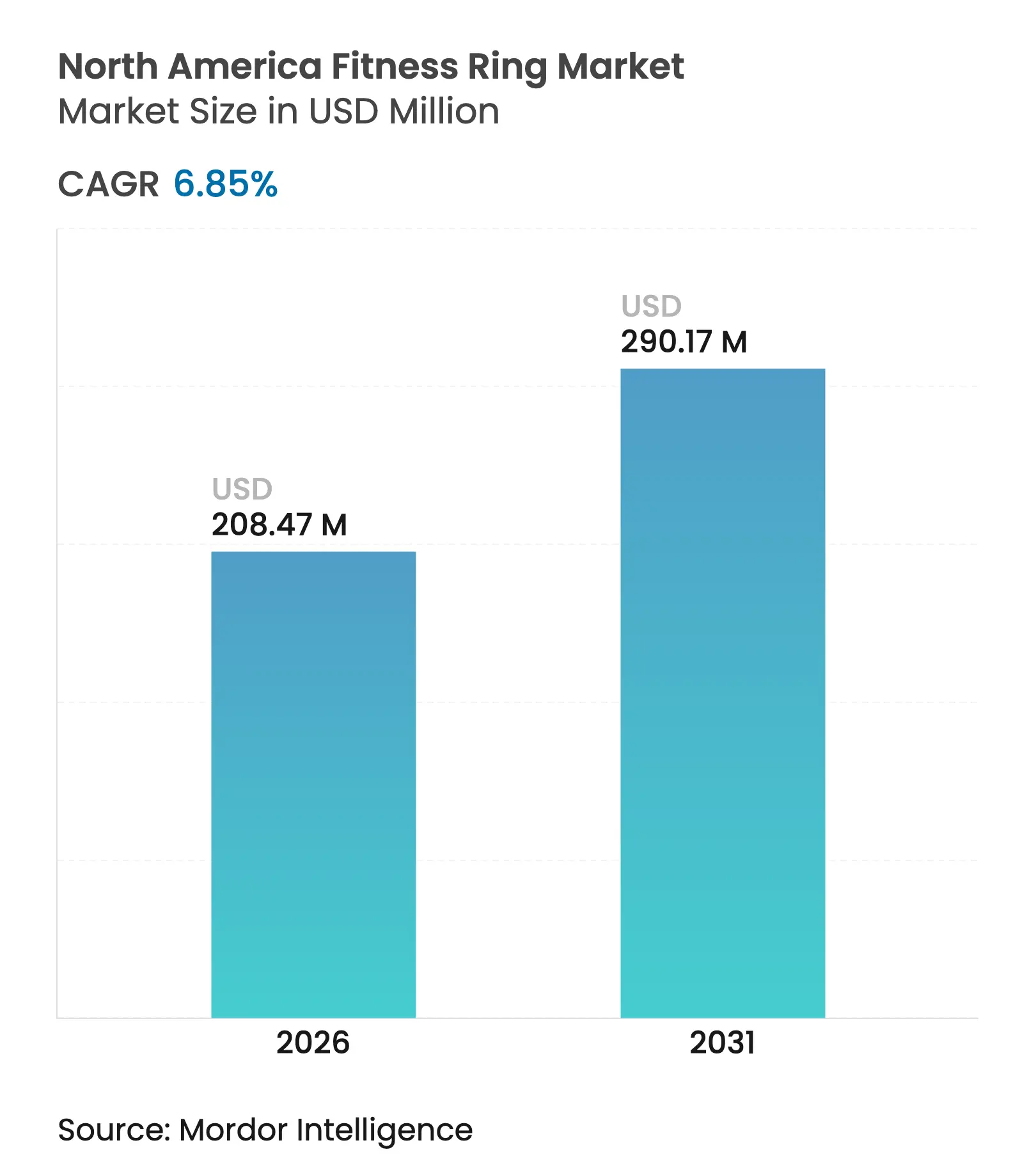

| Market Size (2026) | USD 208.47 Million |

| Market Size (2031) | USD 290.17 Million |

| Growth Rate (2026 - 2031) | 6.85 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The North America fitness ring market size is expected to grow from USD 195.10 million in 2025 to USD 208.47 million in 2026 and is forecast to reach USD 290.17 million by 2031 at 6.85% CAGR over 2026-2031. Continuous regulatory support from the US FDA and Health Canada, coupled with employer reimbursement through HSA and FSA channels, shapes a climate in which smart rings transition from consumer novelties to medically recognized devices.[1]American Academy of Sleep Medicine, “FDA clears Happy Ring by Happy Health,” aasm.org Four structural factors that maintain growth momentum are miniaturized sensors that now capture more than 140 biometric parameters, enterprise wellness programs linking device rollouts to productivity metrics, smartphone ecosystem lock-in that raises switching costs for users, and premium pricing justified by FDA-cleared clinical features. Competitive rivalry intensifies as Oura, Samsung, Google, and a cluster of US start-ups secure approvals for atrial fibrillation, pulse oximetry, and AI-driven sleep diagnostics, encouraging higher research spending on custom SiP designs.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising

technological sophistication of ring-miniaturised sensors

Rising

technological sophistication of ring-miniaturised sensors

| +1.8% | United States leading innovation, Canada following adoption | Medium term (2-4 years) |

(~)

% Impact on CAGR Forecast

:

+1.8%

|

Geographic

Relevance

:

United

States leading innovation, Canada following adoption

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Demand

for screen-free, discreet wearables

Demand

for screen-free, discreet wearables

| +1.2% | Strongest in US professional markets, expanding to Canada | Short term (≤2 years) | |||

Ecosystem

lock-in strategies by smartphone OEMs

Ecosystem

lock-in strategies by smartphone OEMs

| +1.5% | US-driven by Samsung/Apple, spillover to Canada and Mexico | Medium term (2-4 years) | |||

Workplace

wellness programme reimbursements

Workplace

wellness programme reimbursements

| +0.9% | US corporate programs, expanding to Canadian enterprises | Short term (≤2 years) | |||

FDA-cleared

clinical use-cases unlock payer coverage

FDA-cleared

clinical use-cases unlock payer coverage

| +1.1% | United States regulatory leadership, Health Canada following | Long term (≥4 years) | |||

Sports-leagues'

biometric data monetisation deals

Sports-leagues'

biometric data monetisation deals

| +0.7% | US professional sports, expanding to Canadian leagues | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising technological sophistication of ring-miniaturised sensors

North America supplies the majority of global patents on sub-4 gram ring modules incorporating PPG, ECG, and SpO₂ sensors at clinical accuracy thresholds. US-based Happy Health secured the first FDA nod for an AI-powered sleep diagnostic ring, demonstrating that advanced SiP packaging can satisfy Class II device requirements.[2]Medical Device Network, “FDA approves Happy Health's medical-grade wearable smart ring,” medicaldevice-network.com University of Waterloo antenna research overcomes transmission loss to enable 30 m data range, reducing dropouts in Canada’s remote patient monitoring networks. Such advances allow continuous monitoring of latent arrhythmias, oxygen desaturation, and HRV without compromising form factor or comfort.

Demand for screen-free, discreet wearables

Corporate cultures across the United States and Canada favour unobtrusive devices that avoid the distraction of wrist-borne screens. Rings satisfy this social requirement while offering gesture control of smart homes and VR systems, illustrated by the IRIS prototype achieving 24-hour battery life at CES 2025.[3]arXiv, “IRIS: Wireless Ring for Vision-based Smart Home Interaction,” arxiv.org North American professionals endorse discreet wear because it aligns with boardroom etiquette and uniform policies. As a result, shipment volumes to enterprise wellness schemes have doubled since 2024 according to manufacturer declarations.

Ecosystem lock-in strategies by smartphone OEMs

Samsung’s Galaxy Ring pairs with the Galaxy Watch and phone to generate a composite Vitality Score, incentivising users to remain within the brand environment.[4]The Verge, “Samsung has big ambitions for the Galaxy Ring,” theverge.com Apple patent filings describe NFC payments and modular sensor pods that likewise promote retention. These tactics resonate in a region where average device ownership per adult surpasses three, elevating the North America fitness rings market by integrating health data across screens, buds, and rings.

Workplace wellness programme reimbursements

Oura’s FSA/HSA eligibility converts an out-of-pocket expense into a pretax benefit for US employees. Corporate clients report 88% of ring-wearing staff improve sleep quality, supporting employer ROI and stimulating bulk procurement. Canadian firms replicate this model, while insurers begin offering premium rebates for continuous biometric insight, embedding smart rings in occupational health policy.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited

multi-day battery life versus bands & watches

Limited

multi-day battery life versus bands & watches

| -1.3% | Across North America, higher impact in remote Canadian regions | Short term (≤2 years) |

(~)

% Impact on CAGR Forecast

:

-1.3%

|

Geographic

Relevance

:

Across

North America, higher impact in remote Canadian regions

|

Impact

Timeline

:

Short

term (≤2 years)

|

Data-privacy

compliance costs (HIPAA, CPRA)

Data-privacy

compliance costs (HIPAA, CPRA)

| -0.8% | United States federal and state regulations, Canada following | Medium term (2-4 years) | |||

Supply-chain

dependence on custom SiP foundries

Supply-chain

dependence on custom SiP foundries

| -1.1% | North America dependent on APAC manufacturing | Long term (≥4 years) | |||

Nickel-allergy

litigation risk

Nickel-allergy

litigation risk

| -0.4% | United States litigation environment, expanding to Canada | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited multi-day battery life versus bands & watches

Most rings deliver 3–7 days on a single charge, whereas bands exceed 14 days, constraining adoption among hikers, field engineers, and remote workers throughout North America. Samsung’s solid-state battery trials add capacity but raise bill-of-materials, making sub-USD 200 pricing unattainable. Research into battery-free picoRing concepts remains experimental and requires paired devices, limiting near-term commercialisation.

Data-privacy compliance costs (HIPAA, CPRA)

Only 20 US states enforce comprehensive privacy statutes, forcing firms to customize data handling across jurisdictions. CPRA mandates opt-out and deletion workflows that elevate operating costs for start-ups. A peer-reviewed analysis identifies ambiguity regarding whether consumer-generated biometric data qualifies as Protected Health Information, thereby raising litigation risk.

By Product Type: Smart features enlarge the value gap

Smart fitness rings captured 83.45% of the North America fitness rings market in 2025 and are expected to advance at 8.35% CAGR through 2031. The segment benefits from FDA-cleared applications, such as AFib detection by Ultrahuman and pulse oximetry by Movano, which enable rings to be integrated into reimbursable clinical workflows. Consequently, Smart fitness rings support premium pricing and subscription revenues originating from AI-driven health guidance.

Basic Fitness Rings remain largely popular in Mexico, where price sensitivity is high, but their relevance is eroding as sensor costs decline and North American consumers seek clinical-grade outputs. A meta-analysis in Applied Sciences verifies that smart rings match medical devices in terms of sleep staging accuracy, reinforcing the shift. For innovators, this divergence allows for clear segmentation; high-feature rings compete against watches on data depth, while basic rings retreat to budget niches.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital first dominates customer acquisition

Online Stores owned 66.20% of 2025 revenue and project a 9.1% CAGR to 2031. Self-sizing applications and augmented-reality fitting tools reduce return rates, meeting North American consumer expectations for seamless e-commerce journeys. Direct-to-consumer models also accommodate firmware updates and membership plans without retail mark-ups, cementing brand loyalty.

Offline Stores retain relevance for premium metals or custom engraving, where tactile evaluation matters to affluent US and Canadian buyers. Partnerships with Best Buy and medical supply chains allow demonstration kiosks that integrate HRV dashboards on in-store tablets. Retail presence, therefore, strengthens omnichannel narratives that comfort late adopters wary of sizing errors.

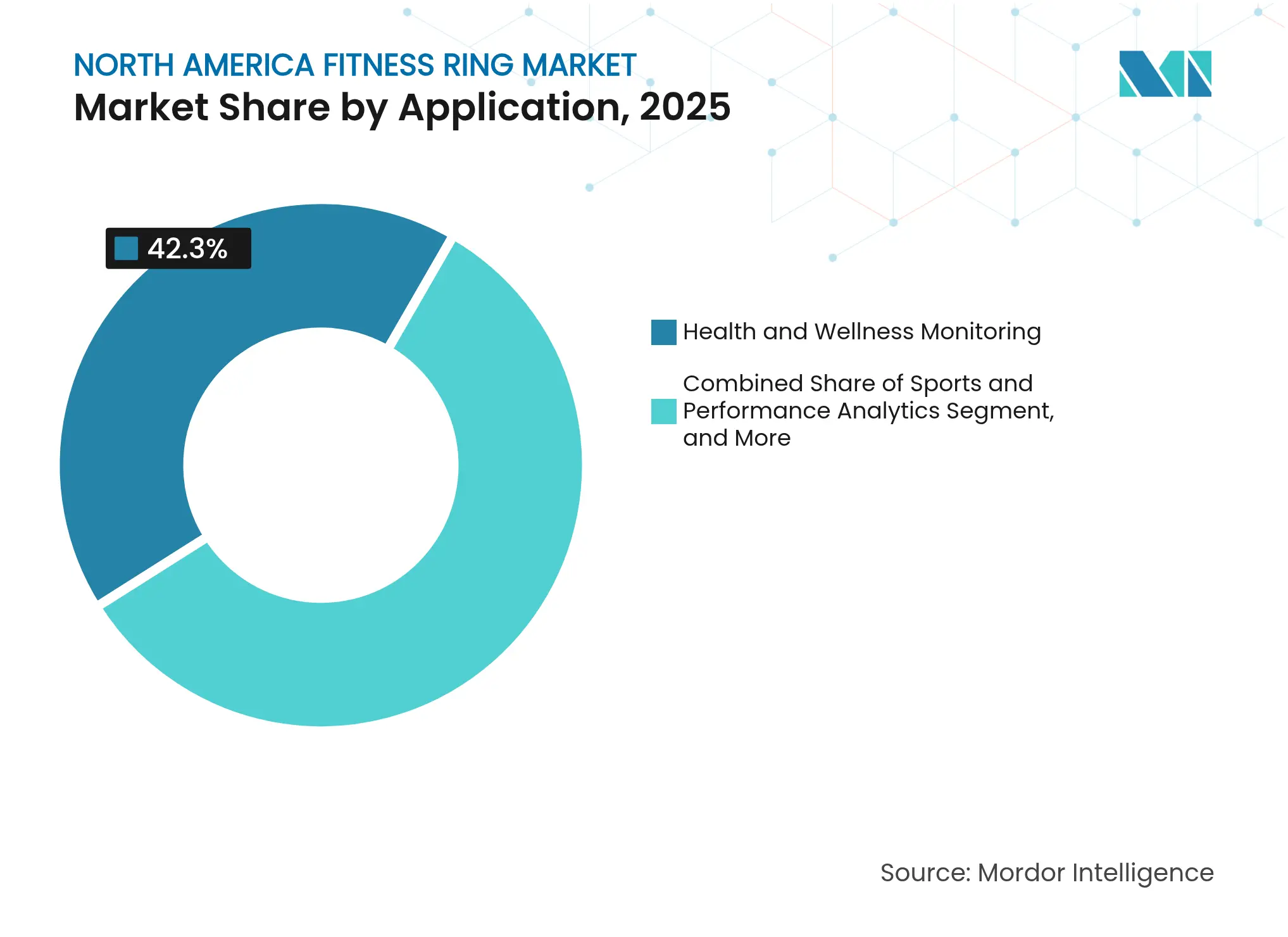

By Application: Clinical validation expands revenue per user

Health and wellness monitoring held a 42.30% share in 2025, while medical and remote patient monitoring is the fastest-growing segment, with a 9.2% CAGR. FDA clearance for sleep apnea diagnosis and glucose data integration aligns with payer priorities to curb chronic disease costs. Telemedicine providers now bundle rings in post-operative kits, which lifts the average selling price and recurring data-service fees.

Sports and Performance Analytics sustains demand via ATP Tour approval for in-match wear, which raises consumer awareness beyond elite athletes. Sleep and Recovery Tracking continues to attract knowledge workers seeking cognitive performance gains, underpinning subscription upgrades that add guided recovery programmes.

Note: Segment shares of all individual segments available upon report purchase

By Price Tier: Premium band drives margin expansion

The USD 200-399 band represented 57.10% of sales in 2025, anchoring volumes. Yet the ≥USD 400 band is on 7.85% CAGR trajectory as titanium builds, sapphire lenses, and AI analytics validate higher price tags for North American buyers who associate medical clearance with trustworthy data.

At a price of ≤ USD 199, competition from Chinese imports intensifies, but lacks FDA approval, which limits uptake among health-focused segments. North American vendors guard their share by emphasizing compliance certifications, local warranties, and integration with payer portals.

The United States anchors the North America fitness rings market with a 90.90% share, reflecting the earliest convergence of regulatory clearance, employer subsidies, and affluent early adopters. Device makers leverage FDA adjudication to position rings as durable medical equipment, qualifying them for pretax spending accounts that shape purchase behaviour. Sports league endorsement, notably the ATP Tour’s wearable approval, reinforces mainstream awareness and social acceptance. At the same time, state-level privacy statutes led by California elevate operational overhead, nudging smaller firms toward partnerships or acquisitions.

Canada offers the fastest expansion path at an 8.1% CAGR because Health Canada honors FDA dossiers through mutual recognition provisions. Government pilot schemes deploy rings for remote cardiac rehabilitation in rural communities, aligning with policy aims to reduce hospital readmissions. Cross-border e-commerce enables Canadian consumers to import US-launched models almost simultaneously, although duty and warranty harmonization remain focal points for brand strategy.

Mexico introduces a long-run growth vector. Rising middle-class income supports adoption, yet price sensitivity channels demand into USD 200-399 tiers. Manufacturers that adapt packaging, language support, and payment plans will gain early foothold while awaiting clearer reimbursement rules. Smartphone penetration topping 80% strengthens ecosystem sync for ring apps, suggesting that once COFEPRIS accelerates device approvals, uptake can mirror the curve seen in Canada five years prior.

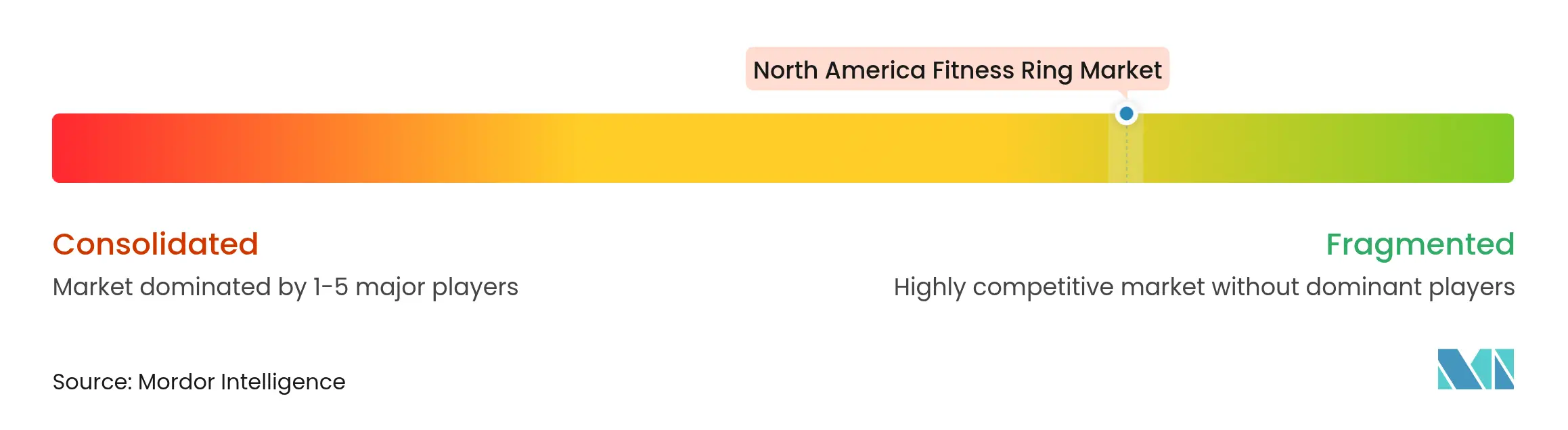

Market Concentration

Competition centres on technology validation and ecosystem reach rather than pure hardware. Oura leads with a USD 5.2 billion valuation after a USD 200 million Series D, enabling deeper AI feature roll-outs and the planned Dexcom glucose sensor link. Samsung quickly followed with Galaxy Ring, integrating vital metrics across its phone and watch lineups, a move designed to capture Android loyalists. Google’s Fitbit division advances patent filings for gesture-enabled rings but has not declared launch timing.

Litigation risk highlights the stakes. Samsung’s pre-emptive suit against Oura was dismissed, yet the event underscores the strategic value of IP portfolios in the North America fitness rings industry. Mid-tier innovators, such as Circular and Happy Health, differentiate themselves via single-use FDA clearances for ECG or sleep testing. Chipset providers Ambiq and Bravechip deliver power savings that reduce the bill of materials by 30%, presenting supply chain leverage for emerging brands.

White-space remains in disease-specific monitoring. Movano’s pulse oximetry and Ultrahuman’s atrial fibrillation features preview chronic condition platforms that could partner with insurers for value-based care. Fashion-tech collaborations, such as Ultrahuman’s 18K gold editions, seek margin upside from consumers who merge jewellery aesthetics with clinical function.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

North America fitness rings market tracks the revenue incurred through selling smart and basic fitness tracker rings offered by market vendors (directly, through partners, and e-commerce platforms) to consumers in North America.

The North America Fitness Rings Report is Segmented by Product Type (Basic Fitness Rings, and Smart Fitness Rings), Distribution Channel (Online Stores, and Offline Stores), Application (Health and Wellness Monitoring, Sports and Performance Analytics, Sleep and Recovery Tracking, and Medical and Remote Patient Monitoring), Price Tier (≤USD 199, USD 200-USD 399, and ≥USD400), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Feasibility Analysis for FBO Services in East Africa

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.