United States Gaming Headsets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

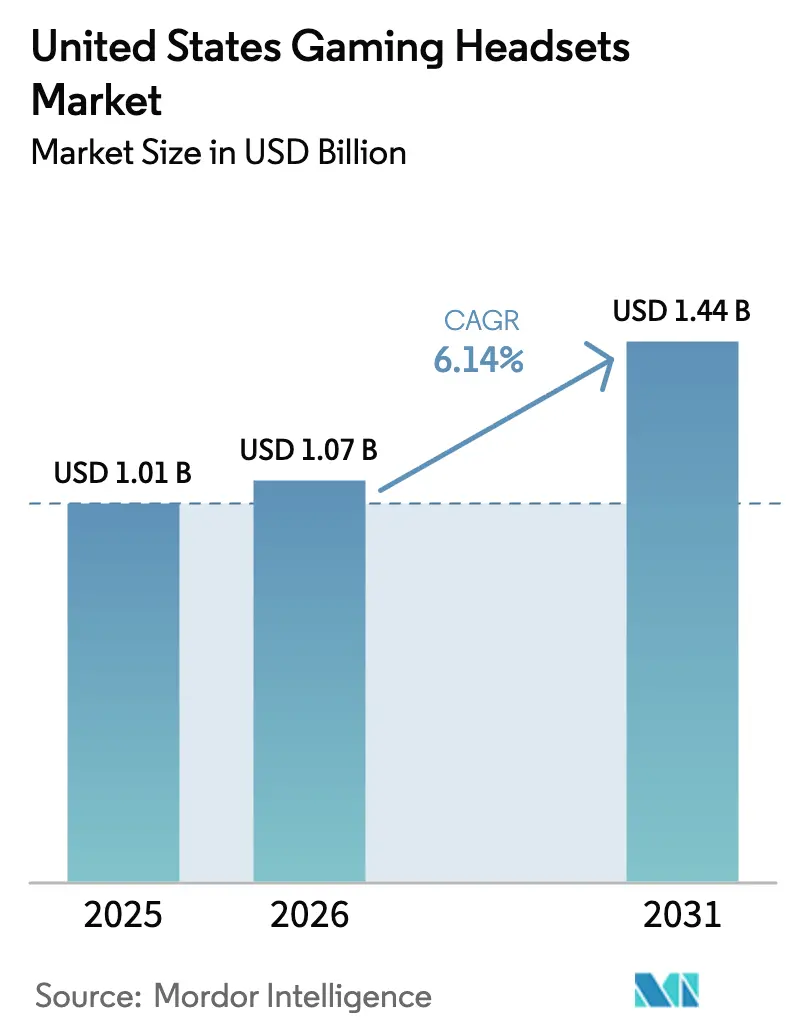

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.07 Billion |

| Market Size (2031) | USD 1.44 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Gaming Headsets Market Analysis by Mordor Intelligence

The United States Gaming Headsets Market size in 2026 is estimated at USD 1.07 billion, growing from 2025 value of USD 1.01 billion with 2031 projections showing USD 1.44 billion, growing at 6.14% CAGR over 2026-2031. The gaming headsets market benefits from sustained esports growth, rising demand for cross-platform voice chat, and headset designs that incorporate AI-driven spatial audio. Wired models keep traction among competitive gamers, yet wireless innovation is accelerating as low-latency protocols mature. Regulatory moves that set noise-exposure caps and e-waste obligations spur product differentiation around hearing health and sustainability. Semiconductor supply headwinds are moderating as manufacturers secure alternate sources, but component pricing remains a margin pressure that favors scale players.

Key Report Takeaways

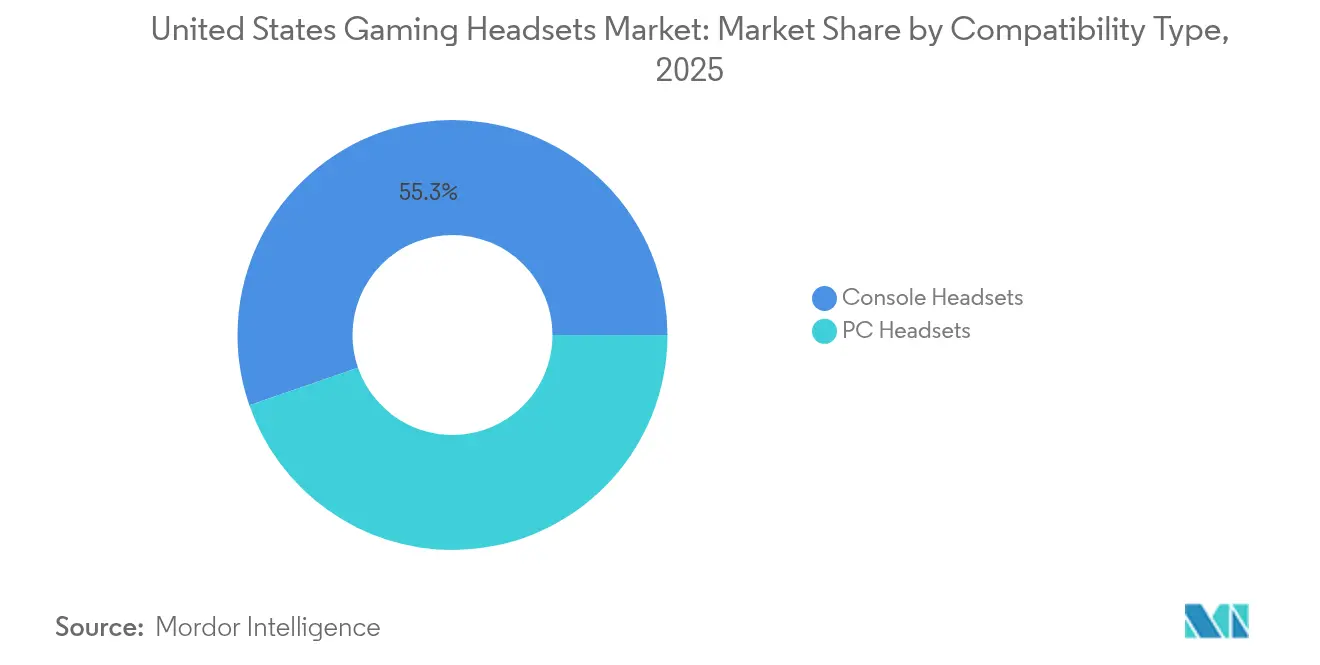

- By compatibility type, console headsets held 55.30% of the gaming headsets market share in 2025, while PC headsets are forecast to expand at a 9.45% CAGR to 2031.

- By connectivity type, wired solutions accounted for 60.75% of the gaming headsets market size in 2025; wireless is set to grow at an 11.32% CAGR through 2031.

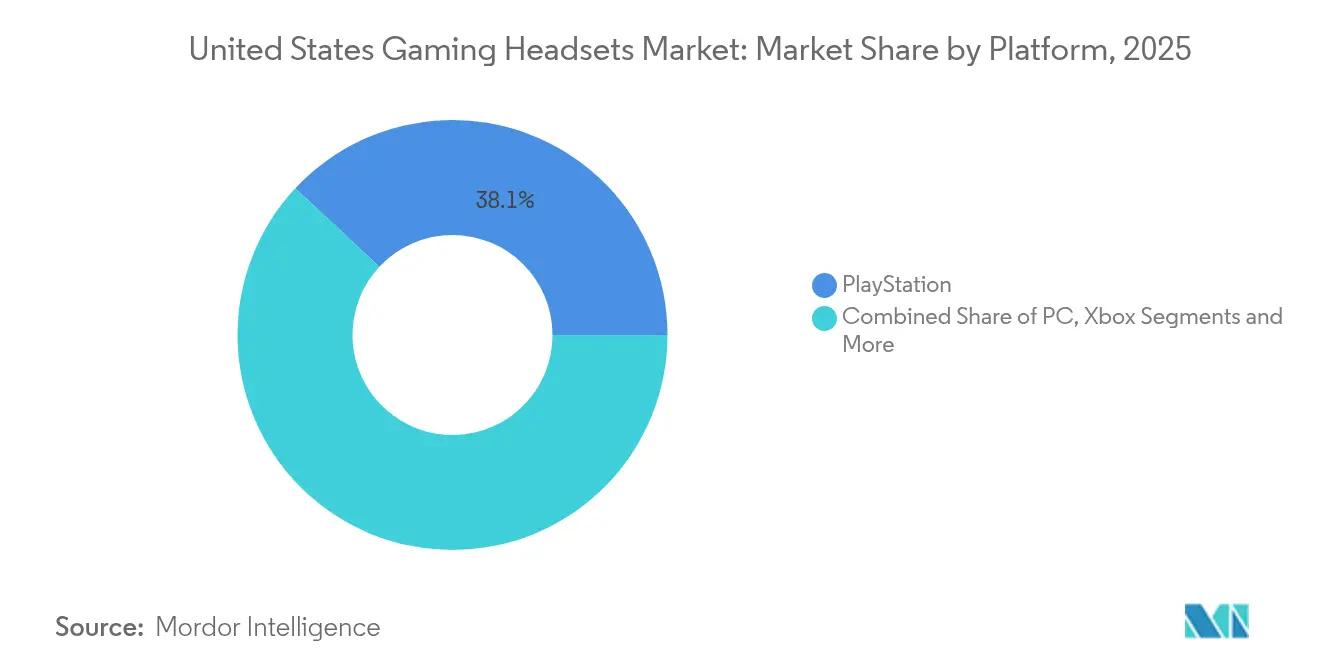

- By platform, PlayStation led with a 38.05% revenue share in 2025, whereas PC gaming records the highest projected CAGR at 8.55% to 2031.

- By sales channel, online distribution commanded 57.60% of the gaming headsets market size in 2025 and is advancing at a 9.85% CAGR.

- By end-user, casual gamers and streamers represented 64.10% of revenue in 2025, but professional esports is projected to expand at a 12.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United states operates as part of an interconnected international environment rather than as a self-contained country level unit. The gaming headsets market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

United States Gaming Headsets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Esports viewership boom & sponsorship influx | +1.8% | West Coast hubs | Medium term (2-4 years) |

| Rising adoption of VR/AR-ready consoles & PCs | +1.2% | National metro markets | Long term (≥ 4 years) |

| Surge in cross-platform multiplayer titles requiring voice chat | +1.5% | Global | Short term (≤ 2 years) |

| Broadband upgrades enabling low-latency spatial audio | +0.9% | Fiber-enabled regions | Medium term (2-4 years) |

| Growing awareness of hearing-health features | +0.7% | California and Oregon | Short term (≤ 2 years) |

| AI-driven audio personalisation & haptics integration | +0.4% | Silicon Valley innovation centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Esports viewership boom & sponsorship influx

Professional esports broadcasts attract growing audiences and corporate sponsors, prompting gamers to replicate tournament-grade setups that prioritize ultra-low-latency audio and certified noise isolation. The Discord Social SDK, launched in March 2025, embeds high-quality comms directly into games, elevating headset performance expectations.[1]Discord, “Discord Launches SDK to Power Social Infrastructure and Communications for Games,” discord.com Sponsorship agreements showcase premium peripherals during live events, turning pro players into high-credibility brand ambassadors. The resulting visibility accelerates the gaming headsets market as mainstream users adopt devices once limited to professional arenas. Manufacturers respond with models certified for league play, reinforcing a cycle where esports shapes mass-market design priorities.

Rising adoption of VR/AR-ready consoles & PCs

Virtual and augmented reality titles demand accurate 3D audio cues that traditional stereo hardware cannot replicate. Sony's patents on AI-generated ambisonic soundfields underline the platform vendor's commitment to immersive sound.[2]Patent Nweon, “Sony Patent | Artificial intelligence (ai)-based generation of ambisonic soundfield,” patent.nweon.com Meta’s dynamic torso reflection filtering targets biologically authentic spatial audio. Such innovations raise consumer expectations and steer the gaming headsets market toward head-tracking sensors, low-latency chipsets, and comfort features that accommodate extended VR sessions. Elevated component requirements translate into premium price points, creating a profitable niche for brands that deliver convincing spatial audio experiences.

Surge in cross-platform multiplayer titles requiring voice chat

Unified voice chat is critical when players transition between console, PC, and mobile environments. Discord’s SDK minimizes fragmentation, making seamless communication a default expectation. The gaming headsets market therefore rewards multipoint connectivity, consistent microphone clarity, and codec flexibility. Wireless versatility becomes a buying trigger as gamers link a single headset to several devices without re-pairing. To sustain low latency, manufacturers are optimizing compression algorithms and adopting dual-radio designs that balance 2.4 GHz and Bluetooth throughput.

Broadband upgrades enabling low-latency spatial audio

Trials of Low Latency, Low Loss, and Scalable Throughput (L4S) technology demonstrate near-instant packet delivery that opens cloud-based audio processing possibilities. As broadband providers plan L4S rollouts,[3]Broadband Forum, “Roadmap launched to implement low latency ‘L4S’ technology into broadband networks,” broadband-forum.org headset vendors experiment with hybrid architectures where on-device DSP manages core functions while the cloud refines spatial algorithms. This shift could lower on-device silicon costs yet heighten service revenues tied to subscription-based audio personalization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor supply volatility | -1.1% | Asian supply chains | Short term (≤ 2 years) |

| Substitution by non-gaming hearables & earbuds | -0.8% | Mobile-first demographics | Medium term (2-4 years) |

| State-level noise-exposure regulations raising compliance costs | -0.4% | California and Oregon | Short term (≤ 2 years) |

| Sustainability & e-waste compliance pressures | -0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor supply volatility

Memory price hikes announced for 2025-2026 increase bill-of-materials costs for DSP-intensive models.[4]TechPowerUp, “Micron Announces Memory Price Increases for 2025-2026 Amid Supply Constraints,” techpowerup.com Concentration of advanced chip fabrication in East Asia exposes the gaming headsets market to geopolitical shocks and natural disasters. Some brands redesign boards around older-node silicon or adopt multi-sourcing, but these mitigations only partially offset cost spikes and may constrain performance.

Substitution by non-gaming hearables and earbuds

Mobile-centric consumers increasingly rely on multipurpose true wireless earbuds that incorporate gaming modes. This substitution risk intensifies when mobile titles dominate playtime, eroding share from premium over-ear headsets. Brands attempt to defend by releasing compact gaming earbuds such as SteelSeries Arctis Gamebuds, yet price-sensitive users can still migrate to generic audio devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compatibility Type: Console momentum sustains revenue leadership

Console headsets captured 55.30% of 2025 revenue, demonstrating entrenched loyalty among platform-specific gamers. The segment, valued at USD 0.56 billion, anchors the gaming headsets market size and sets acoustic tuning benchmarks aligned with PlayStation and Xbox sound engines. Sony’s AI-driven ambisonic advancements amplify demand for console-optimized models.

PC headsets, worth USD 0.45 billion, are on track for a 9.45% CAGR as streaming, modding, and cross-platform play intensify. The open nature of PC hardware fuels an extensive aftermarket for swappable cables, DACs, and ear-cup materials. Brands differentiate through software suites that allow granular EQ, microphone gating, and macro integration. This customization culture attracts power users who boost average selling prices, thereby magnifying PC’s influence on overall gaming headsets market trends.

By Connectivity Type: Wireless innovation narrows the latency gap

Wired options maintained 60.75% revenue share in 2025, corresponding to USD 0.61 billion of the gaming headsets market size. Tournament organizers still insist on cabled links to avoid RF congestion in arenas. In parallel, Qualcomm’s Snapdragon Sound and XPAN protocols enable lossless Wi-Fi audio with sub-20 ms delay. Wireless revenue, now USD 0.4 billion, is forecast to climb 11.32% annually.

Battery advances extend playtime beyond 50 hours, while swappable packs address marathon streaming sessions. Firmware upgrades add multipoint pairing across console, PC, and smartphone. As confidence in link stability rises, more professional teams adopt wireless for scrims, signalling broader mainstream acceptance and boosting the gaming headsets market.

By Platform: PC becomes the growth engine

PlayStation generated 38.05% of 2025 headset revenue, driven by exclusive titles and Tempest 3D AudioTech compatibility that rewards certified gear. PC’s 8.55% forecast CAGR rests on its dual role as a gaming and content-creation hub. High-fidelity microphones, broadcast-ready EQ, and open APIs appeal to streamers who view audio quality as brand equity.

Xbox, Nintendo Switch, and mobile/cloud segments each fill distinct niches. Xbox users value Dolby Atmos integration, Switch owners prioritize portability, and cloud gamers seek codecs resilient to variable bandwidth. Vendors carve targeted SKUs that match these needs, thereby diversifying revenue streams within the gaming headsets market.

By Sales Channel: Digital commerce widens its edge

Online storefronts represented 57.60% of 2025 sales, equal to USD 0.58 billion of the gaming headsets market. Detailed spec sheets, influencer reviews, and algorithmic recommendations convert shoppers who research extensively before purchase. Direct-to-consumer models raise margins and accelerate feedback loops for firmware updates.

Brick-and-mortar outlets remain vital for experiential demos and holiday gifting, yet their share is slipping as click-and-collect integrates showrooming behaviors. Retail chains invest in in-store streaming stations where customers test microphone pickup and sidetone, a tactic that helps retain relevance.

By End-User: Esports professionalism pushes technology frontier

Casual gamers and streamers account for 64.10% of spending, roughly USD 0.65 billion. They gravitate toward RGB aesthetics, plug-and-play setup, and multi-platform flexibility. Professional and semi-pro esports players, though contributing only USD 0.36 billion, influence specifications across the gaming headsets market. Their 12.25% CAGR sparks R&D in tournament-grade wireless, reinforcement for headband fatigue, and 360-degree microphone boom rotation.

League regulations around hardware certification shape design constraints, compelling vendors to balance competitive requirements with mass-market cost targets. This trickle-down effect embeds once-premium features AI noise suppression, fingertip EQ presets, detachable cables into mid-tier models, elevating baseline expectations among mainstream audiences.

Geography Analysis

Regional disparities guide headset adoption patterns across the United States. The West commands the largest share of the gaming headsets market as Silicon Valley and Los Angeles host esports arenas, dev studios, and audio-tech labs. High fiber penetration enables low-latency cloud audio trials, and state mandates on safe listening accelerate the uptake of regulated headsets.

The Northeast and Midwest collectively rank second in revenue, buoyed by dense college esports leagues and robust console ownership. Retail specialists thrive here by staging weekly tournaments that double as product showcases. Rural pockets still contend with inconsistent broadband, slowing adoption of cloud-dependent audio personalization services, but not core device sales.

Southern states exhibit the fastest aggregate growth as mobile titles capture youth demographics. Portable wireless earbuds designed specifically for gaming entice this cohort, edging out traditional over-ear designs in warm climates. Meanwhile, Texas and Georgia data centers underpin national game-streaming infrastructure, indirectly supporting demand for headsets capable of handling compressed cloud audio without artifacts.

Regulatory patchwork complicates go-to-market strategies. Oregon mirrors California in safe-listening statutes, whereas other states focus on e-waste. Brands that market recyclable components and repairable ear pads build goodwill in these jurisdictions. Such regional nuances require adaptive distribution and messaging, yet they collectively reinforce the broader upward trajectory of the gaming headsets market.

The gaming headsets market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Middle East and Africa, Middle East and Africa, and North America, along with detailed country-level analysis for Canada, China, India, United Kingdom, Japan, and Germany.

Competitive Landscape

The gaming headsets market is moderately concentrated. Turtle Beach maintains roughly 40% revenue share through brand lineage and a distribution network that blankets both specialty and mass retail. Its 2024 purchase of Performance Designed Products added controller and charging accessories, facilitating bundled promotions that lock in ecosystem spend.

Logitech leverages Blue Microphones know-how to integrate broadcast-quality mics that appeal to creators, while Razer and SteelSeries prioritize software layers that sync illumination, EQ, and haptics across peripherals. Sony positions first-party headsets as optimal companions for PlayStation’s proprietary 3D audio, capturing platform-loyal buyers.

Patent filings reveal an arms race in AI-mediated sound shaping, variable head-related transfer functions, and vibrotactile cues. Start-ups attempt to disrupt with open-source firmware and modular drivers manufactured from recycled polymers. Although their volumes are modest, such entrants keep price pressure on incumbents and accelerate feature proliferation across the gaming headsets market.

Strategic moves center on vertical integration and cloud services. Meta invests in spatial audio IP to align headsets with Quest VR devices. Qualcomm collaborates with multiple brands to embed Snapdragon Sound reference designs, broadening the pool of wireless offerings that match mobile expectations. As technology gaps narrow, marketing narratives shift toward sustainability, hearing health, and cross-device convenience, themes that increasingly determine brand loyalty.

United States Gaming Headsets Industry Leaders

Logitech International S.A.

Razer Inc.

Corsair Gaming

Sony Interactive Entertainment

HyperX (HP Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Razer launched the Clio gaming chair accessory designed to enhance audio immersion, expanding its peripheral ecosystem.

- March 2025: Discord introduced its Social SDK for unified in-game voice chat, a catalyst for cross-platform headset optimization.

- March 2025: Turtle Beach announced plans to report Q4 2024 and full-year 2024 results following its acquisition of Performance Designed Products.

- October 2024: The ITU approved the H.872 safe-listening standard for gameplay and esports headsets.

United States Gaming Headsets Market Report Scope

Gaming headsets are headphones designed specifically for video games, boast superior sound quality, integrated microphones for in-game communication, and frequently offer additional features like noise cancellation, surround sound, and wireless connectivity. These headsets elevate the gaming experience, delivering crisp audio and enabling seamless communication, particularly in multiplayer and competitive gaming settings.

The United States gaming headsets market is segmented by compatibility type (console headset and PC headset), by connectivity type (wired and wireless), and by sales channel (retail and online). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Console Headsets |

| PC Headsets |

| Wired |

| Wireless |

| Xbox |

| PlayStation |

| Nintendo Switch |

| PC |

| Mobile/Cloud |

| Retail |

| Online |

| Professional and Semi-pro Esports |

| Casual Gamers and Streamers |

| By Compatibility Type | Console Headsets |

| PC Headsets | |

| By Connectivity Type | Wired |

| Wireless | |

| By Platform | Xbox |

| PlayStation | |

| Nintendo Switch | |

| PC | |

| Mobile/Cloud | |

| By Sales Channel | Retail |

| Online | |

| By End-User | Professional and Semi-pro Esports |

| Casual Gamers and Streamers |

Key Questions Answered in the Report

What is the current value of the United States gaming headsets market?

The gaming headsets market stands at USD 1.07 billion in 2026.

Which segment is growing fastest in the gaming headsets market?

Wireless connectivity is expanding at an 11.32% CAGR through 2031.

How large is the PC platform opportunity for headset vendors?

PC-focused revenue is projected to rise at an 8.55% CAGR, outpacing console growth.

Why are safe-listening features becoming standard in gaming headsets?

State regulations and the ITU H.872 standard require exposure tracking and limiters that protect hearing.

Who holds the largest share in the gaming headsets market?

Turtle Beach retains about 39.40% revenue share, leading the competitive field.

How will VR adoption influence headset design?

VR gameplay demands precise 3D audio and head-tracking, so vendors are adding ambisonic processing and comfort features for extended sessions.

Page last updated on: