Animal Nutrition & Wellness

4th JuneDeep-Dive Analysis of Feed Probiotics Across Key Regions

5 Min Read

The North America Feed Anti-Caking Agent Market Report is Segmented by Type (Silicon-Based, Sodium-Based, Calcium-Based, Potassium-Based, and More), by Animal Type (Ruminant, Poultry, Swine, Aquaculture, and More), and by Geography (United States, Canada, Mexico, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

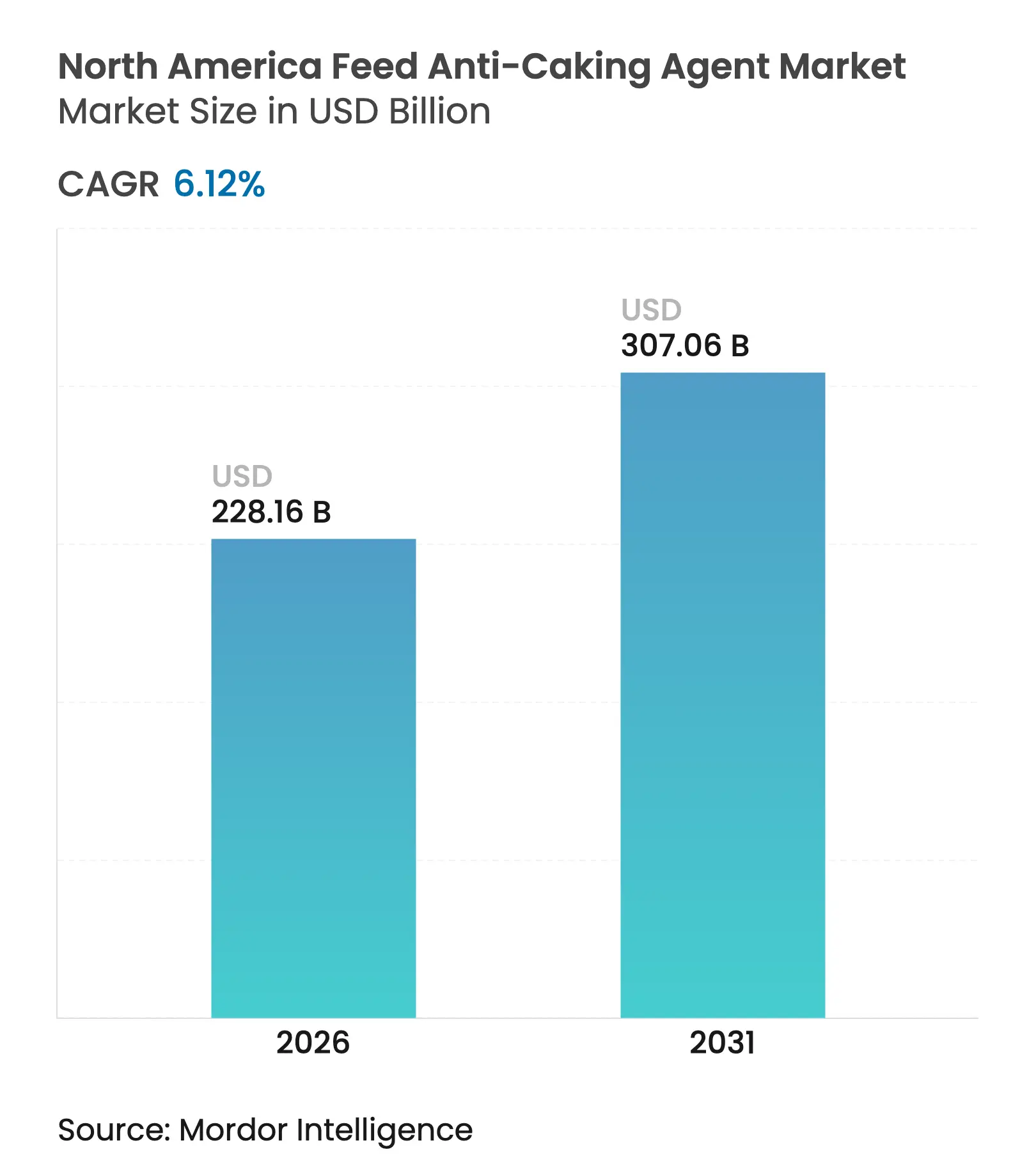

| Market Size (2026) | USD 228.16 Billion |

| Market Size (2031) | USD 307.06 Billion |

| Growth Rate (2026 - 2031) | 6.12 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The North America feed anti-caking agent market size was valued at USD 215 million in 2025 and estimated to grow from USD 228.16 million in 2026 to reach USD 307.06 million by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). The North America feed anti-caking agent market size reflects steady investment in industrial livestock systems, strengthened feed hygiene requirements, and broader deployment of precision dosing platforms. Silicon chemistries maintain the performance benchmark for moisture control in high-throughput mills, while potassium-based alternatives record the fastest unit growth due to their combined flow-conditioning and mold-inhibition capability. Tightening regulatory clarity from the United States Food and Drug Administration (FDA) and the Canadian Food Inspection Agency (CFIA) sustains formulation innovation momentum. Digital-twin adoption across large integrators optimizes additive use, lowers downtime risk, and improves cost visibility, which collectively widens market opportunities for suppliers that bundle mineral anti-caking agents with specialty enzymes and amino acids.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expansion of industrial livestock production Expansion of industrial livestock production | +1.2% | United States, and Mexico (broiler and swine hubs) | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:United States, and Mexico (broiler and swine hubs) | Impact Timeline:Medium term (2-4 years) |

Rising demand for high-quality feed storage and handling Rising demand for high-quality feed storage and handling | +1.0% | United States, and Canada (cold-climate storage stress) | Short term (≤ 2 years) | |||

Emphasis on animal health and feed hygiene Emphasis on animal health and feed hygiene | +0.9% | North America-wide, and export-oriented operations | Long term (≥ 4 years) | |||

Growth in specialty mineral additives Growth in specialty mineral additives | +0.8% | United States, and Canada (premium feed segments) | Medium term (2-4 years) | |||

Cold-chain disruptions increasing moisture fluctuation risk Cold-chain disruptions increasing moisture fluctuation risk | +0.7% | United States (Midwest and Plains states), and Canada | Short term (≤ 2 years) | |||

Digital-twin adoption in feed mills optimizing dosage Digital-twin adoption in feed mills optimizing dosage | +0.6% | United States (large integrators), and early adoption in Canada | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Expansion of Industrial Livestock Production

Broiler output in the United States is set to reach 21.3 million metric tons in 2025, up 2.1% from 2024, while Mexico’s poultry sector added 1.2 million metric tons of new feed capacity in 2024 to serve export markets [1]Source: Economic Research Service, “Livestock, Dairy, and Poultry Outlook February 2025,” United States Department of Agriculture, ers.usda.gov. Higher-capacity mills magnify the cost of unplanned stoppages, so integrators now allocate up to 0.25% of feed cost to anti-caking agents that prevent bridging. Consolidation into fewer mills concentrates throughput risk, driving premium demand across the North America feed anti-caking agent market.

Rising Demand for High-Quality Feed Storage and Handling

In January 2024, winter storms caused 50,000 metric tons of feed caking losses across the United States Midwest, prompting insurers to mandate minimum anti-caking inclusion rates [2]Source: National Weather Service, “Winter Storm Impacts on Agricultural Infrastructure 2024 Assessment,” weather.gov. Calcium-silicate blends with hydrophobic treatment reduce moisture pickup by 30% and are rapidly replacing untreated calcium carbonate in cold-climate mills. Extended rail transit times, which averaged 12 days in 2024, further encourage prophylactic additive use during grain receipt, doubling per-ton consumption and enlarging the North America feed anti-caking agent market.

Emphasis on Animal Health and Feed Hygiene

Salmonella incidence in United States poultry feed declined to 1.8% in 2024, in part due to calcium-propionate fortified anti-caking blends that suppress pathogen growth [3]Source: Center for Veterinary Medicine, “Regulatory Framework for Animal Feed Additives 2024 Guidance,” Food and Drug Administration, fda.gov. Updated the Canadian Food Inspection Agency (CFIA) guidelines classify moisture-induced caking as a critical control point for Hazard Analysis and Critical Control Points certification, favoring precipitated silica that maintains consistent trace-metal profiles. Export-oriented mills adopt synthetic minerals that simplify European Union residue documentation, driving steady volume growth for higher-purity chemistries in the North America feed anti-caking agent market.

Growth in Specialty Mineral Additives

BASF SE introduced a calcium-silicate carrier pre-loaded with chelated trace minerals in 2024, allowing mills to reduce separate premix inventories while securing flowability gains. Evonik Industries reported 11% sales growth for its Sipernat specialty silica line, reflecting the demand shift toward higher-value, engineered minerals. Domestic precipitated silica output reached 420,000 metric tons in 2024, with feed applications now absorbing 8%, up from 6% a year earlier.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatility in mineral raw-material prices Volatility in mineral raw-material prices | -0.6% | United States, and Canada (import-dependent regions) | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.6% | Geographic Relevance:United States, and Canada (import-dependent regions) | Impact Timeline:Short term (≤ 2 years) |

Stringent the United States Food and Drug Administration (FDA) and the Canadian Food Inspection Agency (CFIA) additive regulations Stringent the United States Food and Drug Administration (FDA) and the Canadian Food Inspection Agency (CFIA) additive regulations | -0.5% | United States, and Canada (federal oversight) | Medium term (2-4 years) | |||

Availability of low-cost substitute flow-conditioners Availability of low-cost substitute flow-conditioners | -0.4% | Mexico, and United States (price-sensitive segments) | Short term (≤ 2 years) | |||

Carbon-footprint labeling discouraging inorganic additives Carbon-footprint labeling discouraging inorganic additives | -0.3% | United States (California, Northeast states) | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatility in Mineral Raw-Material Prices

Precipitated silica spot prices fluctuated between USD 620 and USD 780 per metric ton in 2024 because of energy cost swings, while Wyoming bentonite faced rail shortages that elevated prices by 18%. Domestic bentonite output slipped 3% amid permitting delays, and ocean freight for Asian minerals rose 15%, eroding cost advantages for imported calcium carbonate. These price shifts compress feed-mill margins and temper near-term growth in the North America feed anti-caking agent market.

Stringent The United States Food and Drug Administration (FDA) and The Canadian Food Inspection Agency (CFIA) Additive Regulations

Any silicon-based compound not already listed as Generally Recognized as Safe now requires a costly food additive petition, often taking up to 36 months for approval. The Canadian Food Inspection Agency (CFIA) demands bioavailability studies for additives exceeding 2% inclusion, dissuading mills from experimenting with high-dose calcium carbonate in aquaculture feeds. Compliance costs slow adoption of next-generation flow conditioners, moderating the North America feed anti-caking agent market expansion.

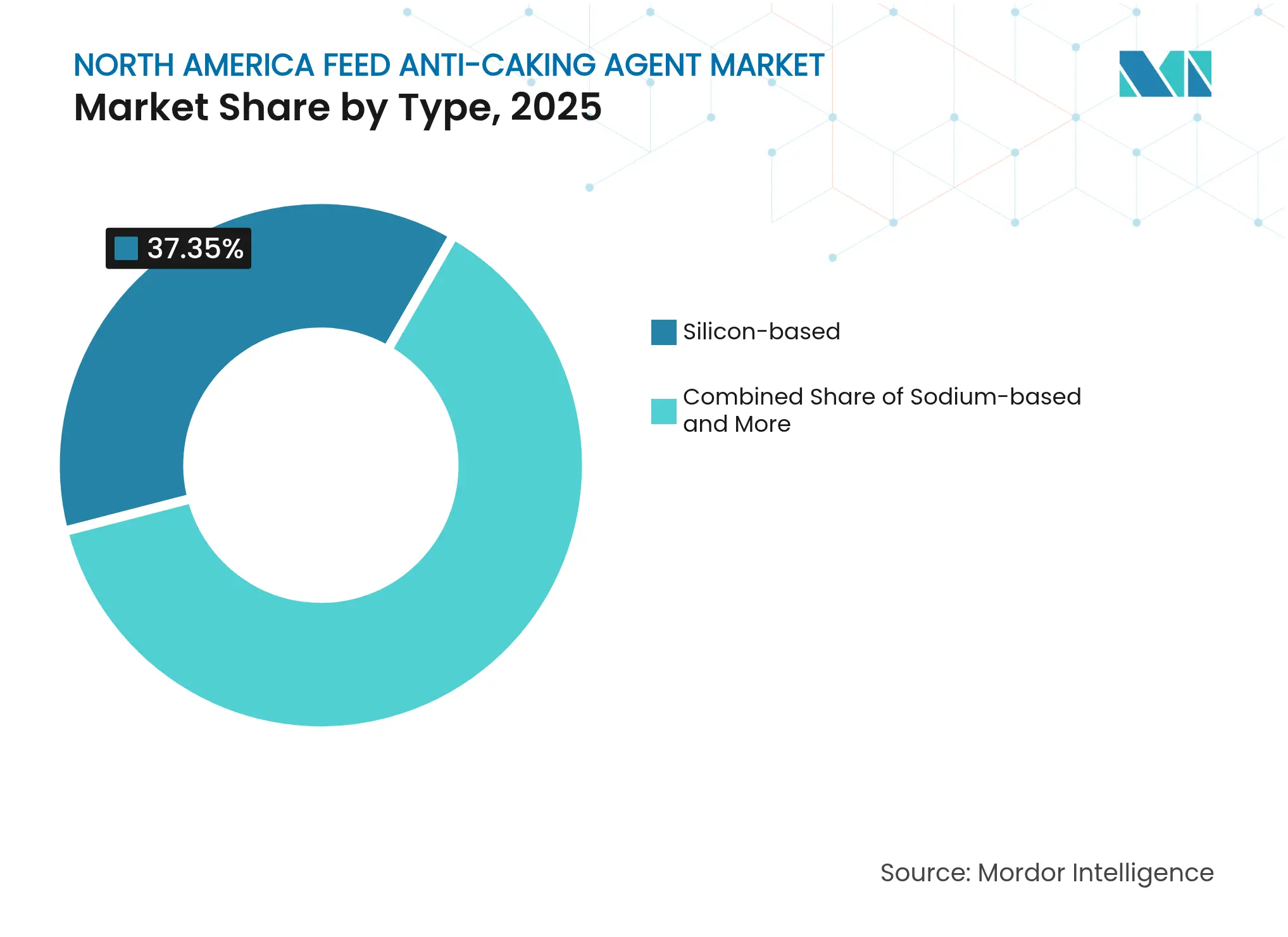

By Type: Silicon Chemistries Anchor Flowability Standards

Silicon-based formulations held a 37.35% share of the North America feed anti-caking agent market in 2025. Precipitated silica dominates high-value poultry mash, where its 3–5 µm particle size improves dispersion and output consistency. Imerys launched hydrophobic calcium silicate in 2024 that maintains efficacy at 80% relative humidity, attracting Gulf Coast mills exposed to moisture spikes. Potassium formate blends are forecast to grow at 8.26% CAGR, favored by organic producers needing antimicrobial support. Sodium aluminosilicate remains a niche choice in aquaculture diets because of its ammonia-binding properties. Calcium carbonate provides basic flow-conditioning for cost-sensitive ruminant feeds but loses performance when moisture rises above 13%.

The silicon chemistries are projected to reach a significant market, as mills prioritize higher adsorption capacity for fine-grind formulations. Calcium variants will track overall growth but cede share to engineered minerals. Potassium introductions broaden the portfolio, especially where mold control intersects with flowability, reinforcing premium tiers within the North America feed anti-caking agent market.

Note: Segment shares of all individual segments available upon report purchase

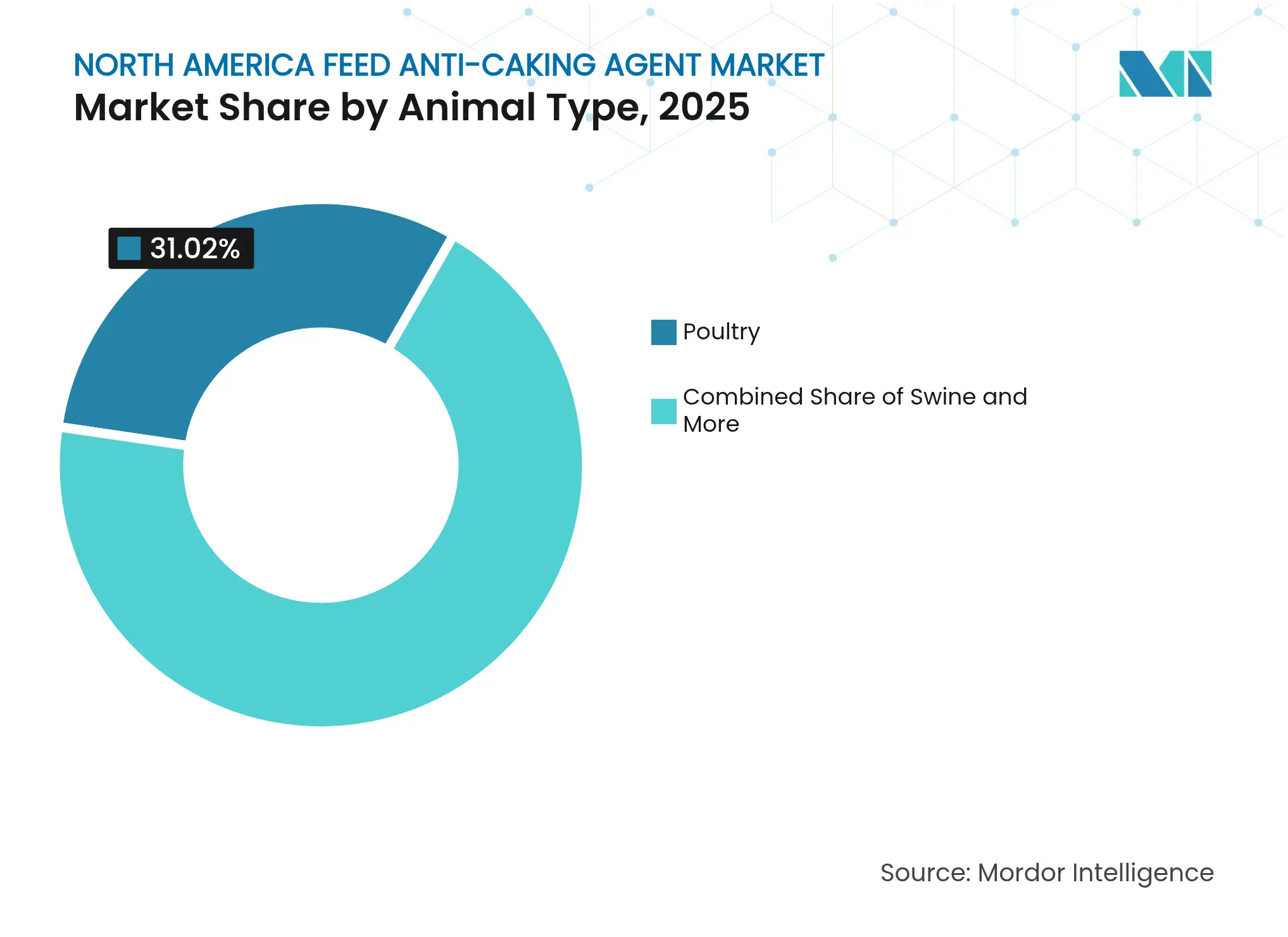

By Animal Type: Poultry Intensity Meets Aquaculture Velocity

Poultry commanded 31.02% of the North America feed anti-caking agent market in 2025, backed by crumble and pellet diets that demand reliable flow through automated systems. Anti-caking inclusions reach 0.30% in humid Southeastern states to prevent bridging and fines accumulation. The North America feed anti-caking agent market size for poultry is projected to grow in tandem with the United States Department of Agriculture's estimate of 21.3 million metric tons of broiler output in 2025.

Aquaculture is growing at a 7.58% CAGR as shrimp and salmon farms transition to commercial micro-pellets that are susceptible to moisture pickup. Sodium aluminosilicate and potassium-based agents extend water stability by more than six minutes, safeguarding feed conversion efficiency. Swine and ruminants adopt calcium carbonate and bentonite for cost reasons, while equine and pet food producers specify premium precipitated silica for dust control in retail packaging. The North America feed anti-caking agent market share within aquaculture is poised to expand, reflecting the sector’s pivot from farm-made rations to industrial extrusion lines.

Note: Segment shares of all individual segments available upon report purchase

The United States represented 61.35% of the Feed Anti-Caking Agent market demand in 2025. Vertically integrated operations in Georgia, Arkansas, and Alabama consumed roughly 2 kg of anti-caking agents per ton of feed, underscoring the importance of feed flowability to large-scale broiler production. Domestic silica suppliers such as J.M. Huber Corporation leverage proximity to grain belts to deliver 48-hour lead times and support just-in-time inventory models. California mills pay 15–20% premiums for carbon-neutral formulations to meet state sustainability mandates, reinforcing a niche premium segment within the North America feed anti-caking agent market.

Canada accounted for a significant share of demand, concentrated in Ontario and Quebec, where cold-season storage drives reliance on hydrophobic calcium silicate. The Canadian Food Inspection Agency (CFIA) revised pre-market assessments to lengthen approval cycles for novel potassium and specialty silica products, tempering the rapid shift toward engineered chemistries. Poultry expansion at 1.8% annually through 2030 still supports incremental growth, with outsized seasonal demand during winter when condensation risk peaks.

Mexico delivered the fastest growth, recording a 6.95% CAGR outlook through 2031. New mills in Jalisco and Veracruz specify silicon-based agents to comply with export certifications, yet overall price sensitivity keeps rice hull ash and zeolite blends in widespread use. Cross-border trade increases transit time, elevating performance requirements and driving gradual migration toward higher-purity minerals. Smaller Central American and Caribbean markets add marginal volume but offer targeted opportunities for distributors with flexible logistics.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

The top five suppliers controlled a significant share of the North America feed anti-caking agent market in 2024. BASF SE’s USD 260 million acquisition of Yara’s animal nutrition unit created a platform that integrates anti-caking agents with enzymes and amino acids, capturing more value per ton of feed. Evonik Industries AG’s USD 150 million purchase of Vetagro added flow conditioners tailored for high-fat poultry diets, enabling bundled offerings validated by digital-twin throughput simulations. Clariant AG and Bühler AG’s technology partnership embeds precipitated silica dosing algorithms within feed-mill automation, differentiating premium minerals through data-driven performance assurance.

Regional quarry operators maintain a share in calcium carbonate and bentonite through 15–20% price discounts, although tightening environmental disclosure rules pressure customers to assess the embedded emissions of mined versus synthetic options. Rice hull ash and algae-derived silica hold less than 2% penetration because of inconsistent particle-size distribution and premium pricing, but attract interest from carbon-conscious buyers in the western United States. Patent filings for hydrophobic-treated silicas and potassium formate enhancements rose 18% in 2024, confirming sustained research even within a mature North America feed anti-caking agent market.

Service capabilities now matter as much as mineral quality. Suppliers deploy field engineers to calibrate dosage based on real-time humidity and feed formulation data, locking in contracts through performance guarantees rather than spot pricing. J.M. Huber Corporation’s ISO 22000 certification strengthens export credentials, while Solvay’s renewable natural gas commitment aligns production with Scope 3 targets set by large integrators. Competitive intensity is therefore shaped not only by cost but also by regulatory compliance, sustainability metrics, and digital integration.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

Anti-caking agents are additives used in the feed industry to prevent lump formation. These agents inhibit naturally occurring fungal metabolites and enhance feed quality. They effectively address issues such as moisture adsorption, nitrogen loss, and caking in granulation caused by mold growth. Additionally, feed anti-caking agents improve packaging systems, simplifying transportation. The North America Anti-Caking Agent Market is segmented by Type (Silicon-based, Sodium-based, Calcium-based, Potassium-based, and Other Chemical Types), Animal Type (Ruminant, Poultry, Swine, Aquaculture, and Other Animal Types), and Geography (United States, Canada, Mexico, and Rest of North America). The report provides market size and forecasts in terms of value (USD) for these segments.

Deep-Dive Analysis of Feed Probiotics Across Key Regions

5 Min Read

Mapping Real Estate Opportunities in Bali

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.