Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

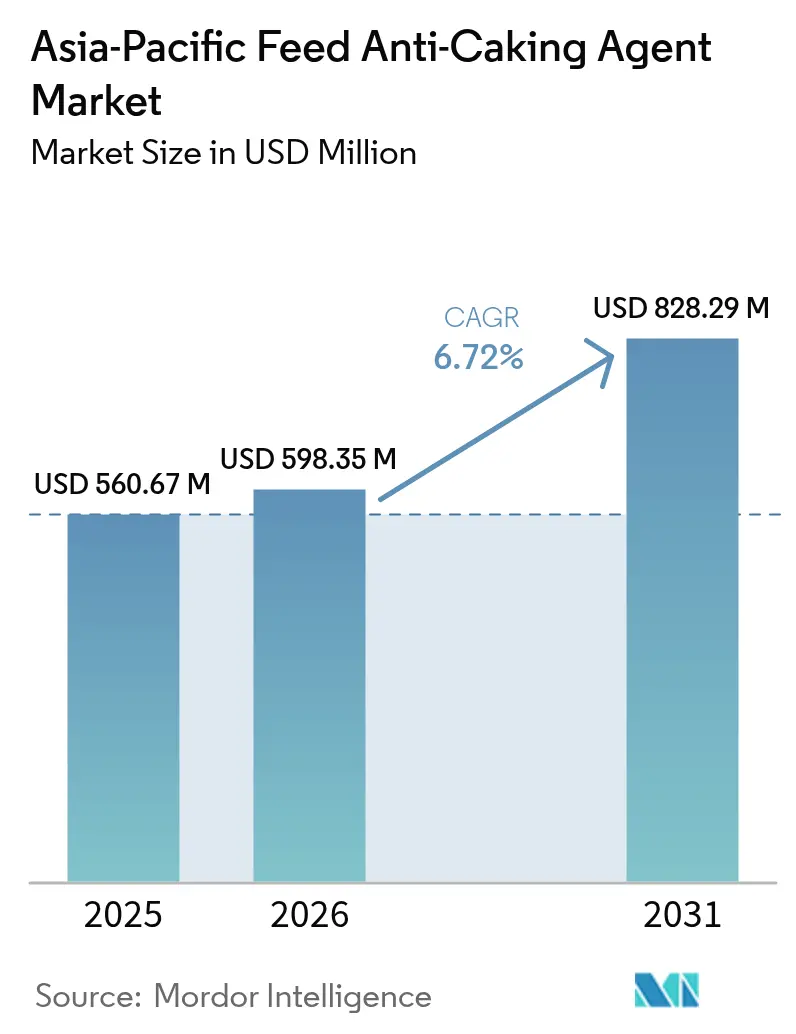

| Base Year Market Size (2025) | USD 560.67 Million |

| Market Size (2026) | USD 598.35 Million |

| Market Size (2031) | USD 828.29 Million |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

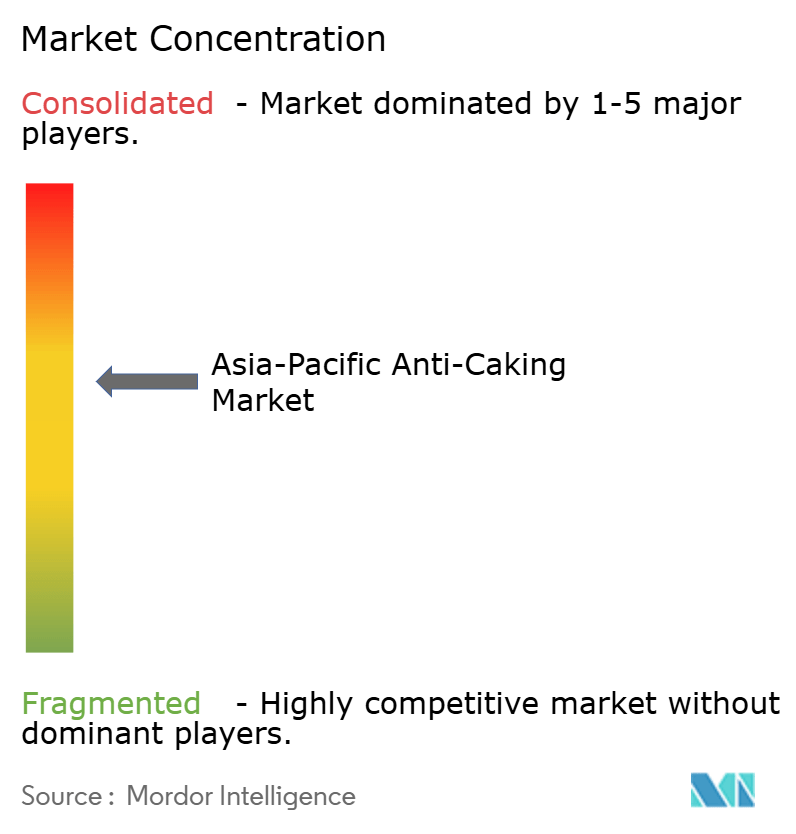

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Feed Anti-Caking Agent Market Analysis by Mordor Intelligence

Asia-Pacific feed anti-caking agent market size in 2026 is estimated at USD 598.35 million, growing from 2025 value of USD 560.67 million with 2031 projections showing USD 828.29 million, growing at 6.72% CAGR over 2026-2031. Growth is supported by large-scale livestock expansion, regulatory tightening on feed safety, and rapid adoption of industrial batching systems that cannot tolerate flow interruptions. Sodium-based products still anchor bulk formulations, yet potassium variants are gaining share as premix manufacturers shift to micro-dosing platforms. Monsoon-related humidity spikes continue to elevate demand for moisture-binding chemistries, while insect protein inclusion has created fresh free-flow challenges. Competitive differentiation is tilting toward suppliers offering traceable, low-arsenic sources and technical support that demonstrably reduce production downtime. Despite modest substitution risk from natural alternatives, synthetics remain indispensable for high-throughput mills, keeping the Asia-Pacific feed anti-caking market on a steady expansion path.

Key Report Takeaways

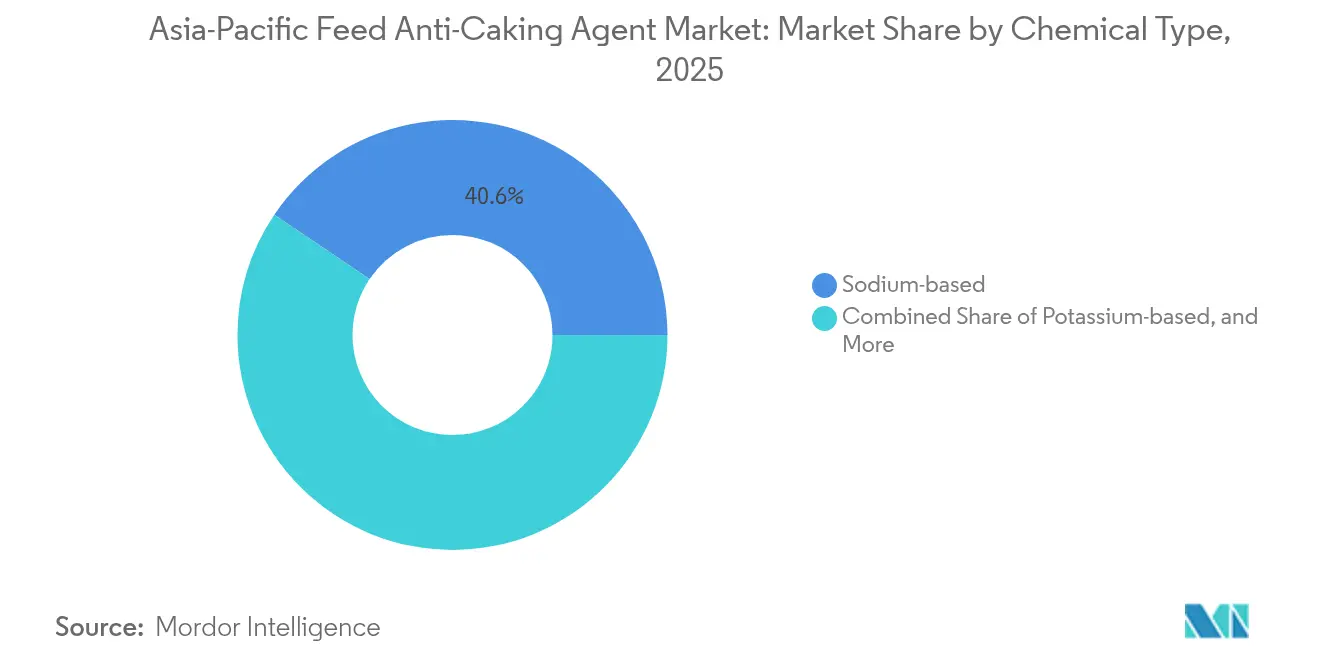

- By chemical type, sodium-based agents led with 40.55% of the Asia-Pacific feed anti-caking market share in 2025, while potassium-based variants are forecast to expand at a 9.03% CAGR to 2031.

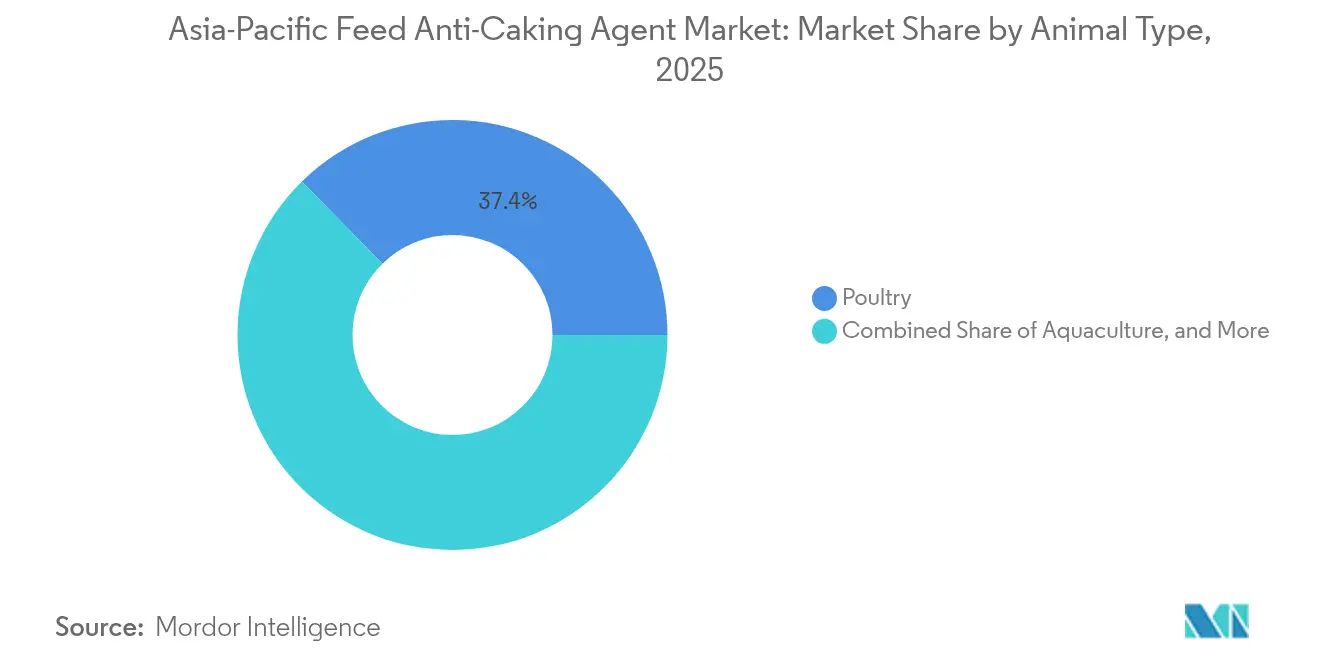

- By animal type, poultry accounted for 37.35% of the Asia-Pacific feed anti-caking market size in 2025, while aquaculture is projected to advance at an 8.52% CAGR through 2031.

- By geography, China contributed 56.40% of revenue in 2025, while India recorded the fastest growth at 9.18% per year to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Feed Anti-Caking Agent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for livestock protein | +1.8% | China, India, and Southeast Asia | Medium term (2-4 years) |

| Expansion of industrial feed mills | +1.5% | India, Vietnam, and Indonesia | Medium term (2-4 years) |

| Mandatory feed safety regulations | +1.2% | China, Japan, and Australia | Long term (≥4 years) |

| Surge in insect-protein inclusion raising free-flow challenges | +0.9% | Thailand, China, and Australia | Short term (≤2 years) |

| Climate-driven rise in feed moisture during monsoons | +0.7% | India, Bangladesh, Myanmar, and Indonesia | Short term (≤2 years) |

| Shift to precision micro-dosing in premixes requiring flow aids | +0.6% | China, Japan, and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Livestock Protein

Per-capita meat intake across the region is converging toward 50 kg per year, a threshold that historically catalyzes feed-mill automation and standardized premix use. China’s 2024 compound feed output surpassed 220 million metric tons, necessitating reliable anti-caking agents to keep tall silos flowing smoothly. India’s layer segment added 12% new capacity in 2024, each complex requiring flow aids to stabilize hygroscopic mineral blends [1]Source: Department of Animal Husbandry and Dairying, “Annual Report 2024-25,” DAHD.NIC.IN. Aquafeed in Vietnam and Thailand is absorbing additives twice as fast as ruminant rations because pellet durability is critical once submerged. As integrators discover that a 0.1% dosage uptick can trim feed waste by 3-4% in automated systems, anti-caking adoption tightens in lockstep with rising protein demand.

Expansion of Industrial Feed Mills

More than USD 2 billion in greenfield feed-mill investments closed during 2024 across India, Indonesia, and the Philippines. Plants rated above 30 metric tons/hectare employ continuous mixers where any bridging halts lines and triggers contract penalties. Cargill now issues regional anti-caking tenders instead of site-level buys, a move that concentrates volume and sharpens price competition [2]Source: Cargill, “Annual Report 2024,” CARGILL.COM. Even smaller rural mills are adopting flow aids to comply with ISO 22000 certification tied to government subsidies. The Asia-Pacific feed anti-caking market therefore benefits directly from every ton of new automated capacity that comes online.

Mandatory Feed Safety Regulations

China began requiring heavy-metal certificates for each silicate shipment in 2024, while Japan cut the arsenic ceiling for silicon dioxide to 2 ppm. Australia mandates mine-to-mill traceability, favoring multinational suppliers with audited supply chains. Compliance raises marginal costs yet locks in higher-grade additives as the only viable option. Small traders lacking documentation are forced out, leading mills to sign multi-year contracts with proven vendors. The Asia-Pacific feed anti-caking market consequently deepens even as regulatory hurdles climb.

Surge in Insect-Protein Inclusion Raising Free-Flow Challenges

Black soldier fly and cricket meals carry 15-20% higher water activity than soy, promoting bridging at relative humidity. Thailand’s CP Foods doubled sodium aluminosilicate dosing in shrimp diets after rolling out insect protein, offset by better pellet durability in export lanes. As approvals for novel proteins spread, formulators pivot toward potassium or calcium chemistries that absorb moisture without hampering amino-acid bioavailability. This trend keeps specialty products in tight demand cycles across the Asia-Pacific feed anti-caking market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of specialized additives | -0.9% | India, Bangladesh, and Myanmar | Short term (≤2 years) |

| Availability of natural alternatives | -0.6% | Australia, New Zealand, and Japan | Medium term (2-4 years) |

| Growing zero-additive labeling in premium feed | -0.5% | Japan, South Korea, and urban China | Long term (≥4 years) |

| Stringent heavy-metal limits on silicate products | -0.4% | Japan, Australia, and Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Specialized Additives

Potassium and calcium variants cost 25-40% more than sodium aluminosilicate, squeezing mills where raw materials already consume 75% of budgets. In India, half of compound feed comes from small mills that substitute cheaper natural clays outside monsoon months. Deferred upgrades keep sodium products dominant in price-sensitive tiers, damping the Asia-Pacific feed anti-caking market’s premium mix until working-capital constraints ease.

Availability of Natural Alternatives

Organic producers in Australia, New Zealand, and Japan utilize rice hulls and cellulose fibers to replace synthetic materials, resulting in a 10-15% reduction in additive spend. Efficacy drops sharply above 10 metric tons/hectare throughput, confining uptake to niche channels worth 2.3% of Japan’s 2024 feed volume [3]Source: Ministry of Agriculture, Forestry and Fisheries, “Organic Livestock Sector Statistics 2024,” MAFF.GO.JP. Even so, consumer preference for clean labels could shave 2-3 percentage points of conventional volume by 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: Potassium Variants Gain Precision Premix Share

Sodium-based agents led with 40.55% of the Asia-Pacific feed anti-caking market share in 2025, while potassium-based variants are forecast to expand at a 9.03% CAGR to 2031, raising their Asia-Pacific feed anti-caking market share in premium premix channels. Bulk feed mills still favor sodium aluminosilicate for its proven efficacy at inclusion rates below 0.3%, but regulatory scrutiny over arsenic and the need to protect tight dosing tolerances are tilting new investment toward potassium and calcium alternatives. Silicon-based flow aids will retain relevance where throughput exceeds 30 metric tons/hectare, yet suppliers are increasingly documenting low-metal content to maintain access to Japan and Australia. Other chemistries, such as magnesium stearate, serve niche markets in aquaculture where pellet buoyancy is crucial.

Innovation momentum sits firmly with potassium. Evonik demonstrated that its sorbate-based powder reduced hopper bridging incidents by 30% in high-speed lines, convincing Japanese and South Korean premix plants to standardize on the chemistry. This carve-out signals diverging product portfolios, cost-driven commodity feed remains sodium territory, while precision-driven premix and specialty aquafeed migrate to potassium or calcium blends. Suppliers able to span both ends of this spectrum will capture the broadest slice of the Asia-Pacific feed anti-caking market.

By Animal Type: Aquaculture Drives Flow-Aid Innovation

Poultry feed consumed 37.35% of the Asia-Pacific anti-caking market in 2025, due to the sector’s large installed capacity and pellet reliance. Yet, aquaculture feed outpaces all others at an 8.52% CAGR, driven by the expansion of shrimp and tilapia production across Thailand, Vietnam, and Indonesia. Water-stability demands mean that each pellet must resist disintegration for at least 30 minutes after immersion. CP Foods’ proprietary blend cuts disintegration by 15%, improving feed conversion and margins. Swine rations in China recovered after ASF, adding volume but with lower dosage intensity compared to poultry.

Ruminant feed remains slower due to pasture systems. TMR adoption in India’s dairies is inching higher, creating new pockets of demand. Pet food and equine rations remain a minor volume but command premium prices due to stringent palatability standards. Overall, aquaculture’s technical requirements continue to drive R&D budgets toward moisture-blocking chemistries, ensuring that this animal segment remains at the cutting edge of the Asia-Pacific feed anti-caking market.

Geography Analysis

China accounted for 56.40% of the Asia-Pacific feed anti-caking market revenue in 2025, underpinned by 220 million tons of compound feed output and state-backed mill consolidation. The top 50 producers now command 65% of national volume, leveraging procurement scale to sign multi-year additive contracts. Heavy-metal testing rules introduced in 2024 erected high compliance barriers that exclude unregistered traders, locking in a share for multinationals capable of mine-level traceability. While absolute demand continues to rise, China’s growth moderates slightly below the regional average as installed capacity saturates.

India is the velocity leader at 9.18% annual growth, fueled by 8 million metric tons of new mill capacity in 2024 and government programs encouraging ISO 22000-certified plants. Monsoon humidity makes anti-caking a non-negotiable requirement, yet price sensitivity splits the market, large integrators opt for premium potassium or calcium products, whereas small mills remain loyal to sodium aluminosilicate. Pending feed additive standards from FSSAI will likely accelerate migration toward certified chemistries from 2026 onward.

Japan and Australia, though smaller in tonnage, wield outsized influence through stringent metal limits and consumer pull for clean labels. By late 2024, twenty-five percent of Japanese premix makers had reformulated their products to include calcium or potassium. Australia’s organic segment embraces natural flow aids despite doubling dosage rates. Collectively, these shifts diversify revenue away from China, reshaping supplier go-to-market playbooks across the Asia-Pacific feed anti-caking market.

Competitive Landscape

The Asia-Pacific feed anti-caking market is moderately concentrated. BASF SE, Kemin Industries, Inc., Alltech Inc., Archer Daniels Midland Company, and Nutreco N.V. (SHV Holdings N.V.) together lead the market, giving them negotiating leverage with large integrators. These multinationals own or control deposits, synthesis plants, and premix facilities, letting them lock in volumes through bundled supply contracts that smaller traders cannot match. Regional mineral processors still compete on landed cost for bulk sodium aluminosilicate, but their share is eroding where compliance audits demand mine-level traceability. The top players, therefore, balance scale economies with documentation strength to defend margins as regulatory scrutiny rises across Japan, Australia, and China.

Strategic moves in 2024-2025 underscore a shift from commodity trading to value-added services. Cargill, Incorporated invested in Ho Chi Minh City to add micro-dosing lines that handle potassium flow aids for shrimp and tilapia feed. BASF SE launched a calcium-based product for organic poultry rations, priced at a 15% premium but compliant with Japan’s 2 ppm arsenic ceiling. Evonik secured ISO 22000 certification for its Shanghai line and filed patents on potassium formulations that cut hopper bridging by 30% in gravimetric systems. Archer Daniels Midland reported Asia-Pacific animal-nutrition revenue up 14% year over year, attributing 8% of that to bundled anti-caking sales into India’s poultry sector. Kemin is locked in a Rajasthan joint venture to guarantee low-arsenic bentonite feedstock, safeguarding access to the strict Japanese and Australian markets.

A tier of emerging challengers is upgrading quality control to chip away at the leaders’ commodity share. Imerys spent USD 18 million to retrofit its Gujarat kaolin plant, enabling calcium silicate supplies at <1 ppm arsenic for export into Japan and Australia. Shandong Longchang and other Chinese clay processors are certifying to ISO 22000, allowing them to under-price multinationals in sodium silicate tenders without sacrificing compliance. Natural-alternative specialists in Australia and New Zealand are cultivating organic channels with rice-hull and cellulose blends, but their efficacy limits volume to sub-niche segments. As feed mills embed uptime metrics in supplier scorecards, technical service on-site dosing audits, metal testing, and line calibration has become the decisive differentiator. Companies that prove tangible throughput gains and maintain transparent sourcing are projected to consolidate further share through 2030, even as regional price competition persists.

Asia-Pacific Feed Anti-Caking Agent Industry Leaders

BASF SE

Kemin Industries, Inc.

Alltech Inc.

Archer Daniels Midland Company

Nutreco N.V. (SHV Holdings N.V.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Aker BioMarine established Aker BioMarine (Shanghai) Co., Ltd. in China to expand its animal feed division. This expansion strengthens the company's position in China's animal nutrition market. The establishment addresses the increasing demand for high-quality animal feed including feed anti-caking agents in China while supporting Aker BioMarine's growth plans across Asia.

- April 2024: Cargill has revealed expansion of its premix manufacturing facility in Ho Chi Minh City, Vietnam, adding capacity for specialized anti-caking formulations tailored to aquaculture feed applications. The investment includes the installation of micro-dosing equipment designed to handle potassium-based flow aids, positioning the facility to serve the growing shrimp and tilapia feed sectors across Southeast Asia.

- October 2023: De Heus India expanded its operations by opening an advanced animal feed plant at Vividha Industrial Park in Rajpura, Punjab. With an annual capacity of 180,000 metric tons, the company has planned to introduce innovative feed solutions for dairy, poultry, and fish farming, aiming to improve livestock productivity.

Asia-Pacific Feed Anti-Caking Agent Market Report Scope

Anti-caking agents are mainly used to ensure that there are no lumps in the feed while providing better and optimal packaging, to make transportation simpler. Asia Pacific Feed Anti-caking Agent Market is segmented By Chemical Type (Silicon-based, Sodium-based, Calcium-based, Potassium-based, and Other Chemical Types), By Animal Type (Ruminants, Poultry, Swine, Aquaculture, Pets, and Other Animal Types) by Geography (China, India, Japan. Australia and the Rest of Asia-Pacific). The report offers the market sizes and forecasts in value (USD) for all the above segments.

By Chemical Type

| Silicon-based |

| Sodium-based |

| Calcium-based |

| Potassium-based |

| Other Chemical Types |

By Animal Type

| Ruminants |

| Poultry |

| Swine |

| Aquaculture |

| Other Animal Types |

By Geography

| China |

| India |

| Japan |

| Australia |

| Rest of Asia-Pacific |

| By Chemical Type | Silicon-based |

| Sodium-based | |

| Calcium-based | |

| Potassium-based | |

| Other Chemical Types | |

| By Animal Type | Ruminants |

| Poultry | |

| Swine | |

| Aquaculture | |

| Other Animal Types | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific feed anti-caking market in 2026?

The Asia-Pacific feed anti-caking market size is USD 598.35 million in 2026.

What is the expected growth rate through 2031?

The market is forecast to post a 6.72% CAGR, reaching USD 828.29 million by 2031.

Which chemical type is growing fastest?

Potassium-based agents lead with a 9.03% projected CAGR because they fit precision micro-dosing systems.

Why is aquaculture important for flow-aid demand?

Shrimp and tilapia pellets must resist water disintegration. This drives an 8.52% CAGR for anti-caking use in aquafeed.

Which country offers the highest growth potential?

India is expanding at 9.18% annually on the back of new automated feed-mill capacity and humid monsoon logistics.

How strict are heavy-metal regulations in the region?

Japan enforces a 2 ppm arsenic limit on silicate additives, compelling suppliers to secure low-contaminant sources and upgrade testing protocols.

Page last updated on: