Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The North America Surveillance Analog Camera Market is Segmented by End-User Industry (Government, Banking, Healthcare, Transportation and Logistics, Industrial, and More), Camera Type (Bullet Cameras, Dome Cameras, and More), Technology (Thermal/Infrared Analog Cameras, and More), Resolution (<2 Megapixel, 2–5 Megapixel, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

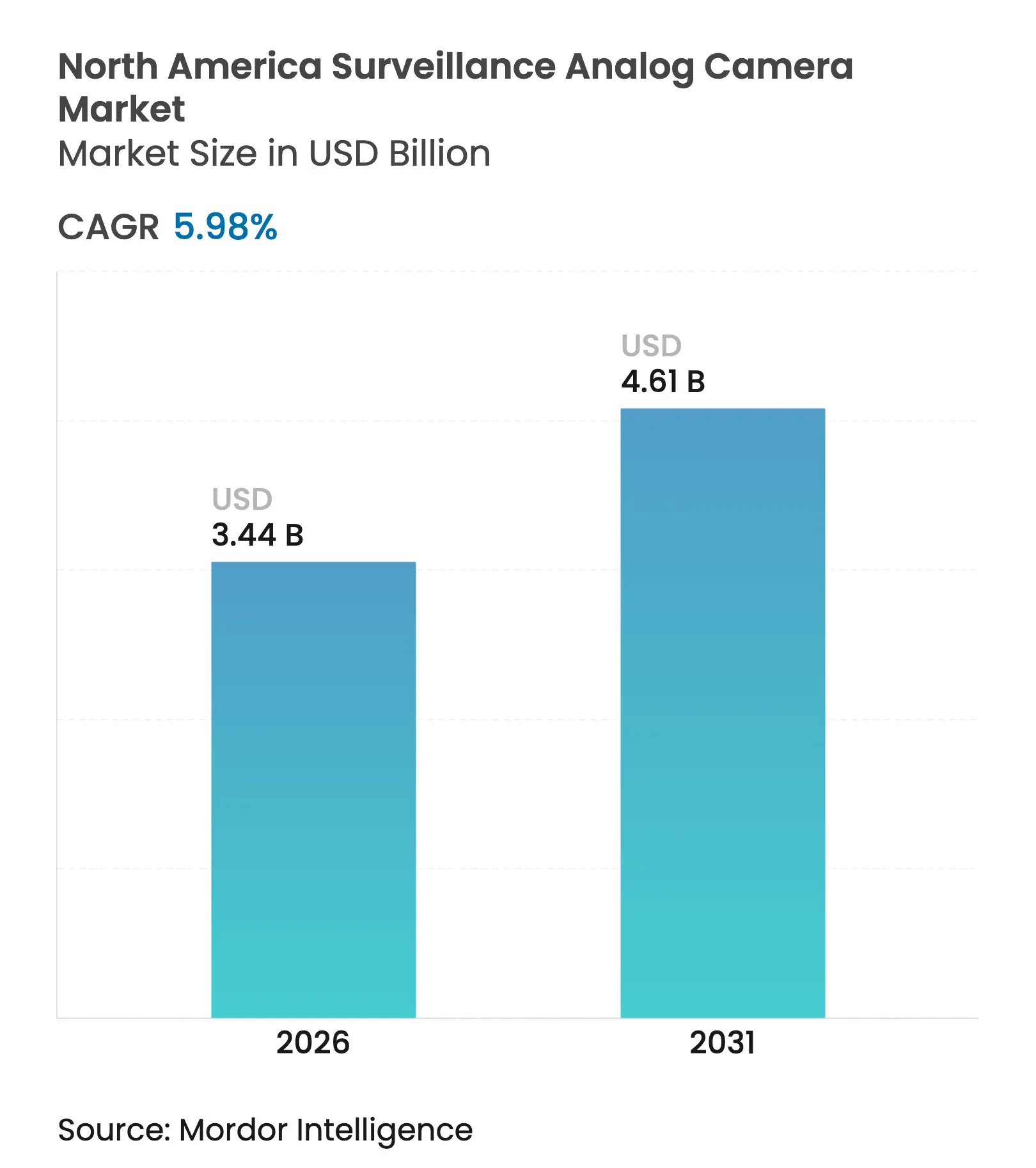

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 4.61 Billion |

| Growth Rate (2026 - 2031) | 5.98 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The North America surveillance analog camera market size was valued at USD 3.25 billion in 2025 and estimated to grow from USD 3.44 billion in 2026 to reach USD 4.61 billion by 2031, at a CAGR of 5.98% during the forecast period (2026-2031). Retrofit programs that reuse coaxial cabling, mandates for vehicle-mounted video, and the rapid shift to HD-analog formats sustain demand even as IP cameras proliferate. Vendors are focusing on cost-efficient resolution upgrades, hybrid DVR platforms, and AI-ready chipsets to keep analog competitive. End-user spending concentrates in government, education, transportation, and cannabis retail, where compliance deadlines and infrastructure constraints favor analog over bandwidth-intensive IP alternatives. Competitive dynamics are in flux as NDAA restrictions curb Chinese dominance and open space for North American, Korean, and Taiwanese suppliers.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing retrofit demand leveraging legacy coaxial cabling in U.S. SME segment Growing retrofit demand leveraging legacy coaxial cabling in U.S. SME segment | +2.1% | United States (SME) | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:United States (SME) | Impact Timeline:Medium term (2-4 years) |

Accelerated HD-analog upgrade cycle across K-12 school districts Accelerated HD-analog upgrade cycle across K-12 school districts | +1.8% | United States (public education) | Short term (≤ 2 years) | |||

State-level mandates for onboard analog video in public transit & school buses State-level mandates for onboard analog video in public transit & school buses | +1.4% | United States, Canada (urban centers) | Medium term (2-4 years) | |||

Expansion of cannabis retail outlets driving low-cost surveillance roll-outs Expansion of cannabis retail outlets driving low-cost surveillance roll-outs | +0.9% | United States, Canada (legal states/provinces) | Short term (≤ 2 years) | |||

Rural municipal projects preferring analog due to limited broadband capacity Rural municipal projects preferring analog due to limited broadband capacity | +0.7% | United States, Canada (rural counties) | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Retrofit Demand Leveraging Legacy Coaxial Cabling in U.S. SME Segment

Small and medium enterprises are replacing dated cameras with HD-over-coax models that deliver up to 400% resolution improvement while retaining existing cabling, cutting installation budgets by 40–60%. Interest is strongest in retail, commercial real estate, and light industrial sites where coax remains serviceable, yet image quality has become inadequate. Power-over-Coax accelerates uptake by eliminating separate power runs, further lowering labor costs.[1]SC&T, “IP vs. Analog Camera System Comparison,” sct.com.tw

Accelerated HD-analog Upgrade Cycle Across K-12 School Districts

Districts are drawing from Smart Schools funds to shift from standard-definition to HD-analog cameras that integrate with legacy DVRs. Hybrid recorders accepting mixed signals allow phased upgrades aligned with annual budgets. Enhanced analytics-facial recognition and object detection-now embedded in HD-analog platforms improve threat response without overloading limited IT resources.[2]Argyle Central School District, “Smart Schools Investment Plan,” nysed.gov

State-Level Mandates for Onboard Analog Video in Public Transit & School Buses

Federal and provincial rules require perimeter-visibility systems on new school buses by 2027, stimulating predictable multi-year procurement cycles. Analog solutions prevail because they tolerate vibration, simplify wiring, and store footage locally for extended periods. A leading supplier has installed 200,000 devices, representing 25% share of the school-bus segment.

Expansion of Cannabis Retail Outlets Driving Low-Cost Surveillance Roll-Outs

States stipulate camera coverage, minimum resolutions, and 45- to 90-day retention. Dispensaries favor analog because compliance hinges on camera count more than advanced networking, and financing remains constrained by federal banking rules. Washington’s 640 × 470-pixel floor and 10 fps recording are easily met with HD-analog packages that keep capex low.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Aggressive price erosion from Chinese OEM/ODM dumping practices Aggressive price erosion from Chinese OEM/ODM dumping practices | -1.2% | North America (entry-level segments) | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.2% | Geographic Relevance:North America (entry-level segments) | Impact Timeline:Short term (≤ 2 years) |

Shrinking global CCD/CMOS supply for analog chipsets Shrinking global CCD/CMOS supply for analog chipsets | -0.8% | Global (impacting North America) | Medium term (2-4 years) | |||

Building-code revisions favoring PoE-IP migration in new constructions Building-code revisions favoring PoE-IP migration in new constructions | -0.6% | United States, Canada (new builds) | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Aggressive Price Erosion from Chinese OEM/ODM Dumping Practices

Entry-level margins have compressed 15-25% since 2023 as Chinese brands undercut domestic producers. NDAA-driven bans in federal and critical-infrastructure bids limit their reach, yet price-sensitive commercial buyers continue to source low-cost imports. North American vendors struggle to match USD 500-4,000 price gaps without offshoring, forcing portfolio rationalization and higher-value after-sales services.[3]Federal Register, “Preventing Access to U.S. Sensitive Personal Data and Government-Related Data,” federalregister.gov

Shrinking Global CCD/CMOS Supply for Analog Chipsets

Foundries prioritize digital sensors for phones and cars, squeezing allocations for analog image processors. Component lead times have lengthened, inflating costs and risking production gaps. U.S. policy papers flag overreliance on Asia for CIS fabrication, urging reshoring incentives that could rebalance supply but will take years to materialize.

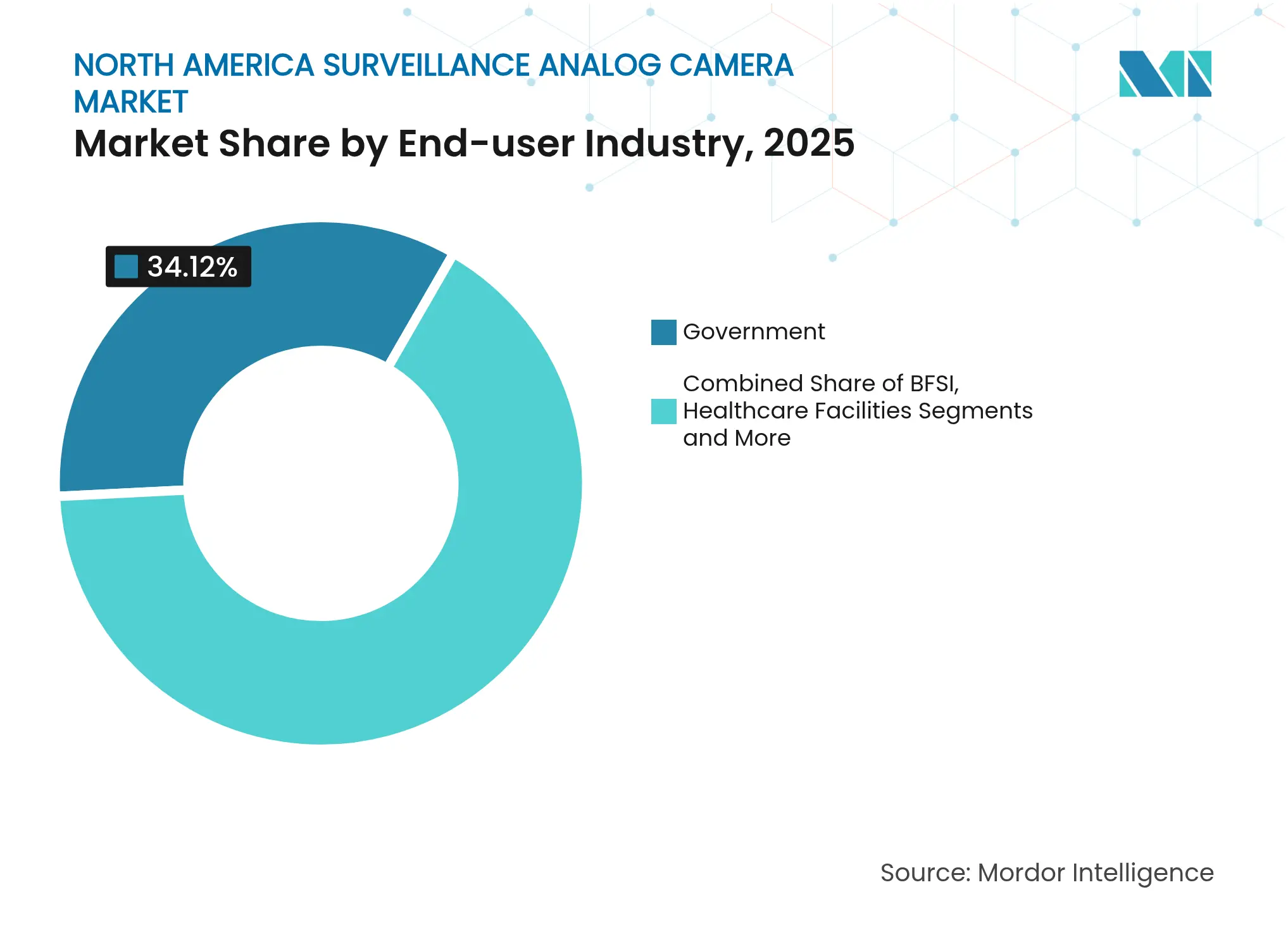

By End-user Industry: Government Sector Anchors Market Stability

Government entities accounted for 34.12% of the North America surveillance analog camera market in 2025, underpinned by vast legacy coax networks that remain serviceable and NDAA-compliant supplier preferences. Budget cycles prioritize phased HD-analog upgrades in courthouses, prisons, and municipal facilities, preserving infrastructure while elevating image clarity. Cannabis retail, though representing a smaller slice of the North America surveillance analog camera market size, is expanding briskly at a 7.32% CAGR on the back of legalization and strict regulatory oversight that prescribes continuous video coverage and long retention.

Transportation agencies mandate ruggedized analog gear for school buses and transit fleets, swelling unit shipments each budget year. Healthcare providers keep analog in restricted wards where closed-circuit isolation mitigates cyber risk. Banks maintain hardwired ATM surveillance lines to deter skimming and provide tamper-proof evidence archives. Industrial operators rely on analog systems that withstand dust, vibration, and extreme temperatures, consistent with Department of Homeland Security guidance on technology selection. Retailers adopt hybrid topologies mixing existing coax in aisles with IP cameras at cash wraps, smoothing budget impact while improving loss-prevention analytics.

Note: Segment shares of all individual segments available upon report purchase

By Camera Type: Bullet Cameras Dominate Outdoor Applications

Bullet designs led with a 37.68% share of the North America surveillance analog camera market size in 2025 and are projected to clock a 10.34% CAGR. Their IP66 housings, extended IR ranges, and adjustable zooms make them the default for perimeter fences and parking lots. Dome variants rank second, prized for vandal resistance and discreet appearance in retail aisles and classrooms. PTZ platforms address wide-area coverage where operators need remote direction control and 30× optical zoom, with the latest releases offering full 360° sweep plus automated tracking. Box formats endure in niche roles requiring custom lenses, while board and covert units cater to ATMs and undercover investigations.

Feature migration is rapid: budget-tier bullets now ship with integrated mics, 130 dB WDR, and color-at-night F1.0 optics, closing historical performance gaps with IP rivals securityworldmarket.com. Vendors bundle analytics-tripwire, line-cross, and loitering-directly on the camera, reducing DVR load and future-proofing legacy installations.

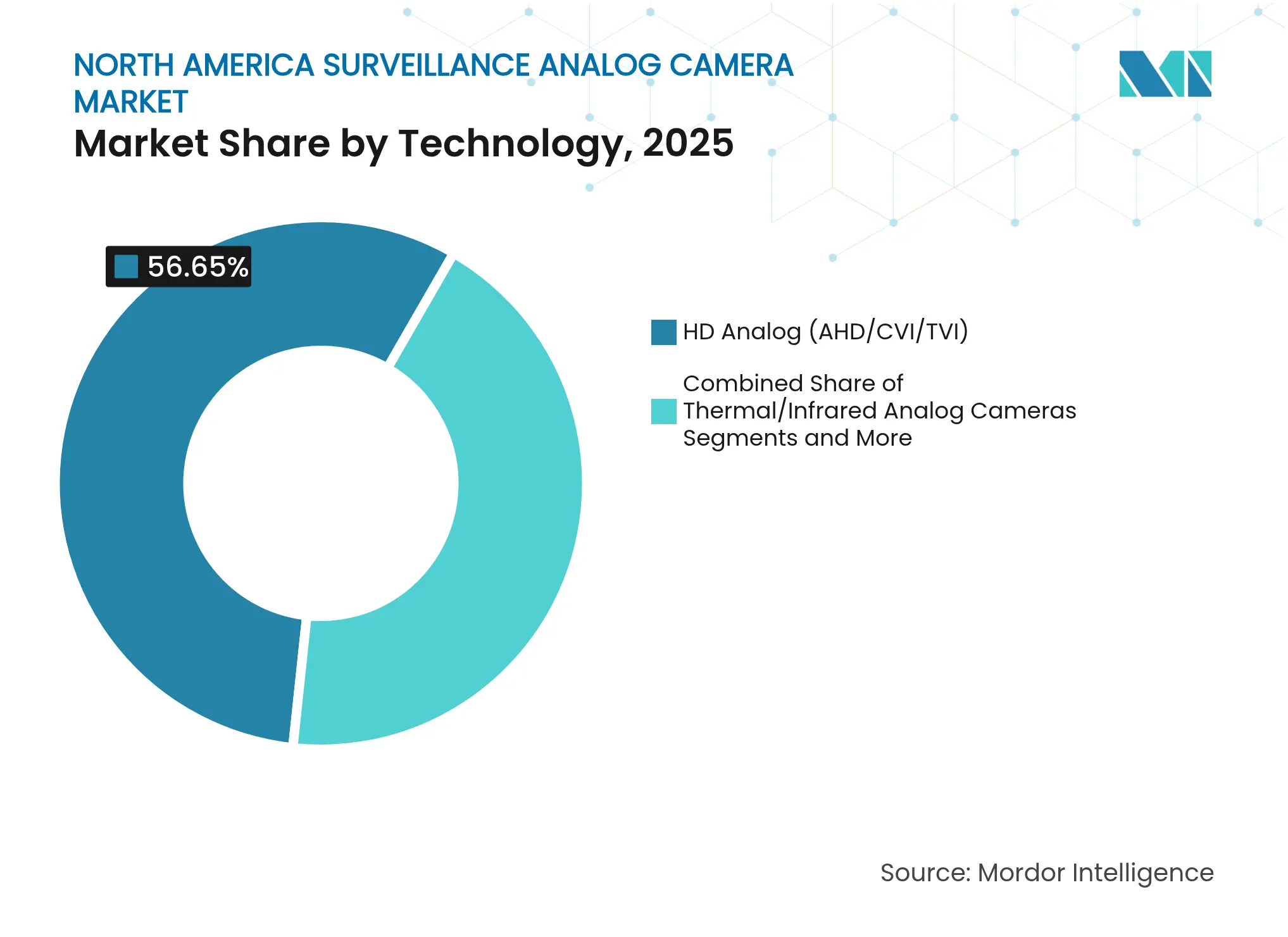

By Technology: HD-Analog Formats Extend Legacy Infrastructure Lifespan

HD-analog protocols—AHD, HD-CVI, and HD-TVI—captured 56.65% of 2025 revenue and remain the backbone of the North America surveillance analog camera market. Each standard supports up to 8 MP over 300–500 m runs, enabling cost-effective 4K upgrades without new cabling. AHD appeals to value buyers; HD-CVI offers stable transmission for larger campuses; HD-TVI balances multi-vendor compatibility at slightly higher price points. Hybrid DVRs that ingest legacy NTSC along with all three HD-analog flavors let integrators stage migrations room-by-room.

The 4K/Ultra-HD analog slice is small but growing at 8.46% CAGR as casinos, border checkpoints, and city-center projects demand forensic-level detail. Standard definition systems continue to phase out except in ultra-budget locations. Security Camera King projects that cross-protocol, cross-generation DVRs will remain indispensable in retrofit roadmaps through 2031

Note: Segment shares of all individual segments available upon report purchase

By Resolution: Higher Megapixel Cameras Narrow Gap with IP Systems

The 2–5 MP bracket controlled 48.95% of revenue in 2025, delivering adequate clarity for identification and modest digital zoom. >5 MP models—including 8 MP 4K bullets—are rising fastest at 8.86% CAGR as chipset costs fall and storage efficiency improves. Sub-2 MP units persist in broad-view hallways and utility rooms but lose share annually.

Advances in signal processing and H.265 compression allow higher bitrates over coax without congesting DVR storage, supporting resolution migration. Market tutorials now guide dispensaries on tailoring megapixel choices to regulatory scene-resolution rules, accelerating the shift to higher pixel-count systems eufy.com. As megapixel counts climb, analog blurs traditional technology lines, offering near-IP image quality while preserving hardwired reliability.

The United States generated 91.05% of 2025 revenue for the North America surveillance analog camera market, reflecting decades of coax infrastructure in government, education, and retail facilities. NDAA rules bar select Chinese vendors, channeling federal and critical-infrastructure orders toward domestic or Korean-made options. Urban centers are accelerating IP adoption, yet fleets of legacy coax remain in mid-tier municipalities, public schools, and SME premises where budget reprioritizations favor HD-analog retrofits.

Rural America presents a distinct opportunity pool. Limited broadband penetration and long fiber trenching distances tilt decisions toward analog solutions that operate independently of continuous network backhaul. County sheriffs, water districts, and transportation agencies deploy solar-powered, DVR-based kits at intersections and depots, sustaining steady unit shipments. States rolling out cannabis licensing frameworks create incremental annual demand spikes centered on compliance deadlines. Canada, while contributing a smaller base, is projected to grow at 6.41% CAGR to 2031, outpacing the regional average. Nationwide cannabis legalization, privacy-balanced regulations, and 2027 bus-camera mandates underpin recurring procurement waves. Large rural territories mirror U.S. connectivity constraints, supporting analog’s value proposition. Canadian integrators emphasize NDAA-style supply chain transparency, giving lift to Korean and North American brands that commit to secure-by-design component sourcing. Cross-border vendors capable of aligning with divergent privacy codes and bilingual labeling requirements capture synergies across the two markets.

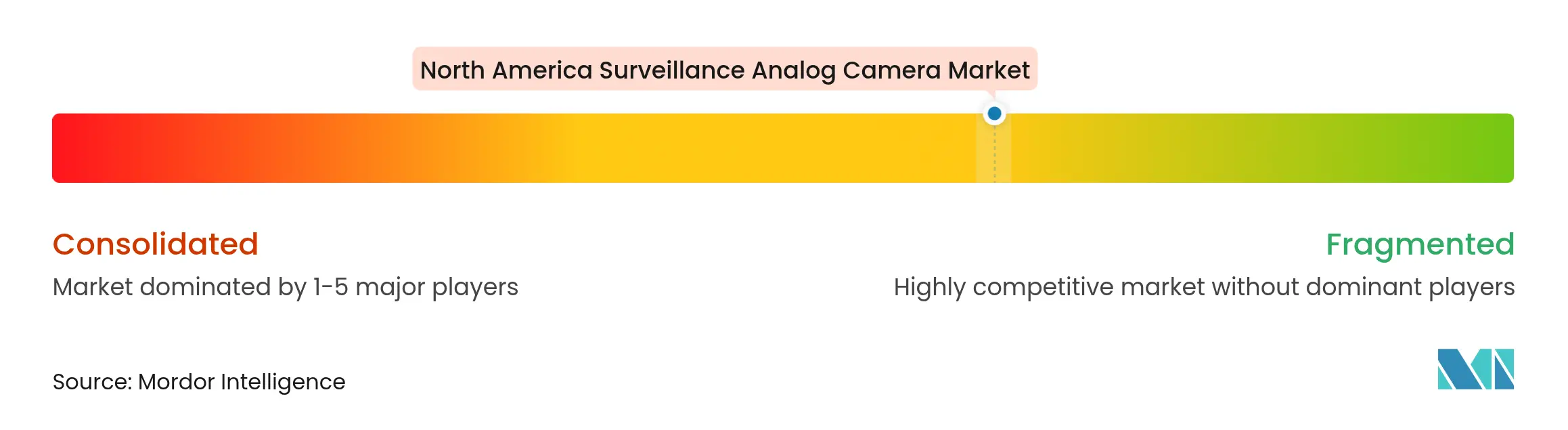

Market Concentration

The top five suppliers account for roughly 60% of the North America surveillance analog camera market, implying moderate concentration. Hikvision and Dahua continue to ship high volumes into private retail and light industrial segments but face erosion where NDAA clauses restrict spend. Hanwha Vision, Motorola Solutions (Avigilon & Pelco), Axis, and Digital Watchdog expand share by positioning as NDAA-compliant partners offering end-to-end hybrids that smooth analog-to-IP transitions.

Strategic moves illustrate this pivot. Digital Watchdog’s alliance with Allied Telesis embeds automated network-health reporting, reducing truck rolls and strengthening total-cost-of-ownership arguments. Hanwha Vision’s 8 K and AI-edge roadmap targets city-wide surveillance contracts and offers drop-in analog replacements packaged with evidence-grade analytics. I-PRO’s education mega-deal underscores vertical selling: bundling cameras, recorders, and training services to reassure school boards about cybersecurity and student safety.

Supply chain resilience has become a competitive wedge. Firms diversify CMOS sourcing toward Taiwanese fabs to mitigate potential export-control shocks. Channel programs emphasize backward-compatible firmware and long-lifecycle support to protect municipal buyers from sudden obsolescence. Overall, success hinges on hybrid architecture proficiency, NDAA alignment, and the agility to scale production while navigating component scarcity.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A surveillance analog camera is a security device that captures video footage in an analog format, typically transmitting signals over coaxial cables to a recording device or monitor. While they offer cost-effective solutions for basic security needs, analog cameras generally provide lower resolution compared to digital or IP cameras and have limited integration capabilities with advanced surveillance technologies.

The study tracks the revenue accrued through the sale of surveillance analog camera products by various players operating in North America. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyzes the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The North American surveillance analog camera market is segmented by end-user industry (government, banking, healthcare, transportation and logistics, industrial, and others) and by country (the United States and Canada). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.