Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

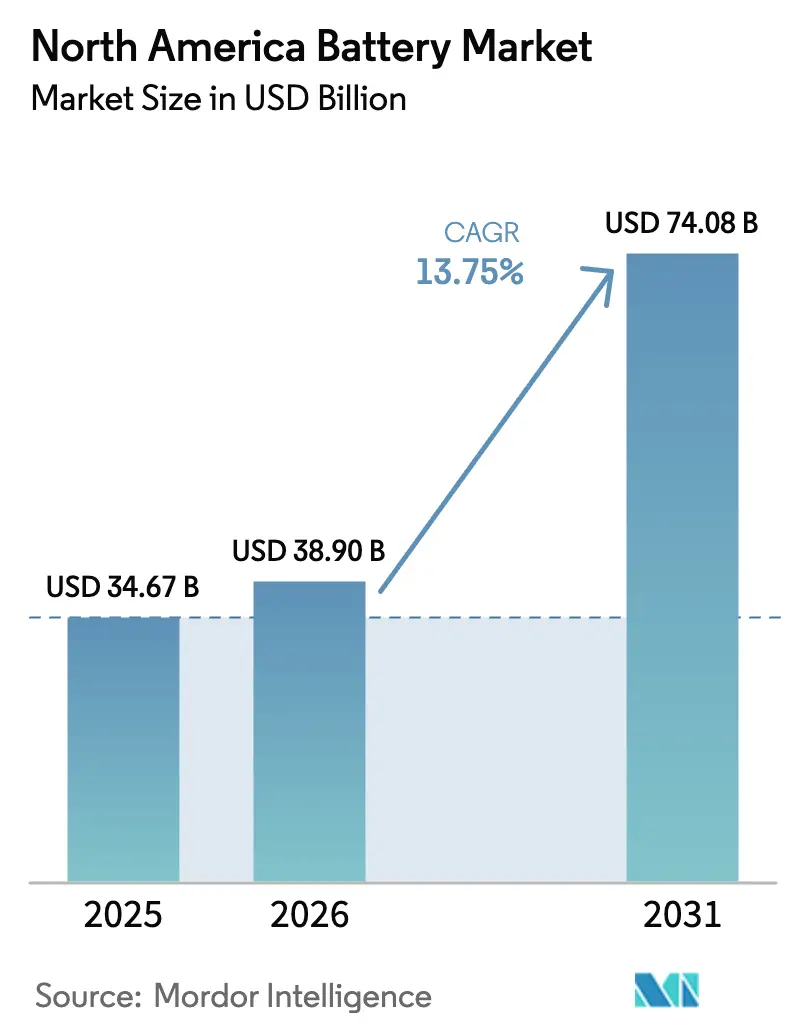

| Base Year Market Size (2025) | USD 34.67 Billion |

| Market Size (2026) | USD 38.90 Billion |

| Market Size (2031) | USD 74.08 Billion |

| Growth Rate (2026 - 2031) | 13.75% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Battery Market Analysis by Mordor Intelligence

The North America Battery Market size is projected to be USD 34.67 billion in 2025, USD 38.90 billion in 2026, and reach USD 74.08 billion by 2031, growing at a CAGR of 13.75% from 2026 to 2031.

Federal production tax credits, state-level storage mandates, and fast-growing electric-vehicle (EV) demand are compressing pack costs, widening addressable use cases, and accelerating capacity additions across the region. Automotive electrification, especially in the light-duty truck and SUV segments that require packs exceeding 100 kilowatt-hours, is pulling forward gigafactory investments and anchoring multiyear supply agreements between automakers and cell manufacturers. At the same time, utility-scale storage targets in California, New York, Texas, and British Columbia are establishing a predictable offtake floor that de-risks financing for new entrants.[1]California Public Utilities Commission, “Storage Procurement Targets,” cpuc.ca.gov Technology differentiation is shifting from cost to performance as solid-state, silicon-anode, and sodium-ion chemistries move from pilot to early commercial scale, expanding the innovation frontier while intensifying competition for skilled labor and critical-material supply.

Key Report Takeaways

- By battery type, secondary rechargeable batteries held 75.5% of the North American battery market share in 2025, while their 15.5% CAGR through 2031 positions them as the fastest-growing battery-type segment.

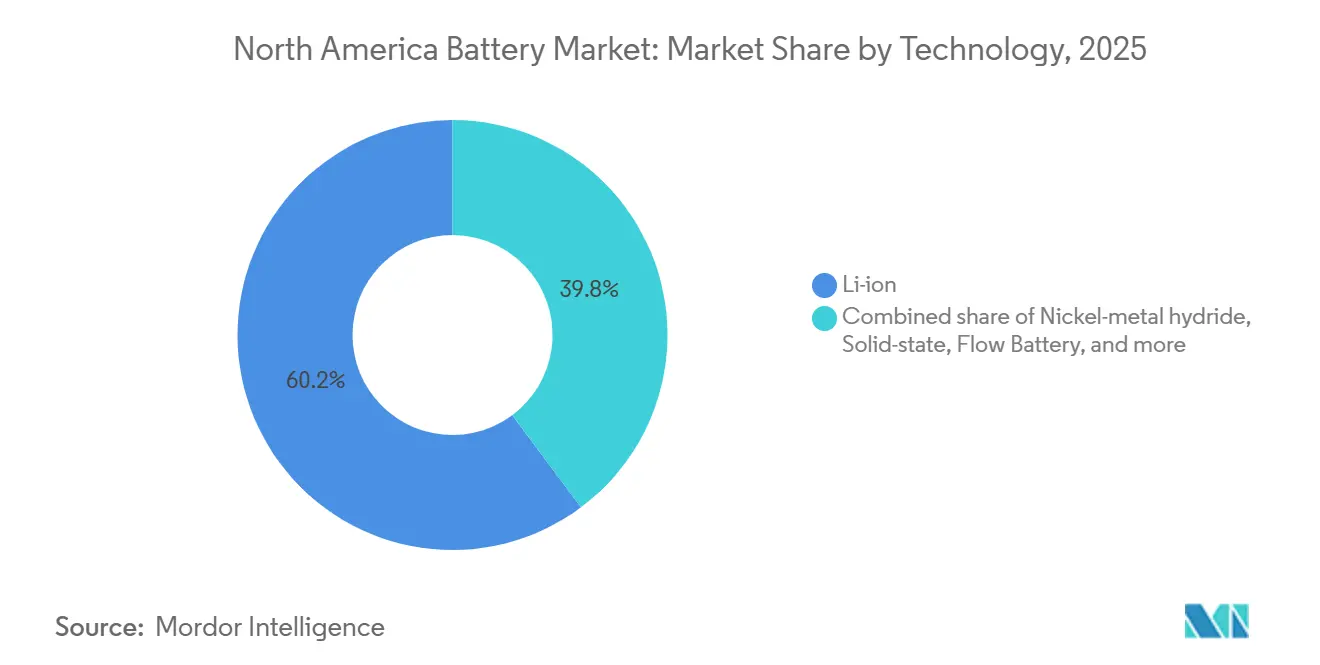

- By technology, lithium-ion technology captured 60.2% of 2025 revenue, yet solid-state cells are forecast to post a 35.8% CAGR, the quickest rate within the technology landscape.

- By application, automotive applications commanded 46.9% of 2025 demand and are projected to expand at a 19.7% CAGR, outpacing all other end uses.

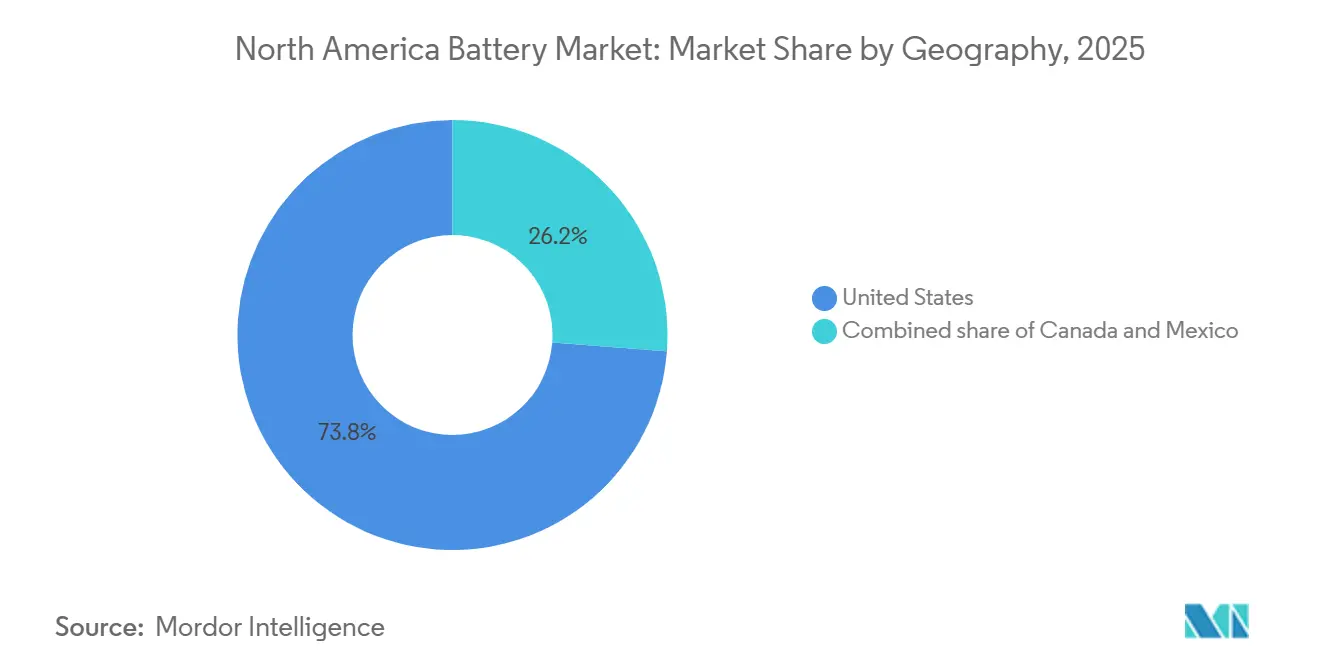

- By geography, the United States accounted for 73.8% of 2025 revenue, whereas Mexico is set to climb at a 28.6% CAGR, the fastest among North American geographies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IRA-fuelled gigafactory build-out compressing pack costs | 3.8% | United States, with spillover to Canada and Mexico | Medium term (2-4 years) |

| On-shoring incentives reducing supply-chain risk for OEMs | 2.7% | United States and Canada, concentrated in Michigan, Ontario, Tennessee, Kentucky | Medium term (2-4 years) |

| Utility-scale storage mandates in CA, NY, TX, BC | 1.9% | California, New York, Texas, British Columbia | Short term (≤2 years) |

| Emerging automaker-battery-maker JVs unlocking capital efficiency | 1.6% | United States and Canada, particularly in EV manufacturing hubs | Medium term (2-4 years) |

| EV-driven average battery size increase (SUV mix) creating volume pull | 2.4% | United States and Canada, driven by consumer preference for larger vehicles | Long term (≥4 years) |

| Recycling tax credits lowering end-of-life costs | 0.9% | United States, with early adoption in Nevada, Georgia, and Ohio | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

IRA-Fuelled Gigafactory Build-Out Compressing Pack Costs

Section 45X of the Inflation Reduction Act (IRA) provides USD 35 per kilowatt-hour for cells and USD 10 per kilowatt-hour for modules manufactured domestically, a structure that triggered USD 110 billion of announced battery investments across 13 states since 2022.[2] U.S. Department of Energy, “Section 45X Advanced Manufacturing Credits,” energy.gov BlueOval SK secured a USD 9.6 billion Department of Energy loan for twin plants in Kentucky and Tennessee, with the first line online in late 2025. Panasonic ramped its De Soto, Kansas, facility to 30 gigawatt-hours in 2025, while Samsung SDI and General Motors broke ground on an Indiana site targeting a 2026 start-up. These projects lower the breakeven utilization threshold from 80% to 60%, accelerating commissioning schedules and enabling a forecast 40% pack-cost decline from 2022 to 2027. As costs fall, total-cost-of-ownership parity between EVs and internal-combustion vehicles is expected as early as 2027, a full two years earlier than many OEMs originally modeled.

On-Shoring Incentives Reducing Supply-Chain Risk for OEMs

Automakers absorbed USD 2.3 billion of extra logistics costs during the 2021–2022 semiconductor crunch, prompting a pivot toward regional cell production that mitigates shipping disruptions and tariff exposure. The IRA’s Foreign Entity of Concern provisions, effective January 2024, disqualify EVs from a USD 7,500 consumer credit if batteries or critical minerals come from Chinese or Russian entities, driving supplier re-mapping. Ultium Cells now runs three U.S. plants totaling 140 gigawatt-hours, trimming cell lead times from 12 to 4 weeks and lowering working-capital needs by about 20%. Stellantis and Samsung SDI followed with a USD 7.3 billion Kokomo facility that secures supply for full-size pickups. Together, these vertically integrated models insulate OEM programs from foreign-exchange swings and logistics bottlenecks, protecting margins during the EV ramp.

Utility-Scale Storage Mandates in CA, NY, TX, BC

California requires 11.5 gigawatts of incremental storage by 2026 and another 15 gigawatts by 2030, spurring record interconnection requests for lithium-ion projects. New York’s Climate Leadership and Community Protection Act targets 6 gigawatts of storage by 2030, backed by a USD 400 million incentive pot launched in 2024. ERCOT added 4.2 gigawatts of batteries in 2024, the largest single-year gain nationwide, as merchants arbitraged peak-price spreads. British Columbia’s CleanBC blueprint seeks 3 gigawatts by 2030, with BC Hydro issuing 1.5 gigawatts of 2025 RFPs. These mandates underpin multiyear offtake contracts that cut project financing costs by 100–150 basis points and create a demand floor independent of EV adoption trajectories.

EV-Driven Average Battery Size Increase (SUV Mix)

Average North American pack size jumped from 62 kilowatt-hours in 2022 to 78 kilowatt-hours in 2025 as consumers gravitated toward electric SUVs and pickups.[3]Ford Motor Company, “F-150 Lightning Battery Specifications,” ford.com The Ford F-150 Lightning, Chevrolet Silverado EV, and Rivian R1T each deploy packs exceeding 130 kilowatt-hours, magnifying cell demand beyond unit-sales growth. A 1% rise in EV penetration now equates to a 1.3% uptick in gigawatt-hour demand, compressing timelines for new-build gigafactory absorption. Cell-to-pack architectures that remove module housings cut part counts by 30% and lift energy density by up to 15%, a design shift favoring vertically integrated OEMs capable of co-engineering cells and structural enclosures. Higher average pack capacities are therefore both a volume and technology catalyst, reinforcing learning-curve cost declines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mid-stream bottlenecks (foil, separator) delay ramp-ups | -1.8% | United States and Canada, affecting new gigafactory commissioning timelines | Short term (≤2 years) |

| Lithium-price volatility widening project IRR band | -1.3% | North America-wide, with heightened exposure in projects reliant on spot-market procurement | Medium term (2-4 years) |

| Tariff uncertainty on Chinese LFP imports | -1.1% | United States, particularly impacting utility-scale ESS and entry-level EV segments | Short term (≤2 years) |

| Skilled-labour shortages at new cell plants | -0.9% | United States and Canada, concentrated in emerging battery-belt states (Kentucky, Tennessee, Georgia, Kansas) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lithium-Price Volatility Widening Project IRR Band

Spot lithium-carbonate prices plunged from USD 80,000 per metric ton in late 2022 to USD 12,000 by June 2024 before rebounding to USD 15,000 by December, a roller-coaster that injected a 12%–15% spread into battery-pack economics. General Motors’ Thacker Pass joint venture aims to secure 40,000 metric tons annually by 2027, shielding 800,000 vehicles per year from spot swings. Yet project IRRs remain highly sensitive; sustained prices below USD 18,000 could extend paybacks beyond 10 years, delaying bank financing for mid-tier cell manufacturers. Smaller firms lacking captive lithium struggle to hit the 80% offtake threshold demanded by lenders, throttling greenfield builds and weighing on near-term capacity additions.

Mid-Stream Bottlenecks (Foil, Separator) Delay Ramp-Ups

Separator film and copper foil constitute 15%-20% of a cell’s bill of materials, but over 70% of global separator capacity sits with three Asian suppliers, leaving new North American lines vulnerable to shortages.[4]Financial Times, “Battery Supply-Chain Constraints,” ft.com Gigafactories that started in 2024 experienced 3- to 6-month qualification delays, pushing revenue ramp-ups into 2026. U.S. copper-foil capacity covered only 150 gigawatt-hours of annual demand in 2024 versus 1,100 gigawatt-hours of announced cell capacity by 2030, forcing OEMs to dual-source from Asia and accept longer lead times. SK Nexilis’ 30,000-metric-ton Kentucky plant, due 2027, will address just a slice of the deficit. Until mid-stream supply expands, gigafactory commissioning schedules remain a gating factor for the North America battery market outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Dominance Accelerates

Secondary rechargeable batteries accounted for 75.5% of the North America battery market share in 2025 and are projected to expand at a 15.5% CAGR to 2031. This growth trajectory reflects surging EV and stationary-storage deployments, both of which require high cycle life and multi-year warranties that favor lithium-ion chemistries. Average pack sizes in electric trucks rose to 78 kilowatt-hours in 2025, lifting cell demand per vehicle and hastening gigafactory utilization ramps. Primary cells, at 24.5% of revenue, grow at single-digit rates, limited to medical, defense, and IoT niches where multi-decade shelf life outweighs rechargeability. Consolidation trends differ by sub-segment; Duracell and Energizer maintain brand pull in consumer alkaline, whereas automotive OEMs increasingly insource lithium-ion, compressing margins for independent suppliers.

Unit economics are also diverging. Tesla’s internal 4680 line hit a 10 gigawatt-hour run rate by September 2025, reducing per-kilowatt-hour costs 15% versus externally sourced 2170 cells and capturing upstream value that previously accrued to vendors. Small primary-battery suppliers benefited from a 12% rise in Department of Defense procurement in 2024, highlighting how performance-critical niches can still yield steady margins despite slower volume growth. Overall, rechargeable capacity additions and associated learning-curve cost declines are locked in as the principal engine of the North America battery market through 2031.

By Technology: Solid-State Gains Outpace Lithium-Ion

Lithium-ion retained 60.2% of 2025 revenue, underpinned by established NMC and LFP chemistries that combine cost competitiveness with automotive-grade safety. Solid-state cells, while representing less than 1% of shipments, are on course for a 35.8% CAGR as pilot lines scale and OEMs chase 400 watt-hour-per-kilogram energy densities. Lead-acid, still critical for starting-lighting-ignition, slipped below 25% as EVs erode the internal-combustion vehicle base and data centers pivot to lithium-ion UPS systems.

QuantumScape and Volkswagen’s PowerCo finalized a licensing pact in April 2025, aiming for initial solid-state deliveries in 2026, signaling readiness for limited commercial adoption. Sodium-ion cells from Natron Energy entered production in Michigan to serve stationary UPS and material-handling use cases where energy density is secondary to cost and cycle life. Flow and lithium-sulfur variants remain restricted to demonstration projects given current cost-per-cycle disadvantages, but continued R&D investment keeps them on the long-term radar for grid storage applications.

By Application: Automotive Segment Drives Volume

Automotive batteries captured 46.9% of 2025 revenue and are forecast to grow 19.7% annually to 2031, cementing their role as the principal volume driver for the North America battery market. Pickup- and SUV-heavy model mixes push pack capacities above 100 kilowatt-hours, magnifying the gigawatt-hour impact of each new EV launch. Industrial stationary storage, at roughly 30% of revenue, posts mid-teen growth as data centers, telecoms, and utilities replace lead-acid and gas peakers with lithium-ion systems that cut operating costs by up to 50%. Portable consumer electronics and power tools hold a 15% share, with cordless tool electrification offsetting slower smartphone replacement cycles.

SLI batteries, now below an 8% share, decline slowly as the regional fleet transitions to EVs. Clarios is repositioning with 12-volt lithium-ion packs for EV auxiliaries, a nascent but strategic hedge against diminishing lead-acid demand. Co-location strategies, such as Ultium Cells’ Spring Hill site, only 5 miles from GM’s truck line, underscore how logistics optimization and just-in-time delivery are now as critical as chemistry advances for competitive advantage.

Geography Analysis

The United States generated 73.8% of 2025 revenue, powered by more than USD 110 billion of post-IRA cell-plant announcements and aggressive state storage mandates. Loan Programs Office commitments totaling USD 18 billion cut weighted-average costs of capital by up to 200 basis points, tipping numerous projects from “proposed” to “under construction.” California, New York, and Texas alone accounted for 60% of 2024 stationary storage deployments, reflecting how policy targets translate directly into near-term volume.

Canada contributed roughly 15% of regional revenue, with Ontario and Quebec capturing the bulk via CAD 15 billion of combined incentives that attracted Stellantis, LG Energy Solution, and Volkswagen gigafactories scheduled to come online between 2025 and 2027. Upstream mineral strength anchors cathode-precursor projects, shortening supply lines for nickel and cobalt and reinforcing the nation’s strategic role in the North America battery market size calculus.

Mexico is growing quickest at a 28.6% CAGR, leveraging USMCA trade rules and lower labor costs to attract both automakers and mid-stream suppliers. Tesla’s Monterrey gigafactory and BYD’s site scouting in Nuevo León signal that announced capacity could quintuple to 50 gigawatt-hours by 2030 if water, electricity, and skilled-labor hurdles are resolved. Component makers—from separator film to electrolytes—are co-locating, mirroring the broader automotive supply-chain migration that has unfolded since the mid-1990s.

Competitive Landscape

The top five suppliers, LG Energy Solution, Panasonic Energy, SK On, Samsung SDI, and Tesla, controlled about 60% of lithium-ion cell capacity in 2025, giving the North America battery market a moderate concentration profile. Joint-venture structures dominate capacity additions, allowing OEMs to secure supply while sharing capital burdens; Ultium Cells’ 140-gigawatt-hour U.S. footprint exemplifies this model. Vertical integration is accelerating: Tesla’s 4680 line reached a 10 gigawatt-hour run rate in 2025, and Ford plans to internalize LFP technology under a CATL license in Michigan by 2026, moves that could further redistribute margin pools.

White-space opportunities are surfacing in solid-state, sodium-ion, and recycling. QuantumScape raised USD 300 million from Volkswagen to co-develop production processes, while Redwood Materials secured a USD 2 billion DOE loan to upscale recycled-cathode output to 500 gigawatt-hours by 2028. Incumbent lead-acid players such as EnerSys are launching lithium-ion product lines to retain industrial customers transitioning away from legacy chemistries. Regulatory compliance with Foreign Entity of Concern rules is also reshaping supply decisions, steering automakers toward U.S. or allied-nation facilities and prompting Chinese firms to consider licensing or local joint ventures to preserve North American market access.

North America Battery Industry Leaders

LG Energy Solution

Panasonic Energy

Tesla (Internal)

Samsung SDI

SK On

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Honda Development and Manufacturing of America has struck a deal to acquire LG Energy Solution's stake in their joint electric vehicle battery plant in Ohio, with the transaction valued at USD 2.85 billion.

- November 2025: Following the inauguration of a new battery plant in Liberty, North Carolina, Toyota unveiled its intention to inject an additional USD 10 billion into its U.S. operations over the coming five years.

- September 2025: Henkel has inaugurated its North America Battery Application Center in Madison Heights, Michigan. This move bolsters the company's regional backing for OEMs and battery producers, offering enhanced material application expertise for EV components.

- July 2025: Nano One Materials Corp., a company specializing in lithium-ion battery cathode active materials (CAM), has been chosen to be part of the Arkansas Lithium Technology Accelerator (ALTA). ALTA is America's inaugural accelerator focused on the lithium and battery supply chain.

North America Battery Market Report Scope

A battery is a device that converts chemical energy contained within its active materials directly into electric energy by means of an electrochemical oxidation-reduction (redox) reaction. This type of reaction involves the transfer of electrons from one material to another via an electric circuit.

The North American battery market is segmented by battery type, technology, application, and geography. By battery type, the market is segmented into primary and secondary. By technology, the market is segmented into lead-acid, Li-ion, nickel-metal hydride, nickel-cadmium, sodium-sulfur, solid-state, flow battery, and emerging chemistries. By application, the market is segmented into automotive, industrial, portable, power tools, SLI, and other applications. The report also covers the market size and forecasts for the North American battery market across the major countries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

By Geography

| United States |

| Canada |

| Mexico |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America battery market in 2026?

The market is estimated at USD 38.90 billion in 2026.

Which battery type is growing fastest?

Secondary rechargeable batteries are expanding at a 15.5% CAGR through 2031 thanks to soaring EV and stationary-storage demand.

What technology will disrupt lithium-ion dominance?

Solid-state cells are poised for the highest growth, with pilot lines moving toward commercial production by 2028.

Why is Mexico attracting battery investments?

Nearshoring incentives under USMCA, lower labor costs, and proximity to U.S. vehicle plants underpin Mexico's 28.6% CAGR through 2031.

What is the main supply-chain bottleneck today?

Separator-film and copper-foil shortages delay gigafactory ramps, extending lead times and forcing continued reliance on Asian suppliers.

How are pack costs expected to change?

Section 45X manufacturing credits and economies of scale are projected to drive a 40% drop in pack costs between 2022 and 2027.

Page last updated on: