Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

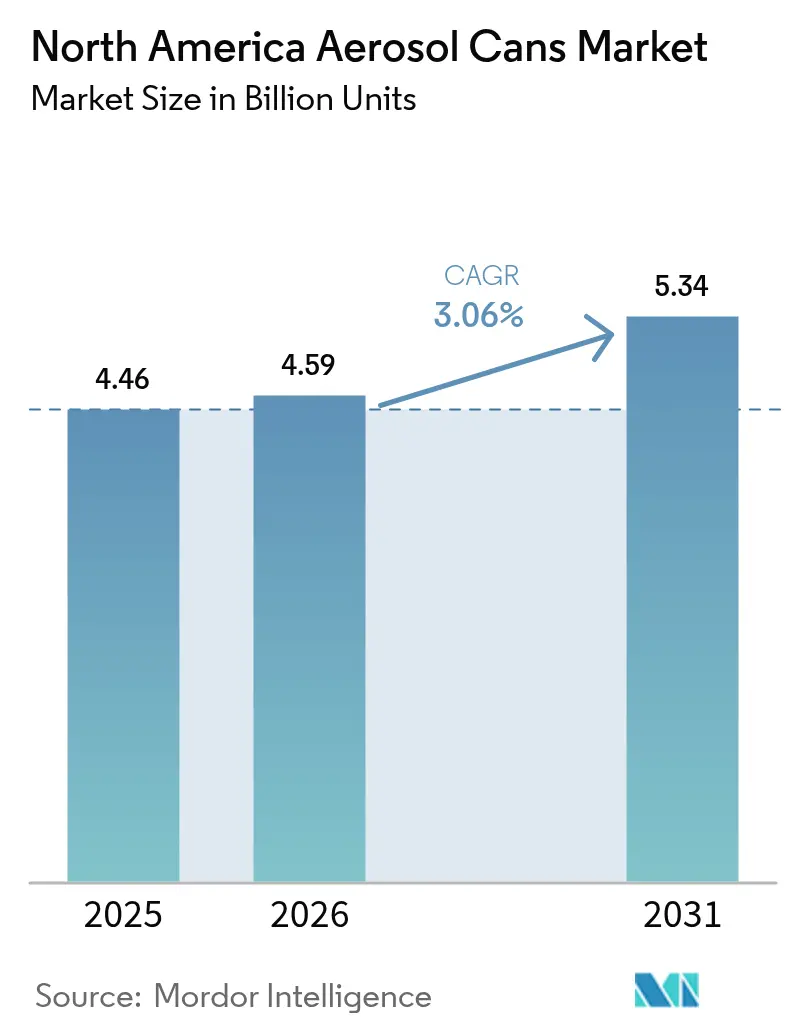

| Base Year Market Size (2025) | 4.46 Billion units |

| Market Volume (2026) | 4.59 Billion units |

| Market Volume (2031) | 5.34 Billion units |

| Growth Rate (2026 - 2031) | 3.06% CAGR |

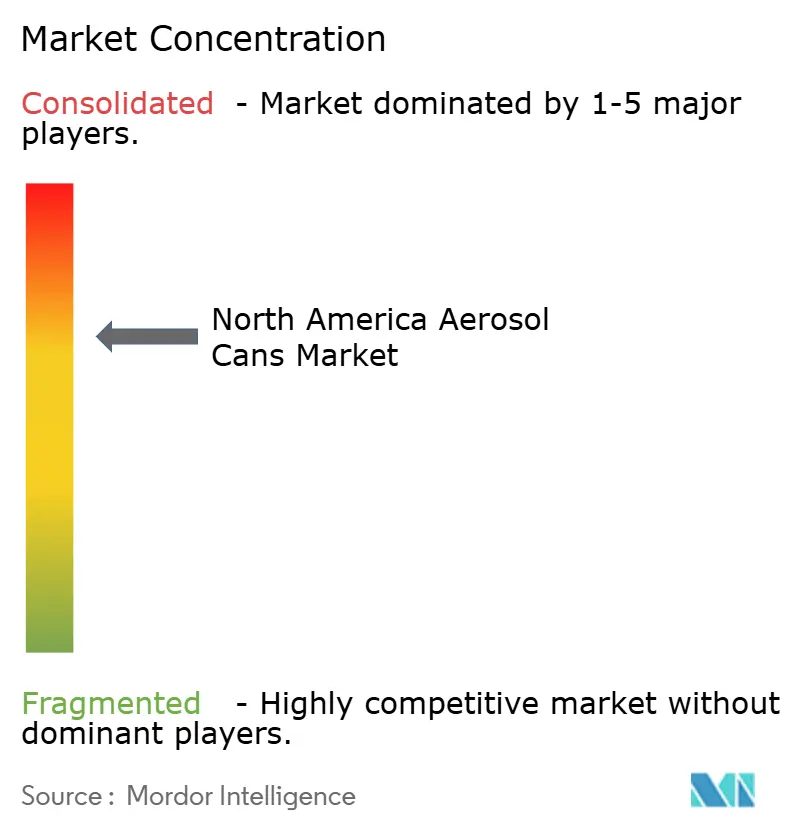

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Aerosol Cans Market Analysis by Mordor Intelligence

The North America aerosol cans market size is expected to grow from 4.46 billion units in 2025 to 4.59 billion units in 2026 and is forecast to reach 5.34 billion units by 2031 at a 3.06% CAGR over 2026-2031. The measured expansion reflects a structural shift toward lighter-gauge alloys, greater post-consumer recycled content, and reformulation driven by hydrofluorocarbon (HFC) restrictions. Federal tariffs that lifted aluminum input costs have intensified converter investment in weight-reduction technologies, while brand owners are experimenting with plastic alternatives for niche fragrance and pharmaceutical launches. Household disinfectant sprays, once a pandemic anomaly, have become staples, boosting demand for higher-capacity cans powered by nitrogen systems that address flammability concerns. In parallel, on-shoring of contract filling in Mexico is rebalancing regional supply chains as manufacturers seek tariff-neutral export corridors into the United States.

Key Report Takeaways

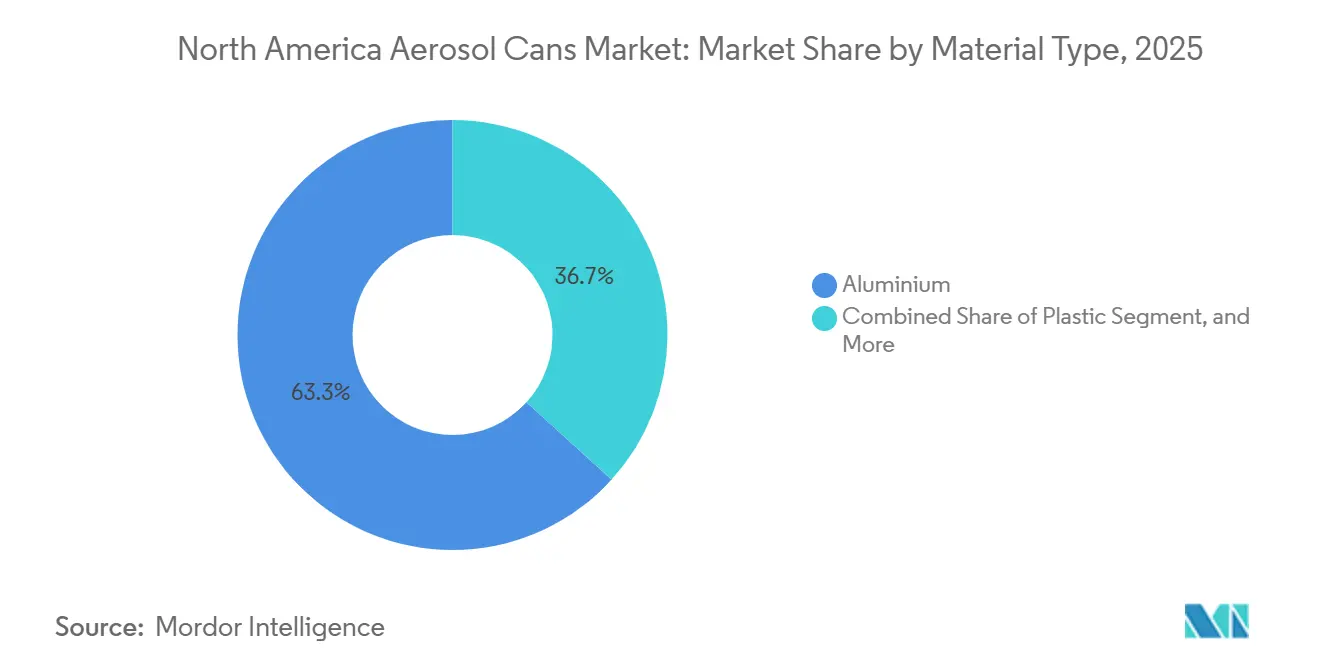

- By material type, aluminum held 63.26% of the 2025 volume of the North America aerosol cans market, while plastic variants are expanding at a 4.02% CAGR through 2031.

- By type, two-piece formats led with a 60.82% share in 2025, whereas three-piece cans are projected to grow at a 3.62% CAGR through 2031.

- By propellant, liquefied-gas systems captured 66.64% of 2025 production, and compressed-gas alternatives are forecast to grow at a 3.68% CAGR over the period.

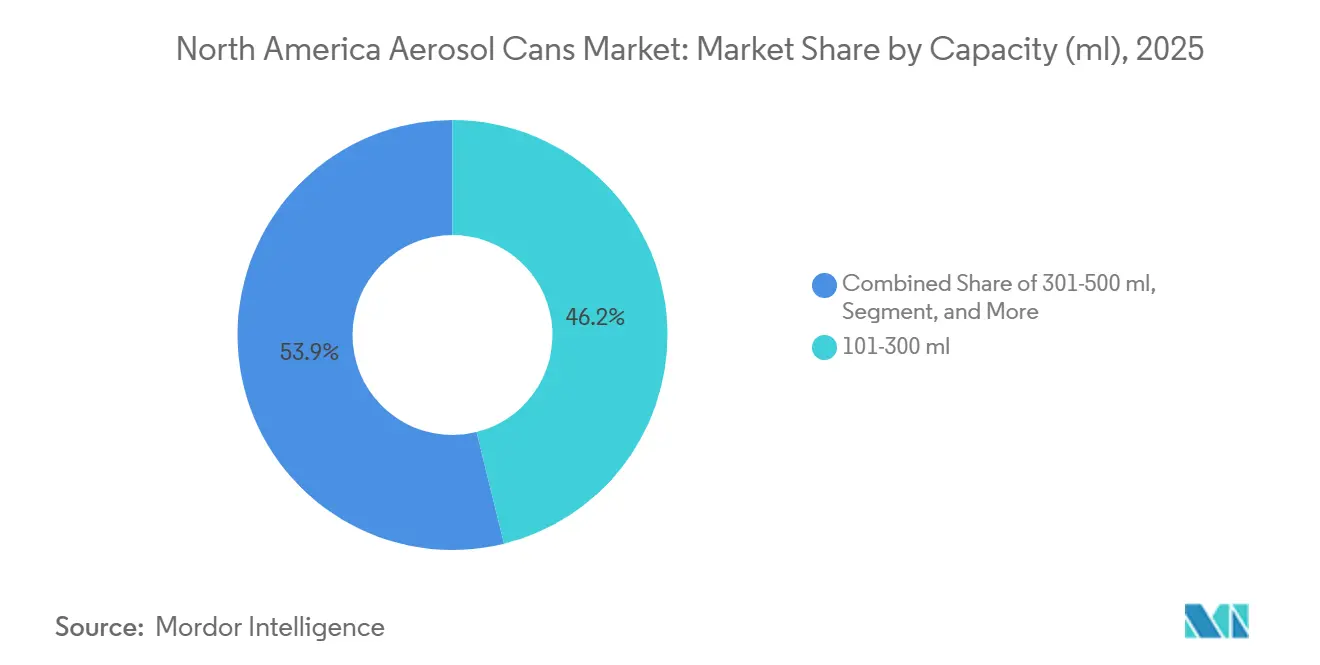

- By capacity, the 101-300 milliliter tier accounted for 46.15% of 2025 shipments and posted the fastest growth at a 3.81% CAGR.

- By end-user industry, personal care commanded 41.32% volume in 2025, yet household care is expected to post the highest 4.42% CAGR through 2031.

- By geography, the United States accounted for 81.27% of regional volume of the North America aerosol cans market in 2025, while Mexico is projected to log a 3.71% CAGR in new greenfield capacity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Aerosol Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand From Personal Care and Cosmetics | +0.9% | United States, Canada, Mexico Premium Tiers | Medium Term (2–4 Years) |

| Acceleration of Household Surface-Care Sprays | +1.1% | North America-Wide, Strongest in U.S. Suburbs | Short Term (≤ 2 Years) |

| Preference for Infinitely Recyclable Aluminium Cans | +0.7% | United States, Canada, Emerging Mexico | Medium Term (2–4 Years) |

| AIM-Act-Driven Switch to Low-GWP Propellants | +0.6% | United States, Canada | Short Term (≤ 2 Years) |

| Growth in Aerosolized Automotive Lubricants | +0.5% | U.S. Industrial Corridors, Canadian Clusters | Long Term (≥ 4 Years) |

| On-Shoring of Contract Filling to De-Risk Supply Chains | +0.4% | United States, Mexico | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Acceleration Of Household Surface-Care Sprays

Demand for disinfectant and multi-surface cleaners remains elevated beyond the pandemic peak. Retailers have widened shelf space for aerosol SKUs that deliver continuous spray coverage and faster application. Brands have responded by shifting from liquefied petroleum gas to nitrogen-powered bag-on-valve platforms that remove flammability concerns and lower volatile organic compound (VOC) emissions. Contract fillers note that line utilization for surface-care products climbed above 90% in 2025, encouraging investment in larger-diameter tooling optimized for 300-500 milliliter cans. The momentum is likely to persist as commercial cleaning contractors prioritize labor savings achieved through faster spray cycles.

Rising Demand From Personal Care and Cosmetics

Deodorants, dry shampoos, and texturizing hair sprays are migrating from stick and pump formats to aerosols as consumers favor quick-dry, residue-free finishes.[1]Sonoco Products Company, “2025 Investor Presentation,” sonoco.com Social-media promotion of gender-neutral fragrances has spurred small-batch production that benefits regional fillers capable of short lead times. However, aluminum can lead times stretched to 16 weeks in 2025, persuading some brands to trial steel bodies despite the 15-20% weight penalty. Continued SKU proliferation secures volume for the aerosol cans market, but supply tightness may cap short-term upside.

Preference For Infinitely Recyclable Aluminium Cans

Corporate sustainability scorecards increasingly reward packaging that fits a closed-loop profile.[2]The Aluminum Association, “Recycling Rates in the United States,” aluminum.org With 75% of all aluminum ever produced still in circulation, brands promote high-recycled-content cans such as Ball’s ReAl alloy, which cuts can weight by 30% and carbon footprint by 25%. Yet municipal programs accepting aerosol cans curbside dropped below the 60% threshold in 2024, forcing How2Recycle to downgrade the recyclability label to “check locally”. The credibility gap could erode premium pricing, underscoring the need for clearer consumer education and improved collection infrastructure.

AIM-Act-Driven Switch To Low-GWP Propellants

The American Innovation and Manufacturing Act reduced allowable HFC volumes by 40% in 2024, compelling fillers to replace HFC-152a with compressed-gas or hydrocarbon blends. Reformulation projects accelerated through 2025, with brands validating spray performance under higher internal pressures that demand thicker can walls. While compliance shields companies from regulatory penalties, material costs rise 10-15% per unit, pressuring margins unless efficiency gains offset the added metal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition From Substitute Packaging Formats | -0.8% | North America-Wide, Strongest in Personal and Household Care | Medium Term (2–4 Years) |

| Aluminium and Steel Price Volatility | -0.6% | United States, Canada, Mexico | Short Term (≤ 2 Years) |

| Rising Disposal-Site Fires Tightening Collection Rules | -0.3% | United States, Canada | Long Term (≥ 4 Years) |

| Capacity Rationalisation After Regional Plant Closures | -0.4% | U.S. Midwest, Canada | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Competition From Substitute Packaging Formats

Trigger sprayers, stick applicators, and refill pouches are reclaiming share as consumers question propellant safety and recyclability.[3]Unilever, “Packaging Choices and Consumer Perceptions Survey,” unilever.com Major personal-care multinationals expanded non-aerosol deodorant lines in 2025, citing research that 30-40% of shoppers avoid aerosols. Cost-sensitive buyers have shifted their preference, granting household-cleaner refill stations a two-percentage-point increase in market share. These buyers are drawn to refill stations, which offer prices 40-60% lower than traditional aerosol cans. This trend is especially pronounced in scenarios where the convenience of aerosols doesn't warrant their premium price.

Aluminium and Steel Price Volatility

Spot premiums for Midwest aluminum ingot rose sharply during pandemic-era logistics disruptions, throttling converter margins inside the North America aerosol cans market. Although long-term supply contracts offer partial insulation, sudden energy-price shocks and international tariff disputes still cascade to can-sheet availability. Smaller fillers, constrained by limited hedging tools, are resorting to thinner gauges or resin overcaps to absorb costs. However, this approach heightens their risk of structural failures and potential brand recalls. As a result, ongoing uncertainties in metal pricing are curbing incremental growth. This trend is likely to persist until there's a stabilization in input economics, either through improved recycling rates or breakthroughs in alternative materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Leads as Plastic Gains Niche Ground

Aluminum retained 63.26% of 2025 shipments of the North America aerosol cans market, reflecting its compatibility with high-pressure propellants and strong consumer perception of recyclability. Plastic, however, is advancing at a 4.02% pace as transparent barrier coatings enable oxygen-sensitive formulas. The aerosol cans market size for plastic formats is anticipated to expand alongside indie fragrance rollouts that prioritize unique bottle shapes over metal gloss. Aluminum lightweighting initiatives, including Ball’s ReAl alloy, reduce raw-material exposure and support corporate carbon-reduction goals. Steel remains entrenched in paint and lubricant channels where dent resistance outweighs the weight penalty.

Secondary-scrap supply rose 4% in 2024, but residual propellant contamination continues to limit aerosol scrap recovery, sustaining dependence on more expensive primary metal. Plastic cans exploit injection-molding flexibility to integrate ergonomic grips and complex actuator seats, features that are cumbersome to implement in metal. As brands weigh cost, aesthetics, and sustainability narratives, material selection will remain fluid, protecting volume for the broader aerosol cans market

By Can Type: Two-Piece Efficiency Confronts Three-Piece Versatility

Two-piece cans accounted for 60.82% of regional output in 2025, driven by high-speed impact extrusion. Three-piece bodies, though slower to produce, are projected to grow 3.62% per year as fillers serving paints and pharmaceuticals value thicker walls and tamper-evident seams. The aerosol cans market share for two-piece construction may erode modestly as contract fillers diversify into specialty runs that suit the modular three-piece setup. One-piece monobloc formats remain premium, targeting fragrances priced above USD 30 where seamless aesthetics can sway purchase intent.

Crown Holdings and Ball Corporation collectively operate more than 60% of the two-piece capacity, leveraging scale to secure favorable aluminum contracts. Mid-tier suppliers dominate three-piece lines, which benefit from lower capital requirements and flexible height adjustments. Pressure-testing standards favor seamless cans for inhalers, yet cost trade-offs keep two-piece solutions relevant for mass-grade personal-care SKUs.

By Propellant Type: Liquefied Gas Dominance Meets Compressed-Gas Momentum

Liquefied hydrocarbons and dimethyl ether powered 66.64% of the North America aerosol cans market in 2025, undergirding economical spray performance. Compressed-gas systems, mainly nitrogen or air, are forecast to rise at 3.68% as AIM-Act quotas squeeze residual HFC use. The aerosol cans market size for compressed-gas applications is anchored in pharmaceutical and surface-care products where brands pitch “propellant-free” credentials. Bag-on-valve pouches enhance 360-degree spray and contamination-free dispensing but complicate recycling due to laminate construction.

Hydrocarbon costs remain low at roughly USD 0.03 per can, preserving their lead in price-sensitive segments. However, retailers tightened shelf-placement rules for flammable SKUs, nudging formulators toward dimethyl ether despite its 20-30% premium. Higher can burst-pressure requirements for compressed gases elevate metal thickness, adding 10-15% material cost yet opening differentiation avenues around continuous spray ergonomics.

By Capacity: 101-300 Milliliter Band Retains Primacy

Mid-range 101-300 milliliter cans held 46.15% share in 2025 and should expand at 3.81% through 2031. Dimensional compatibility with existing high-speed lines and travel-friendly sizing sustain this leadership. Sub-100-milliliter formats benefit from Transportation Security Administration limits that cement demand in the duty-free and hotel channels. Larger 301-500 milliliter cans dominate household cleaners, but e-commerce dimensional weight penalties curb incremental growth.

Manufacturing changeovers to non-standard diameters can exceed USD 0.5 million, deterring brands from experimenting outside established size windows. Oversized industrial cans above 500 milliliters remain essential for lubricants and paints where professional users value reduced refill frequency.

By End-User Industry: Household Care Outgrows Personal Care

Personal care accounted for 41.32% of the North America aerosol can market in 2025 shipments, supported by staple categories such as deodorants and dry shampoos. Household care, however, is projected to log a 4.42% CAGR thanks to entrenched hygiene routines and retailer shelf reallocation favoring aerosol disinfectants. The household cleaners aerosol can market will benefit from nitrogen-powered platforms that address flammability concerns in big-box logistics. Automotive and industrial demand tracks the aging vehicle fleet, while pharmaceutical inhalers maintain steady volume under FDA oversight.

Substitution threats weigh on personal care as stick-and-pump innovations tout propellant-free credentials. Conversely, continuous-spray surface cleaners reduce labor time for janitorial crews, cementing aerosol’s value proposition and supporting category growth beyond pandemic urgency.

Geography Analysis

Mexico is emerging as the fastest-expanding node in the aerosol cans market with a 3.71% projected CAGR. Multinationals are funding greenfield plants near Monterrey and Guadalajara to hedge against tariff uncertainty and to supply domestic demand that rose on the back of rapid urbanization. Proximity to U.S. consumer markets enables cost-efficient cross-border logistics under the United States-Mexico-Canada Agreement.

Canada’s share is comparatively modest but enjoys stability from provincial alignment with U.S. HFC regulations, which creates harmonized compliance pathways for fillers straddling both markets. Investment in automated sorting lines for aerosol scrap in Ontario is expected to lift recovery rates, supporting aluminum circularity goals.

The United States, while holding 81.27% of 2025 volume, faces maturing demand in core personal-care categories. Still, continued shift to low-GWP propellants and lightweight cans should sustain incremental tonnage. Legacy infrastructure in the Midwest and Southeast ensures high-throughput capability, but escalating metal prices and tightening waste-management rules could redirect future expansion south of the border where cost structures remain favorable.

Competitive Landscape

Crown Holdings and Ball Corporation are intensifying lightweighting programs, with Ball rolling out ReAl alloy lines across three U.S. plants in 2025. Ardagh Metal Packaging upgraded its Chicago facility with digital printing presses that enable rapid artwork changes for limited-edition runs, catering to indie fragrance houses seeking shelf differentiation. Trivium Packaging entered a joint venture with a Mexican filler to build a dedicated bag-on-valve line scheduled to come online in 2026, signaling confidence in compressed-gas momentum.

Silgan Holdings launched an online configurator that lets mid-sized brands design actuators, collars, and color schemes in a single interface, shortening concept-to-shelf timelines from six months to three. Smaller specialists, notably CCL Container, exploit gaps in pharmaceutical delivery by offering ultra-light monobloc cans that cut freight weight 20%, an advantage for e-commerce fulfillment. Private-equity interest in regional converters rose in 2025 as investors targeted bolt-on acquisitions that expand niche capabilities, hinting at further consolidation.

Although the top five suppliers controlled roughly 70% of capacity in 2025, customer diversification and specialty niches keep pricing pressure intact. Brand owners increasingly dual-source to mitigate tariff and logistics risks, forcing can makers to maintain cost competitiveness while meeting bespoke sustainability metrics.

North America Aerosol Cans Industry Leaders

Crown Holdings Inc.

Ball Corporation

CCL Container Inc. (CCL Industries Inc.)

Ardagh Group S.A.

Mauser Packaging Solutions (BWAY Holding Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Trivium Packaging broke ground on a USD 120 million aluminum can plant in Nuevo León, Mexico, designed to produce 500 million lightweight aerosol bodies annually.

- November 2025: Ball Corporation completed a USD 75 million retrofit of its Illinois line, adding ReAl alloy capability and boosting recycled content to 90%.

- September 2025: Aptar Group introduced a next-generation bag-on-valve actuator that locks automatically after use, targeting pharmaceutical topical sprays.

- June 2025: Crown Holdings signed a purchase agreement for 20,000 metric tons of low-carbon aluminum from Rio Tinto, securing supply for lightweight aerosol programs.

North America Aerosol Cans Market Report Scope

The North America Aerosol Cans Market Report is Segmented by Material Type (Aluminium, Steel, Tinplate, Plastic, Other Material Type), Can Type (One-piece, Two-piece, Three-piece), Propellant Type (Compressed Gas, Liquefied Gas, Bag-on-Valve), Capacity (Less Than 100 ml, 101-300 ml, 301-500 ml, More Than 500 ml), End-User Industry (Personal Care and Cosmetics, Household Care, Automotive and Industrial, Healthcare and Pharmaceutical, Food and Beverage, Paints and Varnishes, Other End-User Industry), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Volume (Units).

By Material Type

| Aluminium |

| Steel |

| Tinplate |

| Plastic |

| Other Material Type |

By Can Type

| One-piece (Monobloc) |

| Two-piece |

| Three-piece |

By Propellant Type

| Compressed Gas | |

| Liquefied Gas | Hydrocarbon |

| DME | |

| Other Liquefied Gas | |

| Bag-on-Valve |

By Capacity (ml)

| Less Than 100 |

| 101-300 |

| 301-500 |

| More Than 500 |

By End-User Industry

| Personal Care and Cosmetics |

| Household Care |

| Automotive and Industrial |

| Healthcare and Pharmaceutical |

| Food and Beverage |

| Paints and Varnishes |

| Other End-User Industry |

By Country

| United States |

| Canada |

| Mexico |

| By Material Type | Aluminium | |

| Steel | ||

| Tinplate | ||

| Plastic | ||

| Other Material Type | ||

| By Can Type | One-piece (Monobloc) | |

| Two-piece | ||

| Three-piece | ||

| By Propellant Type | Compressed Gas | |

| Liquefied Gas | Hydrocarbon | |

| DME | ||

| Other Liquefied Gas | ||

| Bag-on-Valve | ||

| By Capacity (ml) | Less Than 100 | |

| 101-300 | ||

| 301-500 | ||

| More Than 500 | ||

| By End-User Industry | Personal Care and Cosmetics | |

| Household Care | ||

| Automotive and Industrial | ||

| Healthcare and Pharmaceutical | ||

| Food and Beverage | ||

| Paints and Varnishes | ||

| Other End-User Industry | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large will North American demand for aerosol cans be by 2031?

Shipments are forecast to reach 5.34 billion units by 2031, reflecting a 3.06% CAGR from 2026.

Which end-use segment is expanding the fastest?

Household care sprays are projected to grow at 4.42% CAGR as disinfectant use becomes a routine habit.

What material leads can construction today?

Aluminum retains 63.26% of 2025 volume because of recyclability and pressure tolerance advantages.

Why are compressed-gas propellants gaining ground?

AIM-Act limits on HFCs and retailer fire-safety policies are steering fillers toward nitrogen and air systems despite higher can pressures.

Where are new production plants being built?

Multinationals are adding greenfield capacity in Mexico to hedge tariff risk and serve United States export corridors.

How concentrated is supplier power in the region?

The top five manufacturers control roughly 70% of capacity, placing the market in a moderately concentrated bracket.

Page last updated on: