Nordics Geospatial Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

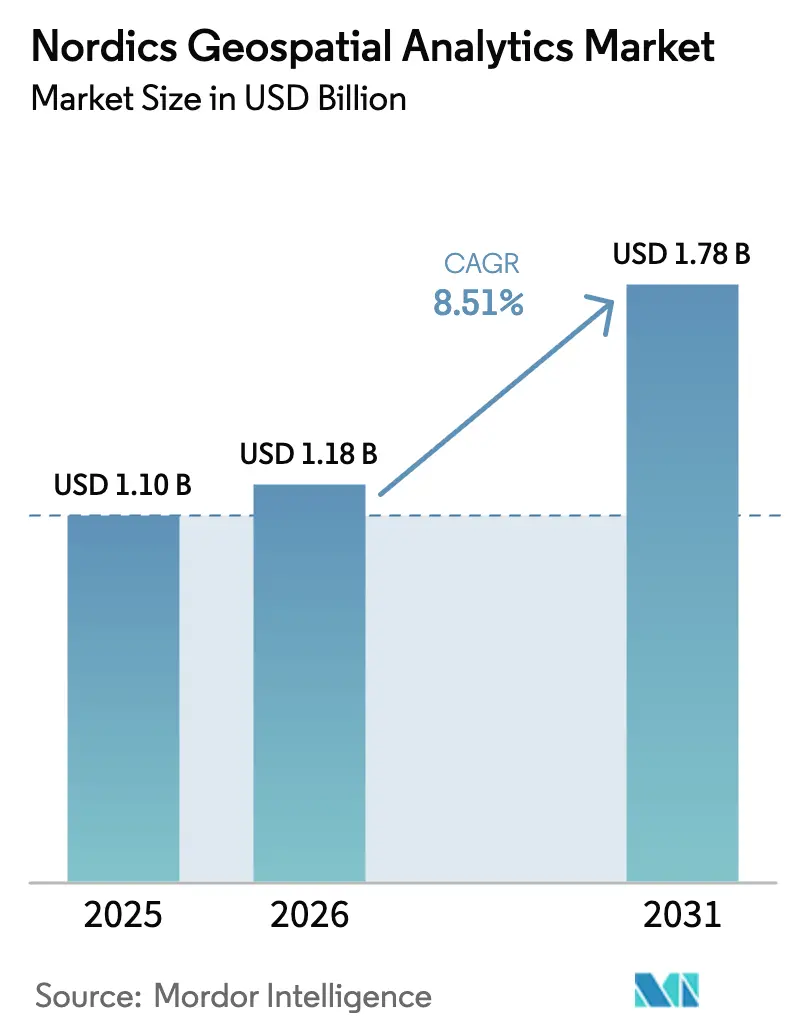

| Base Year Market Size (2025) | USD 1.10 Billion |

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 8.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordics Geospatial Analytics Market Analysis by Mordor Intelligence

The Nordics geospatial analytics market size is projected to expand from USD 1.1 billion in 2025 and USD 1.18 billion in 2026 to USD 1.78 billion by 2031, registering a CAGR of 8.51% between 2026 to 2031. Rapid uptake of Copernicus Sentinel imagery, Galileo High Accuracy Service and European GNSS‐enabled positioning tools continues to lower data-acquisition costs, while municipal digital-twin programs and offshore-wind marine-spatial-planning needs amplify demand for advanced location-intelligence workflows. Cloud processing of terabyte-scale satellite data, rising defense adoption of commercial synthetic-aperture-radar (SAR) constellations and grid-digitization initiatives across the Nordic synchronous area are further widening the addressable opportunity. Competitive dynamics are consolidating around a handful of platform vendors that bundle software, data and consulting, even as service specialists localize around fragmented municipal procurement rules. Collectively, these forces keep momentum firmly in favor of the Nordics geospatial analytics market despite privacy, Arctic-coverage and talent bottlenecks.

Key Report Takeaways

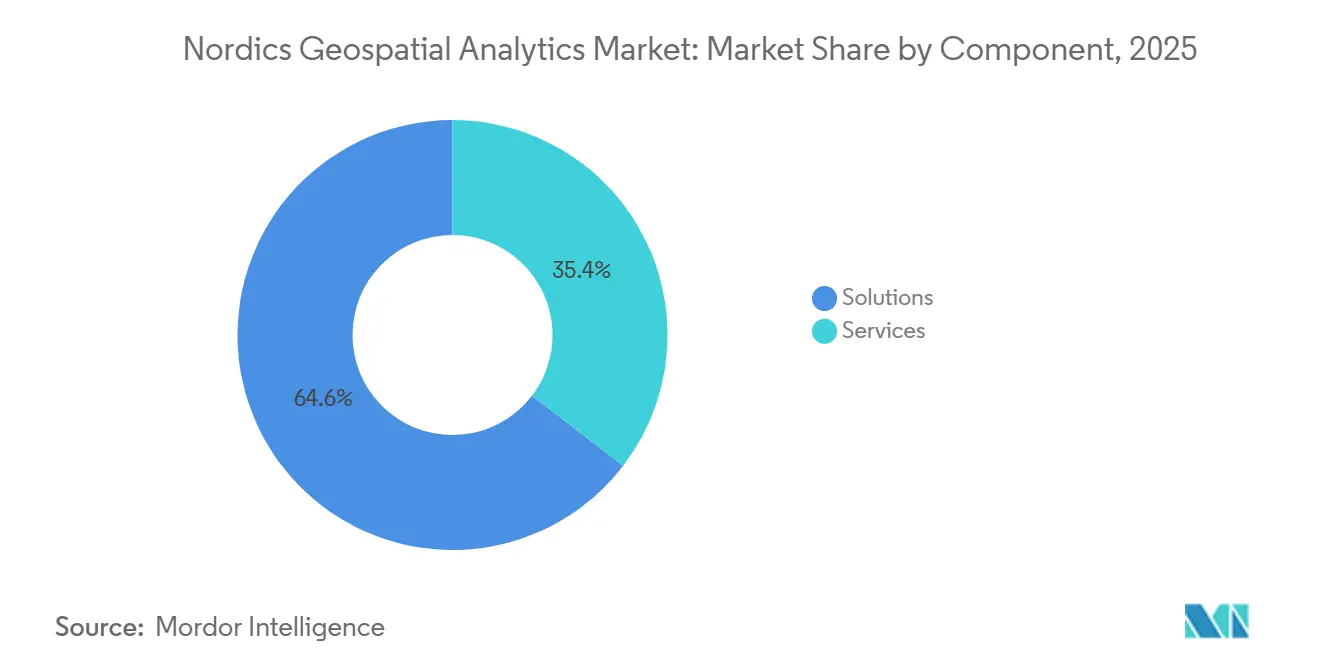

- Solutions led with 64.60% of the Nordics geospatial analytics market share in 2025, while Services is forecast to accelerate at an 11.30% CAGR through 2031.

- Geo-visualization held 33.40% of the Nordics geospatial analytics market share in 2025 revenue, yet Spatial AI and Predictive Modelling are projected to advance at a 12.78% CAGR.

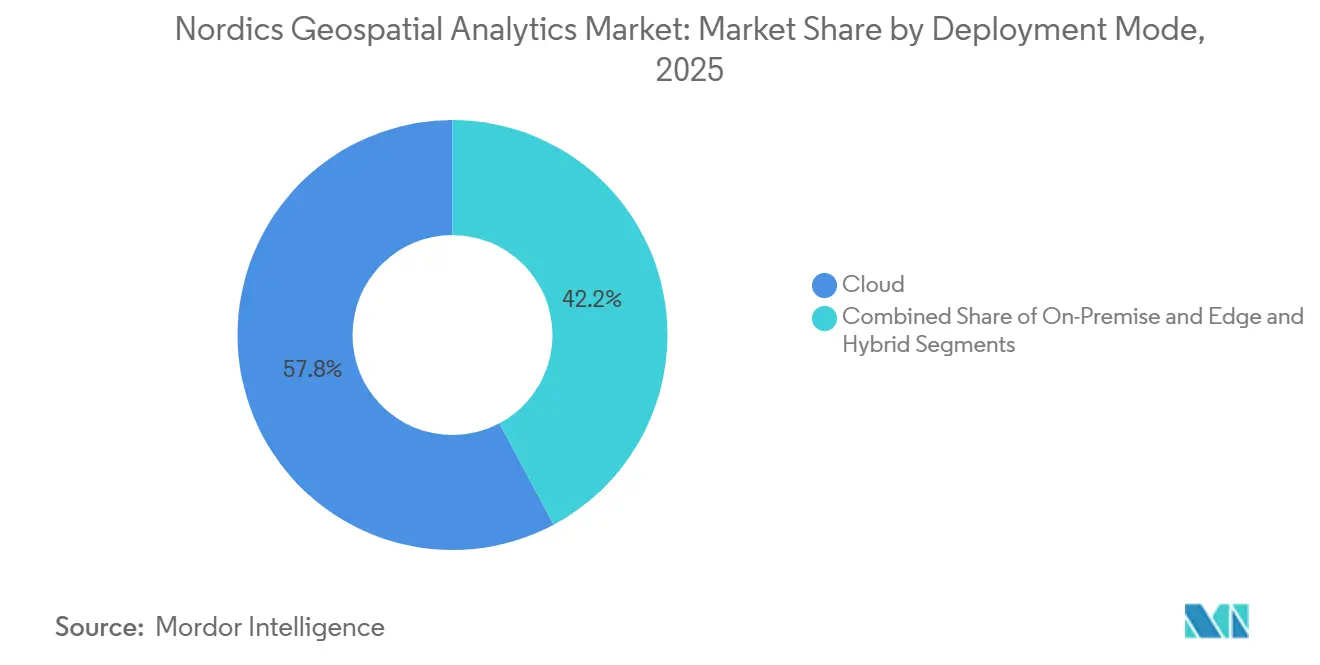

- Cloud deployments commanded 57.80% of the Nordics geospatial analytics market share in 2025, spending and are poised to grow at a 12.20% CAGR, driven by real-time streaming and bulk Sentinel processing.

- Environmental Monitoring and Climate Analysis accounted for 19.40% of the Nordics geospatial analytics market share in 2025 sales, whereas Urban Planning and Digital Twins are expected to rise at a 12.60% CAGR.

- Sweden captured 34.30% of the Nordics geospatial analytics market size in 2025; Finland is forecast to record the fastest 11.80% country-level CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordics Geospatial Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open Geodata and NSDI Maturity | +1.8% | Denmark and Norway lead; Sweden GDPR-constrained; Finland GTK exemplar | Medium term (2-4 years) |

| EU Copernicus and EGNSS Uptake | +2.1% | Global enablement, Nordic early-adopter advantage in Arctic maritime and forestry | Long term (≥4 years) |

| City-Scale Digital Twins and Smart Mobility | +1.5% | Stockholm, Gothenburg, Uppsala, Helsinki, Copenhagen | Medium term (2-4 years) |

| Energy Transition and Grid Digitization | +1.4% | Statnett NOK 150-200 billion program, Nordic Grid Development Plan EUR 36 billion | Long term (≥4 years) |

| Offshore Wind Build-Out and Marine Planning | +1.2% | Norway 30 GW, Denmark North Sea, Sweden Baltic Sea | Medium term (2-4 years) |

| Arctic Connectivity Enabling Data Flows | +0.9% | Norway and Finland Arctic regions, spillover to Iceland geothermal monitoring | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Open Geodata And NSDI Maturity Lower Adoption Friction

Open-access policies continue to erode licensing barriers and expand the geospatial analytics market in the Nordics. Denmark’s Kortforsyningen portal generated DKK 3.5 billion (USD 0.53 billion) in social value by 2016, proving that free foundational datasets unlock downstream commercial use.[1]Danish Ministry of Finance, “The Value of Danish Address Data,” eng.sdfe.dk Norway’s Spatial Data Act mandates open government geodata, enabling start-ups to prototype without up-front acquisition costs. Finland’s Geological Survey openly provides bedrock and mineral layers, catalyzing exploration analytics. Sweden, by contrast, still recovers costs through Lantmäteriet licensing, pushing vendors toward project-based bundles that hide data fees inside consulting engagements.[2]Lantmäteriet, “National Cadastral and Topographic Data Licensing,” lantmateriet.se Divergent regimes, therefore, shape the mix of software and services in each country.

EU Copernicus/EGNSS Uptake Expands Downstream Analytics

Copernicus delivers petabytes of multispectral and SAR scenes at no license cost, fuelling forestry carbon accounting, crop yield modeling, and Arctic sea-ice tracking across the Nordics.[3]European Union Space Programme Agency, “EUSPA EO and GNSS Market Report,” euspa.europa.eu Galileo’s free decimeter-level High Accuracy Service underpins precision agriculture and autonomous-vehicle pilots without the need for expensive RTK subscriptions. Trafikverket trained a self-supervised model on hundreds of terabytes of Copernicus and aerial imagery, slashing annotation effort for road-condition surveys. With EUSPA projecting global GNSS revenue to rise from EUR 199 billion in 2023 to EUR 492 billion by 2031, Nordic players enjoy a multiplier on service demand generated by publicly funded space infrastructure.

City-Scale Digital Twins And Smart Mobility Programs

Helsinki’s 3D+ twin refreshes nightly from cadastral and transport feeds, letting planners stress-test flood and heat scenarios in near real-time.[4]Virtual City Systems, “Helsinki 3D+ Digital Twin Platform,” virtualcitysystems.de Gothenburg’s Virtual Gothenburg uses Unreal Engine to shorten approval cycles through immersive walk-throughs. Regions in Skåne and Uppsala rely on ArcGIS Urban to balance densification with access to green space. The shared architecture, geographic information systems fused with building-information models, creates integration complexity that municipalities outsource, nudging the Nordics geospatial analytics market toward faster-growing Services revenue.

Energy Transition And Grid Digitization Initiatives

Statnett plans to invest NOK 150-200 billion (USD 14.4-19.2 billion) in grid upgrades, all modeled through geospatial route optimization, impact analysis, and dynamic-line-rating simulations. The Nordic Grid Development Plan earmarks EUR 36 billion (USD 40.7 billion) for 15 000 kilometers of new lines.[5]Nordic Energy Regulators, “Nordic Grid Development Plan 2024,” nordicenergyregulators.org GE Vernova’s cloud-native GridOS fuses GIS layers with SCADA feeds to boost capacity 10-15% without steel in the ground. Flow-based market coupling further demands real-time spatial modeling of cross-border constraints, reinforcing cloud adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mixed Data Access Regimes and Licensing Constraints | -1.2% | Sweden GDPR-constrained, fragmented municipal policies | Short term (≤2 years) |

| Fragmented Municipal Procurement Profiles | -0.9% | 1 053 Nordic municipalities with varied budgets and maturity | Medium term (2-4 years) |

| Arctic Backhaul Coverage Gaps | -0.6% | Above 70° N in Norway, Finland and Iceland | Long term (≥4 years) |

| Shortage of Production-Grade GeoAI Talent | -0.7% | All countries, acute in Finland and Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mixed Data Access Regimes And Licensing Constraints

Sweden’s cost-recovery model and GDPR rules raise barriers to fusing cadastral, demographic, and mobility data, dampening location-intelligence use cases versus fully open Denmark. Municipal utilities often impose bespoke sharing agreements on network geometries, forcing vendors into one-off negotiations that erode scalability. Cross-border corridors such as Rail Baltica expose further incompatibilities, slowing multinational deployments. Until harmonized standards mature, the Nordics geospatial analytics market must navigate a patchwork that adds time and legal cost to every expansion sprint.

Fragmented Municipal Procurement And Profiles

The region’s 1 053 municipalities vary widely in staffing and budget, tilting tenders toward incumbents with local footprints. Smaller towns favor on-premise servers for data-sovereignty reasons, delaying migration to cost-efficient SaaS. Sitowise’s five-year Digiroad contract illustrates labor-intensive engagements that restrict scale economies. This two-speed demand, innovative metros versus resource-constrained rural councils, slows interoperable digital-twin federation across borders, curbing the full network effect of a unified Nordics geospatial analytics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominance Yields To Services Integration Demand

Solutions held 64.60% of the Nordics geospatial analytics market share in 2025, underpinned by Hexagon AB, Environmental Systems Research Institute, and Trimble licensing. Yet Services is set to grow at an 11.30% CAGR, reflecting municipal need for data-integration, cloud-migration, and model-operations expertise.

In the medium term, the Nordics geospatial analytics market size for Services is projected to outpace Solutions as clients seek turnkey digital-twin life-cycle support. Consolidation is accelerating: Sitowise added LandPro and VVS-Kompetens to push Swedish headcount to 250 and annual sales to EUR 31 million (USD 35.0 million). Metria’s SEK 650 million (USD 62.4 million) sale to Sikri Holding likewise signals private-equity appetite for annuity-style geospatial consultancies.

By Analysis Type: Geo-Visualization Lead Challenged By Spatial AI Surge

Geo-visualization contributed 33.40% of 2025 revenue, buoyed by immersive planning tools that win stakeholder buy-in. However, Spatial AI and Predictive Modelling are forecast to climb at 12.78% CAGR as machine-learning models transition from research to operations.

Spatial AI platforms for forestry, road maintenance, and offshore wind inspection reduce field costs by up to 60%, accelerating deployment across Scandinavia. The Nordics geospatial analytics market size attributed to Spatial AI is forecast to swell as Trafikverket’s foundation model, Husqvarna’s mower routing, and Terra Labs’ biomass estimation gain traction. Older surface- and network-analysis workstreams remain vital but face price commoditization amid the diffusion of open source.

By Deployment Mode: Cloud Supremacy Reinforced By Edge-Hybrid Arctic Use Cases

Cloud claims 57.80% of 2025 spending and is growing fastest at 12.20% CAGR. SaaS eliminates the need for infrastructure capital, while Sentinel downloads and streaming emergency feeds scale effortlessly on hyperscale platforms.

Edge and hybrid designs still matter. Arctic maritime surveillance and offshore-wind O&M need sub-second latency that satellite backhaul cannot yet guarantee, despite Space Norway’s NOK 2.8 billion (USD 268.8 million) broadband mission. Vendors, therefore, deploy containerized analytics near sensors, federated with cloud cores for long-horizon reporting, keeping the Nordics geospatial analytics market flexible across divergent latency envelopes.

By Application: Environmental Monitoring Lead Gives Way To Digital-Twin Urbanization

Environmental Monitoring and Climate Analysis made up 19.40% of the 2025 turnover. Yet Urban Planning and Digital Twins are projected to rise at 12.60% CAGR, fueled by 3D city models that fuse BIM with GIS to test climate-adaptation strategies.

Transport optimization leverages Galileo H-A S accuracy to shave fleet kilometers, while disaster-response agencies tap near-real-time SAR change detection for flood and wildfire mapping. Defense intelligence demand spikes on the back of ICEYE’s EUR 1.7 billion (USD 1.92 billion) German contract, bolstering the Nordics geospatial analytics industry in security segments.

Geography Analysis

Sweden captured 34.30% of Nordics geospatial analytics market share in 2025, anchored by Hexagon’s global headquarters, Lantmäteriet’s mature cadastre, and clustered digital-twin pilots in Stockholm, Gothenburg, Uppsala, and Skåne. The country’s cost-recovery data pricing tempers growth, but deep vendor presence and sophisticated city programs keep volumes high.

Finland is the fastest-growing geography, forecast to grow at a 11.80% CAGR. ICEYE’s EUR 150 million (USD 169.5 million) Series E, 62-satellite constellation, and German defense deal lift national visibility. Sitowise’s multi-year FTIA contract, combined with Gispo’s open-source expertise, widens the services funnel, boosting Finnish suppliers' share of the Nordics geospatial analytics market.

Norway benefits from a 30 GW offshore wind pipeline, Statnett’s grid upgrades, and the Arctic Satellite Broadband Mission, channeling expenditure toward marine spatial planning, energy, and defense analytics. Denmark, with its fully open Kortforsyningen portal, remains the lowest-friction market for start-ups, especially in marine and built-environment modeling. Iceland, though small, continues to specialize in geothermal and volcanic workflows using Copernicus SAR.

Competitive Landscape

The market is moderately concentrated. Hexagon AB and Environmental Systems Research Institute collectively control a significant portion of platform licensing, while services remain fragmented among regional consultancies. Hexagon’s recent product launches, acquisitions, and planned spin-offs illustrate vertical specialization. ICEYE’s valuation and defense contracts underscore growing demand for commercial SAR feedstock that downstream analytics firms can monetize.

Service-led roll-ups continue: Sitowise’s Nordic expansion, Tietoevry’s embedding of GIS into ERP projects, and Norkart’s dominance in municipal portals showcase localization as a hedge against global-vendor scale. White-space remains in Arctic, marine, and production-grade GeoAI operations, where latency, data scarcity, and talent gaps still deter rivals.

Nordics Geospatial Analytics Industry Leaders

Hexagon AB

Environmental Systems Research Institute, Inc. (Esri)

Trimble Inc.

Tietoevry Oyj

HERE Global B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: ICEYE signed a EUR 1.7 billion German Armed Forces SAR tasking and analytics contract valid through 2030.

- February 2026: Geomatikk Sweden confirmed handling ~200 000 excavation cases annually on Metria maps.

- January 2026: ICEYE expanded its Ukraine Ministry of Defence SAR monitoring agreement.

- December 2025: ICEYE closed a EUR 150 million Series E round, lifting valuation to EUR 2.4 billion.

Nordics Geospatial Analytics Market Report Scope

Geospatial Analytics adds timing and location to conventional data types and creates data visualizations. Maps, graphs, statistical data, and cartograms showing historical or current change may be included in these visualizations. A clearer picture of events is possible by means of this further context. This would allow predictions to be executed faster, simpler, and more accurately.

The Nordics geospatial analytics market is segmented by type (surface analysis, network analysis, geovisualization), end user vertical (agriculture, utility and communication, defence and intelligence, government, mining and natural resources, automotive and transportation, healthcare, real estate, and construction). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions |

| Services |

| On-Premise |

| Cloud |

| Edge and Hybrid |

| Surface Analysis |

| Network Analysis |

| Geo-visualization |

| Spatial AI and Predictive Modelling |

| Other Types |

| Urban Planning and Smart Cities |

| Transportation and Logistics Optimization |

| Environmental Monitoring and Climate Analysis |

| Disaster Management and Emergency Response |

| Agriculture and Precision Farming |

| Energy and Utilities Management |

| Defense, Intelligence, and Public Safety |

| Business Intelligence and Location Intelligence |

| Natural Resources and Mining |

| Other Applications |

| Sweden |

| Norway |

| Denmark |

| Finland |

| Iceland |

| By Component | Solutions |

| Services | |

| By Deployment Mode | On-Premise |

| Cloud | |

| Edge and Hybrid | |

| By Analysis Type | Surface Analysis |

| Network Analysis | |

| Geo-visualization | |

| Spatial AI and Predictive Modelling | |

| Other Types | |

| By Application | Urban Planning and Smart Cities |

| Transportation and Logistics Optimization | |

| Environmental Monitoring and Climate Analysis | |

| Disaster Management and Emergency Response | |

| Agriculture and Precision Farming | |

| Energy and Utilities Management | |

| Defense, Intelligence, and Public Safety | |

| Business Intelligence and Location Intelligence | |

| Natural Resources and Mining | |

| Other Applications | |

| By Country | Sweden |

| Norway | |

| Denmark | |

| Finland | |

| Iceland |

Key Questions Answered in the Report

What is the projected value of the Nordics geospatial analytics market in 2031?

The market is expected to reach USD 1.78 billion by 2031, expanding at an 8.51% CAGR from 2026.

Which segment will grow fastest through 2031?

Services is forecast to post an 11.30% CAGR as municipalities outsource digital-twin and integration work.

Why is Finland the fastest-growing country in the region?

ICEYE’s satellite expansion and large defense contracts, along with Sitowise’s transport projects, lift Finnish demand to an 11.80% CAGR.

How are open data policies shaping adoption?

Denmark’s and Norway’s open-access regimes lower entry barriers, spurring wider commercial use of location intelligence.

What technological trend is disrupting traditional geo-visualization?

Spatial AI and Predictive Modelling is accelerating at 12.78% CAGR as deep-learning models move from pilot to production in forestry, transport and energy monitoring.

Which application is gaining ground on environmental monitoring?

Urban Planning and Digital Twins is rising at a 12.60% CAGR as Scandinavian cities embed BIM-to-GIS workflows for climate-resilient development.

Page last updated on: