Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Iceland Facility Management Market is Segmented by Service Type (Hard Services, and Soft Services), Offering Type (In-House, and Outsourced), and End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, and Other End-User Industries).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

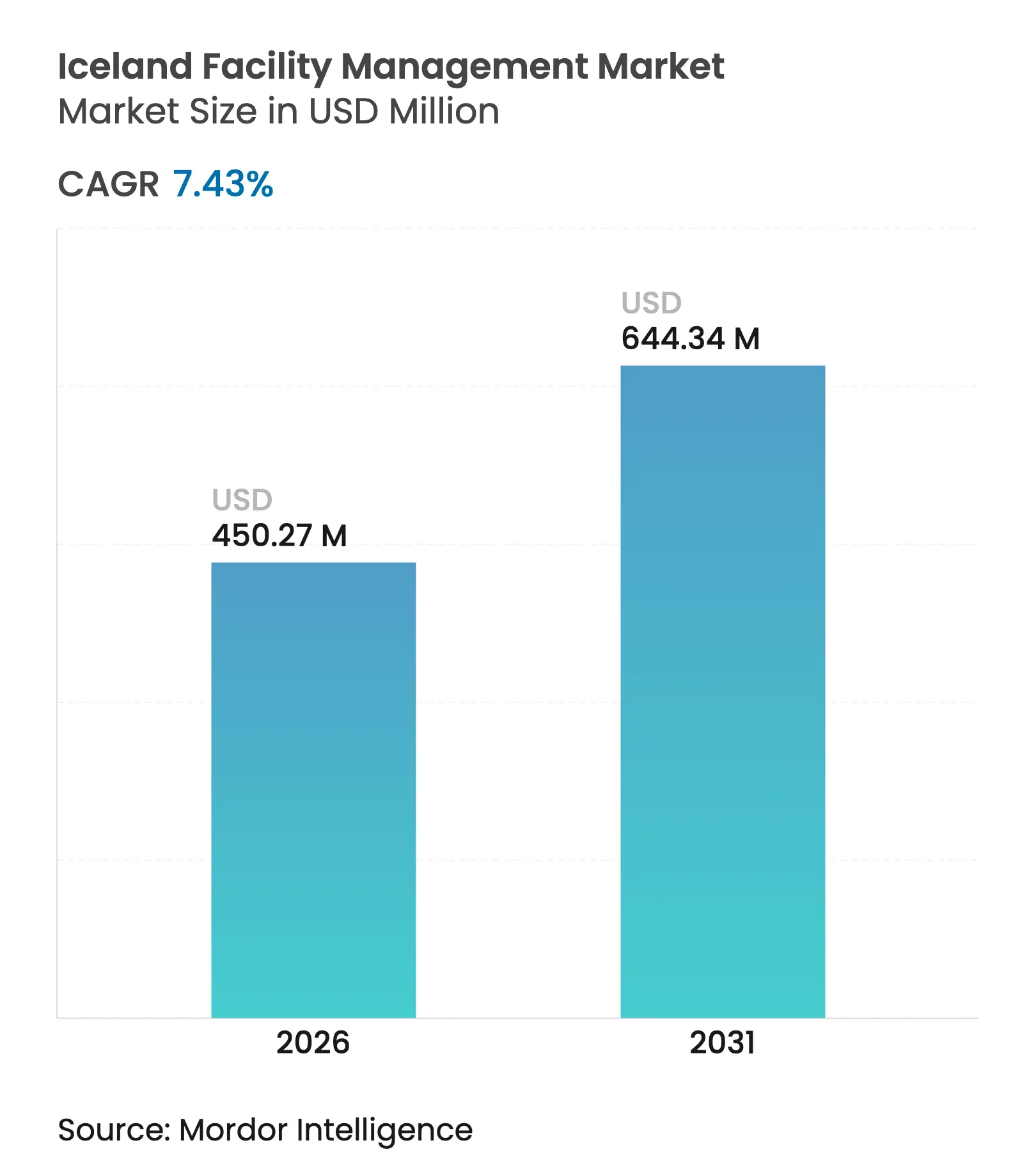

| Market Size (2026) | USD 450.27 Million |

| Market Size (2031) | USD 644.34 Million |

| Growth Rate (2026 - 2031) | 7.43 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Iceland facility management market size in 2026 is estimated at USD 450.27 million, growing from 2025 value of USD 419.15 million with 2031 projections showing USD 644.34 million, growing at 7.43% CAGR over 2026-2031. This growth in the Iceland facility management market rests on three converging themes: mandatory life-cycle assessments for all building permits issued after September 2025, surging digital government services that demand smarter buildings, and a nationwide four-day workweek that is redefining workplace support needs. Geothermal baseload heating has historically kept energy overheads down, yet rising electricity tariffs are now pushing property owners to deploy predictive maintenance and IoT-enabled HVAC upgrades, widening revenue streams for the Iceland facility management market. Hard services retained the greatest allocation of spend in 2024, but a surge in security, catering, and cleaning contracts is propelling soft-service revenue at the fastest clip, while chronic technician shortages continue to steer occupiers toward long-horizon outsourcing agreements in the Iceland facility management market.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Technological advancements in building-management systems

Technological advancements in building-management systems

| +1.8% | National, concentrated in the Reykjavik metropolitan area | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

National, concentrated in the Reykjavik metropolitan area

|

Impact Timeline

:

Medium term (2-4 years)

|

Growth of the real-estate sector

Growth of the real-estate sector

| +1.5% | National, with early gains in Reykjavik, Akureyri, Keflavik | Long term (≥ 4 years) | |||

Increasing emphasis on green-building practices

Increasing emphasis on green-building practices

| +1.2% | National, driven by LCA requirements | Short term (≤ 2 years) | |||

Growing demand for soft FM services

Growing demand for soft FM services

| +1.0% | National, concentrated in commercial districts | Medium term (2-4 years) | |||

Rise in energy costs driving demand for energy-efficient

FM solutions

Rise in energy costs driving demand for energy-efficient

FM solutions

| +0.8% | National, particularly rural areas without geothermal access | Long term (≥ 4 years) | |||

Aging building stock requiring refurbishment and lifecycle

FM services

Aging building stock requiring refurbishment and lifecycle

FM services

| +0.9% | National, concentrated in older urban areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Technological advancements in building-management systems

Early 2024 saw utility Veitur roll out ETOS® sensor networks across transformers, illustrating how live data shrinks maintenance downtime and cuts fault-finding costs, thereby strengthening the Iceland facility management market.[1]Rúnar Svavar Svavarsson, “Why Are You Digitizing Your Transformers?” Reinhausen, reinhausen.com Buildings magazine identified 2025 as a national inflection point for smart HVAC integration thanks to maturing AI tools that self-optimize mechanical loads. Norwegian vendor ClevAir’s SaaS platform entered Iceland with case-proven energy savings of up to 40% in commercial premises, attracting landlords eager to hit carbon-neutral pledges. Adoption accelerates, yet legacy structures often lack backbone cabling, prompting consultancies to package retrofit kits, cybersecurity audits, and 24/7 monitoring into long-term contracts. In aggregate, smarter assets are raising lifetime service values and locking clients into the Iceland facility management market for extended periods.

Growth of the real-estate sector

Islandsbanki reported that home prices in greater Reykjavík rose 0.36% month-on-month in March 2025, confirming market stabilization that unfreezes renovation budgets and spurs demand for the Iceland facility management market. Hilton’s commitment to a 70-room Akureyri Curio Collection hotel and a 170-key Reykjavík flagship doubles the chain’s footprint and embeds multi-year FM contracts for housekeeping, MEP oversight, and LEED-aligned reporting. Bloomberg projected visitor arrivals to climb to 2.5 million in 2026, requiring expanded airport, retail, and logistics capacity—each a steady client for the Iceland facility management market. Construction materials saw heightened volatility in late 2024, steering developers toward FM providers that hedge prices and manage long-lead imports. With housing supply breaching 4,000 listings in April 2025, new residential blocks are handing over to professional managers, reinforcing a forward pipeline for the Iceland facility management market.

Increasing emphasis on green-building practices

Parliament passed a decree mandating life-cycle assessments for every building permit issued after 1 September 2025, forcing owners to document embodied carbon and resource efficiency from day one. The Nordic Swan Ecolabel simultaneously tightened energy-demand ceilings to 10% below nearly zero-energy codes and imposed stringent chemical inventory rules. Landlord Reitir’s ‘Græn leiga’ (Green Lease) aligns tenant behavior with owner performance metrics, using digital dashboards to share live energy use and recycling statistics, an approach rapidly copied across the Iceland facility management market. Sævarhöfði 31, Reykjavík’s flagship circular-economy retrofit, reused structural steel to slash embodied carbon by up to 50%, demonstrating new technical services around selective demolition and materials tracing. Heightened ESG audits by pension funds and GRESB raters have therefore baked low-carbon reporting into master FM agreements, differentiating vendors across the Iceland facility management market.

Growing demand for soft FM services

Nationwide acceptance of a four-day workweek reshaped shift scheduling, compressing support windows while maintaining output targets, thereby propelling soft-service packages in the Iceland facility management market. Securitas Iceland expanded analytics-based guarding and remote patrols, helping the parent group lift technology revenue to 32% of its global mix in 2023. Luxury hotels like ION Adventure incorporated local lava rock décor, requiring bespoke cleaning protocols and specialized material preservatives that premium FM firms now bundle as value-added services. Healthcare estates adopted BIM-ready maintenance workflows; Verkís’s hospital projects layer commissioning data into cloud portals accessed by onsite engineers and offsite experts, raising uptime and regulatory compliance. Collectively, these shifts intensified competition and created new vertical expertise niches inside the Iceland facility management market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Labor-market constraints and skills shortage

Labor-market constraints and skills shortage

| -1.2% | National, acute in Reykjavik, and construction hubs | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-1.2%

|

Geographic Relevance

:

National, acute in Reykjavik, and construction hubs

|

Impact Timeline

:

Short term (≤ 2 years)

|

Economic fluctuations and inflationary pressures

Economic fluctuations and inflationary pressures

| -0.8% | National, with regional variations | Medium term (2-4 years) | |||

A fragmented regulatory environment is delaying

standardized FM certifications

A fragmented regulatory environment is delaying

standardized FM certifications

| -0.6% | National, affecting cross-border operations | Long term (≥ 4 years) | |||

Limited digital infrastructure in older facilities is hampering

the adoption of smart FM tools

Limited digital infrastructure in older facilities is hampering

the adoption of smart FM tools

| -0.4% | Concentrated in older urban areas and rural regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Labor-market constraints and skills shortage

The Directorate of Labour obliges employers to prove domestic scarcity before issuing one-year foreign-worker permits, extendable only twice, limiting rapid workforce expansion for the Iceland facility management market. AOSH mandates Safety Officers above head-count thresholds, inflating compliance costs and widening gaps in qualified technician supply.[2]Administration of Occupational Safety and Health, “Employer Obligations,” vinnueftirlitid.is Edstellar flagged IT and construction trades as the most in-demand for 2025; supply lags fuel wage inflation and overtime premiums that erode FM profit margins. Shorter workweeks increase daily intensity, compelling firms to adopt AI-based rostering tools that remain underutilized in small enterprises. Government reskilling grants exist, but pipeline talent will not offset retirements before 2027, tempering growth momentum in the Iceland facility management market.

Economic fluctuations and inflationary pressures

The OECD expected Icelandic GDP to grow 1.4% in 2025, yet indicated inflation will stay over target until mid-2026, squeezing discretionary maintenance budgets and jolting utilities pricing. Material-price volatility drove developers to seek FM partners skilled in index-linked contracts, but cash-flow risk still shifted some refurbishment into phased rollouts, softening near-term orders for the Iceland facility management market. Residential listings surged and homes lingered longer on the market, constraining landlords’ cash positions and trimming optional upgrades in the short run. Continuous volcanic uplift near Svartsengi diverted state funds toward emergency infrastructure, delaying some planned public-sector retrofits. Together, these cyclical pressures shave basis points off the otherwise robust expansion trajectory of the Iceland facility management market.

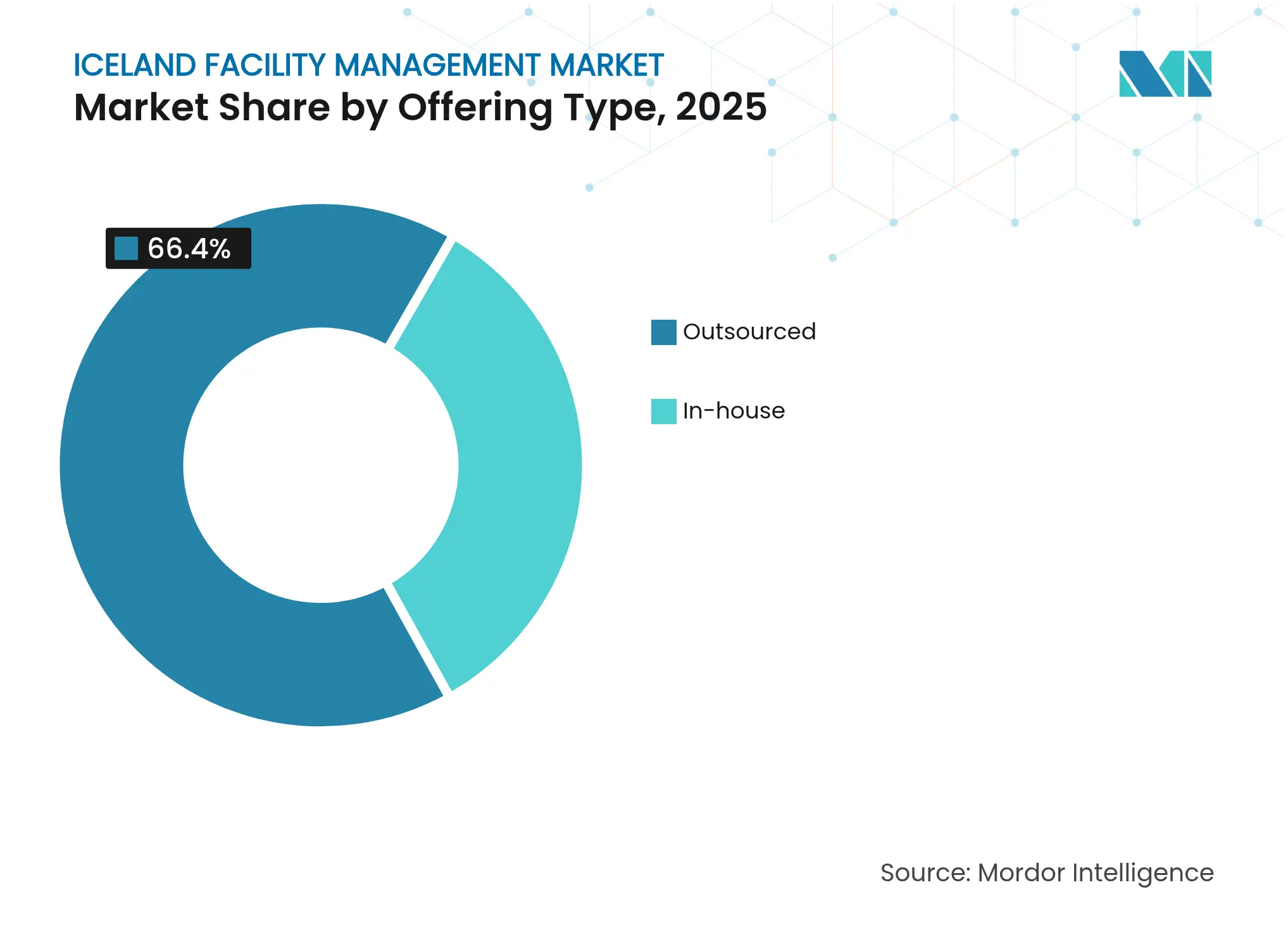

By Offering Type: Outsourcing supremacy, hybrid evolution

Outsourced solutions captured 66.40% of Iceland's facility management market share in 2025 as enterprises grappling with skills shortages shifted toward integrated providers promising single-invoice simplicity. ISS extended its global mandate with Barclays in May 2024, supplying hard, soft, and workplace-experience services, an agreement worth roughly 2.5% of total group revenue and regarded locally as proof of integrated value. Outsourcing’s 8.22% forecast CAGR rests on analytics-driven staffing; providers now crunch occupancy, weather, and events data to match crew sizes, optimizing cost and sustainability metrics throughout the Iceland facility management market.

In-house teams held 33.60% spend in 2025, concentrated in defense, justice, and critical infrastructure, where security sensitivity outweighs cost concerns. The Government Offices Services department preserved onsite engineers for cabinet buildings yet outsourced grounds maintenance to local SMEs, signalling a pragmatic hybrid path. Universities aligned with this model, contracting external experts for elevator refurbishments while managing day-to-day janitorial staff internally. Bundled FM contracts—where two or three services are grouped—are emerging as an intermediate choice, particularly in medium-sized municipalities seeking to test outsourcing without relinquishing full control, foreshadowing gradual migration to external suppliers across the Iceland facility management market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Commercial anchor, institutional surge

Commercial buildings generated 38.30% of the Iceland facility management market size in 2025, buoyed by data-center campuses that exploit Iceland’s cool ambient temperatures and 100% renewable grid power for low-cost cooling. Retail parks adopted omnichannel logistics layouts, adding robotics maintenance and last-mile docking-bay cleaning to contract scopes. Urban office landlords reconfigured floor plates into activity-based zones compatible with shorter workweeks, necessitating dynamic soft-service schedules. These factors cement commercial real estate’s leading weight in the Iceland facility management market.

Institutional and public-infrastructure estates are forecast to post a 7.62% CAGR. Agency FSRE controls 1.9 million m² of state property and is standardizing service-level agreements that reward uptime, pushing bidders toward analytics-rich proposals. Hospital campus expansions such as Landspítali embed BIM-linked asset registries, locking vendors into data-driven preventive maintenance. Transportation projects, including nationwide ramp installations for universal access, are creating recurring inspection workflows. The healthcare subset deserves mention: Verkís’s fire-protection engineering and energy-optimization designs have become reference models for new clinics, opening specialized revenue lanes in the Iceland facility management market.

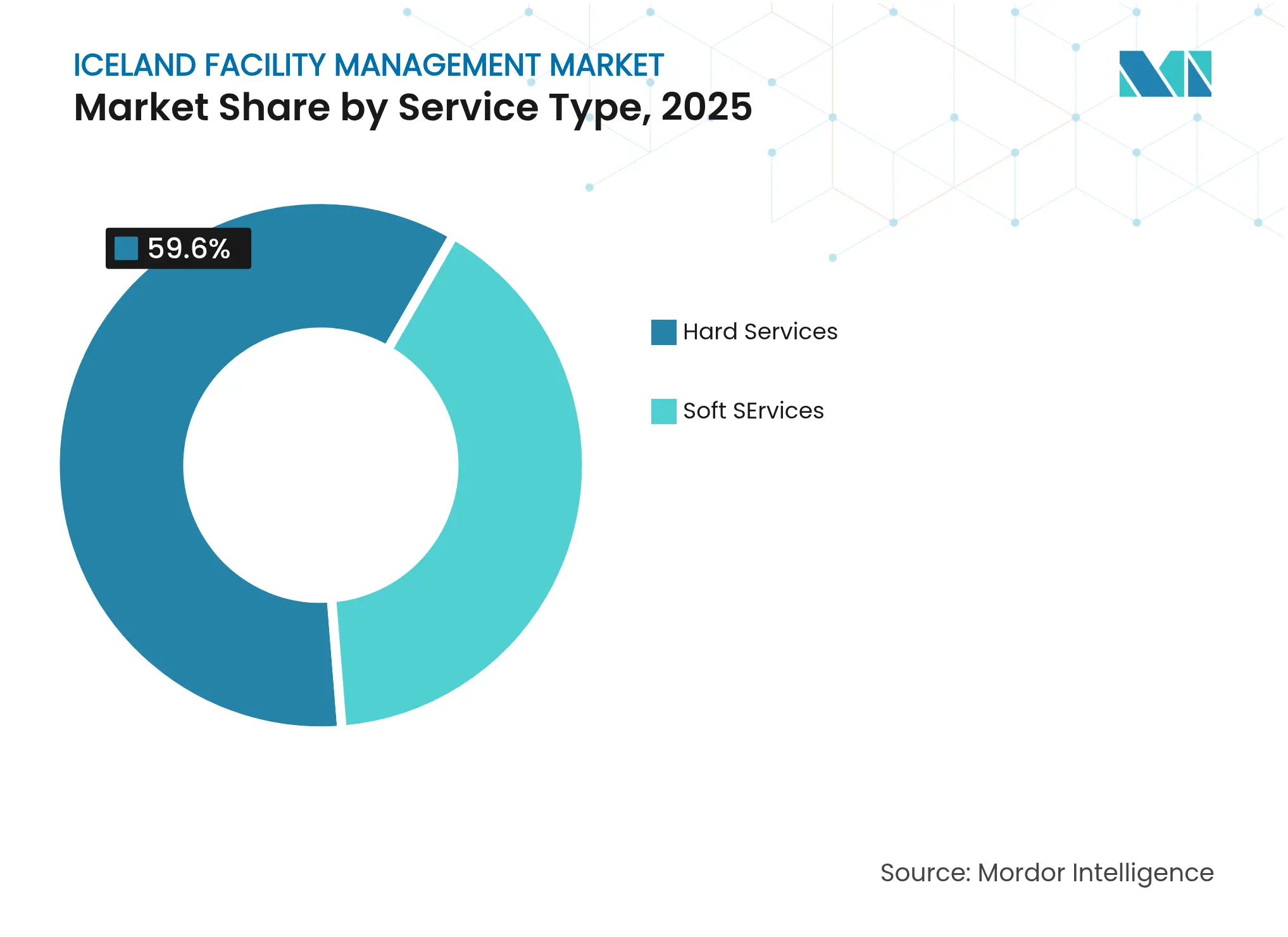

By Service Type: Technical dominance, service-mix evolution

Hard services retained 59.60% revenue share in 2025, underpinned by compulsory HVAC, fire-safety, and electrical inspections dictated by AOSH, which guarantees a continual maintenance workload inside the Iceland facility management market. Veitur’s rollout of grid-sensor technology highlights a shift to predictive rather than scheduled interventions, creating higher-margin analytics packages for FM operators. Asset-management consultancies now embed corrosion monitoring for geothermal pipelines, a critical differentiator in Iceland’s harsh sub-arctic climate. Insurance carriers have begun discounting premiums for properties running certified smart-monitoring platforms, bolstering adoption and deepening the hard-service moat in the Iceland facility management market.

Soft services, however, are slated for a 7.95% CAGR from 2026 to 2031. Cleaning contractors leverage Diversey’s Internet of Clean to track chemical use and indoor-air particulates, aligning with Nordic Swan benchmarks and elevating transparency for occupiers. Security vendors fused CCTV analytics with drone sweeps in remote industrial parks to offset staff shortages. Office-support providers introduced hybrid concierge desks that toggle between physical reception and chatbot after-hours assistance, monetizing digital add-ons at higher margins. Catering firms pivoted to modular service lines that scale with fluctuating headcounts, integrating local produce to match ESG pledges. This breadth of innovation is accelerating share capture for soft services in the Iceland facility management market.

Note: Segment shares of all individual segments available upon report purchase

Reykjavík’s metropolitan footprint accounted for about 64.35% of sector spend in 2025. Government ministries, Iceland’s largest hospital system, and prime hospitality assets cluster downtown, collectively embedding high-frequency preventive maintenance into the Iceland facility management market. Digital Iceland’s push to centralize citizen services requires always-on, cyber-secure buildings, propelling IoT uptake and on-call engineering. Hilton’s forthcoming 170-key CBD property stipulates LEED Gold readiness, raising expected FM sophistication. Retrofitting pre-2000 apartments with smart meters and heat-pump interfaces accelerated following municipal carbon budgets that reward energy savings, further stimulating the Reykjavík tranche of the Iceland facility management market.

Regional Iceland—areas outside the capital—recorded double-digit home-price inflation in 2024, driving developers to complete mixed-use hubs in Akureyri and Selfoss. Hilton’s 70-room countryside hotel in Akureyri brings global brand standards to a rural setting and requires year-round FM support despite seasonal occupancy peaks, broadening the coastal share of the Iceland facility management market. Geothermal coverage gaps in Westfjords and East Iceland attract subsidy-backed heat-pump retrofits, creating specialized service calls for firms brave enough to manage weather-related access issues. At the same time, new aquaculture parks like First Water’s USD 89 million salmon farm impose biosecurity, water-filtration, and waste-handling protocols hitherto unseen in local portfolios.

Distinct industrial nodes punctuate the island. Climeworks’ Mammoth direct-air-capture plant near Hellisheiði came online in 2025 with a 36,000 tpa capacity, demanding corrosion-resistant piping, moisture-control systems, and mineral-injection infrastructure, complexity that only a handful of FM firms can manage. Aluminum smelters in Reyðarfjörður and Hvalfjörður require refractory-lining audits and crane servicing under high-humidity conditions. Recurrent uplift beneath Svartsengi geothermal fields informs emergency preparedness drills and redundant power back-ups that FM firms must orchestrate, sharpening the risk-management spine of the Iceland facility management market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

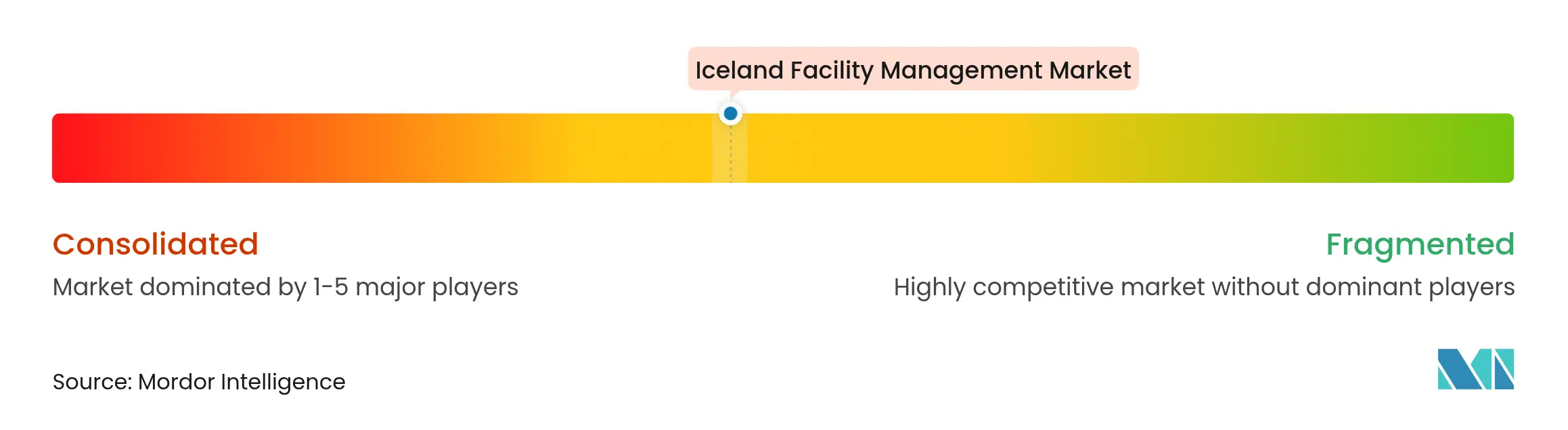

Market Concentration

The Iceland facility management market remains moderately consolidated: the five largest vendors controlled just over 40% of 2024 billings, leaving ample room for local specialists. ISS tops the league yet maintains a sub-15% share, while Securitas capitalizes on AI-enabled guarding to lock multi-year bank and airport contracts.[4]Securitas AB, “Annual and Sustainability Report 2023,” securitas.com Reitir differentiates via its Green Lease program, embedding energy dashboards for tenants and leveraging that data for cross-selling sustainability consulting. Diversey’s Internet of Clean delivers remote consumable monitoring that slashes site visits, a high-tech edge appealing to rural hotels and fish-processing plants.

Engineering consultancies Verkís and EFLA pivoted from design to whole-life stewardship, bundling commissioning, quarterly audits, and regulatory reporting into annuity-style contracts. White-space opportunities lie in geothermal O&M, carbon-capture utilities, and circular-construction advisory—high-barrier niches where local know-how outmuscles global scale. M&A chatter intensified after John Bean Technologies’ 2024 takeover of Marel, signaling appetite for technology-rich bolt-ons that provide immediate skilled-labor access. Given rising ESG compliance hurdles and digital-twin adoption, competitive success increasingly hinges on data analytics, certified sustainability expertise, and workforce-management software proficiency across the Iceland facility management market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Facility management confines multiple disciplines to ensure functionality, comfort, safety, and efficiency of any building by integrating people, place, process, and technology. While Hard services include physical and structural services like fire alarm system lifts, among others, soft services include cleaning, landscaping, security, and similar human-sourced services, providing a solution to end-users such as Commercial Buildings, Retail, Government, Public Entities, etc.

The Iceland facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.