Non-opioid Pain Patch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

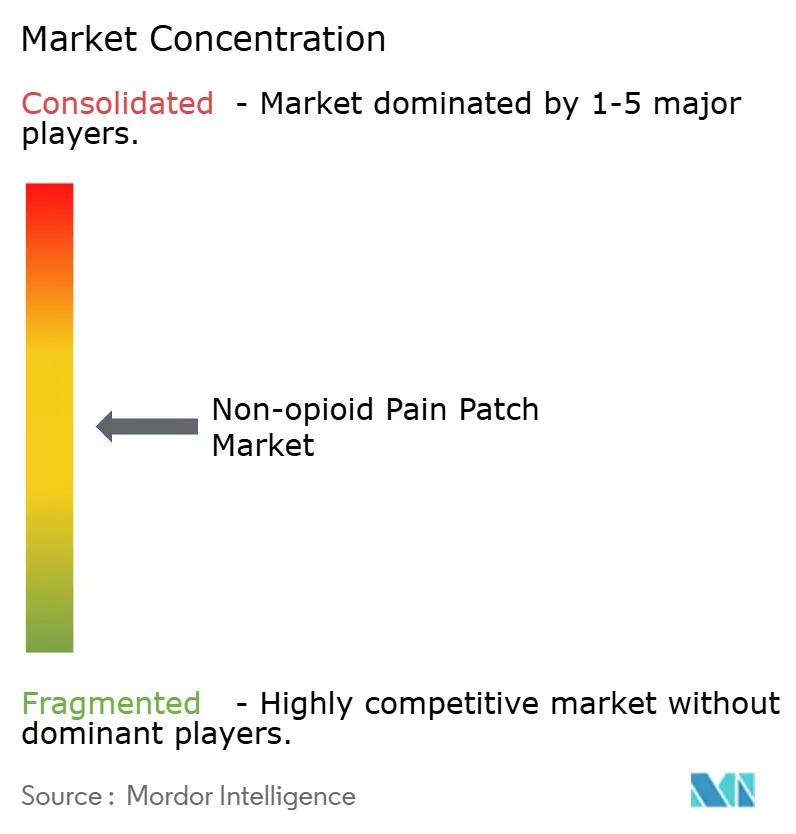

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-opioid Pain Patch Market Analysis by Mordor Intelligence

The Non-opioid Pain Patch market size is expected to grow from USD 1.89 billion in 2025 to USD 2 billion in 2026 and is forecast to reach USD 2.62 billion by 2031 at 5.57% CAGR over 2026-2031. Growth is rooted in the global shift away from opioid prescribing, steady innovation in transdermal delivery, and widening reimbursement for topical analgesics. New microneedle-enhanced systems are raising drug-delivery efficiency while large matrix formats preserve cost advantages for established brands. Online pharmacies are reshaping purchase journeys, letting manufacturers build direct bonds with patients and sharpen pricing transparency. Consolidation continues: Grünenthal’s Qutenza licensing deal with Apotex broadened reach in Canada,[1]Source: Grünenthal GmbH, “Apotex Licenses Canadian Rights to Qutenza,” kommunikasjon.ntb.no while smaller firms such as Enokon Medical posted 87% clinical efficacy with natural-ingredient patches that appeal to safety-conscious users.[2]Source: Enokon Medical, “The Rise of Natural Pain Relief Patches,” enokonmedical.com

Key Report Takeaways

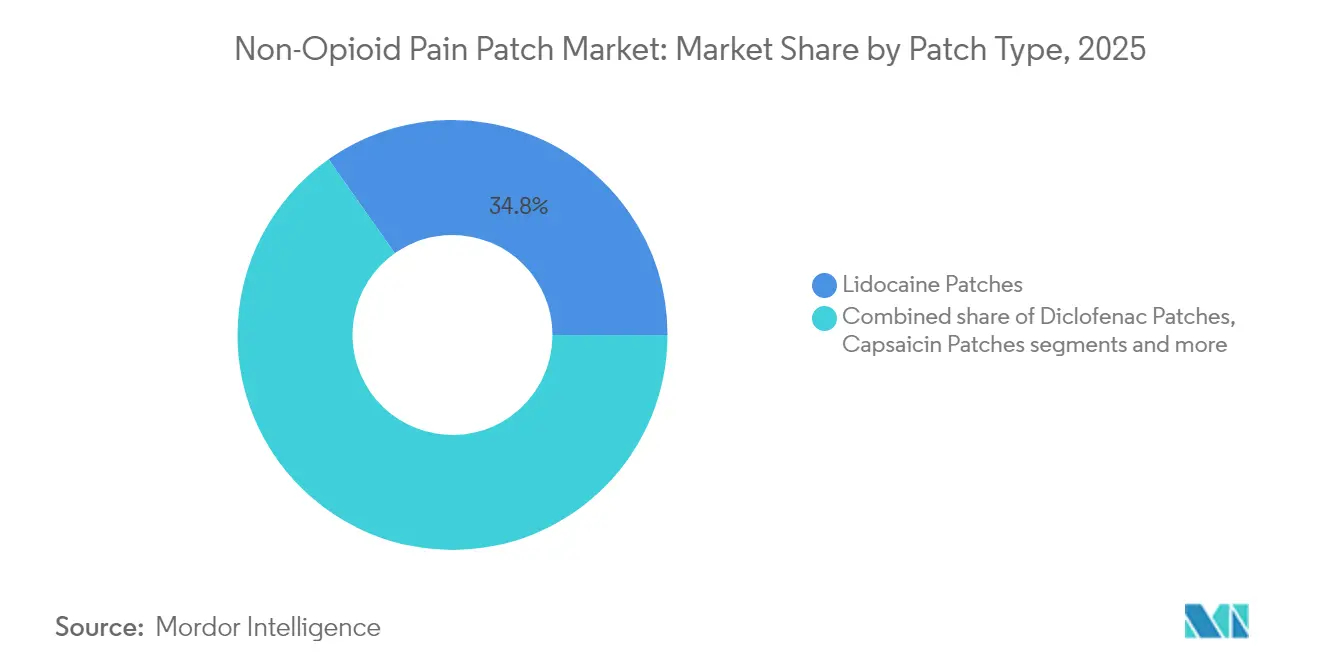

- By patch type, lidocaine patches held 34.78% of the non-opioid pain patch market share in 2025; capsaicin patches are projected to expand at a 6.74% CAGR to 2031.

- By technology, matrix patches led with 47.92% revenue share in 2025, while microneedle-enhanced patches record the highest projected CAGR at 6.88% through 2031.

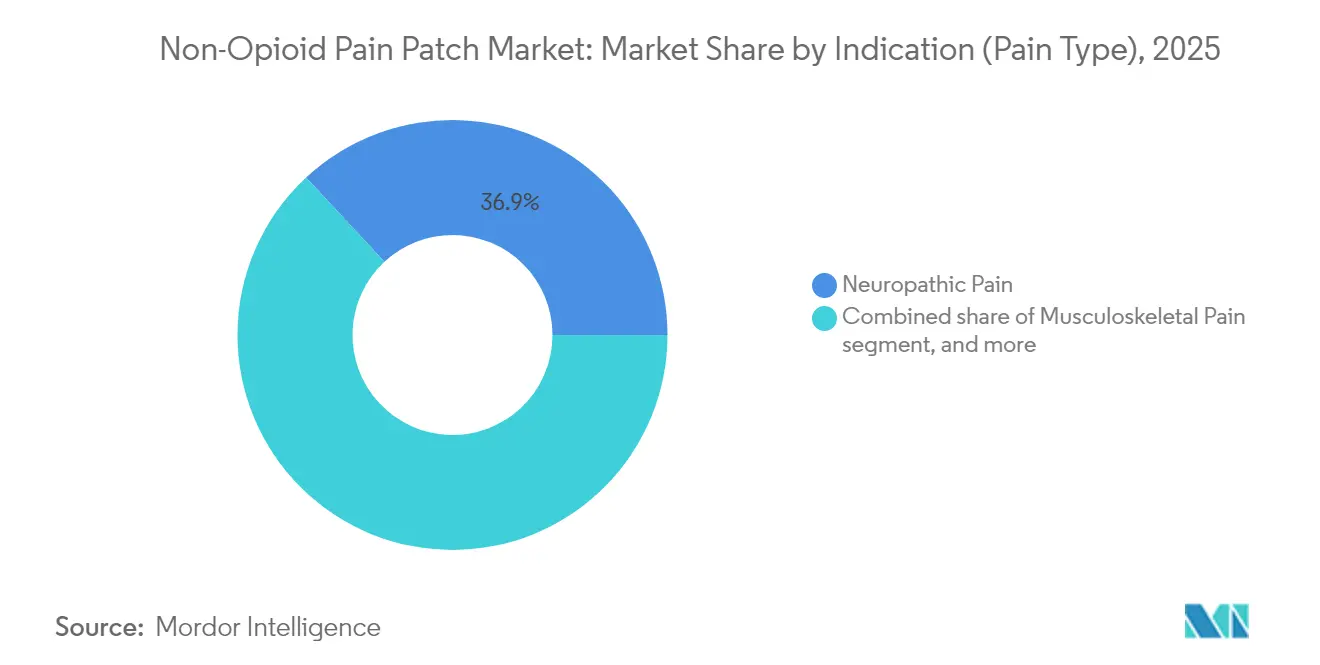

- By indication, neuropathic pain accounted for 36.92% of the non-opioid pain patch market size in 2025 and cancer-associated pain is advancing at a 6.61% CAGR through 2031.

- By distribution channel, retail pharmacies held 44.32% share of the non-opioid pain patch market size in 2025; online pharmacies are forecast to grow at 7.05% CAGR to 2031.

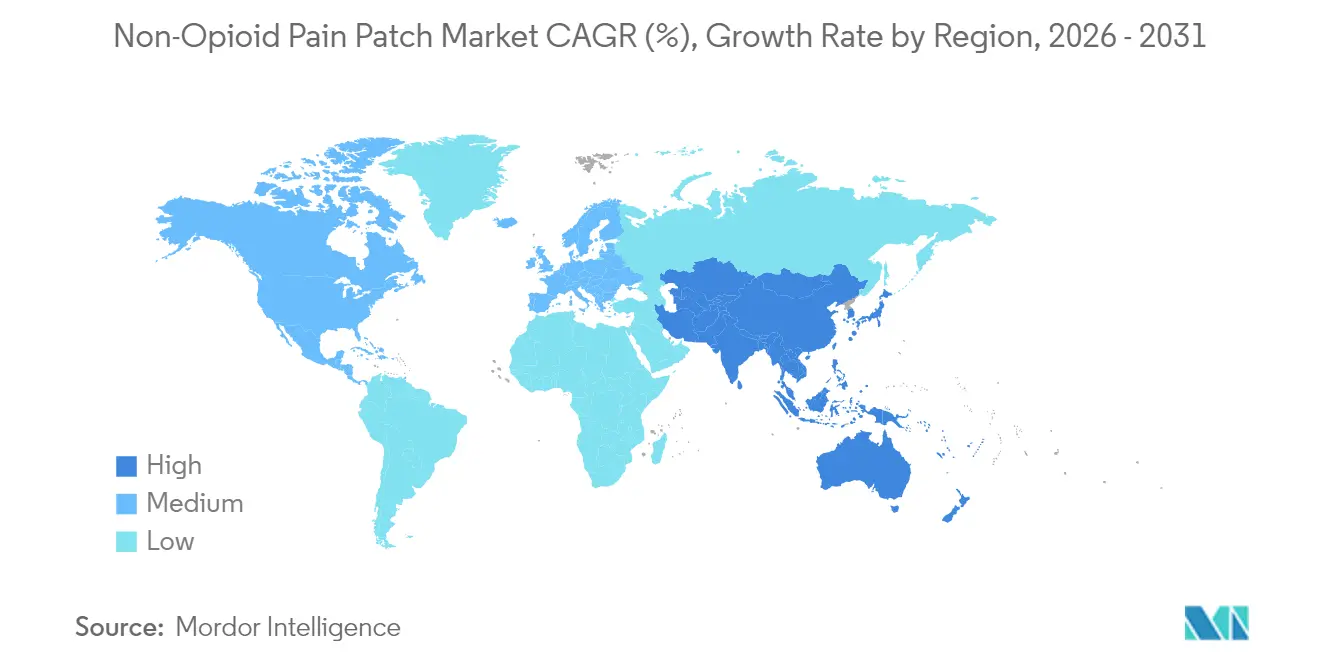

- By geography, North America commanded 39.02% of the non-opioid pain patch market share in 2025, whereas Asia Pacific is set to rise at a 7.55% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Non-opioid Pain Patch Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of pain-related disorders | +1.2% | Global, higher in North America and Europe | Long term (≥ 4 years) |

| Technological advances in transdermal delivery | +1.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Growing consumer preference for OTC analgesics | +0.8% | Global, early in North America and Europe | Medium term (2-4 years) |

| E-commerce and direct-to-consumer expansion | +1.0% | North America, Europe, urban APAC | Short term (≤ 2 years) |

| Regulatory shift toward non-opioid analgesics | +1.4% | North America, spillover to Europe | Medium term (2-4 years) |

| Surge in sports injuries | +0.6% | Global, higher in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising burden of pain-related disorders

More than 1.5 billion people live with chronic pain, and aging societies push neuropathic conditions to the forefront. Diabetes alone is set to affect 783 million adults by 2045, swelling the pool of patients with diabetic peripheral neuropathy. Productivity losses tied to unmanaged pain top USD 300 billion each year in the United States. Payers and clinicians therefore favor localized, low-risk treatments that keep patients active and reduce reliance on systemic drugs.

Technological advances in transdermal delivery

Fourth-generation patches now integrate microneedles that bypass the tough outer skin layer and release analgesics in a controlled manner. Polymer-based microneedle arrays with porous coatings deliver three-times higher loads than metal designs and extend pain-relief duration. Such gains address prior limits for hydrophilic drugs and cut application frequency, raising patient adherence.

Growing consumer preference for OTC analgesics

Heightened awareness of opioid risks and common NSAID side effects steers shoppers toward self-care solutions with minimal systemic exposure. Branded OTC patches highlight drug-in-adhesive builds, longer wear time, and skin-friendly ingredients to win repeat purchase. The trend also encourages premium pricing for advanced formulations with menthol or natural extracts.

E-commerce and direct-to-consumer expansion

Online pharmacies grow faster than any other channel, letting users compare prices and read peer reviews before buying. Subscription models offer refill reminders and bundle pain-management education. Manufacturers leverage digital campaigns to target niche groups such as marathon runners or post-surgical patients, accelerating brand visibility at lower cost than in-store promotions.

Restraints Impact Analysis of Non-opioid Pain Patch Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity vs low-cost oral drugs | -0.9% | APAC, Africa, Latin America | Medium term (2-4 years) |

| Complex regional regulatory hurdles | -0.7% | Global, higher in Europe and Japan | Short term (≤ 2 years) |

| Competition from alternative non-opioid therapies | -0.6% | North America, Europe | Medium term (2-4 years) |

| Humidity-linked shelf-life issues | -0.4% | ASEAN, tropical regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price sensitivity versus low-cost oral analgesics

In many emerging countries a branded patch costs five-to-ten times more than generic ibuprofen tablets. Limited insurance coverage prompts patients to opt for the cheapest immediate relief. India’s drug-makers hope to bridge this gap by launching generic patches as patents expire on over 300 products by 2030, yet near-term affordability hurdles stay in place.

Complex regional regulatory hurdles

Skin-sensitization studies demanded by the European Medicines Agency and Japan’s PMDA often exceed FDA requirements, stretching development cycles and budgets. Smaller firms struggle to fund parallel submissions, slowing global roll-outs. Microencapsulation and hypoallergenic adhesives help cut irritation but still require region-specific testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Non-opioid Pain Patch Market Segment Analysis

By Patch Type:

Lidocaine commands share while capsaicin acceleratesLidocaine products held the largest slice of the non-opioid pain patch market size at 34.78% in 2025, supported by decades of clinical use and broad third-party payment. Strong safety and minimal systemic absorption make lidocaine popular in elderly populations, which are most affected by post-herpetic neuralgia. Grünenthal and Scilex broadened acceptance by delivering thinner, high-adhesion systems that permit exercise and showering without detachment.

Capsaicin patches expand at a 6.74% CAGR, the fastest among patch types, because high-concentration formulations produce multi-month relief from diabetic neuropathy and chemotherapy-induced pain. Older patients achieved statistically significant pain score reductions in a 2025 study that compared capsaicin to standard care. Diclofenac and ketoprofen hold niche roles in musculoskeletal injury management, while natural-ingredient patches from Enokon create a small but visible frontier for chemical-free therapy seekers.

By Technology:

Matrix retains lead; microneedle systems surgeMatrix construction accounted for 47.92% of the non-opioid pain patch market share in 2025. Manufacturers prefer the format because it supports a wide range of APIs at reasonable production cost. Hospitals value the steady plasma levels delivered over 12-24 hours.

Microneedle-enhanced patches post the highest growth at 6.88% CAGR, capitalizing on their ability to open microchannels that improve permeation of hydrophilic molecules like gabapentin. A 2024 carbon-master microneedle prototype raised delivery efficiency threefold compared with earlier metal units. Reservoir systems stay relevant in long-wear chronic treatment, and drug-in-adhesive sheets secure cosmetic appeal with ultra-thin designs. Smart pH-responsive microneedle arrays represent the next wave, adjusting dose to local inflammation levels.

By Indication (Pain Type):

Neuropathic pain leads opportunitiesNeuropathic disorders represented 36.92% of the non-opioid pain patch market size in 2025. Post-herpetic neuralgia and diabetic neuropathy remain the most common uses because they benefit from localized, sustained delivery. New guidelines in major oncology centers now recommend capsaicin patches against chemotherapy-induced neuropathy, expanding eligible patient pools.

Cancer-associated pain posts a 6.61% CAGR and stands as the fastest-growing indication, fueled by longer cancer survival and a need to control neuropathic flares without opioids. Musculoskeletal pain retains a substantial share thanks to high sports injury rates, while postoperative pain scripts grow after hospitals adopt topical protocols to cut opioid days.

By Distribution Channel:

Retail leads, online disruptsRetail pharmacies captured 44.32% of non-opioid pain patch market share in 2025, offering immediate access and pharmacist counseling. Chain stores run loyalty programs that bundle patches with heat wraps or topical gels to deepen wallet share.

Online pharmacies grow at 7.05% CAGR as broadband coverage widens. Platforms showcase detailed video demos, ingredient lists, and user feedback that improve confidence among first-time buyers. Pain Relief Technologies markets its Kailo patch exclusively online, offering 60-day money-back guarantees and installment plans that lower entry cost. Hospital pharmacies continue to serve prescription-only formulations, especially for new neurological diagnoses, while omnichannel pilots link in-store pick-up with home-delivery autoship.

Geography Analysis

North America Non-opioid Pain Patch Market

North America contributed 39.02% of 2025 revenue, reflecting widespread awareness of opioid addiction risks and generous payer coverage for topical analgesics. The 2025 NOPAIN Act funds non-opioid postoperative options, driving hospital uptake of capsaicin and lidocaine systems. U.S. FDA approvals of novel non-opioid treatments also boost clinician confidence FDA.

APAC Non-opioid Pain Patch Market

Asia Pacific posts the fastest regional CAGR at 7.55% through 2031. Japan’s super-aged society faces high rates of post-herpetic neuralgia, and reimbursement committees increasingly reimburse capsaicin 8% patches for long-term relief. In China and India growth hinges on price negotiation; domestic contract manufacturers prepare low-price generics that could widen access once global patents expire.

EMEA, LATAM and ASEAN Non-opioid Pain Patch Market

Europe holds a solid share with strong chronic-pain management frameworks but slower growth because the EMA demands extra skin-sensitization tests. Germany, the United Kingdom, and France incentivize e-prescriptions, easing digital pharmacy adoption. Latin America and the Middle East show moderate growth when private insurers reimburse branded patches in tier-one cities. Humid ASEAN climates challenge supply chains because high moisture shortens shelf life, prompting foil-laminated sachets and desiccant liners.

Regulatory Landscape

Non-opioid pain patches are typically regulated as drug-device combination products, so manufacturers need to align development, quality, and post-market controls across both drug and device requirements. In the United States, the FDA assigns a lead center using the Primary Mode of Action (PMOA) framework (21 CFR 3.2(m), and combination-product current good manufacturing practice integration under 21 CFR Part 4 helps shape inspection readiness and change control for constituent parts.

In Europe, requirements for medicinal products used with a medical device place emphasis on quality documentation expectations (EMA/CHMP/QWP/BWP/259165/2019). The EMA Combination Products Operational Group (COMBO) continues to convene to address lifecycle and regulatory coordination topics (with sessions noted in February 2026 and June 2026), which reinforces region-specific evidence demands for skin irritation or sensitization and device material changes, affecting global rollout sequencing and ongoing compliance for both patch developers and generic entrants.

Competitive Landscape

The non-opioid pain patch market shows moderate concentration. The key players of the market include Grünenthal, Scilex, Teva, Hisamitsu, and Endo. Grünenthal deepens penetration of its Qutenza capsaicin brand through co-promotion with Apotex in Canada, expanding formulary placements in hospital outpatient care. Scilex won share with ZTlido, a lidocaine 1.8% system that sticks through exercise and showering; retrospective claims data show 51.9% of users cut or stopped opioids within months.

Innovators pursue microneedle designs that support high-load gabapentin or combinations of lidocaine and menthol. Device-based entrants such as Kailo employ bioelectric fields rather than active drugs, yet still compete for the same consumer budgets. Midsize firms explore hybrid models that pair patches with digital companion apps for pain tracking and refill reminders.

White-space lies in advanced adhesion chemistries that tolerate perspiration, personalized dose packs based on digital pain diaries, and combination therapy that blends capsaicin with low-dose NSAIDs to attack multiple pain pathways. Cross-licensing and regional distribution deals are expected as multinational firms seek presence in high-growth APAC markets without building full infrastructure.

Non-opioid Pain Patch Industry Leaders

Hisamitsu Pharmaceutical Co. Inc.

Teva Pharmaceuticals Industries Ltd.

Veridian Healthcare

Sanofi

Endo International plc

- *Disclaimer: Major Players sorted in no particular order

Non-opioid Pain Patch Market Companies Covered in this Report

- Hisamitsu Pharmaceutical

- Endo International

- Scilex Pharmaceuticals (Sorrento Therapeutics)

- Teikoku Pharma USA / Teikoku Seiyaku Co.

- Teva Pharmaceutical Industries

- Averitas Pharma (Grünenthal)

- GlaxoSmithKline

- Sanofi

- Mylan (Viatris)

- IBSA Institut Biochimique

- Sparsha Pharma International Pvt. Ltd.

- Veridian Healthcare

- Amneal Pharmaceuticals

Market Opportunities and Future Outlook

Opioid-sparing pain management policies and payer coverage are creating whitespace for both prescription and OTC non-opioid patch portfolios, especially where hospitals and outpatient settings formalize non-opioid pathways. In North America, the NOPAIN Act provides a direct reimbursement tailwind for non-opioid alternatives in postoperative care, which supports broader protocol-level use of topical analgesic options alongside established lidocaine systems.

Differentiation is also shifting beyond conventional matrix formats toward higher-performance and more controllable delivery approaches, supporting line extensions and premium positioning. Recent research momentum in 2026 points to commercializable directions for adhesion-focused designs (such as suction-activated nanofibrous patch concepts) and next-generation microneedle systems that integrate monitoring functionality (including a KAUST wearable microneedle patch concept for real-time drug level tracking via smartphone connectivity). Alongside product innovation, the market offers an access-driven path through additional generic and authorized-generic entries in established patch categories, which can broaden affordability and increase retail and online pharmacy penetration without requiring changes to clinical practice patterns.

Recent Industry Developments in Non-opioid Pain Patch Market

- February 2026: Grünenthal partnered with Australia-based Clinect for exclusive rights to commercialize the Qutenza capsaicin patch in Australia. The deal extends Qutenza into another Asia-Pacific commercialization corridor using a local partner model. It is designed to support faster formulary and channel access without building a standalone footprint.

- April 2025: Transtimulation Research, Inc. received US FDA 510(k) clearance (K243613) for Patch-TEA (Model TRI-21), a Class II transcutaneous nerve stimulator indicated for pain relief. The clearance reinforces competitive pressure from device-based, non-drug patches in localized pain management. It also competes for consumer and clinician budgets.

- October 2024: Hisamitsu Pharmaceutical initiated clinical development of HP-3150, a diclofenac sodium transdermal patch, for chronic lower back pain in the United States. Advancing a new diclofenac patch candidate into US development expands pipeline breadth beyond lidocaine and capsaicin. It also signals continued investment in differentiated patch formats for high-prevalence musculoskeletal indications.

Non-opioid Pain Patch Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market includes factory-made, commercial transdermal pain patches that deliver non-opioid active ingredients through intact skin for pain relief, and that are sold through prescription and OTC channels.

Scope exclusions: Opioid-containing patches, experimental polymer films, and in-clinic compounded topical dressings are not counted.

Segments Covered in This Report

- By Patch Type

- Lidocaine Patches

- Diclofenac Patches

- Capsaicin Patches

- Ketoprofen Patches

- Other Patch Types

- By Technology

- Matrix Patches

- Reservoir Patches

- Drug-in-Adhesive Patches

- Microneedle-Enhanced Patches

- By Indication (Pain Type)

- Neuropathic Pain

- Musculoskeletal Pain

- Cancer-Associated Pain

- Others (Headache, Dental, Post-op)

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the medical and product boundaries, and to build a clean demand context for pain conditions that are commonly treated with topical patches. We relied on public sources such as the US FDA drug label database and safety communications, CDC opioid and pain related statistics, WHO health indicators, and OECD health expenditure and utilization datasets to anchor prevalence, treatment pathways, and policy direction.

To translate that context into market inputs, we also reviewed sources such as UN Comtrade trade statistics for relevant HS codes (where patch and topical categories are visible), peer reviewed articles indexed in PubMed for topical analgesic efficacy and adoption patterns, and national reimbursement and formulary references where available. Company annual reports, investor presentations, and reputable press were used to confirm product presence, launch timing, and channel shifts, and selective paid subscriptions were used only for company financials and patent intelligence. These examples are not exhaustive, and many other public documents were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on clinicians, pharmacists, distributors, and product or regulatory specialists so we could confirm which non-opioid patch types are actually used, and how buying shifts between prescription and OTC behavior. Since this is a global market, we made sure inputs were tested across the Americas, EMEA, and APAC, and then the assumptions were adjusted when local reimbursement, switching behavior, or availability looked meaningfully different.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 17% | APAC: 47% |

| Mid tier: 46% | Functional/Unit leaders: 25% | EMEA: 30% |

| Smaller Players: 21% | Managers: 58% | Americas: 23% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs the treated patient pool and patch usage by linking pain condition prevalence, physician preference for topical therapy, and typical patch consumption per user over a year. Those totals were then converted into value using country-level pricing logic, where list prices, common pack sizes, and channel mix (prescription versus OTC) were used to reflect what is actually paid in the market.

We then sanity-checked the totals using selective bottom-up approximations, such as rolling up visible brand revenues where disclosures exist, and cross-checking implied volumes against patch form-factor norms and shelf availability checks. The model is most sensitive to neuropathic and musculoskeletal pain burden, NSAID and lidocaine patch penetration, reimbursement coverage signals, OTC switching patterns, and inflation-adjusted ASP movement by geography.

For forecasting, we used scenario analysis supported by light regression-style relationships between demand and indicators such as aging population trends, opioid stewardship policies, and channel expansion for pharmacies, with the final growth path being confirmed through expert views gathered in interviews. Where bottom-up evidence was thin in smaller countries, we filled gaps using proxy ratios from comparable markets and then revalidated the implied per-capita usage so the result stayed realistic.

Data Validation & Update Cycle

Before numbers are finalized, we compare outputs against independent signals such as therapy adoption trends, channel shifts between prescription and OTC, and whether implied patch usage per treated patient stays within practical limits. Variance checks are done across countries and across time so sudden jumps are questioned, and the assumptions are reviewed in more than one analyst pass before sign-off.

If a major event changes pricing, regulations, or product availability, we re-contact sources to confirm whether the change is temporary or structural, and then the model is updated. The report is refreshed annually, and before delivery a final review is completed so clients receive an updated view that reflects the latest public data and field feedback.

Mordor Intelligence's Non Opioid Pain Patch Market Sizing Compared With Other Published Estimates

Published market values for non-opioid pain patches can look far apart because each publisher defines the market box differently, and then uses different price bases and time periods for conversion into USD. Differences also show up when one estimate relies on stated list prices and another uses blended channel prices, or when the forecast year is treated as the starting point.

Opioid pain patches are frequently grouped as an add-on in broader pain patch studies, and that item sits outside Mordor Intelligence's scope, which is why some totals look larger even when they discuss similar pain conditions. In other cases, the gap comes from how countries are counted, how OTC volumes are treated versus prescription, and whether the update cycle captures recent channel growth from online pharmacies and changing reimbursement coverage.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.89 B (2025) | |

| Global Consultancy A | USD 0.99 B (2024) | Uses 2024 as the base year and a broader global country list, and the value appears to be built from a different price basis and distribution mix, which can pull the total down versus a 2025 run-rate view. |

| Industry Publisher B | USD 3.70 B (2025) | Likely includes adjacent pain patch categories and wider topical patch coverage, and it may apply higher blended pricing or a broader product basket that goes beyond non-opioid transdermal pain patches. |

Reading the figures side by side, the spread mostly traces back to what is included in the product basket, which year is treated as the starting point, and how pricing is normalized across prescription and OTC channels. Our approach stays traceable because the demand pool, usage rate, and pricing steps are laid out and then cross-checked against real-world adoption signals before the final totals are published.

Key Questions Answered in the Report

Which technology trend is most likely to reshape the non-opioid pain patch market over the next five years?

Microneedle-enhanced patches are set to redefine delivery efficiency by opening micro-channels in the skin that improve permeation of hydrophilic analgesics, extending wear time and reducing application frequency.

Why are capsaicin patches gaining momentum among clinicians treating neuropathic pain?

High-concentration capsaicin provides multi-month relief with a single application, giving physicians a non-systemic option for difficult-to-treat neuropathies such as post-herpetic neuralgia and chemotherapy-induced pain.

How is the rise of online pharmacies influencing competitive strategies for patch manufacturers?

Digital channels enable direct-to-consumer engagement, allowing brands to bundle education, subscription refills and targeted promotions that bypass traditional retail mark-ups.

What regulatory development in the United States is expected to accelerate hospital adoption of topical analgesic patches?

The NOPAIN Act mandates Medicare coverage for non-opioid pain alternatives in outpatient settings, prompting hospitals to integrate patches into perioperative pain protocols.

Which patient demographic is driving sustained demand for lidocaine-based patches?

Older adults, particularly those with co-morbidities that limit systemic NSAID use, prefer lidocaine patches for their favorable safety profile and minimal drug interactions.

Where do white-space opportunities exist for new entrants in this market?

Innovative combinations that unite multiple active ingredients or pair patches with mobile apps for personalized dosing offer untapped potential for differentiation.

Page last updated on: