Diabetic Nephropathy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2025) | USD 5.68 Billion |

| Market Size (2031) | USD 7.20 Billion |

| Growth Rate (2026 - 2031) | 8.04% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diabetic Nephropathy Market Analysis by Mordor Intelligence

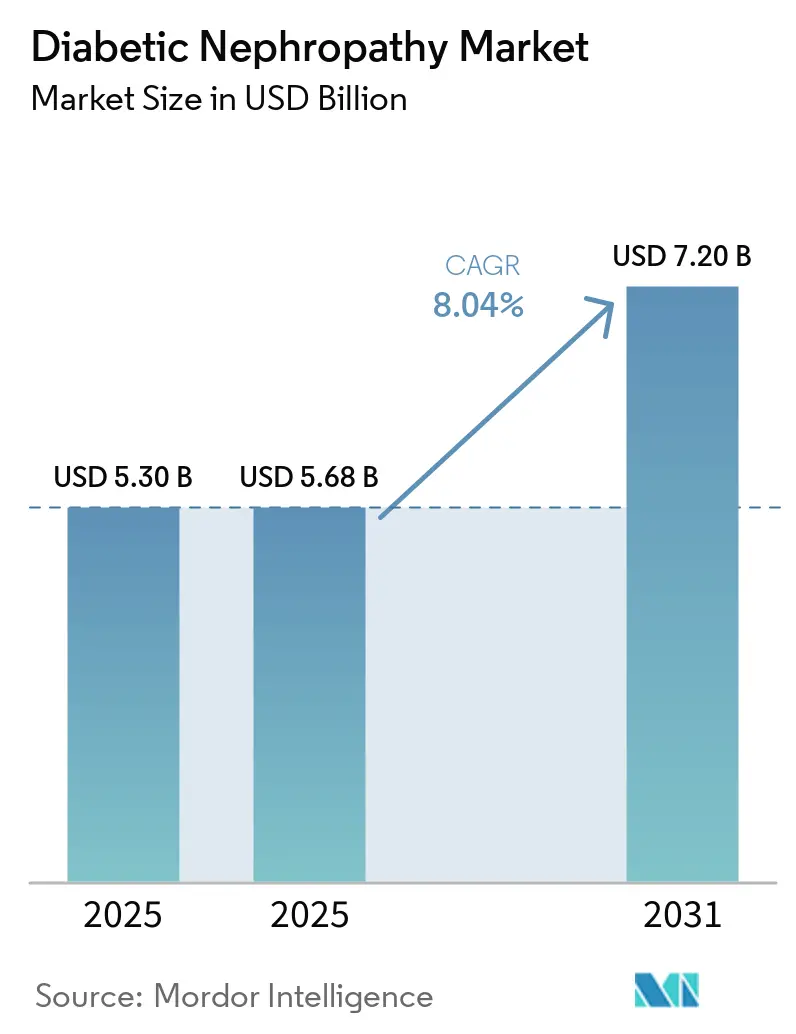

The Diabetic Nephropathy Market size is expected to increase from USD 5.30 billion in 2025 to USD 5.68 billion in 2025 and reach USD 7.20 billion by 2031, growing at a CAGR of 8.04% over 2025-2031.

Following the FDA's January 2025 approval of semaglutide for diabetic kidney disease, prescribing patterns have shifted significantly. This change is driven by the increasing adoption of dual-mechanism regimens that combine SGLT-2 inhibitors with GLP-1 receptor agonists, resulting in improved treatment outcomes. Additionally, value-based payment models are reshaping the market by incentivizing eGFR preservation, integrating multi-omics biomarkers, and encouraging earlier coverage decisions by public insurers. These factors are accelerating the commercial adoption of both therapeutics and diagnostics. On the demographic front, the global population of adults with diabetes is projected to rise from 589 million in 2024 to 853 million by 2050. However, the industry's focus is transitioning from reactive dialysis dependence to proactive nephropathy management, which is emerging as a key revenue driver. Competitive intensity remains moderate, with five leading pharmaceutical companies dominating prescription revenue, while numerous diagnostic firms compete primarily on turnaround times rather than proprietary innovations.

Key Report Takeaways

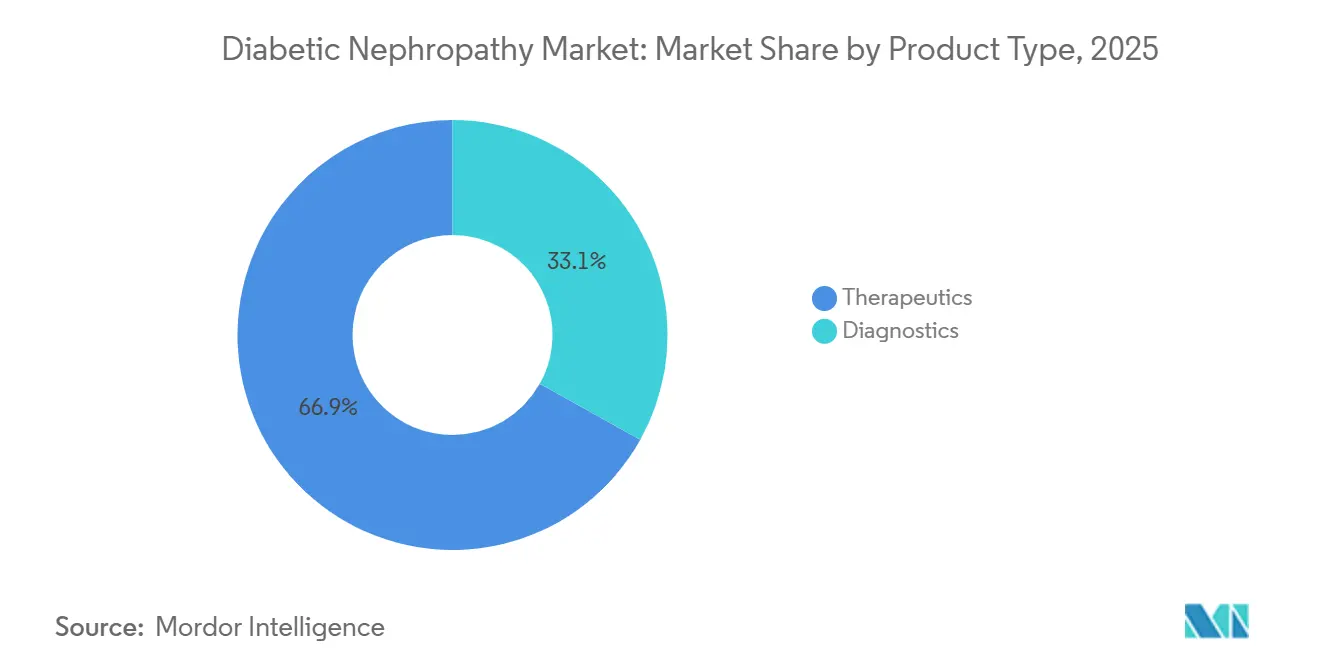

- By product type, therapeutics held 66.9% of the diabetic nephropathy market share in 2025, while diagnostics is advancing at an 8.15% CAGR through 2031.

- By stage of disease, CKD stages 3–4 led with 42.35% revenue in 2025; hyperfiltration is projected to expand at a 9.4% CAGR to 2031.

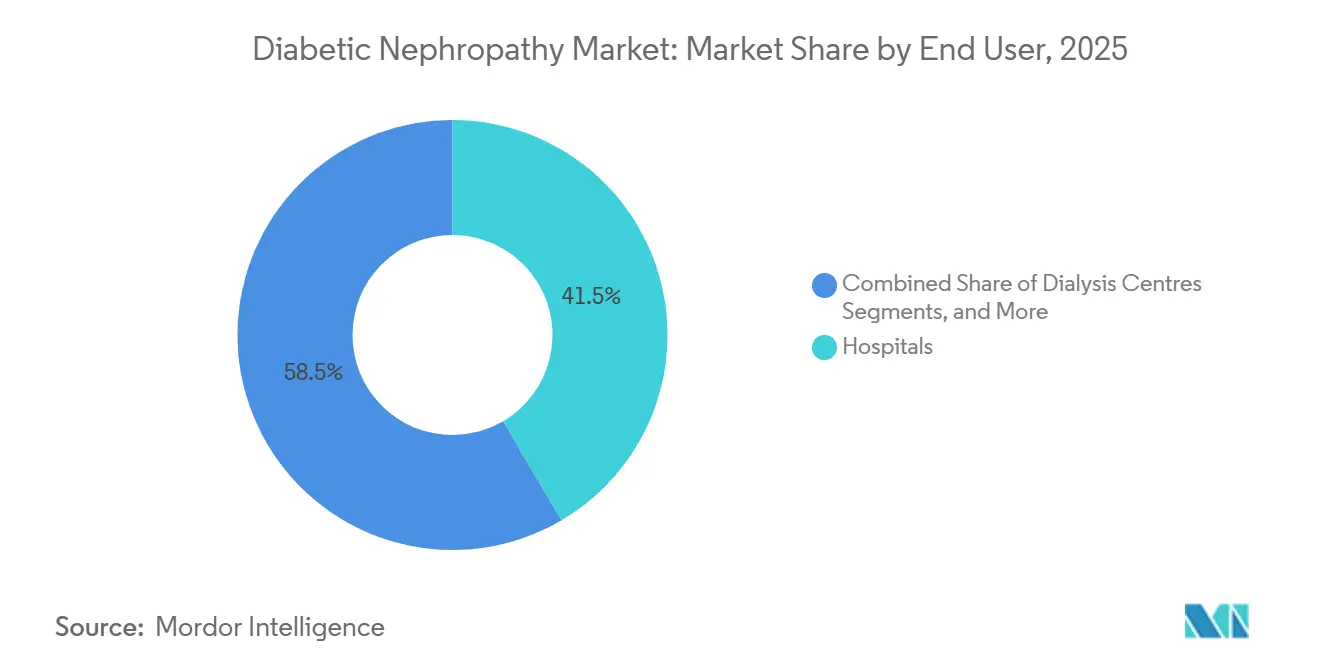

- By end user, hospitals accounted for 41.54% of the diabetic nephropathy market size in 2025, whereas dialysis centers are growing at an 8.8% CAGR through 2031.

- By route of administration, oral drugs captured 67.56% share in 2025 and are set to rise at a 9.1% CAGR during 2026-2031.

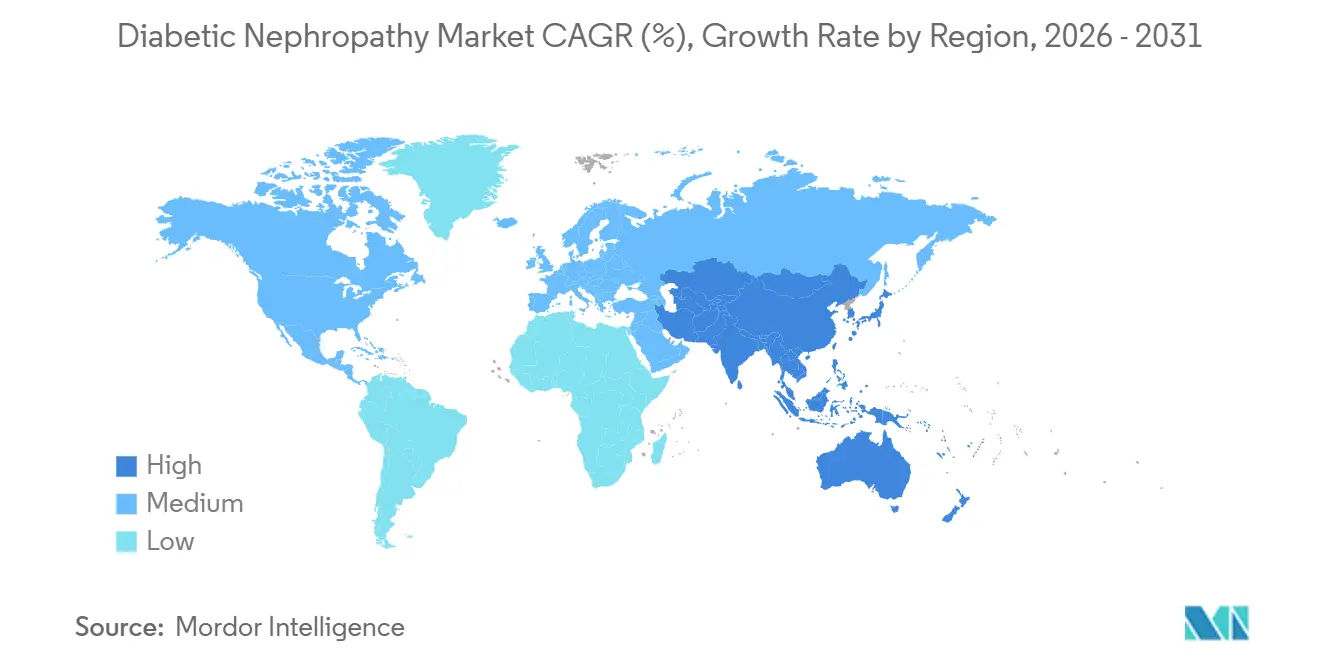

- By geography, North America dominated with 39.67% revenue in 2025; Asia-Pacific is the fastest-growing region at an 8.5% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diabetic Nephropathy Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating Global Diabetes Prevalence | 2.1% | Global, concentrated in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Ageing Population Accelerating CKD Burden | 1.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| Guideline-Mandated Annual Microalbumin Testing | 1.3% | North America, Western Europe | Medium term (2-4 years) |

| Rise of Urinary Multi-Omics Biomarker Panels | 0.9% | Europe, select US academic centers | Medium term (2-4 years) |

| Pay-for-Performance Nephrology Care Models | 1.1% | US (CMS CKCC), UK (NHS), spill-over to Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Diabetes Prevalence

In 2024, the global diabetic population reached 589 million adults, marking a 16% increase compared to 2021. Type 2 diabetes represents 90% of these cases, with 20-40% of patients developing diabetic nephropathy within a decade of diagnosis.[1]R. Hamid, “Projected 68% Rise in Type 2 Diabetes Prevalence Across Asia by 2045,” Journal of Diabetology, jdiabetol.com This growth is concentrated in specific regions, with China and India collectively accounting for 241 million diabetics. However, rural areas in these countries report less than 30% screening penetration for albuminuria, highlighting a significant unmet demand that is expected to grow as national health insurance expands coverage for UACR testing and SGLT-2 inhibitors. In the Middle East and North Africa, diabetes prevalence exceeds 20% in Gulf Cooperation Council nations, driven by factors such as obesity and sedentary lifestyles. However, healthcare systems in these regions face challenges in biomarker testing, often relying on serum creatinine, which is insufficient for detecting early-stage kidney damage. Growth in these markets is primarily driven by epidemiological trends rather than regulatory interventions.

Ageing Population Accelerating CKD Burden

The global population aged 65 and older is expected to grow from 771 million in 2024 to 1.6 billion by 2050. Countries such as Japan, Italy, and Germany already report median ages above 47 years. Age-related nephron loss compounds the impact of diabetes, with non-diabetic individuals losing approximately 10% of glomeruli per decade after age 40. Diabetics with hypertension experience even greater nephron loss, reducing functional capacity by 30-50% over the same period.[2]Claire Jackson, “Continued SGLT2 Inhibitor Use Cuts In-Hospital Mortality in Diabetes by 45%,” Diabetes Care, care.diabetesjournals.org This demographic trend is particularly evident in North America and Europe, where healthcare systems have integrated early detection into routine care through annual eGFR monitoring for older diabetic patients. In contrast, Asia-Pacific nations face challenges as rapidly aging populations in countries like South Korea and Thailand coincide with underdeveloped chronic disease management systems. This has created demand for point-of-care UACR devices that bypass centralized laboratory delays. Compliance frameworks such as ISO 15189 are gaining traction in the region, ensuring quality standards for diagnostics.

Guideline-Mandated Annual Microalbumin Testing

Recent guidelines have emphasized the importance of UACR screening for diabetic patients. Annual UACR testing is now recommended for all adults with diabetes, representing a shift from earlier risk-based approaches. This change aligns practices in the United States with those in Europe and Australia. The increased focus on testing has driven a significant rise in test volumes, although reimbursement rates have declined due to bundled payment negotiations. Adherence to these guidelines varies geographically, with North America and Western Europe achieving over 70% compliance, while Eastern Europe and Latin America lag at around 40%, hindered by limited laboratory access and physician adoption. Regulatory bodies have not mandated testing but have emphasized early detection in treatment protocols, indirectly encouraging broader adoption.

Rise of Urinary Multi-Omics Biomarker Panels

Traditional UACR testing provides limited insights into kidney damage beyond glomerular permeability. Multi-omics panels address this gap by measuring additional biomarkers such as NGAL, KIM-1, and Cystatin-C, along with proteomic classifiers like CKD273, which aggregates urinary peptides into a risk score for disease progression. These advanced panels have demonstrated high sensitivity in identifying at-risk populations that conventional methods often overlook. However, their adoption remains limited to select European laboratories due to high costs and infrastructure requirements. In the United States, these panels are classified as investigational, restricting reimbursement and broader use. While these technologies are seen as innovative, their implementation faces challenges, including the need for advanced equipment and specialized expertise. Regulatory pathways are evolving, with some approvals granted in Europe, but entry into the US market remains delayed due to regulatory hurdles.

Restraints Impact Table*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Low Physician Awareness in Primary Care | -0.8% | Global, acute in rural US, India, Sub-Saharan Africa | Medium term (2-4 years) |

| Adverse-Event Concerns with Endothelin Antagonists | -0.5% | Global, regulatory focus in US and EU | Short term (≤ 2 years) |

| Limited Reimbursement for Novel Biomarker Tests | -0.8% | Global, acute in rural US, India, Sub-Saharan Africa | Medium term (2-4 years) |

| AI Diagnostic Algorithms Facing Regulatory Delay | -0.5% | Global, regulatory focus in US and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pay-for-Performance Nephrology Care Models

In 2024, CMS introduced the Comprehensive Kidney Care Contracting (CKCC) initiative, engaging 4,200 nephrologists who accepted financial risk. Providers face penalties of up to 5% of capitated payments if dialysis rates exceed benchmarks, while outperformers gain shared savings. Early 2024 data shows CKCC participants increased SGLT-2 inhibitor prescriptions by 31% and UACR testing by 18% compared to fee-for-service models, driven by incentives to delay ESRD progression.[3]Y. Chen, “Epidemiology of Diabetic Kidney Disease in China,” Frontiers in Endocrinology, frontiersin.org In Australia, Kidney Health Australia is advocating for comparable reforms, though fragmented state-level funding has delayed implementation. Pay-for-performance models favor oral therapeutics like SGLT-2 and GLP-1 due to simpler adherence monitoring and lower costs, disadvantaging IV-administered drugs like endothelin antagonists that require intensive safety oversight. Compliance with value-based care is becoming a competitive edge, with companies embedding real-world evidence teams to align with CKCC outcomes.

Low Physician Awareness in Primary Care

A 2024 survey revealed that 43% of US primary-care physicians rarely ordered UACR tests for diabetic patients with normal serum creatinine, and 38% were unaware of the renal benefits of SGLT-2 inhibitors beyond glucose control. This gap is more pronounced in rural and underserved areas, where medical education on diabetic kidney disease lags and UACR test turnaround times discourage proactive screening. In India, a 2025 study found fewer than 20% of general practitioners in tier-2 cities could correctly interpret UACR thresholds, often confusing them with 24-hour urine protein tests. In Sub-Saharan Africa, low physician density and limited access to albuminuria testing force reliance on less accurate methods like dipstick urinalysis. Educational programs have shown potential but scale slowly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutics Dominance Meets Diagnostic Innovation

In 2025, therapeutics captured 66.90% of the market share, driven by the adoption of oral SGLT-2 inhibitors and GLP-1 receptor agonists in fixed-dose combinations. These combinations aim to enhance eGFR preservation while reducing the pill burden. Diagnostics, with a 33.10% share, are growing at an 8.15% CAGR through 2031, supported by the commercialization of biomarker panels like Cystatin-C, NGAL, and KIM-1, transitioning from research tools to clinical-grade assays. Within therapeutics, SGLT-2 inhibitors dominate, led by products like Farxiga and Jardiance, which gained FDA approval for CKD indications in 2021 and 2023, respectively. GLP-1 receptor agonists are the fastest-growing segment, with a 9.5% CAGR, fueled by the approval of semaglutide for diabetic kidney disease in 2025. Endothelin receptor antagonists and calcium-channel blockers serve niche roles, while ACE inhibitors and ARBs are losing prominence due to the superior outcomes of SGLT-2 inhibitors, though they remain prevalent in cost-sensitive markets.

By Stage of Disease: Late-Stage Volume Versus Early-Stage Growth

Chronic Kidney Disease Stages 3–4 accounted for 42.35% of the market share in 2025, reflecting the trend of diagnoses occurring after eGFR drops below 60 mL/min/1.73m², when symptoms prompt medical evaluation. The hyperfiltration segment is the fastest-growing, with a 9.40% CAGR, driven by early intervention models that reward proactive screening and treatment. Microalbuminuria (Stage 1) and macroalbuminuria (Stage 2) together represent about 35% of the market, with growth supported by guidelines promoting earlier screenings. End-stage renal disease (Stage 5) holds a smaller share as patients transition to dialysis or transplantation, though diagnostic services for ESRD patients remain a significant revenue driver.

By End User: Hospitals Lead, Dialysis Centers Surge

Hospitals held 41.54% of the market share in 2025, serving as the primary centers for diagnosing advanced diabetic nephropathy in patients requiring inpatient care. Dialysis centers are the fastest-growing segment, with an 8.80% CAGR, benefiting from earlier detection and better-preserved kidney function in ESRD patients, enabling incremental dialysis initiation. Specialty clinics, including endocrinology and nephrology practices, account for 28% of the market, bridging primary and tertiary care while adopting cost-effective care models involving pharmacists and nurse practitioners.

By Route of Administration: Oral Convenience Dominates, Injectables Gain Share

Oral formulations led with a 67.56% market share in 2025 and are the fastest-growing route at a 9.10% CAGR, driven by SGLT-2 inhibitors and oral GLP-1 receptor agonists like semaglutide, which simplify adherence and reduce injection aversion. Injectable therapies, holding 32.44% of the market, are growing at a slower 6.8% CAGR due to patient resistance to injections and logistical challenges in distribution. The oral segment's growth is further supported by the development of fixed-dose combinations aimed at improving adherence in populations struggling with polypharmacy.

Geography Analysis

In 2025, North America accounted for 39.67% of the market share, driven by CMS policies that reimburse SGLT-2 inhibitors and GLP-1 agonists for diabetic kidney disease under Medicare Part B. These policies, combined with Comprehensive Kidney Care Contracting models, support early-stage interventions. The U.S., with 34.8 million diabetics, faces a significant gap in care as only 48% of eligible patients receive annual UACR screenings, despite 37% showing kidney impairment. Health systems are addressing this gap through electronic health record alerts and pharmacist-led outreach. In Canada, while SGLT-2 inhibitors are covered under provincial formularies, reimbursement for advanced biomarkers like Cystatin-C remains inconsistent. This creates a two-tier diagnostic system, with provinces like Ontario and British Columbia offering advanced testing, while rural areas rely on serum creatinine methods.

Asia-Pacific is the fastest-growing region, with an 8.50% CAGR projected through 2031. Growth is fueled by China's 140 million diabetics, 20% of whom exhibit microalbuminuria. National policies mandating the inclusion of SGLT-2 inhibitors in provincial essential medicine lists ensure hospital access and drive price reductions of 50–70% through volume-based procurement. In India, the landscape is fragmented. Private hospitals in major cities like Delhi, Mumbai, and Bangalore provide comprehensive diabetic nephropathy care, including advanced biomarkers. However, government primary health centers in smaller cities lack basic UACR testing, pushing patients to private laboratories for self-funded diagnostics.

Competitive Landscape

The diabetic nephropathy market is moderately concentrated. The top five players, AstraZeneca, Novo Nordisk, Boehringer Ingelheim, Eli Lilly, and Bayer, collectively account for approximately 55% of pharmaceutical revenue. However, no single company dominates, driving intense price competition in the SGLT-2 and GLP-1 segments as patents expire and biosimilars enter the market. For example, canagliflozin's loss of exclusivity in 2025 led to a 40% price drop within six months. In diagnostics, competition among Abbott, Roche, Siemens Healthineers, Beckman Coulter, and regional laboratories is based on assay turnaround times and integration into hospital systems rather than proprietary biomarkers. This focus has compressed margins to single digits for standard tests like UACR. Strategic trends show large-cap pharma focusing on label expansions, such as AstraZeneca's Farxiga gaining approvals for CKD, heart failure, and Type 2 diabetes, while biotechs like Chinook Therapeutics and Reata Pharmaceuticals target underserved mechanisms like endothelin antagonism and Nrf2 activation, aiming for premium pricing if safety profiles are favorable.

Three key areas present white-space opportunities. First, oral fixed-dose combinations that integrate SGLT-2, GLP-1, and finerenone into a single pill could address the 40% discontinuation rate caused by polypharmacy fatigue. Second, point-of-care UACR devices for primary-care offices and retail clinics can mitigate delays in centralized laboratory turnarounds, which often hinder proactive screening. Third, AI-driven risk-stratification platforms combining eGFR trajectories, imaging, and genomics can identify rapid progressors, enabling precise therapy allocation. Emerging disruptors like Renalytix are leveraging AI algorithms to predict kidney-failure risks, securing regulatory and reimbursement milestones. Technology is reshaping market dynamics. Novo Nordisk's digital health platform, which pairs Ozempic prescriptions with app-based adherence tracking and automated refill reminders, has increased six-month persistence rates to 68%, compared to 52% for unmonitored patients. This real-world effectiveness has earned preferred formulary placement. Companies investing in CMS CKCC-aligned outcome registries, which provide real-world evidence on eGFR preservation and hospitalization avoidance, are gaining a competitive edge in value-based contracts, a critical advantage in a pay-for-performance environment.

Diabetic Nephropathy Industry Leaders

AstraZeneca plc

Bayer AG

Eli Lilly and Company

Johnson & Johnson

AbbVie Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BioMed X launched a diabetic kidney disease research project with the Government of Barbados under the EU-backed PharmaNext Program.

- November 2025: Bayer’s Phase III FINE-ONE trial showed finerenone lowered UACR 25% over six months in Type 1 diabetes with CKD, presented at ASN Kidney Week.

- January 2025: Novo Nordisk gained FDA approval for semaglutide to cut kidney failure and cardiovascular death risk in Type 2 diabetes with CKD, based on the FLOW trial showing a 24% composite risk reduction.

Global Diabetic Nephropathy Market Report Scope

As per the scope of the report, diabetic nephropathy is a serious kidney complication affecting 30–40% of people with type 1 or type 2 diabetes, caused by long-term high blood sugar damaging the kidney's filtering units (glomeruli). It is the leading cause of chronic kidney disease and kidney failure (ESRD), often resulting in protein leakage into urine, high blood pressure, and potential kidney failure requiring dialysis.

The diabetic nephropathy market is segmented by product type, stage of disease, end user, route of administration (therapeutics), and geography. By product type, the market is segmented into therapeutics and diagnostics. The therapeutics segment includes ACE inhibitors, angiotensin II receptor blockers (ARBs), SGLT-2 inhibitors, endothelin receptor antagonists, GLP-1 receptor agonists, calcium-channel blockers, and others. The diagnostics segment includes urine albumin-to-creatinine ratio (UACR), 24-hour urine albumin, serum creatinine, estimated GFR (eGFR) algorithms, imaging (ultrasound, MRI), novel biomarkers (Cystatin-C, NGAL, KIM-1, etc.), and others. By stage of disease, the market is segmented into hyperfiltration (pre-clinical), micro-albuminuria (stage 1), macro-albuminuria (stage 2), chronic kidney disease (stage 3-4), and end-stage renal disease (stage 5). By end user, the market is segmented into hospitals, specialty clinics, dialysis centers, diagnostic laboratories, and academic & research institutes. By route of administration (therapeutics), the market is segmented into oral and injectable. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Therapeutics | ACE Inhibitors |

| Angiotensin II Receptor Blockers (ARBs) | |

| SGLT-2 Inhibitors | |

| Endothelin Receptor Antagonists | |

| GLP-1 Receptor Agonists | |

| Calcium-Channel Blockers | |

| Others | |

| Diagnostics | Urine Albumin-to-Creatinine Ratio (UACR) |

| 24-h Urine Albumin | |

| Serum Creatinine | |

| Estimated GFR (eGFR) Algorithms | |

| Imaging (Ultrasound, MRI) | |

| Novel Biomarkers (Cystatin-C, NGAL, KIM-1, etc.) | |

| Others |

| Hyperfiltration (Pre-clinical) |

| Micro-albuminuria (Stage 1) |

| Macro-albuminuria (Stage 2) |

| Chronic Kidney Disease (Stage 3-4) |

| End-Stage Renal Disease (Stage 5) |

| Hospitals |

| Specialty Clinics |

| Dialysis Centres |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Oral |

| Injectable |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Therapeutics | ACE Inhibitors |

| Angiotensin II Receptor Blockers (ARBs) | ||

| SGLT-2 Inhibitors | ||

| Endothelin Receptor Antagonists | ||

| GLP-1 Receptor Agonists | ||

| Calcium-Channel Blockers | ||

| Others | ||

| Diagnostics | Urine Albumin-to-Creatinine Ratio (UACR) | |

| 24-h Urine Albumin | ||

| Serum Creatinine | ||

| Estimated GFR (eGFR) Algorithms | ||

| Imaging (Ultrasound, MRI) | ||

| Novel Biomarkers (Cystatin-C, NGAL, KIM-1, etc.) | ||

| Others | ||

| By Stage of Disease | Hyperfiltration (Pre-clinical) | |

| Micro-albuminuria (Stage 1) | ||

| Macro-albuminuria (Stage 2) | ||

| Chronic Kidney Disease (Stage 3-4) | ||

| End-Stage Renal Disease (Stage 5) | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Dialysis Centres | ||

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| By Route of Administration (Therapeutics) | Oral | |

| Injectable | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the diabetic nephropathy market be by 2031?

It is forecast to reach USD 8.04 billion by 2031, growing at a 7.2% CAGR from 2026 to 2031.

Which therapy class currently generates the most revenue?

Oral SGLT-2 inhibitors lead 2025 sales, helping therapeutics secure 66.9% of global revenue.

Which region is expanding fastest?

Asia-Pacific is projected to rise at an 8.5% CAGR through 2031 due to high diabetes prevalence and expanding access to SGLT-2 inhibitors.

What diagnostic innovation is gaining momentum?

Multi-omics urinary panels that add NGAL, KIM-1, and CKD273 to conventional albumin tests are scaling in European labs and promise 85% sensitivity for early decline.

Which stage of disease is the fastest-growing revenue segment?

Hyperfiltration, the preclinical phase, is growing 9.4% annually as pay-for-performance models push earlier screening and treatment.

Are value-based care models reshaping adoption patterns?

Yes, U.S. and U.K. risk-sharing contracts have boosted SGLT-2 prescriptions by more than 30% and increased UACR testing 18%, directly lifting market growth.

Page last updated on: