Insulin Lispro Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

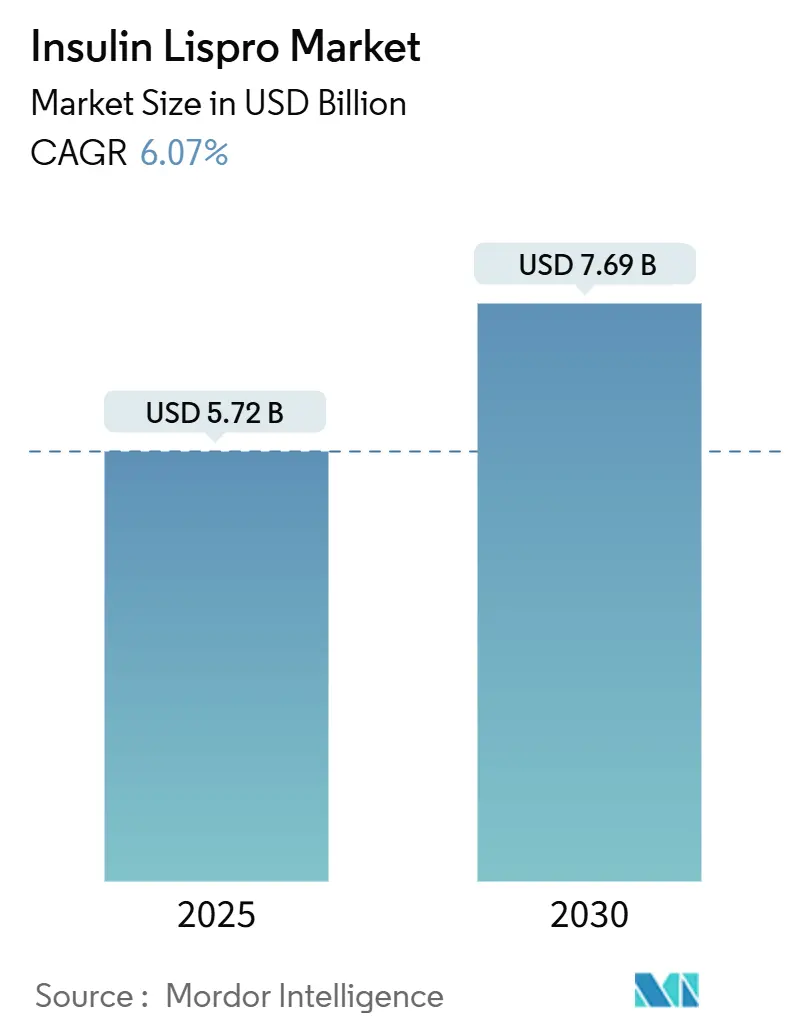

| Market Size (2025) | USD 5.72 Billion |

| Market Size (2030) | USD 7.69 Billion |

| Growth Rate (2025 - 2030) | 6.07% CAGR |

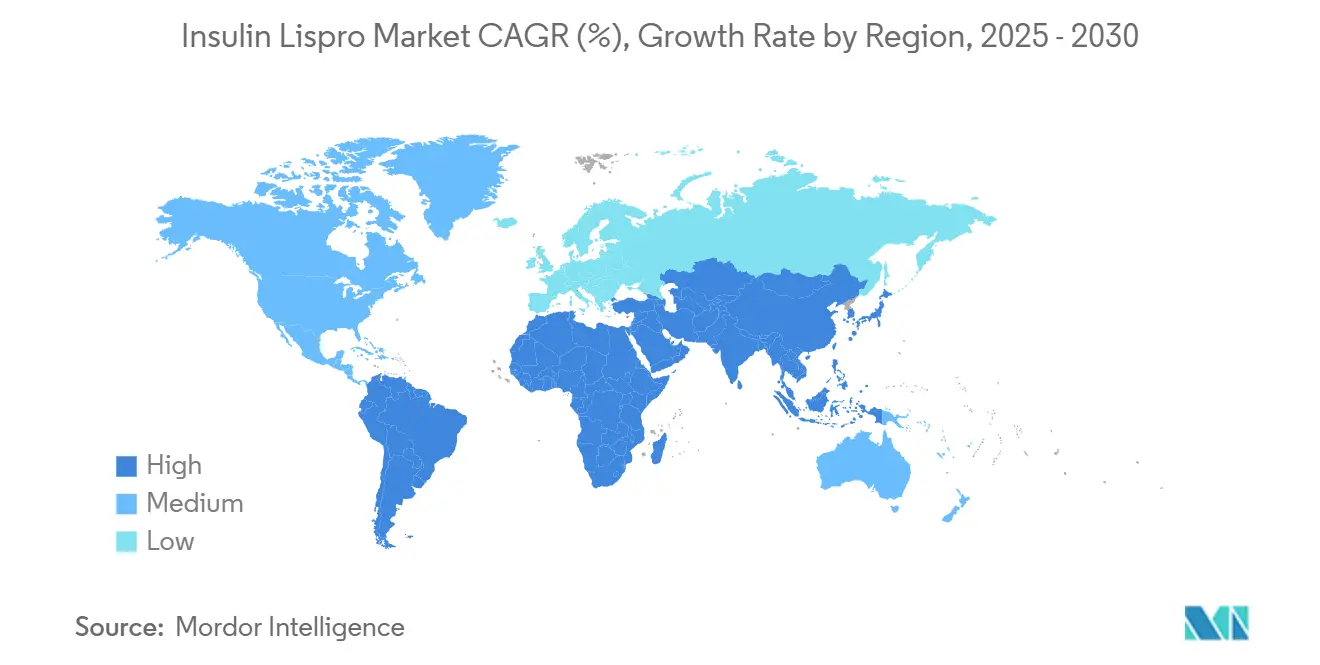

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulin Lispro Market Analysis by Mordor Intelligence

The insulin lispro market size stands at USD 5.72 billion in 2025 and is expected to reach USD 7.69 billion by 2030, advancing at a 6.07% CAGR over the forecast period. The steady expansion reflects resilient demand supported by rapid‐acting analog preference, biosimilar-driven price elasticity, and rising Type 2 diabetes prevalence. North America remains the largest revenue contributor, while Asia-Pacific records the fastest uptake as demographic pressure and healthcare digitization unlock fresh demand. Regulatory tailwinds—most notably the FDA’s streamlined interchangeability rules—accelerate biosimilar penetration that reshapes competitive pricing without dampening overall volume. Technology convergence around continuous glucose monitoring (CGM) and automated insulin delivery systems further stimulates premium‐segment growth, counterbalancing margin pressure from new entrants. Manufacturers respond by investing in high-dose formulations, smart pen ecosystems, and vertically integrated digital platforms that enhance patient adherence while differentiating beyond pure price competition.[1]U.S. Food and Drug Administration, “FDA Clears First Device to Enable Automated Insulin Dosing for Individuals with Type 2 Diabetes,” fda.gov

Key Report Takeaways

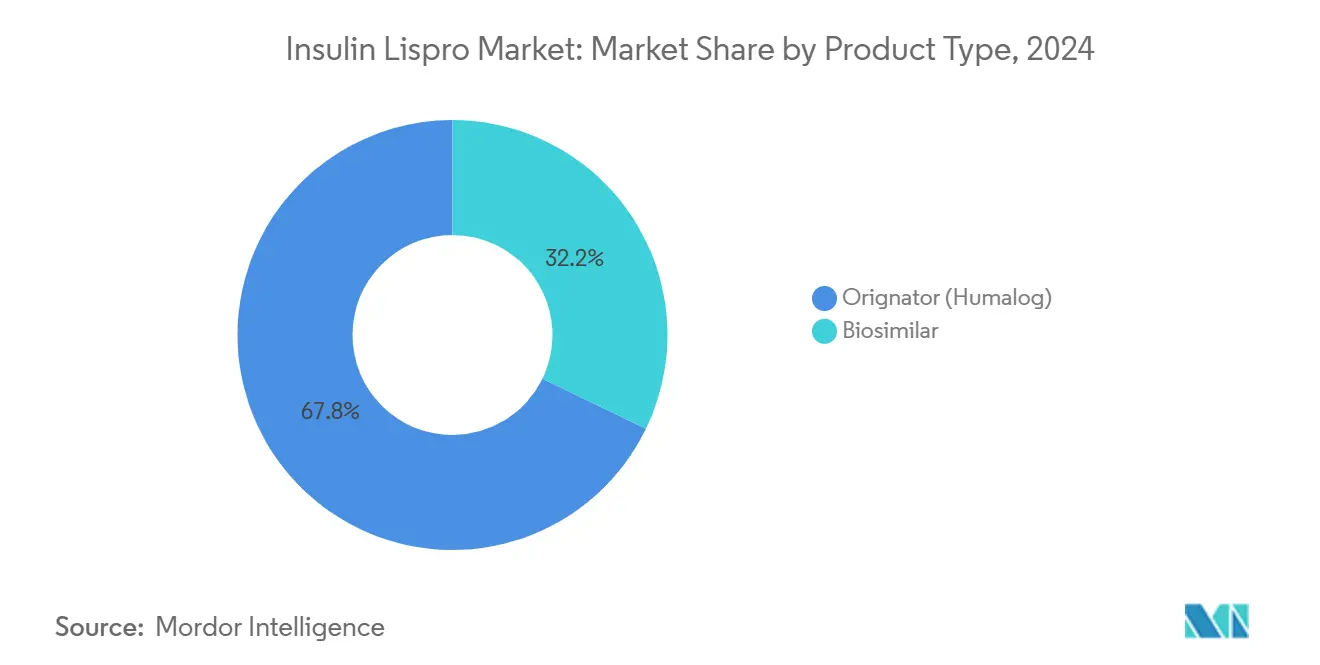

- By product type, originators held 67.81% of the insulin lispro market share in 2024, whereas biosimilars are projected to post an 11.04% CAGR through 2030.

- By formulation device, prefilled pens led with a 47.68% share in 2024; re-usable cartridges are forecast to expand at an 8.95% CAGR between 2025 and 2030.

- By concentration, U-100 accounted for a 74.62% share of the insulin lispro market size in 2024, while U-200 is poised to grow at a 10.56% CAGR over the same period.

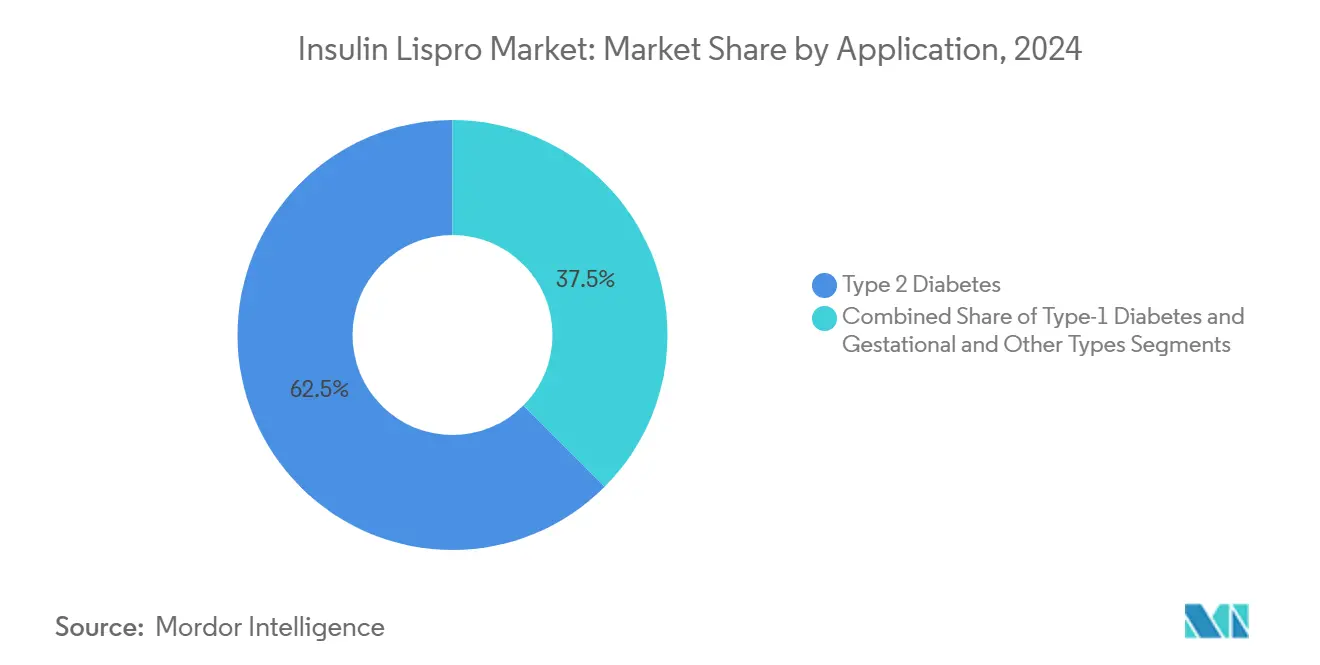

- By application, Type 2 diabetes commanded a 62.52% share in 2024, and gestational and other types are advancing at a 9.34% CAGR through 2030.

- By distribution channel, retail pharmacies captured a 51.37% share in 2024, whereas online pharmacies are projected to log a 10.53% CAGR to 2030.

- By geography, North America represented 41.46% revenue share in 2024; Asia-Pacific is projected to record the highest regional CAGR of 9.06% from 2025 to 2030.

Global Insulin Lispro Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global Type 2 diabetes prevalence | +1.6% | Global, highest in Asia-Pacific & MEA | Long term (≥ 4 years) |

| Clinical preference for rapid-acting analogs | +0.8% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Pen & cartridge device adoption | +1.2% | Global, led by developed markets | Medium term (2-4 years) |

| Biosimilar approvals and price elasticity | +0.9% | North America & Europe, spillover to emerging markets | Short term (≤ 2 years) |

| CGM-pump algorithm integration | +0.7% | North America & Europe, early urban APAC | Medium term (2-4 years) |

| Value-based reimbursement in middle-income | +0.6% | Core APAC, Latin America, selective MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Type-2 Diabetes Prevalence

Rising diabetes prevalence provides the single largest structural demand tailwind for the insulin lispro market. Forecasts indicate 1.31 billion cases by 2050, with Type 2 diabetes comprising 96% of the burden.[2]Rajesh Kumar, “Digital Health Technology in Diabetes Management in the Asia–Pacific Region,” PMC, pmc.ncbi.nlm.nih.gov China alone recorded 233 million patients in 2024, translating to a 15.88% prevalence that underpins sustained insulin demand. Younger onset in urban Asia-Pacific populations prolongs treatment duration, locking in lifelong therapy cycles. Egypt exemplifies Middle East acceleration as prevalence is expected to climb from 20.9% in 2021 to 23.5% by 2045.[3]Wei Zhang, “AI-Driven Management of Type 2 Diabetes in China,” PMC, pmc.ncbi.nlm.nih.gov Such demographic momentum insulates market growth from macroeconomic volatility over the long term.

Clinical Preference for Rapid-Acting Insulin Analogs

Physicians consistently prioritize rapid-acting analogs for their closer physiologic match to mealtime glucose excursions, faster onset, and lower hypoglycemia risk. The American Diabetes Association’s 2025 standards reinforce analog preference, especially for gestational care, where dose precision is critical. Pipeline innovation, such as once-weekly glucose-responsive formulations under the Type 1 Diabetes Grand Challenge, sustains the premium niche despite generic pressure. These clinical advantages translate into prescriber loyalty that tempers erosion from biosimilar discounting.

Pen & Cartridge Device Adoption Improving Adherence

Prefilled pens, smart reusable cartridges, and emerging patch pumps simplify dosing and digitally capture adherence data, tackling the 50% non-compliance challenge seen in diabetes care. Bluetooth-enabled pens that automatically log doses into smartphone apps are gaining widespread reimbursement, supporting physician monitoring and algorithmic titration. Embecta’s 300U patch pump submission illustrates continued device diversification that widens addressable patient segments who seek needle-free or reduced-frequency options. Improved convenience directly lifts insulin lispro utilization as more patients transition from oral agents to injectable regimens sooner.

Biosimilar Approvals Spurring Price-Elastic Volume Growth

The FDA’s February 2025 approval of Merilog as the first rapid-acting biosimilar and the June 2024 elimination of mandatory switching studies dramatically lowered entry barriers. Biocon’s plan to roll out five biosimilars within 18 months exemplifies how pricing competition boosts unit demand in volume-sensitive markets. China’s volume-based procurement achieved 42% insulin price cuts, signaling the magnitude of elasticity when payers see viable substitutes. While near-term margins contract, aggregate demand lifts, sustaining overall revenue growth in the insulin lispro market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin erosion from biosimilar price competition | –0.9% | Global, strongest in North America & Europe | Short term (≤ 2 years) |

| Stringent interchangeability requirements | –0.6% | North America & Europe | Medium term (2-4 years) |

| Cold-chain vulnerabilities in tropical delivery | –0.4% | APAC, MEA, Latin America tropical regions | Long term (≥ 4 years) |

| Shift toward oral GLP-1 and non-insulin injectables | –0.8% | Global, led by developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin Erosion from Biosimilar Price Competition

Price discounts averaging 20–30% on launch are eroding originator gross margins within months of biosimilar entry. Sanofi’s Merilog benchmarks the trend, prompting aggressive rebate strategies from incumbents to defend formulary status. Payers leverage this dynamic to negotiate deeper cuts, compressing profitability even as volumes rise. The challenge intensifies in markets like China, where centralized tenders lock multiyear price ceilings. To sustain earnings, manufacturers must pivot toward high-concentration or digitally integrated offerings that justify premium positioning.

Stringent Interchangeability Requirements by Regulators

Despite recent FDA easing, interchangeability still demands robust switching data and post-market surveillance, adding cost and time for smaller entrants. European Union procedures mirror the complexity, and many national policies still mandate prescriber consent before substitution. Such hurdles slow automatic pharmacy-level switching, tempering near-term biosimilar uptake and preserving a measure of price discipline in the insulin lispro market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biosimilars Narrow the Gap

Originators dominated with 67.81% revenue in 2024, reflecting entrenched prescriber familiarity and extensive real-world evidence backing Humalog. The insulin lispro market size for originator products was USD 3.87 billion in 2024, compared with USD 1.84 billion for biosimilars. Robust payer incentives and streamlined U.S. interchangeability rules are forecast to propel biosimilars at an 11.04% CAGR, shrinking the dominance gap yet expanding the overall insulin lispro market through price-elastic uptake. Merilog’s U.S. launch validates the regulatory path while Biocon’s forthcoming interchangeable aspart sets a competitive tone that may accelerate formulary shifts.

Biosimilar adoption is expected to exceed 35% of total prescriptions by 2030, yet originators counter with differentiated offerings such as weekly efsitora alfa and integrated smart-pen programs. These enhancements preserve loyalty among complex cases and in markets where substitution remains physician-driven. As competitive intensity mounts, the insulin lispro industry sees incumbents bundling value-added support—training, data platforms, and adherence monitoring—to retain hospital purchasing committees.

By Formulation Device: Smart Technology Drives Pen Preference

Prefilled pens delivered 47.68% revenue share in 2024 as they match patients' desire for convenience and precise dosing. This segment accounted for USD 2.73 billion of the insulin lispro market size, well ahead of vials. Enhanced needle geometry, dose counters, and connectivity features position pens as the centerpiece of digital health ecosystems. Reusable cartridges, propelled by sustainability mandates and cost savings, lead growth at 8.95% CAGR from 2025 to 2030, particularly in Europe, where environmental policies shape procurement choices.

Vial usage persists in hospitals, yet the shift toward outpatient self-management favors portable formats. Patch pumps and pen-pump hybrids emerging from Embecta and other innovators broaden the options set, underlining how device variety reinforces overall insulin lispro market expansion. As these systems integrate CGM feeds and algorithmic dosing, they create lock-in benefits that cushion suppliers against pure price wars.

By Concentration: High-Dose Needs Bolster U-200 Upside

U-100 formulations retained a 74.62% share in 2024, synonymous with standard care protocols. In value terms, this equated to USD 4.27 billion of the insulin lispro market size. U-200, however, is rising swiftly at a 10.56% CAGR, catering to insulin-resistant Type 2 patients requiring high mealtime doses. Humalog U-200 KwikPen halves the injection volume without altering pharmacokinetics, improving tolerance and adherence for individuals regularly exceeding 20 units per meal.

Though biosimilars initially target U-100 to maximize addressable volume, late-cycle pipeline candidates are expected to replicate high-concentration formats, intensifying choice. For incumbents, early investment in U-200 manufacturing capacity forms a strategic moat, elevating barriers for price-focused challengers and preserving premium margins within this specialized niche of the insulin lispro market.

By Application: Type 2 Diabetes Anchors Demand

Type 2 diabetes accounted for 62.52% of revenue in 2024, equal to USD 3.58 billion in the insulin lispro market size. Rising obesity and earlier disease onset broaden the candidate pool for rapid-acting analog introduction, moving insulin initiation forward in treatment algorithms. Gestational and other diabetes segments, while smaller, are set to outpace at 9.34% CAGR as screening protocols tighten and guidelines favor insulin for pregnancy safety. The ADA’s 2025 emphasis on analog use in gestational diabetes supports this trajectory.

Ongoing FDA approvals for automated dosing technologies aimed at Type 2 cohorts increase the pool of patients managed on prandial insulin. These systems leverage insulin lispro pharmacodynamics to deliver tight postprandial control, thereby entrenching the molecule in advanced treatment pathways even as alternative injectables expand.

By Distribution Channel: Digital Front Doors Accelerate Access

Retail pharmacies still own 51.37% share due to widespread brick-and-mortar presence and insurer contracting power. Yet online channels are poised for 10.53% CAGR growth as subscription models like Amazon Pharmacy’s USD 35-per-month program unlock transparent pricing and convenient delivery. For many chronic users, automated refills and bundled telehealth consultations reduce service friction, driving channel migration.

Hospital pharmacies maintain relevance for newly diagnosed patients and complex case titration, but subsequent prescription renewals increasingly route through digital platforms. Federal scrutiny of pharmacy benefit managers spreads, highlighted in a 2024 HHS margin study, may further open the door to direct-to-consumer supply models that compress costs and enhance price visibility.

Geography Analysis

North America retained 41.46% revenue share in 2024, equaling USD 2.37 billion within the insulin lispro market. Robust reimbursement, widespread CGM adoption, and rapid biosimilar approvals sustain high penetration. Digital pharmacy initiatives and the first automated dosing clearance for Type 2 patients reinforce volume growth even as list prices face downward pressure. Manufacturers mitigate supply chain risk through domestic fill-finish expansions, aiming to avert shortfalls experienced in 2024.

Asia-Pacific delivers the highest growth at a 9.06% CAGR to 2030. China’s 233 million diabetes population prompts large-scale procurement programs that compress price yet bolster unit uptake. Parallel investments in AI-driven disease management apps foster adherence and data-driven titration. India’s CDSCO approval of inhaled Afrezza enlarges modality choice and may accelerate first-line insulin adoption among injection-averse patients. Rising middle-class access to insurance schemes amplifies volumes across Southeast Asia.

Europe maintains stable demand under universal coverage frameworks. EMA rigor ensures biosimilar confidence, while environmental procurement criteria advance reusable cartridge uptake. Southern markets pursue cost containment, negotiating bulk discounts tied to outcome metrics. The Middle East and Africa, though nascent, see diabetes prevalence outpacing infrastructure; focused cold-chain investments and WHO prequalification programs slowly extend reach. South America shows uneven progress, with Brazil leading acceleration through public-sector tender reforms that invite biosimilar bids.

Competitive Landscape

The insulin lispro market is moderately concentrated. Intensifying biosimilar entry steadily fragments share, compelling incumbents to differentiate via technology integration. Eli Lilly trials weekly efsitora alfa to shift treatment paradigms toward reduced-frequency plans. Sanofi earmarks EUR 1.3 billion for high-volume production lines adaptable to both originator and biosimilar output, safeguarding supply reliability.

New entrants such as Biocon and Wockhardt exploit regulatory streamlining, bringing competitive price points that force rebating maneuvers among leaders. Cross-industry alliances proliferate; Abbott pairs its Libre CGM with multiple pump makers, and Medtronic expands algorithm licensing to pen makers, knitting hardware and software into closed-loop ecosystems. These collaborations generate switching barriers beyond drug cost, recasting competition around total‐care solutions rather than molecule commoditization.

Manufacturing resilience also becomes a strategic lever. Companies upgrade cold-chain monitoring technologies and diversify regional fill-finish operations to insulate against logistics shocks. Sustainability commitments drive exploration of lower-carbon production and recyclable device housings, appealing to payers incorporating environmental metrics into bid evaluations. Collectively, these moves indicate an industry pivot from price defense to holistic value creation rooted in technology, reliability, and patient-centric service.

Insulin Lispro Industry Leaders

Eli Lilly and Company

Sanofi S.A.

Sandoz International GmbH

Wockhardt Ltd.

Biocon Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Adocia shared encouraging news today: its partner Tonghua Dongbao reported positive Phase 3 results for BioChaperone Lispro (THDB0206), an ultra-rapid insulin that could give people with diabetes faster, more convenient blood-sugar control.

- August 2024: FDA clears Insulet’s SmartAdjust technology for automated insulin dosing in adults with Type 2 diabetes, the first system of its kind for this patient group.

Global Insulin Lispro Market Report Scope

| Originator (Humalog) |

| Biosimilar (e.g., Admelog, Biocon Lispro) |

| Vial |

| Prefilled Pen |

| Re-usable Cartridge |

| U-100 |

| U-200 |

| Type-1 Diabetes |

| Type-2 Diabetes |

| Gestational & Other Types |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Originator (Humalog) | |

| Biosimilar (e.g., Admelog, Biocon Lispro) | ||

| By Formulation Device | Vial | |

| Prefilled Pen | ||

| Re-usable Cartridge | ||

| By Concentration | U-100 | |

| U-200 | ||

| By Application | Type-1 Diabetes | |

| Type-2 Diabetes | ||

| Gestational & Other Types | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the insulin lispro market in 2025?

The insulin lispro market size is USD 5.72 billion in 2025 and is projected to reach USD 7.69 billion by 2030.

Which region is growing fastest for insulin lispro?

Asia-Pacific registers the highest CAGR at 9.06% between 2025 and 2030, fueled by large diabetes populations in China and India.

What drives the shift toward pen devices?

Prefilled and smart pens enhance dosing accuracy, reduce injection anxiety, and integrate with smartphone apps, lifting adherence and overall demand.

How are biosimilars affecting pricing?

First-to-market biosimilars such as Merilog launch with discounts that compress originator margins yet expand total volume through greater affordability.

Why is U-200 gaining popularity?

U-200 pens cut injection volume in half, benefiting insulin-resistant patients who require high mealtime doses, thereby improving comfort and adherence.

What role do automated insulin delivery systems play?

FDA-cleared closed-loop systems marry CGM data with adaptive algorithms, optimizing lispro dosing and demonstrating superior postprandial control in both Type 1 and Type 2 diabetes.

Page last updated on: