NLP In Healthcare and Life Science Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

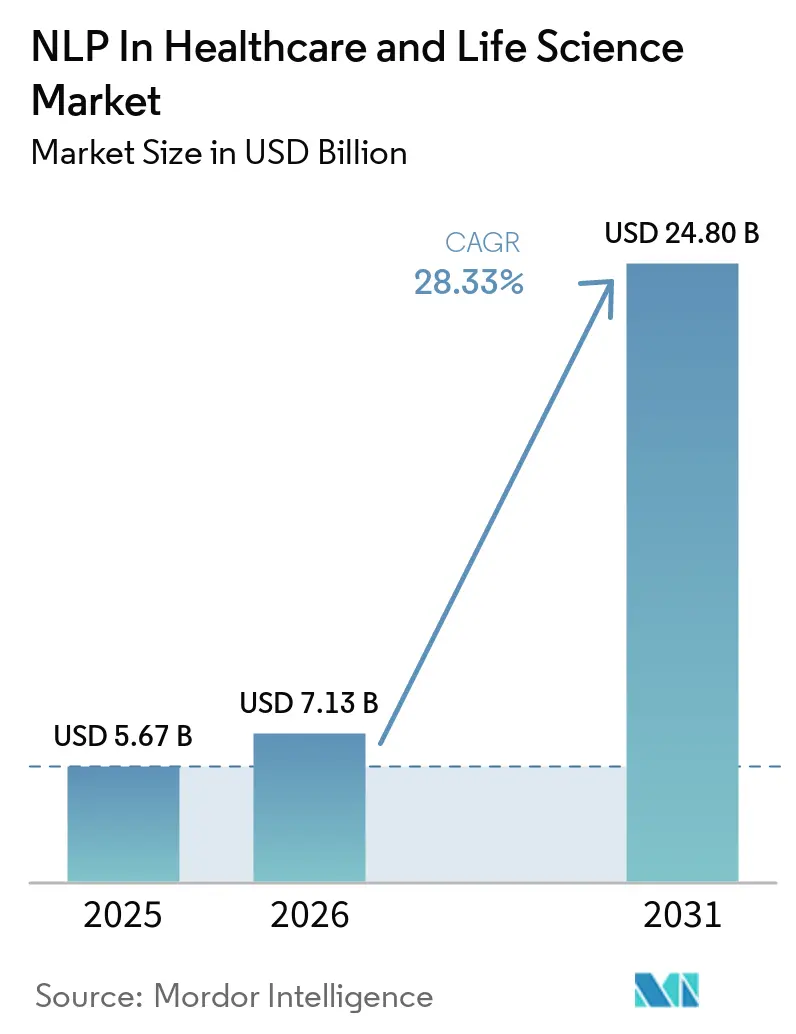

| Market Size (2026) | USD 7.13 Billion |

| Market Size (2031) | USD 24.80 Billion |

| Growth Rate (2026 - 2031) | 28.33% CAGR |

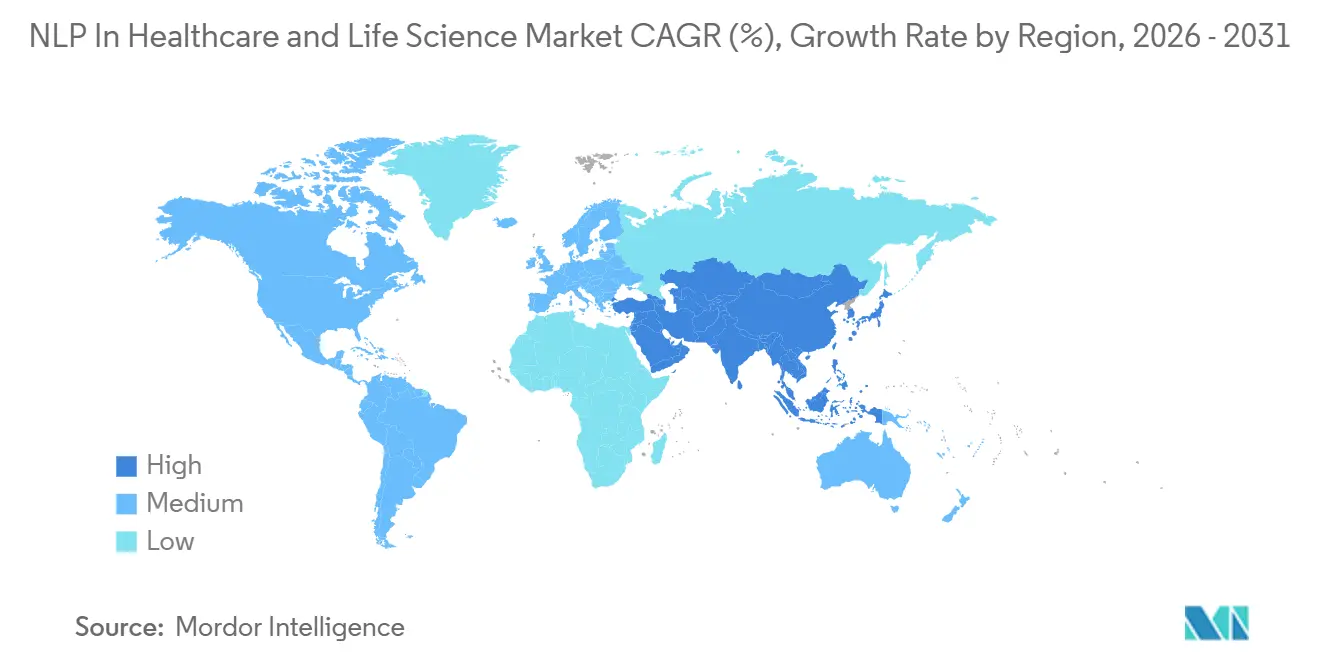

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

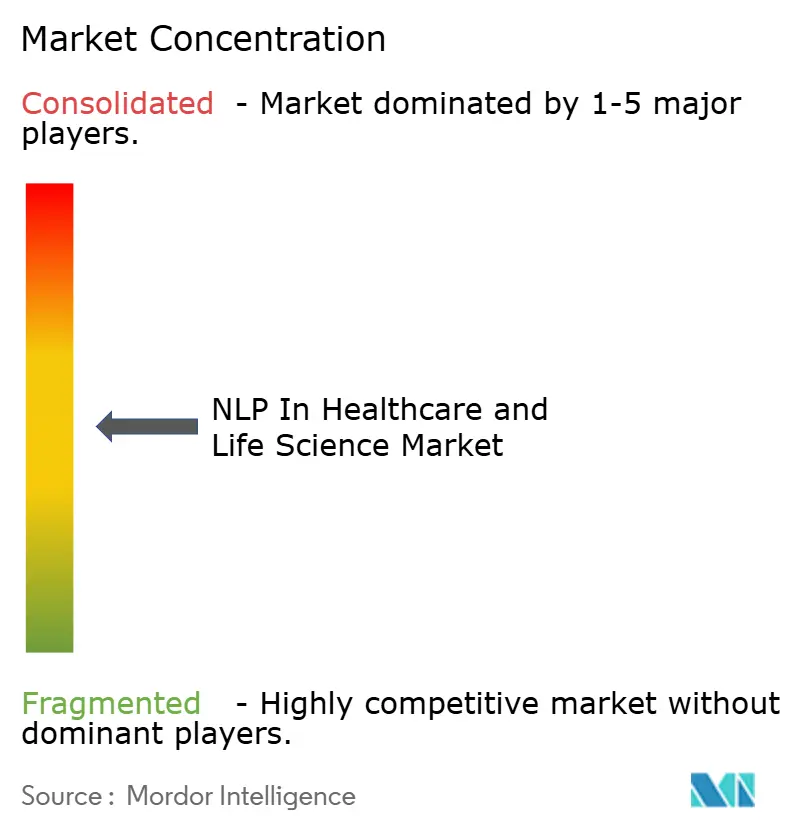

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

NLP In Healthcare and Life Science Market Analysis by Mordor Intelligence

The NLP In Healthcare And Life Science Market size is expected to increase from USD 5.67 billion in 2025 to USD 7.13 billion in 2026 and reach USD 24.80 billion by 2031, growing at a CAGR of 28.33% over 2026-2031.

Health systems now treat these tools as core infrastructure for extracting knowledge from clinical text, supporting risk assessment, and automating administrative work rather than using them only for documentation support. The shift from rules-based parsing to transformer models and generative systems is widening the usable scope across physician notes, radiology narratives, pathology reports, and multilingual patient interactions at enterprise scale. Demand is also being reinforced by the steady buildup of unstructured clinical and research content, which keeps the need for high-volume text extraction central to procurement decisions in both provider and life sciences settings. North America remains the commercial anchor, while Asia-Pacific is expanding faster as digitization programs and local language requirements push more deployments across diverse care settings. The NLP in healthcare and life science market is also becoming more competitive around hyperscaler stacks, EHR-embedded AI, and specialist vendors, with traceability and auditability now shaping buyer preference because clinical liability from inaccurate outputs remains a live concern.

Key Report Takeaways

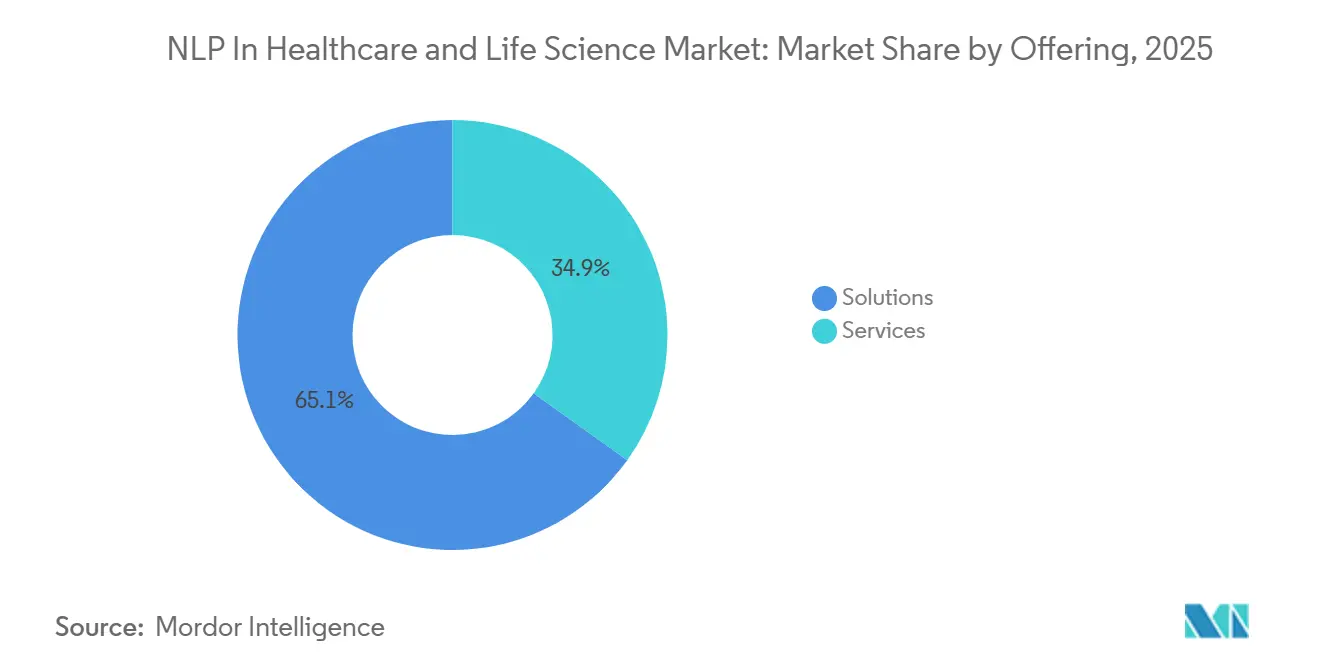

- By offering, solutions segment held 65.12% revenue share in 2025, while services are projected to expand at 29.67% CAGR through 2031.

- By deployment mode, cloud-based deployment captured 61.82% share in 2025, while hybrid deployment is forecast to grow at 30.82% CAGR through 2031.

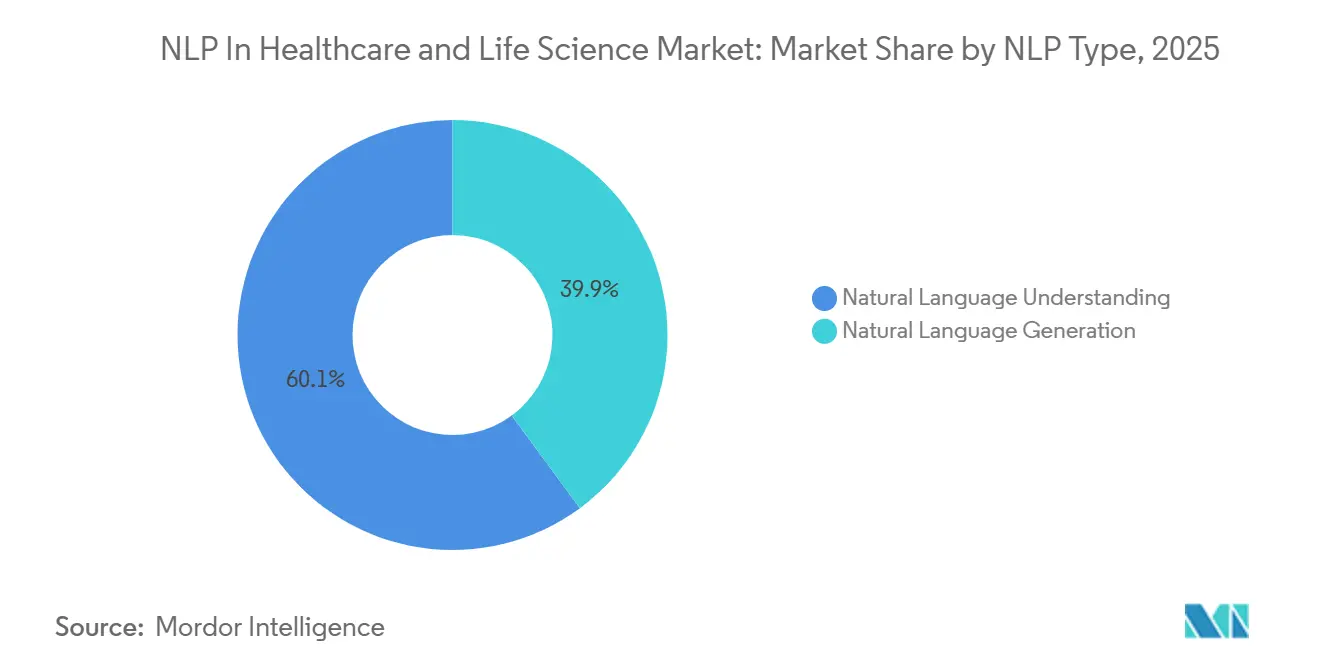

- By NLP type, natural language understanding led with 60.14% share in 2025, while natural language generation is projected to advance at 31.91% CAGR through 2031.

- By NLP technique, named entity recognition accounted for 37.23% share in 2025, while predictive risk analytics is expected to record a 31.58% CAGR through 2031.

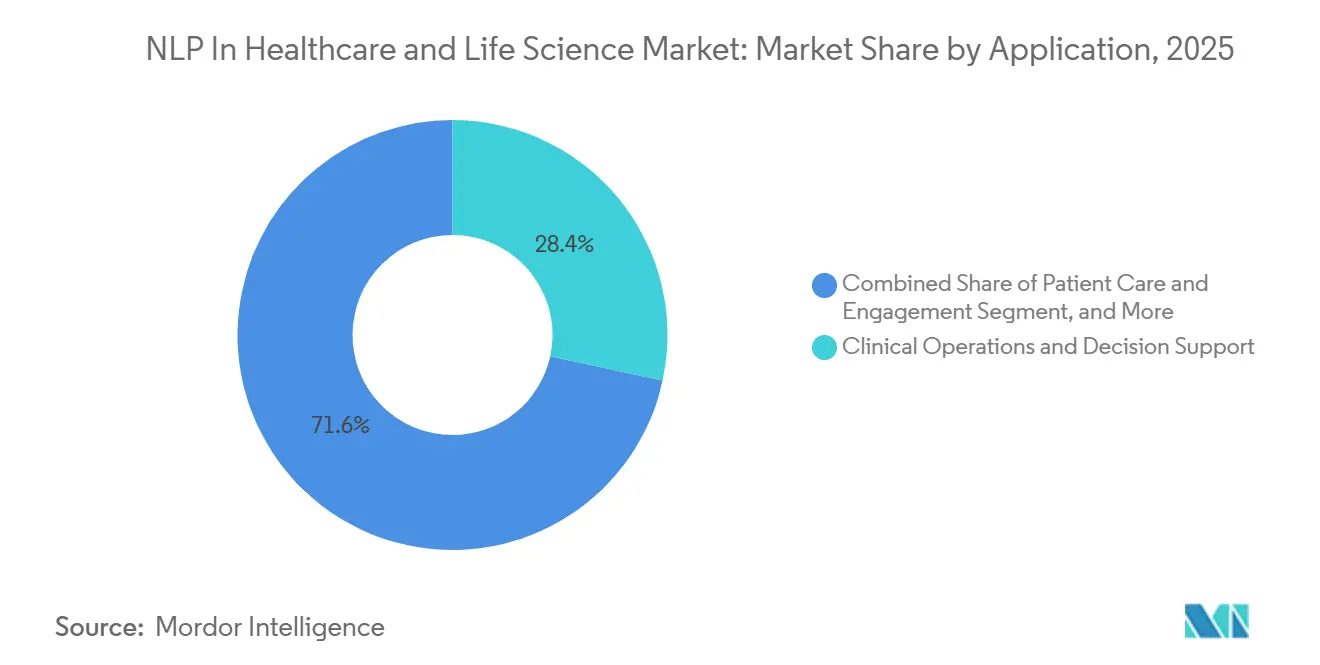

- By application, clinical operations and decision support held 28.43% share in 2025, while clinical trial matching is forecast to expand at 29.64% CAGR through 2031.

- By end user, healthcare providers represented 31.81% share in 2025, while pharmaceutical and biotechnology companies are projected to grow at 35.14% CAGR through 2031.

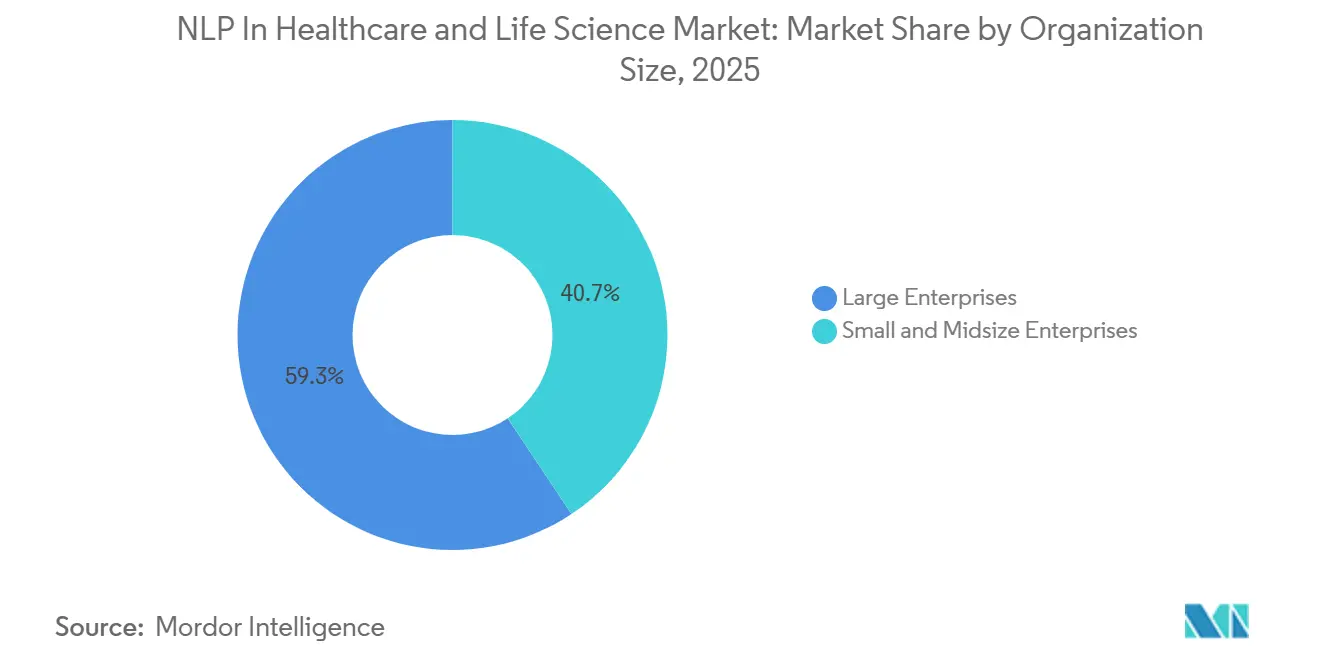

- By organization size, large enterprises commanded 59.33% share in 2025, while small and midsize enterprises are expected to post a 30.53% CAGR through 2031.

- By geography, North America held 43.23% of the NLP in healthcare and life science market share in 2025, while Asia-Pacific is forecast to grow at 32.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global NLP In Healthcare and Life Science Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Unstructured Clinical and Research Text Volumes | +6.2% | Global | Long term (≥ 4 years) |

| Accelerating Demand for Automated Clinical Documentation and Scribing | +5.8% | North America & EU | Short term (≤ 2 years) |

| Clinical Trial Matching and Real-World Evidence Extraction at Scale | +4.5% | North America, EU | Medium term (2-4 years) |

| GenAI-Enabled Medical Coding and Summary Generation | +4.2% | North America | Medium term (2-4 years) |

| AI Governance, Auditability, and Traceability Requirements | +2.5% | Global, EU lead | Short term (≤ 2 years) |

| Multilingual Healthcare Content Processing Across Fragmented Care Settings | +2.1% | APAC, MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Unstructured Clinical and Research Text Volumes

The core growth engine is no longer basic EHR digitization because that transition had already matured in many developed markets before 2026. What is driving demand now is the rising volume of unstructured content coming from ambient documentation tools, telehealth transcripts, remote monitoring logs, and AI-assisted clinical notes. Amazon Connect Health entered the market in 2026 with ambient documentation support across more than 22 specialties, which shows how quickly new text streams are moving into production care workflows. Netsmart also reported a 275% increase in ambient documentation adoption across its network of more than 1,300 client organizations after deployment, which points to a much larger base of machine-generated notes entering provider systems. That combination keeps the NLP in healthcare and life science market on a long demand cycle because buyers now need extraction pipelines for diagnoses, medications, and findings from both traditional clinician notes and newly generated documentation streams.[1]Amazon Web Services, “Introducing Amazon Connect Health, Agentic AI for Healthcare, Built for the People Who Deliver It,” AWS for Industries, aws.amazon.com

Accelerating Demand for Automated Clinical Documentation and Scribing

Documentation burden remains one of the clearest commercial entry points for clinical NLP. A 2026 systematic review and meta-analysis found that AI tools, including NLP and large language models, reduce documentation burden when supported by practical quality control. Microsoft stated in 2026 that Dragon Copilot was being used by more than 100,000 clinicians each day across 9 countries and that it could capture multilingual conversations in 58 languages and convert them into structured notes. Oracle also reported that its Clinical AI Agent had saved U.S. doctors more than 200,000 documentation hours, and AtlantiCare achieved a 41% reduction in documentation time in ambulatory care after deployment. As this use case scales, the NLP in healthcare and life science market is shifting from simple transcription value toward code suggestion, diagnostic support, and risk workflows that create a deeper platform relationship with providers.[2]Nature Publishing Group, “TrialMatchAI, an End-to-End AI-Powered Clinical Trial Recommendation System to Streamline Patient-to-Trial Matching,” Nature Communications, nature.com

Clinical Trial Matching and Real-World Evidence Extraction at Scale

The demand for life sciences is rising because trial recruitment and evidence generation both depend on reading large volumes of unstructured patient records. A 2026 prospective study reported that Massive Bio’s neuro-symbolic multi-agent platform matched cancer patients to trials 4 times faster than conventional methods after processing more than 157,000 clinical document pages across 3,804 patients. Nature Communications also published TrialMatchAI in 2026, and the system achieved a 92% match rate for oncology patients against active trial criteria through a retrieval-augmented framework built on fine-tuned open-source models. John Snow Labs also positioned its Patient Journey platform around FDA real-world evidence needs, which shows how extracted clinical text is moving closer to regulatory and sponsor workflows. This widens the NLP in healthcare and life science markets beyond provider productivity and gives vendors access to recurring, higher-value programs linked to recruitment, cohort discovery, and submission support.[3]John Snow Labs, “Redefining Real-World Evidence, John Snow Labs Introduces First FDA-Ready Patient Journey Platform,” John Snow Labs, johnsnowlabs.com

GenAI-Enabled Medical Coding and Summary Generation

Medical coding is moving away from rules-heavy systems and toward models that interpret clinical context across full notes. AWS launched Amazon Connect Health in March 2026 with coding capabilities that generate ICD-10 and CPT suggestions from clinical documentation and attach source traceability with confidence scoring for compliance review. A 2026 medRxiv study also found that fine-tuned PubMedBERT models delivered more reliable performance than prompt-based large language models for hierarchical clinical coding under CMS Hierarchical Condition Category frameworks. Epic also reported coding-related gains from Penny AI, which reflects a wider market shift toward measuring coding quality at the system level rather than focusing only on speed. That change supports the NLP in healthcare and life science market because domain-tuned platforms with audit trails are better placed than generic model providers when buyers evaluate reimbursement risk and compliance exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Gaps With Legacy EHR and Claims Stacks | -1.8% | Global | Medium term (2-4 years) |

| Limited Domain-Labeled Training Data for Specialty Medicine | -1.4% | Global | Long term (≥ 4 years) |

| Model Hallucination and Clinical Liability Concerns | -1.9% | North America & EU | Short term (≤ 2 years) |

| Data Privacy and Sovereignty Constraints | -1.3% | EU, APAC, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Model Hallucination and Clinical Liability Concerns

Hallucination remains the most visible barrier for generative clinical NLP in high-stakes settings. A 2026 study in npj Digital Medicine found that large language models gave unsafe responses to patient medical questions at rates that still require strong human oversight before they can sit inside routine workflows. A 2026 review in Frontiers in Digital Health reached a similar conclusion and noted that even medically tuned models can behave unsafely in specific clinical contexts. This matters because medication reconciliation, diagnostic support, and summary generation all depend on factual precision rather than fluent output. For that reason, the NLP in healthcare and life science market is rewarding platforms with audit trails, source grounding, and review controls, while buyers remain cautious toward thin wrappers around general-purpose models.

Data Privacy and Sovereignty Constraints

Privacy and sovereignty rules continue to shape how clinical NLP gets deployed across regions. GDPR Article 9 protections for health data and the EU AI Act’s high-risk framework for clinical AI add clear documentation, governance, and oversight obligations for vendors operating in Europe. A 2026 Scientific Reports study showed that locally deployed and systematically optimized models could reach 98% performance parity with cloud-based systems for Japanese medical personnel's health information extraction. That result reduces the technical risk of local deployment, but it also raises the architecture burden for vendors that need to balance data residency rules with strong model performance. As a result, the NLP in healthcare and life science market is increasingly favoring hybrid and localized deployment models in regions where cross-border health data movement remains tightly controlled.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Narrow the Gap as Customization Demands Rise

Solutions held 65.12% of the NLP in healthcare and life science market share in 2025, which reflected the installed base of software used for documentation, coding, and analytics across large integrated delivery systems. That lead came from established software contracts and the central role of packaged NLP tools inside provider workflows. Clinical documentation, coding support, and analytics remain the core software use cases that support this segment’s scale. The installed base still matters because hospitals tend to prefer proven systems when text extraction touches reimbursement, compliance, and care workflows.

Services are projected to grow at 29.67% CAGR through 2031 as buyers ask for deployment support, EHR integration, model tuning, and ongoing governance rather than only a software license. Health systems increasingly want vendors to adapt models to proprietary clinical corpora and maintain them after go-live. John Snow Labs said in 2026 that its Healthcare NLP platform includes more than 2,800 pre-trained models and regularly updated pipelines tied to changing ontologies and use cases. That type of service-heavy relationship increases recurring revenue and raises switching costs once a system is embedded into clinical and life sciences workflows. The NLP in healthcare and life science market is therefore shifting toward end-to-end accountability, which puts pressure on software-only vendors that cannot support customization, retraining, and governance over time.

By Deployment Mode: Cloud Dominates, Hybrid Surges on Sovereignty Pressure

Cloud-based deployment accounted for 61.82% of the 2025 market, supported by large hyperscaler investments and the practical ease of scaling model training and inference through shared infrastructure. Microsoft Azure, AWS HealthLake, and Google Cloud helped shape this lead by making healthcare-focused AI tooling easier to deploy inside enterprise environments. Cloud also suits organizations that want faster implementation and lower upfront infrastructure costs. That remains especially relevant for broad provider networks and multisite life sciences programs that need centralized model management.

Hybrid deployment is forecast to advance at 30.82% CAGR through 2031 because many health systems want cloud flexibility without moving identifiable data outside approved environments. The pressure is strongest in Europe, Japan, and Gulf markets where sovereignty and localization policies limit how patient data can be transmitted or stored. The 2026 Scientific Reports paper on Japanese medical PHI extraction showed that optimized local models can approach cloud-level performance, which lowers the penalty of keeping sensitive workloads on site. On-premises systems still retain a role in military health networks and large institutions with older infrastructure, but their share is likely to decline as hybrid models offer a more practical middle path. The NLP in healthcare and life science market is therefore moving toward mixed architectures where sensitive inference stays local and broader orchestration or model management sits in the cloud.

By NLP Type: NLU Leads, NLG Accelerates on Generative AI Momentum

Natural Language Understanding held 60.14% share in 2025, which kept it in the leading position because most mature healthcare NLP workflows still depend on the extraction, classification, and interpretation of existing text. NLU remains central to clinical concept extraction, named entity recognition, and assertion detection inside EHR-linked systems. Those functions support diagnosis capture, medication extraction, adverse event review, and structured documentation. This gives NLU a broad installed role across both provider and research settings.

Natural Language Generation is projected to grow at 31.91% CAGR through 2031 as generative models become standard for drafting discharge summaries, patient communications, and clinical notes. Microsoft reported in 2026 that Dragon Copilot could turn patient-clinician conversations into structured EHR notes in 58 languages, which illustrates the commercial pull behind generation-led tools. Buyers now evaluate generated content on fluency, factual accuracy, and alignment with existing EHR templates, not only on traditional precision metrics. That changes procurement criteria because a generated summary must fit directly into the care workflow and stand up to review. The NLP in healthcare and life science market is rewarding vendors that can deliver generation with strong clinical grounding, while general-purpose models without healthcare-specific controls face a harder path into enterprise care environments.

By NLP Technique: Named Entity Recognition Anchors the Stack, Predictive Risk Analytics Leads Growth

Named Entity Recognition captured 37.23% share in 2025, making it the foundational layer for most clinical NLP stacks. It supports extraction of medications, procedures, conditions, and findings from discharge notes, pathology reports, and radiology narratives. A 2025 JMIR AI study that processed 138,250 clinical notes reported a precision score of 0.989 for procedure entities using Spark NLP clinical models. That level of production maturity explains why NER remains deeply embedded across provider, payer, and life sciences use cases.

Predictive Risk Analytics is projected to grow at 31.58% CAGR through 2031 as payers and providers push text-derived features into population health and risk adjustment workflows. Clinical text gives these systems context that structured claims fields often miss, especially around disease severity, social factors, and follow-up risk. The remaining techniques, including optical character recognition, sentiment analysis, text classification, topic modeling, and summarization, continue to serve narrower but durable roles in healthcare operations. Summarization is gaining more momentum as larger EHR platforms add chart preparation and pre-visit review tools into daily clinician workflow. The NLP in healthcare and life science market size for predictive risk analytics is strengthening because organizations increasingly want models that do more than read text and can translate that text into measurable operational or clinical prioritization.

By Application: Clinical Operations Leads, Clinical Trial Matching Accelerates

Clinical operations and decision support represented 28.43% of the NLP in healthcare and life science market size in 2025, reflecting how provider organizations remain the main site of deployment for ambient documentation, coding support, chart review, and clinical assistance tools. This segment benefits from daily workflow frequency because it touches routine documentation and care coordination activities. Hospitals and physician groups also see direct value when these tools reduce charting time or improve documentation completeness. That keeps clinical operations at the center of current deployment volume.

Clinical trial matching is forecast to expand at 29.64% CAGR through 2031 as sponsors and research networks use AI to screen patients and compare records against complex protocol criteria. The Massive Bio study and the TrialMatchAI publication both point to how much time and manual effort can be removed when oncology documents are processed at scale. Patient care and engagement, biomedical research, and administrative operations remain meaningful adjacent uses because text extraction supports communication, evidence generation, and workflow automation across the care continuum. IQVIA also introduced IQVIA.ai in 2026 to bring agentic AI into clinical, commercial, and real-world evidence workstreams, which shows how these application areas are starting to converge around shared data pipelines. The NLP in healthcare and life science market is therefore broadening from provider efficiency into research execution and evidence development, while genomics and precision medicine continue to gain relevance as free-text records are linked with molecular and longitudinal patient data.

By End User: Healthcare Providers Anchor Demand, Pharma and Biotech Accelerates Fastest

Healthcare providers commanded 31.81% of the 2025 market because they generate the largest volumes of clinical documentation and remain the main buyers of ambient scribing and decision support tools. Provider demand is rooted in daily workflow pressure, reimbursement requirements, and the need to organize text from diverse care settings. The segment also benefits from stronger procurement maturity in large health systems where EHR-connected tools can scale across departments. That keeps providers in the lead even as use cases spread further into research and payer workflows.

Pharmaceutical and biotechnology companies are projected to grow at 35.14% CAGR through 2031 as NLP becomes more central to drug development, real-world evidence extraction, and trial design. Tempus said in 2026 that it was building multimodal foundation models trained on more than 500 petabytes of de-identified data, including 45 million patient journeys, to support precision oncology and trial optimization. John Snow Labs also tied its Patient Journey Intelligence platform to FDA real-world evidence standards, which shows how sponsor and payer workflows are beginning to overlap through shared extraction needs. Healthcare payers continue to invest in prior authorization and risk adjustment automation, while medical device companies and government agencies remain smaller but steadily growing users of the technology. The NLP in healthcare and life science market is widening across end users, but providers still anchor current demand because their documentation workflows are the main source of both input data and operational return.

By Organization Size: Large Enterprises Lead, SMEs Accelerate Through API Accessibility

Large enterprises held 59.33% share in 2025 because they had the budgets, IT teams, and systems integration capacity needed to roll out clinical NLP across large multisite environments. These organizations also tend to manage higher data volumes and more complex compliance needs, which favors enterprise-grade platforms with governance controls. Large provider groups, academic medical centers, and multinational life sciences companies were therefore better positioned to deploy early and scale faster. That structural advantage explains why the segment still dominates current spending.

Small and midsize enterprises are expected to grow at 30.53% CAGR through 2031 as cloud-native and API-based platforms reduce the cost and complexity of deployment. Suki said in January 2026 that its ambient AI platform had reached more than 450 practices and 3,400 monthly active users within the athenahealth ecosystem, which shows adoption moving beyond large integrated delivery networks. The arrival of easier-to-consume healthcare AI tools is lowering the entry barrier for ambulatory practices, specialty groups, and regional systems, even if governance expectations still separate enterprise-grade deployments from lighter tools. Smaller organizations remain price sensitive, but faster implementation and reduced infrastructure burden make adoption more realistic than it was in earlier years. The NLP in healthcare and life science market is therefore broadening across organization sizes as accessibility improves, even though large enterprises still set the pace for high-value and highly governed deployments.

Geography Analysis

North America accounted for 43.23% of the 2025 market, which kept it in the leading regional position for healthcare NLP adoption. The United States remains the center of demand because procurement is supported by deep EHR penetration, large provider networks, and broad vendor activity across provider, payer, and life sciences use cases. Microsoft and Oracle both expanded their healthcare AI offerings in 2026, which reinforced the region’s role as the main commercial proving ground for enterprise clinical NLP. AWS also added support in 2026 for the CMS Interoperability and Prior Authorization Final Rule inside HealthLake, which gives U.S. payers and connected vendors a direct compliance-driven use case for NLP-enabled authorization workflows. The NLP in healthcare and life science market remains most mature in North America because infrastructure readiness, reimbursement pressure, and vendor presence all align more clearly there than in most other regions.

Europe continues to advance under a stricter compliance model that shapes both deployment timing and vendor positioning. GDPR Article 9 rules and the EU AI Act’s high-risk obligations for clinical AI require stronger evidence around oversight, governance, and documentation before large deployments can scale. Germany and the United Kingdom remain the main national demand centers, while Nordic systems stand out as strong environments for governance-led clinical AI programs because of high digitization and stronger institutional trust. The NLP in healthcare and life science market in Europe is therefore moving forward with a more measured pace, as interoperability gaps and regulatory diligence slow near-term rollout even while they strengthen the long-run quality bar for approved solutions.

Asia-Pacific is projected to grow at 32.53% CAGR through 2031, making it the fastest-expanding regional cluster in this space. Growth is being supported by large patient populations, clinician shortages, stronger digital health investment, and the need to process healthcare content across multiple languages and fragmented care settings. Japan is emerging as an important case because local deployment is gaining technical credibility and because RIKEN published a Japanese medical LLM in May 2026 that achieved 90.8% accuracy on specialist licensing benchmarks in hospital-oriented environments. That kind of local model development fits sovereignty-driven procurement patterns and makes deployment more realistic where institutions prefer on-premises or tightly controlled environments. Middle East and Africa remains an earlier-stage opportunity led by Gulf initiatives, while South America is still concentrated in private provider networks in countries such as Brazil and Argentina. The NLP in healthcare and life science market in these regions is still smaller than in North America or Europe, but local-language requirements and public system modernization continue to create a longer runway for adoption.

Competitive Landscape

The NLP in healthcare and life sciences space is moderately concentrated at the platform layer and still fragmented across specialist vendors. Microsoft’s Dragon Copilot scale and Oracle’s continued expansion of Clinical AI Agent show how major vendors are using installed relationships to deepen their role in clinician workflow. AWS has also entered more directly with Amazon Connect Health, combining ambient documentation, coding support, and source traceability inside one purpose-built healthcare offer. The NLP in healthcare and life science market is therefore being shaped by a small group of platform vendors that control key enterprise entry points, even though no single company appears to dominate the full field.

Specialist vendors are competing by going deeper into narrow use cases rather than trying to match platform breadth. John Snow Labs is one example because it focuses on healthcare-specific NLP assets, de-identification, and real-world evidence workflows that require domain tuning and regulatory alignment. IQVIA is targeting the life sciences layer more directly through IQVIA.ai, which links agentic AI with research, commercial, and real-world evidence tasks rather than focusing only on provider documentation. This creates a split in the field where large vendors own broad workflow distribution and specialists try to win on task depth, validation, and sector credibility. The NLP in healthcare and life science market still has clear white space in multilingual clinical processing, rare disease workflows, behavioral health, and sovereignty-ready deployment stacks, which leaves room for focused challengers even as large vendors consolidate around the biggest enterprise accounts.

Strategic moves in 2025 and 2026 show that competition is no longer centered only on model performance. Microsoft expanded Dragon Copilot capabilities at HIMSS 2026 with ICD-10 specificity suggestions, reusable clinical documents, multilingual capture, and broader nurse and radiologist workflows. Oracle moved Clinical AI Agent into inpatient and emergency department settings in 2026 after proving ambulatory time savings, which shows how vendors are expanding from one care setting into adjacent workflows once performance is established. Suki also strengthened its ambulatory position through the athenahealth ecosystem, which suggests smaller specialists can still defend niches when they integrate quickly and fit tightly into day-to-day practice. The NLP in healthcare and life science market is likely to remain mixed between large platforms and focused specialists because enterprise buyers want scale and governance, while smaller clinical teams still reward vendors that solve a narrow workflow faster.

NLP In Healthcare and Life Science Industry Leaders

Cerner Corporation

Epic Systems Corporation

Oracle Corporation

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AWS launched Amazon Connect Health, a purpose-built agentic AI solution for healthcare incorporating ambient clinical documentation, ICD-10/CPT medical coding, and pre-visit patient insights. The launch supported over 22 specialties with full source traceability. Amazon One Medical's ambient documentation exceeded 1 million clinical visits, and Netsmart reported a 275% increase in adoption across its 1,300+ client organizations.

- March 2026: Microsoft introduced new Dragon Copilot capabilities at HIMSS 2026, including proactive ICD-10 specificity suggestions, reusable custom clinical documents, multilingual conversation capture in 58 languages, and expanded nurse and radiologist workflows. The platform reached over 100,000 daily clinician users across 9 countries.

- March 2026: Oracle Health made its Clinical AI Agent for note generation available in U.S. inpatient and emergency department settings. The solution has cumulatively saved U.S. doctors over 200,000 documentation hours, with AtlantiCare achieving a 41% decrease in documentation time following ambulatory deployment.

- August 2025: Oracle launched an all-new AI-driven EHR for U.S. ambulatory providers, featuring voice-first interaction and conversational AI for clinical queries, with acute care functionality expansion planned for 2026.

Global NLP In Healthcare and Life Science Market Report Scope

Natural Language Processing (NLP) in healthcare and life sciences is a subset of artificial intelligence that empowers computers to understand, interpret, and generate human language. It transforms vast amounts of unstructured medical data, such as clinical notes, lab reports, and biomedical literature, into actionable, structured insights.

The NLP in Healthcare and Life Sciences Market is segmented by offering, deployment mode, NLP type, technique, application, end user, and organization size. By offering, it includes solutions and services. By deployment mode, platforms are delivered as cloud‑based, on‑premises, or hybrid systems. By NLP type, the market covers natural language understanding and natural language generation. By NLP technique, it spans named entity recognition, optical character recognition, sentiment analysis, text classification, topic modeling, text summarization, and advanced analytics such as predictive risk analytics.

By application, NLP is used in clinical operations and decision support, patient care and engagement, biomedical research and drug development, administrative and operations management, genomics and precision medicine, clinical trial matching, medical education and knowledge dissemination, and risk and compliance management. By end user, adoption is driven by healthcare providers, healthcare payers, pharmaceutical and biotechnology companies, healthcare researchers, public health and government agencies, and medical device companies. Finally, by organization size, the market serves both large enterprises and small and midsize enterprises.

| Solutions |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Natural Language Understanding |

| Natural Language Generation |

| Named Entity Recognition |

| Optical Character Recognition |

| Sentiment Analysis |

| Text Classification |

| Topic Modeling |

| Text Summarization |

| Predictive Risk Analytics |

| Clinical Operations and Decision Support |

| Patient Care and Engagement |

| Biomedical Research and Drug Development |

| Administrative and Operations Management |

| Genomics and Precision Medicine |

| Clinical Trial Matching |

| Medical Education and Knowledge Dissemination |

| Risk and Compliance Management |

| Healthcare Providers |

| Healthcare Payers |

| Pharmaceutical and Biotechnology Companies |

| Healthcare Researchers |

| Public Health and Government Agencies |

| Medical Device Companies |

| Large Enterprises |

| Small and Midsize Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Solutions | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By NLP Type | Natural Language Understanding | |

| Natural Language Generation | ||

| By NLP Technique | Named Entity Recognition | |

| Optical Character Recognition | ||

| Sentiment Analysis | ||

| Text Classification | ||

| Topic Modeling | ||

| Text Summarization | ||

| Predictive Risk Analytics | ||

| By Application | Clinical Operations and Decision Support | |

| Patient Care and Engagement | ||

| Biomedical Research and Drug Development | ||

| Administrative and Operations Management | ||

| Genomics and Precision Medicine | ||

| Clinical Trial Matching | ||

| Medical Education and Knowledge Dissemination | ||

| Risk and Compliance Management | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Pharmaceutical and Biotechnology Companies | ||

| Healthcare Researchers | ||

| Public Health and Government Agencies | ||

| Medical Device Companies | ||

| By Organization Size | Large Enterprises | |

| Small and Midsize Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of NLP in healthcare and life science by 2031?

It is forecast to reach USD 24.80 billion by 2031 from USD 7.13 billion in 2026, expanding at a 28.33% CAGR over 2026-2031.

Which region leads current adoption of healthcare NLP solutions?

North America led with 43.23% share in 2025 because of strong EHR penetration, mature procurement conditions, and broad vendor activity.

Which region is growing fastest through 2031?

Asia-Pacific is the fastest-growing region with a projected 32.53% CAGR through 2031, supported by digital health investment and multilingual care requirements.

Which offering type is expanding faster, solutions or services?

Services are growing faster at 29.67% CAGR because buyers increasingly need deployment support, model tuning, EHR integration, and governance after implementation.

Why is natural language generation gaining traction in clinical workflows?

Natural language generation is advancing at 31.87% CAGR because health systems are using it for ambient scribing, discharge summaries, patient letters, and structured note creation.

What is the main risk slowing enterprise adoption of generative clinical NLP?

Model hallucination remains the main concern because inaccurate but plausible outputs can create clinical risk, which is why buyers now favor grounded and auditable systems.

Page last updated on: